India Impact Investing Market Size, Share, Trends and Forecast by Asset Class, Offerings, Investment Style, Investor Type, and Region, 2026-2034

India Impact Investing Market Summary:

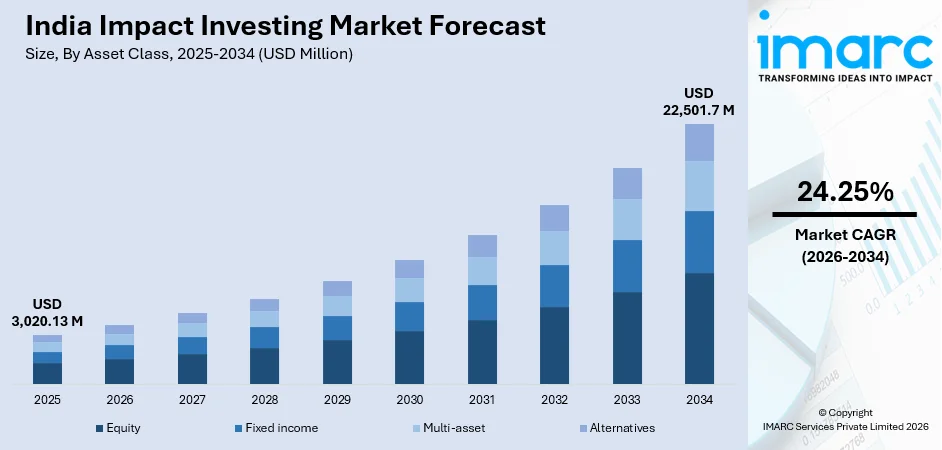

The India impact investing market size was valued at USD 3,020.13 Million in 2025 and is projected to reach USD 22,501.7 Million by 2034, growing at a compound annual growth rate of 24.25% from 2026-2034.

The market is driven by increasing awareness of sustainable development goals, growing institutional participation in socially responsible investments, and supportive government policies fostering social enterprise ecosystems. The rising adoption of environmental, social, and governance frameworks among domestic and international investors is accelerating capital flows toward impact-driven enterprises across sectors such as financial inclusion, healthcare, education, and climate technology. The convergence of development finance with private capital continues to expand the India impact investing market share.

Key Takeaways and Insights:

- By Asset Class: Equity dominates the market with a share of 42.6% in 2025, driven by the preference for direct ownership stakes in impact-driven enterprises and higher return potential associated with equity instruments.

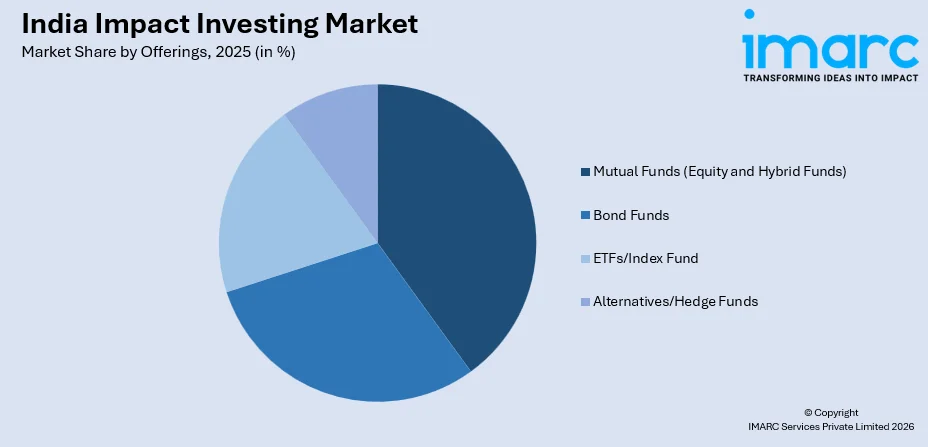

- By Offerings: Mutual funds (equity and hybrid funds) leads the market with a share of 39.8% in 2025, owing to their diversified exposure, regulatory accessibility, and growing investor appetite for impact-oriented, professionally managed portfolios.

- By Investment Style: Active represents the largest segment with a market share of 71.4% in 2025, driven by the need for hands-on portfolio management and rigorous impact measurement ensuring alignment with social outcomes.

- By Investor Type: Institutional investors dominate the market with a share of 64.9% in 2025, owing to growing mandates for ESG-compliant portfolios among pension funds, insurance companies, and development finance institutions.

- By Region: West India leads the market with a share of 33.2% in 2025, driven by the concentration of financial hubs, venture capital ecosystems, and impact enterprise headquarters in Maharashtra and Gujarat.

- Key Players: The India impact investing market exhibits a moderately fragmented competitive landscape, with dedicated impact investment funds operating alongside development finance institutions, private equity firms, and family offices across diversified impact sectors and investment stages.

To get more information on this market Request Sample

The India impact investing market is experiencing robust expansion fueled by a convergence of structural and policy-driven factors. The government's commitment to sustainable development, the establishment of dedicated platforms for social enterprises, and evolving regulatory mandates are creating a conducive environment for impact capital mobilization. Rising awareness among institutional and retail investors regarding the dual benefits of financial returns and measurable social outcomes is further accelerating market growth. In October 2025, EIB Global committed up to $60 million to the India Energy Transition Fund supporting renewable energy, EVs, and circular economy projects, strengthening sustainable infrastructure financing in India. Moreover, India's vast developmental needs across healthcare, education, financial inclusion, clean energy, and agriculture present significant investment opportunities. The increasing maturity of the startup ecosystem, the growth of blended finance models, and the expanding role of family offices in impact capital allocation are contributing to a dynamic and evolving market landscape that attracts both domestic and global capital.

India Impact Investing Market Trends:

Rise of Blended Finance Models

The Indian impact investing landscape is witnessing a significant shift toward blended finance structures that combine philanthropic, concessional, and commercial capital to address development challenges. These innovative financing mechanisms are enabling risk mitigation for private investors while unlocking capital for underserved sectors. In December 2025, UNDP’s Climate Finance Network partnered with The Blended Finance Company to design a guarantee facility supporting climate-smart agriculture financing in India, improving capital access for vulnerable smallholder ecosystems. Development finance institutions and foundations are increasingly deploying catalytic first-loss capital that attracts mainstream investors into impact deals.

Growing Integration of Technology in Impact Measurement

Impact investors in India are increasingly leveraging advanced digital tools and analytics frameworks to measure, verify, and report social and environmental outcomes. The adoption of artificial intelligence, data analytics, and blockchain-based verification systems enhancing transparency and accountability across impact portfolios. In June 2025, NITI Aayog released its “India’s Data Imperative” report introducing data-quality scorecards and maturity frameworks to strengthen digital governance and trust in data-driven systems. This technological integration is moving the market beyond traditional self-reported metrics toward real-time, evidence-based impact assessment. Enhanced measurement capabilities are strengthening investor confidence, enabling more rigorous due diligence processes, and facilitating standardized reporting aligned with global sustainability frameworks and development goal indicators.

Expansion of Climate Technology Investments

Climate technology is emerging as one of the fastest-growing verticals within India's impact investing ecosystem, reflecting the country's ambitious sustainability commitments and the global transition toward low-carbon economies. Investors are channeling significant capital into enterprises focused on renewable energy, sustainable mobility, circular economic solutions, and carbon management technologies. In August 2024, Sembcorp Industries began work on India’s first large-scale commercial green hydrogen and ammonia facility in Tamil Nadu to support clean energy exports and industrial decarbonisation. The intersection of climate action with commercial viability is attracting a diverse range of investors, from dedicated climate funds to mainstream venture capital firms.

Market Outlook 2026-2034:

The India impact investing market is poised for sustained revenue growth over the forecast period, underpinned by deepening ESG integration, regulatory evolution, and expanding investor participation. Revenue is expected to witness significant expansion as institutional mandates for sustainable investments are strengthened and new capital pools, including retail investors and family offices, enter the market. The growing pipeline of investable enterprises across climate technology, healthcare, education, and financial inclusion, alongside supportive government policies, are collectively expected to drive robust revenue generation, positioning India as a leading destination for impact capital globally. The market generated a revenue of USD 3,020.13 Million in 2025 and is projected to reach a revenue of USD 22,501.7 Million by 2034, growing at a compound annual growth rate of 24.25% from 2026-2034.

India Impact Investing Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Asset Class |

Equity |

42.6% |

|

Offerings |

Mutual Funds (Equity & Hybrid Funds) |

39.8% |

|

Investment Style |

Active |

71.4% |

|

Investor Type |

Institutional Investors |

64.9% |

|

Region |

West India |

33.2% |

Asset Class Insights:

- Equity

- Fixed income

- Multi-asset

- Alternatives

Equity dominates with a market share of 42.6% of the total India impact investing market in 2025.

The equity asset class holds the leading position in the India impact investing market, reflecting investor preference for direct ownership in impact-driven enterprises that offer substantial growth potential. Equity investments allow investors to actively participate in governance and strategic decision-making, ensuring alignment between financial objectives and social impact goals. In February 2026, the Securities and Exchange Board of India proposed reducing the minimum investment requirement for Social Impact Funds from ₹2 lakh to ₹1,000 to expand participation and democratize access to equity-based impact investments.

The strong equity orientation of the market is also driven by the historical performance of equity impact investments, which have demonstrated competitive returns comparable to conventional private equity. The availability of diverse equity instruments, including venture capital, growth equity, and listed sustainability-focused funds, provides investors with multiple entry points across varying risk-return spectrums. As the impact enterprise pipeline matures and more companies reach later funding stages, equity participation is expected to strengthen further, reinforcing its dominant position within the overall asset class landscape.

Offerings Insights:

Access the comprehensive market breakdown Request Sample

- Mutual Funds (Equity and Hybrid Funds)

- Bond Funds

- ETFs/Index Fund

- Alternatives/Hedge Funds

Mutual funds (equity and hybrid funds) lead with a share of 39.8% of the total India impact investing market in 2025.

Mutual funds (equity and hybrid funds) dominate the India impact investing market as the preferred investment vehicle, offering investors a structured and professionally managed pathway to deploy capital toward socially responsible enterprises. These funds provide diversified exposure across multiple impact sectors simultaneously, reducing concentration risk while maintaining alignment with sustainability objectives. The accessibility and regulatory oversight associated with mutual fund structures make them particularly attractive to both institutional allocators and emerging retail participants seeking meaningful, outcome-oriented investment opportunities.

The dominance is further reinforced by their ability to bridge the gap between conventional investment expectations and impact-oriented mandates, appealing to a broad spectrum of investors navigating the evolving responsible finance landscape. Asset management companies are increasingly launching dedicated impact-themed fund categories that integrate environmental, social, and governance considerations into portfolio construction, expanding the product ecosystem available to investors. As awareness of sustainable investing deepens across domestic and international investor communities, mutual funds remain the most scalable and accessible conduit for mobilizing meaningful impact capital.

Investment Style Insights:

- Active

- Passive

Active exhibits a clear dominance with a 71.4% share of the total India impact investing market in 2025.

The active dominates the India impact investing market, driven by the inherent complexity of impact assessment and the need for hands-on portfolio management throughout the investment lifecycle. Active managers conduct extensive due diligence, maintain ongoing engagement with portfolio companies, and implement rigorous impact measurement frameworks to ensure that investments deliver both financial returns and measurable social outcomes. In September 2025, Paytm Money partnered with JioBlackRock to launch an AI-driven Systematic Active Equity fund in India, using data analytics and research-led stock selection to strengthen active portfolio management practices.

Active management is further preferred because impact investing requires continuous monitoring of both financial performance and social impact metrics simultaneously. Fund managers actively support investee companies through strategic guidance, capacity building, and access to professional networks, which enhances value creation beyond mere capital provision. The relatively nascent stage of the Indian impact investing ecosystem also necessitates active involvement to navigate regulatory complexities, market inefficiencies, and the evolving landscape of social enterprise business models demanding close investor engagement.

Investor Type Insights:

- Institutional Investors

- Retail Investors

Institutional investors lead with a market share of 64.9% of the total India impact investing market in 2025.

Institutional investors represent the leading segment in the India impact investing market, reflecting the growing integration of impact and sustainability mandates within the investment strategies of pension funds, insurance companies, development finance institutions, and sovereign wealth funds. These investors bring significant scale of capital, long investment horizons, and sophisticated risk management capabilities that are well-suited for impact investing. Their participation provides credibility and stability to the market, encouraging broader investor confidence and attracting additional capital from diverse sources.

The leadership of institutional investors is further reinforced by evolving regulatory requirements that encourage consideration of environmental, social, and governance factors in portfolio construction. International development finance institutions have been particularly active in catalyzing impact capital flows into India, often serving as anchor investors in dedicated impact funds. The growing track record of competitive returns from Indian impact investments is attracting an increasing number of mainstream institutional allocators who view impact as a complement rather than a compromise to their financial objectives and fiduciary responsibilities.

Regional Insights:

- North India

- South India

- East India

- West India

West India dominates with a market share of 33.2% of the total India impact investing market in 2025.

West India holds the dominant position in the market, anchored by key states that serve as the primary financial and entrepreneurial hubs of the country. The concentration of venture capital firms, impact investment funds, financial institutions, and social enterprise headquarters in major western metropolitan areas creates a robust ecosystem for impact capital deployment. Superior infrastructure, access to skilled talent pools, and proximity to regulatory bodies further strengthen the region's leadership, enabling efficient deal origination, execution, and portfolio management across multiple impact sectors.

The dominance of West India is also supported by the region's strong manufacturing base, thriving fintech ecosystem, and growing clean energy sector, all of which present attractive investment opportunities for impact-focused capital. The presence of key financial exchanges dedicated social enterprise platforms, and a dense network of intermediaries including accelerators, incubators, and advisory firms contribute to efficient deal flow and transaction execution. The region's established corporate social responsibility culture among large industrial conglomerates also fosters a supportive environment for sustained impact investing activity.

Market Dynamics:

Growth Drivers:

Why is the India Impact Investing Market Growing?

Supportive Regulatory Framework and Government Initiatives

The Indian government and regulatory bodies have introduced progressive policies catalyzing growth in the impact investing market. The establishment of dedicated platforms for social enterprises has created structured avenues for capital raising from broader investor bases. Mandatory sustainability reporting requirements for listed companies are enhancing corporate transparency on environmental and social metrics, driving investor confidence. In December 2024, Securities and Exchange Board of India issued standardized Business Responsibility and Sustainability Reporting (BRSR) Core disclosure norms, making sustainability reporting mandatory for listed entities from FY 2024–25 onward to strengthen ESG transparency. Government-backed innovation programs provide technical and infrastructure support to impact-driven startups, nurturing a pipeline of investable enterprises. These cumulative regulatory and institutional developments are creating an enabling environment that reduces investment barriers and fosters sustained market expansion.

Rising ESG Integration Among Mainstream Investors

The integration of environmental, social, and governance criteria into mainstream investment decision-making is serving as a powerful growth driver for the India impact investing market. Institutional investors, including pension funds, insurance companies, and mutual fund houses, are increasingly embedding sustainability considerations into portfolio construction processes. Global institutional investors are allocating dedicated capital toward Indian sustainability-compliant companies, drawn by the country's economic growth trajectory and expanding responsible business landscape. The proliferation of sustainability-focused mutual funds and the development of dedicated indices on domestic stock exchanges are collectively channeling mainstream capital toward impact investments.

Expanding Role of Family Offices and Domestic Capital

Indian family offices are emerging as a significant source of impact capital, transitioning from traditional philanthropic giving toward structured impact investment strategies that blend legacy objectives with financial innovation. This evolution is unlocking substantial pools of domestic private wealth for deployment into socially relevant enterprises across healthcare, education, and sustainable development sectors. In February 2026, Premji Invest committed ₹300 crore in equity to JS Auto Cast, strengthening long-term capital support for industrial and sustainability-aligned enterprises in India’s investment ecosystem. Family offices bring patient capital, deep sectoral knowledge, and entrepreneurial networks that complement institutional funding.

Market Restraints:

What Challenges the India Impact Investing Market is Facing?

Limited Standardization of Impact Measurement

The absence of universally accepted frameworks for measuring and reporting social and environmental outcomes remains a significant restraint. Different investors and enterprises employ varying methodologies and metrics, making it challenging to compare impact performance across portfolios. This lack of standardization creates information asymmetry, complicates due diligence processes, and deters risk-averse institutional investors from increasing their impact allocations.

Shortage of Growth-Stage Impact Funds

The Indian impact investing ecosystem faces a notable gap in dedicated growth-stage funds capable of providing larger ticket sizes needed to scale proven impact enterprises. While early-stage funding has become increasingly accessible through angel investors and seed funds, the transition from venture-stage to growth-stage financing remains constrained, limiting the ability of successful social enterprises to expand operations.

Regulatory Complexity and Operational Challenges

Impact investors operating in India navigate a complex regulatory landscape spanning multiple government agencies, compliance requirements, and sector-specific regulations. Foreign investment regulations, tax structures, and reporting obligations create operational friction for both domestic and international impact funds. These cumulative compliance burdens increase transaction costs, extend deal timelines, and may discourage potential investors from entering the market.

Competitive Landscape:

The India impact investing market features a dynamic and evolving competitive landscape characterized by a diverse mix of market participants operating across multiple investment stages, asset classes, and impact sectors. The market includes dedicated impact investment funds, development finance institutions, venture capital and private equity firms with impact mandates, family offices, and increasingly, mainstream asset management companies launching ESG-focused products. Competition is intensifying as both domestic and international investors seek to deploy capital into high-growth impact enterprises. The market is witnessing growing specialization, with participants focusing on specific sectors such as climate technology, financial inclusion, or healthcare, while others adopt generalist approaches spanning multiple impact verticals.

Recent Developments:

-

In September 2025, International Finance Corporation partnered with JBM Group and GreenCell Mobility to finance electric bus deployment across Indian cities, supporting clean mobility, and scalable low-carbon urban transport aligned with national sustainability and impact investment priorities through catalytic private capital mobilization initiatives.

India Impact Investing Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Asset Classes Covered |

Equity, Fixed income, Multi-asset, Alternatives |

|

Offerings Covered |

Mutual Funds (Equity and Hybrid Funds), Bond Funds, ETFs/Index Fund, Alternatives/Hedge Funds |

|

Investment Styles Covered |

Active, Passive |

|

Investor Types Covered |

Institutional Investors, Retail Investors |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Impact Investing Market Report

The India impact investing market size was valued at USD 3,020.13 Million in 2025.

The India impact investing market is expected to grow at a compound annual growth rate of 24.25% from 2026-2034 to reach USD 22,501.7 Million by 2034.

Equity held the largest India impact investing market share, driven by growing sustainability mandates among pension funds, insurance companies, and development finance institutions that deploy large-scale capital into impact-oriented portfolios.

Key factors driving the India impact investing market include supportive regulatory frameworks such as the social stock exchange, rising ESG integration among institutional investors, an expanding pipeline of scalable impact enterprises, and increasing adoption of blended finance models.

Major challenges include limited standardization of impact measurement frameworks, a shortage of dedicated growth-stage impact funds, regulatory complexity across sectors and investment structures, information asymmetry between investors and enterprises, and the evolving maturity of the impact investing ecosystem in terms of exit pathways and secondary market liquidity.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)