India Implantable Medical Devices Market Size, Share, Trends and Forecast by Product, Material, End User, and Region, 2026-2034

India Implantable Medical Devices Market Summary:

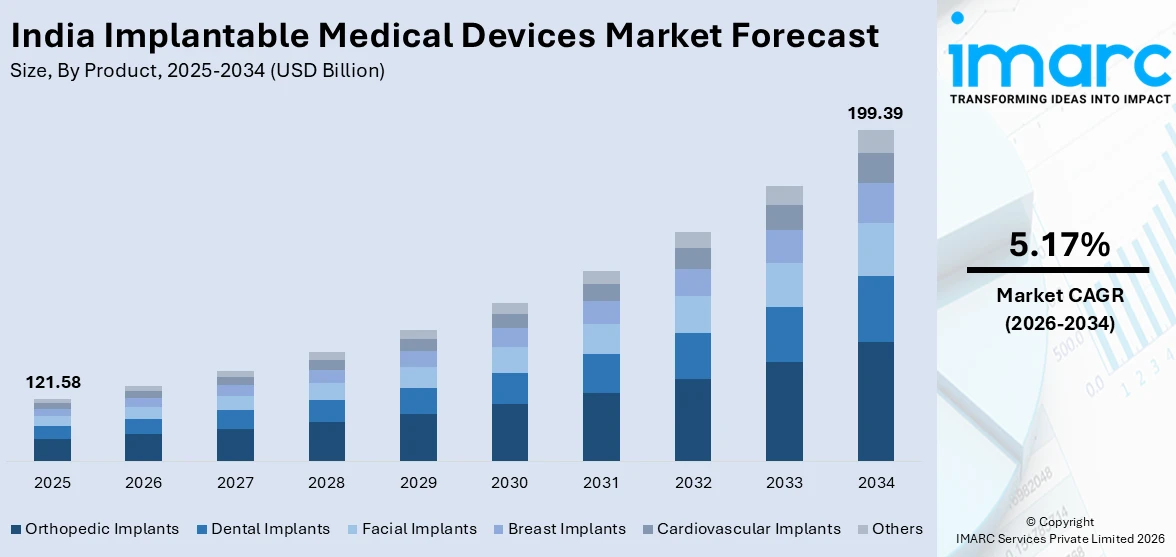

The India implantable medical devices market size was valued at USD 121.58 Billion in 2025 and is projected to reach USD 199.39 Billion by 2034, growing at a compound annual growth rate of 5.17% from 2026-2034.

The India implantable medical devices market is experiencing robust momentum as the country undergoes a significant demographic and healthcare transformation. Rising incidence of chronic and lifestyle-related disorders, expanding hospital networks, and increasing patient awareness are collectively fueling demand for advanced implantable solutions. Government-led healthcare reforms, improving surgical infrastructure, and growing medical tourism further contribute to the expanding adoption of implantable devices, strengthening the India implantable medical devices market share.

Key Takeaways and Insights:

- By Product: Orthopedic implants dominate the market with a share of 34.5% in 2025, driven by rising musculoskeletal disorders, aging demographics, and growing joint replacement procedures across urban and semi-urban healthcare facilities.

- By Material: Metals lead the market with a share of 58.5% in 2025, owing to their superior load-bearing strength, biocompatibility, and widespread application in orthopedic, cardiovascular, and dental implant categories.

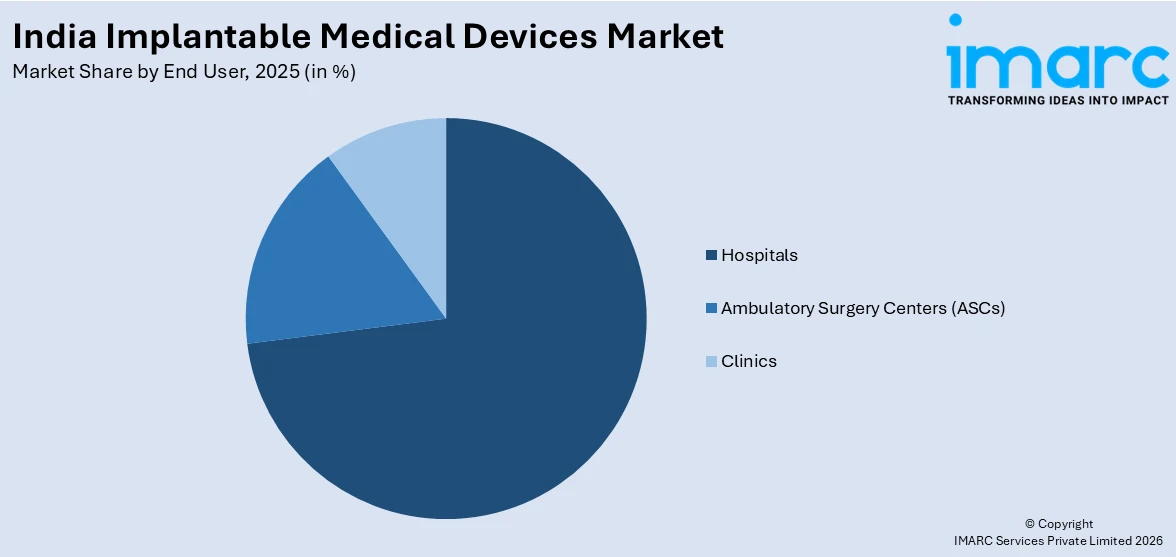

- By End User: Hospitals represent the largest segment with a market share of 72.5% in 2025, supported by advanced surgical infrastructure, specialist availability, and high patient volumes requiring complex implantation procedures.

- By Region: North India dominates the market with a share of 35.5% in 2025, reflecting the concentration of tertiary-care hospitals, medical colleges, and a dense population base driving demand for implantable medical devices.

- Key Players: The India implantable medical devices market features a dynamic competitive landscape with multinational corporations and domestic manufacturers competing across product segments. Companies are pursuing innovation through advanced materials, minimally invasive designs, and strategic collaborations to broaden their market presence and strengthen distribution networks nationwide.

To get more information on this market Request Sample

The India implantable medical devices market is evolving rapidly, supported by the convergence of demographic shifts, technological advancements, and policy reforms. India’s growing elderly population, projected to exceed 20% of the total population by 2050, is significantly increasing the incidence of age-related conditions such as osteoarthritis, cardiovascular disease, and spinal degeneration, amplifying the need for surgical implants. The Production-Linked Incentive (PLI) scheme for medical devices, with a financial outlay of Rs 3,420 crore, has catalyzed domestic manufacturing, with 19 greenfield projects already commissioned and production of 44 high-end medical device categories underway as of 2024. Moreover, the expanding reach of government-backed health insurance programs is enhancing affordability and accessibility of advanced implant-based surgical procedures. Improved financial coverage is enabling a larger section of the population, particularly in smaller cities and semi-urban areas, to undergo complex implant treatments. This broader access to quality healthcare services is supporting higher procedural volumes and contributing significantly to the overall growth of the India implantable medical devices market.

India Implantable Medical Devices Market Trends:

Rising Adoption of 3D-Printed and Customized Implants

The adoption of additive manufacturing in implantable devices is gaining significant traction across India, enabling the production of patient-specific, geometrically complex implants with superior fit and reduced material waste. This technology is particularly transformative for orthopedic and spinal applications where anatomical precision is critical for surgical outcomes. For instance, in August 2025, OIC International, Medi Mold, and AddUp announced a strategic partnership to establish India’s first advanced 3D printing-powered orthopedic implant manufacturing facility at the Andhra Pradesh MedTech Zone in Visakhapatnam, with an investment outlay exceeding Rs 100 crore.

Growth of Minimally Invasive Implant Procedures

Minimally invasive surgical approaches are transforming the implantable devices landscape as patients increasingly seek shorter hospital stays, reduced trauma, and quicker recovery. Continuous improvements in implant design, precision instruments, and robotic-assisted platforms are allowing surgeons to perform complex procedures through smaller incisions with greater accuracy. For instance, the introduction of advanced spinal implant systems in the Indian market highlights the shift toward technologies that support minimally invasive techniques. Such innovations reflect the rising demand for sophisticated surgical solutions that improve clinical outcomes and enhance patient comfort.

Expanding Medical Device Parks and Localized Manufacturing

India is witnessing a significant expansion in dedicated medical device manufacturing infrastructure, reducing import dependency and improving the affordability of implantable devices. The establishment of medical device parks in states such as Tamil Nadu, Uttar Pradesh, Madhya Pradesh, and Himachal Pradesh is creating ecosystems with shared testing facilities, regulatory infrastructure, and supply chain support. For instance, in March 2024, thirteen greenfield medical device manufacturing plants commenced operations under the PLI scheme, expanding domestic production capacity for cancer-care equipment, imaging devices, and body implants.

Market Outlook 2026-2034:

The India implantable medical devices market is positioned for sustained expansion, driven by rising chronic disease prevalence, ongoing healthcare infrastructure development, and increasing government support for domestic manufacturing. Growing adoption of smart implants, biodegradable materials, and personalized surgical solutions is expected to reshape treatment paradigms. Expansion of health insurance coverage and medical tourism will further broaden patient access to advanced implant procedures across all regions. Additionally, continuous investments in research and surgeon training programs are likely to enhance procedural success rates and accelerate long-term market growth. The market generated a revenue of USD 121.58 Billion in 2025 and is projected to reach a revenue of USD 199.39 Billion by 2034, growing at a compound annual growth rate of 5.17% from 2026-2034.

India Implantable Medical Devices Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product |

Orthopedic Implants |

34.5% |

|

Material |

Metals |

58.5% |

|

End User |

Hospitals |

72.5% |

|

Region |

North India |

35.5% |

Product Insights:

- Orthopedic Implants

- Dental Implants

- Facial Implants

- Breast Implants

- Cardiovascular Implants

- Others

Orthopedic implants dominate the market with a share of 34.5% of the total India implantable medical devices market in 2025.

Orthopedic implants represent the largest product segment, driven by the escalating burden of musculoskeletal disorders, rising road traffic accidents, and an expanding geriatric population in India. The growing prevalence of osteoarthritis, projected to affect over 60 million adults, alongside increasing sedentary lifestyles and obesity, is significantly boosting demand for joint replacement and fracture fixation devices. Hospitals in metro and tier-2 cities are witnessing a substantial rise in knee and hip replacement surgeries, with advanced implant technologies including robotic-assisted procedures and 3D-printed prosthetics improving surgical precision and patient outcomes.

The segment is supported by a combination of domestic innovation and global investment, fostering continuous technological progress. Advancements in implant surface engineering and material enhancements are improving durability, biocompatibility, and patient outcomes, reflecting the growing focus on precision-driven orthopedic solutions in India. Additionally, the India orthopedic implants market size reached USD 2.35 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 4.95 Billion by 2033, exhibiting a growth rate (CAGR) of 8.02% during 2025-2033, reflecting strong sustained demand across joint reconstruction, trauma fixation, and spinal implant categories.

Material Insights:

- Polymers

- Metals

- Ceramics

- Biologics

Metals lead the market with a share of 58.5% of the total India implantable medical devices market in 2025.

Metallic biomaterials maintain a commanding position in the India implantable medical devices market, attributed to their proven load-bearing capacity, corrosion resistance, and extensive application across orthopedic, cardiovascular, and dental implant categories. Titanium alloys and stainless steel remain the most widely utilized materials for joint prostheses, bone plates, screws, and cardiovascular stents due to their established biocompatibility profiles and mechanical strength. The segment is further supported by ongoing research into advanced alloy compositions and surface treatments that enhance implant longevity and reduce rejection rates.

Domestic manufacturers are progressively shifting toward advanced metallic materials to align with evolving global quality benchmarks. While conventional stainless steel has been widely used in orthopedic applications, there is growing preference for refined grades and titanium-based alloys that offer superior strength, corrosion resistance, and biocompatibility. This transition reflects the industry’s emphasis on meeting international regulatory expectations and enhancing product reliability. The introduction of next-generation metal-based cardiovascular implants with improved drug-delivery coatings further highlights the continued prominence of metallic innovations within the broader implantable devices segment in India.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Hospitals

- Ambulatory Surgery Centers (ASCs)

- Clinics

Hospitals represent the highest revenue with a 72.5% share of the total India implantable medical devices market in 2025.

Hospitals maintain an overwhelming share of the implantable medical devices market, driven by their advanced surgical infrastructure, availability of specialist surgeons, and capacity for complex implantation procedures requiring intensive post-operative care. There are multi-specialty and super-specialty facilities in all the metropolitan centers in India, guaranteeing large volumes of patients in joint replacement, cardiovascular stents placement, and spinal surgeries. The use of government-funded hospitals, such as Ayushman Bharat, is increasing access to implant-based treatment for the weaker groups of the population.

The ongoing expansion of hospital infrastructure is playing a vital role in market growth. The establishment of new premier medical institutions and the strengthening of existing facilities are extending advanced surgical capabilities to emerging cities, improving access to complex implant procedures and specialized care. Furthermore, the Union Budget 2025-26 allocated Rs 99,858 crore to the healthcare sector, reinforcing investments in hospital modernization, specialty departments, and surgical equipment procurement that directly support higher adoption of implantable devices.

Regional Insights:

- North India

- West and Central India

- South India

- East India

North India holds the largest share at 35.5% of the total India implantable medical devices market in 2025.

North India commands the largest regional share, driven by the concentration of premier tertiary-care hospitals, medical colleges, and specialty clinics across states such as Delhi, Uttar Pradesh, and Rajasthan. The high population base of the region, combined with the improved rates of urbanization and increased cases of chronic diseases such as cardiovascular disorders and musculoskeletal diseases create a high demand for implantable devices. The location of large healthcare centers in the Delhi-NCR area, backed by well-developed surgical facilities and the availability of specialists, only adds to the dominance of the region in the market.

Government-led initiatives are actively strengthening healthcare capacity in North India. The Greater Noida manufacturing corridor is emerging as a key hub targeting oncology and imaging equipment production, with state-level efforts aligned with federal PLI incentives to localize medical device manufacturing. In January 2024, DJ College of Dental Sciences and Research in Modinagar, Delhi NCR, launched the DJ Clinico Excellencia Academy offering advanced implantology courses, reflecting the region’s growing focus on expanding specialized implant-related education and clinical capacity.

Market Dynamics:

Growth Drivers:

Why is the India Implantable Medical Devices Market Growing?

Rising Prevalence of Chronic and Age-Related Diseases

India is witnessing a significant epidemiological shift, with non-communicable diseases now constituting the dominant share of the national disease burden. The rising prevalence of cardiovascular conditions, diabetes, osteoarthritis, and spinal disorders is creating consistent demand for implantable solutions across diverse therapeutic categories. A steadily expanding elderly population is further intensifying the requirement for joint replacements, cardiac stents, pacemakers, and spinal implants, as age-related degenerative diseases become more common and long-term treatment needs increase across the country. Diabetes cases alone are projected to rise from 77 million in 2025 to 134.2 million by 2045, increasing the need for drug-delivery implants and monitoring systems. Lifestyle factors including sedentary behavior, dietary changes, and rising obesity rates among urban populations further compound the demand for surgical intervention and advanced implantable devices.

Government Initiatives and Policy Support for Domestic Manufacturing

The Indian government has introduced structured policy initiatives to strengthen the domestic medical devices ecosystem and lower reliance on imports. Supportive incentive programs are encouraging local production of high-value medical technologies, promoting greenfield manufacturing investments and expanding export potential. In addition, the implementation of a dedicated national policy framework has provided strategic direction for research, quality standards, and innovation. The development of specialized medical device parks across multiple states is further enhancing manufacturing infrastructure, supply chain efficiency, and industry collaboration, thereby reinforcing India’s position as an emerging hub for advanced medical device production. Additionally, the Union Budget 2025-26 scaled up PLI budget allocations for the medical devices sector to Rs 1.97 lakh crore, enabling local production of advanced equipment and implants.

Expanding Healthcare Infrastructure and Insurance Coverage

The rapid expansion of healthcare infrastructure across India is directly supporting the growth of implantable medical devices. The rising concentration of hospitals in emerging cities is significantly enhancing access to complex surgical procedures that require advanced implantable devices. Expanding healthcare networks are enabling patients in semi-urban regions to receive specialized treatments closer to home. Additionally, government-backed health insurance initiatives are broadening financial coverage for secondary and tertiary care services, including procedures such as pacemaker implantation, joint replacement, and coronary stent placement. This improved affordability and accessibility are contributing to higher procedural volumes and supporting sustained growth in the implantable medical devices market across India. This expanded insurance coverage has created demand-side pressure for quality surgical infrastructure across previously underserved regions. Furthermore, FDI inflows into the medical and surgical appliances sector reached Rs 27,900.25 crore between April 2000 and June 2025, reflecting strong investor confidence in India’s growing healthcare delivery ecosystem and medical device sector.

Market Restraints:

What Challenges the India Implantable Medical Devices Market is Facing?

High Import Dependency and Cost Barriers

Despite progress in domestic manufacturing, India continues to import approximately 70-80% of its medical devices, creating cost and supply chain vulnerabilities. The high price of advanced implantable devices, particularly imported orthopedic prostheses and cardiac devices, limits accessibility for price-sensitive consumers and constrains adoption in middle and lower-income segments, especially in rural and semi-urban areas where affordability remains a critical barrier to treatment.

Regulatory Complexities and Approval Delays

The evolving regulatory landscape, while improving, still presents challenges for manufacturers seeking to introduce new implantable devices in the Indian market. Unpredictable approval timelines from the Central Drugs Standard Control Organization, coupled with inconsistencies in state-level licensing requirements, can delay product launches and increase compliance costs. These regulatory hurdles particularly affect smaller domestic manufacturers seeking to compete with established multinational players.

Limited Specialist Availability in Rural Regions

The uneven distribution of trained surgical specialists across India remains a significant constraint on implantable device adoption. Advanced implant procedures require highly skilled surgeons, specialized infrastructure, and post-operative care capabilities that are concentrated primarily in metropolitan centers. The shortage of orthopedic, cardiovascular, and neurosurgery specialists in rural and tier-3 areas limits patient access to implant-based treatments despite improving insurance coverage.

Competitive Landscape:

The India implantable medical devices market exhibits an intensely competitive landscape characterized by the coexistence of established multinational corporations and a growing cohort of domestic manufacturers. Competition is driven by product innovation, pricing strategies, distribution network expansion, and regulatory compliance capabilities. Multinational companies leverage their technological expertise and global research infrastructure to introduce advanced implant systems, while Indian manufacturers focus on cost-effective alternatives designed for the domestic patient anatomy and clinical requirements. Strategic acquisitions, joint ventures, and manufacturing partnerships are reshaping market dynamics, with increasing private equity investment signaling confidence in the sector’s long-term growth trajectory. The government’s emphasis on self-reliance and localized production is further intensifying competition as companies seek to establish domestic manufacturing bases.

Recent Developments:

- In May 2024, KKR signed definitive agreements to acquire Healthium MedTech, a Bengaluru-based medical devices company, from Apax Partners in a deal valued at approximately Rs 7,000 crore (USD 839 million). Healthium, the world’s fourth-largest surgical suture manufacturer with an 18% market share in India, has a presence in more than 90 countries across wound closure, arthroscopy, and advanced wound care product categories.

- In May 2024, Abbott launched the XIENCE Sierra everolimus-eluting coronary stent system in India, expanding its cardiovascular implant portfolio. The advanced drug-eluting stent system is designed to improve patient outcomes in coronary artery interventions through enhanced drug delivery and stent architecture.

India Implantable Medical Devices Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Orthopedic Implants, Dental Implants, Facial Implants, Breast Implants, Cardiovascular Implants, Others |

| Materials Covered | Polymers, Metals, Ceramics, Biologics |

| End Users Covered | Hospitals, Ambulatory Surgery Centers (ASCs), Clinics |

| Regions Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Implantable Medical Devices Market Report

The India implantable medical devices market size was valued at USD 121.58 Billion in 2025.

The India implantable medical devices market is expected to grow at a compound annual growth rate of 5.17% from 2026-2034 to reach USD 199.39 Billion by 2034.

Orthopedic implants held the largest revenue share of 34.5% in 2025, driven by the rising prevalence of musculoskeletal disorders, an aging population, and increasing joint replacement surgical volumes across urban and semi-urban healthcare facilities in India.

Key factors driving the India implantable medical devices market include the rising prevalence of chronic diseases, expanding healthcare infrastructure, government initiatives such as the PLI scheme, increasing health insurance penetration, and technological advancements in implant design and materials.

Major challenges include high import dependency, elevated costs of advanced implantable devices, regulatory complexities and approval delays, limited specialist availability in rural regions, and supply chain constraints affecting domestic manufacturing scalability.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)