India In-App Advertising Market Size, Share, Trends and Forecast by Type, Platform, Application, and Region, 2026-2034

India In-App Advertising Market Summary:

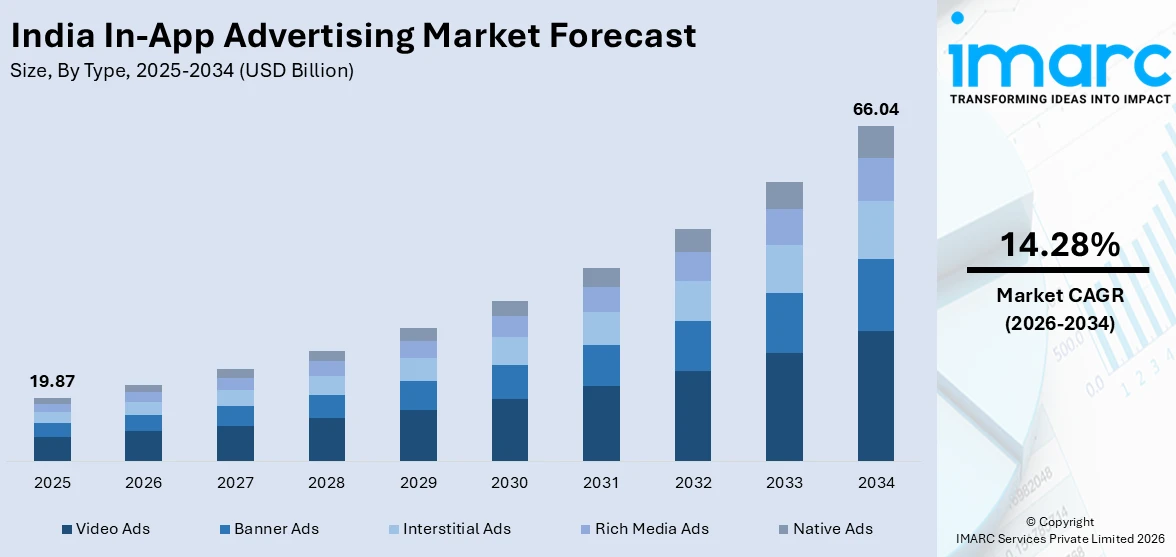

The India in-app advertising market size was valued at USD 19.87 Billion in 2025 and is projected to reach USD 66.04 Billion by 2034, growing at a compound annual growth rate of 14.28% from 2026-2034.

The in-app advertising sector in India is growing as brands devote more resources to mobile-centric strategies fueled by the rising adoption of smartphones and cost-effective data services. Increased funding in programmatic advertising, the rise of video and interactive ad types, and enhancements in artificial intelligence (AI)-based targeting are transforming demand trends. The growing digital commerce landscape, heightened mobile gaming interaction, and escalating app-centric user habits are contributing to the India in-app advertising market share.

Key Takeaways and Insights:

- By Type: Video ads lead the market with a share of 35% in 2025, driven by the growing individual preference for immersive short-form and rewarded video content across mobile applications.

- By Platform: Android represents the largest segment with a market share of 70% in 2025, reflecting India's overwhelming reliance on the Android operating system across budget and mid-range smartphone categories.

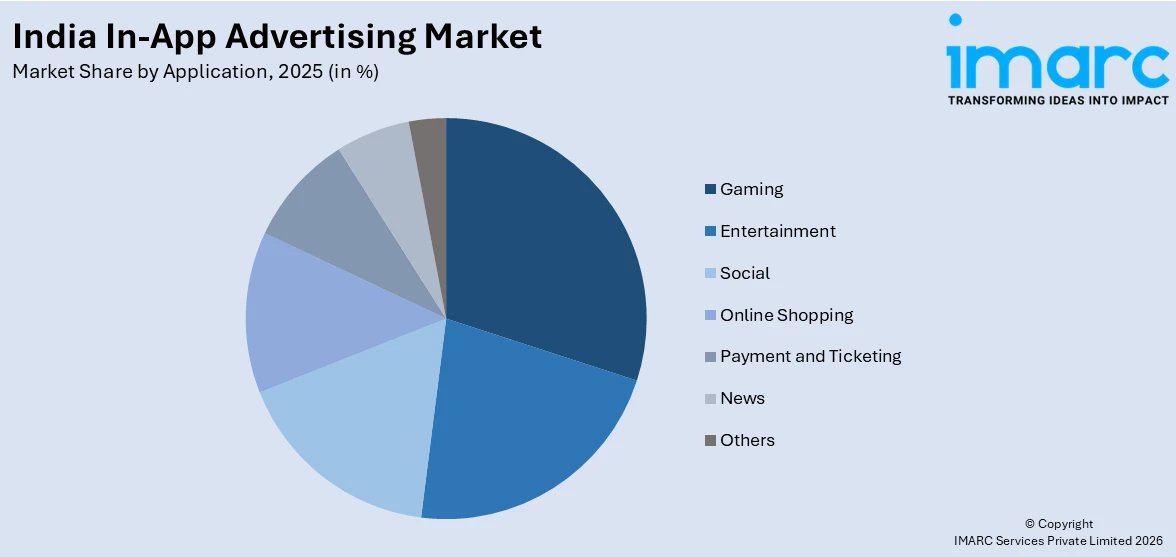

- By Application: Gaming dominates the market with a share of 29% in 2025, fueled by India's massive mobile gaming user base and the effectiveness of rewarded and interstitial ad placements within gaming environments.

- Key Players: The India in-app advertising market features intense competition among global technology platforms and domestic adtech innovators, with companies leveraging AI-driven optimization, programmatic buying, and cross-channel monetization to capture advertiser spending.

To get more information on this market Request Sample

The India in-app advertising market is strongly influenced by the country’s position as one of the world’s largest mobile-first digital economies, where smartphones serve as the primary gateway to the internet for a broad cross-section of the population. The scale of this opportunity is substantial, with India projected to have over 900 million active internet users by 2025, creating an expansive addressable audience for advertisers seeking reach and frequency within app environments. As digital consumption continues to rise across commerce, entertainment, and financial services applications, mobile devices account for a dominant share of total digital advertising expenditure. Within mobile, in-app placements contribute the majority of revenue, supported by higher engagement levels, immersive ad formats, and advanced targeting capabilities. This convergence of scale, usage intensity, and monetization efficiency continues to anchor sustained growth in the in-app advertising segment across the country.

India In-App Advertising Market Trends:

Rapid Smartphone Penetration and Affordable Data Access

India is experiencing sustained rise in smartphone adoption across urban and rural regions, supported by affordable devices and competitively priced mobile data services. This widening access is deepening digital participation across income segments, increasing time spent on applications spanning communication, entertainment, commerce, and financial services. The strength of this penetration is reflected in the Comprehensive Modular Survey: Telecom, 2025, which reported smartphone ownership among youth aged 15–29 at 95.5% in rural areas and 97.6% in urban centers, underscoring near-universal access within key demographics. As mobile devices anchor internet usage, advertisers are directing higher budgets toward in-app environments that offer scale, segmentation precision, and measurable engagement outcomes.

Rise of Mobile Gaming and Digital Entertainment Platforms

Mobile gaming and streaming applications are developing into high-engagement digital environments supported by substantial daily active user bases. Free-to-play gaming models depend heavily on advertising-led monetization, incorporating rewarded videos and interactive formats that encourage voluntary participation and sustained session times. The commercial significance of this segment is evident, with the India mobile gaming market valued at USD 3.5 billion in 2025 and projected by IMARC Group to reach USD 12.0 billion by 2034. Entertainment and short-video platforms similarly rely on advertising income to fund content creation and distribution. Elevated engagement levels within these applications enhance ad visibility, interaction rates, and brand recall, strengthening in-app advertising effectiveness.

Growth of Digital Payments and E-Commerce

The rapid growth of digital payments and online commerce platforms is catalyzing the demand for performance-oriented in-app advertising across India. As people browse products, complete transactions, and engage with brands through mobile applications, advertisers are using in-app placements to influence purchase decisions at critical conversion points. The scale of this opportunity is reflected in data from IBEF, which values India’s e-commerce industry at INR 10,82,875 crore (USD 125 billion) in 2024 and projects expansion to INR 29,88,735 crore (USD 345 billion) by 2030 at a 15% CAGR. Behavioral insights generated within shopping and payment apps enable sharper targeting and campaign optimization, reinforcing monetization potential within integrated app ecosystems.

Market Outlook 2026-2034:

The in-app advertising market in India is set for ongoing growth during the forecast period, fueled by increasing smartphone usage, a rise in digital commerce, and shifting advertiser approaches toward mobile-centric engagement. The market generated a revenue of USD 19.87 Billion in 2025 and is projected to reach a revenue of USD 66.04 Billion by 2034, growing at a compound annual growth rate of 14.28% from 2026-2034. Improvements in AI-driven targeting, the proliferation of 5G connectivity, and the increasing importance of video and interactive ad formats are anticipated to boost revenue streams and strengthen India's role as a vital growth engine in the global in-app advertising landscape.

India In-App Advertising Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Type | Video Ads | 35% |

| Platform | Android | 70% |

| Application | Gaming | 29% |

Type Insights:

- Banner Ads

- Interstitial Ads

- Rich Media Ads

- Video Ads

- Native Ads

Video ads dominate with a market share of 35% of the total India in-app advertising market in 2025.

Video ads lead the market due to their strong engagement rates and superior storytelling ability. Short-form and reward-based videos capture user attention far more effectively than static banners, especially among young mobile-first audiences. India’s rapid growth in affordable smartphones and low-cost data plans is accelerating video viewership across gaming, social media, and OTT platforms. Advertisers prefer video formats because they allow brand narratives, product demonstrations, and emotional messaging within seconds, driving higher click-through and conversion rates. The measurable performance metrics attached to video campaigns further strengthen advertiser confidence and repeat spending. This dominance continues across diverse app categories nationwide at present scale.

Another key factor supporting video ad leadership is the rise of programmatic buying and advanced targeting tools within Indian app ecosystems. Brands can segment audiences by location, language, device usage, and behavioral patterns, ensuring that video creatives reach high-intent users. The popularity of vernacular content has also encouraged localized video campaigns that resonate strongly beyond metro cities. Rewarded video formats in mobile games offer tangible incentives, increasing completion rates and positive brand recall. In addition, social commerce integrations within apps enable seamless transitions from video viewing to in-app purchases, strengthening return on ad spend for performance-driven marketers. This sustained effectiveness secures their top revenue share position in the market.

Platform Insights:

- Android

- iOS

- Others

Android leads with a market share of 70% of the total India in-app advertising market in 2025.

Android represents the largest segment owing to its overwhelming smartphone user base across urban and rural regions. The availability of affordable Android devices from multiple domestic and international manufacturers has expanded mobile internet penetration at scale. This wide reach makes Android the preferred platform for advertisers seeking mass visibility and consistent campaign performance. App developers also prioritize Android-first launches, resulting in a larger inventory of apps across gaming, entertainment, fintech, and e-commerce. The open ecosystem supports diverse ad formats and seamless third-party integrations, enabling efficient monetization. Higher install volumes further generate substantial ad impressions daily across diverse consumer segments nationwide.

Another factor contributing to Android's dominance is its significant presence in tier II and tier III cities, where mobile usage is still growing quickly. Advertisers focusing on regional language audiences consider Android highly effective because of its extensive reach beyond just premium device users. The Google Play ecosystem additionally offers advanced analytics, real-time bidding, and scalable campaign management, providing marketers with quantifiable results. In-app purchases, digital payments, and social media engagement are predominantly found on Android devices, enhancing monetization prospects. Reduced app development expenses for Android compared to iOS motivate startups and local developers to create Android-centric applications, further increasing ad inventory. This ongoing scale benefit maintains Android's lead in platform market share.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Entertainment

- Gaming

- Social

- Online Shopping

- Payment and Ticketing

- News

- Others

Gaming exhibits a clear dominance with a 29% share of the total India in-app advertising market in 2025.

Gaming commands the largest share of in-app advertising, supported by a vast and highly engaged user base spanning multiple age cohorts. Mobile games attract millions of daily active users who spend extended durations within applications, generating frequent and high-visibility advertising opportunities. Reflecting this scale, India’s online gaming sector is projected to expand more than two-fold, rising from INR 31,938 Crore in 2024 to INR 78,551 Crore by 2029, reinforcing advertiser interest in the segment. Strong repeat usage, diverse ad formats, and reliance on ad-based monetization collectively sustain gaming’s dominance within the in-app advertising landscape.

Another factor supporting gaming’s leadership is the effectiveness of rewarded advertising formats within gameplay environments. Users are more willing to watch ads in exchange for in-game currency, extra lives, or exclusive features, resulting in high completion rates. The interactive nature of playable ads further boosts engagement compared to static formats. Gaming apps also benefit from strong penetration in tier II and tier III cities, supported by affordable smartphones and low data costs. Brands across e-commerce, fintech, and entertainment sectors increasingly use gaming platforms for performance marketing campaigns. The combination of scale, engagement depth, and monetization efficiency secures gaming’s top position in application share across India.

Regional Insights:

- North India

- South India

- East India

- West India

North India serves as a significant center for in-app advertising, fueled by the high population density in major cities like Delhi-NCR and nearby urban locations. The area gains from higher digital literacy levels, increasing disposable incomes, and considerable smartphone usage in both urban and semi-urban areas. The Ministry of Statistics (MoSPI) announced that per capita Net National Income rose to ₹2,05,324 in FY2024-25, compared to ₹1,88,892 in FY2023-24, indicating enhanced earnings and better consumption ability. The clustering of corporate offices and advertising firms also boosts the need for focused mobile advertising efforts, positioning North India as a crucial region for in-app ad expenditure distribution.

South India is emerging as a rapidly growing center for in-app advertising, backed by its sophisticated technology infrastructure and dense presence of IT centers in cities like Bangalore, Hyderabad, and Chennai. The area's digitally advanced population shows significant involvement with mobile apps across gaming, entertainment, and e-commerce. Higher average incomes and better internet connectivity are facilitating the use of premium ad formats, making South India a vital player in the growth of in-app advertising revenue.

East India offers considerable growth opportunities for in-app advertising as digital adoption speeds up in both metropolitan and tier-two cities, such as Kolkata, Patna, and Bhubaneswar. Government-driven digitalization efforts and the accessibility of budget-friendly smartphones are broadening the app user population among previously neglected demographics. The increasing penetration of e-commerce and the heightened engagement in mobile gaming within the region are generating new advertising inventory sources that brands are more frequently aiming for in their regional campaign executions.

West India is a key contributor to in-app advertising revenue, supported by Mumbai's role as India's financial and entertainment hub, along with the booming commercial environments in Ahmedabad and Pune. The area shows robust mobile commerce engagement, elevated social media interaction, and considerable interest in entertainment and streaming apps. The combination of a strong advertising industry presence, elevated urbanization levels, and wealthy individual demographics positions West India as a crucial market for the expansion of in-app advertising.

Market Dynamics:

Growth Drivers:

Why is the India In-App Advertising Market Growing?

Advancements in Ad Technology and Programmatic Buying

Continuous developments in mobile advertising frameworks are greatly enhancing the effectiveness and accuracy of in-app campaigns throughout India. Platforms for programmatic buying, backed by real-time bidding processes and cohesive data management systems, facilitate automated media purchases and precise audience targeting on a large scale. Enhanced ad formats, including rewarded video, interactive banners, and native placements, improve engagement while maintaining the overall app experience and usability. Concurrent improvements in fraud detection technologies and brand safety protocols are strengthening advertiser trust in mobile ecosystems. These innovations lower transactional inefficiencies, enhance revenue realization for publishers, and facilitate complex, performance-oriented campaign execution, thereby supporting the growth of the in-app advertising market in India.

Growth of Regional and Vernacular Content

The increasing preference for regional language content is significantly expanding India’s digital audience beyond metropolitan centers, drawing substantial participation from Tier II and Tier III cities. Applications offering vernacular news, entertainment, social networking, and short-form video are witnessing stronger adoption as users engage more comfortably in their native languages. This shift is encouraging ecosystem-level investments, reflected in 2024 when PhonePe launched the Indus Appstore in New Delhi, introducing a localized Android marketplace featuring over 2 lakh apps across 45 categories, discovery support in 12 Indian languages, and a short-video feature for app exploration, alongside zero listing fees for one year. Such initiatives reinforce localized engagement and strengthen monetization potential within diverse app environments.

Rising Digital Advertising Budgets and Performance Focus

Brands across India are progressively reallocating marketing budgets from traditional media channels to digital platforms, supported by stronger measurability and refined targeting capabilities. In-app advertising, in particular, offers real-time campaign optimization, granular audience segmentation, and detailed attribution tracking that align closely with performance-led marketing priorities. Advertisers are placing greater emphasis on return on investment, selecting channels that provide transparent analytics on impressions, clicks, installs, and conversions. The integration of advertisements with app-based commerce ecosystems and digital payment interfaces further strengthens conversion tracking and revenue accountability. This performance-oriented allocation of spending continues to drive sustained shift toward scalable and data-backed in-app advertising formats.

Market Restraints:

What Challenges the India In-App Advertising Market is Facing?

Data Privacy Regulations and User Consent Requirements

India's evolving data protection framework, particularly the implementation of the Digital Personal Data Protection Act, is creating compliance complexities for in-app advertisers reliant on behavioral targeting. Restrictions on third-party data collection and requirements for explicit user consent are challenging established targeting methodologies, requiring platforms to develop alternative privacy-first advertising approaches.

Ad Fatigue and Rising User Resistance

Rising exposure to advertisements within mobile applications is contributing to user fatigue and diminishing engagement with traditional ad formats. Frequent or intrusive placements can disrupt user experience, prompting individuals to exit applications or install ad blocking tools. This behavior reduces overall ad visibility and weakens the effectiveness and perceived return on investment of in app advertising strategies for developers and marketers.

Monetization Challenges in a Price-Sensitive Market

India’s predominantly price sensitive consumer base creates monetization challenges for in app advertisers aiming to achieve premium engagement outcomes. Lower average revenue per user relative to developed markets limits advertiser budgets for high cost interactive and video formats. This environment places downward pressure on cost per impression rates and constrains overall revenue generation potential for app publishers and advertising platforms.

Competitive Landscape:

The India in-app advertising market exhibits intensifying competition characterized by the presence of global technology platforms, specialized mobile advertising networks, and emerging domestic adtech innovators. Market participants are differentiating through investments in AI-powered optimization engines, programmatic buying capabilities, and cross-channel monetization solutions. Strategic emphasis on privacy-compliant targeting methodologies, contextual advertising, and first-party data partnerships is reshaping competitive positioning. The evolving regulatory environment and growing advertiser demand for measurable outcomes are driving consolidation and innovation across the value chain, fostering a dynamic competitive ecosystem.

Recent Developments:

- January 2025: Aarki Inc. launched Aarki Labs in Bangalore to strengthen innovation in AI-powered advertising and performance marketing solutions. The new center planned to focus on deep neural networks, privacy-first ad technologies, and product development.

India In-app advertising Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Banner Ads, Interstitial Ads, Rich Media Ads, Video Ads, Native Ads |

| Platforms Covered | Android, iOS, Others |

| Applications Covered | Entertainment, Gaming, Social, Online Shopping, Payment and Ticketing, News, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India In-app Advertising Market Research Report and Industry Forecast Report

The India in-app advertising market size was valued at USD 19.87 Billion in 2025.

The India in-app advertising market is expected to grow at a compound annual growth rate of 14.28% from 2026-2034 to reach USD 66.04 Billion by 2034.

Video ads dominate the market with the largest revenue share of 35% in 2025, driven by rising user engagement with short-form and rewarded video content across mobile applications, creating premium monetization opportunities.

Key factors driving the India in-app advertising market include sustained growth in smartphone adoption across urban and rural regions, supported by affordable devices and data plans; the Comprehensive Modular Survey: Telecom, 2025, reported ownership among youth at 95.5% in rural and 97.6% in urban areas, expanding advertiser reach.

Major challenges include evolving data privacy regulations under India's Digital Personal Data Protection Act, rising ad fatigue among mobile users, monetization constraints in a price-sensitive market, and the need for privacy-compliant targeting alternatives as third-party data restrictions intensify.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)