India In Vitro Diagnostics Market Size, Share, Trends and Forecast by Test Type, Product, Usability, Application, End User, and Region, 2026-2034

India In Vitro Diagnostics Market Size & Forecast 2026-2034

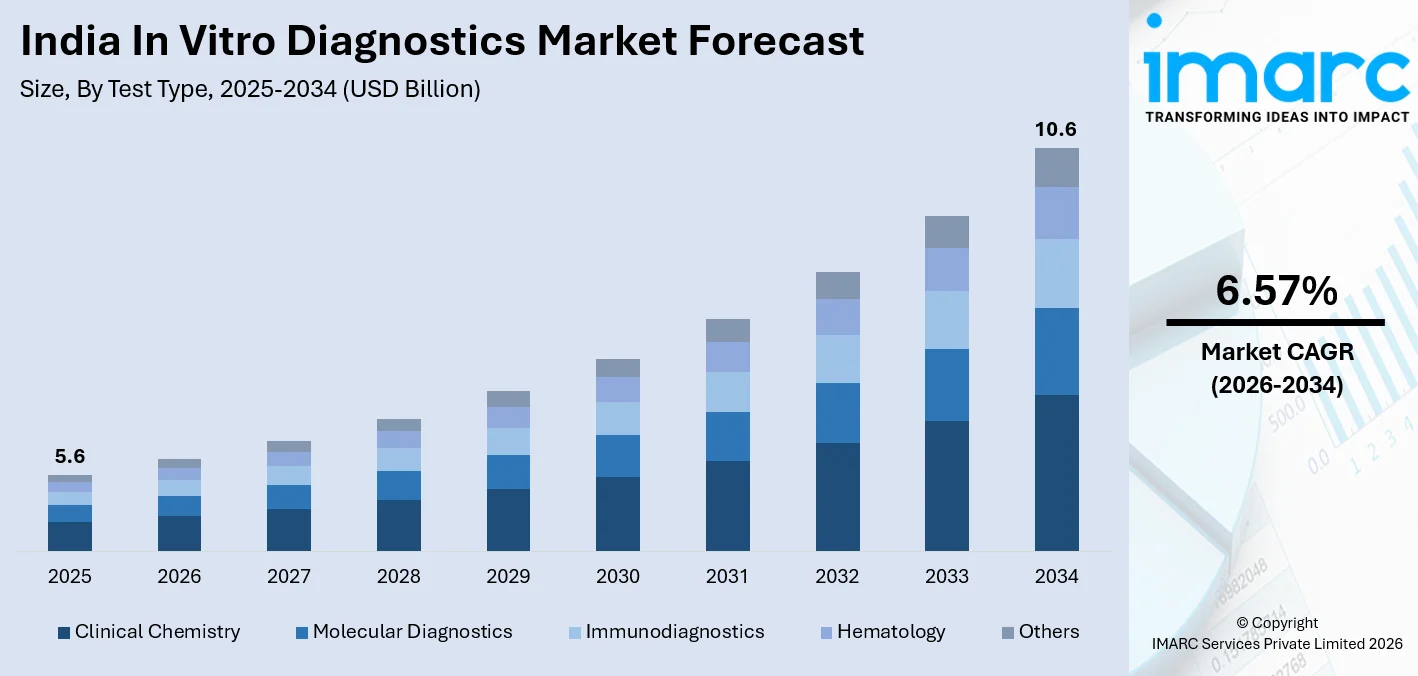

India in vitro diagnostics market size stood at USD 5.6 Billion in 2025, and it is expected to reach USD 10.6 Billion by 2034, with a compound annual growth rate of 6.57% during 2026-2034. The in vitro diagnostics market in India is growing at a fast rate, driven by factors like the rising incidence of infectious and non-communicable diseases, government spending in universal healthcare, and the rapid adoption of molecular and point of care technologies. In 2024, India registered 26.18 lakh tuberculosis cases, the highest as compared to the rest of the world. This is a clear indication of the demand for diagnostic testing at all levels of healthcare delivery. An increase in domestic production of reagents under the Production Linked Incentive Scheme and rising adoption of automated laboratory technologies will only add to the India in vitro diagnostics market share.

To get more information on this market Request Sample

India In Vitro Diagnostics Industry Analysis: Key Insights

- Clinical chemistry accounted for 28.4% by test type in 2025 of the India in vitro diagnostics market in 2025 because mass deployment of automated biochemistry analysers for routine glucose, renal, and hepatic panel testing firmly anchors this segment as the highest-volume test type category.

- Reagents and kits commanded a 63.2% share by product in 2025, driven by the consumable economics of diagnostics, high repeat-purchase frequency across a large installed instrument base, and PLI-linked scale-up of domestic reagent production by Indian manufacturers.

- Disposable IVD devices held 58.7% of the usability segment in 2025, as infection-control protocols and regulatory preference for single-use consumables, combined with rapid POCT rollout in primary health centres, entrench disposables as the standard format across all care settings.

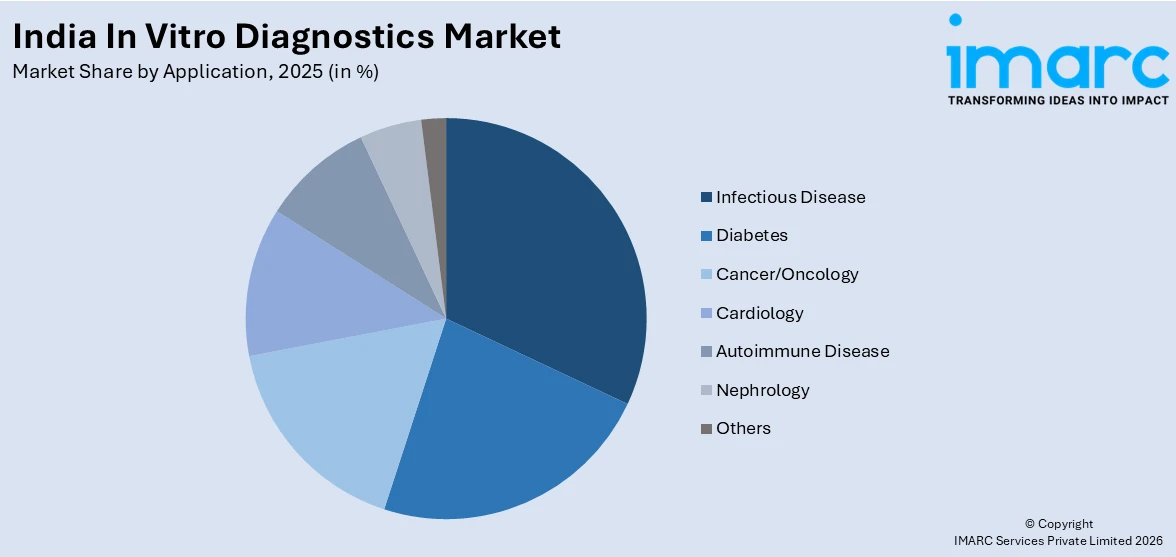

- Infectious disease diagnostics led at 24.6% by application in 2025, underpinned by India's large and persistent caseloads of tuberculosis, malaria, dengue, HIV, and hepatitis, all of which are supported by structured national health programme testing mandates.

- Hospitals laboratories dominated end-user demand at 35.1% by end user in 2025, supported by expanding hospital infrastructure, dedicated in-house pathology departments in corporate hospital chains, and PM-JAY-funded patient volumes requiring diagnostic support.

- West and Central India accounted for 31.8% by region in 2025, and this is the highest concentration across all four regions, anchored by Maharashtra and Gujarat's dense private hospital networks, a mature pharmaceutical manufacturing ecosystem, and above-average per-capita health expenditure.

India In Vitro Diagnostics Market Trends and Dynamic 2026:

Market Trends

Integration of AI-Powered Platforms and Laboratory Automation

India’s diagnostic laboratories are adopting in vitro diagnostics industry market trends in artificial intelligence data analytics and pre-analytical processing automation to reduce turnaround times and minimize human error. In January 2024, Siemens Healthineers and the Indian Institute of Science (IISc) inaugurated the Siemens Healthineers-Computational Data Sciences (CDS) Collaborative Laboratory for AI in Precision Medicine. Meanwhile, in September 2025, ICMR and CDSCO released 39 standardised IVD evaluation protocols through the IVD validation portal at the VRDL Conclave. This provides a framework that not only supports but actively promotes the use of validated automated systems in clinical laboratory settings in India.

Rapid Expansion of Point-of-Care Testing Infrastructure

The decentralisation of diagnostic services to primary health centers, pharmacies, and communities is changing the way diagnostic services are provided to patients. The bioeconomy in India has risen from a $10 billion in 2014 to $165.7 billion in 2024, which is a reflection of the scale of indigenous diagnostic manufacturing capacity. In April 2025, Healthians launched its 'Health on Wheels' initiative for Mumbai, which is a mobile diagnostic service for residential areas, reflecting a structural change in diagnostic services from traditional hospital and lab models in tier-2 and tier-3 cities.

Accelerated Clinical Adoption of Molecular Diagnostics

Molecular tests such as real-time PCR and next-generation sequencing technologies are shifting from reference labs to mainstream use, with government programs to eliminate infectious diseases serving as catalysts. In March 2025, HaystackAnalytics introduced its TB One whole-genome sequencing pre-processing kit at the ICMR Innovation Summit. It is meant to support drug resistance profiling of tuberculosis pathogens. In April 2025, ABL Diagnostics signed an exclusive distribution deal with Genient Tech to provide its DeepChek and UltraGene molecular assay platforms. It is meant to increase access to validated molecular tests across various hospitals. These catalysts of growth in the in vitro diagnostics market continue to shift molecular tests from reference labs to mainstream use.

Growth Drivers

Rising dual burden of infectious and non-communicable diseases: India is home to one of the most complex disease landscapes in the world, with high-volume communicable disease programmes and a growing number of patients with chronic diseases. With 26.18 lakh TB cases confirmed in 2024, the scale of repeat diagnostic tests is built into both public and private healthcare paradigms. The TB Mukt Bharat Abhiyan programme screened 19 crore people and resulted in 24.5 lakh patients being detected, resulting in a high volume of repeat rapid molecular and conventional diagnostic tests in district and primary healthcare facilities in India.

Government healthcare investment and universal health coverage expansion: India’s Union Budget 2026-27 allocated ₹ 1,06,530.42 crores to Ministry of Health, reflecting an increase of nearly 10% over the revised estimates of FY 2025–26, directly increasing public diagnostic procurement budgets. The allocation to PM-ABHIM is up by 67.66% to ₹ 4,770 Crore, supporting district-level laboratory infrastructure development. The allocation to NHM of INR 39,390 crore maintains the IDSP network of district-level laboratories, ensuring ongoing government-funded test volumes are available for communicable disease diagnostics. The India in vitro diagnostics market forecast is supported by this pipeline of public sector investment.

Rising Chronic Disease Prevalence: India's expanding diabetic population, growing cancer burden, and cardiovascular disease incidence are creating sustained high-frequency testing requirements across hospital and clinical laboratory settings.

- Expanding Private Diagnostic Chain Networks: Corporate diagnostic chains like Thyrocare, Dr. Lal PathLabs, and Metropolis are expanding their collection center networks to tier 2 cities, thus increasing accessibility of tests and driving reagent consumption growth across India.

- Foreign Investment and Technology Transfer: Multinational Diagnostics Companies are strengthening local partnerships and manufacturing commitments, thereby transferring advanced assay technologies and raising the technical level of diagnostic products available in India.

- Digital Health Integration and Tele-Diagnostics: Bharatnet broadband roll-out to PHCs facilitates digital laboratory connectivity, tele-diagnostic consultations, and remote interpretation of results, thereby expanding the utility of IVD products to untapped rural geographies.

Market Restraints

Fragmented regulatory and accreditation environment: India's diagnostic industry is currently operating in a heterogeneous environment with a lack of state-level implementation of the Clinical Establishments Act, leading to variable quality levels across India. Mandatory clinical validation in individual clinical settings also adds to the timelines in getting products cleared in India, especially for small Indian players and importers of new technologies in assays.

High level of dependency on imports of high-end diagnostic equipment: India is still largely dependent on imports of high-end molecular diagnostic equipment, mass spectrometers, and immunology automation systems from Germany, the US, and Japan. Such a high level of dependency on imports is a concern in India due to fluctuations in exchange rates and long lead times in procurement.

Lack of skilled personnel in laboratory and molecular diagnostics: India is also facing a structural shortage of skilled personnel in laboratory and molecular diagnostics, which is impacting the current level of usage of existing diagnostic assets and limits the adoption of high-end molecular diagnostic equipment that require skilled personnel to operate.

India In Vitro Diagnostics Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Test Type | Clinical Chemistry | 28.4% | 2025 |

| Product | Reagents and Kits | 63.2% | 2025 |

| Usability | Disposable IVD Devices | 58.7% | 2025 |

| Application | Infectious Disease | 24.6% | 2025 |

| End User | Hospitals Laboratories | 35.1% | 2025 |

| Region | West and Central India | 31.8% | 2025 |

Test Type Insights

Clinical Chemistry- 28.4% Market Share (2025) | Leading Test Type

Clinical chemistry analysers form the operational backbone of India's hospital and commercial diagnostic laboratories, handling the highest daily testing volumes across glucose, renal, hepatic, and lipid panels. These instruments are central to chronic disease management for India's over 77 million diagnosed diabetics and are standard equipment in both public tertiary hospitals and private diagnostic chains. The strong installed base led by Transasia Bio-Medicals and multinational brands, generates sustained reagent consumption, making clinical chemistry the highest-revenue and highest-volume test type in the India in vitro diagnostics market.

|

Segment Breakdown Clinical Chemistry (28.4%) · Molecular Diagnostics · Immunodiagnostics · Hematology · Others |

Product Insights

Reagents and Kits- 63.2% Market Share (2025) | Leading Product

This dominance of reagents and kits is also linked to the economics of consumables and diagnostics, as well as the increased number of installed bases in India. As laboratories increase their scale of testing, there is a corresponding increase in consumables, thereby ensuring a steady flow of revenue. The implementation of PLI-based incentives has encouraged Indian manufacturers, including Agappe Diagnostics and J. Mitra & Co., to modernize their production lines to cater to clinical chemistry and immunology reagent requirements.

|

Segment Breakdown Reagents and Kits (63.2%) · Instruments |

Usability Insights

Disposable IVD Devices- 58.7% Market Share (2025) | Leading Usability

Single-use diagnostic consumables, which include lateral flow rapid test strips, capillary blood collection devices, and pre-filled reagent cartridges, are favored across India’s wide spectrum of healthcare delivery systems due to their infection control benefits and ease of use. In February 2026, ECDS, which operates in the field of sustainable development technologies, announced its plan to establish its first medical equipment manufacturing unit in India, which will be located in Ujjain, Madhya Pradesh. The investment of Rs 780 crore will be done on a joint venture (JV) basis with three South Korean companies. The unit will be set up on 15.60 acres of land at the Medical Equipment Park in Vikram Udyogpuri, Ujjain. This is indicative of the scale of requirement for disposable diagnostic consumables and is also a reflection of increased investor confidence in India’s domestic ecosystem for consumable IVD products.

|

Segment Breakdown Disposable IVD Devices (58.7%) · Reusable IVD Devices |

Application Insights

Access the comprehensive market breakdown Request Sample

Infectious Disease- 24.6% Market Share (2025) | Leading Application

India has 25% of the global tuberculosis burden. In 2024, India reported a record number of 26.18 lakh tuberculosis cases. The diagnostic market is also seeing significant volumes in dengue, malaria, typhoid, HIV, and hepatitis B and C, owing to government mandates. The national program for disease elimination is also driving demand for IVD kits and reagents in primary and district healthcare centers. Hence, infectious diseases diagnostics is the largest market segment.

|

Segment Breakdown Infectious Disease (24.6%) · Diabetes · Cancer/Oncology · Cardiology · Autoimmune Disease · Nephrology · Others |

End User Insights

Hospitals Laboratories- 35.1% Market Share (2025) | Leading End User

In-house hospital labs are responsible for emergency, inpatient, and outpatient diagnostic work, which cannot be outsourced. Hence, this is another captive market segment. Corporate hospital chains like Apollo, Fortis, and Manipal are investing in high-throughput automated lab equipment to keep up with increasing patient volumes in multi-specialty hospitals. Public sector hospitals receiving grants under PM-ABHIM and NHM are also investing in lab equipment.

|

Segment Breakdown Hospitals Laboratories (35.1%) · Clinical Laboratories · Point-of-care Testing Centers · Academic Institutes · Patients · Others |

Regional Insights

West and Central India- 31.8% Market Share (2025) | Leading Region

West and Central India is home to the in vitro diagnostics market, with Maharashtra and Gujarat being the commercial core of this industry. Mumbai is home to the national diagnostic chains' headquarters, including Dr. Lal PathLabs, SRL Diagnostics, and Metropolis, which have high-volume central laboratories conducting diagnostic tests for Maharashtra, Goa, and Madhya Pradesh. Ahmedabad and Pune are gaining prominence as pharmaceutical and medical device manufacturing centers related to diagnostics.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

31.8%

|

|

Key States

|

Maharashtra, Gujarat, Goa, Madhya Pradesh |

|

Major Growth Drivers

|

Dense private hospital networks, pharmaceutical manufacturing cluster, high per-capita health expenditure, multinational diagnostics presence |

|

Outlook

|

Sustained regional leadership with premium diagnostics growth |

|

Regional Breakdown West and Central India (31.8%) · South India · North India · East and Northeast India |

South India:

South India has a high healthcare literacy rate and an advanced private hospital market, as well as a developing life science manufacturing industry. Tamil Nadu and Karnataka are the major contributors to this market. Siemens has committed an investment of INR 1,300 crore to develop a new R&D and manufacturing facility in Bengaluru in 2020. This is an indication of Siemens' trust in South India's ability to develop high-complexity diagnostic solutions. Cepheid has expanded its domestic production facility in Karnataka to develop GeneXpert TB cartridges, which are being produced domestically and reducing dependence on imports for essential diagnostic reagents.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Karnataka, Tamil Nadu, Andhra Pradesh, Telangana, Kerala |

|

Major Growth Drivers

|

Life-sciences manufacturing cluster, IT sector healthcare spending, high surgical specialisation density, Bengaluru R&D investment |

|

Outlook

|

Strong growth anchored by Bengaluru diagnostics hub |

North India:

North India is influenced by Delhi NCR, which is home to large numbers of tertiary care hospitals, as well as the high population densities of UP, Rajasthan, Punjab, and Haryana. The NHM Integrated Disease Surveillance Programme has built upon integrated public sector diagnostic centers in UP and other states, thereby steadily increasing government-funded volumes of communicable disease testing. Delhi NCR represents a high-value, high-tech environment within private hospital and diagnostic chain groups.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Delhi NCR, Uttar Pradesh, Punjab, Haryana, Uttarakhand |

|

Major Growth Drivers

|

Tertiary-care hospital concentration, NHM public lab network expansion, high TB and dengue caseload, large salaried population |

|

Outlook

|

Robust growth via government health programme roll-out |

East and Northeast India:

East and Northeast India remains the most underpenetrated regional market, characterised by infrastructure gaps, a higher reliance on government health programmes, and lower private sector diagnostic density. However, targeted policy interventions are shifting the trajectory. Bharatnet broadband rollout to primary health centres is enabling digital laboratory connectivity and tele-diagnostics in remote areas.

|

Metric

|

Details

|

|---|---|

|

Key States

|

West Bengal, Odisha, Bihar, Assam, Jharkhand, Northeastern states |

|

Major Growth Drivers

|

Bharatnet connectivity, Day Care Cancer Centre expansion, NHM investment, rising financial inclusion and digital health literacy |

|

Outlook

|

Fastest catch-up growth from low penetration base |

Market Outlook 2026-2034

What is the future outlook of the India in vitro diagnostics market?

The India In Vitro Diagnostics market is expected to sustain steady revenue growth through 2034

The in vitro diagnostics market in India is expected to see sustained growth over the next decade and beyond, driven by factors like a growing population with a high median age, formalization of the healthcare industry, and rising access to diagnostic services in tier-2 and tier-3 cities. Ongoing expansion of domestic production capacity with support from the government’s PLI scheme, rising investments in diagnostics infrastructure by foreign players, and favourable regulatory environments set by CDSCO and ICMR will further solidify supply-side conditions in the in vitro diagnostics market in India. Sustained sales of high-end molecular and immunoassay solutions, laboratory informatics solutions enabled with artificial intelligence, and rising access to POCT solutions in the country’s primary care segment will collectively support India’s in vitro diagnostics market outlook through 2034, with demand drivers in the public and private sectors converging around rising testing needs and sophistication.

India In Vitro Diagnostics Market: Leading Key Players

The India in vitro diagnostics market has been influenced by the competitive dynamics of the industry, with the presence of both multinationals and the growing list of local industry players, whose cost-effective indigenous product development, PLI incentives-backed manufacturing scale, and widespread distribution network across tier 2 and tier 3 markets are collectively driving the quality and accessibility of diagnostic services.

| Company | Leading Brands | Highlights |

|---|---|---|

| Roche Diagnostics India Pvt Ltd | cobas series, Elecsys, ACCU-CHEK | Global diagnostics leader with a comprehensive portfolio; advanced molecular and immunoassay platforms deployed across top Indian hospital laboratory networks |

| Abbott Healthcare Pvt Ltd | ARCHITECT, Alinity, Afinion, i-STAT | Expanded collaboration with Maharashtra hospital networks; strong POCT and immunoassay franchise across public and private healthcare settings |

| Siemens Healthineers India | ADVIA, IMMULITE, MAGNETOM | Committed INR 1,300 crore for Bengaluru R&D and manufacturing hub (announced in 2020) |

Some other major key players in the India in vitro diagnostics market are Transasia Bio-Medicals Ltd, Beckman Coulter India, Thermo Fisher Scientific, bioMérieux, Bio-Rad Laboratories, Sysmex India, J. Mitra & Co., Agappe Diagnostics, Molbio Diagnostics, Mylab Discovery Solutions, and Becton Dickinson India.

Latest Development & News:

- In September 2025, India's regulatory authorities launched the IVD validation portal at the VRDL Conclave, providing a structured digital platform for manufacturers to register and validate diagnostic products for the Indian market. Simultaneously, ICMR and CDSCO released 39 standardised IVD evaluation protocols establishing performance benchmarks across test categories. The launch streamlines the approval pathway for new diagnostic assays entering India and strengthens the regulatory infrastructure underpinning domestic and imported IVD products.

- In April 2025, ABL Diagnostics entered an exclusive distribution agreement with Genient Tech to commercialise the DeepChek and UltraGene molecular assay platforms across Indian hospital networks, broadening access to validated molecular diagnostics for HIV drug-resistance testing and hepatitis profiling. In the same month, T&D Diagnostics commenced manufacturing of Starkwert fluorescence immunoassay diagnostic kits in India through a partnership with Noida-based Genenest, marking an import-substitution milestone in rapid quantitative POCT reagents.

- In March 2025, HaystackAnalytics launched the TB One whole-genome sequencing pre-processing kit at the ICMR Innovation Summit, enabling genomic drug-resistance profiling for tuberculosis directly from clinical specimens using next-generation sequencing. The launch represented a significant advance for precision tuberculosis management within India's national TB elimination programme framework, supporting clinicians with actionable pathogen genotyping data to guide drug-resistance treatment decisions.

India In Vitro Diagnostics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Test Types Covered | Clinical Chemistry, Molecular Diagnostics, Immunodiagnostics, Hematology, Others |

| Products Covered | Reagents and Kits, Instruments |

| Usabilities Covered | Disposable IVD Devices, Reusable IVD Devices |

| Applications Covered | Infectious Disease, Diabetes, Cancer/Oncology, Cardiology, Autoimmune Disease, Nephrology, Others |

| End Users Covered | Hospitals Laboratories, Clinical Laboratories, Point-of-Care Testing Centers, Academic Institutes, Patients, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India In Vitro Diagnostics Market Report

The India in vitro diagnostics market was valued at USD 5.6 Billion in 2025.

The India in vitro diagnostics market is anticipated to reach a value of USD 10.6 Billion by 2034.

Clinical chemistry dominates the market with a share of 28.4% in 2025, driven by the widespread deployment of automated biochemistry analysers for routine glucose, renal, hepatic, and lipid panel testing in hospital and commercial diagnostic laboratory settings across India.

Reagents and kits dominate the market with a share of 63.2% in 2025, driven by the consumable economics of diagnostics, high repeat-purchase frequency generated by India's large installed instrument base, and growing domestic reagent manufacturing capacity under PLI scheme incentives.

Disposable IVD devices dominate the market with a share of 58.7% in 2025, as single-use consumables are preferred across all care settings for infection-control advantages, regulatory compliance, and operational simplicity in both high-throughput hospital labs and point-of-care testing environments.

Infectious disease dominates the market with a share of 24.6% in 2025, underpinned by India's large and persistent communicable disease burden, including tuberculosis, malaria, dengue, and HIV, supported by structured national health programme testing mandates that generate consistent diagnostic test volumes.

Hospitals laboratories dominate the market with a share of 35.1% in 2025, because in-house hospital labs handle emergency, inpatient, and outpatient diagnostic workloads that cannot be efficiently outsourced. Growing hospital infrastructure and PM-JAY-funded patient volumes reinforce this segment's structural leadership.

West and Central India dominates the market with a share of 31.8% in 2025, because of the region's high concentration of private hospital networks, pharmaceutical manufacturing infrastructure, and the commercial density of Maharashtra and Gujarat, which together generate the highest per-capita diagnostic test volumes in India.

Key growth factors include India's dual infectious and non-communicable disease burden, the Union Budget 2026-27's 10% increase in health ministry allocation, PLI-linked domestic reagent and instrument manufacturing incentives, expansion of molecular and POCT platforms into tier-2 cities, and regulatory modernisation through CDSCO's standardised IVD validation protocols.

Some of the major players in the India in vitro diagnostics market are Roche Diagnostics India Pvt Ltd, Abbott Healthcare Pvt Ltd, Siemens Healthineers India, Transasia Bio-Medicals Ltd, Beckman Coulter India, Thermo Fisher Scientific, bioMérieux, Bio-Rad Laboratories, Sysmex India, J. Mitra & Co., Agappe Diagnostics, Molbio Diagnostics, Mylab Discovery Solutions, and Becton Dickinson India.

There are several challenges confronting the India in vitro diagnostics market. The regulatory landscape remains fragmented due to inconsistent state-level implementation of the Clinical Establishments Act and complex CDSCO validation requirements for new products. High dependence on imported high-value diagnostic instruments exposes the sector to currency and supply-chain risks. A persistent shortage of skilled laboratory technicians and limited reimbursement coverage for advanced tests under public health schemes further constrain market development.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)