India In Vitro Fertilization (IVF) Market Size, Share, Trends and Forecast by Product, Procedure Type, Cycle Type, End User, and Region, 2026-2034

India In Vitro Fertilization (IVF) Market Summary:

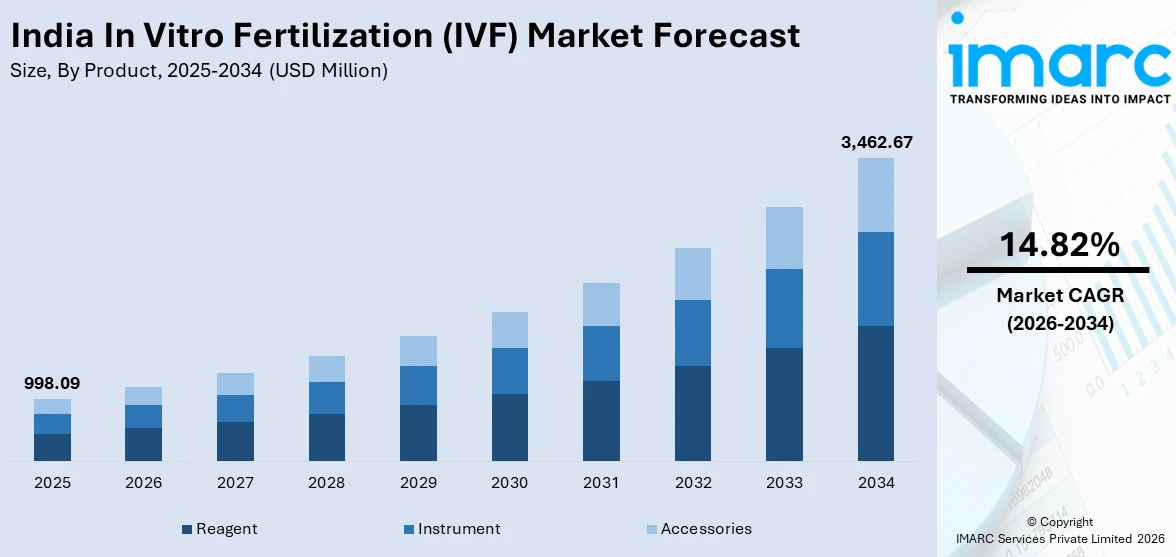

The India in vitro fertilization (IVF) market size was valued at USD 998.09 Million in 2025 and is projected to reach USD 3,462.67 Million by 2034, growing at a compound annual growth rate of 14.82% from 2026-2034.

The India in vitro fertilization (IVF) market is experiencing significant growth driven by rising infertility rates, increasing awareness about assisted reproductive technologies, and evolving societal attitudes toward fertility treatments. The growing urbanization, delayed marriages, sedentary lifestyles, and environmental factors are contributing to escalating reproductive health challenges. Additionally, rapid technological advancements in embryo selection and cryopreservation, expanding healthcare infrastructure into tier-2 and tier-3 cities, supportive government regulatory frameworks, and the emergence of India as a leading fertility tourism destination are collectively reshaping the competitive landscape and creating substantial opportunities for stakeholders.

Key Takeaways and Insights:

- By Product: Reagent dominates the market with a share of 48% in 2025, driven by the critical role of culture media, cryopreservation solutions, and sperm processing media in enabling successful embryo development and improving clinical outcomes across fertility clinics nationwide.

- By Procedure Type: Fresh non-donor leads the market with a share of 40% in 2025, owing to higher success rates associated with fresh embryo transfer cycles and the growing patient preference for utilizing autologous gametes in treatment.

- By Cycle Type: Conventional IVF represents the largest segment with a market share of 45% in 2025, reflecting widespread clinical adoption, established treatment protocols, and cost-effectiveness compared to advanced techniques, making it the preferred choice for first-time fertility patients.

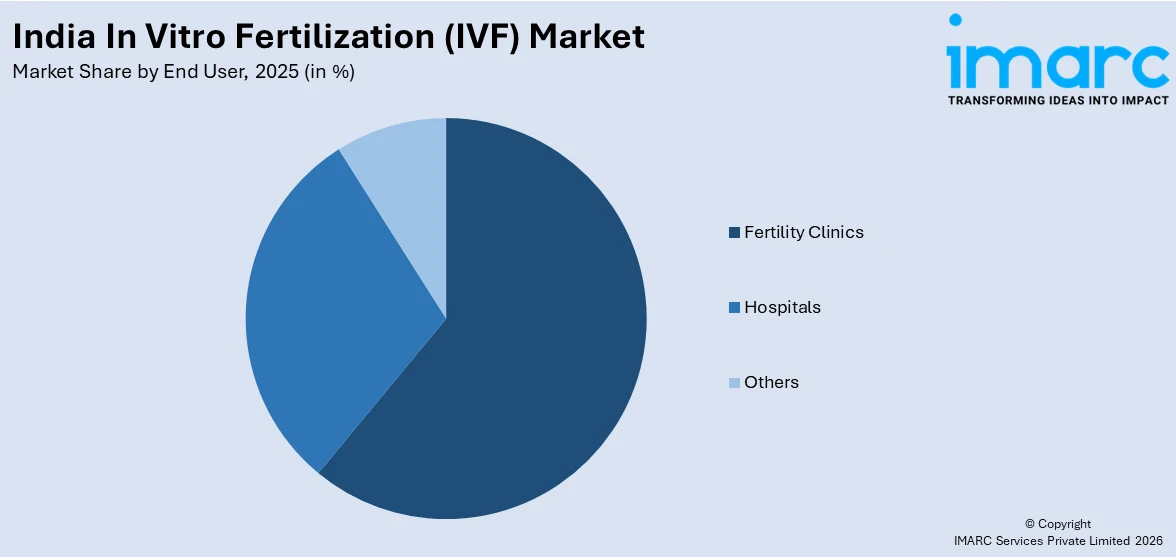

- By End User: Fertility clinics dominates the market with a share of 61% in 2025, supported by specialized infrastructure, dedicated embryology expertise, patient-centric care models, and the rapid expansion of organized fertility chains across metropolitan and emerging cities.

- By Region: South India leads the market with a share of 35% in 2025, due to advanced healthcare infrastructure, high concentration of fertility clinics in states like Tamil Nadu, Karnataka, and Kerala, and greater awareness about reproductive health.

- Key Players: The India IVF market exhibits intense competitive dynamics, with established fertility chains expanding through acquisitions, technology partnerships, and geographic penetration into underserved regions while investing in artificial intelligence and precision medicine capabilities.

To get more information on this market Request Sample

The India IVF market is driven by rising infertility prevalence, changing lifestyle patterns, and increasing demand for advanced reproductive healthcare. Delayed parenthood among urban professionals, combined with higher incidence of reproductive disorders, such as polycystic ovary syndrome (PCOS) and endometriosis, is expanding the need for assisted fertility treatments. The growing awareness and improving social acceptance of IVF are encouraging more couples to seek clinical intervention. Furthermore, technological advancements in embryo culture, cryopreservation, genetic screening, and laboratory automation are enhancing success rates and boosting patient confidence. Digital health tools, including teleconsultations and decision-support platforms, are improving early engagement and treatment planning. Rapid expansion of private fertility clinics is improving access and strengthening healthcare infrastructure. For instance, in 2025, Birla Fertility & IVF announced the launch of its first fertility center in Jalandhar, marking its 51st clinic nationwide and second in Punjab. The new center aimed to expand access to advanced fertility treatments like IVF, ICSI, IUI, and fertility preservation, addressing rising lifestyle-related fertility challenges, such as PCOS, diabetes, and hypertension in the region.

India In Vitro Fertilization (IVF) Market Trends:

Growth of Data-Driven Patient Engagement Tools

Digital decision-support tools are emerging as a significant trend in India’s IVF market by enhancing patient awareness, transparency, and early engagement. Fertility clinics are increasingly leveraging online platforms to provide preliminary assessments that help individuals better understand their reproductive health before scheduling consultations. In 2025, Indira IVF launched a personalized IVF Success Calculator that evaluated medical inputs, including AMH levels and sperm parameters, to estimate projected success rates across treatment cycles. Such technology-driven tools empower patients with data-based insights, improve confidence in clinical pathways, encourage proactive consultation, and ultimately support broader participation in fertility treatment services across India.

Expansion of Home-Based and Hybrid IVF Care Models

The adoption of hybrid and home-enabled fertility treatment models is transforming service delivery within India IVF market. Patients are increasingly prioritizing convenience, discretion, and fewer hospital visits, particularly among working professionals balancing demanding schedules. In 2025, Seeds of Innocens introduced India’s first fully integrated at-home IVF platform, combining teleconsultations, app-based treatment tracking, home delivery of hormone injections, and limited in-clinic visits under medical supervision. This approach represents a broader transition toward decentralized reproductive care, extending access beyond traditional hospital settings while preserving clinical oversight. Such flexible models are expanding patient reach and enhancing overall treatment accessibility across India.

Introduction of Structured IVF Financing and Risk-Sharing Solutions

Innovative financing mechanisms are becoming an important trend supporting IVF market growth in India, as high treatment costs have traditionally restricted access for many couples. Insurance-linked and installment-based payment solutions are increasingly being introduced to improve affordability and reduce financial stress. For instance, in 2025, CarePay launched HopeGuard, India’s first integrated IVF insurance and no-cost EMI solution to improve affordability in fertility care. The offering covered up to three IVF cycles and provided a refund if treatment is unsuccessful, giving patients greater financial confidence. By combining instant insurance activation with flexible payment options, HopeGuard also helped clinics expand access while reducing financing risk. By lowering economic barriers and sharing risk, these solutions are strengthening long-term market growth.

Market Outlook 2026-2034:

The India in vitro fertilization (IVF) market demonstrates notable growth potential throughout the forecast period, underpinned by escalating infertility prevalence, technological innovation, and expanding healthcare infrastructure. The market generated a revenue of USD 998.09 Million in 2025 and is projected to reach a revenue of USD 3,462.67 Million by 2034, growing at a compound annual growth rate of 14.82% from 2026-2034. Increasing adoption of AI-enabled diagnostics, the growing acceptance of fertility treatments across socioeconomic segments, regulatory standardization, rising medical tourism inflows, and aggressive expansion by organized fertility chains into smaller cities are expected to sustain robust revenue growth across the forecast horizon.

India In Vitro Fertilization (IVF) Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product |

Reagent |

48% |

|

Procedure Type |

Fresh Non-donor |

40% |

|

Cycle Type |

Conventional IVF |

45% |

|

End User |

Fertility Clinics |

61% |

|

Region |

South India |

35% |

Product Insights:

- Reagent

- Cryopreservation Media

- Embryo Culture Media

- Ovum Processing Media

- Sperm Processing Media

- Instrument

- Imaging Systems

- Incubators

- Cryosystems

- IVF Cabinet

- Ovum Aspiration Pump

- Sperm Separation Systems

- Micromanipulator Systems

- Others

- Accessories

Reagent leads with a market share of 48% of the total India in vitro fertilization (IVF) market in 2025.

Reagent accounts for the majority of the market share attributed to its essential role in every stage of the IVF process, ranging from fertilization to embryo development. This includes culture media, sperm preparation solutions, cryopreservation reagents, and buffers that support optimal laboratory conditions. Since IVF is highly dependent on controlled environments, the quality and consistency of reagents directly influence treatment outcomes. With the increasing number of IVF cycles performed across India, demand for reliable and specialized reagent continues to rise steadily among fertility clinics and IVF laboratories.

Another key driver is the growing adoption of advanced assisted reproductive technologies, which require a wider range of specialized reagents for procedures, such as ICSI, embryo freezing, and genetic testing. Fertility centers also prioritize premium reagents to improve success rates and maintain accreditation standards. Continuous innovation by manufacturers, along with rising investments in IVF infrastructure, further strengthens the market for reagent. Its recurring usage in each cycle, unlike durable equipment, ensures consistent usage, making reagent the dominant segment in the industry.

Procedure Type Insights:

- Fresh Donor

- Frozen Donor

- Fresh Non-donor

- Frozen Non-donor

Fresh non-donor dominates with a market share of 40% of the total India in vitro fertilization (IVF) market in 2025.

Fresh non-donor represents the largest segment because of strong patient preference for using their own gametes during treatment. Many couples prioritize a biological connection to the child, making fresh non-donor cycles the first option recommended by fertility specialists. This approach is commonly advised for women with adequate ovarian reserve and favorable health conditions. Since the eggs and sperm are retrieved and fertilized within the same cycle, it aligns well with standard IVF protocols followed across leading fertility centers in India.

Another factor supporting its dominance is the perception of higher success rates in selected patient groups when fresh embryos are transferred without freezing. The procedure also avoids additional costs associated with donor compensation and long-term cryostorage. Cultural and social considerations in India further encourage couples to pursue non-donor options before exploring donor-based alternatives. With improved stimulation protocols and laboratory capabilities, fresh non-donor cycles continue to deliver reliable outcomes, reinforcing their position as the leading procedure type in the market.

Cycle Type Insights:

- Conventional IVF

- IVF with ICSI

- IVF with Donor Eggs

Conventional IVF exhibits a clear dominance with a 45% share of the total India in vitro fertilization (IVF) market in 2025.

Conventional IVF holds the biggest market share driven by its long-standing clinical acceptance and suitability for a broad range of infertility cases. It remains a preferred first-line treatment for couples facing tubal blockage, ovulatory disorders, or unexplained infertility. The procedure is widely available across fertility centers and is supported by experienced specialists familiar with standardized protocols. Compared to more complex techniques, conventional IVF is relatively cost-effective, making it accessible to a larger patient base across urban and semi-urban regions of India.

Another reason for its dominance is the consistent success rates achieved through improved laboratory practices and embryo culture techniques. Many fertility clinics continue to recommend conventional IVF before moving to advanced procedures like ICSI, unless medically necessary. The process involves fewer additional interventions, which helps manage overall treatment costs for patients. The growing awareness, increasing infertility rates, and trust built over decades further sustain its demand. These factors collectively position conventional IVF as the leading segment within India’s expanding IVF treatment landscape.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Fertility Clinics

- Hospitals

- Others

Fertility clinics lead with a market share of 61% of the total India in vitro fertilization (IVF) market in 2025.

Fertility clinics dominate the market owing to their specialized focus on reproductive medicine, advanced diagnostics, and laboratory-intensive assisted conception procedures. Unlike general hospitals, these centers are equipped with dedicated IVF labs, trained embryologists, and personalized treatment protocols that enhance clinical outcomes and patient confidence. Clinics also provide integrated services like counseling, hormone therapy, cryopreservation, and genetic screening, making them the preferred choice for structured fertility care. This dominance is reinforced by rapid network expansion, as in 2025 Birla Fertility & IVF committed ₹500 crore to double its India presence from 50 to 100 centers while also planning entry into ASEAN and West Asia. The company prioritized tier-2 and tier-3 cities through a hub-and-spoke model to improve access to fertility care amid rising infertility rates. This strategy supported its ambition to become a leading global reproductive health provider while addressing India’s declining fertility trends.

Another factor driving the dominance of fertility clinics is their patient-centric approach and operational flexibility. These centers typically provide shorter waiting times, customized treatment plans, and transparent pricing packages tailored to different budgets. Strong word-of-mouth referrals and higher success rate visibility further strengthen their market position. In addition, fertility clinics actively invest in advanced technologies, such as ICSI, blastocyst culture, and embryo freezing, helping them remain competitive. This combination of specialization, accessibility, and technological capability positions fertility clinics as the leading segment in the market.

Regional Insights:

- North India

- West and Central India

- South India

- East India

South India dominates with a market share of 35% of the total India in vitro fertilization (IVF) market in 2025.

South India leads the market due to its strong concentration of well-established fertility clinics, advanced medical infrastructure, and high awareness among patients. Cities like Chennai, Bengaluru, and Hyderabad are becoming major hubs for reproductive healthcare, attracting couples from across the country. The region also benefits from the presence of skilled embryologists, experienced specialists, and early adoption of newer IVF technologies, which improves treatment success rates and builds trust among patients seeking reliable fertility solutions.

Another key reason South India dominates the market is its strong healthcare investment ecosystem and the growing medical tourism appeal. The region benefits from well-developed private hospitals, specialized fertility centers, and comparatively affordable treatment packages, attracting both domestic and international patients. This expansion is evident in 2025, when Birla Fertility & IVF opened a new center in Hyderabad’s Gachibowli area. The facility provided a full range of fertility services, including IVF, ICSI, egg and sperm preservation, and genetic testing, supported by advanced labs and global clinical protocols. The company highlighted its focus on patient-first care with strong emphasis on transparent counselling and clear cost communication to build trust.

Market Dynamics:

Growth Drivers:

Why is the India In Vitro Fertilization (IVF) Market Growing?

Rise of Venture Capital–Backed Fertility Platform Models

Investors are increasingly backing structured, technology-enabled fertility platforms that aim to standardize clinical quality while supporting independent specialists. This trend reflects the growing confidence in scalable and professionally managed IVF networks. For example, in 2025, Bessemer Venture Partners invested ₹125 crore in Series A funding to support the launch of Pluro Fertility and IVF at a ₹1,000 crore valuation. The platform followed a clinical partnership model, assisting doctors with operations, compliance, and technology while offering equity participation. Such investment-led expansion is strengthening organized growth, improving service consistency, and accelerating consolidation within India’s evolving fertility care ecosystem.

Increasing Demand from Tier-Two and Tier-Three City Populations

The IVF market in India is expanding beyond metropolitan centers as demand rises in tier-two and tier-three cities. Improved healthcare awareness, rising income levels, and better access to specialized fertility services are encouraging more couples in smaller urban regions to seek assisted reproduction. Fertility clinic networks are increasingly targeting these markets through new centers and outreach initiatives. For instance, in 2025, Nova IVF Fertility inaugurated its 100th center in Jammu, marking a major expansion milestone across India. The launch strengthened access to fertility care in tier 2 and tier 3 cities, addressing declining fertility rates and rising reproductive health challenges nationwide. As geographic penetration improves, the patient base is widening significantly. This shift toward broader regional adoption is becoming a crucial factor impelling the market growth.

Improved Patient Education and Awareness Through Fertility Campaigns

Awareness initiatives by healthcare providers, fertility associations, and public health organizations are improving patient understanding of infertility causes and available treatment options. Better education encourages earlier medical consultation and reduces delays in seeking fertility care. Counseling services and awareness campaigns are also helping normalize assisted reproduction across diverse communities. In 2025, Apollo Fertility launched its #GuessTheIVFBaby campaign to challenge misconceptions and reduce stigma around IVF and assisted reproduction. Timed with World IVF Day, the initiative combined digital outreach and on-ground activities across 12 Indian cities, reaching audiences through Apollo’s 22 centers nationwide. The campaign also promoted early fertility screening, awareness about egg freezing and PCOD, and encourages open, science-based conversations to support individuals and couples on their parenthood journey.

Market Restraints:

What Challenges the India In Vitro Fertilization (IVF) Market is Facing?

High Treatment Costs Limiting Access for Middle and Low-Income Populations

The substantial cost of IVF treatments remains a significant barrier constraining broader adoption, particularly among middle and low-income couples who constitute the majority of India’s population. Multiple treatment cycles, expensive medications, diagnostic procedures, and limited insurance coverage create cumulative financial burdens that many families cannot sustain. The absence of widespread employer-sponsored fertility benefits and inadequate government subsidization further restrict market penetration among economically vulnerable segments.

Cultural Stigma and Awareness Gaps Impeding Treatment-Seeking Behavior

Deep-rooted cultural stigma surrounding infertility continues to impede market development across India, particularly in rural and semi-urban areas. Social taboos around discussing reproductive health, misconceptions about IVF procedures, and fear of community judgement discourage open dialogue and delay help-seeking behavior. These awareness gaps result in significant underreporting of infertility cases and delayed treatment initiation, reducing the overall addressable patient population.

Shortage of Trained Fertility Specialists and Embryologists in Emerging Regions

The limited availability of trained reproductive medicine specialists, embryologists, and andrologists, particularly outside metropolitan cities, constrains the expansion of quality fertility services into underserved regions. The specialized nature of IVF procedures demands extensive clinical training and laboratory expertise that require years of dedicated education, creating a supply-demand gap that limits the geographic reach of advanced fertility care nationwide.

Competitive Landscape:

The India IVF market exhibits increasingly intense competitive dynamics characterized by the presence of organized fertility chains, standalone specialized clinics, and multi-specialty hospital groups competing across geographic segments and service tiers. Market dynamics reflect strategic positioning through aggressive network expansion, technology-driven differentiation via artificial intelligence and genetic testing integration, acquisitions of regional fertility providers, and investment in brand marketing to address cultural barriers. The competitive landscape is further shaped by emerging digital health platforms offering remote fertility consultations, the growing investor interest evidenced by significant private equity and venture capital inflows, and increasing emphasis on standardized clinical protocols to improve treatment outcomes and patient experience across metropolitan and tier-2 markets.

Recent Developments:

- January 2026: Aksigen IVF launched India’s first immersive IVF Knowledge Centre in Mumbai (Andheri East) to improve fertility awareness and patient education. The Bharat Daftary Knowledge Centre uses interactive zones, digital tools, and guided expert walkthroughs to simplify IVF science, reduce anxiety, and address myths around reproductive health. The initiative aims to support informed decision-making while strengthening transparency, trust, and doctor–patient communication in fertility care.

- December 2025: Intas Pharmaceuticals announced an exclusive partnership with IntegriMedical to introduce India’s first needle-free injection system (N-FIS) for IVF and gynecology treatments. The technology delivered medication via a high-pressure jet stream through a micro-orifice in the skin, eliminating needles and reducing pain, anxiety, and tissue trauma. The collaboration aimed to enhance patient comfort and compliance.

India In Vitro Fertilization (IVF) Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered |

|

| Procedure Types Covered | Fresh Donor, Frozen Donor, Fresh Non-donor, Frozen Non-donor |

| Cycle Types Covered | Conventional IVF, IVF with ICSI, IVF with Donor Eggs |

| End Users Covered | Fertility Clinics, Hospitals, Others |

| Regions Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India In Vitro Fertilization (IVF) Market Report

The India in vitro fertilization (IVF) market size was valued at USD 998.09 Million in 2025.

The India in vitro fertilization (IVF) market is expected to grow at a compound annual growth rate of 14.82% from 2026-2034 to reach USD 3,462.67 Million by 2034.

Reagent dominates the market with 48% revenue share in 2025, driven by the critical role of culture media, cryopreservation solutions, and sperm processing media in enabling successful embryo development and improving clinical outcomes across fertility clinics nationwide.

Key factors driving the India in vitro fertilization (IVF) market include the availability of innovative financing models that are improving affordability and reducing financial uncertainty. In 2025, CarePay launched HopeGuard, offering insurance coverage for up to three IVF cycles with a refund for unsuccessful treatment, alongside no-cost EMI options, expanding access and boosting patient confidence.

Major challenges include high treatment costs limiting access for middle and low-income populations, cultural stigma and awareness gaps impeding treatment-seeking behavior, shortage of trained fertility specialists in emerging regions, and limited insurance coverage for fertility procedures.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)