India Industrial Automation Market Size, Share, Trends and Forecast by Component, Industry, Vertical, and Region, 2026-2034

India Industrial Automation Market Size, Share, Trends & Forecast (2026-2034)

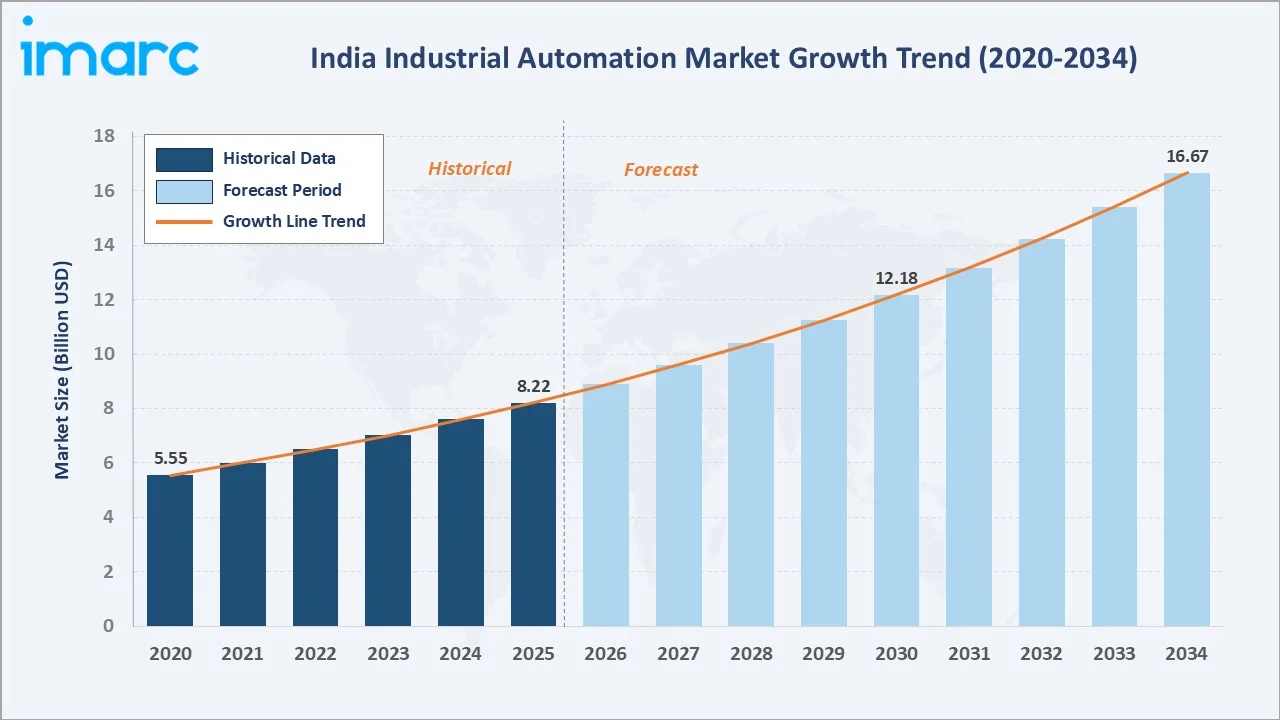

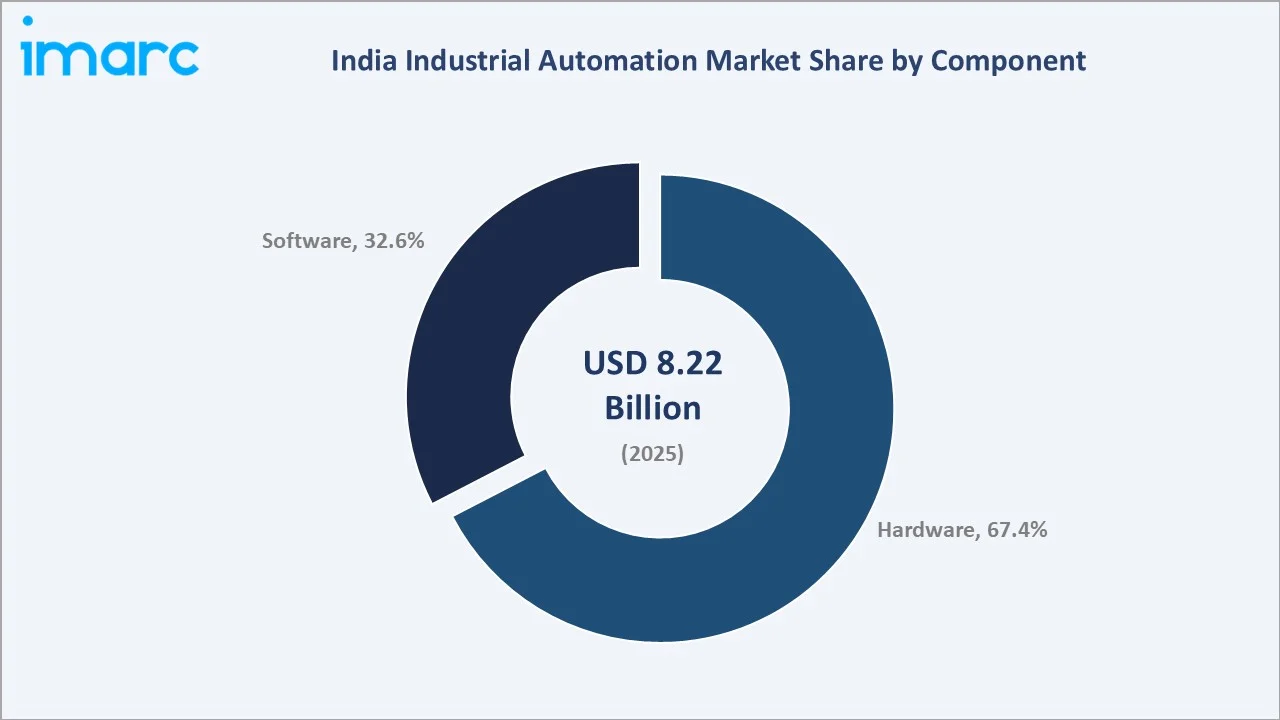

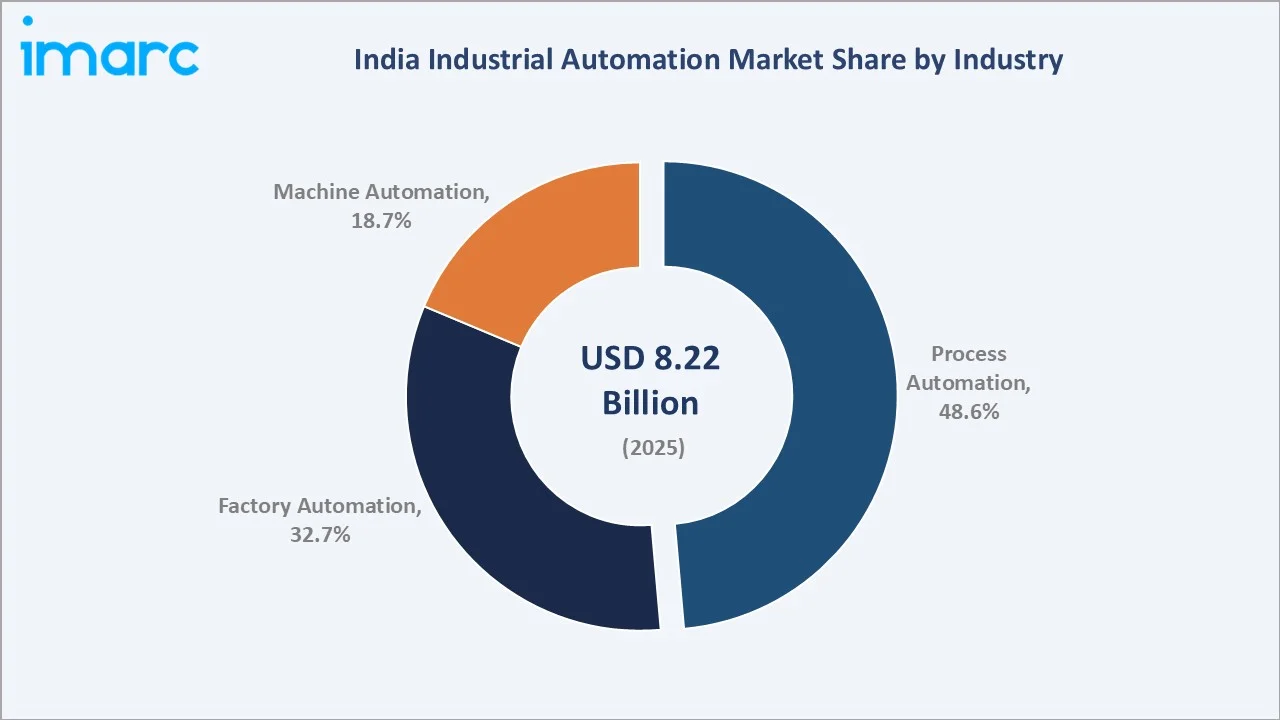

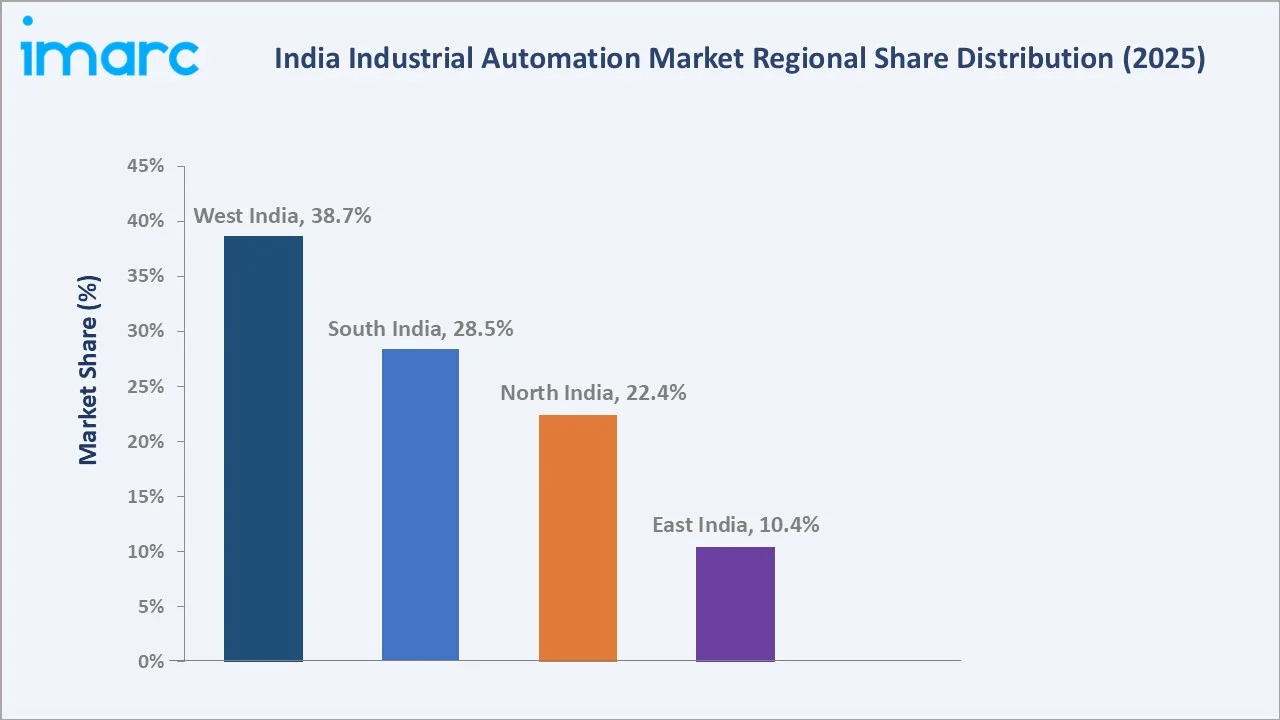

The India industrial automation market was valued at USD 8.22 Billion in 2025 and is projected to reach USD 16.67 Billion by 2034, exhibiting a CAGR of 8.17% during 2026-2034. India's manufacturing Purchasing Managers' Index (PMI) rose to 59.2 in October 2025, reflecting strong order growth, faster output, and sustained job gains - factors that, together with Make in India momentum and rising labor-cost-driven plant modernization, are the primary drivers shaping the market growth.

Hardware leads the component segment at 67.4%, process automation dominates industry at 48.6%, and West India commands 38.7% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.22 Billion |

|

Forecast Market Size (2034) |

USD 16.67 Billion |

|

CAGR (2026-2034) |

8.17% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West India (38.7%, 2025) |

|

Fastest Growing Region |

South India (28.5%, 2025) |

|

Leading Component |

Hardware (67.4%, 2025) |

|

Leading Industry |

Process Automation (48.6%, 2025) |

The India industrial automation market expanded from USD 5.55 Billion in 2020 to USD 8.22 Billion in 2025, supported by accelerating Industry 4.0 adoption, government-backed manufacturing initiatives, and rapid digital retrofits across mid-tier plants. Anchored at USD 12.18 Billion in 2030, the path to USD 16.67 Billion by 2034 is reinforced by sustained capital expenditure in automotive, electronics, pharmaceuticals, and food processing.

To get more information on this market, Request Sample

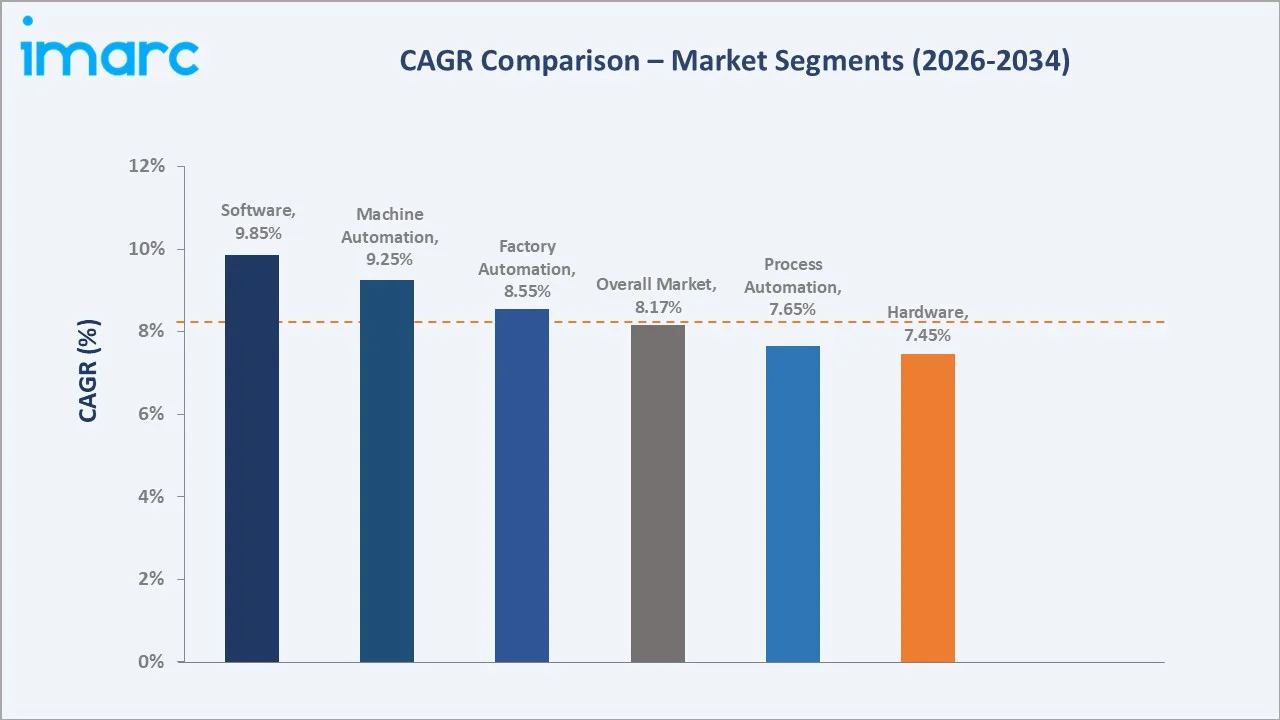

CAGR trajectories across component and industry sub-segments show software and machine automation expanding faster than the overall 8.17% market CAGR, driven by cloud-native MES adoption, edge analytics, and AI-led predictive maintenance.

Executive Summary

The India industrial automation market is on a strong growth path from USD 5.55 Billion in 2020 to USD 16.67 Billion by 2034. Automation has moved beyond capacity-led greenfield projects to modular brownfield retrofits with payback windows under two years. Falling sensor and controller costs, combined with rising labor costs and quality-led export commitments, are pushing manufacturers toward integrated control architectures. Government-backed Make in India and PLI schemes continue to anchor long-term demand.

Hardware dominates the component segment at 67.4% in 2025, supported by sustained shipments of programmable logic controllers, drives, sensors, and industrial robots. Process automation leads industry at 48.6%, fueled by demand from refining, chemicals, pharmaceuticals, and food and beverage (F&B) plants. West India commands 38.7% regional share, led by Maharashtra and Gujarat through dense automotive, chemical, and pharma clusters. India ranked third globally in AI competitiveness in Stanford University's 2025 Global AI Vibrancy Ranking, accelerating the convergence of industrial AI with traditional automation across the manufacturing sector.

Key Market Insights

|

Insight |

Data |

|

Leading Component |

Hardware - 67.4% share (2025) |

|

Second Component |

Software - 32.6% share (2025) |

|

Leading Industry |

Process Automation - 48.6% share (2025) |

|

Second Industry |

Factory Automation - 32.7% share (2025) |

|

Leading Region |

West India - 38.7% share (2025) |

|

Fastest Growing Region |

South India - 28.5% share (2025) |

|

Top Companies |

Siemens, ABB, Schneider Electric, Rockwell Automation, Honeywell International Inc. |

Key Analytical Observations Expanding on the Data Above:

- Hardware dominance at 67.4% is anchored by deep installed bases of PLCs, HMIs, drives, motion controllers, and field instruments across automotive, metals, and process plants. Continued investment in Tier-2 industrial clusters is sustaining hardware-led replacement cycles.

- Software at 32.6% is the faster-growing component slice, supported by cloud-based MES, SCADA modernization, asset performance management, and AI-enabled analytics. Open and software-defined automation architectures are reducing lock-in and accelerating subscription-led adoption.

- Process automation leadership at 48.6% reflects the depth of refining, chemicals, fertilizers, pharmaceuticals, and F&B assets across India. Distributed control systems, advanced process control, and safety instrumented systems remain core capital priorities for these plants.

- Factory automation at 32.7% is being reshaped by discrete-manufacturing modernization in automotive, electronics, and consumer durables. Robotics, machine vision, and AGVs are increasingly bundled into modular retrofit packages by integrators serving mid-tier plants. As per IMARC Group, the India robotics market size was valued at USD 1.98 Billion in 2025.

- West India at 38.7% leads on the strength of Maharashtra and Gujarat's automotive, chemicals, pharma, and ports clusters. Strong industrial corridor development and export-oriented manufacturing investments continue to reinforce automation demand across the region.

India Industrial Automation Market Overview

Industrial automation refers to the use of control systems, sensors, robotics, and software to operate industrial equipment with limited human intervention. Typical Indian deployments span PLCs, DCS, SCADA, HMIs, drives, motion control, machine vision, robots, and manufacturing execution systems.

The Indian ecosystem brings together component manufacturers, software platform providers, system integrators, distributors, end-use industries, service partners, regulatory bodies, and R&D hubs. Together, they enable connected operations across automotive, electronics, pharma, F&B, metals, energy, and water utilities.

Market Dynamics

To evaluate market opportunities, Request Sample

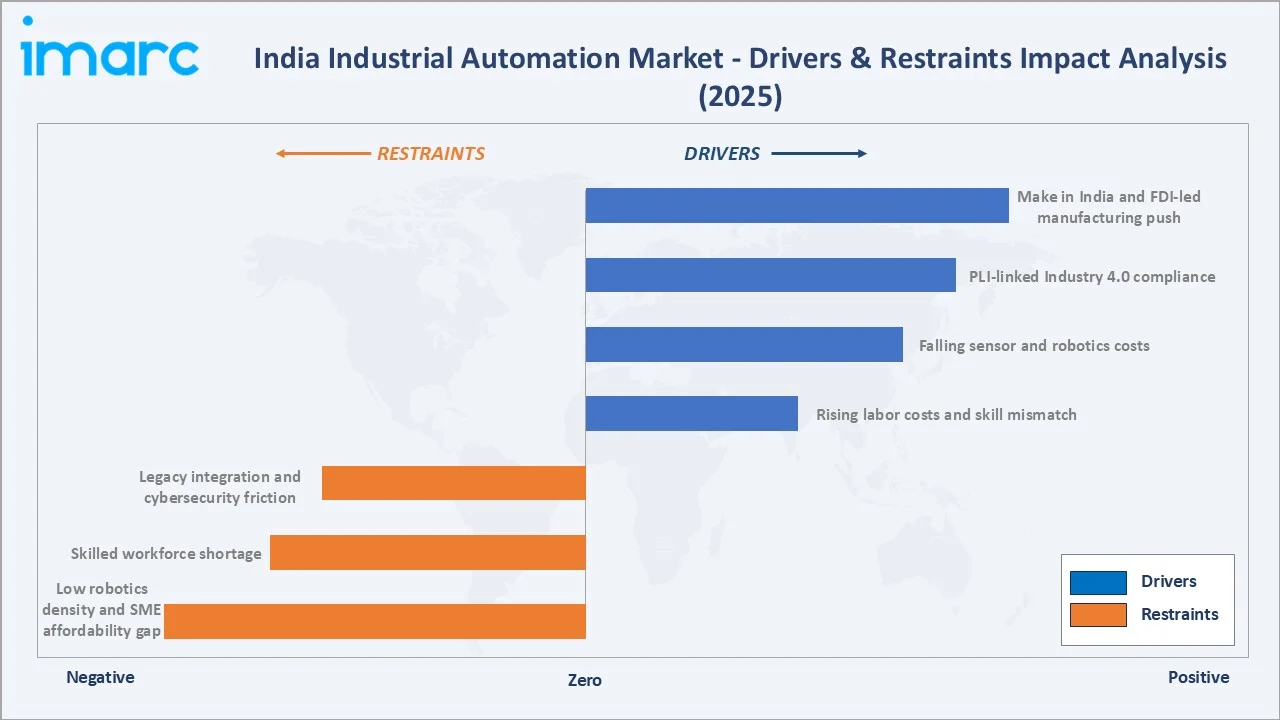

Market Drivers

- Make in India and FDI-led manufacturing push: In 2025, FDI in India's manufacturing industry attained INR 14,45,781 Crore (USD 165.1 Billion), a 69% rise over the past decade, channeling fresh capacity into automotive, electronics, and pharma plants - all of which specify advanced controllers and robots as baseline equipment.

- PLI-linked Industry 4.0 compliance: PLI disbursements are tied to real-time output and efficiency metrics, pushing beneficiaries to install advanced controllers, vision systems, and plant-wide software for compliance and incentive unlocking.

- Falling sensor and robotics costs: Lower component prices and modular automation kits are bringing payback windows under two years, broadening adoption across mid-sized and small enterprises in Tier-2 industrial clusters.

- Rising labor costs and skill mismatch: Wage inflation, attrition in industrial clusters, and stricter quality standards for export markets are nudging manufacturers toward higher line automation, machine vision inspection, and cobot deployment.

Market Restraints

- Low robotics density and SME affordability gap: Industrial automation adoption remains uneven across India's manufacturing base, with many SMEs delaying automation investments due to high upfront costs and limited access to financing. Lower robotics penetration in labor-intensive sectors continues to restrict large-scale deployment beyond major industrial hubs.

- Skilled workforce shortage: A persistent shortfall of plant engineers, integrators, and OT cybersecurity specialists is slowing project execution and lengthening commissioning timelines, particularly in Tier-2 and Tier-3 cities.

- Legacy integration and cybersecurity friction: Mixed-vintage installed bases, proprietary protocols, and rising OT-security incidents add cost and complexity to brownfield retrofits, especially in process industries with long asset lives.

Market Opportunities

- MSME retrofit wave: Affordable IIoT kits, edge controllers, and cobots are unlocking automation for India's MSME base, with secondary cities emerging as integration hotbeds backed by lower land costs and growing mechatronics talent pools.

- Semiconductor and electronics manufacturing scale-up: Approval of new fabs and ATMP units under the India Semiconductor Mission is creating sustained demand for cleanroom automation, machine vision, and advanced process control systems.

- Software-defined and open automation: Growing adoption of vendor-neutral and open automation platforms is enabling more flexible system integration, faster upgrades, and improved interoperability across industrial environments.

Market Challenges

- Fragmented system integrator quality: Wide variation in integrator capability across regions creates execution risk and rework cost for end users, particularly in complex multi-vendor brownfield environments.

- Capital sensitivity in Tier-3 supplier base: Smaller component suppliers operate on thin margins and face challenges in financing automation upgrades, even where productivity gains are clearly demonstrable.

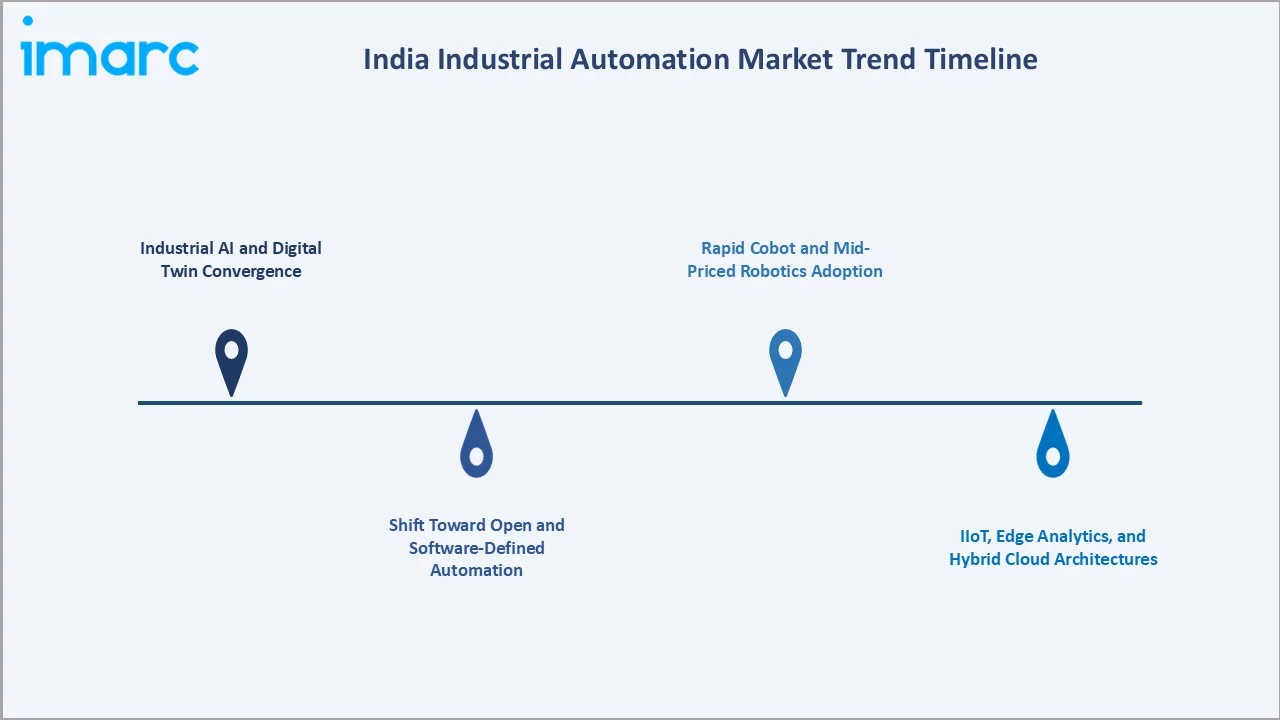

Emerging Market Trends

1. Industrial AI and Digital Twin Convergence

AI-enabled simulation, predictive maintenance, and software-defined production are moving from pilots to live deployments across automotive, semiconductor, and energy customers. In March 2026, Siemens announced an expanded partnership with NVIDIA leveraging more than 10,000 software and AI experts based in India to build an industrial AI operating system, signaling deep localization of high-end automation R&D in the country.

2. Shift Toward Open and Software-Defined Automation

Manufacturers are moving away from rigid, proprietary stacks toward vendor-neutral, plug-and-play architectures. This reduces lifecycle engineering cost, simplifies multi-vendor integration, and enables faster system upgrades, while supporting predictive maintenance and stronger cybersecurity baselines.

3. Rapid Cobot and Mid-Priced Robotics Adoption

Collaborative robots and mid-priced six-axis arms are gaining ground in electronics, packaging, and consumer durables. Their lower footprint, simpler programming, and faster integration timelines are making them attractive for SMEs that previously lacked the budget for full-scale industrial robots.

4. IIoT, Edge Analytics, and Hybrid Cloud Architectures

Hybrid architectures are keeping latency-sensitive control loops on-premise while pushing non-critical telemetry to the cloud for real-time visibility. Edge gateways, time-series databases, and asset performance platforms are becoming standard add-ons in retrofit projects across process and discrete sectors.

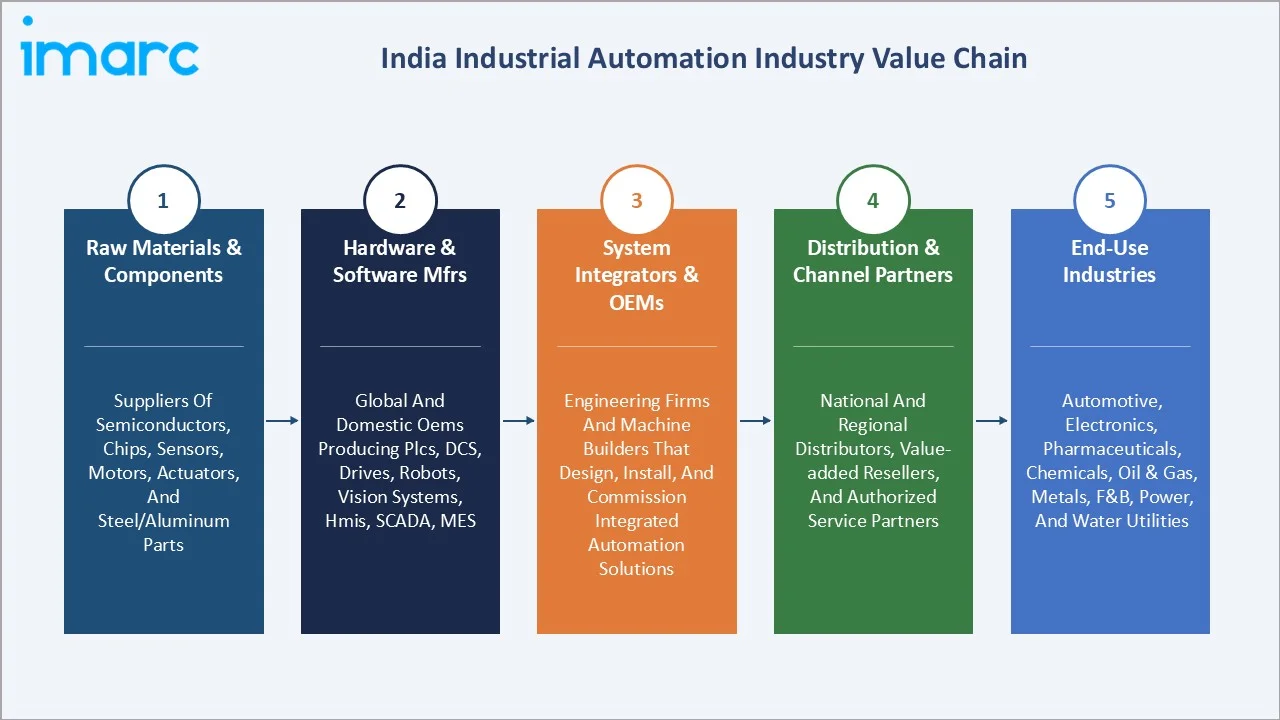

Industry Value Chain Analysis

The India industrial automation value chain spans five core stages from raw materials and components through end-use industries. Hardware manufacturing and software platform delivery capture the highest value-add, while integrators and channel partners drive downstream conversion in this regulated and engineering-intensive category.

|

Stage |

Key Players / Examples |

|

Raw Materials & Components |

Suppliers of semiconductors, electronic chips, precision components, sensors, motors, actuators, and steel and aluminum parts feeding the automation hardware base |

|

Hardware & Software Manufacturers |

Global and domestic OEMs producing PLCs, DCS, drives, robots, machine vision systems, HMIs, SCADA, MES, and asset performance software platforms |

|

System Integrators & OEMs |

Engineering firms and machine builders that design, install, and commission integrated automation solutions tailored to plant-specific process and quality requirements |

|

Distribution & Channel Partners |

National and regional distributors, value-added resellers, and authorized service partners that extend reach into Tier-2 and Tier-3 industrial clusters |

|

End-Use Industries |

Automotive, electronics, pharmaceuticals, chemicals, oil and gas, metals, F&B, power, and water utilities running the deployed automation assets |

Players that combine deep hardware manufacturing scale with strong software portfolios and integrator networks tend to capture larger wallet share, while specialist integrators serve niche process or sector-specific needs.

Technology Landscape in the India Industrial Automation Industry

Industrial AI and Predictive Maintenance

AI-driven anomaly detection and predictive maintenance are becoming standard in new deployments. Vendors are integrating AI agents directly into PLC and MES layers, enabling real-time decision support and reduced unplanned downtime.

Digital Twins and Simulation

Digital twin platforms are letting manufacturers simulate factories, train operators, and validate process changes virtually before commissioning. Adoption is broadening from automotive into pharma, F&B, and metals.

Smart Connectivity and IIoT

Wireless sensors, edge gateways, and 5G-ready industrial networks are extending automation visibility into legacy assets. Open protocols are simplifying multi-vendor data exchange and unified plant dashboards.

Robotics and Cobots

Indian customers are increasingly specifying six-axis robots and cobots in new lines, with applications spanning welding, painting, assembly, palletizing, and inspection. Improved safety standards and easier programming tools are widening the addressable use cases.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Hardware |

67.4% |

2025 |

|

Industry |

Process automation |

48.6% |

2025 |

|

Vertical |

🔒 |

🔒 |

2025 |

|

Region |

West India |

38.7% |

2025 |

By Component

Hardware commands a 67.4% majority share in 2025, anchored by sustained demand for PLCs, DCS, drives, motors, sensors, HMIs, and industrial robots across automotive, metals, refining, and pharma plants. Replacement cycles, capacity additions, and new fabs are sustaining hardware-led spending across regions.

To access detailed market analysis, Request Sample

Software at 32.6% in 2025 is the faster-growing slice, driven by SCADA upgrades, cloud-native MES, asset performance management, and AI-led analytics. Software-defined and open automation models are accelerating subscription adoption and reducing vendor lock-in over the forecast period.

By Industry

Process automation leads with 48.6% share in 2025, reflecting the depth of India's refining, chemicals, fertilizers, pharmaceuticals, and F&B assets. DCS, advanced process control, safety instrumented systems, and asset integrity software remain priority spend categories for these plants.

Factory automation at 32.7% share is supported by automotive, electronics, and consumer durables modernization. Rising deployment of robotics, machine vision systems, and automated material handling solutions is further strengthening productivity and precision across discrete manufacturing facilities.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

West India |

38.7% |

Strong industrial cluster density, established automotive and chemicals base, mature port-led trade infrastructure, and supportive state-level investment incentives |

|

South India |

28.5% |

Expanding electronics and semiconductor manufacturing, growing aerospace and defense base, deep IT-OT engineering talent, and rising automotive OEM presence |

|

North India |

22.4% |

Sustained automotive and consumer-durables manufacturing, expanding logistics and food-processing capacity, and proximity to large domestic consumption markets |

|

East India |

10.4% |

Concentration of metals, mining, and heavy engineering, rising port-linked industrial corridors, and gradual modernization of legacy process assets |

West India at 38.7% in 2025 leads the market, supported by Maharashtra's deep automotive and pharma cluster, Gujarat's chemicals and refining base, and rising fab and ATMP plans. A dense supplier ecosystem and mature integrator base further entrench regional dominance.

South India at 28.5% is the fastest-growing region through 2034. Expanding electronics manufacturing in Tamil Nadu and Karnataka, aerospace and defense in Bengaluru, and a deep mechatronics talent pool are accelerating regional demand for advanced automation.

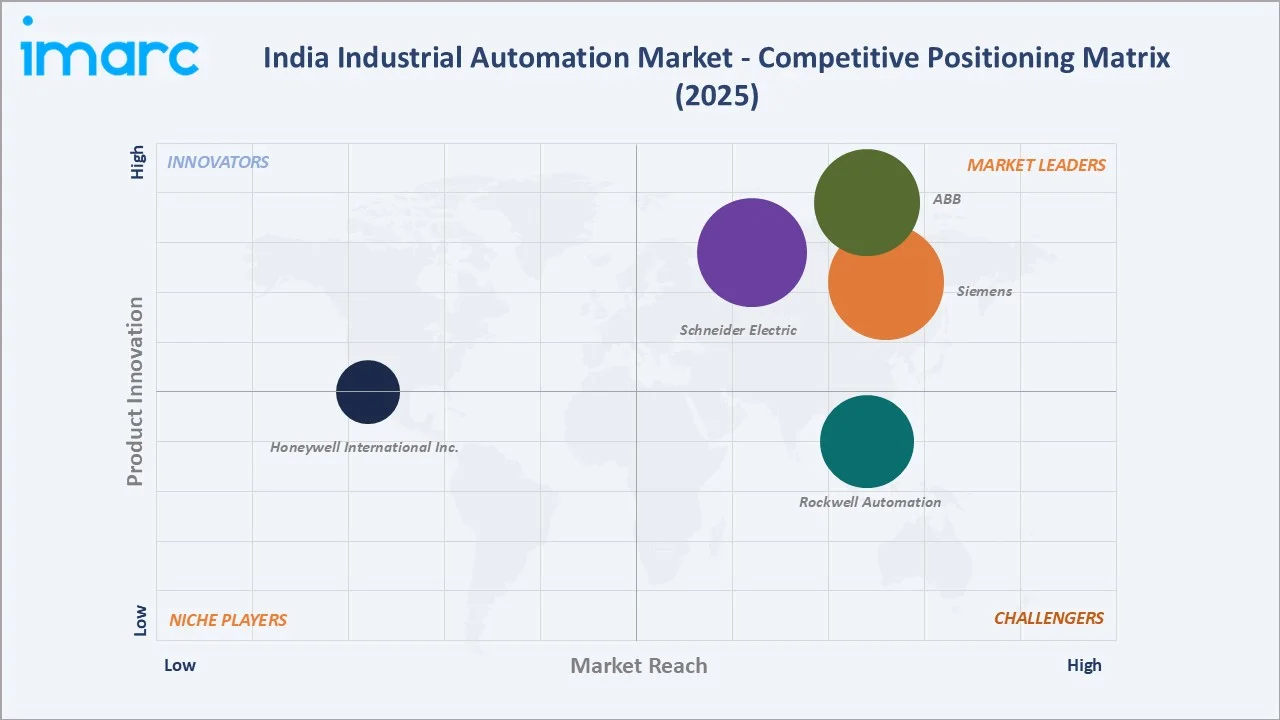

Competitive Landscape

The India industrial automation market is moderately concentrated, with multinational leaders dominating brand recognition, integrator depth, and software platform reach, while regional specialists serve niche process and sector-specific needs. Multi-vendor integration capability and software platform breadth form the key competitive moats.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Siemens |

SINUMERIK ONE, SINUMERIK 828D |

Leader |

Integrated hardware-software portfolio with deep India manufacturing footprint and digital industries focus |

|

ABB |

ABB IRB 6700, IRB 1300 |

Leader |

Robotics-led discrete automation strategy combined with strong process automation and electrification reach |

|

Schneider Electric |

EcoStruxure, Modicon PLCs, Harmony HMIs, |

Leader |

Open and software-defined automation platforms paired with energy management and sustainability solutions |

|

Rockwell Automation |

Allen-Bradley, FactoryTalk |

Challenger |

Discrete automation specialization with strong PLC and MES platforms targeting automotive and consumer goods |

|

Honeywell International Inc. |

Experion PKS, Honeywell Forge Performance+ |

Emerging |

Process automation and industrial software portfolio with cybersecurity and connected-plant focus |

Key parent companies include Siemens, ABB, Schneider Electric, Rockwell Automation, and Honeywell International Inc., among others.

Key Company Profiles

Siemens

Siemens is among the largest industrial automation suppliers in India, serving customers across digital industries, smart infrastructure, mobility, and energy. The India operation runs 32 factories with deep coverage of process and discrete automation customers.

- Product Portfolio: SINUMERIK ONE and the compact mid-range SINUMERIK 828D, and SIMATIC industrial automation systems.

- Recent Developments: In January 2025, the company launched MACHINUM at IMTEX 2025 to digitalize the Indian machine tool industry, with a stated potential to reduce setup time by up to 20% and minimize energy consumption up to 18%.

- Strategic Focus: Combining locally manufactured hardware with global software platforms and AI capabilities to support Make in India and large infrastructure modernization programs.

ABB

ABB is a leading global automation, robotics, and electrification supplier with an extensive Indian footprint. The Indian business serves process automation, discrete automation, and motion customers across automotive, metals, cement, food and beverage, and pharmaceuticals.

- Product Portfolio: IRB-series industrial robots including the heavy-payload IRB 6700 and the compact IRB 1300, AC and DC drives, motors, low- and medium-voltage products, and distributed control systems.

- Recent Developments: In October 2025, ABB India, the subsidiary of ABB, launched a new robotics-driven production line for energy-efficient variable speed drives at its Peenya factory in Bengaluru, increasing local VSD module output by approximately 25%.

- Strategic Focus: Localizing high-efficiency drives, robotics, and process automation manufacturing while strengthening integrator and channel ecosystems aligned with Atmanirbhar Bharat.

Rockwell Automation

Rockwell Automation is a pure-play industrial automation and digital transformation supplier, focused on discrete and hybrid manufacturing in India. The company emphasizes integrated control, information, and connected-services portfolios.

- Product Portfolio: Allen-Bradley PLCs and HMIs, FactoryTalk software suite, and SecureOT Solution Suite.

- Recent Developments: In April 2024, Rockwell Automation announced a new manufacturing facility in India - a 98,000-square-foot factory in Chennai, placing focus on the semiconductor sector and data center equipment. The site would be situated in the same industrial park as Rockwell's CUBIC manufacturing facility to enhance supply chain resilience and generate more job opportunities for workers.

- Strategic Focus: Deepening discrete automation reach in automotive, consumer goods, and life sciences while expanding software-led recurring revenue streams.

Market Concentration Analysis

The India industrial automation market is moderately concentrated, with the top five companies (Siemens, ABB, Schneider Electric, Rockwell Automation, and Honeywell International Inc.) collectively estimated to hold a sizeable share of multinational automation revenue across process, discrete, and motion segments.

Barriers to entry include strong installer-channel relationships, multi-decade installed bases, certification requirements across hazardous-area and safety-critical assets, and the deep software portfolios needed for Industry 4.0 and AI deployments.

Consolidation is gradually accelerating through software acquisitions, joint ventures with Indian integrators, and bundling of automation hardware with energy and digital services. Local manufacturing scale and after-sales reach further reinforce the competitive position of established players.

Investment & Growth Opportunities

Fastest-Growing Segments

Software at 32.6% and machine automation at 18.7% are expected to grow faster than the overall 8.17% market CAGR through 2034. Cloud-native MES, AI-led analytics, and modular cobot retrofits are among the fastest-rising sub-areas.

Emerging Sub-Markets

South India at 28.5% is the highest-growth region, with Tamil Nadu, Karnataka, and Telangana leading electronics, aerospace, and semiconductor-led demand. East India at 10.4% remains the largest untapped opportunity as port-led corridors and metals modernization expand.

Venture & Investment Trends

Capital is concentrated in industrial AI, OT cybersecurity, edge analytics platforms, cobots, and MES-as-a-service. Investment is also expanding into local manufacturing of drives, sensors, and robots, supported by PLI-linked capacity additions.

Future Market Outlook (2026-2034)

The India industrial automation market is forecast to expand from USD 8.22 Billion in 2025 to USD 16.67 Billion by 2034 at a CAGR of 8.17%, adding nearly USD 8.45 Billion in incremental annual market value over the forecast period.

Four forces will shape the market through 2034: industrial AI moving from pilots to production; convergence of OT and IT through software-defined automation; deeper localization of high-end automation manufacturing; and rapid SME automation adoption supported by lower-cost cobots and edge controllers.

By 2034, AI agents and digital twins will be embedded across most new automotive, electronics, and process plants, while subscription-led software revenue is expected to form a meaningfully larger share of vendor revenue mix in India.

Research Methodology

Primary Research

Primary research included structured interviews with senior plant managers, automation OEM leaders, system integrator executives, and industry association representatives across automotive, electronics, pharma, refining, and metals customers, validating market sizing, segment shares, and adoption trajectories.

Secondary Research

Secondary sources included data from the Press Information Bureau, Invest India, IBEF, Ministry of Heavy Industries, IEEMA, NASSCOM, and the International Federation of Robotics, alongside annual reports, investor presentations, and press releases of listed automation suppliers operating in India.

Forecasting Models

Forecasts combined top-down and bottom-up models, drawing on installed-base assumptions, capacity addition pipelines, PLI-linked deployment schedules, average automation intensity per industry, and segment-wise pricing trends. Scenario analysis addressed capex cyclicality and component price variation.

India Industrial Automation Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Hardware, Software |

| Industries Covered | Process Automation, Factory Automation, Machine Automation |

| Verticals Covered | Pharmaceutical, Food and Beverage Machinery, Energy Equipment/Mining/Utilities, Packaging Machinery, Automotive, Textile/Fabric/Coating Machinery |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Siemens, ABB, Schneider Electric, Rockwell Automation, Honeywell International Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India industrial automation market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India industrial automation market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India industrial automation industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Industrial Automation Market Report

The India industrial automation market was valued at USD 8.22 Billion in 2025, supported by Make in India momentum, PLI-linked capacity additions, and rapid digital retrofits.

The market is projected to grow at an 8.17% CAGR from 2026 to 2034, reaching USD 16.67 Billion, supported by Industry 4.0 adoption and rising automation intensity.

Hardware leads at 67.4% in 2025, anchored by PLCs, drives, and robots. Software at 32.6% is the faster-growing slice, driven by MES, SCADA, and AI analytics.

Process automation dominates at 48.6% in 2025, driven by refining, chemicals, pharma, and F&B. Demand for distributed control systems, advanced process control, and real-time monitoring solutions continues to rise as manufacturers prioritize operational efficiency, safety compliance, and energy optimization.

West India commands 38.7% share in 2025, led by Maharashtra and Gujarat through automotive, chemicals, and pharma clusters. South India at 28.5% is the fastest-growing region.

Leading parent companies include Siemens, ABB, Schneider Electric, Rockwell Automation, and Honeywell International Inc.

Make in India, PLI schemes, falling sensor and robotics costs, rising labor costs, and the push for export-grade quality are key drivers of automation adoption across plants.

PLI disbursements are linked to real-time output and efficiency tracking, prompting beneficiaries to install advanced controllers, vision systems, and plant-wide software for compliance.

Industry 4.0 is enabling integration of IIoT, AI, digital twins, and cloud-based MES, helping Indian manufacturers improve productivity, quality, and sustainability across plant operations.

Industrial AI is enabling predictive maintenance, process optimization, and software-defined production, with India emerging as a global hub for automation AI engineering and deployment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)