India Industrial Packaging Market Size, Share, Trends and Forecast by Product, Material, Application, and Region, 2026-2034

India Industrial Packaging Market Summary:

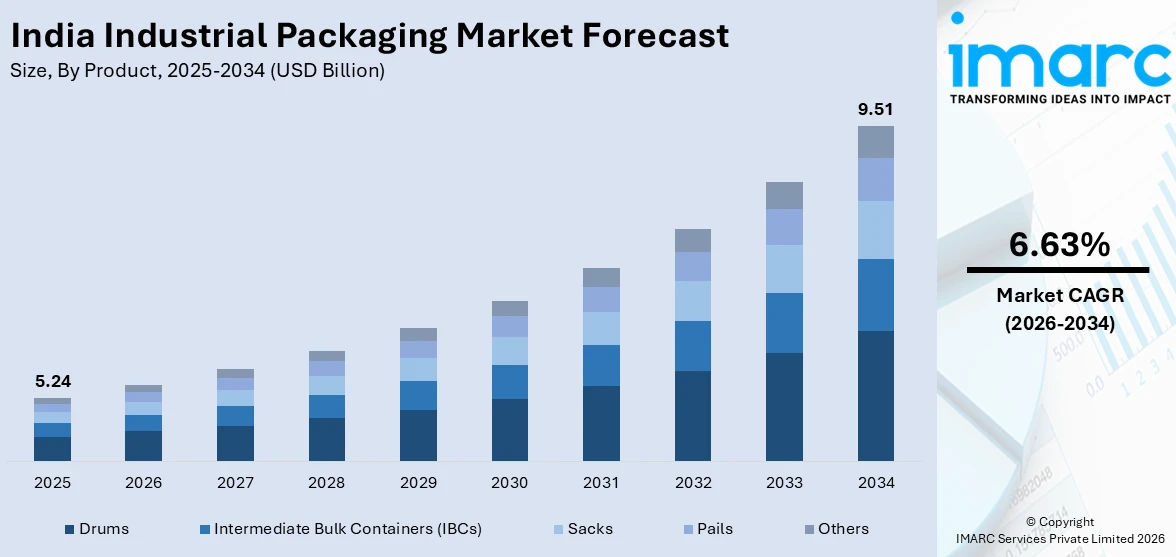

The India industrial packaging market size was valued at USD 5.24 Billion in 2025 and is projected to reach USD 9.51 Billion by 2034, growing at a compound annual growth rate of 6.63% from 2026-2034.

The market is driven by the rapid expansion of manufacturing, chemical, and pharmaceutical industries across the country, supported by strong government initiatives promoting industrial development and infrastructure growth. Rising export activity, increasing domestic consumption of packaged goods, and the growing need for safe, compliant containment solutions across diverse end-use sectors including petroleum, food processing, and automotive are collectively reinforcing sustained demand and shaping the India industrial packaging market share.

Key Takeaways and Insights:

- By Product: Drums dominate the market with a share of 34.8% in 2025, driven by their versatility in bulk liquid storage, chemical containment, and multi-industry transport applications.

- By Material: Plastic leads the market with a share of 42.1% in 2025, owing to its lightweight nature, chemical resistance, durability, and cost efficiency across industrial applications.

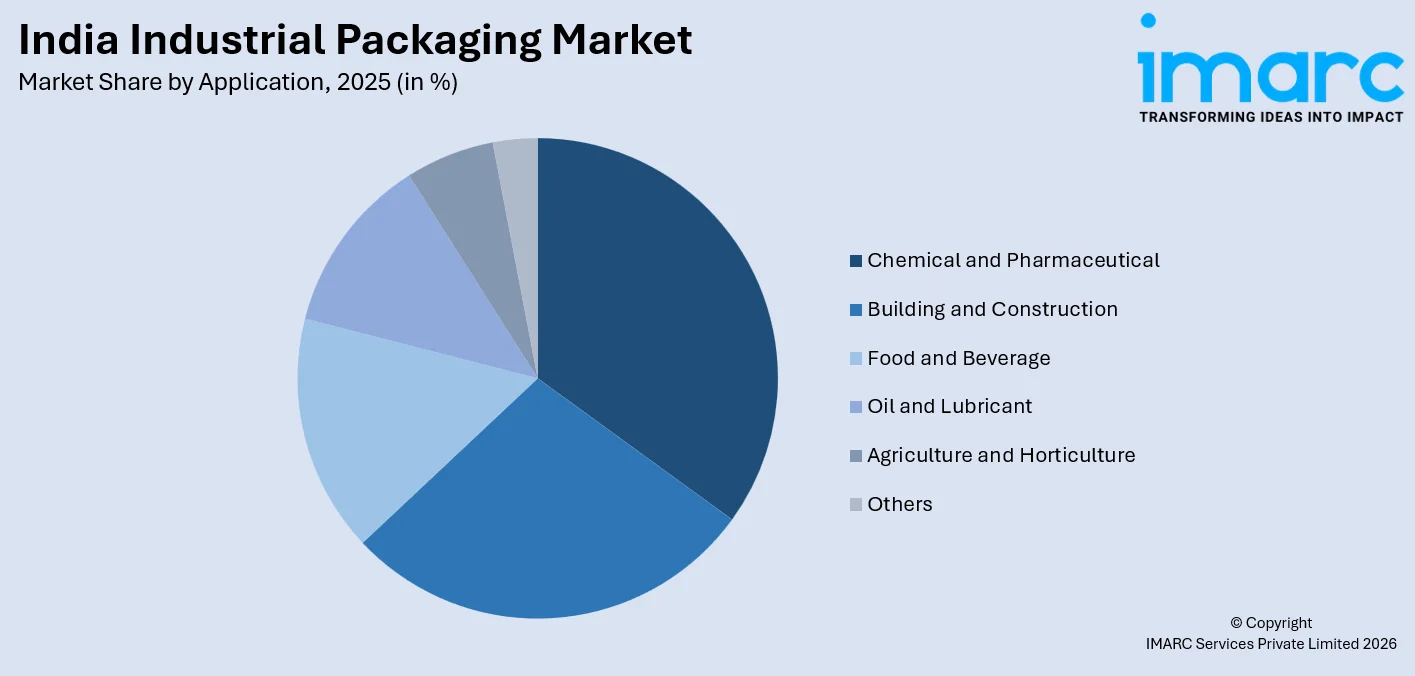

- By Application: Chemical and Pharmaceutical represents the largest segment with a market share of 30.5% in 2025, driven by stringent safety, compliance, and contamination-prevention requirements across these sectors.

- By Region: West and Central India leads the market with a share of 32.0% in 2025, owing to the concentration of chemical, pharmaceutical, and petrochemical manufacturing hubs.

- Key Players: The India industrial packaging market is moderately competitive, with domestic and international players focusing on sustainable materials, product innovation, and sector-specific customization to strengthen their market positioning across diverse industrial end-use segments.

To get more information on this market Request Sample

The India industrial packaging market is experiencing sustained growth driven by expanding industrial output and the increasing need for safe, reliable containment solutions across multiple sectors. The country's robust manufacturing base, growing chemical processing capacity, and pharmaceutical production scale are creating consistent demand for specialized packaging formats. Additionally, the proliferation of export-oriented industries has accelerated the adoption of compliant, internationally certified packaging systems. Government-led infrastructure development and industrial corridor programs are further stimulating demand across tier-two and tier-three industrial regions. Investment in automation within packaging operations, coupled with the integration of smart tracking and tamper-evident features, is reshaping operational efficiency. The rising focus on sustainability is encouraging a gradual shift toward recyclable and reusable industrial packaging materials, reflecting the evolving priorities of manufacturers and end-users across India's diverse industrial landscape.

India Industrial Packaging Market Trends:

Adoption of Sustainable and Recyclable Packaging Materials

India's industrial packaging sector is witnessing a marked transition toward environmentally responsible materials. Manufacturers are increasingly integrating recycled polymers, bio-based composites, and reclaimed materials into their packaging product lines. In November 2025, India launched the National Packaging Innovation Challenge, encouraging startups and students to develop environmentally responsible, scalable packaging solutions, supporting sustainability, export competitiveness, and Aatmanirbhar Bharat goals. This shift is being accelerated by corporate sustainability commitments, tighter environmental compliance standards, and rising customer expectations for greener supply chains. The move supports India industrial packaging market growth by reducing lifecycle costs and aligning with circular economy principles gaining traction across the country's manufacturing and logistics sectors.

Integration of Smart Packaging Technologies

The industrial packaging landscape in India is rapidly embracing intelligent technologies that enhance supply chain transparency and product safety. Features such as RFID tags, QR codes, tamper-evident seals, and temperature-sensitive indicators are becoming standard in high-value industrial applications. These innovations allow manufacturers, distributors, and end-users to monitor product conditions in real time, reduce spoilage, and ensure regulatory compliance. In April 2025, Avery Dennison expanded its India presence with a new RFID inlay and label manufacturing facility in Pune, aimed at accelerating smart traceability solutions across sectors including pharmaceuticals and logistics. Pharmaceutical and chemical industries are leading the adoption of smart packaging to meet traceability mandates and manage complex distribution networks effectively.

Growth of Flexible and Lightweight Industrial Packaging Formats

Flexible packaging formats, including intermediate bulk containers, multi-layer films, and collapsible containers, are gaining significant traction across India's industrial sectors. These formats offer advantages in storage efficiency, transport cost reduction, and adaptability to varying product types. In September 2025, the 12th Speciality Films & Flexible Packaging Global Summit in Mumbai attracted 2,200+ delegates and 800 organizations, highlighting India’s position as a prominent center for flexible and multi-layer packaging innovation with government and global brand support. As logistics networks become more sophisticated and cost-conscious, demand for packaging solutions that minimize material usage without compromising protection is intensifying. The shift toward lightweight formats is particularly prominent in food processing, agrochemical, and automotive components sectors, reflecting a broader industry-wide optimization of material and freight costs.

Market Outlook 2026-2034:

The India industrial packaging market is poised for robust revenue expansion through the forecast period, driven by accelerating industrial activity, infrastructure development, and export-oriented manufacturing growth. Rising investments in chemical processing, pharmaceutical production, and food and beverage manufacturing will sustain demand for advanced packaging formats. The focus on sustainability, regulatory compliance, and supply chain modernization will further drive innovation. Adoption of intelligent and automated packaging solutions is expected to create new revenue streams, positioning India as a significant growth market globally. The market generated a revenue of USD 5.24 Billion in 2025 and is projected to reach a revenue of USD 9.51 Billion by 2034, growing at a compound annual growth rate of 6.63% from 2026-2034.

India Industrial Packaging Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product |

Drums |

34.8% |

|

Material |

Plastic |

42.1% |

|

Application |

Chemical and Pharmaceutical |

30.5% |

|

Region |

West and Central India |

32.0% |

Product Insights:

- Intermediate Bulk Containers (IBCs)

- Sacks

- Drums

- Pails

- Others

Drums dominate with a market share of 34.8% of the total India industrial packaging market in 2025.

Drums are among the most versatile and durable packaging formats used in India's industrial ecosystem. Their construction from materials such as steel, high-density polyethylene, and fiber allows them to safely contain a wide range of substances, including corrosive chemicals, petroleum products, and pharmaceutical raw materials. In December 2025, Aditya Better Container expanded production of plain fibre drums at its Pondicherry facility to meet growing industrial demand for sustainable, recyclable bulk packaging solutions across chemical and pharma sectors.

This continued adoption of drums across chemical processing, petroleum refining and food-grade applications is due to compliance with national and international safety standards. Their proven ability to accommodate liquid, semi-liquid, and solid contents without degradation or contamination risks makes them preferred across facilities with stringent quality control requirements. Growing investments in chemical manufacturing corridors and expanding pharmaceutical supply chains are further strengthening demand for drums as the primary containment solution across India’s industrial packaging landscape.

Material Insights:

- Paperboard

- Plastic

- Metal

- Wood

- Fiber

Plastic leads with a share of 42.1% of the total India industrial packaging market in 2025.

Plastic remains the most widely adopted material in India's industrial packaging sector owing to its lightweight properties, moldability, and compatibility with a broad spectrum of industrial chemicals and substances. High-density polyethylene and polypropylene variants are extensively used in drums, carboys, IBCs, and industrial crates, offering superior resistance to moisture, acids, and alkaline compounds. The material's ability to be manufactured in varied configurations and colors for product identification further enhances its operational utility.

The growing regulatory orientation toward quality and containment safety in chemical and pharmaceutical industries keeps reinforcing plastic as a central material in industrial packaging. Advances in polymer engineering have led to the creation of multi-layer and co-extruded plastic containers with enhanced barrier properties capable of extending shelf life and protecting product integrity. Recycled or recyclable grades of plastic also are increasingly available and offer manufacturers avenues for continuing to meet performance requirements alongside the emerging sustainability mandates in India’s industrial packaging industry.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Chemical and Pharmaceutical

- Building and Construction

- Food and Beverage

- Oil and Lubricant

- Agriculture and Horticulture

- Others

Chemical and pharmaceutical exhibits a clear dominance with a 30.5% share of the total India industrial packaging market in 2025.

The chemical and pharmaceutical industries in India generate some of the highest demand for specialized industrial packaging, given the sensitivity and regulatory rigor associated with product handling and distribution. Packaging used in these sectors must meet stringent material compatibility, chemical resistance, and contamination-prevention standards. As per sources, Domino Printech introduced advanced coding and marking technologies for pharmaceutical packaging at CPHI & PMEC India, enabling end-to-end traceability from blister packs to pallet-level aggregation to meet global compliance requirements.

India's pharmaceutical manufacturing sector is one of the largest in the world, generating consistent demand for high-quality primary and secondary industrial packaging. Similarly, the country's expanding specialty chemicals, agrochemicals, and fine chemicals industries require customized packaging that can withstand varying temperatures, pressures, and reactive conditions. The need for documented traceability, batch identification, and compliance with Good Manufacturing Practice guidelines reinforces demand for precision-engineered packaging across the chemical and pharmaceutical application landscape in India.

Regional Insights:

- Northern India

- West and Central India

- South India

- East and Northeast India

West and Central India dominates with a market share of 32.0% of the total India industrial packaging market in 2025.

West and Central India represents the most industrially active packaging market in the country, anchored by the presence of major industrial clusters in states such as Maharashtra, Gujarat, and Madhya Pradesh. These states host a high density of chemical parks, pharmaceutical special economic zones, and petrochemical processing units that generate substantial and continuous demand for industrial packaging solutions. The region's well-developed logistics infrastructure further supports efficient packaging supply chains and distribution networks.

The dominance of West and Central India in the industrial packaging market is reinforced by the scale of its manufacturing base and export-oriented industrial activity. The region's deep integration with India's chemical corridor and pharmaceutical manufacturing ecosystem creates demand for diverse product types, including drums, IBCs, carboys, and specialized containment systems. Continued investment in industrial infrastructure, warehousing capacity, and manufacturing expansion across the region is expected to sustain its leadership position throughout the forecast period.

Market Dynamics:

Growth Drivers:

Why is the India Industrial Packaging Market Growing?

Rapid Expansion of Chemical and Petrochemical Industries

India's chemical and petrochemical sectors have undergone substantial growth, resulting in intensified demand for industrial packaging solutions capable of safely handling reactive, corrosive, and hazardous materials. Dedicated chemical manufacturing zones and integrated petrochemical complexes developed across key industrial states are driving sustained demand for certified containment packaging. In September 2025, the Bulk Drug Park in Una, Himachal Pradesh received environmental clearance to strengthen domestic production of active pharmaceutical ingredients and reduce import dependence, reinforcing India’s pharmaceutical manufacturing ecosystem. The increasing production of specialty chemicals, agrochemicals, and industrial solvents requires packaging that adheres to national and international material safety standards.

Growth of the Pharmaceutical Manufacturing Sector

India holds a prominent position in global pharmaceutical manufacturing, generating consistent demand for precision-engineered industrial packaging across primary and secondary formats. The sector's stringent quality control, batch traceability, and Good Manufacturing Practice compliance requirements necessitate the use of specialized containers, closures, and barrier packaging that prevent contamination and preserve product integrity. According to reports, the Government of India approved financial incentives under the Production Linked Incentive (PLI) scheme for pharmaceuticals to strengthen domestic manufacturing of critical drugs and active pharmaceutical ingredients. Rising production of active pharmaceutical ingredients, finished formulations, and biologics is driving the adoption of high-performance plastic, glass, and composite industrial packaging formats.

Government Initiatives Supporting Industrial Infrastructure Development

Sustained government investment in industrial corridors, special economic zones, and manufacturing clusters is creating new demand centers for industrial packaging across previously underserved regions. Policy programs aimed at boosting domestic manufacturing, reducing import dependency, and developing industrial logistics networks are enabling packaging manufacturers to expand their geographic reach and production capacity. Incentives for industrial zone development and export promotion are attracting large-scale manufacturers across chemical, automotive, food processing, and pharmaceutical sectors whose operations generate significant and recurring demand for industrial packaging solutions, thereby fueling consistent market growth.

Market Restraints:

What Challenges the India Industrial Packaging Market is Facing?

High Cost of Compliant Packaging Solutions

Meeting national and international standards for industrial packaging requires significant material and process investment. Certified packaging that fulfills chemical resistance, structural integrity, and labeling compliance standards often carries a higher cost burden, limiting accessibility for smaller manufacturers. This creates pricing pressure and may lead some market participants to opt for substandard alternatives that compromise safety and regulatory adherence, posing risks to product quality and end-user safety.

Environmental Regulations on Plastic Packaging

Increasing regulatory pressure to reduce single-use and non-recyclable plastic is creating operational challenges for industrial packaging producers. While plastic remains the dominant material, evolving environmental mandates require investment in sustainable alternatives, recycling infrastructure, and product redesign. Transitioning toward compliant, eco-friendly packaging formats entails significant research, development, and capital expenditure, which can constrain short-term profitability and operational flexibility for manufacturers.

Supply Chain Disruptions and Raw Material Volatility

Industrial packaging manufacturers face persistent challenges from fluctuating raw material prices, particularly for resins, steel, and aluminum. Supply chain disruptions affecting material availability and lead times can delay production, increase costs, and reduce margins. These uncertainties are especially impactful for small and mid-sized packaging producers operating with limited inventory buffers and procurement capacity, affecting their ability to maintain consistent supply to industrial end-users.

Competitive Landscape:

The India industrial packaging market is characterized by a diverse mix of domestic manufacturers, regional suppliers, and multinational packaging groups competing across product categories and end-use sectors. Market participants are actively investing in the development of sustainable packaging materials, advanced manufacturing processes, and customized solutions designed to meet the specific requirements of chemical, pharmaceutical, petroleum, and food processing industries. Competition is further intensified by the drive to achieve international certifications, enhance product durability, and optimize packaging design for cost-effective logistics. Strategic expansions, capacity enhancements, and the adoption of automated production technologies are shaping the evolving competitive dynamics of India's industrial packaging sector.

India Industrial Packaging Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Intermediate Bulk Containers (IBCs), Sacks, Drums, Pails, Others |

| Materials Covered | Paperboard, Plastic, Metal, Wood, Fiber |

| Applications Covered | Chemical and Pharmaceutical, Building and Construction, Food and Beverage, Oil and Lubricant, Agriculture and Horticulture, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Industrial Packaging Market Research Report and Industry Forecast Report

The India industrial packaging market size was valued at USD 5.24 Billion in 2025.

The India industrial packaging market is expected to grow at a compound annual growth rate of 6.63% from 2026-2034 to reach USD 9.51 Billion by 2034.

Drums held the largest India industrial packaging market share, favored for their durability, versatility, and compliance with chemical and hazardous material containment standards across diverse industrial applications in the country.

Key factors driving the India industrial packaging market include expanding chemical and pharmaceutical manufacturing, rising export activity, government industrial infrastructure initiatives, growing demand for compliant packaging, and increasing adoption of sustainable and smart packaging formats.

Major challenges include high compliance-related packaging costs, evolving environmental regulations on plastic materials, raw material price volatility, supply chain disruptions, and limited access to advanced packaging technologies among smaller regional manufacturers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)