India Instant Coffee Market Size, Share, Trends and Forecast by Packaging, Coffee Type, Distribution Channel, and Region, 2026-2034

India Instant Coffee Market Size, Share, Trends & Forecast (2026-2034)

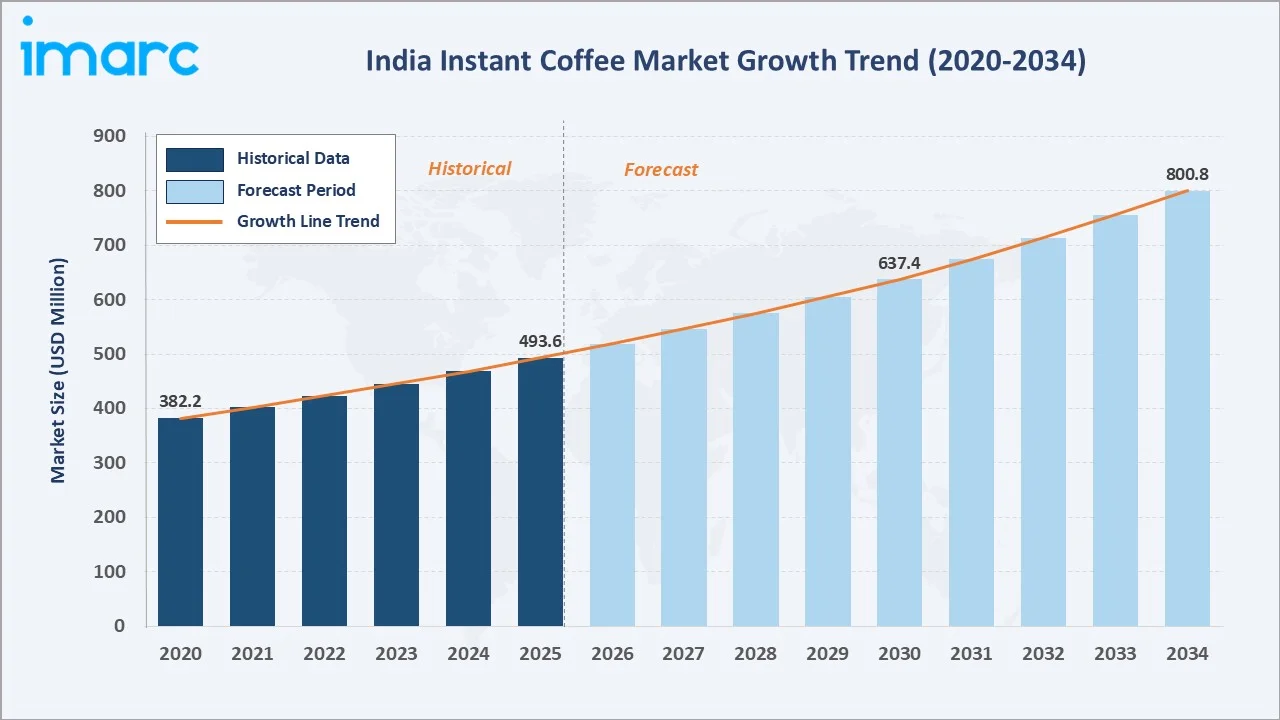

The India instant coffee market was valued at USD 493.6 Million in 2025 and is projected to reach USD 800.8 Million by 2034, exhibiting a CAGR of 5.25% during 2026-2034. Rising urbanization, rapid expansion of cafe culture among urban youth, growing demand for convenience-led beverages, and Nestlé's launch of its Nescafé Ready-to-Drink range in India in 2025 are the primary drivers shaping the market growth.

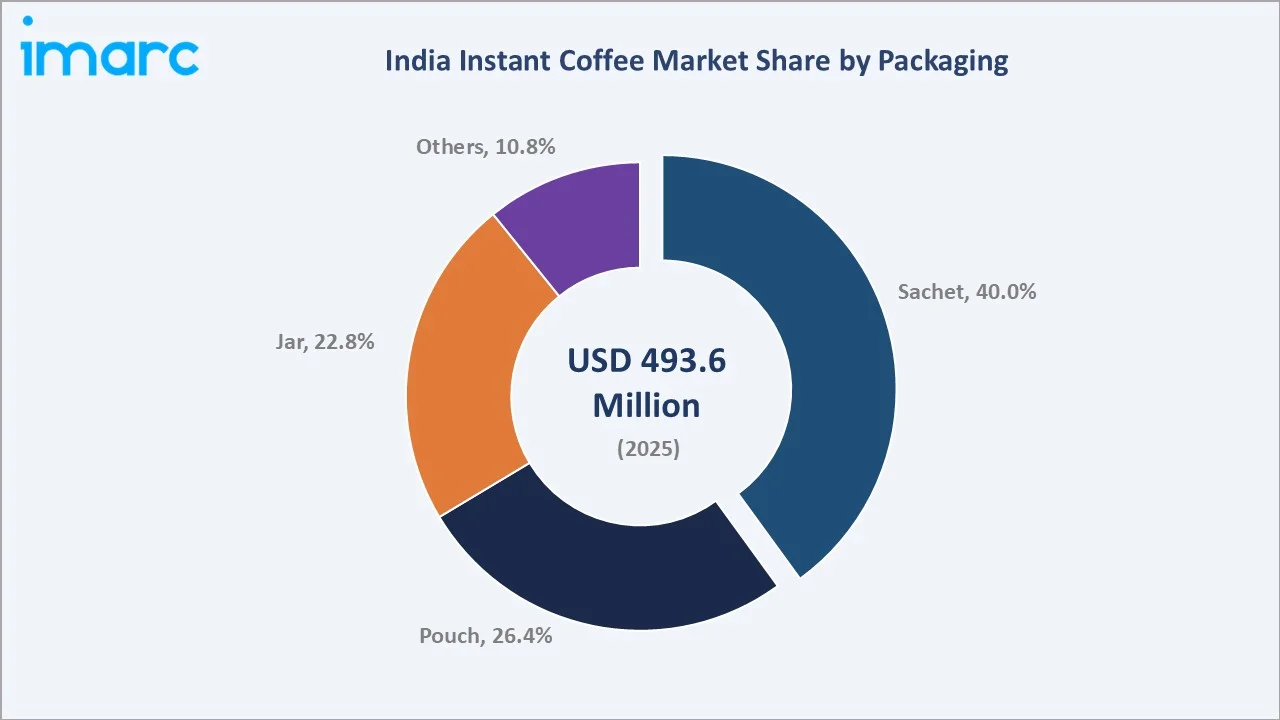

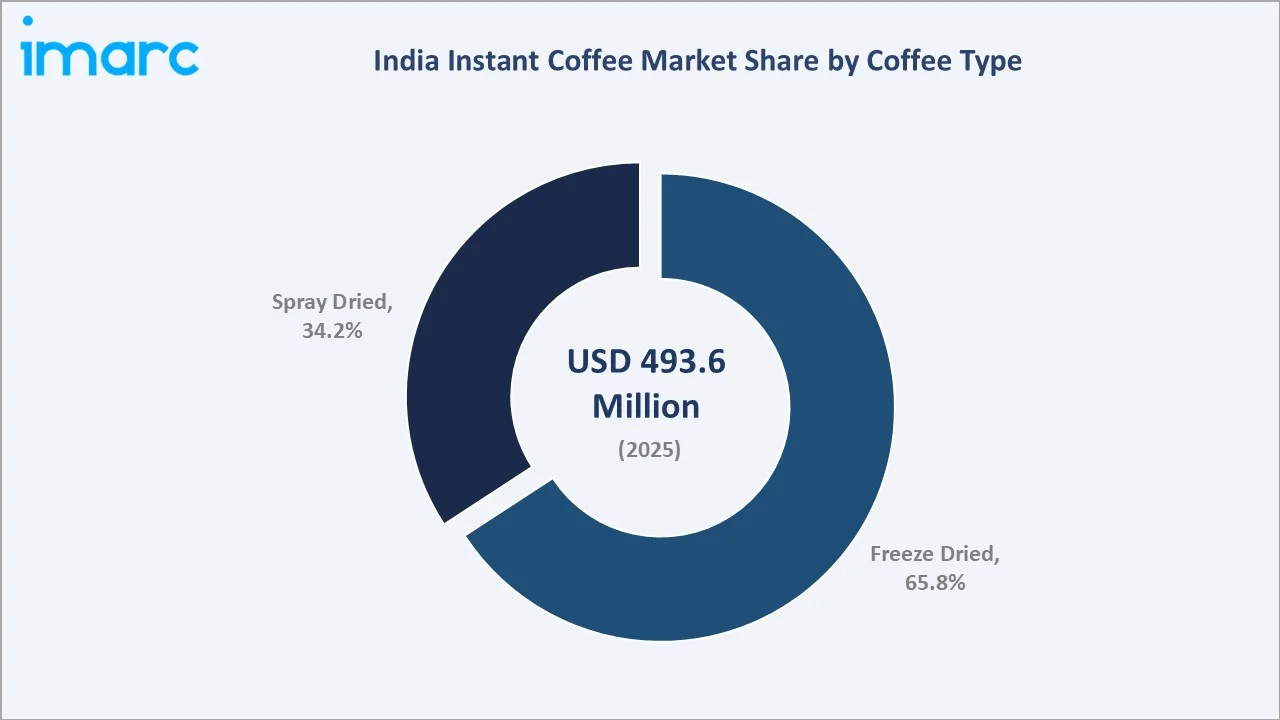

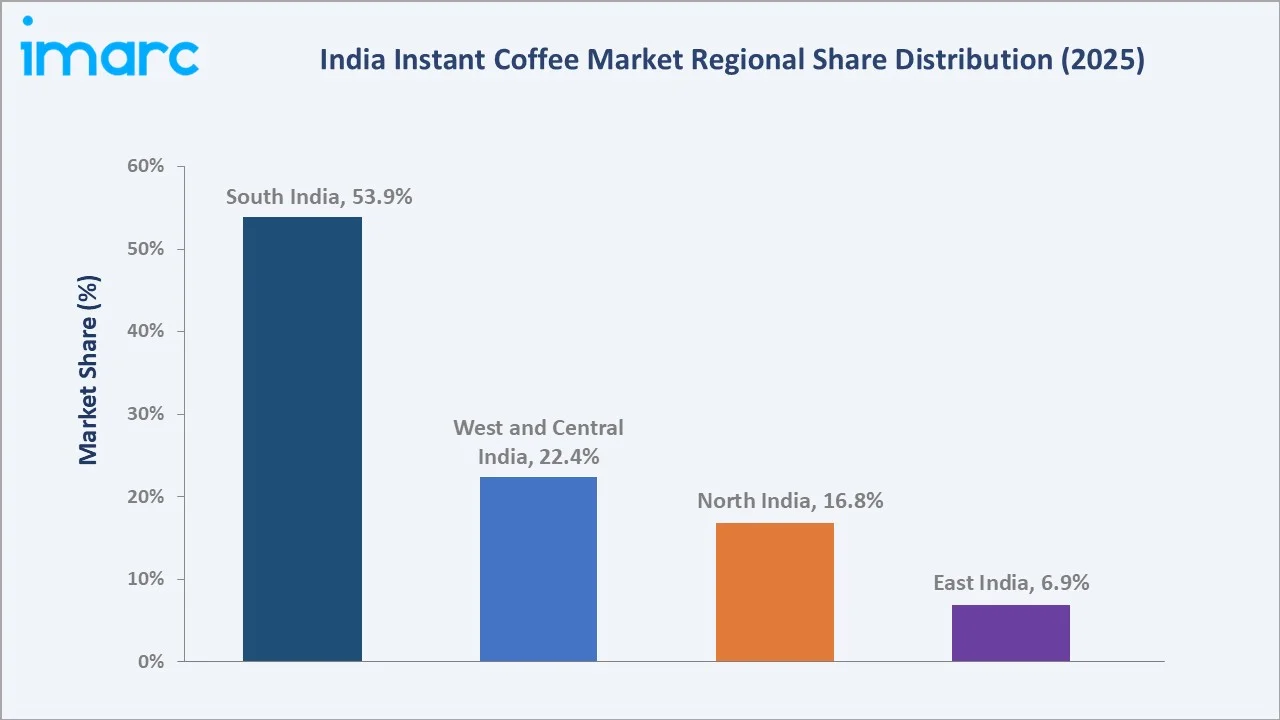

Sachet leads the packaging segment at 40.0%, freeze dried dominates the coffee type segment at 65.8%, and South India commands 53.9% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 493.6 Million |

|

Forecast Market Size (2034) |

USD 800.8 Million |

|

CAGR (2026-2034) |

5.25% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South India (53.9%, 2025) |

|

Fastest Growing Region |

East India (6.9%, 2025) |

|

Leading Packaging |

Sachet (40.0%, 2025) |

|

Leading Coffee Type |

Freeze Dried (65.8%, 2025) |

The India instant coffee market expanded from USD 382.2 Million in 2020 to USD 493.6 Million in 2025, fueled by accelerating urbanization, rising disposable income, and the steady migration of households from traditional brews toward convenience formats. Anchored at USD 637.4 Million in 2030, the forecast to USD 800.8 Million by 2034 is supported by sustained premiumization and category expansion across e-commerce.

To get more information on this market, Request Sample

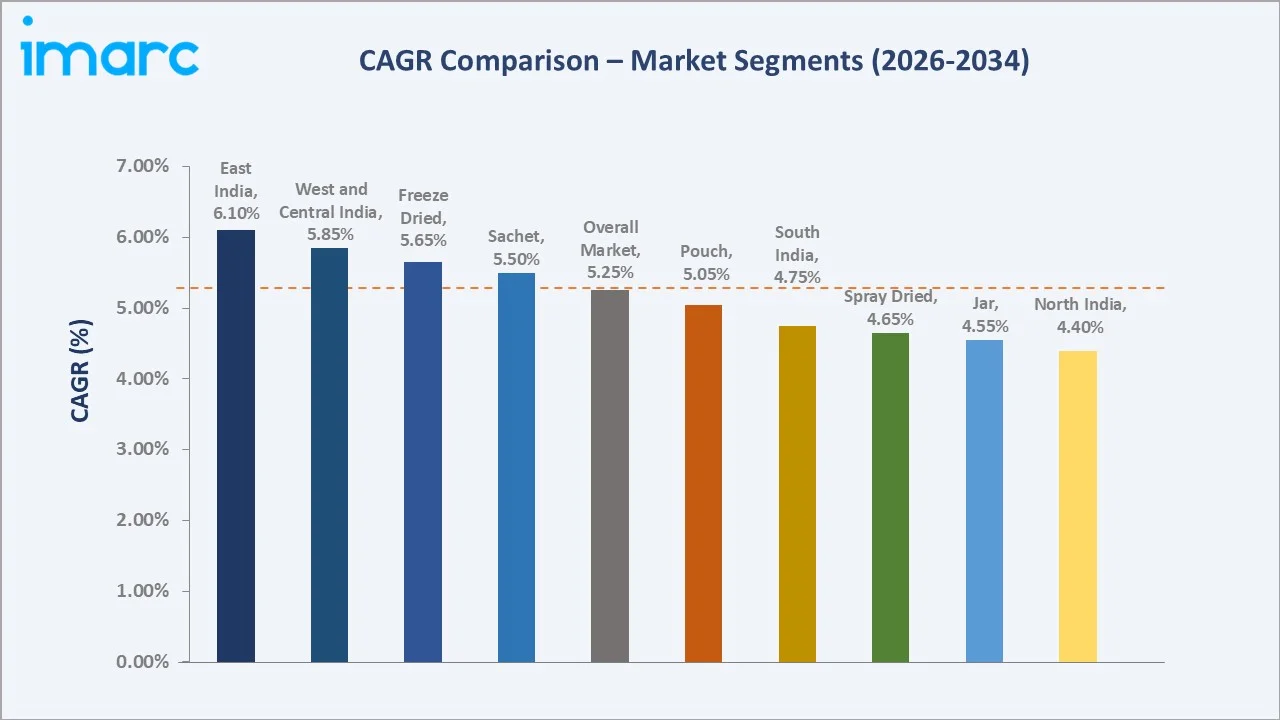

CAGR trajectories across packaging and coffee type sub-segments show East India, West and Central India, freeze dried, and sachet expanding faster than the overall 5.25% market CAGR, driven by category penetration in newer geographies and continued shift toward premium freeze dried offerings.

Executive Summary

The India instant coffee market is on a steady growth path from USD 382.2 Million in 2020 to USD 800.8 Million by 2034. Instant coffee has shifted from being a beverage of the urban household to a daily-use category across small towns and youth segments. Faster lifestyles, rising disposable income, and category innovation in formats and flavors are encouraging households to adopt instant coffee as a regular drink.

Sachet leads the packaging segment at 40.0% in 2025, supported by single-serve affordability and deep general trade reach. Freeze dried leads the coffee type segment at 65.8%, fueled by superior aroma retention and rising premium-tier consumption in the India instant coffee market. South India commands 53.9% regional share, led by Karnataka, Tamil Nadu, and Kerala, supported by deep coffee-drinking heritage and a strong domestic coffee processing base. As per PIB, Karnataka, Kerala, and Tamil Nadu accounted for 96% of India’s coffee production, with Karnataka leading at an estimated 2,80,275 MT (2025–26).

Key Market Insights

|

Insight |

Data |

|

Leading Packaging |

Sachet - 40.0% share (2025) |

|

Second Packaging |

Pouch - 26.4% share (2025) |

|

Leading Coffee Type |

Freeze Dried - 65.8% share (2025) |

|

Second Coffee Type |

Spray Dried - 34.2% share (2025) |

|

Leading Region |

South India - 53.9% share (2025) |

|

Fastest Growing Region |

East India - 6.9% share (2025) |

|

Top Companies |

Nestlé, Unilever, Tata Consumer Products Limited, Cothas Coffee Co., Sleepy Owl Coffee |

Key Analytical Observations Expanding on the Data Above:

- Sachet dominance at 40.0% is driven by its low entry price point and the deep general trade penetration of single-serve formats across tier 2 and tier 3 cities. Sachets continue to act as the primary trial vehicle for new instant coffee consumers.

- Pouch share at 26.4% reflects steady acceptance among regular household buyers, who prefer larger refill packs for in-home consumption. Modern trade and online channels are further supporting pouch volumes.

- Freeze dried leadership at 65.8% is fueled by superior aroma and taste retention compared with spray dried products. As per IBEF, India’s coffee shipments rose 27% during January -April 2026, indicating the strength of the country's freeze dried processing base.

- Spray dried at 34.2% remains essential for mass market and food service applications, where price sensitivity and dispensing speed matter more than flavor intensity.

- South India at 53.9% leads the country, supported by long-standing coffee culture, proximity to growing regions in Karnataka and Kerala, and the dense presence of brand-owner manufacturing units across the southern belt.

India Instant Coffee Market Overview

Instant coffee in India refers to soluble coffee in powder, granular, or agglomerated form that dissolves quickly in hot or cold water. It is sold in sachets, pouches, jars, and other formats, with freeze dried and spray dried being the two principal processing routes.

The ecosystem connects coffee growers in Karnataka, Kerala, and Tamil Nadu with processing and extraction units, brand-owner manufacturers, packaging suppliers, modern and general trade retailers, and rapidly growing e-commerce platforms, together delivering finished instant coffee to households, offices, and the HoReCa channel across the country.

Market Dynamics

To evaluate market opportunities, Request Sample

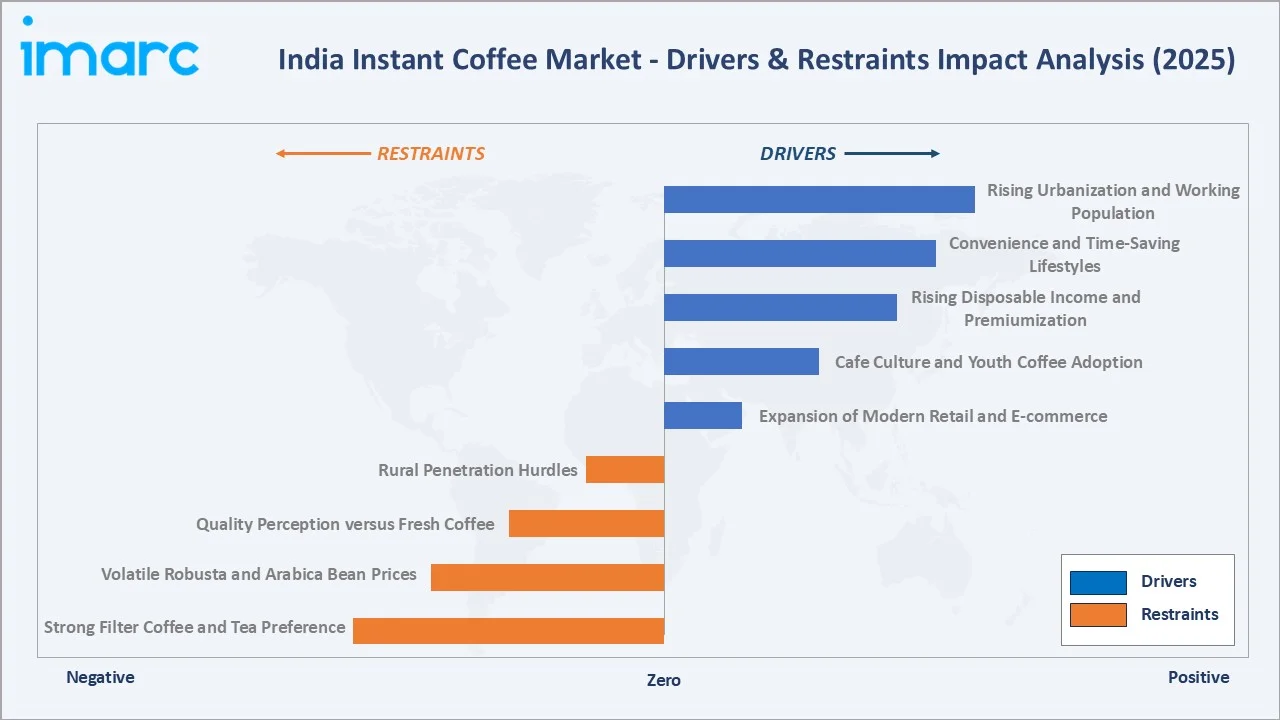

Market Drivers

- Rising Urbanization and Working Population: Faster work cycles in urban India are pushing households toward quick-prep beverages. According to the recent Economic Survey 2023-24, it is anticipated that over 40 percent of India's population will reside in urban regions by 2030. Instant coffee fits the morning and office routine of a growing segment of dual-income families.

- Convenience and Time-Saving Lifestyles: Single-serve sachets and easy-to-mix pouches meet the demand for hassle-free preparation. These formats simplify usage with minimal effort, quick mixing, and consistent portion control.

- Rising Disposable Income and Premiumization: Consumers are trading up from basic spray dried jars to freeze dried premium variants, driving value growth ahead of volume growth. Gold tier and roastery launches are visibly expanding shelf space.

- Cafe Culture and Youth Coffee Adoption: Exposure to cafe-style beverages through QSRs and Indian coffee chains is making cold coffee, frappes, and flavored instants part of regular consumption among Gen Z and millennial buyers.

- Expansion of Modern Retail and E-commerce: Online grocery platforms and modern trade chains are widening assortment, supporting larger pack sizes and enabling direct-to-consumer launches by smaller, premium brands.

Market Restraints

- Strong Filter Coffee and Tea Preference: South Indian filter coffee and the deeply rooted tea culture across the rest of the country continue to limit instant coffee adoption beyond a defined consumer base. Traditional taste preferences and brewing rituals reinforce this consumption pattern.

- Volatile Robusta and Arabica Bean Prices: Sharp swings in green coffee prices over the past two years have squeezed manufacturer margins and forced selective price hikes and grammage adjustments at the shelf, pressuring affordability.

- Quality Perception versus Fresh Coffee: A section of urban coffee enthusiasts views instant coffee as inferior to freshly roasted and brewed alternatives, restraining premium and super premium adoption in the highest-spending households.

- Rural Penetration Hurdles: Lower category awareness, weak cold-chain support for ready-to-drink launches, and the dominance of tea-based hot beverages slow rural conversion to instant coffee.

Market Opportunities

- Cold Coffee and Ready-to-Drink Expansion: Rising youth preference for chilled, on-the-go coffee creates a clear runway for ready-to-drink and cold coffee mixes, supported by growing cold chain reach in urban India.

- Direct-to-Consumer Premium Brands: Newer entrants are using e-commerce, subscriptions, and social media to build premium freeze dried brands, opening a higher-margin pocket alongside the mainstream sachet category. As per IMARC Group, the India e-commerce market size was valued at USD 129.72 Billion in 2025.

- Tier 2 and Tier 3 City Penetration: Rising aspirational consumption in smaller cities allows established players to deepen distribution with affordable sachets and value pouches, backed by regional language advertising.

Market Challenges

- Pressure on Robusta Supply Chain: India relies on Robusta-rich blends for instant coffee production, and global Robusta supply tightness adds raw material risk for manufacturers.

- Counterfeit and Loose Coffee in Open Markets: Loose, unbranded coffee powder sold in many neighborhood stores limits branded category growth and creates quality inconsistency for first-time buyers.

- Sustainability and Packaging Compliance: Tightening regulations on plastic sachets and laminate pouches require investment in recyclable and compostable formats, raising near-term packaging costs across the category.

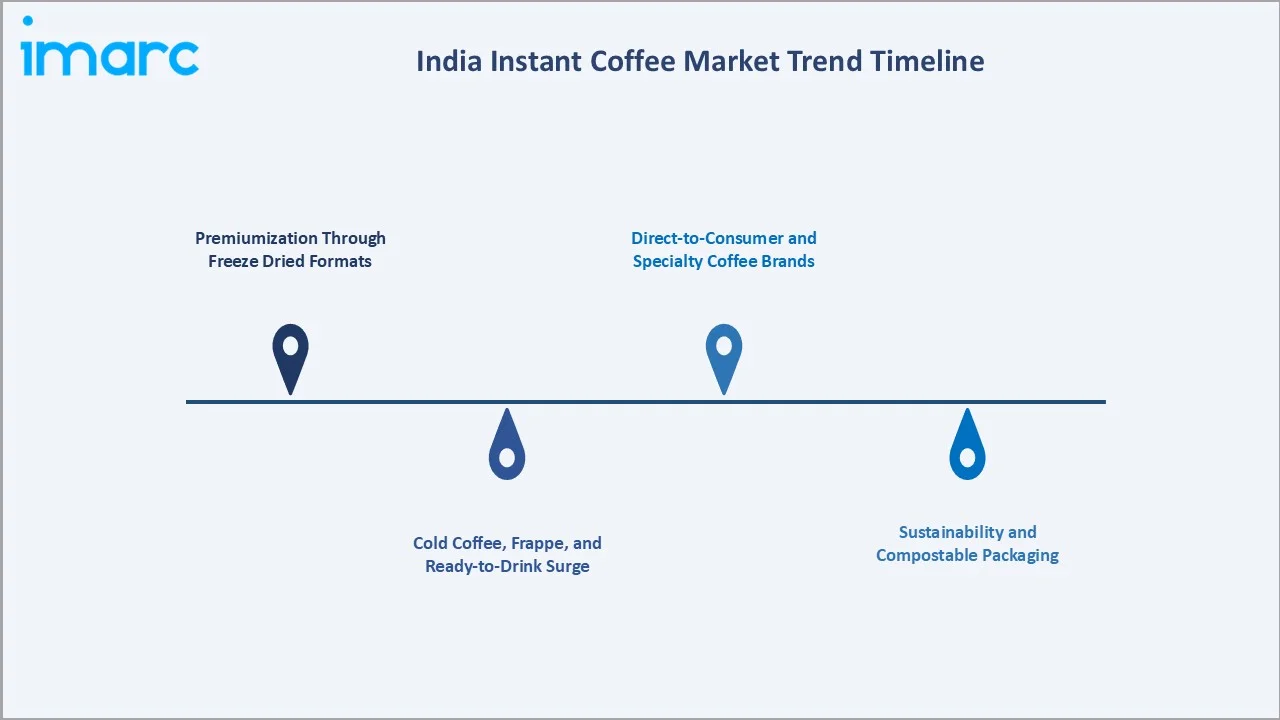

Emerging Market Trends

1. Premiumization Through Freeze Dried Formats

Freeze dried instant coffee is steadily replacing spray dried variants in metro households, supported by improved aroma, smoother taste, and the launch of gold and dark roast tiers from leading brands. This trend is shifting the category mix toward higher value per gram across both modern trade and e-commerce.

2. Cold Coffee, Frappe, and Ready-to-Drink Surge

Single-serve cold coffee mixes, frappe sachets, and chilled ready-to-drink cans are becoming a meaningful sub-category among Gen Z buyers. Their appeal is driven by café-style taste, convenience, and strong traction across modern retail and online channels.

3. Direct-to-Consumer and Specialty Coffee Brands

Indian startups are entering the instant coffee category with cold brew sachets, single origin instants, and flavored options like hazelnut and French vanilla. These brands lean on e-commerce, social media, and subscription models, opening a premium pocket above traditional jar SKUs.

4. Sustainability and Compostable Packaging

Brand owners are testing recyclable laminates, paper-based pouches, and refill jars to reduce plastic load. Sustainability claims are increasingly prominent on premium freeze dried packs, aligning with rising consumer expectations and tightening packaging regulations.

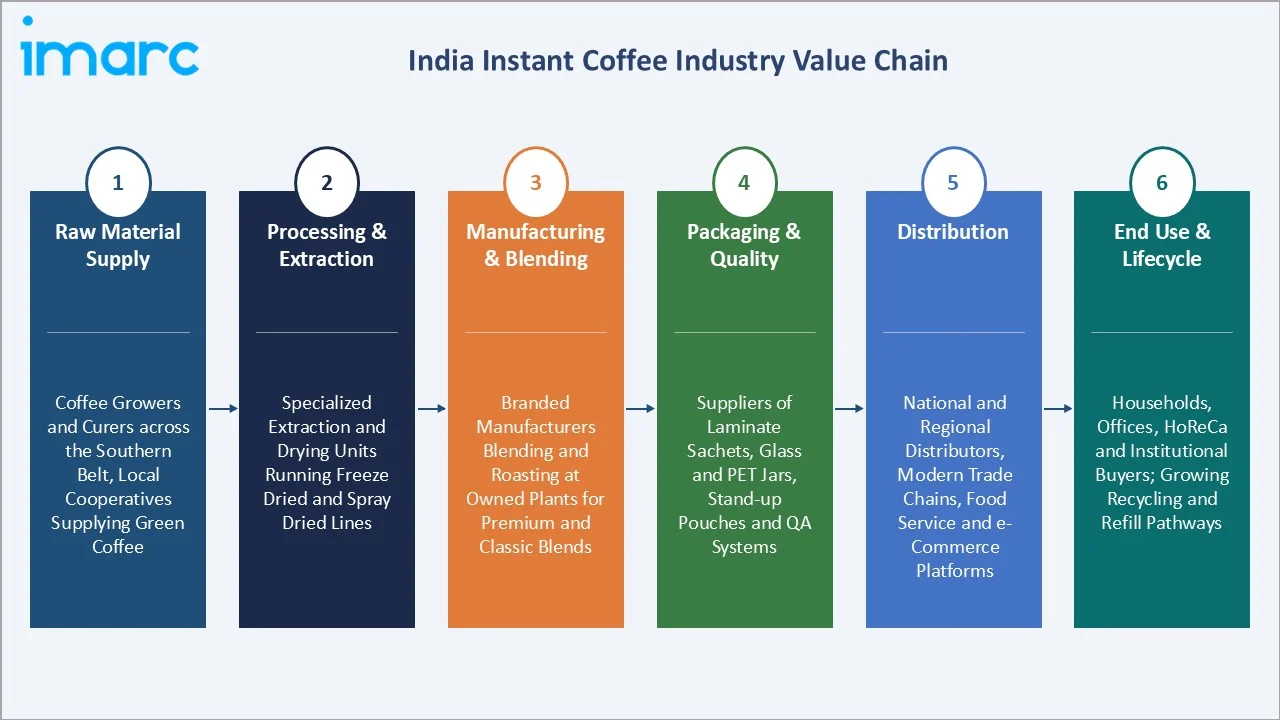

Industry Value Chain Analysis

The India instant coffee value chain spans six stages from coffee bean cultivation through end user consumption. Processing, extraction, and brand-owner manufacturing capture the highest value-add, while distribution depth and retail shelf control define downstream competitive advantage in this convenience category.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Coffee growers and curers operating across the southern coffee belt, supported by curing units and local cooperatives that supply green coffee for further processing |

|

Processing & Extraction |

Specialized extraction and drying units running freeze dried and spray dried lines, often as export oriented or contract manufacturing facilities |

|

Manufacturing & Blending |

Branded manufacturers blending and roasting at owned plants, with dedicated capacities for premium gold tier, classic, and chicory blends |

|

Packaging & Quality |

Suppliers of laminate sachets, glass and PET jars, stand-up pouches, and quality assurance systems aligned with food safety norms |

|

Distribution |

National and regional distributors, modern trade chains, organized food service operators, and rapidly scaling e-commerce platforms |

|

End Use & Lifecycle |

Households, offices, HoReCa, and institutional buyers, with growing recycling and refill pathways for jars and outer cartons |

Vertically integrated players that operate both plantations and instant coffee manufacturing facilities in South India, along with those running dedicated freeze-dried and spray-dried capacities, achieve stronger control over input costs and quality compared to companies relying on third-party processing.

Technology Landscape in the India Instant Coffee Industry

Freeze Drying and Aroma Capture

Freeze drying remains the technology of choice for premium instant coffee, with manufacturers investing in low-temperature freezing, aroma-recovery systems, and granulation control to deliver superior cup quality. Aroma capture during extraction is now a critical differentiator at the gold and roastery tier.

Spray Drying and Process Efficiency

Modern spray drying lines focus on energy efficiency, lower particle moisture, and improved solubility for cold water mixing. These advances support large-volume production for sachet and value pouch SKUs while keeping the unit cost competitive.

Packaging Innovation and Smart Formats

Multi-layer flexible laminates, oxygen-barrier films, and refillable jars are reducing oxidation and extending shelf life, while compostable and mono-material pouches are emerging in pilot launches. QR-based traceability and on-pack sourcing claims are gaining ground on premium SKUs.

Cold Coffee, Ready-To-Drink, and Personalization

Cold-soluble blends, capsule systems, and ready-to-drink lines are creating new touchpoints with younger buyers. Connected coffee machines, app-based personalization, and limited-edition seasonal flavors are starting to enter premium retail and HoReCa segments.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Packaging |

Sachet |

40.0% |

2025 |

|

Coffee Type |

Freeze Dried |

65.8% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

South India |

53.9% |

2025 |

By Packaging

Sachet commands a 40.0% majority share in 2025, supported by single-use affordability, low-entry trial pricing, and deep general trade reach across both urban and small-town markets. Its small pack size also enables higher purchase frequency and easy access for price-sensitive consumers.

To access detailed market analysis, Request Sample

Pouch follows at 26.4% in 2025, driven by larger household pack adoption and growing modern trade and online refill purchases. Refill-oriented usage and better value per unit further support repeat purchases among regular consumers.

By Coffee Type

Freeze dried leads with a 65.8% share in 2025, driven by superior aroma retention, premium positioning, and growing acceptance of higher-tier instant coffee in metros. This segment captures the bulk of category value growth as households trade up from spray dried jars.

Spray dried accounts for 34.2% share in 2025, sustained by mass market demand, food service applications, and the value tier where sachet sales remain strong. Cost-effective production keeps spray dried relevant for first-time and price-sensitive buyers.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South India |

53.9% |

Deep coffee-drinking culture, proximity to growing regions, dense manufacturing base, and strong urban household consumption |

|

West and Central India |

22.4% |

Rising urbanization, growing modern retail penetration, expanding cafe and quick-service restaurant footprint, and rising disposable income |

|

North India |

16.8% |

Increasing youth coffee adoption, expanding e-commerce reach, growing premiumization, and rising acceptance of cold coffee formats |

|

East India |

6.9% |

Improving distribution depth, gradual cafe culture expansion, rising aspirational consumption, and growing modern retail penetration |

South India at 53.9% in 2025 leads the country, fueled by long-standing coffee heritage in Karnataka, Tamil Nadu, and Kerala, dense plantation and processing infrastructure, and a mature retail and HoReCa ecosystem that supports both mass and premium tiers.

West and Central India at 22.4% is supported by rising urbanization in Maharashtra and Gujarat, where modern retail and the cafe channel are expanding rapidly. Growing youth demographics and increasing exposure to out-of-home coffee consumption further support demand growth in the region.

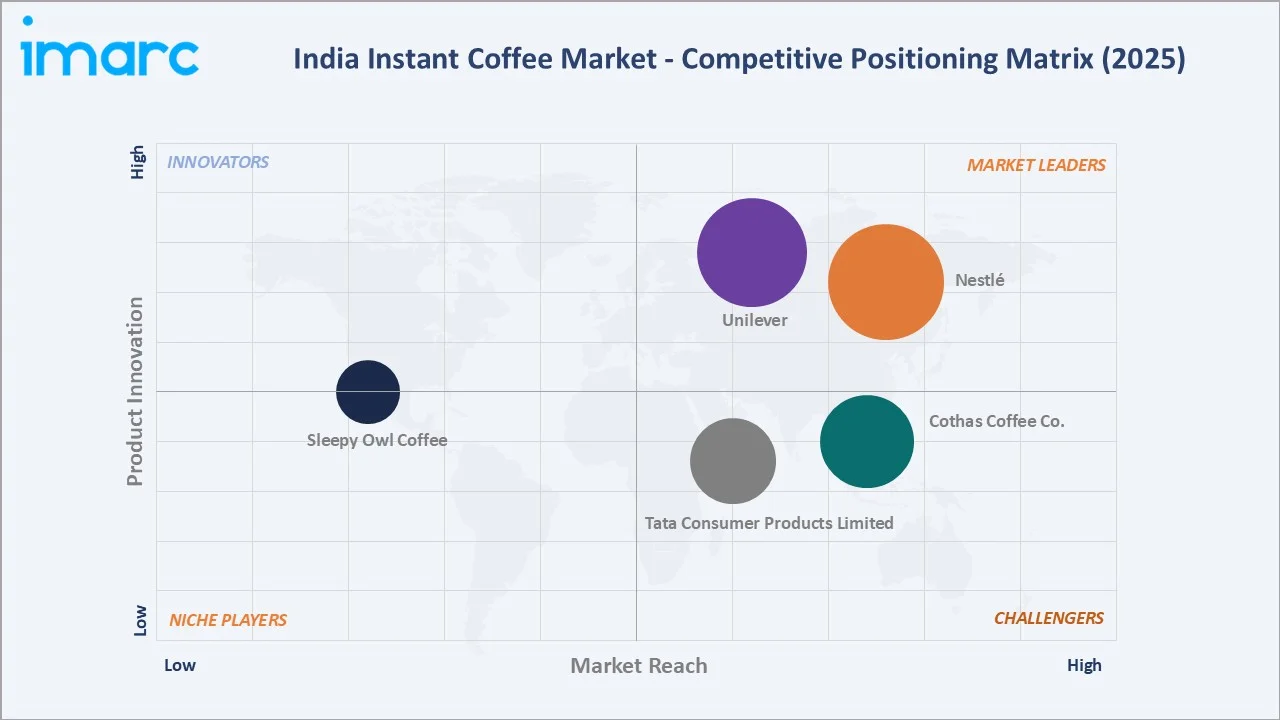

Competitive Landscape

The India instant coffee market is moderately consolidated at the top, with multinational majors leading on brand awareness and distribution, while domestic players hold strong positions in private label, B2B export, and regional retail. Manufacturing scale, blend expertise, and shelf reach form the principal competitive moats.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Nestlé |

Nescafé Classic, Nescafé Gold |

Leader |

Premium portfolio expansion, deep distribution reach, and continued investment in marketing and category innovation |

|

Unilever |

Bru Gold Premium Instant Coffee |

Leader |

Strong household reach across urban and tier 2 cities, value-led pricing, and ongoing premium tier innovation |

|

Tata Consumer Products Limited |

Tata Coffee Grand, Tata Coffee Gold |

Challenger |

Vertically integrated coffee operations, premium tier focus, and growing modern trade and online presence |

|

Cothas Coffee Co. |

Royal Blend, Classic Blend |

Challenger |

Focus on strong regional brand loyalty, consistent quality positioning, and gradual entry into modern trade |

|

Sleepy Owl Coffee |

Dark Roast Instant Coffee, Hazelnut Instant Coffee, French Vanilla Instant Coffee, Original Instant Coffee |

Emerging |

Direct-to-consumer premium positioning, strong online and modern trade play |

Key players include Nestlé, Unilever, Tata Consumer Products Limited, Cothas Coffee Co., and Sleepy Owl Coffee, among others.

Key Company Profiles

Unilever

Unilever, through its Indian subsidiary Hindustan Unilever Limited, markets the Bru brand, which has been a household coffee brand in India for over five decades and remains one of the leading instant coffee brands in the country, particularly strong in South Indian markets.

- Product Portfolio: Bru Gold Premium Instant Coffee at the premium freeze dried tier, supported by Bru Cappuccino across value sachet packs, mid-tier pouches, and premium jars.

- Recent Developments: Bru continues to refresh its premium tier through Bru Gold Premium with periodic packaging upgrades and marketing campaigns highlighting South Indian filter coffee heritage and modern instant coffee occasions.

- Strategic Focus: Family-friendly positioning, broad household reach, value-led mass packs, and steady premiumization through its Gold range across modern trade and e-commerce.

Tata Consumer Products Limited

Tata Consumer Products Limited operates across the coffee value chain, owning plantations in South India and running export-oriented instant coffee manufacturing facilities. The company also leverages its strong domestic distribution network and brand portfolio to expand its presence in the premium and mass instant coffee segments.

- Product Portfolio: Tata Coffee Grand, Tata Coffee Gold, along with a range of instant coffee variants, blends, and formats.

- Recent Developments: In November 2025, Tata Coffee Grand, an instant coffee brand from Tata Consumer Products, launched its new campaign called ‘Not Just Your Regular Coffee’. The campaign depicted Gen Z as a group that could readily share beliefs, challenges traditional norms, and make decisions that reflected their personal identity.

- Strategic Focus: Vertical integration, premium freeze dried portfolio expansion, and synergy with the broader Tata Consumer beverage business across coffee, tea, and water categories.

Sleepy Owl Coffee

Sleepy Owl Coffee, founded in 2016, has emerged as one of India's leading direct-to-consumer specialty coffee brands. The company focuses on premium positioning, innovative formats, and strong digital-first engagement to capture urban, younger consumers.

- Product Portfolio: Dark Roast Instant Coffee, Hazelnut Instant Coffee, French Vanilla Instant Coffee, and Original Instant Coffee, alongside cold brew packs, hot brew bags, ground coffee, and premix coffee.

- Recent Developments: In April 2026, Sleepy Owl Coffee raised USD 1.3 Million in fresh funding to expand distribution, enhance brand recognition, and accelerate product development. It continues to introduce new flavors and formats to cater to evolving consumer preferences and premium consumption trends.

- Strategic Focus: Premium direct-to-consumer positioning, strong digital marketing and content-led brand building, and rapid expansion across modern trade, e-commerce, and quick-commerce channels.

Market Concentration Analysis

The India instant coffee market is moderately concentrated, with the top five companies (Nestlé, Unilever, Tata Consumer Products Limited, Cothas Coffee Co., and Sleepy Owl Coffee) estimated to account for a majority of branded retail share in 2025.

Barriers to entry include large-scale freeze dried and spray dried processing capacity, multi-year retailer relationships, sustained marketing investment, and the brand equity that incumbents have built over decades. These factors favor well-capitalized companies with integrated coffee supply.

Consolidation activity is gradual but visible through portfolio expansions, premium tier launches, joint ventures, and contract manufacturing tie-ups. Scale advantages in sourcing, processing, distribution, and brand investment continue to reinforce the position of leading players in the India instant coffee market.

Investment & Growth Opportunities

Fastest-Growing Segments

Freeze dried at 65.8% is expanding faster than the overall 5.25% market CAGR through 2034, supported by premiumization. Sachet at 40.0% continues to drive new-user acquisition, while pouch is gaining traction for in-home pantry stocking.

Emerging Geographies

East India at 6.9% is the highest-growth regional pocket, with improving distribution and modern retail expansion. North India and West and Central India represent the largest untapped opportunities as cafe culture and youth coffee adoption deepen in tier 2 and tier 3 cities.

Venture & Investment Trends

Investor capital is concentrated in direct-to-consumer instant coffee startups, cold coffee and ready-to-drink players, and sustainable packaging innovation. Investment is also flowing into capacity expansion at established freeze dried processors who serve both domestic brands and export buyers.

Future Market Outlook (2026-2034)

The India instant coffee market is forecast to expand from USD 493.6 Million in 2025 to USD 800.8 Million by 2034 at a CAGR of 5.25%, adding roughly USD 307 Million in incremental annual market value over the forecast period.

Four forces will shape the market through 2034. Premiumization will continue to lift category value through freeze dried, gold, and roastery tiers. Cold coffee and ready-to-drink will broaden the consumption occasion. E-commerce and direct-to-consumer brands will redefine premium discovery. In addition, sustainability requirements will reshape packaging and supply chain choices.

By 2034, instant coffee is expected to be a mainstream daily beverage in a growing share of urban Indian households, with cold formats, single origin instants, and personalized blends emerging as meaningful pockets above the traditional sachet and jar core.

Research Methodology

Primary Research

Primary research included structured interviews with senior brand managers at instant coffee manufacturers, sourcing leads at freeze dried and spray dried processors, modern trade buyers, e-commerce category heads, and HoReCa operators, validating market sizing, regional split, packaging mix, and coffee type evolution.

Secondary Research

Secondary sources included Coffee Board of India statistics, annual reports and investor presentations of listed players, government trade and production data, industry association publications, customs and export databases, and press releases on category launches and capacity additions.

Forecasting Models

Market forecasts used a combination of top-down and bottom-up models, integrating per-capita consumption growth, regional household penetration, average pack size and price evolution, and category mix shifts between freeze dried and spray dried. Scenario analysis addressed bean price volatility and packaging cost evolution.

India Instant Coffee Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Packagings Covered | Jar, Pouch, Sachet, Others |

| Coffee Types Covered | Coffee Types Covered |

| Distribution Channels Covered | Business-To-Business, Supermarkets and Hypermarkets, Independent Retailers, Departmental Stores, Online, Others |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | Nestlé, Unilever, Tata Consumer Products Limited, Cothas Coffee Co., Sleepy Owl Coffee, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India instant coffee market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the India instant coffee market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India instant coffee industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Instant Coffee Market Report

The India instant coffee market was valued at USD 493.6 Million in 2025, supported by rising urbanization, premium freeze dried adoption, and expanding modern retail and e-commerce reach.

The market is projected to grow at a 5.25% CAGR from 2026 to 2034, reaching USD 800.8 Million, supported by premiumization, cafe culture, and rising youth coffee adoption.

Sachet leads at 40.0% in 2025, driven by single-serve affordability and deep general trade reach. Pouch at 26.4% serves regular household buyers preferring larger refill packs.

Freeze dried dominates at 65.8% in 2025, driven by superior aroma retention, premium positioning, and growing metro household acceptance, while spray dried accounts for 34.2%.

South India commands 53.9% in 2025, led by Karnataka, Tamil Nadu, and Kerala, fueled by deep coffee heritage, dense manufacturing, and a mature retail ecosystem.

Leading players include Nestlé, Unilever, Tata Consumer Products Limited, Cothas Coffee Co., and Sleepy Owl Coffee.

Freeze dried preserves aroma and flavor through low-temperature processing, while spray dried uses hot air for faster, cost-efficient production typically used in mass and food service applications.

E-commerce platforms are expanding premium freeze dried discovery, enabling direct-to-consumer brand launches, and supporting larger pack sizes through subscription and recurring purchase models.

Cold coffee mixes, frappe sachets, and ready-to-drink cans are creating a new consumption occasion among Gen Z buyers, with leading players expanding portfolios to address this demand.

Premiumization is shifting consumers toward freeze dried, gold, and roastery variants, lifting category value growth ahead of volume and creating a higher-margin pocket above traditional sachet sales.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)