India Instant Noodles Market Size, Share, Trends and Forecast by Type, Distribution Channel, and Region, 2026-2034

India Instant Noodles Market Size, Share, Trends & Forecast (2026-2034)

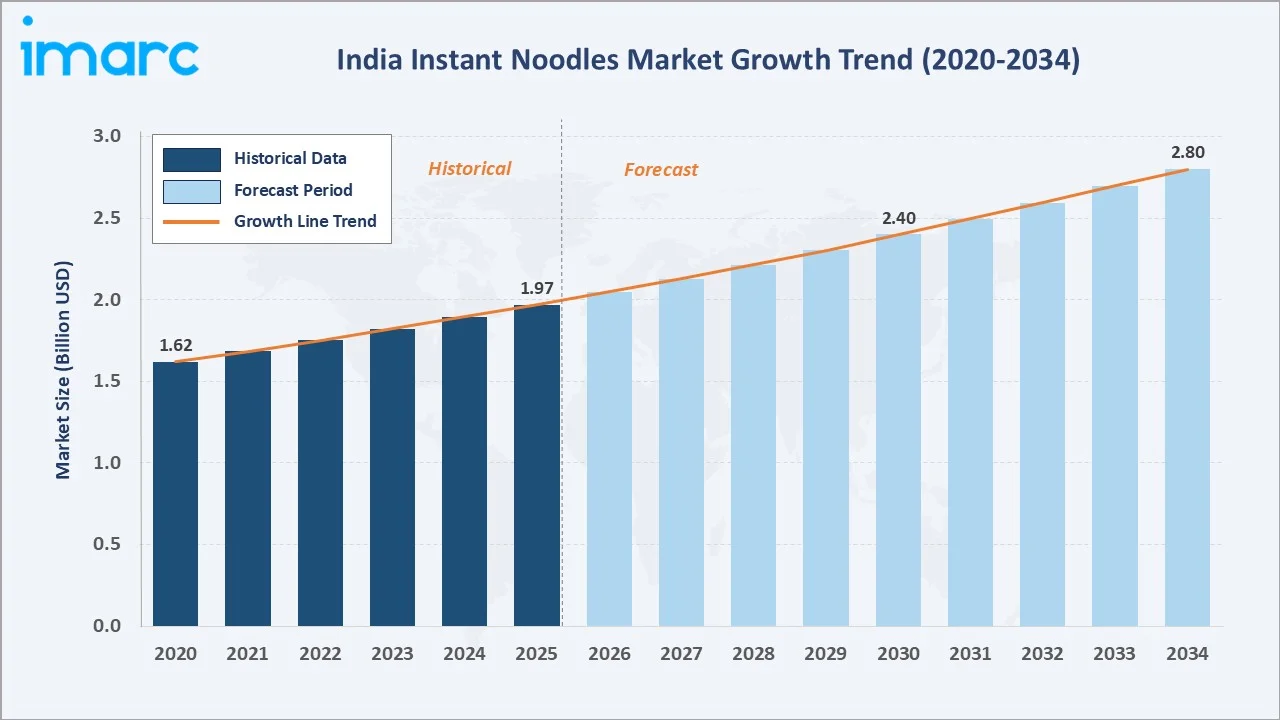

The India instant noodles market reached USD 1.97 Billion in 2025 and is projected to reach USD 2.80 Billion by 2034, growing at a CAGR of 4.01% during 2026-2034. Rising urbanization, nuclear family structures, and the growing working professional population are primary demand drivers. The market has expanded from USD 1.62 Billion in 2020 and is forecast to anchor at USD 2.40 Billion in 2030. Fried noodles dominate with a 70.0% share in 2025. Supermarkets/Hypermarkets lead distribution at 42.0%. North India commands 29.0% of regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.97 Billion |

|

Forecast Market Size (2034) |

USD 2.80 Billion |

|

CAGR (2026-2034) |

4.01% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Fried (70.0%, 2025) |

|

Leading Distribution Channel |

Supermarkets/Hypermarkets (42.0%, 2025) |

|

Leading Region |

North India (29.0%, 2025) |

The India instant noodles market expanded steadily from USD 1.62 Billion in 2020 to USD 1.97 Billion in 2025, underpinned by demand resilience across income segments. The market is forecast to cross USD 2.40 Billion by 2030 and reach USD 2.80 Billion by 2034, reflecting broad-based consumption growth driven by convenience-seeking urban and semi-urban lifestyles.

To get more information on this market, Request Sample

The non-fried segment is the fastest-growing type, driven by health-conscious product reformulation trends. Online stores post the highest CAGR among distribution channels (~7.5%), as quick commerce platforms transform urban retail dynamics. The overall market is expected to record a steady 4.01% CAGR, with premiumization and product diversification shaping growth trajectories across all segments through 2034.

Executive Summary

The India instant noodles market at USD 1.97 Billion in 2025 is one of the most commercially active food convenience segments in the Asia-Pacific region. India ranked third globally in instant noodle consumption, recording approximately 8,320 million servings in 2024. This consumption scale underscores the deep-rooted acceptance of instant noodles as an everyday meal solution across diverse income groups and geographies.

Market growth from 2026 to 2034 will be driven by four structural forces: continued urbanization accelerating demand for convenient meal solutions; expanding e-commerce and quick commerce platforms improving product accessibility; health-driven product innovation attracting new consumer demographics; and aggressive flavor diversification - particularly Korean and regional Indian flavors, sustaining consumer engagement. Non-fried variants and premium products are expected to outpace overall market CAGR during the forecast period.

Fried noodles retain their 70.0% share in 2025, preferred for superior texture, flavor depth, and rapid rehydration. Supermarkets/Hypermarkets command 42.0% of distribution, reflecting organized retail penetration in urban India. North India leads regionally at 29.0%, followed by West India (26.4%), South India (24.8%), and East India (19.8%). The market is projected to reach USD 2.80 Billion by 2034 at a 4.01% CAGR, representing a commercially resilient and innovation-driven consumer category.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Fried - 70.0% share (2025) |

|

Dominant Distribution Channel |

Supermarkets/Hypermarkets - 42.0% (2025) |

|

Leading Region |

North India - 29.0% (2025) |

|

Market Opportunity |

Health-focused variants; Korean-flavor noodles; quick commerce; Tier-2 city expansion |

|

Key Companies |

NESTLÉ S.A., ITC Limited, CG Corp Global, Unilever, and Patanjali Group |

Key Analytical Observations Supporting The Above Insights:

- Fried at 70.0% (2025): The frying process delivers distinctive texture, richer flavors, and faster rehydration. Wide availability at sub-Rs 15 entry price points and mass consumer preference sustain dominant segment leadership through 2034.

- Supermarkets/Hypermarkets at 42.0% (2025): Wide product assortment, multi-brand visibility, bulk-buy promotions, and organized retail penetration in Tier-1 and Tier-2 cities sustain modern trade channel dominance.

- Online Stores fastest growing (~7.5% CAGR): Quick commerce (10-30 minute delivery) is creating incremental demand in urban markets. Multi-pack value bundles, app-only promotions, and subscription models are converting urban millennial households into recurring online buyers.

- North India at 29.0% (2025): High population density, strong spicy masala flavor preference, and well-established distribution networks across metropolitan and semi-urban areas sustain regional market leadership.

- Health-focused innovation as growth catalyst: Millet-based, air-dried, and preservative-free noodles are attracting previously hesitant health-conscious demographics, creating premium niche segments with above-market CAGR potential.

India Instant Noodles Market Overview

The India instant noodles market is positioned at the intersection of scale, convenience, and evolving consumer preference - constituting one of the largest single-country instant noodle markets in Asia by consumption volume. Instant noodles function as a primary meal substitute, a snack option, and an affordable daily convenience food across urban, semi-urban, and rural consumer segments. The category is commercially resilient, anchored in sub-Rs 20 entry-level price points, broad kirana and modern retail distribution, and adaptability to diverse regional taste profiles.

The market ecosystem integrates domestic wheat-based noodle manufacturing, palm oil procurement, regional flavor masala development, multilayer packaging, organized modern trade distribution, and a rapidly growing e-commerce infrastructure. Macroeconomic tailwinds include rising per-capita income, growing urbanization, expanding nuclear families, and time-constrained dual-income households that prioritize convenience. The Production Linked Incentive (PLI) scheme for food processing - supported by the Ministry of Food Processing Industries - is creating structural capacity expansion in the instant noodle manufacturing base.

Market Dynamics

To evaluate market opportunities, Request Sample

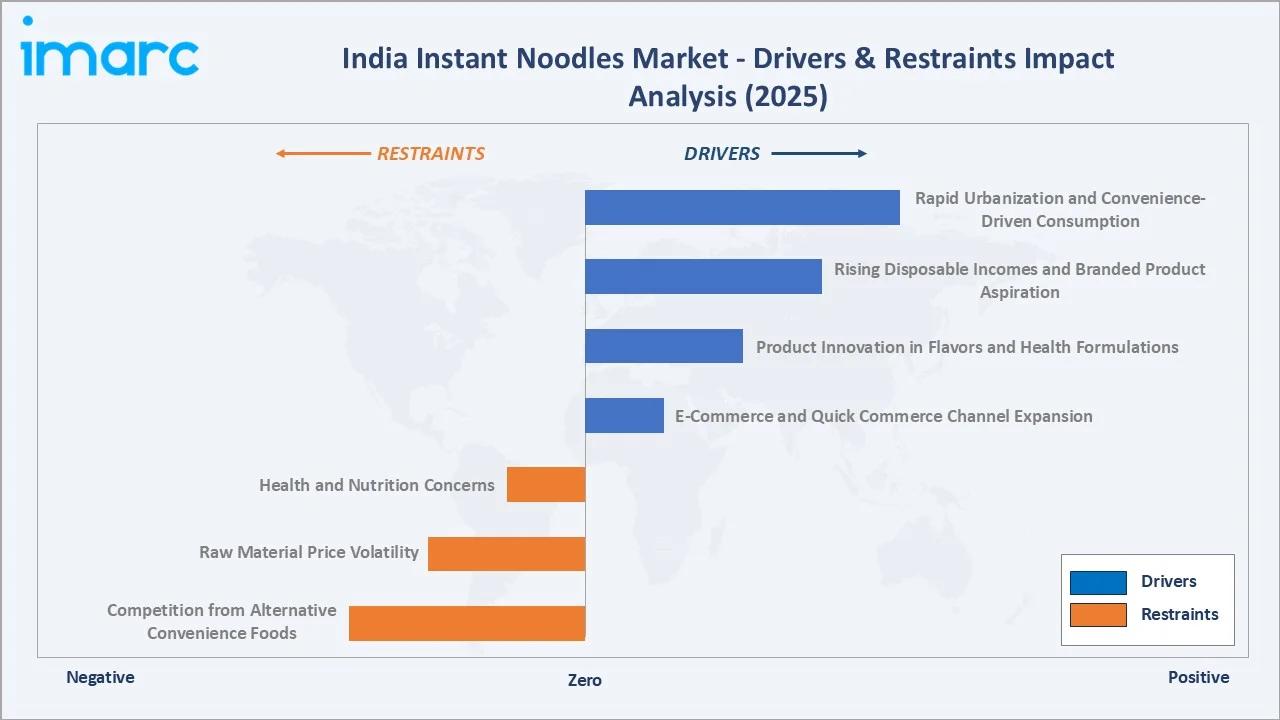

Market Drivers

- Rapid Urbanization and Convenience-Driven Consumption: India's urban population is projected to reach 600 million by 2036. Growing nuclear families, increasing working-professional density, and time-constrained lifestyles in metropolitan and Tier-2 cities are structurally increasing demand for ready-to-cook meal solutions. Instant noodles fulfill this convenience need at accessible price points across income segments.

- Rising Disposable Incomes and Branded Product Aspiration: Household final consumption expenditure reached over Rs 200 trillion in 2024-25. Rising incomes are enabling consumers to trade up from economy to mid-premium instant noodle variants. This income-driven premiumization is supporting above-market-CAGR growth in health-positioned and premium-flavor noodle segments.

- Product Innovation in Flavors and Health Formulations: Manufacturers continuously introduce regional flavor variants, Korean-inspired formats, and health-focused products using millets, whole grains, and reduced sodium content. Innovation attracts new demographic cohorts, particularly health-conscious millennials and Gen Z, while retaining core mass consumers through product variety. This cycle of innovation sustains category engagement and branded product conversion.

- E-Commerce and Quick Commerce Channel Expansion: The explosive growth of quick commerce platforms (Blinkit, Zepto, Swiggy Instamart) and e-commerce marketplaces has materially improved product accessibility in urban markets. E-commerce penetration in food and grocery is expected to reach 10-12% of organized food retail by 2027 (Ministry of Commerce and Industry estimates), driving incremental instant noodle demand above traditional retail channels.

Market Restraints

- Health and Nutrition Concerns: Growing consumer awareness around high sodium content, refined carbohydrates, and artificial flavor preservatives in conventional instant noodles is creating purchase hesitancy in health-conscious urban segments. FSSAI regulatory scrutiny on food additives, labeling requirements, and nutritional disclosure norms adds compliance pressure on manufacturers, particularly for imported and premium variants.

- Raw Material Price Volatility: Instant noodle manufacturers face commodity price cycles in wheat flour (maida), palm oil, and spice ingredients. Wheat price volatility, driven by global supply disruptions and monsoon-dependent domestic harvests, directly affects production costs. Palm oil price fluctuations impact the fried segment disproportionately, compressing manufacturer margins in a price-sensitive consumer market.

- Competition from Alternative Convenience Foods: Ready-to-eat (RTE) and ready-to-cook (RTC) categories, poha mixes, upma mixes, pasta, frozen foods, and meal kits, compete for the same consumer convenience occasion. QSR expansion in Tier-2 and Tier-3 cities creates an out-of-home eating alternative, particularly for the core 18-35 age instant noodle consumer cohort.

Market Opportunities

- Health-Focused and Millet-Based Product Innovation: Demand for millet-based, air-dried, non-fried, and fortified instant noodles represents a commercially under-penetrated premium niche. FSSAI's Eat Right India initiative and government millet promotion under the International Year of Millets 2023 have created consumer receptivity. Manufacturers developing clean-label, preservative-free noodles can command 20-30% premium pricing over conventional SKUs.

- Tier-2 and Tier-3 City Market Penetration: These geographies represent the most commercially underpenetrated instant noodle market. Rising disposable incomes, expanding modern retail infrastructure, and growing branded product aspiration create significant volume growth potential. Distribution network investment in these cities represents a high-return market expansion strategy for major manufacturers.

Market Challenges

- Food Safety Regulatory Compliance: FSSAI quality standards, including labeling requirements, nutritional disclosure norms, and permissible additive limits, require continuous product reformulation and compliance investment. The 2015 Maggi recall, triggered by FSSAI action on MSG and lead content, permanently raised the compliance threshold for all market participants and underscored the material business risk of regulatory non-compliance.

- Unorganized and Local Competition: The category faces competition from unbranded, locally manufactured noodles at sub-economy price points, particularly in rural and semi-urban markets. These products undercut branded manufacturer pricing, limiting market penetration in the most price-sensitive consumer segment and complicating brand premiumization strategies in geographies below Tier-2 classification.

Emerging Market Trends

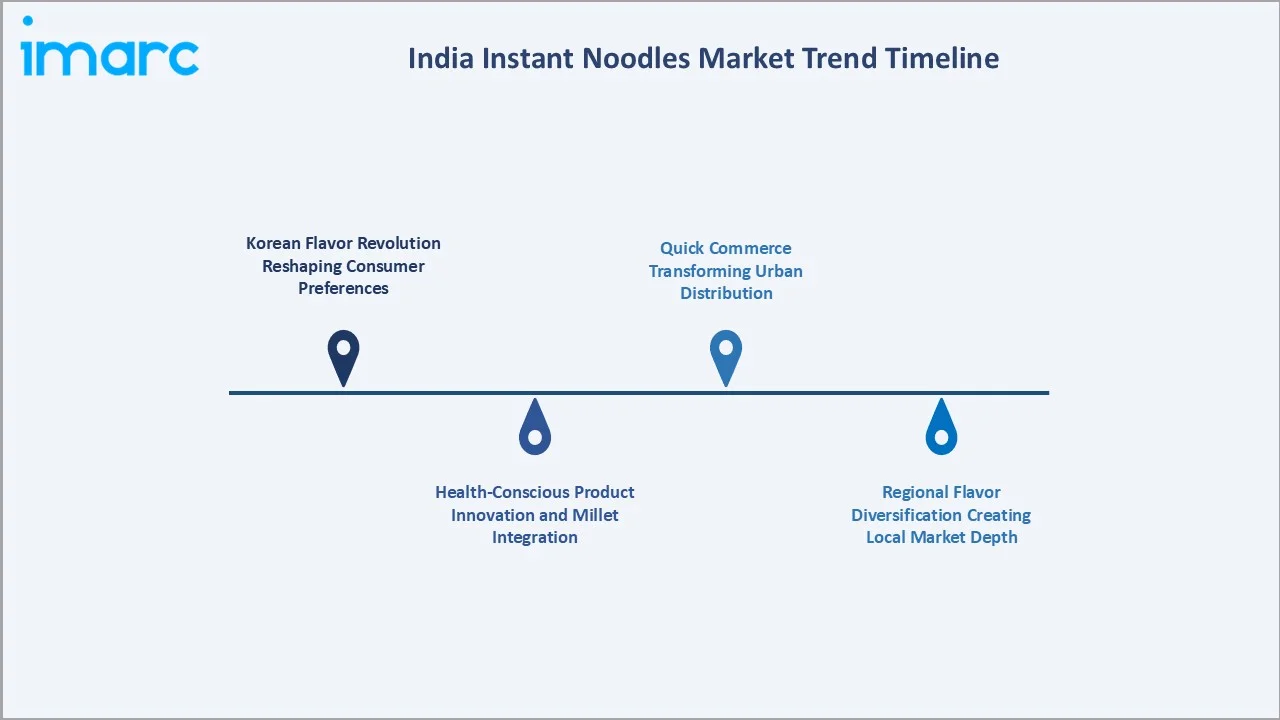

1. Korean Flavor Revolution Reshaping Consumer Preferences

The K-drama and K-pop cultural wave has catalyzed unprecedented consumer demand for authentic Korean-style instant noodles across urban India. Brands are launching dedicated Korean-flavor variants - including Buldak-style spicy ramen - to capture this demand. In October 2024, VRB Consumer Products launched WokTok by Veeba with five Korean-influenced flavors including Spicy Korean. Korean-style instant noodle searches on e-commerce platforms have grown over 200% since 2022, reflecting strong category pull among millennials and Gen Z consumers.

2. Health-Conscious Product Innovation and Millet Integration

Manufacturers are actively reformulating products to incorporate millets, whole grains, oats, and reduced sodium, aligning with India's National Nutrition Mission targets. In September 2023, Slurrp Farm launched preservative-free, air-dried millet noodles for children. Government promotion of millets under the International Year of Millets 2023 initiative has created regulatory and consumer tailwinds for millet-based instant noodle formats, enabling premium pricing of 20-40% above conventional SKUs.

3. Quick Commerce Transforming Urban Distribution

Quick commerce platforms (10-30 minute delivery) are fundamentally reshaping instant noodle purchasing behavior in urban India. Instant noodles are a structurally ideal quick commerce product - compact, non-perishable, high impulse purchase affinity. Platform-exclusive bundle SKUs, app-only promotions, and subscription models are generating incremental volume above traditional retail. Quick commerce is expected to represent 8-10% of urban instant noodle sales by 2027.

4. Regional Flavor Diversification Creating Local Market Depth

Manufacturers are developing state-specific masala variants - Chicken Chettinad, Pav Bhaji, Achari, and Northeast India-inspired flavors - to deepen consumer engagement. This hyper-local flavor strategy is particularly effective in South and East India, where regional taste preferences diverge significantly from the North Indian masala norm, enabling brands to command local market share premiums through authentic taste differentiation.

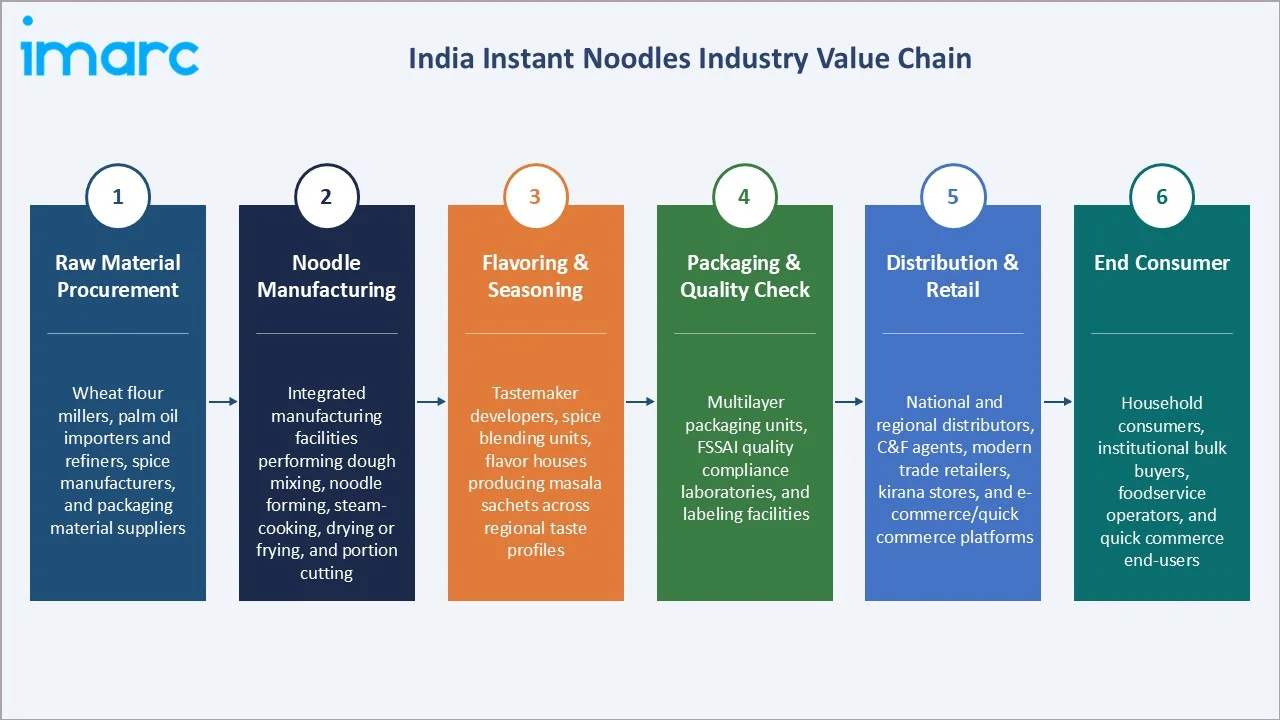

Industry Value Chain Analysis

The India instant noodles value chain is an integrated agri-food processing ecosystem spanning commodity procurement through consumer delivery. The chain's commercial structure creates India's competitive instant noodle dynamic, where large-scale domestic manufacturers compete alongside regional players across a wide price spectrum.

|

Stage |

Key Participants |

|

Raw Material Procurement |

Wheat flour millers, palm oil importers and refiners, spice manufacturers, and packaging material suppliers |

|

Noodle Manufacturing |

Integrated manufacturing facilities performing dough mixing, noodle forming, steam-cooking, drying or frying, and portion cutting |

|

Flavoring & Seasoning |

Tastemaker developers, spice blending units, flavor houses producing masala sachets across regional taste profiles |

|

Packaging & Quality Check |

Multilayer packaging units, FSSAI quality compliance laboratories, and labeling facilities |

|

Distribution & Retail |

National and regional distributors, C&F agents, modern trade retailers, kirana stores, and e-commerce/quick commerce platforms |

|

End Consumer |

Household consumers, institutional bulk buyers, foodservice operators, and quick commerce end-users |

The flavoring and seasoning stage is commercially the most differentiating element. Proprietary masala blends represent core intellectual property of leading manufacturers. Packaging innovation, particularly transition to sustainable multilayer flexible packaging, is an emerging capital expenditure priority driven by EPR regulations under India's Plastic Waste Management Rules (amended 2022).

Technology Landscape in the India Instant Noodles Industry

Air-Drying and Non-Frying Processing Technology

Air-drying technology, using forced hot-air dehydration rather than palm oil frying, is the most commercially significant technological shift in India's instant noodles industry. Non-fried variants produced through air-drying contain 80-90% less fat than conventional fried noodles (per FSSAI nutritional guidelines), enabling manufacturers to position products in the premium health segment. Adoption of air-drying technology is growing at above-industry-average rates, though production costs remain 15-20% higher than conventional frying.

Automation and High-Speed Manufacturing

Leading manufacturers are investing in automated, high-speed noodle production lines capable of producing 1,000-1,500 blocks per minute, significantly reducing per-unit manufacturing cost. Robotic packaging systems, automated quality vision inspection, and continuous manufacturing processes have improved operational efficiency while reducing human error in seasoning portioning. These investments support large-scale manufacturers in defending cost-competitive positions against regional players.

Sustainable Packaging Innovation

Extended Producer Responsibility (EPR) regulations under India's Plastic Waste Management Rules (amended 2022) are compelling manufacturers to transition to recyclable, compostable, or reduced-plastic packaging alternatives. Paper-based cup noodle packaging, single-material polyolefin wrappers, and packaging weight reduction are under active development. NESTLÉ India and ITC have committed to 100% recyclable packaging targets across their food product portfolios.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Fried |

70.0% |

2025 |

|

Distribution Channel |

Supermarkets/Hypermarkets |

42.0% |

2025 |

|

Region |

North India |

29.0% |

2025 |

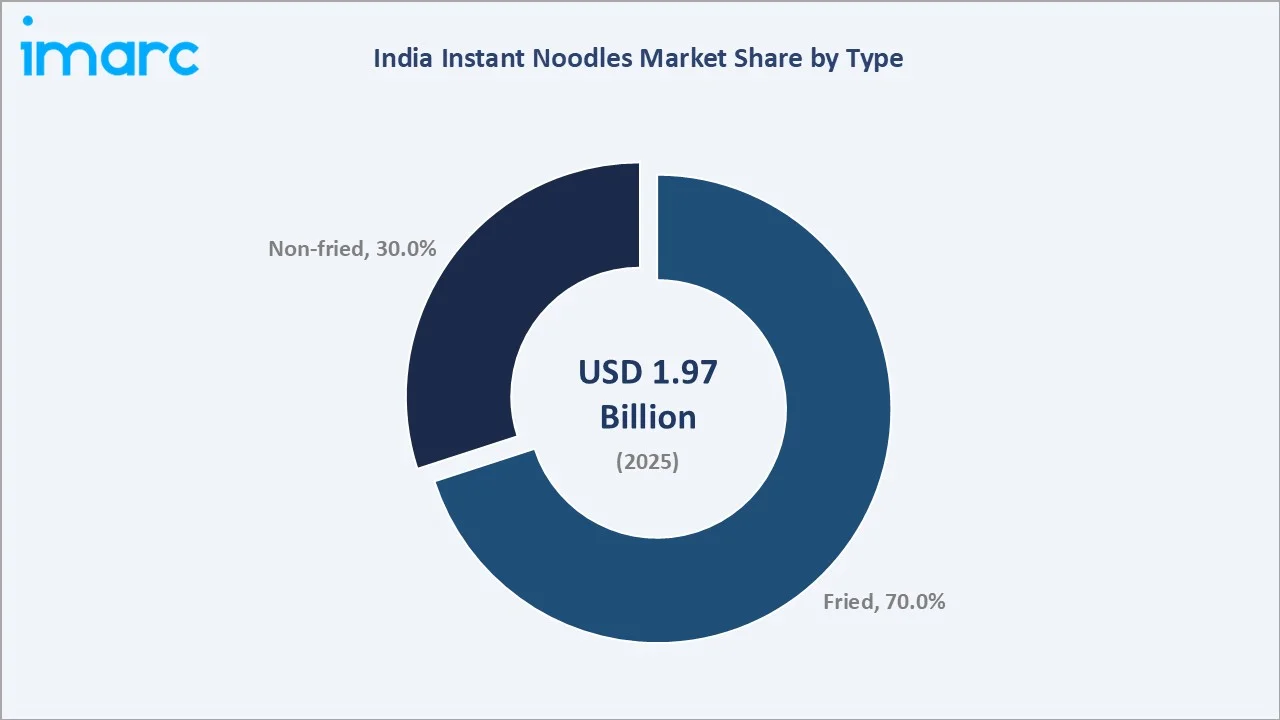

By Type

Fried noodles lead the India instant noodles market with a 70.0% share in 2025. The frying process delivers superior consumer-preferred texture, distinctive crunchiness with rich aroma, and enables faster rehydration during preparation. The segment's dominance is reinforced by sub-Rs 15 entry-level SKUs that maintain affordability across India's price-sensitive consumer base. Major manufacturers including NESTLÉ India (Maggi) and ITC (YiPPee!) have built their mass-market portfolios around fried noodle formats.

To access detailed market analysis, Request Sample

Non-fried noodles at 30.0% represent the fastest-growing type segment, driven by consumer health consciousness and FSSAI regulatory support for nutritionally enhanced food products. Air-dried, steamed, and whole-grain non-fried variants are attracting premium consumers willing to pay 20-40% above conventional fried SKU pricing. The segment's CAGR (~5.8%) is expected to outpace the overall market through 2034, gradually increasing its market share.

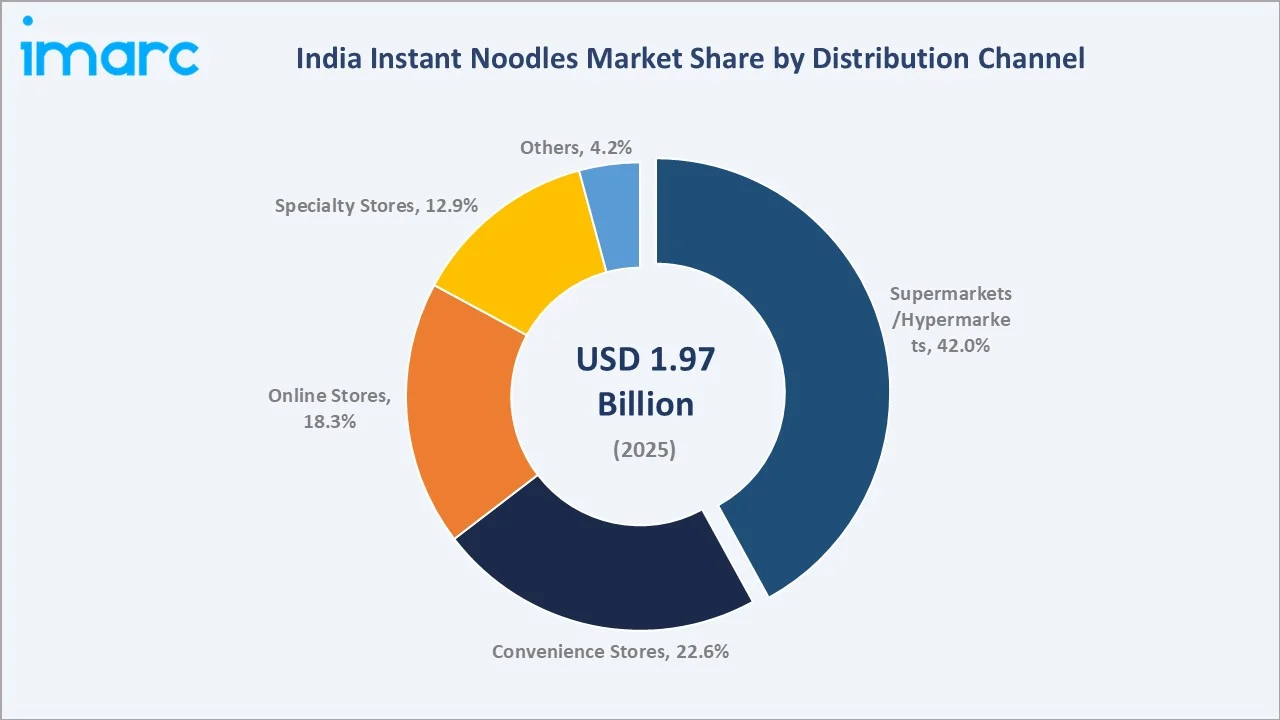

By Distribution Channel

Supermarkets/Hypermarkets command 42.0% of the India instant noodles distribution mix in 2025. Modern organized retail channels offer extensive product assortment, multi-brand visibility, and promotional activity that drives impulse purchase and bulk buying. Key retail chains including D-Mart, Reliance Smart, and organized hypermarket chains have established strong instant noodle shelf positioning across their store networks in Tier-1 and Tier-2 cities.

Convenience stores at 22.6% reflect neighborhood retail proximity in everyday consumption. Online stores at 18.3% are the fastest-growing channel, driven by quick commerce adoption and multi-pack e-commerce bundles. Specialty stores at 12.9% serve niche premium and imported instant noodle demand. Others (kirana stores and foodservice) account for the remaining 4.2%.

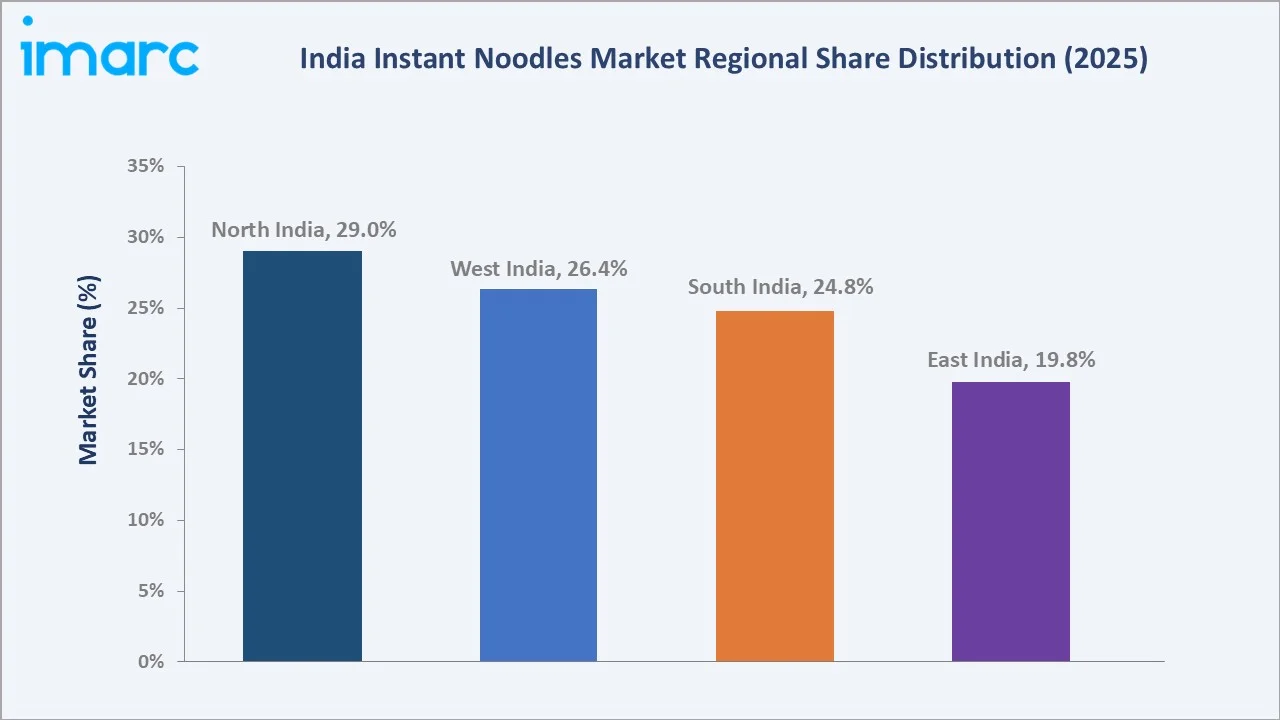

Regional Market Insights

|

egion |

Share (2025) |

Key Characteristics & Drivers |

|

North India |

29.0% |

High population density, strong spicy masala flavor preference, well-established distribution in metro and semi-urban markets |

|

West India |

26.4% |

Urban consumer concentration in Mumbai, Pune, and Ahmedabad supporting branded variant demand; strong modern retail penetration |

|

South India |

24.8% |

Growing demand for regional flavor variants; strong e-commerce adoption in Bengaluru and Hyderabad; health-conscious consumers driving non-fried demand |

|

East India |

19.8% |

Rising per-capita income driving branded product aspiration; growing distribution expansion; demand for Northeast India regional flavor variants |

North India's 29.0% leadership reflects deep-rooted masala noodle preference, led by Maggi's historically strong brand equity in Hindi-speaking markets. West India's 26.4% share reflects Mumbai's dense urban consumer base and broad modern retail penetration. South India at 24.8% demonstrates the strongest growth in non-fried and premium variants, reflecting Bengaluru and Hyderabad's health-conscious IT-sector professional demographics.

East India at 19.8% is commercially the most underpenetrated region relative to population scale, but exhibits above-overall-market growth potential. Rising incomes in Kolkata, Bhubaneswar, and Northeast India's urban centers, combined with strong local flavor preferences in Northeastern states, create structured demand expansion opportunity for manufacturers investing in region-specific product development and distribution infrastructure.

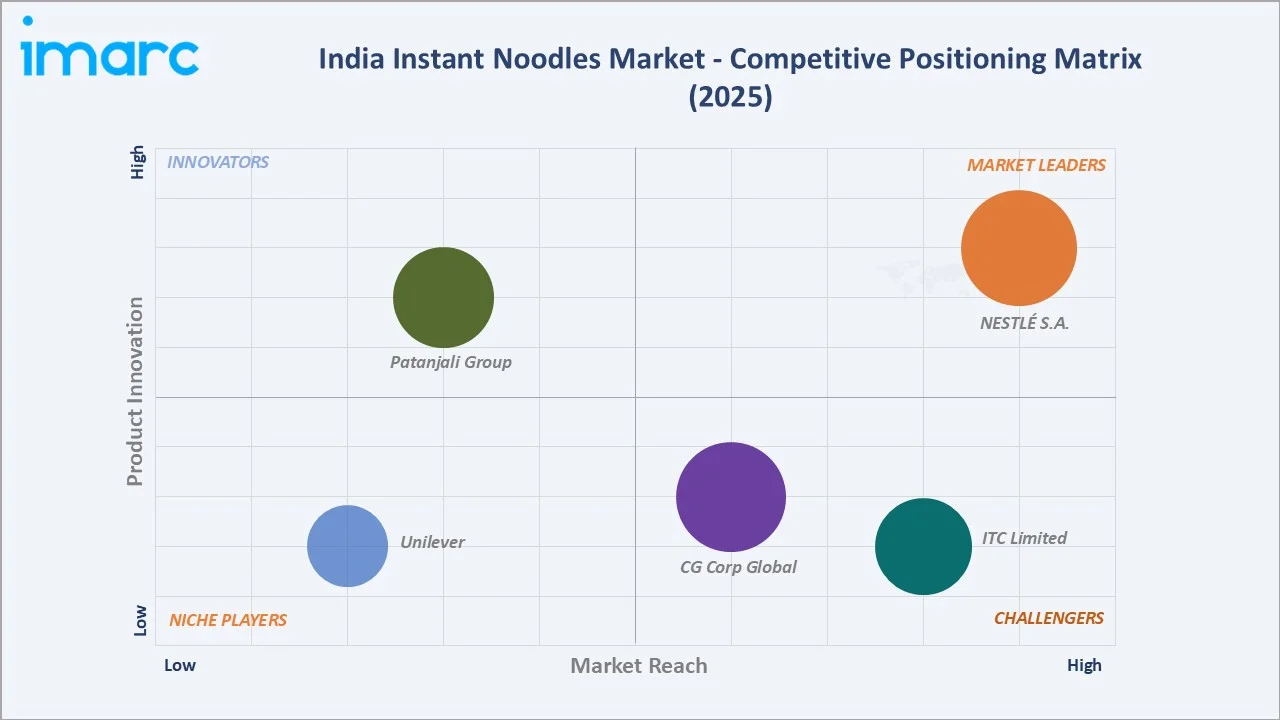

Competitive Landscape

The India instant noodles market operates under a concentrated competitive structure, with NESTLÉ's Maggi brand commanding an estimated 50-55% of the organized branded market by value in 2025 - one of the most dominant single-brand market positions in any Indian packaged food category. ITC's Sunfeast YiPPee! is the primary challenger at approximately 20-25% market share, followed by CG Corp Global's Wai Wai, Unilever's Knorr variants, and Patanjali's Atta Noodles. Competition is intensifying through product innovation, digital marketing, and distribution expansion.

|

Company |

Key Brands |

Market Position |

Core Strength |

|

NESTLÉ S.A. |

Maggi |

Market Leader |

50+ year brand equity and 5 million+ retail touchpoints create unmatched category pull |

|

ITC Limited |

Sunfeast YiPPee! |

Strong Challenger |

Distinctive round block format and aggressive Tier-2 city distribution systematically growing market share |

|

CG Corp Global |

Wai Wai |

Strong Challenger |

Operates CG Foods India Pvt. Ltd., eat-dry snacking format and strong presence in East India and Northeastern states create differentiated occasion |

|

Unilever |

Knorr |

Niche Player |

Operates Hindustan Unilever, premium brand positioning and international flavor repertoire serve the premium urban consumer segment |

|

Patanjali Group |

Patanjali Atta Noodles |

Innovator |

Operates Patanjali Ayurved Limited, whole wheat positioning and Ayurvedic brand association attract health-conscious consumers at accessible price points |

Key Company Profiles

NESTLÉ S.A.

NESTLÉ India, a subsidiary of NESTLÉ S.A., is the dominant player in India's instant noodles market through its flagship Maggi brand, which created India's instant noodles category in 1983. Maggi commands an estimated 50-55% of the organized branded market by value in 2025.

- Key Brands: Maggi 2-Minute Noodles, Maggi Nutri-licious Atta Noodles, Maggi Cuppa, Maggi Oats Noodles, and others.

- Recent Developments: In September 2024, NESTLÉ launched Maggi Happy Bowl atta noodle variants enriched with a source of protein, calcium, vitamin A, and fiber, in two distinctive flavors- 'Yummy Masala' and 'Twisty Tomato'.

- Strategic Focus: Defending market leadership through distribution reach, flavor innovation, and premiumization of the Maggi portfolio into Atta and Oats noodle variants targeting health-conscious consumers.

ITC Limited

ITC's Sunfeast YiPPee! is the primary challenger in India's instant noodles market, achieving approximately 20-25% branded market share through consistent product differentiation and aggressive Tier-2 city distribution investment since its 2010 launch.

- Key Brands: YiPPee! Classic Masala, YiPPee! Saucy Noodles, YiPPee! Mood Masala, and others.

- Strategic Focus: Growing market share in North and East India through distributor network expansion and health-variant premiumization.

Market Concentration Analysis

The India instant noodles market is highly concentrated at the top, with the top two brands (Maggi and YiPPee!) by NESTLÉ and ITC Limited, respectively, commanding an estimated 70-80% of the organized branded market by value in 2025. This duopolistic structure reflects the powerful first-mover advantages, distribution network depth, and brand equity that established players maintain. The unorganized sector, including locally manufactured noodles sold in loose formats, represents an additional 15-20% of total market volume, creating a de-concentration effect at unit volume level.

Market concentration is evolving through two opposing forces: NESTLÉ India's continued portfolio expansion and distribution deepening maintaining structural market leadership, while ITC's systematic distribution investment and product differentiation creates sustained competitive pressure. New entrants from the Korean instant noodle segment (Samyang) are creating premium niche competition without materially threatening the mass market duopoly.

Investment & Growth Opportunities

Highest Growth Segments

Online and quick commerce distribution channels (~7.5% CAGR) are the fastest-growing market access vectors. Tier-2 and Tier-3 city branded market penetration represents the highest-volume incremental opportunity, with an addressable consumer base of 400-500 million in these geographies.

Emerging Investment Opportunities

India's instant noodle investment opportunity is centered on three commercial themes: health-positioned product innovation capturing the premium wellness consumer; regional flavor authenticity creating local market depth and resisting national brand competition; and e-commerce/quick commerce capability building enabling urban market share defense against platform-native brands.

Investment Themes

- Health-focused instant noodle manufacturing investment: Air-drying technology, millet-based formulation, and FSSAI-compliant clean-label manufacturing represent the most commercially defensible premium product investment in India's instant noodles category.

- E-commerce and quick commerce brand building: Platform-exclusive SKU development, influencer-led digital marketing, and subscription-model revenue generation represent the most commercially efficient urban market share acquisition strategy.

- Regional flavor IP development: State-specific masala formulation creates local market differentiation and defensible taste preference positions in South, East, and Northeast India where national masala flavors underperform regional taste preferences.

Future Market Outlook (2026-2034)

The India instant noodles market is projected to grow from USD 1.97 Billion in 2025 to USD 2.80 Billion by 2034, delivering a 4.01% CAGR. The market will anchor at USD 2.40 Billion by 2030, representing a structural growth milestone underpinned by India's urbanization, rising incomes, and continuous product innovation cycles.

Three structural forces define the commercial trajectory through 2034. First, urbanization-driven convenience demand will sustain category growth above India's overall food and beverage market CAGR. Second, product premiumization through health-positioned variants will shift the revenue mix toward non-fried and specialty noodles, improving average selling prices through the forecast period. Third, digital retail channel maturation will create demand pools in geographies previously inaccessible to organized branded distribution.

By 2034, the non-fried segment is expected to represent 38-40% of total market value (from 30.0% in 2025), online channels are forecast to account for 25-28% of distribution (from 18.3% in 2025), and regional flavor variants are projected to represent 30-35% of total SKU-level revenue for major manufacturers - reflecting a structurally more diversified, health-oriented, and digitally accessed market.

Research Methodology

Primary Research

Primary research comprised structured interviews with India instant noodles industry stakeholders, including Supply Chain Directors, Category Managers, Brand Marketing Heads, Key Account Managers of organized retail chains, e-commerce platform category teams, and consumer survey data from instant noodle buyers across North, West, South, and East India. Surveys covered household purchase frequency, brand preference, and channel usage across urban, semi-urban, and rural segments.

Secondary Research

Secondary research encompassed India food processing sector reports from Ministry of Food Processing Industries (MoFPI), FSSAI annual reports and product registration data, company annual reports (NESTLÉ India, ITC Limited), World Instant Noodles Association consumption data, APEDA export-import statistics, organized retail sector reports from Ministry of Commerce and Industry, and e-commerce market analysis. Over 60 secondary sources were reviewed and triangulated for data reliability.

Forecasting Models

Market revenue forecasts were developed using a consumption-based demand model: India's urban and semi-urban household population by income segment multiplied by instant noodle purchase frequency and average transaction value per segment. A convenience food penetration growth model was applied to project category consumption share expansion. Historical data from 2020-2025 was used to calibrate forecast model assumptions and validate CAGR trajectories.

India Instant Noodles Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Fried, Non-fried |

| Distribution Channels Covered | Supermarkets/Hypermarkets, Specialty Stores, Convenience Stores, Online Stores, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | NESTLÉ S.A., ITC Limited, CG Corp Global, Unilever, Patanjali Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Instant Noodles Market Report

The India instant noodles market reached USD 1.97 Billion in 2025, driven by urbanization, convenience demand, product innovation, and expanding distribution channels across organized retail and e-commerce platforms.

The market grows at a CAGR of 4.01% during 2026-2034, supported by health-focused product innovation, quick commerce expansion, and Tier-2 city distribution penetration driving sustained demand growth.

Fried noodles dominate with a 70.0% share in 2025, preferred for superior texture, faster rehydration, and richer flavor profiles aligned with mass consumer preferences across India.

Supermarkets/Hypermarkets lead with 42.0% share in 2025, driven by wide product assortment, multi-brand visibility, and promotional activities attracting urban convenience-seeking consumers.

North India leads with 29.0% share in 2025, driven by high population density, strong spicy masala flavor preference, and well-established branded product distribution networks.

The market is projected to reach USD 2.40 Billion by 2030, reflecting steady growth anchored in urbanization, product premiumization, and expanding digital distribution channels.

Leading companies include NESTLÉ S.A., ITC Limited, CG Corp Global, Unilever, and Patanjali Group, among others.

Health-focused noodle formulations, quick commerce channel expansion, Tier-2 city market penetration, and Korean-flavor variant launches represent the highest-growth investment opportunities.

Rising consumer health awareness, FSSAI nutrition labeling requirements, and government millet promotion are driving non-fried noodle adoption among urban millennial and Gen Z consumers.

Quick commerce platforms are creating incremental demand in urban markets. Online channels are projected to reach 25-28% of total distribution by 2034, up from 18.3% in 2025.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)