India IoT Connectivity Market Size, Share, Trends and Forecast by Component, Application, Enterprise Size, End Use Industry, and Region, 2026-2034

India IoT Connectivity Market Summary:

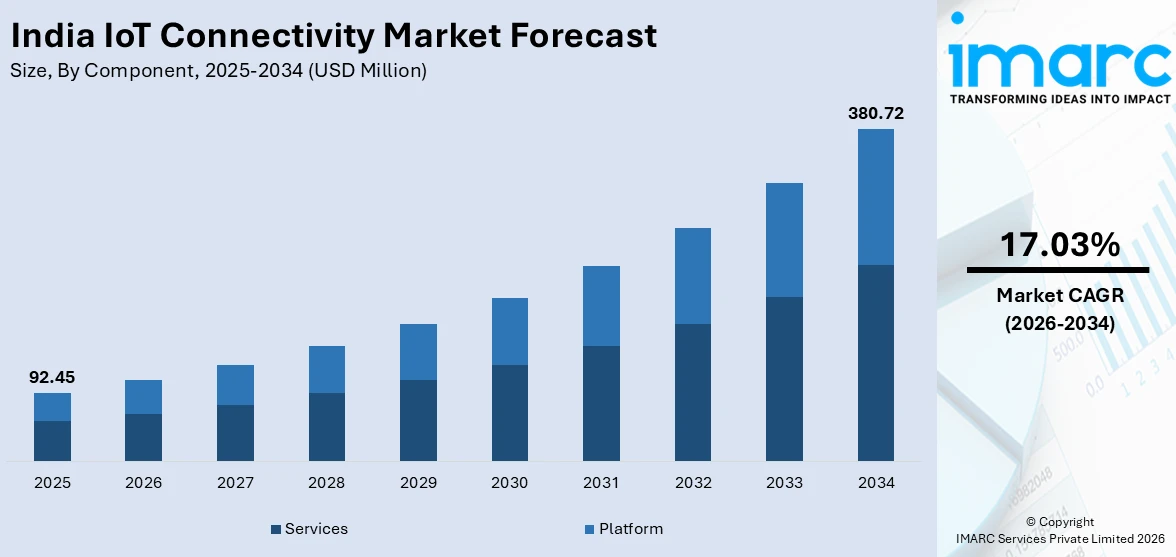

The India IoT connectivity market size was valued at USD 92.45 Million in 2025 and is projected to reach USD 380.72 Million by 2034, growing at a compound annual growth rate of 17.03% from 2026-2034.

The India IoT connectivity market is experiencing growth driven by accelerating digital transformation across industrial and individual user segments. Government-led initiatives promoting smart infrastructure, widespread adoption of next-generation wireless technologies, and increasing enterprise demand for real-time data analytics are reshaping connectivity requirements. The convergence of advanced networking protocols with intelligent device ecosystems is creating unprecedented opportunities across energy, manufacturing, transportation, and healthcare sectors, is propelling the growth of the market.

Key Takeaways and Insights:

- By Component: Services dominate the market with a share of 65% in 2025, driven by the rising demand for managed connectivity solutions, system integration, consulting, and analytics services that enable enterprises to deploy and optimize IoT networks efficiently.

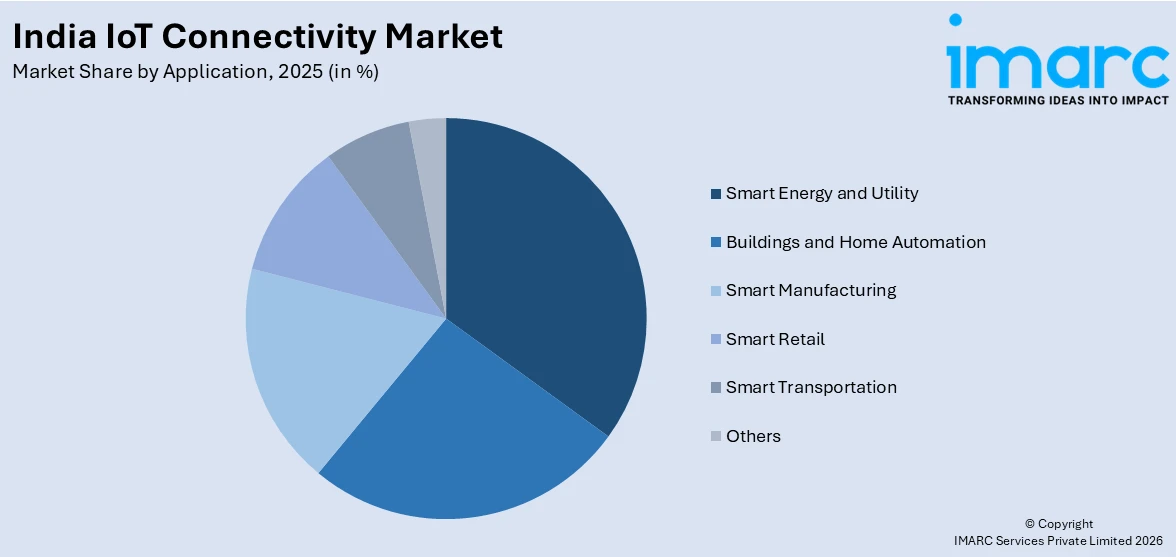

- By Application: Smart energy and utility lead the market with a share of 22% in 2025, propelled by the government’s ambitious smart metering program and the increasing adoption of IoT-enabled grid monitoring and energy management solutions.

- By Enterprise Size: Large enterprises represent the largest segment with a market share of 60% in 2025, owing to their substantial technology budgets, advanced digital infrastructure, and strategic investments in scalable IoT connectivity platforms across operations.

- By End Use Industry: Manufacturing dominates the market with a share of 18% in 2025, supported by the accelerating adoption of Industry 4.0 technologies, predictive maintenance systems, and connected factory solutions across automotive and electronics sectors.

- Key Players: The India IoT connectivity market exhibits moderate competitive intensity, with multinational technology corporations competing alongside domestic telecom operators and IT service providers across enterprise connectivity, platform integration, and managed service segments. Some of the key players in the market include Ericsson, Cisco Systems, Inc., Orange Business Services, Bharti Airtel Limited, and Vodafone.

To get more information on this market Request Sample

The India IoT connectivity market is gaining substantial momentum as the nation undergoes a comprehensive digital transformation spanning industrial, urban, and user ecosystems. Rapid expansion of 4G and 5G networks, rising fiber penetration, and wider availability of low power wide area technologies are enabling seamless machine to machine communication across sectors. Manufacturing units are deploying connected sensors to monitor equipment performance and reduce downtime, while utilities are adopting smart meters for real time energy management. Smart city programs are integrating connected surveillance, traffic control, and waste management systems to improve service delivery. In addition, households are embracing connected appliances, security systems, and wearable devices, driving higher data traffic and SIM activation. A notable development came in 2025, when Jio Platforms launched 10 new 5G standalone network slices across India, creating dedicated virtual lanes for enterprise, IoT, gaming, and fixed wireless access. These SLA backed slices deliver assured, scalable performance for specific applications, supporting advanced IoT deployments and reinforcing the country’s transition toward high performance 5G standalone infrastructure.

India IoT Connectivity Market Trends:

Rise of Satellite-Based IoT Connectivity for Remote Coverage

The rise of satellite IoT solutions is strengthening India’s IoT connectivity market by extending coverage to remote, rural, and geographically challenging areas where terrestrial networks remain limited. Space-based connectivity supports reliable, near real-time data transmission for mission-critical use cases across agriculture, logistics, maritime operations, and environmental monitoring. In 2024, Dhruva Space and France-based Kinéis announced plans to launch a Kinéis IoT payload onboard the Dhruva Space P-30 satellite to enable global space-based IoT connectivity. The collaboration aims to support applications such as forest fire and flood detection, expanding IoT adoption beyond traditional network boundaries.

Indigenous IoT Chip Development Strengthening Domestic Capabilities

India’s focus on building a self-reliant IoT hardware ecosystem is accelerating the growth of IoT connectivity by expanding local device manufacturing and lowering component costs. Indigenous semiconductor development supports wider integration of connectivity modules across consumer and industrial devices, reducing import dependence and supply chain risks. In 2024, IIT Madras-incubated Mindgrove Technologies launched Secure IoT, India’s first indigenously designed and marketed microcontroller chip built on RISC-V architecture and clocked at 700 MHz, priced about 30% lower than comparable alternatives. Targeting wearables, smart appliances, and access control systems, the chip strengthens domestic electronics production and increases the base of connected devices nationwide.

Expansion of Enterprise IoT Management Platforms Across Industries

The growing enterprise demand for centralized IoT device and connectivity management is driving higher adoption of IoT connectivity services in India. Businesses require real-time monitoring, remote troubleshooting, SIM lifecycle control, and analytics-driven insights to manage large fleets of connected assets efficiently. Telecom operators are responding with integrated platforms that simplify deployment and operations at scale. In 2024, Vodafone Idea’s enterprise arm, Vi Business, launched ‘IoT Smart Central’, a self-care IoT connectivity and device management platform for enterprises. The platform provided real-time monitoring, remote SIM lifecycle management, predictive maintenance, and advanced analytics-based billing across sectors, such as automotive, banking, and utilities. It enabled businesses to centrally control and troubleshoot IoT assets, supporting end-to-end lifecycle management from onboarding to ongoing operations.

Market Outlook 2026-2034:

The India IoT connectivity market demonstrates strong growth potential throughout the forecast period, underpinned by accelerating digital infrastructure investments and expanding enterprise adoption of connected technologies. The market generated a revenue of USD 92.45 Million in 2025 and is projected to reach a revenue of USD 380.72 Million by 2034, growing at a compound annual growth rate of 17.03% from 2026-2034. This trajectory is supported by the nationwide deployment of 5G infrastructure, the growing demand for managed IoT services, and expanding applications across smart utilities, manufacturing automation, and urban management systems.

India IoT Connectivity Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Component | Services | 65% |

| Application | Smart Energy and Utility | 22% |

| Enterprise Size | Large Enterprises | 60% |

| End Use Industry | Manufacturing | 18% |

Component Insights:

- Platform

- Services

Services dominate with a market share of 65% of the total India IoT connectivity market in 2025.

Services lead the market because of the growing need for managed connectivity, integration, and ongoing support across complex IoT deployments. Enterprises increasingly rely on service providers for device provisioning, network management, data monitoring, and cybersecurity. As IoT ecosystems expand, organizations require expert assistance to ensure stable connectivity across thousands of distributed devices. Managed services reduce operational burden and allow businesses to focus on core activities. Demand for consulting, system integration, and maintenance contracts continues to rise alongside large-scale IoT rollouts. This recurring revenue model strengthens the share of services within the overall IoT connectivity component landscape nationwide.

Another reason for service dominance is the rapid evolution of connectivity technologies and regulatory requirements. Enterprises seek specialized partners to manage multi-network environments that combine cellular, LPWAN, and satellite connections. Ongoing software updates, troubleshooting, and performance optimization require continuous technical support. Many businesses prefer subscription-based service models that provide predictable costs and scalable solutions. Data security and compliance management further increase reliance on expert service providers. As IoT deployments move from pilot stages to full-scale implementation, long-term service agreements become essential. This sustained need for technical expertise and lifecycle management secures services as the leading component in India’s IoT connectivity market.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Buildings and Home Automation

- Smart Energy and Utility

- Smart Manufacturing

- Smart Retail

- Smart Transportation

- Others

Smart energy and utility lead with a market share of 22% of the total India IoT connectivity market in 2025.

Smart energy and utility hold the biggest market share due to large-scale deployment of smart meters, grid monitoring systems, and energy management platforms. Government programs promoting power distribution reforms and smart city development are accelerating connected infrastructure adoption. Utilities increasingly rely on IoT-enabled devices to track electricity usage, detect outages, and reduce transmission losses in real time. These systems require stable and scalable connectivity solutions across urban and rural networks. The push toward renewable energy integration further drives the demand for connected monitoring tools. Continuous data collection and remote asset control strengthen operational efficiency, making this segment the largest contributor to IoT connectivity demand nationwide.

Another factor supporting this leadership is the growing need for efficient water and gas distribution management. IoT sensors installed in pipelines, storage units, and substations enable predictive maintenance and minimize resource wastage. State utilities and private operators invest in connected platforms to improve billing accuracy and enhance consumer transparency. Low-power wide-area networks and cellular IoT technologies provide reliable coverage for dispersed infrastructure assets. Rising electricity usage and urban expansion increase the need for automated load management systems. The scale of nationwide infrastructure modernization ensures long-term connectivity contracts, reinforcing smart energy and utility as the dominant application within India’s IoT connectivity market.

Enterprise Size Insights:

- Small and Medium-sized Enterprises

- Large Enterprises

Large enterprises exhibit a clear dominance with a 60% share of the total India IoT connectivity market in 2025.

Large enterprises lead the market owing to their substantial investment capacity and complex operational networks. Industries, such as manufacturing, energy, transportation, and telecommunications, deploy large-scale IoT systems to monitor assets, optimize production, and improve supply chain visibility. These organizations require secure, high-volume connectivity solutions capable of supporting thousands of connected devices across multiple locations. Dedicated IT teams and established digital strategies enable faster integration of IoT platforms into existing infrastructure. Strong capital budgets allow long-term contracts with connectivity providers, ensuring stable revenue streams. This scale of deployment positions large enterprises as the primary drivers of IoT connectivity demand nationwide.

Another reason for their dominance is the need for real-time analytics and centralized control across geographically dispersed operations. Large enterprises depend on IoT connectivity for predictive maintenance, fleet tracking, smart facility management, and remote monitoring of critical equipment. Compliance requirements and data security standards further drive them toward advanced, managed connectivity services. Many corporations are also integrating IoT with cloud computing and artificial intelligence to enhance decision-making accuracy. The ability to pilot projects and expand deployments quickly gives large organizations a competitive edge. Continued digital transformation initiatives across core industries reinforce their leading share in India’s IoT connectivity market.

End Use Industry Insights:

- Transportation

- Manufacturing

- Energy and Utilities

- Healthcare

- Retail

- Residential

- Government

- Insurance

- Others

Manufacturing dominates with a market share of 18% of the total India IoT connectivity market in 2025.

Manufacturing represents the largest segment driven by the increasing adoption of smart factory solutions and industrial automation. Connected sensors, machines, and control systems enable real-time monitoring of production lines, equipment health, and inventory levels. Indian manufacturers are investing in IoT connectivity to improve productivity, reduce downtime, and maintain consistent quality standards. Integration of robotics and automated material handling systems further expands the number of connected devices within plants. Reliable connectivity is essential to support data exchange between machines and centralized control platforms. This ongoing shift toward digital manufacturing environments drives significant demand for scalable IoT connectivity solutions nationwide.

Another factor behind manufacturing’s leadership is the push toward predictive maintenance and energy optimization across large facilities. IoT-enabled devices help detect performance anomalies early, reducing unexpected breakdowns and operational losses. Export-oriented industries rely on connected systems to meet global compliance standards and traceability requirements. Government initiatives encouraging domestic production and industrial modernization are also accelerating digital upgrades. Private sector investments in automotive, electronics, pharmaceuticals, and heavy engineering create sustained connectivity needs. The scale and complexity of factory operations require continuous data transmission and secure network management, reinforcing manufacturing as the dominant segment in market.

Regional Insights:

- North India

- West and Central India

- South India

- East India

North India holds a significant share in the IoT connectivity market, driven by the concentration of government institutions, technology enterprises, and advanced healthcare facilities in Delhi and surrounding states. The region benefits from strong telecommunications infrastructure and high digital adoption rates among enterprises. States, including Uttar Pradesh and Haryana are experiencing increasing IoT deployments in smart city infrastructure and industrial automation, supported by robust broadband connectivity and progressive state-level digital transformation policies.

West and Central India holds a prominent position in the market, supported by Maharashtra’s thriving technology ecosystem and Gujarat’s expanding manufacturing base. Mumbai and Pune serve as major hubs for enterprise IoT adoption across financial services, logistics, and industrial automation sectors. The region’s well-developed telecommunications infrastructure, concentration of multinational corporations, and progressive smart city implementations in cities like Ahmedabad and Nagpur are accelerating demand for advanced IoT connectivity solutions.

South India commands a notable market position driven by the technology corridors of Bengaluru, Hyderabad, and Chennai that serve as innovation centers for IoT solution development and deployment. The region’s strong information technology heritage, skilled workforce, and presence of major semiconductor and electronics manufacturing facilities create a conducive ecosystem for IoT connectivity adoption. Karnataka and Tamil Nadu are leading IoT implementation across automotive manufacturing, healthcare, and smart agriculture applications.

East India is emerging as a growing market for IoT connectivity, driven by increasing government investments in infrastructure development and digital inclusion programs across states like West Bengal, Odisha, and Bihar. The region’s expanding industrial base, particularly in steel manufacturing, mining, and agriculture, presents significant opportunities for IoT deployment. Smart metering initiatives and rural broadband expansion under BharatNet are progressively building the connectivity foundation necessary for broader IoT adoption across eastern states.

Market Dynamics:

Growth Drivers:

Why is the India IoT Connectivity Market Growing?

Government-Led Digital Infrastructure Investments Accelerating IoT Deployment

The Indian government’s comprehensive digital transformation agenda is creating a powerful foundation for IoT connectivity market expansion. Strategic initiatives spanning smart city development, energy sector modernization, and industrial digitization are channeling substantial public investment into connected infrastructure. The Smart Cities Mission has been instrumental in driving IoT adoption across urban management systems, with 7,188 projects worth INR 1,44,237 Crore completed across 100 selected cities as of July 2024. Additionally, the Digital India program and policies supporting machine-to-machine communication standards are establishing regulatory frameworks that encourage IoT deployment. These government-led initiatives are reducing barriers to entry, stimulating private sector participation, and creating scalable demand for connectivity platforms across diverse sectors and geographic regions throughout the country.

Nationwide 5G Rollout Enabling Advanced IoT Applications

The rapid expansion of 5G telecommunications infrastructure across India is fundamentally enhancing the capability and reliability of IoT connectivity networks. The ultra-low latency, massive device density support, and significantly higher bandwidth offered by 5G networks are enabling real-time applications in industrial automation, healthcare monitoring, and autonomous transportation that were previously constrained by network limitations. India achieved nationwide 5G coverage across 779 out of 783 districts by October 2024, with over 4.6 lakh base transceiver stations deployed. Furthermore, GSMA’s Mobile Economy Asia Pacific 2024 projects India will have 641 Million 5G connections by 2030, representing nearly half of all mobile connections. This infrastructure buildout is creating a high-performance connectivity layer that supports increasingly sophisticated IoT use cases and drives investment in connected technologies.

Rising Adoption of Smart Consumer Appliances

The growing demand for smart home appliances is accelerating IoT connectivity adoption across India. Individuals are increasingly choosing connected devices that offer remote access, automation, and energy monitoring through mobile apps and cloud platforms. Manufacturers are embedding IoT modules directly into everyday products, expanding the need for reliable wireless connectivity solutions across households. A recent example is Signify’s 2025 launch of its Ecolink BLDC ceiling fans in India, including the AiroGeometry Smart and AiroJewel Smart models, which integrated with the Wiz IoT platform to enable remote control and device automation, reinforcing the expansion of connected ecosystems in residential spaces.

Market Restraints:

What Challenges the India IoT Connectivity Market is Facing?

Connectivity Infrastructure Gaps in Rural and Remote Regions

Despite significant progress in urban telecommunications deployment, substantial connectivity gaps persist in rural and remote areas across India, limiting IoT adoption in agriculture, environmental monitoring, and distributed energy applications. Inadequate broadband penetration, unreliable power supply, and insufficient network coverage in geographically challenging terrains create barriers to deploying IoT solutions in underserved regions. These infrastructure limitations constrain market growth beyond metropolitan centers and restrict the addressable market for connectivity providers.

Data Security and Privacy Concerns Impeding Enterprise Adoption

The growing apprehensions regarding data security, privacy vulnerabilities, and cybersecurity threats associated with interconnected device networks are creating hesitancy among potential enterprise adopters. The proliferation of connected devices across critical infrastructure sectors like energy, healthcare, and manufacturing expands the attack surface for cyber intrusions. Insufficient standardization of security protocols, limited encryption capabilities in legacy devices, and evolving regulatory requirements around data protection are collectively slowing deployment decisions among risk-averse organizations.

High Implementation Costs and Interoperability Challenges

The substantial capital investment required for comprehensive IoT connectivity deployment, including hardware procurement, platform licensing, integration services, and ongoing maintenance, remains a significant barrier for smaller enterprises and budget-constrained organizations. Additionally, the fragmented IoT ecosystem comprising multiple connectivity protocols, proprietary platforms, and incompatible device standards creates interoperability challenges that increase implementation complexity. These cost and compatibility barriers particularly affect small and medium enterprises seeking to adopt connected technologies.

Competitive Landscape:

The India IoT connectivity market exhibits moderate competitive intensity characterized by the presence of global telecommunications corporations, multinational technology providers, and domestic IT service companies competing across connectivity platforms, managed services, and enterprise integration solutions. Market participants are pursuing differentiated strategies ranging from comprehensive end-to-end connectivity offerings to specialized vertical-focused solutions targeting specific industries. Strategic partnerships between telecom operators and cloud service providers are reshaping competitive dynamics by enabling bundled connectivity-analytics solutions. The market is also witnessing increasing activity from innovative startups developing niche solutions for emerging use cases, including satellite-based IoT, low-power wide-area networks, and edge computing-integrated connectivity platforms. Investment in research and development (R&D) capabilities, spectrum acquisition, and network infrastructure expansion remains central to competitive positioning as enterprises demand scalable, secure, and interoperable connectivity solutions.

Some of the key players in the market include:

- Ericsson

- Cisco Systems, Inc.

- Orange Business Services

- Bharti Airtel Limited

- Vodafone

Recent Developments:

- February 2026: Panasonic launched its 2026 residential AC lineup in India, introducing 57 new models with a focus on durability, energy efficiency, and IoT connectivity. The ACs integrate with Panasonic’s MirAIe IoT platform, offering app-based remote control, AI-driven adaptive cooling, energy tracking, and Matter-enabled smart home compatibility.

- February 2025: IoT communications and data analytics startup Probus Smart Things raised USD 5 Million in a Series A1 round led by Unicorn India Ventures, taking its total funding to USD 8 Million. The company planned to use the capital to scale its IoT-based smart grid and smart metering solutions, expand its dual communication modules, and integrate AI into its networking stack.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered | Platform, Services |

| Applications Covered | Buildings and Home Automation, Smart Energy and Utility, Smart Manufacturing, Smart Retail, Smart Transportation, Others |

| Enterprises Size Covered | Small and Medium-sized Enterprises, Large Enterprises |

| End Use Industries Covered | Transportation, Manufacturing, Energy and Utilities, Healthcare, Retail, Residential, Government, Insurance, Others |

| Regions Covered | North India, West and Central India, East India, South India |

| Companies Covered | Ericsson, Cisco Systems, Inc., Orange Business Services, Bharti Airtel Limited, Vodafone, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India IoT Connectivity Market Research Report and Industry Forecast Report

The India IoT connectivity market size was valued at USD 92.45 Million in 2025.

The India IoT connectivity market is expected to grow at a compound annual growth rate of 17.03% from 2026-2034 to reach USD 380.72 Million by 2034.

Services dominate the market with 65% revenue share in 2025, driven by rising enterprise demand for managed connectivity solutions, system integration, and analytics services that streamline IoT deployment and operational management.

Key factors driving the India IoT connectivity market include the rise of satellite IoT solutions that expand coverage in remote and rural regions. In 2024, Dhruva Space and Kinéis partnered to launch a satellite IoT payload enabling near real time connectivity for agriculture, logistics, and disaster monitoring.

Major challenges include connectivity infrastructure gaps in rural and remote regions, data security and privacy concerns among enterprise adopters, high implementation costs for smaller organizations, interoperability issues across fragmented IoT protocols, limited skilled workforce availability, and evolving regulatory frameworks for data governance.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)