India K-12 Education Market Size, Share, Trends and Forecast by Application, Institution, Delivery Mode, and Region, 2026-2034

India K-12 Education Market Size, Share, Trends & Forecast (2026-2034)

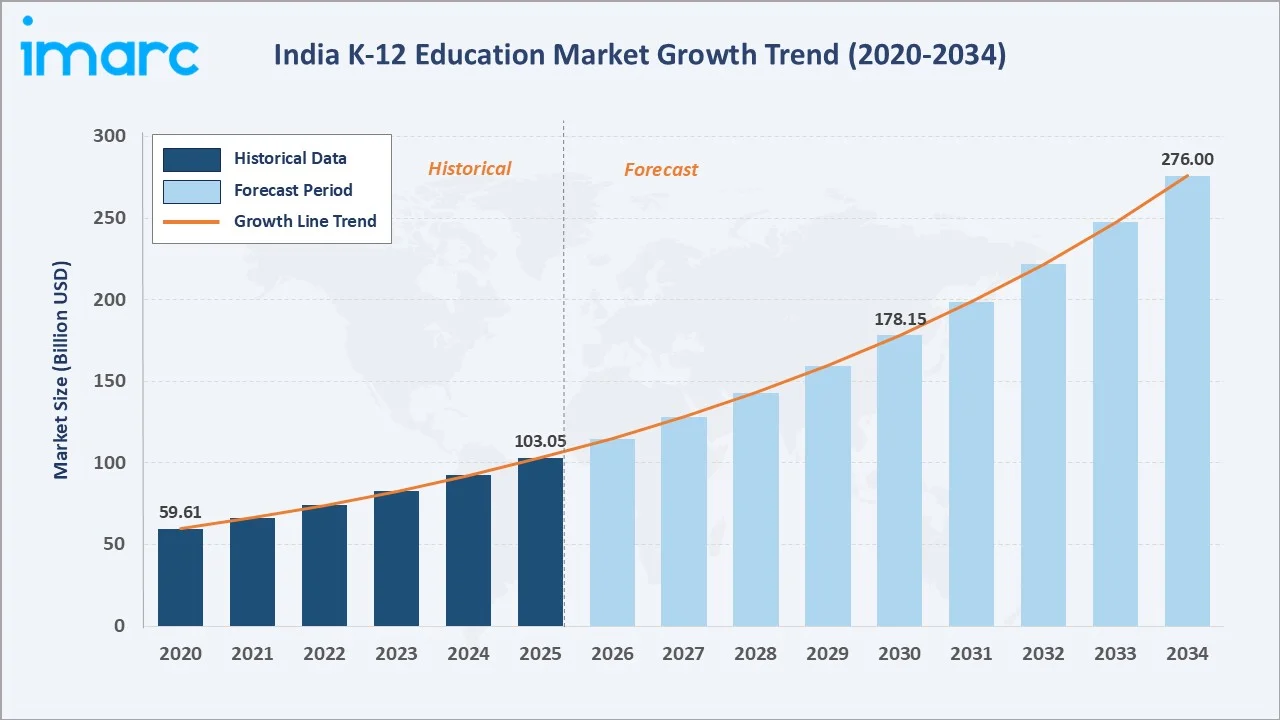

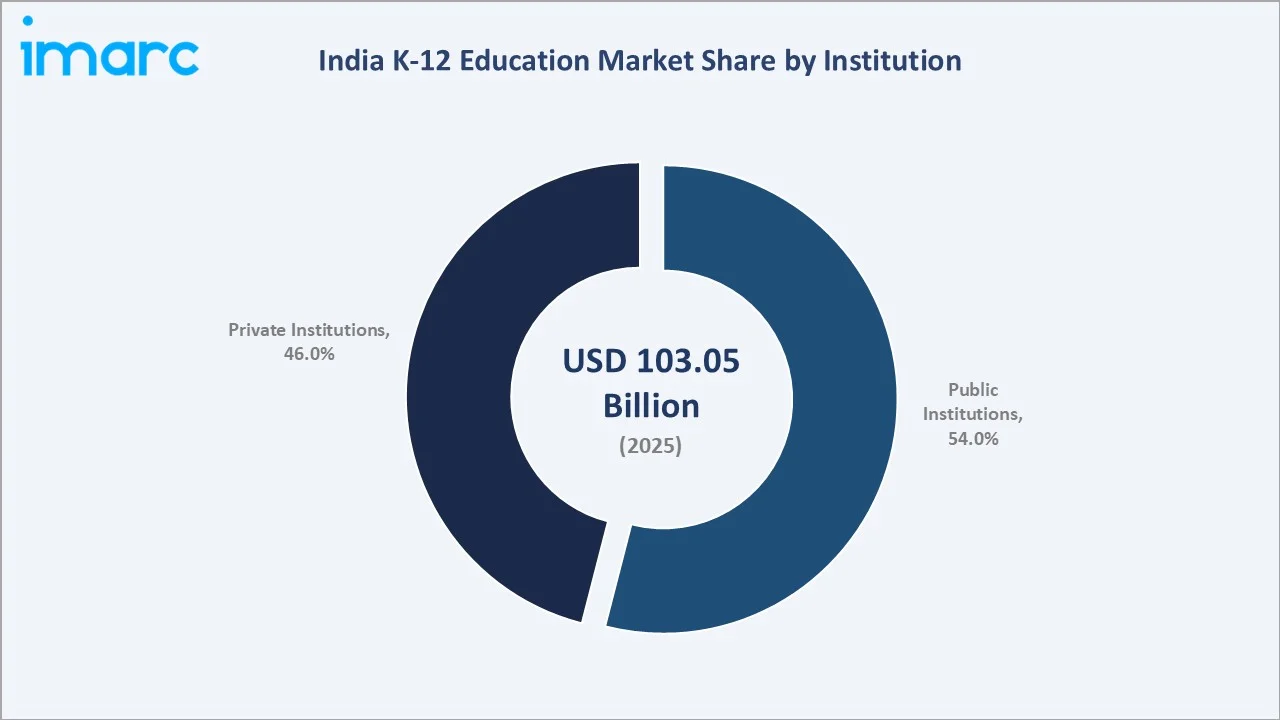

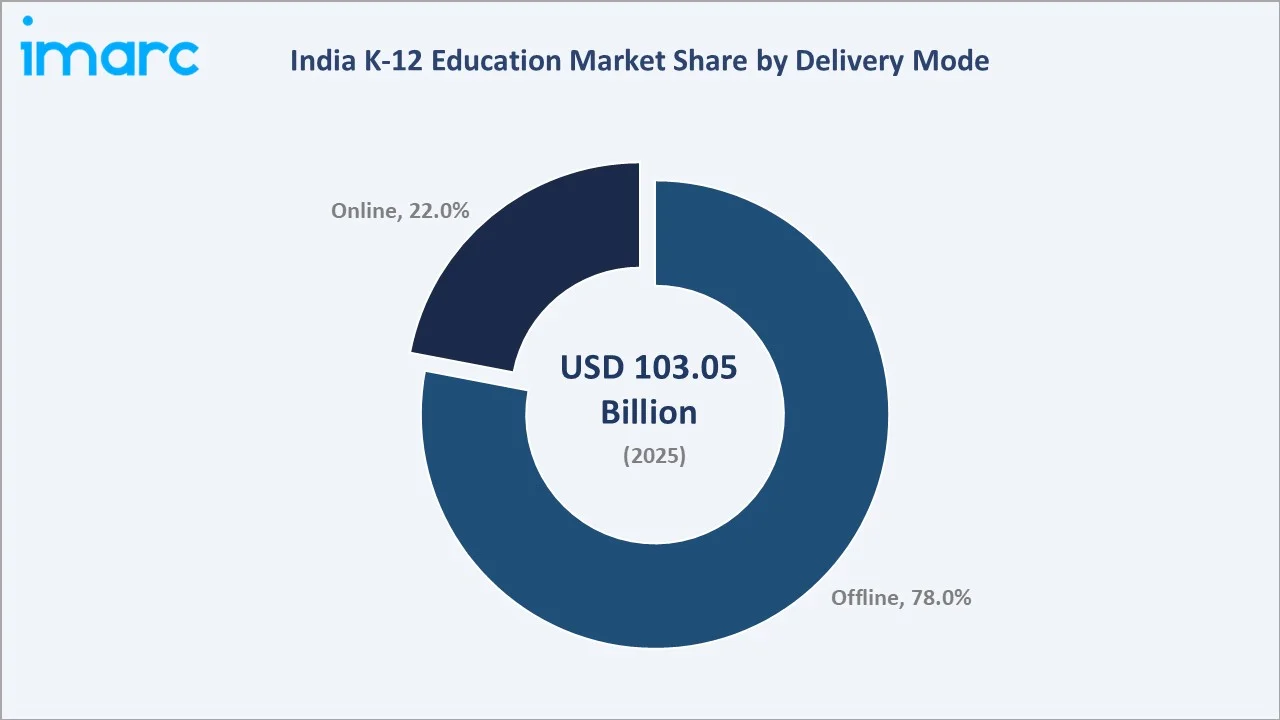

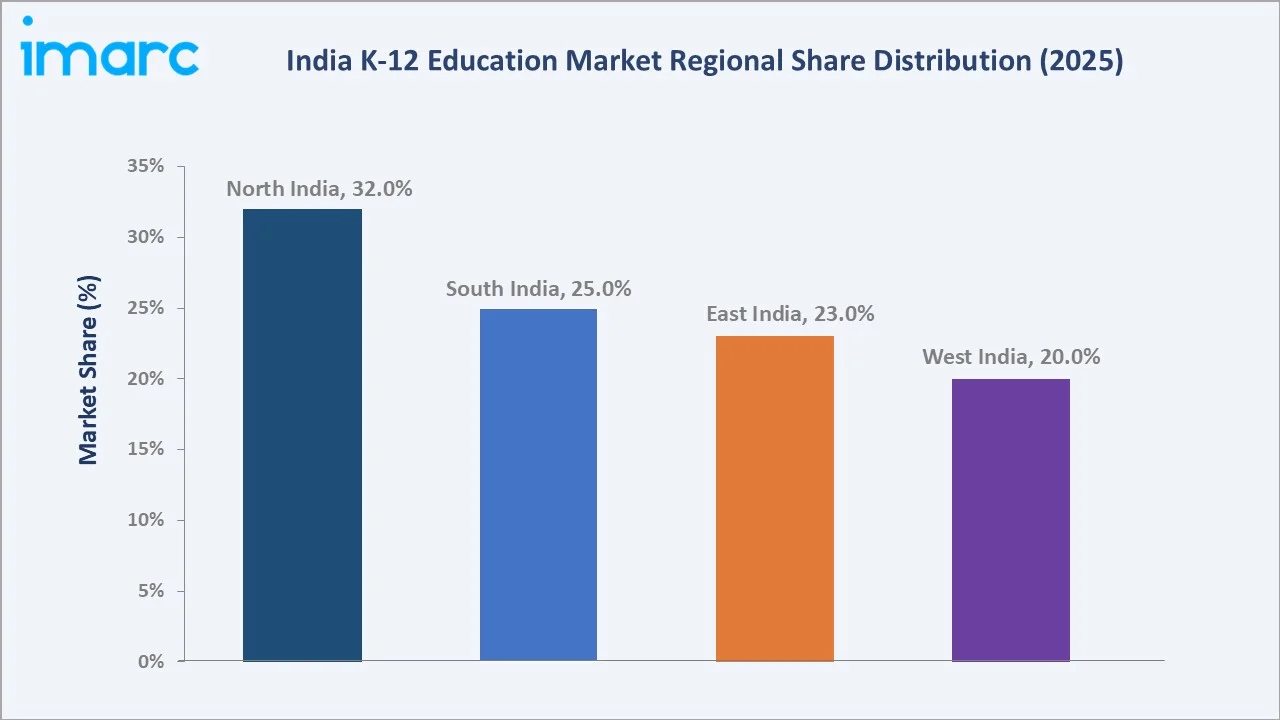

The India K-12 education market was valued at USD 103.05 Billion in 2025 and is projected to reach USD 276.00 Billion by 2034, expanding at a CAGR of 11.57% during the forecast period (2026-2034). Growth is driven by India’s National Education Policy (NEP) 2020 implementation, 260 million-strong K-12 student population across 1.5 million schools, rising household income spurring private school enrollment, and post-COVID EdTech adoption normalization. Public institutions lead with 54% share, while offline delivery dominates at 78%. North India commands 32% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 103.05 Billion |

|

Forecast Market Size (2034) |

USD 276.00 Billion |

|

CAGR (2026-2034) |

11.57% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Region |

North India (32.0%, 2025) |

|

Fastest Growing Region |

East India (CAGR ~11.9%, 2026-2034) |

The India K-12 education market growth expanded from USD 59.61 Billion in 2020 to USD 103.05 Billion in 2025, driven by COVID-19 digital acceleration, post-pandemic private school fee recovery, and NEP 2020 implementation investments. Anchored at USD 178.15 Billion in 2030, the forecast to USD 276.00 Billion by 2034, supported by India’s demographic dividend and rising per-capita income, driving quality education spending.

To get more information on this market, Request Sample

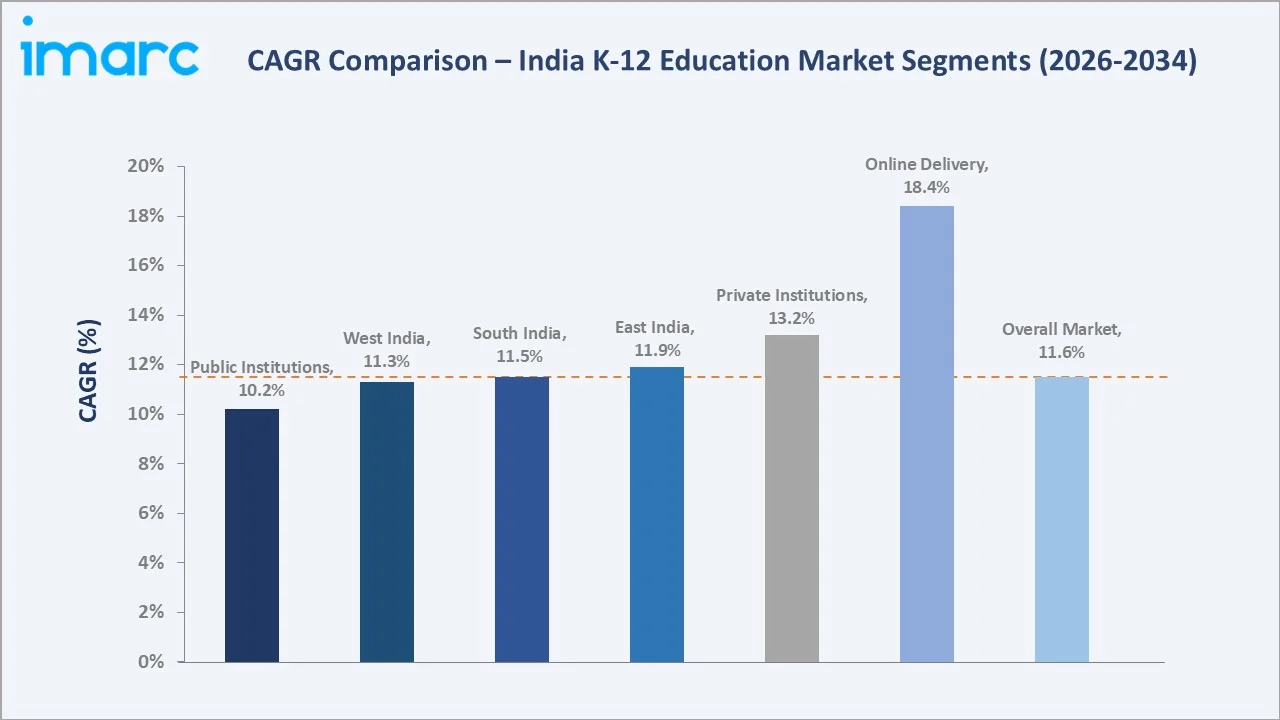

The CAGR across key segments with online delivery at ~18.4% CAGR grows fastest, reflecting India’s 750 million+ active internet users adopting EdTech for supplementary learning, competitive exam preparation, and hybrid school models. East India at ~11.9% CAGR outpaces the national average, driven by rising literacy investments in West Bengal, Odisha, Bihar, and Jharkhand under government flagship programs and private school expansion into Tier 2 cities.

Executive Summary

The India K-12 education market has expanded from USD 59.61 Billion in 2020 to USD 103.05 Billion in 2025, driven by post-COVID EdTech adoption, NEP 2020 implementation catalyzing curriculum reforms, rising private school fee premiums as India’s middle class aspires to quality education, and government’s Samagra Shiksha scheme covers 1.16 million schools, over 156 million students and 5.7 million Teachers of Govt. and Aided schools. India’s K-12 market is uniquely positioned: with 260 million K-12 students, 1.5 million schools, and a demographic dividend of youth under 25 years, the structural demand for quality K-12 education is one of the most durable and policy-anchored growth stories in education markets. The market’s 11.57% CAGR forecast to USD 276.00 Billion by 2034 reflects the convergence of rising household incomes, NEP 2020’s systematic shift toward competency-based learning, and EdTech’s growing share of supplementary education spending.

Public institutions at 54% represent India’s vast government school ecosystem serving students in free or nominally priced education, generating revenue from government capital expenditure on school infrastructure, digital transformation, mid-day meal programs, and teacher salaries. Private institutions at 46% are growing at ~13.2% CAGR as India’s growing middle class increasingly prioritizes private CBSE and international curriculum schools for perceived quality differentiation. Offline delivery’s 78% dominance reflects India’s 1.5 million physical schools’ persistent centrality, while online at 22% is growing at 18.4% CAGR, the fastest segment, as smartphone penetration, with approximately 85.5% of households possessed at least one smartphone, and affordable data costs enable rural EdTech adoption.

North India’s 32% dominance reflects the Indo-Gangetic Plain’s population concentration and Delhi-NCR’s premium private school market. East India at 23% is growing fastest at ~11.9% CAGR as Bihar, Odisha, and West Bengal’s rapidly expanding private school sector and government school digital transformation programs create the market’s highest incremental demand growth.

Key Market Insights

|

Insight |

Data |

|

Dominant Institution Type |

Public – 54.0% revenue share (2025) |

|

Dominant Delivery Mode |

Offline – 78.0% revenue share (2025) |

|

Leading Region |

North India – 32.0% revenue share (2025) |

|

Fastest Growing Region |

East India (CAGR ~11.9%, 2026-2034) |

Key analytical observations supporting the above data:

- Public institutions at 54% driven by government education expenditure scale: The Ministry of Education’s total budget allocation has increased to ₹128,650 crore, reflecting a 6.22% rise compared to the Budget Estimates for 2024-25, represents the dominant funding source for K-12 market revenue, with Samagra Shiksha scheme, PM SHRI Yojana’s INR 27,360 crore, and state-level education budgets collectively creating systematic government investment.

- Offline delivery at 78% reflecting school system’s physical infrastructure anchoring: India’s 1.5 million schools represent a high investment in physical infrastructure (land, buildings, furniture, labs) that structurally anchors offline learning as the primary K-12 delivery mode.

- North India at 32% anchored by population size and Delhi-NCR premium school market: Uttar Pradesh’s schools (India’s largest state school system) and Bihar’s schools collectively generate high K-12 market revenue.

India K-12 Education Market Overview

India’s K-12 education market encompasses all formal and supplementary education services for children from Kindergarten (age 3–6) through Grade 12 (age 17–18), including government school systems, private unaided and aided schools, international curriculum schools, EdTech supplementary learning platforms, private tutoring and coaching centres, educational publishing, and digital learning infrastructure. The ecosystem integrates government schools, private schools, EdTech platforms, educational publishers, and regulatory bodies under the overarching governance of the Ministry of Education’s National Education Policy 2020.

Applications encompass foundational literacy and numeracy, subject depth and STEM development, and board examination and competitive entrance preparation. Macroeconomic influences include India’s GDP growth, increasing household education spending, demographic dividend, urbanization creating private school demand in Tier-2/3 cities, NEP 2020’s curriculum reforms generating new EdTech content demand, and government Samagra Shiksha and PM SHRI Yojana investment systematically upgrading the public school ecosystem.

Market Dynamics

To evaluate market opportunities, Request Sample

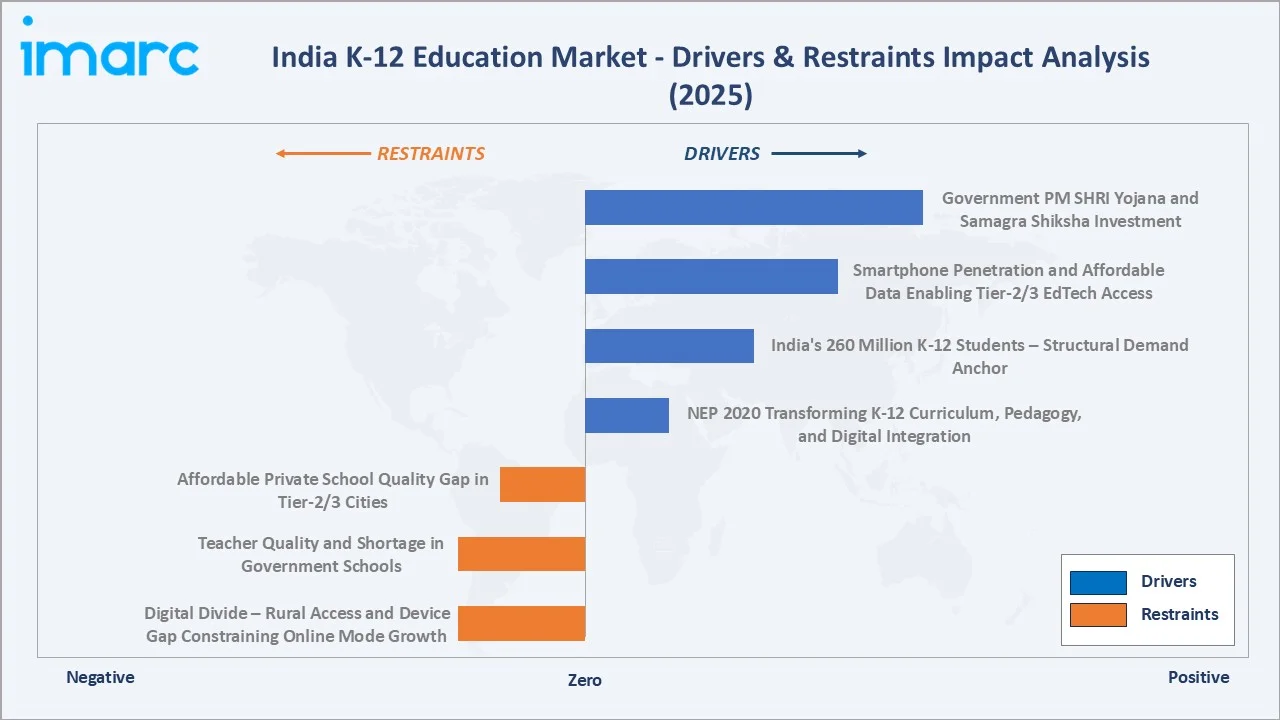

Market Drivers

- NEP 2020 Transforming K-12 Curriculum, Pedagogy, and Digital Integration: India’s National Education Policy 2020, the first comprehensive education reform in 34 years, is systematically transforming the K-12 ecosystem through three structural interventions: the 5+3+3+4 foundational-preparatory-middle-secondary pedagogical framework replacing the existing 10+2 structure; mother tongue medium of instruction mandate through Grade 5 creating multi-language content demand for EdTech and publishers; and competency-based assessment framework (PARAKH) replacing rote memorization board examinations.

- India’s 260 Million K-12 Students – Structural Demand Anchor: India’s 260 million K-12 enrolled students across 1.5 million schools, the world’s largest by enrolment, generate structural annual demand for educational services that grows predictably with India’s birth rate.

- Smartphone Penetration and Affordable Data Enabling Tier-2/3 EdTech Access: India, with approximately 85.5% of households possessed at least one smartphone, combined with JIO’s data revolution, has created the world’s most democratized mobile EdTech access environment.

Market Restraints

- Digital Divide – Rural Access and Device Gap Constraining Online Mode Growth: India’s 60% rural population face persistent barriers to online K-12 learning adoption: rural homes have no smartphone; electricity supply in rural India averages 20–22 hours per day; internet connectivity in rural India averages 25–40 Mbps insufficient for BYJU’S and Vedantu’s HD video streaming.

- Teacher Quality and Shortage in Government Schools: India’s government mentioned a shortage of 7,22,413 teachers at the elementary level and 1,24,262 teachers at the secondary level. This teacher quality and quantity deficit constrains the public-school system’s ability to deliver NEP 2020’s competency-based learning outcomes.

Market Opportunities

- Government School Digital Transformation Under PM SHRI and NDEAR: PM SHRI Yojana’s INR 27,360 crore program to transform 14,500 schools into National Education Policy model schools, including smart classrooms, digital labs, coding labs, and teacher professional development, creates an EdTech and digital infrastructure procurement opportunity concentrated in government schools.

- AI-Powered Personalized K-12 Learning at Scale: India’s 260 million K-12 students represent the world’s largest single-market opportunity for AI-driven personalized learning, where machine learning recommendation engines, natural language processing in Indian languages, and adaptive assessment algorithms can deliver individualized learning pathways impossible in 40–60-student physical classrooms.

Market Challenges

- Affordable Private School Quality Gap in Tier-2/3 Cities: India’s affordable private schools charging INR 5,000–25,000 annually, the segment serving India’s aspirational lower-middle-class families, face the most acute quality crisis, suggesting a quality gap versus fee-adjusted expectations.

- Rural EdTech Last-Mile Infrastructure and Content Relevance: India’s rural K-12 EdTech penetration is constrained beyond connectivity by content relevance. BYJU’S and Vedantu’s content are primarily in English and CBSE curriculum, while most of India’s rural K-12 students are in state board medium-of-instruction schools (Hindi, Telugu, Tamil, Kannada, Marathi, Bengali).

Emerging Market Trends

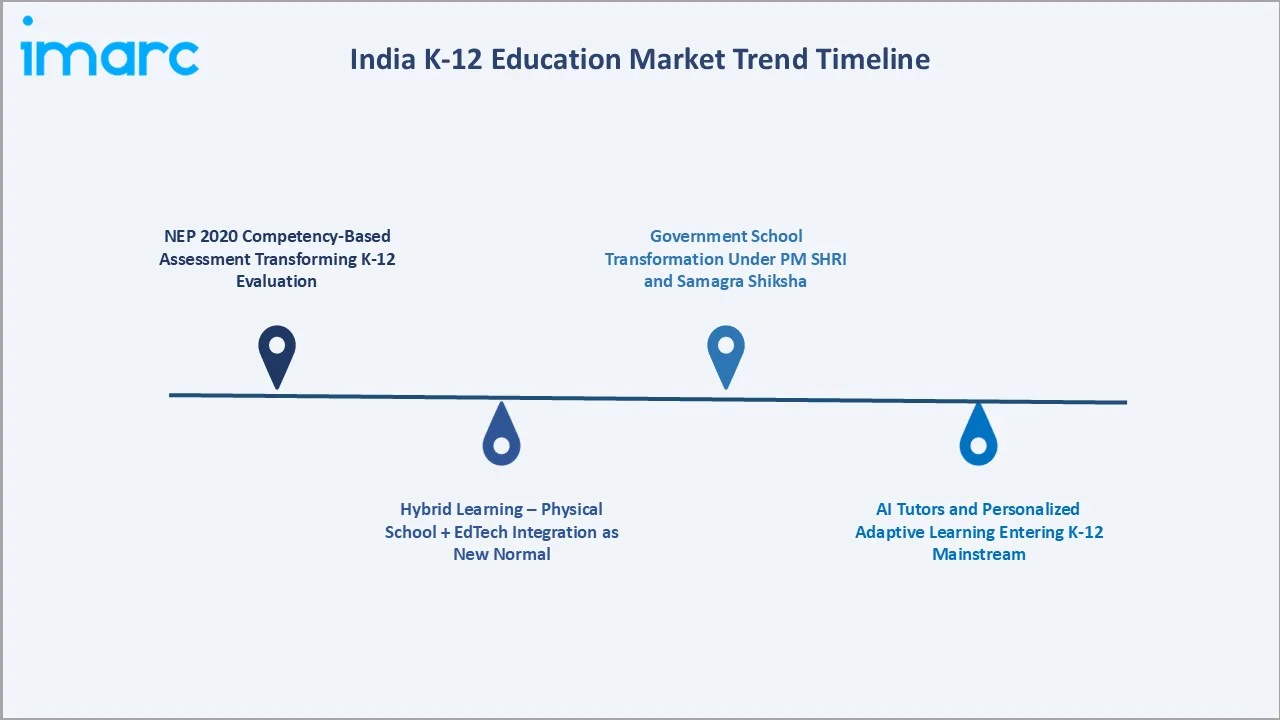

1. NEP 2020 Competency-Based Assessment Transforming K-12 Evaluation

India’s PARAKH (Performance Assessment, Review and Analysis of Knowledge for Holistic Development) framework under NEP 2020 is replacing the traditional 100-mark final examination model with continuous, competency-based portfolio assessment from Grade 3 onwards.

2. Hybrid Learning – Physical School + EdTech Integration as New Normal

India’s K-12 market is converging on a hybrid model where physical school attendance integrates with EdTech supplementation rather than online-only or offline-only binary choices. Most of urban India’s K-12 students simultaneously attend physical schools and use 1–2 EdTech platforms for supplementary learning.

3. AI Tutors and Personalized Adaptive Learning Entering K-12 Mainstream

Large language model-powered AI tutors, capable of answering student questions in Hindi, Telugu, Tamil, and 10+ Indian languages in real time, are entering India’s K-12 market as the transformative technology of the 2026–2030 period.

4. Government School Transformation Under PM SHRI and Samagra Shiksha

India’s government school transformation programs are converting the public system from a low-quality enrollment anchor into a technology-enabled, quality-competitive institution for the first time in India’s post-independence history. PM SHRI Yojana’s over 14,500 model schools, each receiving infrastructure funding and mandatory digital lab, coding lab, and smart classroom installation, are creating a tier of government schools competitive with mid-market private schools.

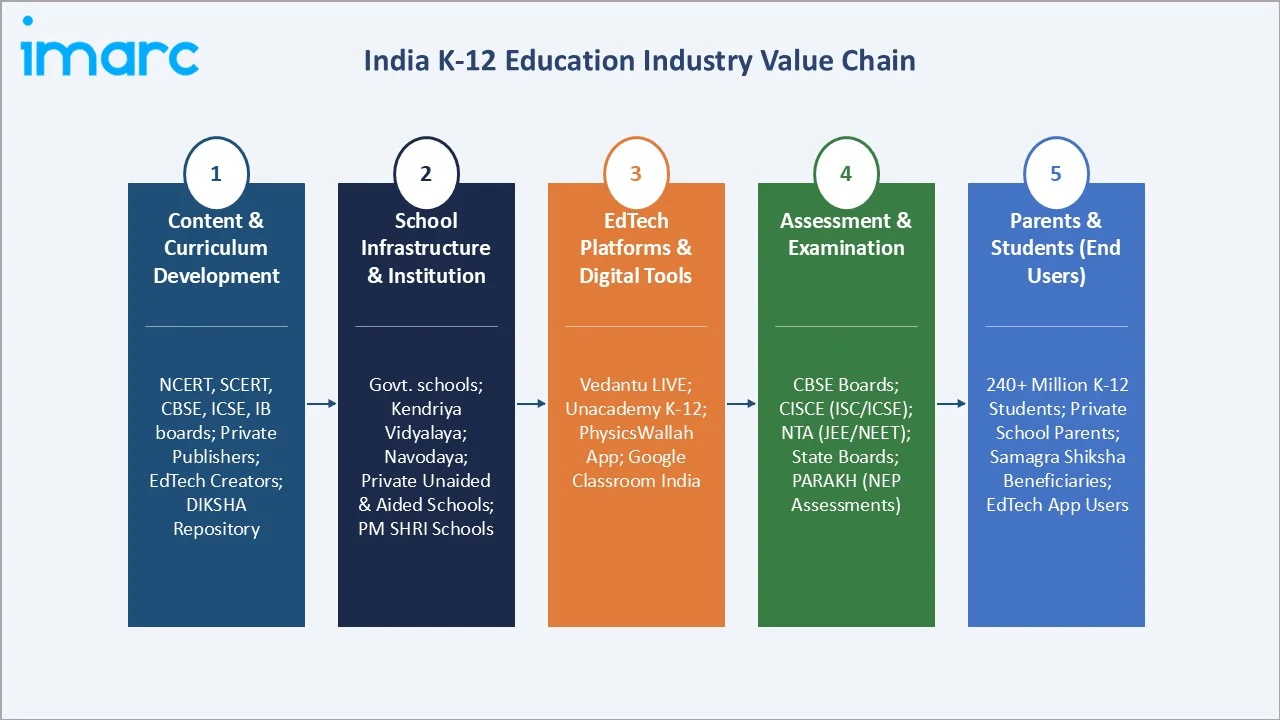

Industry Value Chain Analysis

India’s K-12 education value chain integrates content and curriculum development through institutional delivery, digital supplementation, assessment, and parental consumer purchasing across India’s 1.5 million schools and 260 million-strong K-12 student base.

|

Stage |

Key Participants |

|

Content & Curriculum Development |

NCERT (National Council of Educational Research and Training) national curriculum framework; State Councils of Educational Research and Training (SCERT) – state-level syllabus; CBSE, ICSE, IB, Cambridge Board curriculum development; Private content publishers; EdTech content creators; DIKSHA (Digital Infrastructure for Knowledge Sharing) government digital content repository |

|

School Infrastructure & Institution |

Government schools; Central government schools – Kendriya Vidyalaya Sangathan, Navodaya Vidyalaya Samiti; Private unaided schools; Private aided schools; International schools; CBSE-affiliated schools; CISCE-affiliated; PM SHRI Yojana schools |

|

EdTech Platforms & Digital Tools |

Vedantu LIVE online classes; Unacademy K-12 preparation; Google Classroom India, PhysicsWallah |

|

Assessment & Examination |

CBSE Board Examinations; CISCE (ISC/ICSE Boards); National Testing Agency (NTA) – JEE, NEET entrance preparation feedback; State Board examinations; PARAKH (Performance Assessment, Review and Analysis of Knowledge for Holistic Development) – NEP standardized assessments |

|

Parents & Students (End Users) |

240+ million K-12 students (2025); parents representing education expenditure at private schools; government school parents with Samagra Shiksha scheme beneficiaries; supplementary tutoring families; smartphone-owning parents adopting EdTech apps |

Private school operators and EdTech platforms capture the highest per-student revenue, premium private schools at INR 80,000–3,00,000 per student annually versus government schools’ INR 2,000–10,000 effective per-student cost from government budgets.

Technology Landscape in the India K-12 Education Industry

AI-Powered Adaptive Learning and Personalization

India’s K-12 EdTech platforms are investing heavily in AI-powered adaptive learning systems that dynamically adjust content difficulty, pace, and format based on individual student performance data.

Gamification and Game-Based Learning

India’s K-12 EdTech sector has adopted gamification as the primary engagement mechanism for elementary and middle school students (K-8) who demonstrate 3‑5× higher session engagement with gamified content versus traditional video lectures.

National Digital Education Architecture (NDEAR) and Government EdTech

NDEAR – India’s national digital education platform mandated by NEP 2020 to create an interoperable, open-API education technology ecosystem, is the most significant government education technology initiative in scale and ambition. NDEAR’s open architecture enables private EdTech providers to integrate content through APIs, allowing BYJU’S, Extramarks, and Pearson content to reach DIKSHA’s 50M+ government school users through a single national platform.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Application | High School (9-12) | 46.0% | 2025 |

| Institution | Public | 54.0% | 2025 |

| Delivery Mode | Offline | 78.0% | 2025 |

| Region | North India | 32.0% | 2025 |

By Institution

Public institutions lead at 54.0% market share (2025). Government schools comprise 69% of the total 14.72 lakh schools serving students under free RTE-guaranteed education from Classes 1–8. Government K-12 expenditure includes teacher salaries, infrastructure, digital transformation, and mid-day meal program collectively constituting the market’s revenue base.

To access detailed market analysis, Request Sample

Private institutions at 46.0% are growing at ~13.2% CAGR, driven by rising household incomes, expanding private school chains, fee premium growth, and India’s middle-class aspiration premium. Private school revenue encompasses tuition fees, textbook and stationery sales, extracurricular activity fees, transport, and digital subscription fees, creating per-student revenue 5–25× higher than government school equivalents.

By Delivery Mode

Offline delivery leads at 78.0% market share (2025). Physical school attendance remains the primary K-12 delivery mode reinforced by RTE Act attendance requirements, CBSE board examination school affiliation mandates, social peer learning value, and India’s parental preference for supervised structured learning environments. India’s 1.5 million schools, 8.5 million teachers and 250 million children represent the physical infrastructure backbone of offline K-12 delivery that cannot be rapidly substituted by digital alternatives regardless of EdTech investment levels.

Online delivery at 22.0% is growing at 18.4% CAGR, the fastest segment, primarily serving supplementary K-12 education alongside physical school attendance rather than replacing it. This category includes EdTech subscription revenue, private tutoring migrated online, entrance exam coaching (NEET, JEE), and school-provided digital learning resources.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

32.0% |

Delhi-NCR’s premium private school cluster, including DPS, Ryan International, Modern School, Cambridge School; UP’s highest number of schools; Haryana, Rajasthan, Punjab’s rapidly expanding private school ecosystem |

|

South India |

25.0% |

Tamil Nadu’s highly literate population driving premium private school demand; Kerala’s near-100% literacy and Kerala model of education quality excellence; Andhra Pradesh and Telangana’s Engineering and Medical entrance exam coaching ecosystem generating supplementary education demand |

|

East India |

23.0% |

West Bengal’s schools and Kolkata’s premium private school market; Bihar’s rapidly expanding private school sector aspiration for quality education; Odisha’s government school digitization under Odisha Education Reform |

|

West India |

20.0% |

Maharashtra’s schools, including Mumbai’s premium international school cluster, and Gujarat’s rapidly growing private school ecosystem, driven by high business community education investment |

North India’s 32.0% dominance is reinforced by the concentration of India’s premium K-12 coaching ecosystem in Kota, Rajasthan, with JEE and NEET aspirants. UP’s highest number of schools serving India’s most populous state creates the largest single state K-12 revenue pool, while Delhi’s government school transformation model demonstrates that quality improvement in public systems is commercially demonstrated and replicable across North India states.

South India’s 25.0% share is supported by Kerala’s near-100% literacy, creating India’s highest per-capita K-12 education spending, Tamil Nadu’s primary school enrollment rate, and Bangalore’s technology-driven parent community with India’s highest EdTech subscription rate per capita. East India’s 23.0% share with the fastest regional CAGR reflects the transformative growth potential of Bihar and Jharkhand’s rapidly expanding private school ecosystems.

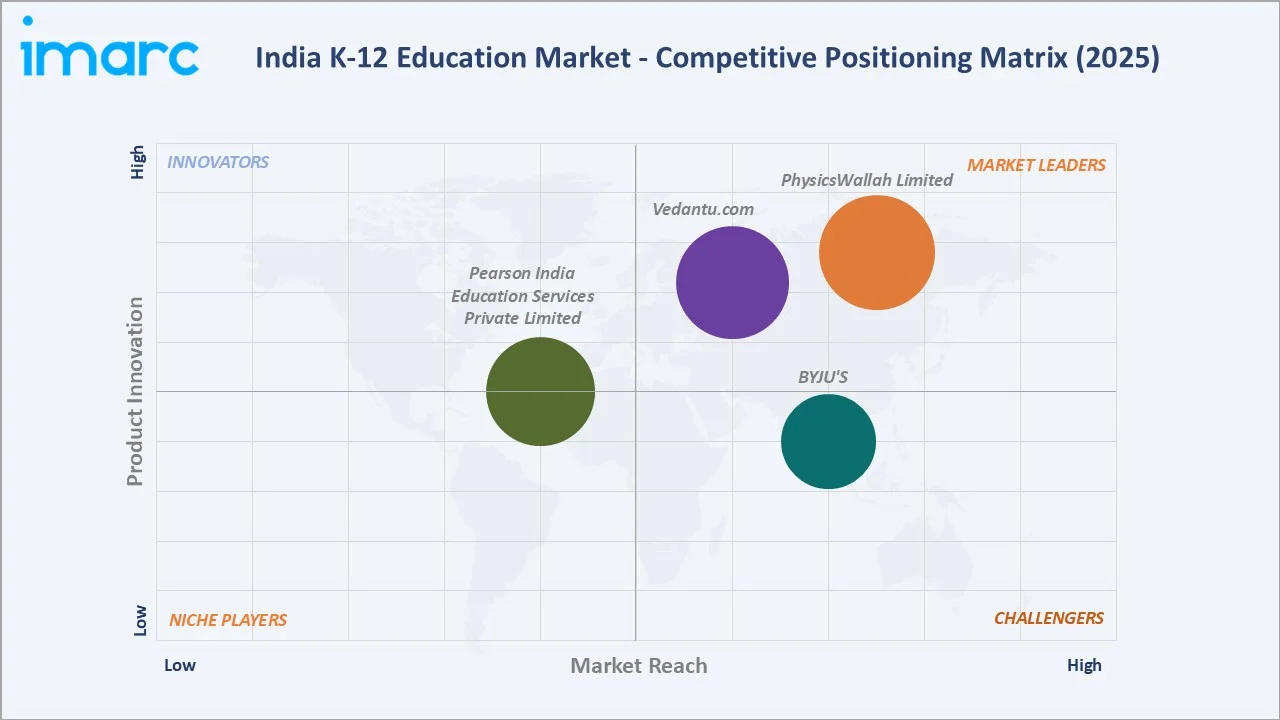

Competitive Landscape

India’s K-12 education market is moderately concentrated at the EdTech platform level and highly fragmented at the physical school level. BYJU’S and Vedantu collectively account for approximately 35–40% of India’s organized online K-12 supplementary education market by paid subscriber revenue.

|

Company Name |

Brand / Platform |

Market Position |

Core Strength |

|

Physicswallah Limited |

PhysicsWallah App, PW Vidyapeeth |

Market Leader |

PhysicsWallah’s price disruption strategy – JEE/NEET K-12 content created India’s most democratized K-12 online learning access |

|

Vedantu.com |

Vedantu LIVE, WAVE |

Market Leader |

India’s leading live online teaching platform for K-12 subscribers; Vedantu’s proprietary WAVE (Whiteboard Audio Video Environment) technology enables real-time teacher-student interaction |

|

Pearson India Education Services Private Limited |

Pearson MyInsights, Pearson Test of English (PTE), Versant |

Established |

Provides textbook publishing, digital content, and assessment solutions for K-12; Pearson India’s textbook and workbook portfolio covers CBSE, ICSE, and international curriculum K-12 content |

|

BYJU'S |

BYJU'S Learning App |

Market Challenger |

India’s most funded EdTech company; Over 6 million new students accessed BYJU'S in March 2020 |

At the school level, no single chain controls more than 1% of India’s 1.5 million schools. DPS Society, Ryan International, and EuroKids together represent less than 0.15% of total India K-12 schools by count, making the physical school market one of India’s most fragmented commercial sectors.

Key Company Profiles

Physicswallah Limited

PhysicsWallah is India’s EdTech democratization success story. Founded in 2020 by Alakh Pandey, who began teaching on YouTube from a basic setup in Prayagraj, PhysicsWallah built YouTube subscribers and app users through teaching that Tier-2 and Tier-3 city students found relatable, affordable, and effective.

- Product Portfolio: PhysicsWallah App, PW Vidyapeeth.

- Recent Developments: In February 2026, PhysicsWallah expanded beyond its core test preparation segment into the K-12 school education space, having invested ₹400 crore so far in its wholly owned subsidiary, Penpencil Edu Services, as part of its planned K-12 expansion.

- Strategic Focus: Price democratization as primary competitive moat, maintaining 5–10× price advantage versus premium EdTech competitors to access aspirational K-12 students outside premium pricing range; Vidyapeeth physical expansion creating offline-digital hybrid across India’s Tier-2/3 cities.

Vedantu.com

Vedantu is India’s leading live online K-12 teaching platform. Vedantu’s core innovation, real-time LIVE teaching with teacher-student interaction via proprietary WAVE technology, differentiated it from BYJU’S’ pre-recorded video model by recreating the traditional tutoring experience at scale.

- Product Portfolio: Vedantu LIVE, WAVE.

- Recent Developments: In September 2025, Vedantu raised $11 million (about Rs 98 crore) in fresh capital from existing investors, including ABC World Asia, Accel India and Omidyar Network.

- Strategic Focus: Sustainable profitability model with lower customer acquisition cost through content-led organic growth; Tier-2 and Tier-3 city market deepening as primary revenue growth vector; WAVE platform B2B licensing to schools as institutional revenue diversification.

Market Concentration Analysis

India’s K-12 education market exhibits dual-tier concentration: moderate in the EdTech supplementary segment and highly fragmented in the physical school segment. In the online/EdTech K-12 supplementary market, BYJU’S and Vedantu collectively hold approximately 40–45% share by paid subscriber revenue, a moderate concentration comparable to global EdTech markets where incumbent scale creates acquisition cost advantages and content breadth moats that prevent easy challenger entry.

India’s physical K-12 school market is one of the world’s most fragmented commercial sectors, with 1.5 million schools with no single operator controlling more than 500 schools. DPS Society, Ryan International, and EuroKids together represent less than 0.15% of India’s total school count. This extreme fragmentation reflects India’s K-12 school market’s geographic distribution across 640 districts, local community trust requirements for school selection, and regulatory barriers to school chain consolidation.

Investment & Growth Opportunities

Fastest Growing Segments

Online delivery (~18.4% CAGR), private institutions (~13.2% CAGR), East India regional market (~11.9% CAGR), international curriculum schools (~15–20% CAGR), and AI-powered adaptive K-12 tutoring (~30–40% CAGR from 2025 base) represent India’s highest-growth K-12 investment vectors through 2034.

Emerging Market Opportunities

Bihar and UP’s rapidly expanding private school sector represents high investments in addressable annual K-12 revenue by 2030 as these two states’ combined population reaches middle-income EdTech and private school affordability thresholds. International school market expansion in Hyderabad, Pune, and Ahmedabad represents premium K-12 revenue growing at 15–20% annually.

Investment Themes

India’s K-12 EdTech sector attracted venture investment, contracted sharply in 2023–2024 as unit economics challenged emerged, and is rebuilding with profitability-first business models from 2025 onwards.

- Key technology investment themes: AI personalized K-12 tutor development, vernacular language (Hindi/regional) K-12 content creation, government school EdTech B2B platform development, NEP 2020 competency assessment tools, school management SaaS for India’s private schools, and international Indian diaspora K-12 curriculum platforms.

- Policy investment catalysts: PM SHRI Yojana’s INR 27,360 crore, NDEAR digital education infrastructure, NEP 2020 teacher training fund, and National AI Mission’s education AI vertical collectively represent high government K-12 education investment through 2030 that creates systematic EdTech procurement demand.

Future Market Outlook (2026-2034)

The India K-12 education market is entering its most transformational phase and also its most commercially compelling. From USD 103.05 Billion in 2025, the market will reach USD 276.00 Billion by 2034, at an 11.57% CAGR that makes India’s K-12 market the world’s fastest-growing large-scale education market by absolute annual value addition.

Three structural forces anchor this growth trajectory with a visibility that few commercial markets can claim: India’s demographic structure; NEP 2020’s decade-long implementation timeline; and India’s rising middle class systematically migrating from government to private schools and from classroom-only to hybrid EdTech-supplemented learning at a pace that compounds both private school fee revenue and EdTech subscription revenue simultaneously.

Research Methodology

Primary Research

Primary research included structured interviews with 130+ industry stakeholders in 2025, comprising EdTech company executives, private school principals and management across DPS, Ryan International, EuroKids, and regional chains, state education department officials, NEP 2020 implementation committee representatives, CBSE and CISCE examination board officials, and parents and students across metro and Tier-2 city focus groups.

Secondary Research

Secondary research encompassed Ministry of Education Annual Report 2024–2025, UDISE+ (Unified District Information System for Education) school statistics 2023–2024, ASER 2024 Annual Education Status Report, UNESCO Education Statistics India data, NASSCOM EdTech India Report 2024, IVCA (Indian Venture and Alternate Capital Association) EdTech investment data, company financial filings, Samagra Shiksha budget documents, and PM SHRI Yojana progress reports. Over 200 secondary sources were reviewed.

Forecasting Models

Market forecasts were developed using a bottom-up student enrollment × revenue per student × institution type aggregation validated against top-down macroeconomic models. Key inputs include UDISE+ enrollment trends, household income distribution projections, NEP 2020 implementation timeline milestones, EdTech adoption S-curve by geography and income segment, government education budget trajectory, and private school fee growth historical data.

India K-12 Education Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Applications Covered | Elementary School (K-5), Middle School (6-8), High School (9-12) |

| Institutions Covered | Public, Private |

| Delivery Modes Covered | Online, Offline |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Physicswallah Limited, Vedantu.com, Pearson India Education Services Private Limited, BYJU'S, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India K-12 education market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India K-12 education market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India K-12 education industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India K-12 Education Market Report

The India K-12 education market was valued at USD 103.05 Billion in 2025 and is projected to reach USD 276.00 Billion by 2034.

The India K-12 education market is forecast to grow at a CAGR of 11.57% during 2026-2034, driven by NEP 2020 reforms, 260M student population, rising private school demand, and EdTech adoption growth.

Public institutions lead with 54.0% revenue share (2025), reflecting India’s annual government education expenditure serving government school students.

Offline leads with 78.0% market share (2025), anchored by India’s 1.5 million physical schools, RTE Act mandatory attendance for Classes 1–8, and CBSE board exam affiliation requirements.

North India leads with 32.0% market share (2025), driven by UP’s schools, Delhi-NCR’s premium private school market, and Kota’s K-12 coaching ecosystem.

Key companies include Vedantu.com, Physicswallah Limited, BYJU'S, and Pearson India Education Services Private Limited.

Key drivers include NEP 2020 curriculum reforms, India’s 260M K-12 student population, rising household incomes driving private school migration, smartphone penetration enabling EdTech adoption, and government PM SHRI Yojana school transformation.

Key trends include AI tutors in K-12, NEP 2020 competency assessment, hybrid physical-digital learning, IB/IGCSE international school expansion, government school digital transformation, and PhysicsWallah-style price democratization of EdTech.

Online delivery grows at 18.4% CAGR driven by smartphone users, world’s cheapest data, COVID-19 normalized EdTech habits, and platforms like BYJU’S, Vedantu, and PhysicsWallah reaching Tier-2/3 city students.

Key challenges include rural digital divide, teacher quality gap, EdTech unit economics sustainability post-COVID, and regulatory complexity across 28 state boards and NEP 2020 transition.

Top opportunities include AI K-12 tutor development, government school EdTech B2B contracts (PM SHRI INR 27,360 crore), private school PE consolidation, NEP 2020 assessment tools, vernacular language EdTech, and international Indian diaspora K-12 curriculum platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade