India Kitchen Appliances Market Size, Share, Trends and Forecast by Product Type, Structure, Fuel Type, Distribution Channel, Application, and Region, 2026-2034

India Kitchen Appliances Market Size, Share, Trends & Forecast (2026-2034)

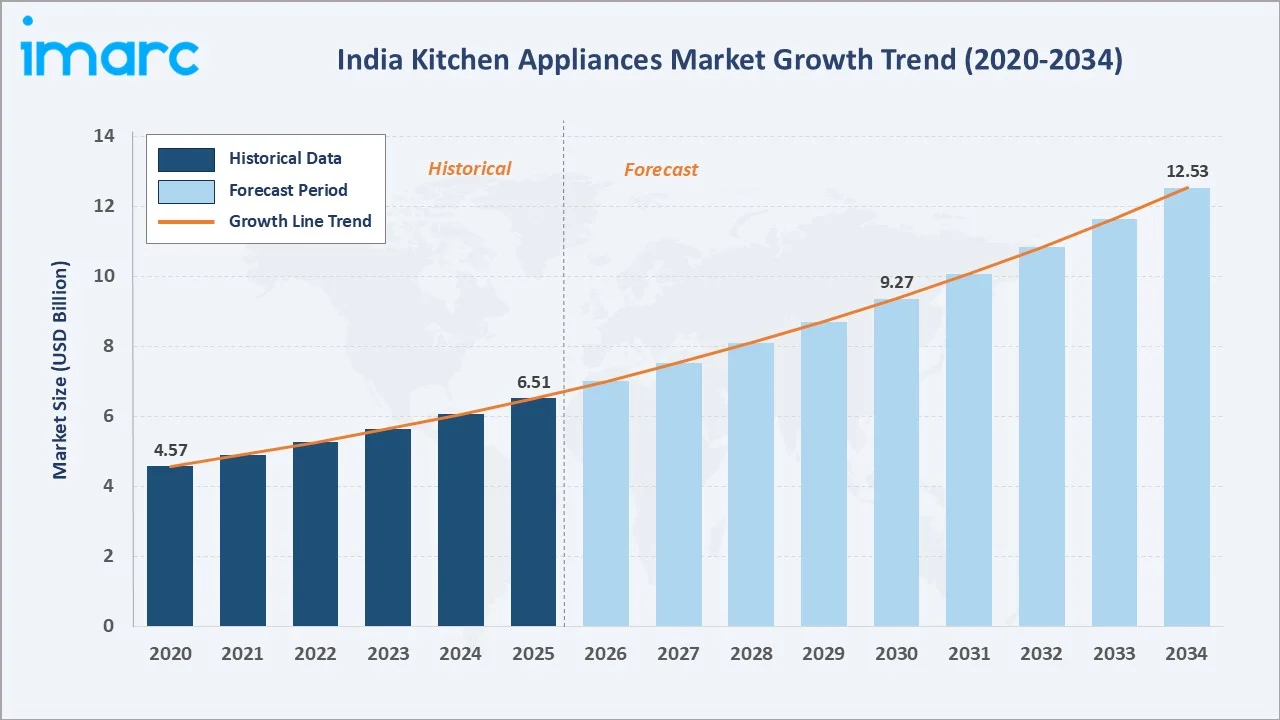

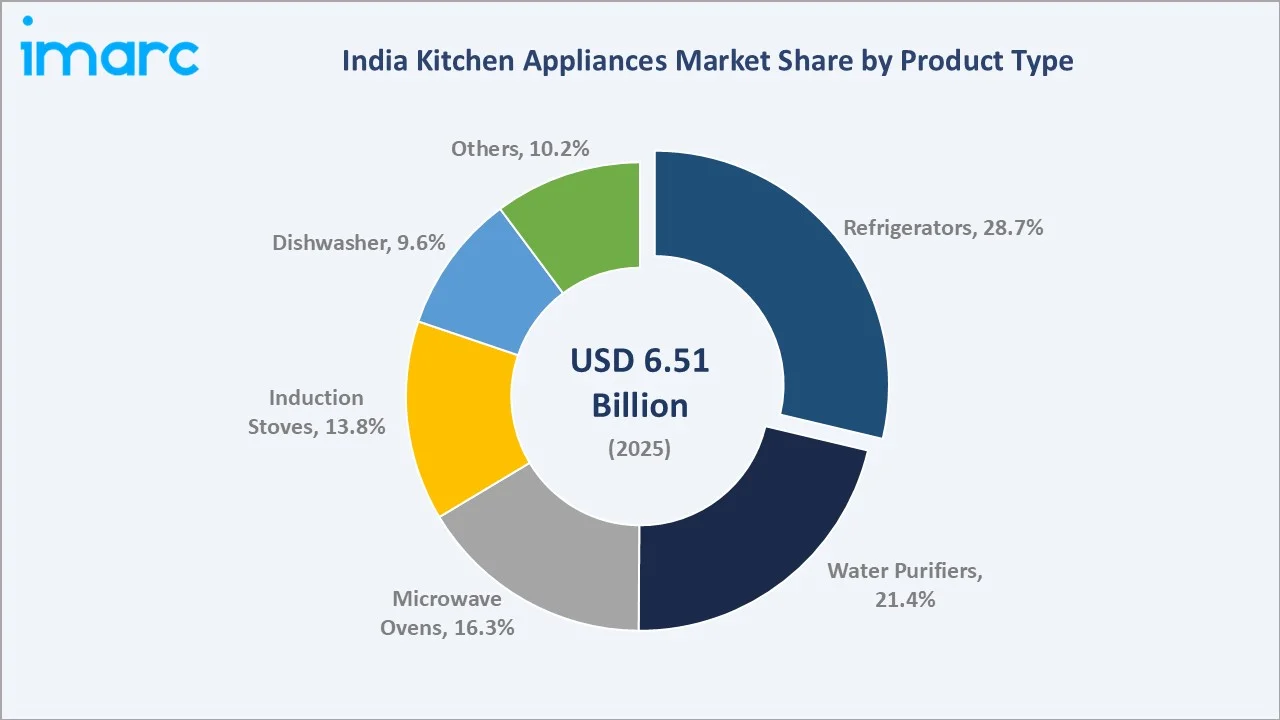

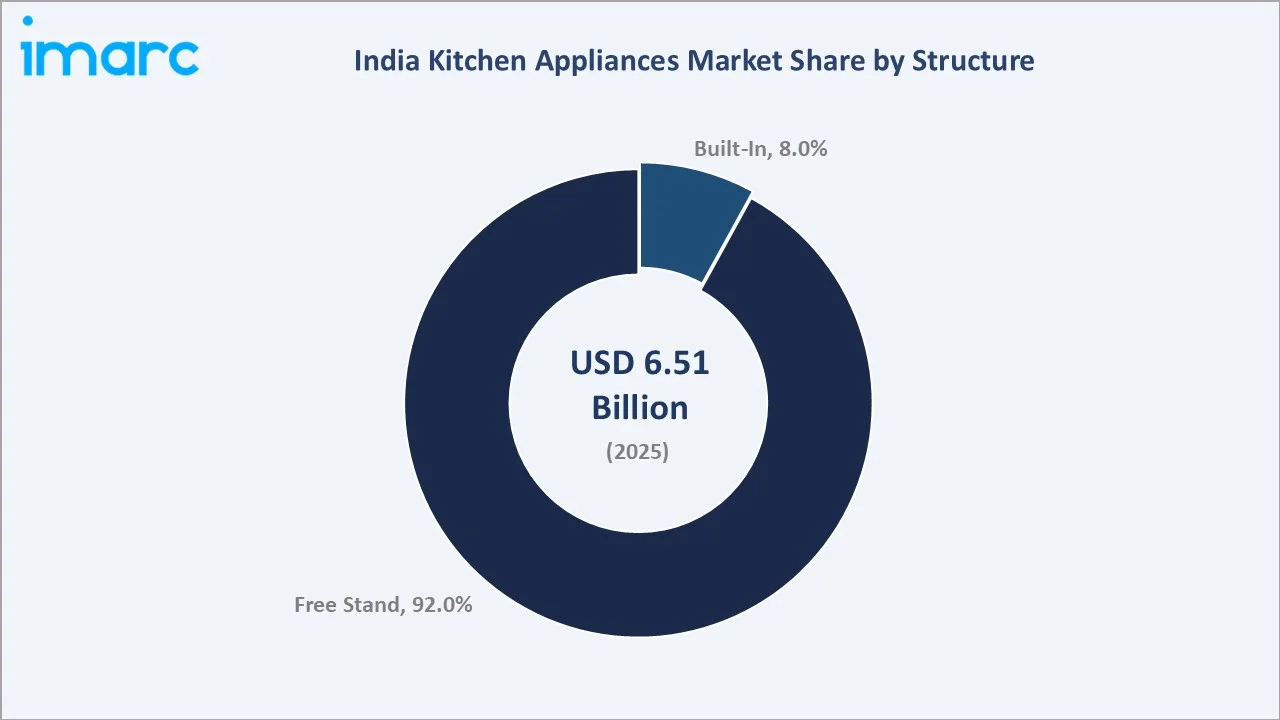

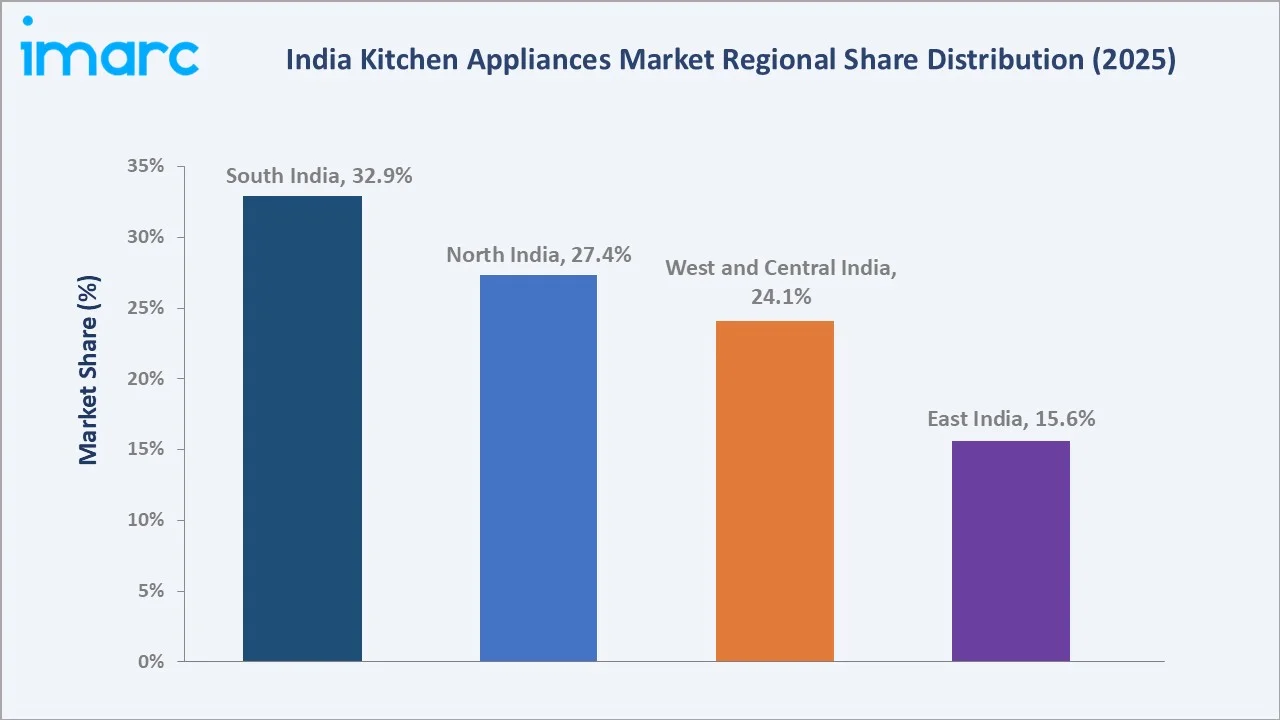

The India kitchen appliances market reached USD 6.51 Billion in 2025 and is projected to reach USD 12.53 Billion by 2034, growing at a CAGR of 7.32% during 2026-2034. The market is driven by rising urbanization, with more than 40% of India's population living in urban areas by 2030, increasing disposable incomes, changing lifestyles, and growing demand for convenient and time-saving cooking solutions. Refrigerators lead the product type at 28.7%. Free stand dominates structure at 92.0%. South India commands 32.9% of market revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.51 Billion |

|

Forecast Market Size (2034) |

USD 12.53 Billion |

|

CAGR (2026-2034) |

7.32% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Refrigerators (28.7%, 2025) |

|

Dominant Structure |

Free Stand (92.0%, 2025) |

|

Leading Region |

South India (32.9%, 2025) |

The market expanded from USD 4.57 Billion in 2020 to USD 6.51 Billion in 2025, anchored at USD 9.27 Billion in 2030, and forecast to reach USD 12.53 Billion by 2034. COVID-19's home cooking revolution established a permanently elevated appliance adoption baseline, as Indian consumers who invested in air fryers, induction stoves, and microwave ovens during the pandemic demonstrated a 3x higher likelihood of repeat category purchase, sustaining post-pandemic market momentum above the pre-COVID trajectory.

To get more information on this market, Request Sample

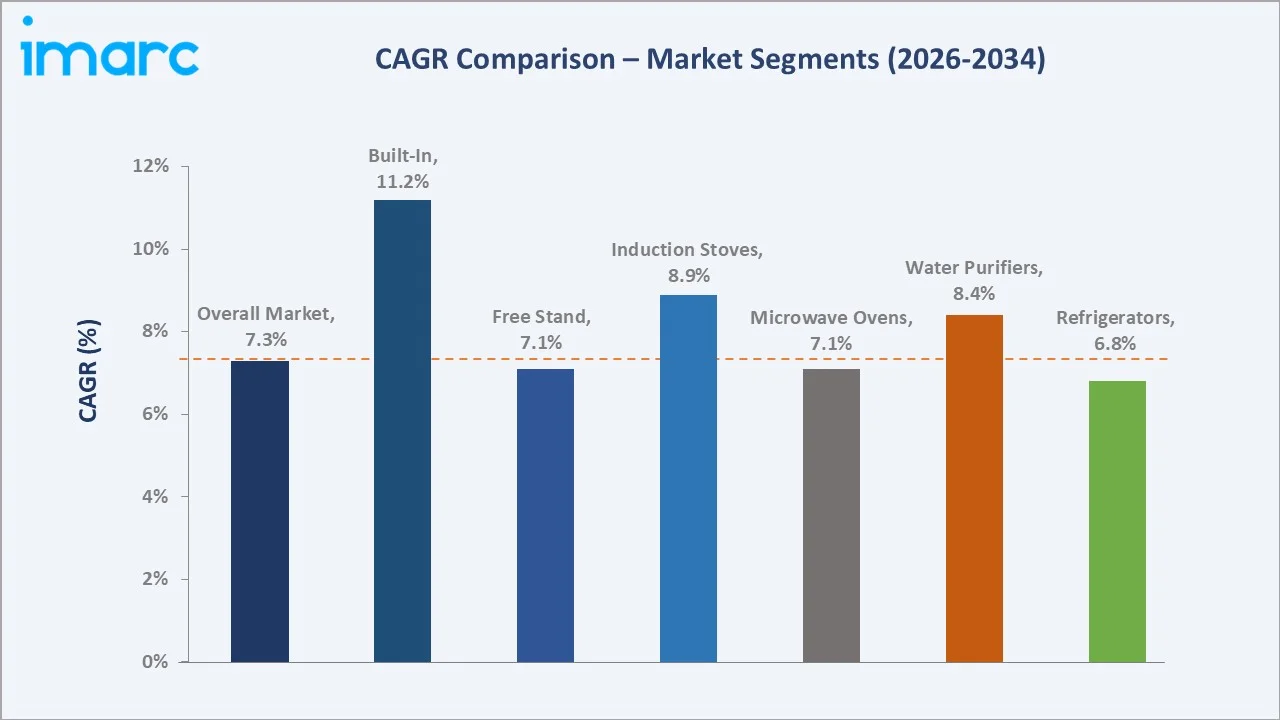

Built-in kitchen structure grows fastest at ~11.2% CAGR (2026-2034), driven by India's premium residential real estate boom, luxury hospitality expansion, and interior designer specification in premium projects. Induction stoves grow at ~8.9% CAGR as PM Ujjwala Yojana LPG transition creates energy-diversification demand and ultra-affordable range democratizes induction cooking for India's Tier-2/3 city markets.

Executive Summary

The India kitchen appliances market reached USD 6.51 Billion in 2025, establishing India as one of Asia's largest kitchen appliances markets and one of the world's fastest-growing major markets by absolute demand addition. India's kitchen appliances market is structurally unique, simultaneously serving the world's most aspirational first-time buyers, a rapidly premiumizing upgrade segment, and a nascent premium built-in kitchen segment. The market is projected to reach USD 12.53 Billion by 2034 at 7.32% CAGR.

Refrigerators at 28.7% lead as India's most fundamental kitchen appliance, creating the world's largest single-product appliance expansion opportunity. Free stand structure at 92.0% dominates as India's mass market serves households across all income segments through standalone appliances purchased independently across retail channels. South India, at 32.9%, leads through Tamil Nadu, Karnataka, and Kerala's highest per-capita appliance ownership.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Refrigerators - 28.7% share (2025) |

|

Dominant Structure |

Free Stand - 92.0% market share (2025) |

|

Leading Region |

South India - 32.9% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Refrigerators at 28.7%: The refrigerator segment dominates due to its essential role in daily food storage, increasing urban household penetration, and rising demand for energy-efficient and smart cooling solutions. Growing consumption of packaged and frozen foods, improving rural electrification, and replacement demand for larger and premium models further strengthen segment dominance.

- Free stand at 92.0%: The free-standing segment dominates due to its affordability, easy installation, mobility, and compatibility with both traditional and modern kitchen layouts. Higher adoption across urban and semi-urban households, along with strong availability through retail and e-commerce channels, continues to support segment growth.

- South India at 32.9%: South India's kitchen appliance leadership reflects multiple structural advantages: Tamil Nadu and Kerala's universal electrification; South India's matrilineal household traditions; IFB Industries' Goa manufacturing and Bengaluru's innovation ecosystem creating appliance technology proximity; and South India's fish and rice-dominant diet requiring specific appliances.

India Kitchen Appliances Market Overview

India's kitchen appliances market encompasses all electrical and electronic appliances used in food preparation, storage, and beverage purification within residential, commercial, and institutional kitchen environments. The market includes major appliances (refrigerators, dishwashers, microwave ovens), cooking appliances (induction stoves, ovens, air fryers, rice cookers), food preparation equipment (mixer grinders, food processors, hand blenders), water management appliances (water purifiers, water heaters), and small appliances (electric kettles, toasters, sandwich makers, coffee makers).

The ecosystem integrates component suppliers, appliance manufacturers, certification bodies, a multi-tier distribution network, modern trade chains, e-commerce platforms, and after-sales service networks. Macroeconomic factors include rising disposable incomes, rapid urbanization, expanding middle-class population, and increasing residential construction activity.

Market Dynamics

To evaluate market opportunities, Request Sample

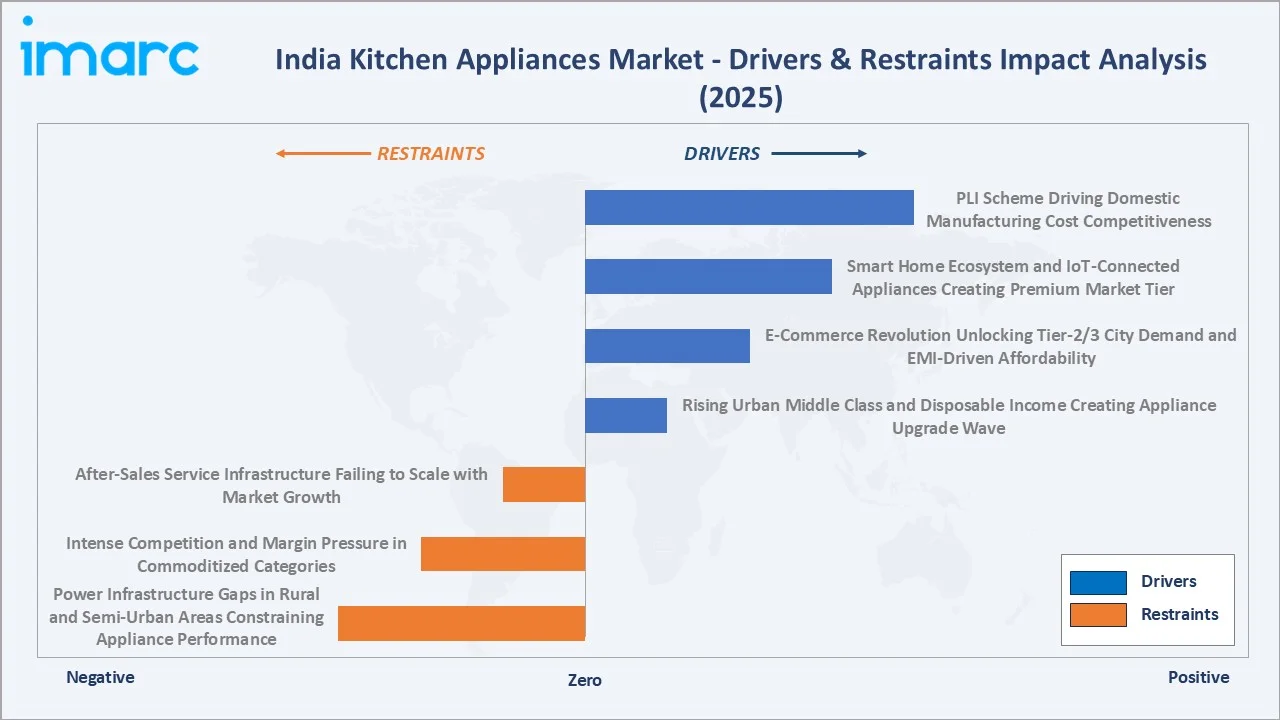

Market Drivers

- Rising Urban Middle Class and Disposable Income Creating Appliance Upgrade Wave: India's middle class is projected to reach 715 million (or 47% of the population) in 2030–31, with each additional middle-class household representing high initial kitchen appliance investment. Dual-income urban households are the key driver of appliance premiumization; working couples with combined incomes are India's fastest-growing premium appliance buyer segment, investing in inverter frost-free refrigerators, dishwashers, convection microwave ovens, and IoT-connected water purifiers as time-saving, energy-efficient household infrastructure.

- E-Commerce Revolution Unlocking Tier-2/3 City Demand and EMI-Driven Affordability: Flipkart's Big Billion Day and Amazon India's Great Indian Festival have transformed India's kitchen appliance market geography.

- Smart Home Ecosystem and IoT-Connected Appliances Creating Premium Market Tier: In May 2026, Dylect launched a new range of smart kitchen products, including slow juicers and stand mixers. India's 5G subscriber base growth provides the connectivity infrastructure enabling reliable IoT appliance operation. Voice assistant integration is normalizing smart kitchen interaction among India's English and Hindi-speaking smartphone users.

Market Restraints

- Power Infrastructure Gaps in Rural and Semi-Urban Areas Constraining Appliance Performance: India's rural electricity supply creates operational challenges for sensitive electronic kitchen appliances. Voltage fluctuation damages microwave oven magnetrons and refrigerator compressors at 3-5x higher rates than urban deployment, increasing service costs and consumer dissatisfaction.

- Intense Competition and Margin Pressure in Commoditized Categories: The basic single-door refrigerator segment operates on 8-12% gross margins that make distribution and after-sales investment economically challenging. This margin pressure is driving consolidation toward value-added IoT features, premium product line extensions, and service-based revenue models that sustain profitability as hardware margins compress.

Market Opportunities

- Dishwasher Category Creating India's Largest Untapped Kitchen Appliance Market: The dishwasher category is creating a major untapped market opportunity due to rising urban lifestyles, increasing dual-income households, and growing demand for time-saving home solutions. Higher awareness regarding water-efficient cleaning, hygiene, and smart kitchen adoption is encouraging consumers to shift toward automatic dishwashing appliances, especially in metropolitan and premium residential segments.

- Premium Built-In Kitchen Segment Driven by India's Luxury Real Estate Boom: India's luxury residential real estate growth represents a built-in kitchen specification opportunity. Interior designers are increasingly specifying complete built-in kitchen suites from branded products for premium developer projects.

Market Challenges

- After-Sales Service Infrastructure Failing to Scale with Market Growth in Non-Metro Markets: India's kitchen appliance market expansion into Tier-2/3 cities is outpacing after-sales service infrastructure investment. This service gap creates consumer dissatisfaction that reduces repurchase rates and brand loyalty in new market geographies. Online purchase returns for large appliances remain high due to delivery damage and installation complexity in non-metro markets, adding reverse logistics costs that reduce e-commerce profitability in non-metro expansion.

- Consumer Finance Access Gap in Rural and Semi-Urban Markets Limiting Premium Adoption: Limited access to consumer financing in rural and semi-urban markets is restricting the adoption of premium kitchen appliances such as dishwashers, built-in ovens, smart refrigerators, and modular kitchen solutions. Lower credit penetration, affordability concerns, and limited availability of EMI-based purchasing options continue to slow the shift toward high-value and technologically advanced appliances in these regions.

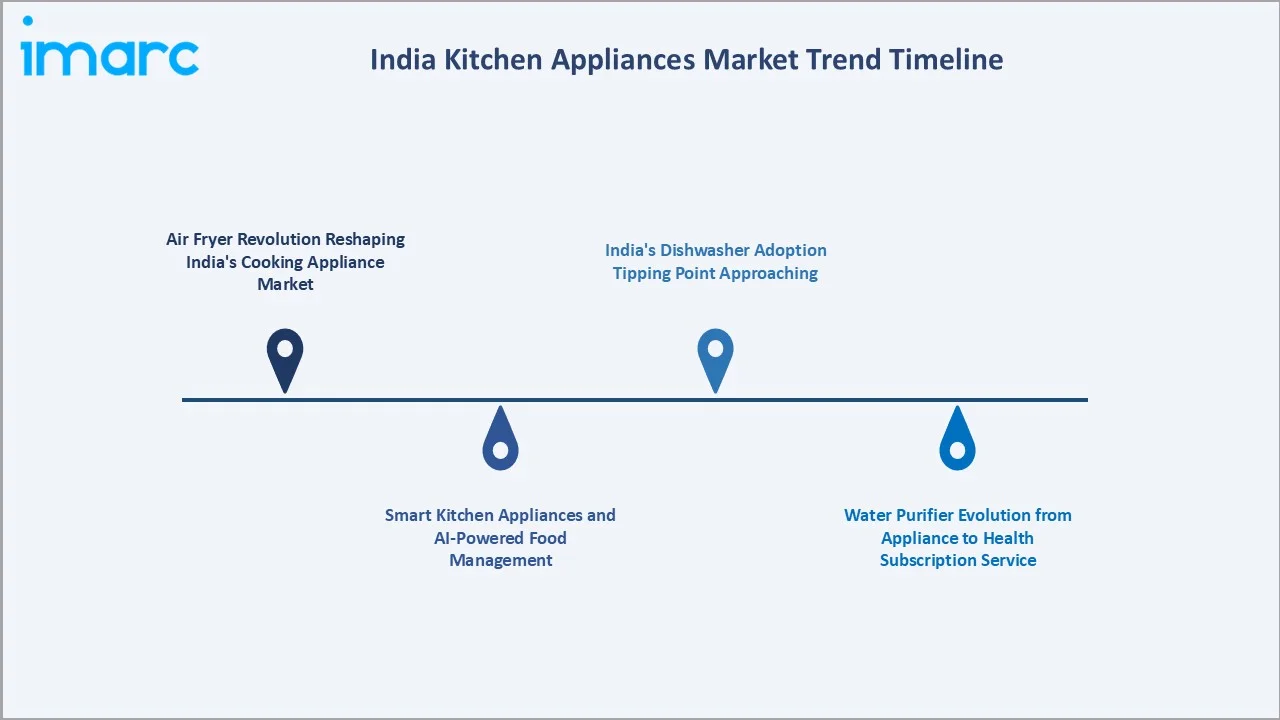

Emerging Market Trends

1. Air Fryer Revolution Reshaping India's Cooking Appliance Market

The air fryer revolution is emerging as consumers increasingly seek healthier, low-oil cooking alternatives and convenient meal preparation solutions. Rising health awareness, busy urban lifestyles, and growing interest in smart and multifunctional cooking appliances are accelerating adoption across middle- and high-income households. Manufacturers are expanding product portfolios with compact, energy-efficient, app-connected, and multi-cooking air fryer models to cater to evolving consumer preferences and modern kitchen setups.

2. Smart Kitchen Appliances and AI-Powered Food Management

Smart kitchen appliances and AI-powered food management are emerging as consumers increasingly adopt connected and intelligent cooking solutions for convenience and efficiency. In March 2026, Philips Home Appliances launched Philips OneChef, an all-in-one smart cooking appliance designed to simplify everyday cooking. OneChef combines 33 smart cooking functions in a single appliance, powered by Philips’ AmbiHeat technology.

3. Water Purifier Evolution from Appliance to Health Subscription Service

Water purifier evolution from a standalone appliance to a health subscription service is emerging as consumers increasingly prioritize safe drinking water, convenience, and preventive healthcare. Companies are introducing subscription-based models that include purifier installation, filter replacement, maintenance, water quality monitoring, and app-based service management under recurring payment plans. This trend is helping brands build long-term customer relationships while improving affordability and adoption of advanced RO, UV, and smart purification systems across urban households.

4. India's Dishwasher Adoption Tipping Point Approaching

India’s dishwasher adoption tipping point is emerging due to rising urbanization, dual-income households, compact lifestyles, and growing demand for time-saving home solutions. Consumers are increasingly recognizing the benefits of dishwashers in improving hygiene, reducing manual effort, and optimizing water usage, especially in metropolitan and premium residential segments. Manufacturers are responding with compact, energy-efficient, and India-specific dishwasher models designed for local cooking habits, helping expand adoption beyond early urban consumers.

Industry Value Chain Analysis

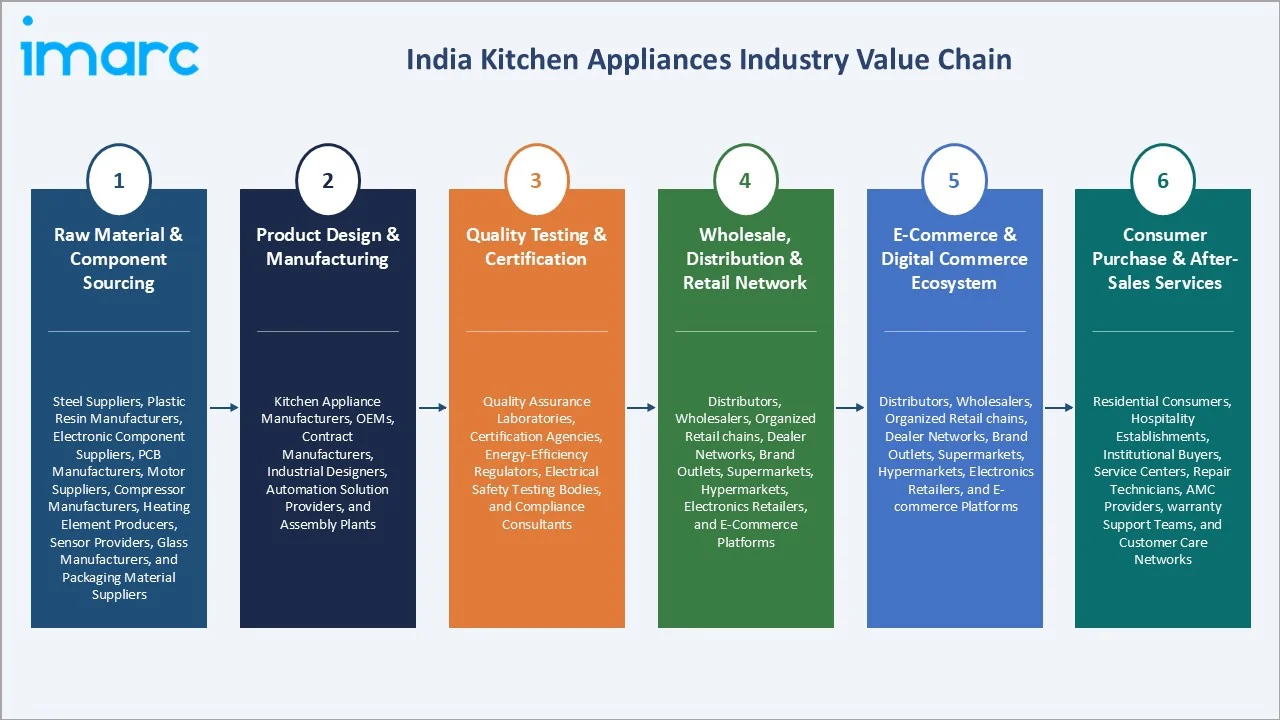

India's kitchen appliances value chain integrates international component sourcing, domestic assembly, quality certification, multi-tier distribution, modern retail and e-commerce, and after-sales service. Brand manufacturers earn 18-35% gross margins on premium products and 8-15% on mass-market products; national distributors earn 5-8% margins; retailers earn 12-20% margins; and e-commerce platforms charge 10-18% platform and logistics fees.

|

Stage |

Key Participants |

|

Raw Material & Component Sourcing |

Steel suppliers, plastic resin manufacturers, electronic component suppliers, PCB manufacturers, motor suppliers, compressor manufacturers, heating element producers, sensor providers, glass manufacturers, and packaging material suppliers. |

|

Product Design & Manufacturing |

Kitchen appliance manufacturers, OEMs, contract manufacturers, industrial designers, automation solution providers, and assembly plants. |

|

Quality Testing & Certification |

Quality assurance laboratories, certification agencies, energy-efficiency regulators, electrical safety testing bodies, and compliance consultants. |

|

Wholesale, Distribution & Retail Network |

Distributors, wholesalers, organized retail chains, dealer networks, brand outlets, supermarkets, hypermarkets, electronics retailers, and e-commerce platforms. |

|

E-Commerce & Digital Commerce Ecosystem |

Online marketplaces, direct-to-consumer platforms, digital payment providers, logistics companies, quick-commerce operators, and installation service partners. |

|

Consumer Purchase & After-Sales Services |

Residential consumers, hospitality establishments, institutional buyers, service centers, repair technicians, AMC providers, warranty support teams, and customer care networks. |

The after-sales service tier is becoming increasingly strategic as IoT-connected appliances enable predictive maintenance, remote diagnostics, and subscription-based service models.

Technology Landscape in the India Kitchen Appliances Industry

Inverter Compressor Technology Revolutionizing Refrigerator Efficiency

Inverter compressor technology is improving refrigerator energy efficiency, temperature stability, and operational durability. Unlike conventional compressors, inverter-based systems adjust cooling performance according to usage patterns, helping reduce electricity consumption, noise levels, and wear on components. Rising consumer preference for energy-efficient appliances, increasing electricity cost awareness, and stronger adoption of premium refrigerators are accelerating the penetration of inverter technology across urban and semi-urban households.

Reverse Osmosis Technology and Next-Generation Water Purification

Reverse osmosis technology and next-generation water purification systems are shaping the technology landscape through advanced filtration, mineral retention, UV and UF purification, and smart water-quality monitoring features. Manufacturers are increasingly integrating IoT connectivity, filter replacement alerts, AI-based purification adjustment, and touchless operation to improve convenience, safety, and efficiency. Growing concerns regarding water contamination, health awareness, and demand for premium smart kitchen solutions are accelerating the adoption of technologically advanced water purification appliances across households and commercial spaces.

Induction and Convection Technology Convergence in Multi-Function Cooktops

The convergence of induction and convection technologies in multi-function cooktops enables faster, energy-efficient, and versatile cooking solutions. Manufacturers are developing smart cooktops with features such as precise temperature control, preset cooking modes, touch interfaces, and IoT-enabled operation to enhance convenience and cooking performance. Rising urban lifestyles, compact kitchen adoption, and growing consumer preference for multifunctional and energy-saving appliances are driving demand for these advanced cooking systems.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Refrigerators |

28.7% |

2025 |

|

Structure |

Free Stand |

92.0% |

2025 |

|

Fuel Type |

🔒 |

🔒 |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

South India |

32.9% |

2025 |

By Product Type

Refrigerators lead at 28.7% market share (2025). India's refrigerator market spans five categories: single door, double door frost-free, side-by-side, French door, and mini refrigerators. Samsung, LG, and Whirlpool collectively command 65%+ of India's refrigerator market by value. The double-door frost-free category is growing at 12%+ annually as urban households upgrade from single-door models.

To access detailed market analysis, Request Sample

Water purifiers at 21.4% grow at ~8.4% CAGR, driven by the safe water imperative and rural expansion. Microwave ovens at 16.3% are revitalized by air fryer integration and millennials' health-conscious cooking. Induction stoves at 13.8% grow fastest among product types at ~8.9% CAGR through Pigeon's affordable range. Dishwashers at 9.6% represent India's most under-penetrated premium category. Others at 10.2% encompass mixer grinders, electric kettles, rice cookers, OTGs, air fryers, coffee makers, and food processors.

By Structure

Free stand dominates at 92.0% market share (2025). India's free-standing kitchen appliance dominance reflects the country's household structure, where standalone appliances purchased independently from general retail and e-commerce channels constitute the only feasible appliance acquisition model. The free-stand category includes all price tiers, 92% of India's kitchen appliance purchase decisions being made independently of any kitchen design context.

Built-in at 8.0% grows fastest at ~11.2% CAGR, driven by India's premium residential construction delivering luxury apartments annually, specifying modular kitchen infrastructure. Built-in appliances include hobs, built-in ovens, built-in microwaves, built-in dishwashers, integrated refrigerators, and range hoods, typically purchased as a coordinated set from a premium brand through modular kitchen studios or premium home appliance showrooms.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

South India |

32.9% |

High urbanization, strong consumer durable adoption, rising disposable incomes, and growing demand for modular kitchens and premium appliances. The region also benefits from strong retail penetration, technology awareness, and increasing adoption of smart and energy-efficient kitchen solutions. |

|

North India |

27.4% |

Driven by expanding urban households, rising middle-class spending, premium residential development, and increasing demand for built-in and multifunctional kitchen appliances. Growth in organized retail, e-commerce, and smart home adoption is further supporting regional market expansion. |

|

West and Central India |

24.1% |

Supported by strong metropolitan consumption, commercial development, hospitality growth, and higher spending on lifestyle and home improvement products. The region also benefits from a strong distribution network and increasing penetration of premium and connected kitchen appliances. |

|

East India |

15.6% |

Characterized by improving electrification, rising urbanization, expanding retail infrastructure, and growing awareness of modern kitchen appliances. Increasing adoption among middle-income households and rising e-commerce accessibility are gradually supporting market growth. |

South India's 32.9% market leadership reflects structural advantages compounded over decades, universal electrification, high female workforce participation, strong consumer credit culture, and the region's manufacturing proximity to LG and Samsung plants, improving product availability and service quality.

North India's 27.4% generates the highest average transaction value per appliance unit. West and Central India's 24.1% is anchored by Maharashtra's Mumbai-Pune corridor, India's largest metropolitan appliance market by absolute revenue. East India's 15.6% represents the market's largest untapped frontier.

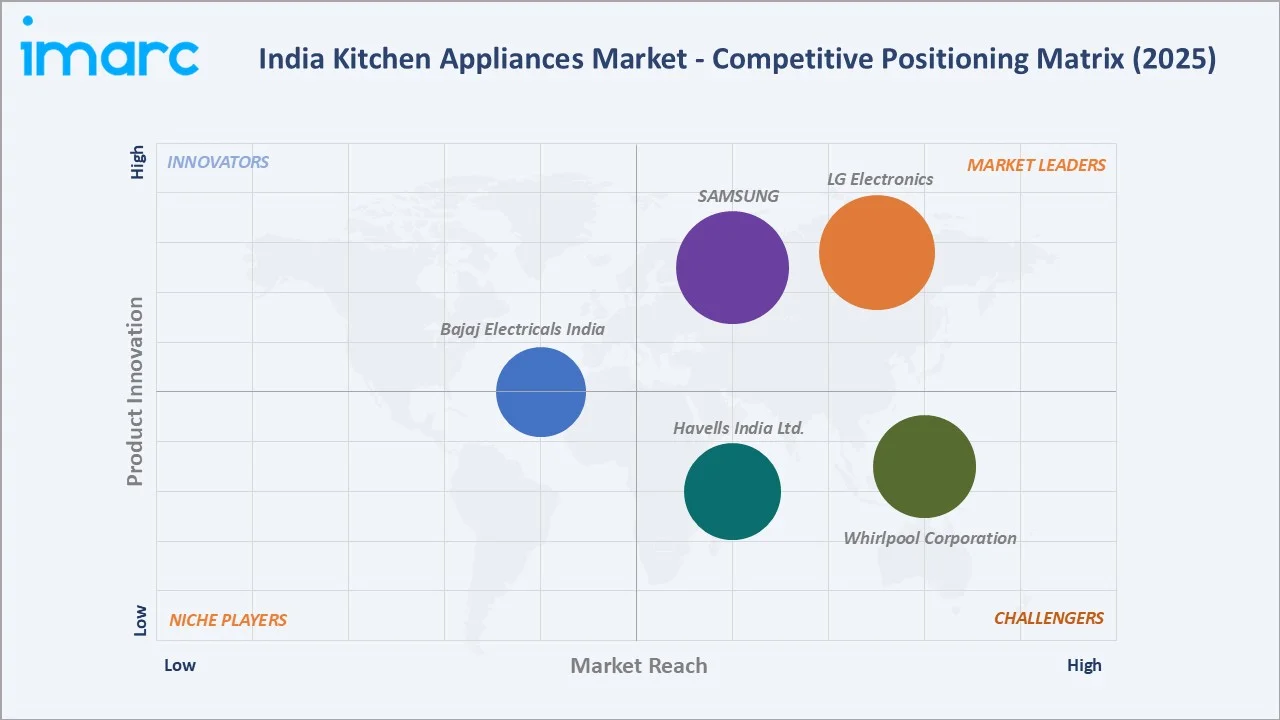

Competitive Landscape

India's kitchen appliances market is moderately concentrated; LG Electronics and Samsung collectively command approximately 35-40% of total market revenues across their combined product portfolios. The market is more fragmented than China's due to India's strong domestic brands, category specialists, and the structural advantage of trust-based Indian brands, particularly in Tier-2/3 city markets.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

LG Electronics |

LG Refrigerators, LG Microwave Ovens, LG Dishwashers, LG Water Purifiers |

Market Leader |

LG play an active role in world markets with an assertive global business policy. As a result, LG controls more than 142 local subsidiaries worldwide |

|

SAMSUNG |

Refrigerators, Microwave Ovens, Dishwashers |

Market Leader |

One of the well-known and largest home appliances companies |

|

Whirlpool Corporation |

Refrigerators, Microwave Ovens, Dishwashers |

Strong Challenger |

The company owns three manufacturing facilities in India at Faridabad, Puducherry and Pune. Each manufacturing setup is designed in ways conducive to growth and expansion while also ensuring efficiency and state-of-the-art processes. |

|

Havells India Ltd. |

Refrigerators, Water Purifiers, Air Fryers, Mixer Grinders, Induction Cooktops, |

Strong Challenger |

Havells India Limited is a leading FMEG company with a strong global presence, manufacturing a wide range of electrical products for residential, commercial, and industrial use. |

|

Bajaj Electricals India |

Mixers, Juicers, Table Blenders, Stand Mixers, Oven Toaster Griller (OTG), Microwave Ovens, Coffee Makers, Air Fryers, Electric Cookers, Electric Kettles, Toasters |

Established Player |

Bajaj portfolio includes product lines that range from affordable & mass-market to luxurious and cater to every economic group. |

The competitive landscape is being reshaped by domestic manufacturing, smart home platform lock-in, and e-commerce brand democratization.

Key Company Profiles

LG Electronics

LG Electronics India is the Indian subsidiary of Korea's LG Electronics Inc. and one of the largest kitchen appliance brands by total revenue.

- Product Portfolio: LG Refrigerators, LG Microwave Ovens, LG Dishwashers, LG Water Purifiers.

- Recent Developments: In May 2026, LG Electronics India launched refrigerators, dishwashers, water purifiers, and microwave ovens as part of its 2026 lineup in India.

- Strategic Focus: Expanding premium smart appliances through AI-enabled, energy-efficient, and connected kitchen solutions tailored to evolving urban consumer lifestyles.

SAMSUNG

Samsung is the world's largest appliance manufacturer by revenue and India's #1 refrigerator brand by unit sales.

- Product Portfolio: Refrigerators, Microwave Ovens, Dishwashers.

- Recent Developments: In April 2026, Samsung India launched new schemes under Samsung Finance+ to make its smart home appliances more accessible to customers across the country for purchasing Samsung appliances such as refrigerators, washing machines, ACs and microwaves. This service is available at over 8000 stores nationwide.

- Strategic Focus: Strengthening its premium smart kitchen portfolio through AI-powered, IoT-connected, and energy-efficient appliances designed for modern and digitally connected households.

Market Concentration Analysis

India's kitchen appliances market exhibits moderate concentration at the brand level with high concentration in specific product categories. LG and Samsung collectively command 30-35% of total market revenues, with Whirlpool, Havells, and Bajaj adding 15-20%. The top 5 brands control approximately 50-55% of organized market revenues.

Market concentration is expected to gradually increase through 2034 as PLI manufacturing consolidation and smart home platform lock-in reward scale advantages. However, the market's category diversity, geographic complexity, and income stratification will sustain a long tail of category specialists and regional champions that prevent the hyper-consolidation observed in more homogeneous markets. International consolidation in the global appliance industry may manifest in India through the acquisition of domestic challengers by international players seeking India manufacturing platforms and distribution network access.

Investment & Growth Opportunities

Fastest Growing Segments

Built-in structure (~11.2% CAGR), induction stoves by product type (~8.9% CAGR), water purifiers (~8.4% CAGR), dishwasher category (~15-18% CAGR within appliances), South India premium upgrade segment (~9-10% regional CAGR), and IoT-connected smart appliances (~25%+ CAGR within premium tier) represent India's highest-growth kitchen appliance investment vectors through 2034.

Emerging Market Opportunities

India's rural kitchen appliances market represents the kitchen appliances industry's largest underdeveloped frontier. A rural-optimized refrigerator addressing India's rural electrified-but-unserved households could create an incremental market segment by 2034 that no current appliance brand has systematically pursued beyond entry-level product listing.

Investment Themes

- Dishwasher market development as India's largest untapped category opportunity: IFB's category education model is demonstrating 18%+ annual category growth as critical mass is achieved. Investment in the category of education could accelerate the category toward 5% urban penetration by 2030, creating a dishwasher market opportunity.

- Smart home ecosystem development creating appliance brand lock-in value: Samsung SmartThings and LG ThinQ demonstrate that connected appliance ecosystems generate 40-50% higher repurchase rates and 25-30% higher average transaction values as connected users prefer the same-brand second appliances for seamless integration. An Indian brand developing a comprehensive smart home kitchen ecosystem could create India's first domestic smart kitchen platform, capturing the premium segment.

Future Market Outlook (2026-2034)

The India kitchen appliances market is projected to grow from USD 6.51 Billion in 2025 to USD 12.53 Billion by 2034, delivering a 7.32% CAGR over the forecast period. The market's anchor value of USD 9.27 Billion in 2030 represents a kitchen appliances industry at a structural inflection point, where smart IoT-connected appliances have transitioned from a premium niche to mainstream urban purchase, the dishwasher category has crossed 5% urban household penetration to enter a self-sustaining category growth, and India's built-in kitchen segment has grown to 15-20% of premium residential real estate specifications nationally.

Three structural forces define India's kitchen appliances market growth trajectory with high confidence through 2034: India's urban middle-class expansion creates a demand compounding effect that sustains above-GDP appliance market growth regardless of macroeconomic cycles; PLI scheme manufacturing investment enabling cost-competitive India-made appliances that expand the addressable market by reducing effective price points at every product tier, simultaneously improving domestic manufacturer margins and making quality appliances accessible to India's household segment; and India's 5G-enabled smart home ecosystem creating brand-loyalty lock-in among urban premium buyers who invest in connected kitchens and prefer brand-ecosystem consistency for subsequent purchases.

Research Methodology

Primary Research

Primary research comprised structured interviews with 65+ industry stakeholders (2025), including VP Sales and Marketing directors from LG Electronics India, Samsung India, Whirlpool of India, IFB Industries, and Havells India; category buyers from Croma (Infiniti Retail), Reliance Digital, and Amazon India Kitchen & Home; BEE (Bureau of Energy Efficiency) star rating program officers; CEAMA (Consumer Electronics and Appliances Manufacturers Association) industry officials; consumer research interviews with 200+ household appliance buyers across South, North, West, and East India; and modern kitchen studio owners across Bengaluru, Mumbai, Delhi, and Hyderabad.

Secondary Research

Secondary research encompassed CEAMA (Consumer Electronics and Appliances Manufacturers Association) annual market data 2024-2025, BEE Appliance Efficiency Database 2025, GfK India Kitchen Appliances Market Share Report Q4 2025, Euromonitor International India Home Appliances Data 2025, company annual reports, Amazon India Best Seller and market data analysis, Flipkart Electronics category GMV data, Government of India PLI White Goods scheme disbursement reports, Ministry of Housing and Urban Affairs smart city appliance data, and India real estate market reports (Knight Frank, JLL India). Over 95 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up product type x structure models calibrated against GfK India quarterly sell-out data by product category, BEE registration volume growth rates by product category, CEAMA annual shipment data, e-commerce category GMV growth from Amazon and Flipkart public disclosures, and residential real estate delivery data for the built-in kitchen segment projection. Key inputs include India household income quintile growth projections, rural electrification completion timeline (REC Limited data), BEE star rating threshold changes and their historical market disruption impact models, PLI scheme manufacturing capacity addition schedules, and India urban household formation rates.

India Kitchen Appliances Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Refrigerators, Microwave Owens, Induction Stoves, Dishwasher, Water Purifiers, Others |

| Structures Covered | Built-In, Free Stand |

| Fuel Types Covered | Cooking Gas, Electricity, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Online Stores, Departmental Stores, Others |

| Applications Covered | Residential, Commercial |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | LG Electronics, SAMSUNG, Whirlpool Corporation, Havells India Ltd., Bajaj Electricals India, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India kitchen appliances market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the India kitchen appliances market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India kitchen appliances industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Kitchen Appliances Market Report

The India kitchen appliances market reached USD 6.51 Billion in 2025, driven by rising urban middle-class disposable income, pandemic-driven home cooking adoption that permanently elevated appliance ownership, e-commerce penetration unlocking Tier-2/3 city demand, and India's luxury real estate boom creating built-in kitchen specification demand.

The market grows at 7.32% CAGR during 2026-2034, reaching USD 12.53 Billion by 2034, driven by middle-class household expansion, PLI-enabled cost reduction expanding the addressable market, smart IoT ecosystem brand lock-in, dishwasher category adoption crossing the tipping point, and East India's electrification unlocking first-time buyer households.

Refrigerators lead at 28.7% through India's household penetration. Induction stoves grow fastest at ~8.9% CAGR, driven by Pigeon's range democratizing induction cooking, making electricity-based cooking financially advantageous.

Free stand leads at 92.0% as India's non-modular kitchen households purchase appliances independently across all retail channels.

South India leads at 32.9%, driven by Tamil Nadu, Kerala, and Karnataka's highest per-capita appliance ownership, Kerala's Gulf remittance-funded premium appliance demand, Bengaluru's IT workforce premium purchase behavior, IFB's Goa manufacturing creating South India product availability advantages, and South India's dual-income household culture favoring time-saving kitchen appliances.

Leading companies include LG Electronics, SAMSUNG, Whirlpool Corporation, Havells India Ltd., and Bajaj Electricals, among others.

The market is projected to reach approximately USD 9.27 Billion by 2030, with smart IoT appliances at Tier-1 city sales, dishwashers crossing 5% urban household penetration, the built-in kitchen market growth, and e-commerce serving Tier-3 towns with installation services.

LG ThinQ and Samsung SmartThings connected kitchen platforms generate 40-50% higher repurchase rates and 25-30% higher average transaction values as connected users prefer brand-ecosystem consistency.

Tamil Nadu's urban refrigerator penetration, Kerala's Gulf remittance economy enabling premium appliance spending, Karnataka's Bengaluru IT workforce premium purchase behavior, IFB's South India manufacturing proximity, universal electrification since the 1990s, and South India's matrilineal household income directed toward consumer durables collectively create India's highest-intensity kitchen appliance market.

Three priority opportunities: PLI-enabled domestic manufacturing, capturing cost advantages as 15-25% import duty elimination improves competitive positioning; dishwasher category development, investing in education to accelerate adoption toward 5% urban penetration; and smart home kitchen ecosystem development for Indian brands to capture premium segment loyalty through comprehensive IoT integration, competing with LG ThinQ and Samsung SmartThings.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)