India Laptop Market Size, Share, Trends and Forecast by Type, Design, Screen Size, Price, End Use, and Region, 2026-2034

India Laptop Market Size & Forecast 2026-2034

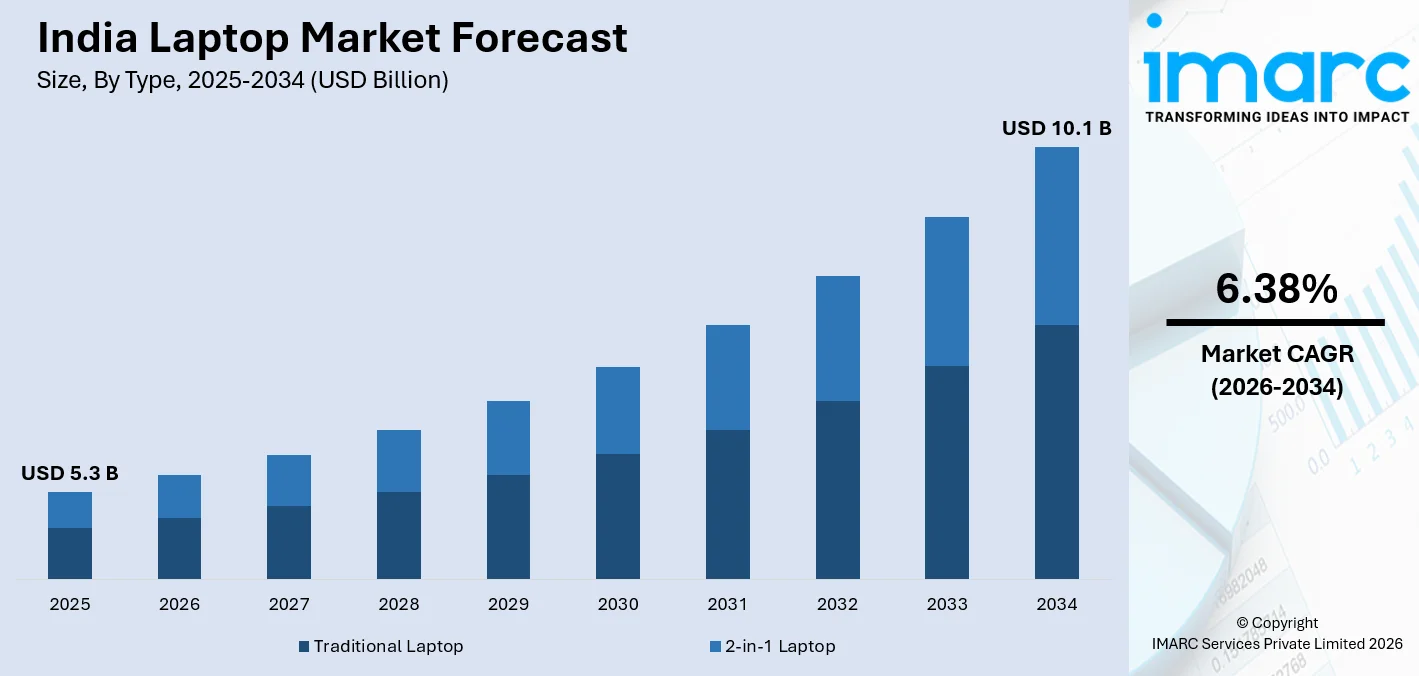

The India laptop market, valued at USD 5.3 Billion in 2025, is on a firm upward trajectory and is projected to reach USD 10.1 Billion by 2034, growing at a CAGR of 6.38% during 2026-2034. This growth is further fueled by a combination of underlying structural demand drivers such as the rapid pace of digital adoption, increasing e-governance initiatives, robust growth in the online education segment, and a nascent but rapidly evolving startup culture that is changing the face of computing in India, both in urban and rural India. The Ministry of Electronics and Information Technology (MeitY) announced an investment of INR 41,863 crores and a production value of INR 2,58,152 crores in January 2026. These approvals are expected to generate 33,791 direct employment opportunities.

To get more information on this market Request Sample

India Laptop Industry Analysis - Key Insights

- Traditional Laptop commands 72.6% of type share in 2025 - Their reliability, cost-effectiveness, and recognition among the student community, professionals, and SMEs continue to make them the most sought-after laptops in the country.

- Notebook leads at 48.9% of design share in 2025 - The optimal combination of cost-effectiveness, specifications, and usability among the student community, professionals, and SMEs ensures the dominance of the notebook segment as the most sought-after type in the country.

- 15.0” to 16.9” leads at 36.4% of screen size share in 2025 - The price bracket of the laptops offered under this category ensures the optimal combination of portability and display size, making them equally popular among the student community using e-learning tools and professionals requiring high usability to manage multitasking.

- INR 40,000 to INR 80,000 dominates at 41.7% of price share in 2025 - The price bracket of the laptops offered under this category ensures the optimal combination of aspirational value and cost-effectiveness, making them highly popular among young professionals, college-goers, and entrepreneurs.

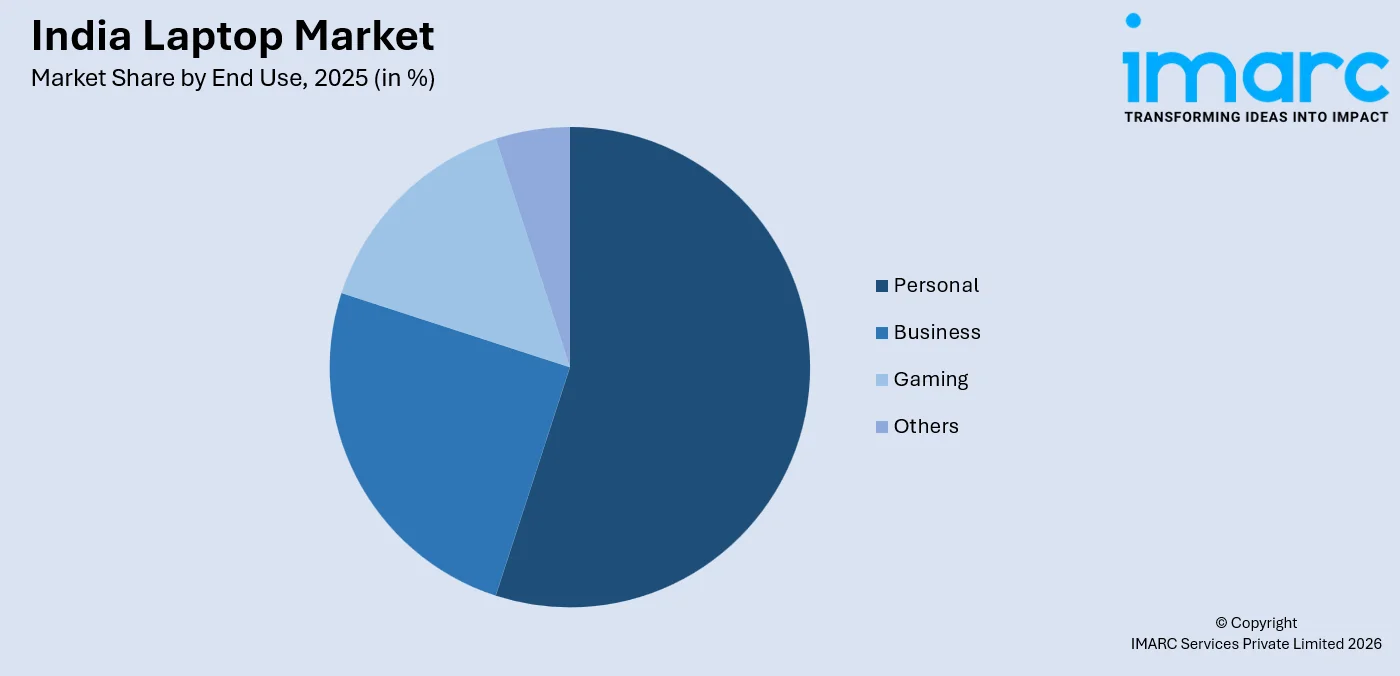

- Personal leads at 52.8% of end use share in 2025 - The ownership of the laptops among the Indian populace for individual usage such as educational needs, entertainment, freelancing, etc. ensures the dominance of the country as the largest market for laptop sales.

- South India leads regionally at 33.5% in 2025 - The tech-savvy culture of the region, the presence of IT hubs such as Bengaluru, Hyderabad, Chennai, etc., and the high literacy rate of the region sustain the largest market share of laptop sales.

India Laptop Market Trends and Dynamics 2026

Market Trends

Remote work culture and hybrid employment models are reshaping laptop demand

The professional environment in India has experienced a revolutionary shift since the advent and proliferation of hybrid working patterns. The laptops have become an integral part of the professional environment in India. The shift towards flexible employment patterns in Corporate India has resulted in a consistent demand for laptops that can handle video conferencing and other resource-intensive applications. According to the 2025 workforce survey undertaken by NASSCOM, over 80% of India’s IT professionals are engaged in permanent or semi-permanent hybrid employment patterns. The trend is consistent in terms of replacement and new sales in all the key cities and Tier 1 cities in India. The manufacturers have responded to these requirements by launching laptops that are specifically designed for the Indian environment. The laptops offer a slim design, all-day battery life, MIL-spec ratings for durability, and Wi-Fi 6E connectivity. The regional language support and dual-keyboard layouts are becoming integral parts of the mid-range laptops in India. The trend is expected to boost the India laptop market in the future.

Digital education expansion is driving structural, long-term laptop adoption

With the rapid growth of the online education sector in the country, the laptop has become a vital academic aid for the academic community, from students at the school-going age to undergraduate students, as well as professionals seeking to acquire additional skills. The efforts of the government to distribute laptops, the digital literacy drive, as well as the rapid growth of EdTech platforms, have cumulatively widened the scope of the academic community from which the laptop industry can draw its customers, reaching the hitherto untapped semi-urban population. The India Brand Equity Foundation (IBEF) states that digital channels currently account for 62% of the student enrollment base in the country, which speaks volumes for the reliance placed on the product within the current Indian academic landscape.

This base is not limited to the urban population either, as the current trend for parents of students in Tier 2 and Tier 3 cities is to spend on the purchase of laptops, as opposed to other luxury goods, as a means of investing in the education of their children. The industry is responding to this trend by launching packages with app subscriptions, antivirus solutions, as well as warranty, thereby reaching the family buyer, creating opportunities for repeat purchase, as well as brand loyalty for the emerging generation of technology users in the country.

Growth Drivers

Rising disposable incomes and consumer financing accessibility

India's expanding middle class and increasing per capita disposable income are increasingly transforming the laptop from a professional tool to a common household technology product. The democratization of consumer finance, enabled by zero-cost EMI options, 'buy now, pay later' platforms, and cashback offers during festive seasons, has significantly reduced the purchase cost for the average consumer, especially for first-time buyers in semi-urban and rural areas. The major e-commerce platforms, namely Flipkart and Amazon, have regularly reported laptops as the highest-grossing category during festive sales, reflecting the sustained intent of consumers, which is not limited to peak demand during the festive season.

Additionally, the growth of organized retail for electronics brands, including Croma, Reliance Digital, as well as brand-owned experience centers, has expanded the reach for consumers to get a 'touch and feel' of the product, thereby increasing the willingness of traditional buyers to purchase a laptop. The warranty and service center network have also enhanced the confidence of buyers after the purchase, making the ownership of a laptop a less intimidating prospect for the digitally evolving mid-market consumer in the country.

Government initiatives and PLI schemes for local manufacturing

The Production Linked Incentive scheme introduced by India for IT hardware has emerged as a major structural catalyst for the laptop market in India, helping drive investments in laptop manufacturing and reducing the overall cost of laptops sold in the country. The government's Make in India initiative for laptop original equipment manufacturers, including international brands, and domestic electronics manufacturers is gradually reducing dependence on imported laptops while creating a cost-effective inventory ecosystem for laptop consumers in India.

The government's Production Linked Incentive scheme has already seen commitments from various multinational brands, including HP, Dell, and Lenovo, for increasing their assembly operations in India. Analysts are of the view that this would result in faster inventory replenishments, lower logistics costs, and higher product customization for laptop consumers in India. The state government schemes that offer laptops to students in Uttar Pradesh, Tamil Nadu, Karnataka, and other states continue to drive volume demand for laptops, thereby supporting the overall laptop market forecast in India.

- Expansion of the Gaming Industry: The online gaming industry is expected to grow to USD 9.1 billion by 2029 from 3.7 billion in 2024 (IBEF). This would lead to an increased demand for gaming laptops with dedicated GPUs, cooling systems, and high refresh rate screens for gaming enthusiasts.

- Startups Ecosystem and Growth of Entrepreneurship Culture: The country ranks third globally as a startup ecosystem with over 115,000 registered startups as of 2025. This would ensure the consistent demand for reliable performance-oriented laptops for the technology, fintech, healthtech, and creative industries.

- 5G Deployment and Connectivity-Optimized Laptops: The 5G rollout is also rapidly expanding in the country. This would lead to an increased demand for 5G-enabled laptops with 5G modems and Wi-Fi 6 connectivity for cloud access for professionals who operate outside the broadband environment.

- Affordability of Chinese Brands and Domestic Brands: Brands like Infinix, realme, and domestic laptop manufacturers are launching their products for the mass market segment for below INR 30,000. This would increase the overall laptop user base as first-timers would also be attracted to laptop purchases.

Market Restraints

High price wars and margin squeeze: The presence of low-cost Chinese brands, domestic assemblers, and established international OEMs competing heavily in the same price bands has led to a significant squeeze on the average selling prices. This is beneficial for the end consumer but creates a margin squeeze for the middle-tier manufacturers who must invest heavily in promotional expenses to maintain brand presence.

Infrastructure gaps in Tier 3 and Rural India: While significant progress has been made in the digital infrastructure space, power reliability, high-speed internet penetration, and authorized service support remain gaps that continue to impact the penetration of products in the most rural parts of India.

Smartphone substitution for price-sensitive consumers: Where mobile internet is the primary driver of digital adoption, the feature-rich smartphone is increasingly replacing the use case for a basic laptop for surfing the internet, social media, and basic document editing. For some segments of consumers, the incremental value proposition of a laptop over a high-end smartphone is difficult to rationalize.

India Laptop Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Traditional Laptop | 72.6% | 2025 |

| Design | Notebook | 48.9% | 2025 |

| Screen Size | 15.0" to 16.9" | 36.4% | 2025 |

| Price | INR 40,000 to INR 80,000 | 41.7% | 2025 |

| End Use | Personal | 52.8% | 2025 |

| Region | South India | 33.5% | 2025 |

Type Insights

Traditional Laptop - 72.6% Market Share (2025) | Leading Type

The traditional laptops have maintained their dominance in the laptop market of India. This segment leads the market by a large margin, making up almost three-fourths of the overall laptop market size in 2025. The dominance of traditional laptops can be attributed to the overall familiarity of the form factor, the reliability of the traditional design for professional as well as academic needs, and the overall cost-effectiveness of traditional laptops over the 2-in-1 hybrid versions.

Additionally, the large student base of India—the largest in the world—coupled with the financially savvy nature of small businesses, ensures the traditional clamshell form factor is the default solution for most users. Hardware upgradeability is an important distinguishing factor among traditional laptops. This segment of traditional laptops allows users to upgrade the RAM as well as the hard drive of the laptop. This increases the overall lifecycle of the traditional laptop. This segment leads the overall laptop market of India due to the institutional buying habits of schools, colleges, and government agencies. Traditional laptops are the default choice of most of these segments due to the overall compatibility of the traditional form factor with a large number of operating systems. Additionally, the overall acquisition cost of traditional laptops is lower.

|

Segment Breakdown Traditional Laptop (72.6%) · 2-in-1 Laptop |

Design Insights

Notebook - 48.9% Market Share (2025) | Leading Design

The notebook segment leads the laptop design preferences in India, supported by its mainstream standing that caters to the widest cross-section of customers. With an affordable price point falling under the INR 25,000 to INR 80,000 category, the notebook offers the best balance of computing power in a traditional form factor that is equally popular among new customers, students, and professionals requiring a cost-effective computing solution. The widespread availability of notebooks through mass retail channels, online stores, and government tender programs has helped the category achieve the default laptop status among the Indian populace, including those residing in rural areas.

The dominance of the design segment can be attributed to the functional buying behavior of the Indian customer base. Unlike the ultrabook segment, which enjoys a premium due to its thin form factor and premium materials, the notebook offers an adequate display size, computing power, and battery life to the Indian customer base. Companies such as HP, Lenovo, Dell, and ASUS have focused on placing the largest volume of products under the notebook segment due to the functional buying habits of the mainstream Indian customer.

|

Segment Breakdown Notebook (48.9%) · Ultrabook · Others |

Screen Size Insights

15.0" to 16.9" - 36.4% Market Share (2025) | Leading Screen Size

Laptops in this range of screen sizes between 15" and 16.9" are the most popular in India, accounting for over one-third of all laptop sales in 2025. This is also due to the close match of this laptop size range to Indian consumers’ tastes, where users can expect a viewing experience that is significantly higher than that offered by smartphones or tablets but not as unwieldy as larger laptop sizes that are closer to workstations. This is particularly important for students who need to do complex coursework, professionals who need multiple windows open for applications, and home users who need to stream content for entertainment.

The usability of this laptop size is also augmented by its weight, where the majority of 15" laptops sold in India fall in the range of 1.8-2.2 kg, offering adequate portability for students or commuters but also offering larger keyboards that are suitable for finance professionals who need full numeric keypads for data entry applications. The consistency of this laptop size over several years is also a reflection of Indian consumers’ consensus on this issue, which is not likely to alter significantly during the forecast period of 2026-2034.

|

Segment Breakdown 15.0" to 16.9" (36.4%) · Up to 10.9” · 11" to 12.9” · 13" to 14.9" · More than 17" |

Price Insights

INR 40,000 to INR 80,000 - 41.7% Market Share (2025) | Leading Price

The INR 40,000 to INR 80,000 price segment represents the optimal price segment for India’s laptop market. The segment accounts for more than two-fifths of the overall market volume in 2025. The segment caters to a remarkably diverse consumer base. The segment includes laptops for college students who want their first high-end computing experience. The segment also includes laptops for young professionals who want their first high-end computing experience. The segment also includes laptops for SME operators who want high-end computing for professional use. Within this segment, customers can choose from 11th or 12th generation Intel Core i5 and i7 chips.

Customers can also choose from 8GB to 16GB RAM variants. Customers can choose from full-HD IPS displays and solid-state drive variants. The performance characteristics of laptops in this segment can satisfy most professional and academic requirements. Consumer financing has played a remarkably instrumental role in sustaining the dominance of this segment. The no-cost EMI option for 6 to 24 months effectively brings down the monthly expenditure to INR 1,700-3,300. The expenditure is comparable to premium smartphone segment expenditure for middle-class Indian households. The festive season promotions, especially during Diwali sales on Flipkart and Amazon India, focus a high volume of purchasing intent in this segment.

|

Segment Breakdown INR 40,000 to INR 80,000 (41.7%) · Less than INR 40,000 · More than INR 80,000 |

End Use Insights

Access the comprehensive market breakdown Request Sample

Personal - 52.8% Market Share (2025) | Leading End Use

Personal usage accounts for more than half of laptop usage in India in 2025. This is because personal usage encompasses a mix of e-learning, home entertainment, freelance work, and personal productivity, which has made laptop usage a household necessity, as opposed to a professional requirement. In addition, the post-pandemic normalization of work-from-home and study-from-home arrangements will sustain a high baseline for personal laptop usage, which will continue to rise beyond pre-2020 growth rates. This segment includes students, homemakers, freelance workers, content creators, and gaming enthusiasts, among others.

Further, personal usage will receive a boost from the growing usage of laptops for personal and entertainment purposes, such as content creation and gaming. The growing content creation economy in India, with more than 800 million social media users, will drive demand for laptops with high-end features such as graphics, color displays, and processing power for video creation and streaming on social media platforms like YouTube and Instagram, where a growing number of creators are seeking a professional career in social media and video streaming. The gaming segment, in particular, will attract first-time buyers in the age group of 16 to 28, adding a growing number of personal laptop buyers to sustain the dominance of personal usage in the laptop end-user segment in the coming years.

|

Segment Breakdown Personal (52.8%) · Business · Gaming · Others |

Regional Insights

South India - 33.5% Market Share (2025) | Leading Region

The presence of IT hubs in cities like Bengaluru, Hyderabad, and Chennai is also a major reason for this dominance, as these cities together account for over three million technology professionals who upgrade their laptops every year, thereby creating a strong laptop market in this region.

The presence of a strong academic system is also a major reason why this region dominates the laptop market of India, given that this region accounts for a disproportionate number of premier engineering colleges, management schools, and research institutions that create a strong laptop market due to the laptop requirements of students.

The state governments of Tamil Nadu and Karnataka have also initiated large-scale laptop schemes for students, which has helped this region gain a higher laptop market size compared to other regions of India. The presence of a strong after-sales service system, well-developed electronics retail markets, and high internet connectivity rates also contribute to this region's dominant laptop market of India.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

33.5%

|

|

Key States

|

Karnataka, Tamil Nadu, Telangana, Kerala, Andhra Pradesh |

|

Major Growth Drivers

|

IT/BPO industry concentration, premier academic institutions, high digital literacy, state government laptop schemes, strong after-sales networks |

|

Outlook

|

Largest and most technologically mature regional market |

|

Segment Breakdown South India (33.5%) · North India · West and Central India · East and Northeast India |

North India:

North India, which includes the Delhi-NCR region, Uttar Pradesh, and Punjab, has a growing consumer base for laptops. This growth is driven by the increasing number of educational institutes in the region, a growing startup scene in Gurugram and Noida, and a massive student laptop scheme undertaken by the respective state governments. The fact that the Delhi-NCR region is a major hub for corporate houses provides a boost for laptop sales for corporate and SME requirements for professional laptops.

|

Metric

|

Details

|

|---|---|

|

Major Growth Drivers

|

Corporate procurement, state government schemes, education sector growth, e-commerce penetration |

|

Outlook

|

High-growth region with significant government-driven volume |

West and Central India:

The West and Central India regions include the states of Maharashtra, Gujarat, Madhya Pradesh, Chhattisgarh, and Goa. There is an increasing trend of laptop usage among consumers in this region. Mumbai's financial services and media industry are the major growth drivers for laptop demand. The presence of a robust IT and education industry in the city of Pune also fuels the demand for laptops. The MSME industry in the state of Gujarat is also a major growth driver for laptop demand. Madhya Pradesh and Chhattisgarh are also witnessing an increasing trend of laptop demand with the government's initiative towards digital literacy and the development of higher education infrastructure in the states. Mumbai's premium segment is also supporting the demand for ultra books. Goa's hospitality industry is also adding to the laptop demand.

|

Metric

|

Details

|

|---|---|

|

Major Growth Drivers

|

Financial services sector, MSME growth, creative economy, premium consumer spending |

|

Outlook

|

Premium and enterprise-oriented regional market |

East and Northeast India:

East and Northeast India, which includes the states of West Bengal, Odisha, Assam, Sikkim, Meghalaya, Tripura, Mizoram, Manipur, Nagaland, and Arunachal Pradesh, has a growing consumer base for laptops. This is driven by a high number of universities and educational institutions in the region, expanding digital literacy initiatives undertaken by the respective state governments, and a growing information technology services industry based out of Kolkata. Additionally, the Northeast region benefits from targeted government connectivity programs such as Bharat Net, which are steadily improving internet access across remote and hilly areas. This combined region currently has one of the least developed consumer bases for laptops in the country; however, it holds a significant degree of untapped market potential, particularly as urbanization increases in cities like Guwahati, Bhubaneswar, and Kolkata, and as younger, digitally aware demographics enter the workforce.

|

Metric

|

Details

|

|---|---|

|

Major Growth Drivers

|

Digital infrastructure investment, university enrollment growth, IT services expansion |

|

Outlook

|

Emerging growth market with rising digital adoption |

Market Outlook 2026-2034

What is the future outlook of the India Laptop Market?

The India laptop market is expected to sustain consistent, technology-driven revenue growth through 2034.

The Indian laptop market is expected to experience continuous and structurally driven growth during the forecast period, driven by underlying demographic trends, increasing investments in digital infrastructure, and an environment where the government is increasingly recognizing access to digital devices as a key national growth agenda. The country’s population of 1.4 billion+ individuals has a median age of less than 30 years, thereby ensuring a continuous flow of first-time laptop buyers for students, young professionals, and the youth. The compounding effect of increasing disposable incomes, continuously declining real cost of devices due to lower production costs of locally manufactured products under the PLI scheme and increasing consumer finance penetration will drive the market size over time.

The technological evolution of laptop hardware is also expected to act as a growth multiplier for the Indian laptop market over the forecast period. The increasing adoption of artificial intelligence-enabled processing chips, such as those offered by Qualcomm Snapdragon X series or Intel Core Ultra series, is expected to drive hardware upgrade cycles as consumers and enterprises seek to leverage productivity benefits offered by artificial intelligence-enabled processing. The increasing adoption of 5G connectivity options is also expected to drive demand for connectivity-optimized lightweight laptops. The gaming and creator economy are also expected to drive demand for mid-to-high-end laptops among the youth population of the country. Additionally, demand for laptops is also expected to be driven by the country’s educational institutions and government bodies.

India Laptop Market - Leading Key Players

The market for laptops in India is characterized by high competition from multinational brands across the globe and an increasing number of value-focused competitors focusing on India’s price-sensitive mid-market segment. The key players in the market are continually investing in India-specific product localization and improving after-sales support and manufacturing partnerships to further consolidate their position in one of the world’s fastest-growing markets for laptops.

| Company | Leading Brands | Highlights |

|---|---|---|

| HP Inc. | HP Pavilion, HP Envy, HP Spectre | Consistent market leader in India; strong presence across education, SME, and enterprise segments with localized service network |

| Lenovo India | IdeaPad, ThinkPad, Legion | Largest global PC manufacturer; dominates Indian professional and gaming segments through aggressive pricing and extensive after-sales coverage |

| Dell Technologies | Inspiron, XPS, Alienware | Strong enterprise and premium consumer positioning; direct sales model and expanding experience stores reinforce customer acquisition |

Other key players in Indian market are ASUS, Acer, Apple, Samsung, MI, Realme, MSI and other local brands.

Latest Developments & News

- In January 2026, During CES 2026, HP announced a robust 2026 lineup with a strong focus on AI-enabled PCs. The 2026 lineup includes a premium OmniBook Ultra 14, a flexible EliteBook X G2 series that supports different chipsets from Intel, AMD, and Qualcomm, and the rebranding of the OMEN gaming division to HyperX. The key highlights include AI capabilities up to 85 TOPS, OLED screens, and ultra-thin form factors.

- In March 2026, Apple revealed that it is introducing the MacBook Neo, an entry-level laptop designed to increase the company’s presence in value-conscious markets like India. The new product is designed to attract students, young professionals, and first-time users of Apple products who seek a powerful product with a seamless ecosystem experience without the premium price. The new product is part of Apple’s efforts to reach value-conscious consumers while leveraging its large base of iPhone users to drive the adoption of its Mac products in new markets for laptops.

- In January 2026, Lenovo unveiled its concept Legion Pro Rollable gaming laptop at CES 2026, featuring a unique display technology that allows for an expandable OLED display, extending beyond its initial size of a 16-inch screen to an ultrawide format of over 21 inches. This is intended to offer enhanced gaming and interactive experiences through dynamic screen size adjustment, thereby emphasizing Lenovo’s focus on future laptop technology and gaming innovations.

India Laptop Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Traditional Laptop, 2-in-1 Laptop |

| Designs Covered | Ultrabook, Notebook, Others |

| Screen Sizes Covered | Up to 10.9", 11" to 12.9", 13" to 14.9", 15.0" to 16.9", More than 17" |

| Prices Covered | Less than INR 40,000, INR 40,000 to INR 80,000, More than INR 80,000 |

| End Uses Covered | Personal, Business, Gaming, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Acer Inc., Apple Inc., ASUSTeK Computer Inc., Dell Inc., HP Development Company L.P., Lenovo Group Limited, Samsung Electronics Co. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India laptop market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India laptop market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India laptop industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Laptop Market Report

The India laptop market was valued at USD 5.3 Billion in 2025.

The India laptop market is projected to reach USD 10.1 Billion by 2034.

Traditional laptop dominate the market with a share of 72.6% in 2025, driven by their established reliability, broad availability, competitive pricing, and suitability for the vast student, professional, and SME buyer base that forms the backbone of Indian laptop demand.

The Notebook design commands the market with a 48.9% share in 2025, reflecting Indian consumers’ strong preference for mainstream, affordably priced devices that deliver practical computing performance without the premium associated with ultrabook form factors.

The INR 40,000 to INR 80,000 price leads with a 41.7% market share in 2025. This range captures the aspirational mid-market where Indian buyers find the optimal combination of performance, features, and affordability, further supported by consumer financing options that make these devices widely accessible.

Some of the major players in the India laptop market include HP Inc., Lenovo India, Dell Technologies, ASUS India, Acer India, Apple India, Samsung India, MSI India, among others.

Key trends include the growing adoption of AI-PC platforms with integrated NPU processors, the sustained growth of hybrid work arrangements driving professional laptop upgrades, the rapid expansion of India’s gaming and esports community fueling demand for high-performance laptops and increasing regional demand from Tier-2 and Tier-3 cities as digital infrastructure improves.

South India currently leads the India laptop market, accounting for a 33.5% regional share in 2025. The region benefits from the highest concentration of IT and BPO employers, premier academic institutions, high digital literacy rates, and well-developed retail and service infrastructure that together sustain the largest and most sophisticated regional laptop market in the country.

Growth is driven by rising digital education enrollment and government laptop distribution schemes, the increasing hybrid work adoption rate among Indian professionals, the rapid expansion of the gaming and content creation economy, Production Linked Incentive scheme investments reducing device costs through local manufacturing, and the progressive penetration of consumer financing enabling aspirational purchases across India’s expanding middle class.

Challenges include intensifying price competition compressing manufacturer margins, the continued substitution of basic laptop use cases by feature-rich smartphones in price-sensitive segments, infrastructure limitations in Tier-3 and rural markets constraining last-mile distribution and after-sales service delivery, and the risk of demand concentration in urban and semi-urban markets leaving large rural populations underserved.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)