India Leather Chemicals Market Size, Share, Trends and Forecast by Product, Process, Application, and Region, 2026-2034

India Leather Chemicals Market Summary:

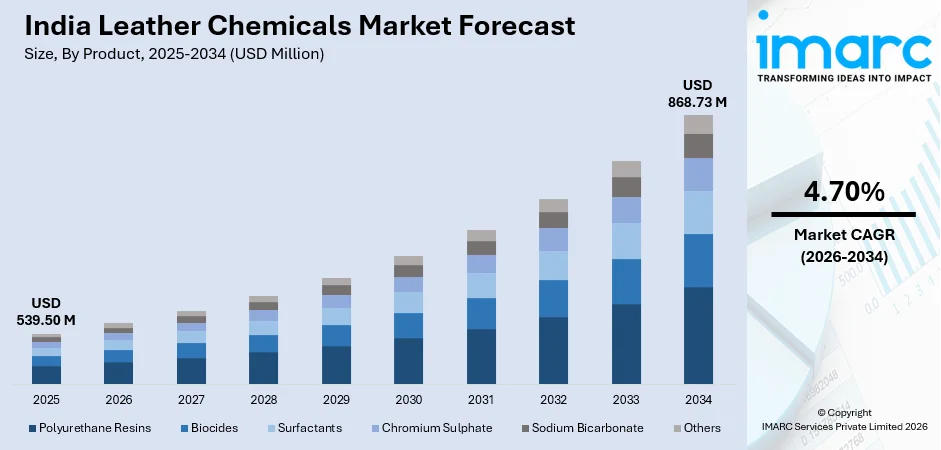

The India leather chemicals market size was valued at USD 539.50 Million in 2025 and is projected to reach USD 868.73 Million by 2034, growing at a compound annual growth rate of 4.70% from 2026-2034.

The India leather chemicals market is propelled by expanding domestic leather production, rising demand for high-performance finishing products, and a robust export-oriented footwear manufacturing base. Government-backed initiatives fostering infrastructure development and sustainable tanning practices are accelerating chemical adoption across multiple applications. The shift toward eco-friendly formulations and innovative processing technologies continues to shape the India leather chemicals market share.

Key Takeaways and Insights:

- By Product: Polyurethane resins dominate the market with a share of 30.5% in 2025, owing to their superior flexibility, water resistance, and durability, making them ideal for premium leather finishing in footwear, upholstery, and garment applications across India.

- By Process: Tanning and dyeing leads the market with a share of 34.2% in 2025, driven by its foundational role in leather processing, ensuring quality, color consistency, and structural stability across diverse end-use sectors including footwear and accessories.

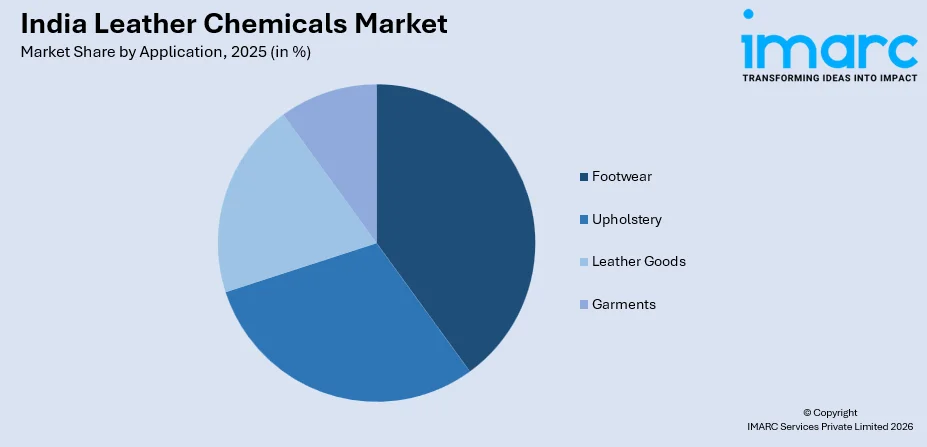

- By Application: Footwear represents the largest segment with a market share of 36.8% in 2025, reflecting India's position as the world's second-largest footwear producer and growing export demand for premium-quality leather shoes across global markets.

- By Region: West India comprises the largest region with 38.5% share in 2025, driven by well-established leather production clusters in Maharashtra, thriving chemical manufacturing infrastructure, and strong linkages to domestic and international footwear and leather goods industries.

- Key Players: Key players drive the India leather chemicals market through continuous innovation in eco-friendly formulations, strategic regional expansions, and investment in advanced finishing technologies. Their collaboration with tanneries, footwear manufacturers, and international buyers strengthens supply chains, enhances product quality, and accelerates adoption of sustainable chemical processing solutions across diverse industry segments.

To get more information on this market Request Sample

India is a prominent player in the global market for leather products, with a reputation for being a leading manufacturer and consumer of leather footwear products. The high cattle and buffalo population of India ensures a ready supply of raw hides for processing into leather products, which is a basic advantage for suppliers of leather chemicals. The government's policy guidelines for the development of the leather and footwear industry have created a high demand for leather chemicals by laying emphasis on turnover development and export market growth. The exports of leather and footwear products from India have shown high growth in recent years, which is a reflection of high demand for products in the market, thereby increasing the demand for leather chemicals at every stage of processing. The development of specific schemes for the development of the leather and footwear sectors has helped to create a conducive atmosphere for suppliers of leather chemicals.

India Leather Chemicals Market Trends:

Rising Adoption of Eco-Friendly and Bio-Based Leather Chemicals

India's leather chemicals sector is undergoing a significant transition toward sustainable formulations, driven by increasingly stringent environmental regulations and shifting international buyer preferences. Bio-based substitutes like vegetable tannins, enzyme-based processing agents, and plant-derived colors are gradually taking the place of conventional chemical inputs in tanneries across key manufacturing clusters. The implementation of zero liquid discharge policies in industrial tanning zones has accelerated this trend, encouraging chemical manufacturers to develop low-volatile organic compound and non-toxic solutions. International demand for verifiably sustainable leather goods, particularly from European and North American markets, is compelling Indian exporters to integrate green chemistry practices into their processing workflows, creating sustained long-term growth in eco-conscious chemical segments.

Increasing Demand for High-Performance Finishing Chemicals

The surge in premium leather applications across footwear, automotive interiors, and luxury accessories is driving a corresponding rise in demand for specialized finishing chemicals in India. As domestic consumers increasingly gravitate toward premium, branded leather goods and global buyers seek superior surface quality and durability, tanneries are investing in advanced polyurethane-based coatings, wax emulsions, and cross-linking agents. These chemicals impart critical functional properties including scratch resistance, color fastness, and tactile quality that distinguish high-value finished leather from commodity-grade materials. The trend is closely linked to India's growing footwear export momentum, where strict international quality specifications require consistent and reproducible chemical finishing standards.

Technological Advancements in Tanning and Dyeing Processes

Innovations in tanning and dyeing technologies are reshaping chemical usage patterns across India's leather processing industry. The adoption of chrome recycling systems and high-exhaustion tanning processes is reducing chemical waste while maintaining the high quality required for export-grade leather. Additionally, the diffusion of computerized color-matching systems and digital print-compatible dye formulations is enabling tanneries to meet precise international color specifications efficiently. These technological upgrades, partly encouraged through schemes supporting the Central Leather Research Institute's collaboration with industry stakeholders, are improving both the precision and environmental profile of the tanning and dyeing process, prompting greater adoption of specialized chemical inputs across Indian leather production clusters.

Market Outlook 2026-2034:

The market for leather chemicals in India is expected to record a robust and continuous growth pattern over the course of the forecast period, driven by a favorable combination of demand-side and supply-side factors. The rising growth rate of India’s domestic footwear and leather products market, along with a healthy export market, is expected to maintain a consistent demand for chemicals at all stages of processing. The government’s initiatives in the form of the Indian Footwear and Leather Development Programme and the Focus Product Scheme are also expected to boost investments in infrastructure development in the leather industry, which would further fuel demand for leather chemicals. The trend of using environmentally friendly chemicals and high-quality finishing agents is also expected to create differentiation among players in the market. The rising demand for leather in automobiles and high-end products is also expected to create incremental demand for high-quality leather chemicals. The rising investments in R&D and collaborative partnerships between players in different countries are also expected to improve the quality of chemicals in the market. The market generated a revenue of USD 539.50 Million in 2025 and is projected to reach a revenue of USD 868.73 Million by 2034, growing at a compound annual growth rate of 4.70% from 2026-2034.

India Leather Chemicals Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product |

Polyurethane Resins |

30.5% |

|

Process |

Tanning and Dyeing |

34.2% |

|

Application |

Footwear |

36.8% |

|

Region |

West India |

38.5% |

Product Insights:

- Biocides

- Surfactants

- Chromium Sulphate

- Polyurethane Resins

- Sodium Bicarbonate

- Others

Polyurethane resins dominate with a market share of 30.5% of the total India leather chemicals market in 2025.

Polyurethane resins have emerged as the most extensively utilized product in India's leather chemicals market, owing to their exceptional performance characteristics across a broad range of leather processing applications. Their unique combination of flexibility, mechanical strength, water repellency, and abrasion resistance makes them indispensable in the finishing and coating stages of leather production. These properties are particularly critical in footwear manufacturing, where the finished leather must withstand sustained mechanical stress while maintaining aesthetic appeal. The versatility of polyurethane-based formulations enables their adaptation across multiple substrate types, from full-grain bovine leather to split leather and suede, ensuring consistent finishing quality across diverse product lines.

The sustained dominance of polyurethane resins in the India leather chemicals market is further reinforced by continuous innovation in resin chemistry and formulation design. Manufacturers are progressively developing water-based polyurethane systems that maintain the performance advantages of traditional solvent-borne variants while aligning with tightening environmental compliance requirements and zero liquid discharge mandates. Growing emphasis on recyclable and low-emission finishing materials is accelerating the transition toward next-generation polyurethane technologies that balance functional performance with ecological responsibility. This convergence of regulatory imperatives and evolving end-market quality expectations is expected to sustain polyurethane resins as the leading product segment throughout the forecast period.

Process Insights:

- Tanning and Dyeing

- Beamhouse Chemicals

- Finishing Chemicals

Tanning and dyeing leads with a share of 34.2% of the total India leather chemicals market in 2025.

Tanning and dyeing chemicals represent the most critical and volume-intensive chemical input category in the leather processing value chain, directly determining the fundamental quality attributes of finished leather. The tanning process transforms raw animal hides into stable, durable, and commercially viable leather by chemically cross-linking collagen fibers, preventing decomposition and imparting desired physical properties. Dyeing chemicals subsequently impart colorfastness, surface uniformity, and aesthetic depth to the processed leather. In India, where tanning clusters in Tamil Nadu, Uttar Pradesh, and West Bengal process large volumes of bovine and caprine hides annually, the demand for tanning and dyeing chemical inputs remains consistently high and closely correlated with overall leather production volumes.

The dominance of tanning and dyeing chemicals in India's leather chemicals market is also shaped by the growing adoption of advanced tanning technologies that improve efficiency and environmental performance. Chrome-based tanning agents, which have historically anchored this segment, are increasingly being supplemented by vegetable and synthetic tanning alternatives as Indian tanneries respond to international buyer sustainability mandates. Major tanning clusters are progressively embracing zero liquid discharge technologies and renewable energy integration to meet the rigorous environmental expectations of export markets in Europe and North America, demonstrating the transformative shift occurring within the tanning and dyeing chemical segment toward more responsible and innovative processing approaches.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Footwear

- Upholstery

- Leather Goods

- Garments

The footwear segment exhibits a clear dominance with a 36.8% share of the total India Leather Chemicals market in 2025.

The footwear segment commands the largest share of the India leather chemicals market, reflecting the country's status as the world's second-largest producer and consumer of leather footwear. India's established manufacturing clusters in Tamil Nadu, Uttar Pradesh, Punjab, and West Bengal produce millions of pairs of leather shoes annually for both domestic consumption and international export. Each pair of leather footwear requires chemical inputs at multiple production stages including beamhouse processing, tanning, dyeing, and finishing, creating a sustained and high-volume demand stream for leather chemicals. The expanding export orientation of Indian footwear manufacturers, combined with rising domestic premiumization, further intensifies chemical requirements per unit of output.

India's robust export growth in leather and footwear directly amplifies demand for high-performance finishing and tanning chemicals, as international buyers from the United States, Germany, and the United Kingdom impose stringent quality and sustainability specifications on sourced leather footwear. Meeting these exacting standards requires consistent and reproducible chemical processing at every production stage, incentivizing tanneries to adopt premium formulations that enhance surface quality, durability, and compliance credentials. The continued influx of foreign investment into India's footwear manufacturing sector further reinforces the footwear segment's leading position within the leather chemicals market, generating sustained incremental demand for specialized chemical inputs across expanding production capacities.

Regional Insights:

- North India

- South India

- East India

- West India

West India represents the leading segment with a 38.5% share of the total India leather chemicals market in 2025.

West India holds the leading position in the regional market for leather chemicals in India, driven by the presence of well-developed leather and leather chemicals manufacturing facilities in Maharashtra. The state is home to prominent leather clusters in Kolhapur, Bhiwandi, and Mumbai, which are known for their specialization in producing leather products such as sandals, shoes, and other leather items. The high contribution of Maharashtra to national leather sandal production capacity, along with a well-developed distribution network for specialty chemicals, makes West India a major regional market for both domestic and international leather chemicals.

The region is also well-positioned for potential partnerships between domestic leather chemicals players and international specialty chemicals companies looking to expand their presence in the domestic market, given the presence of prominent financial and commercial hubs in the region. Vinati Organics, a Mumbai-based manufacturer of specialty chemicals with a specific portfolio of leather chemicals, is a notable example of West India's potential to support high-tech specialty chemicals production. The government’s initiatives to develop leather clusters in the region are expected to maintain West India’s leading regional market position over the forecast period.

Market Dynamics:

Growth Drivers:

Why is the India Leather Chemicals Market Growing?

Government Initiatives and Policy Support for the Leather Sector

India's leather chemicals market has received substantial impetus from a series of targeted government policies designed to strengthen the leather and footwear industry's global competitiveness. The Indian Footwear and Leather Development Programme represents a flagship intervention, channeling substantial budgetary resources into infrastructure development, environmental compliance support, technology modernization, and export promotion across the leather value chain. The Union Budget 2025-26 further reinforced sectoral support through the introduction of a Focus Product Scheme targeting a major increase in industry turnover and export earnings, creating significant downstream demand for specialty leather chemicals. The government's reduction of Basic Customs Duty on wet blue leather to zero effective February 2025, combined with the elimination of export duty on crust leather, has reduced raw material costs for tanneries and incentivized expanded processing activity. These policy measures collectively expand operational activity at tanneries and leather goods manufacturers, translating into heightened consumption of chemical inputs across every processing stage, from beamhouse operations through tanning, dyeing, and finishing. Additionally, the establishment of mega leather clusters with centralized effluent treatment facilities supports chemical suppliers in integrating their offerings within organized production environments.

Expanding Footwear and Leather Goods Export Sector

India's emergence as a leading global exporter of leather footwear and leather goods has become one of the most powerful structural drivers of the leather chemicals market. As the world's second-largest footwear producer, India benefits from deep manufacturing expertise, abundant raw material availability, and cost-effective production conditions that attract international sourcing partners. The adoption of the China-plus-one diversification strategy by global leather brands has accelerated the redirection of sourcing orders toward Indian manufacturers, creating sustained growth in leather processing volumes. This expanding export activity creates a compounding demand effect for leather chemicals, as higher processing volumes require greater quantities of chemical inputs at each stage of production. International buyers from the United States, Germany, and the United Kingdom impose stringent quality and sustainability requirements on their Indian suppliers, which incentivizes the adoption of premium and specialized chemical formulations that enhance leather quality and compliance. The resulting upgrading of chemical inputs across India's export-oriented tanneries has meaningfully increased average chemical consumption per unit of processed leather, elevating market value beyond what volume growth alone would suggest.

Rising Domestic Demand for Premium Leather Products

India's rapidly expanding middle-class consumer base, combined with accelerating urbanization and increasing disposable incomes, is generating strong domestic demand for premium leather products including footwear, upholstery, leather goods, and garments. This premiumization trend is fundamentally reshaping the quality requirements imposed on leather chemical inputs, as manufacturers serving domestic branded markets must meet exacting standards for aesthetic consistency, durability, and surface finish. Higher-value leather goods require more sophisticated chemical processing across tanning, dyeing, and finishing stages, resulting in greater volumes and superior grades of chemical inputs per unit of production. India's robust fashion and lifestyle sector, combined with the growing presence of organized retail and e-commerce platforms, is expanding market access for premium leather goods to a wider consumer base. The automotive sector represents an additional and increasingly significant demand channel, as India's growing passenger vehicle market drives sustained demand for high-quality leather upholstery requiring specialized automotive-grade chemical treatments. Furthermore, rising awareness among Indian consumers regarding the traceability and sustainability credentials of leather goods is encouraging manufacturers to invest in bio-based and eco-certified chemical formulations, further elevating the value profile of chemical inputs consumed across the domestic market.

Market Restraints:

What Challenges the India Leather Chemicals Market is Facing?

Environmental Regulatory Compliance Challenges

The leather tanning process generates substantial volumes of chromium-laden effluents, sulfides, and solid waste that require intensive chemical treatment and management. Indian tanneries, particularly smaller and medium-sized units, face significant financial and operational burdens in meeting increasingly stringent environmental compliance requirements, including zero liquid discharge mandates. The cost of installing and maintaining requisite effluent treatment infrastructure can constrain production capacity and reduce profitability, discouraging chemical innovation investment and limiting overall market expansion for leather chemical suppliers dependent on tannery sector growth.

Raw Material Price Volatility

The production of leather chemicals is highly dependent on petrochemical derivatives, mineral salts, and agricultural inputs whose prices are subject to significant and often unpredictable fluctuations. Chromium salts, vegetable tannins, and polyurethane precursors have experienced notable price instability driven by supply chain disruptions, geopolitical tensions, and shifting agricultural conditions. Such volatility makes accurate cost forecasting difficult for chemical manufacturers, squeezes profit margins when price increases cannot be passed through to tannery customers, and creates a challenging environment for long-term production planning and investment decision-making within the India leather chemicals market.

Competition from Synthetic Leather Alternatives

The growing consumer and manufacturer interest in synthetic and vegan leather alternatives presents a structural demand restraint for the India leather chemicals market. As polyurethane and polyvinyl chloride-based synthetic leathers become increasingly sophisticated in their aesthetic and functional properties, they attract adoption from footwear and accessories brands seeking to reduce costs and address animal welfare concerns. The displacement of genuine leather by synthetic alternatives in certain product categories proportionally reduces the demand for leather chemicals, creating a moderate but persistent headwind for market participants dependent on natural leather processing volumes and end-market expansion.

Competitive Landscape:

India’s leather chemicals market has a competitive environment with local presence of multinational specialty chemical producers and domestic players with extensive technical knowledge of local leather processing requirements. Multinational players use their worldwide research and development facilities to develop innovative, environment-friendly, and technically advanced products to cater to local tannery requirements. Domestic players compete on the basis of cost advantage and local understanding of environmental regulations. Strategic partnerships of local distributors with international chemical producers have emerged as an essential factor of competition in this sector. Companies are increasingly focusing on the formulation of environment-friendly products to cater to the local tanning industry. Chrome-free tanning agents, water-based polyurethane finishers, and biodegradable surfactants have emerged as essential products of the sector with multinational players focusing on formulating environment-friendly products to cater to local tanning requirements.

Recent Developments:

- In January 2024, Pidilite Industries Limited formed a strategic partnership with Italy-based Syn-Bios, a specialist in leather tanning research and global chemical marketing, to distribute Syn-Bios products across India, Sri Lanka, Bangladesh, Nepal, and Vietnam. The alliance also encompasses a technical collaboration aimed at providing integrated chemical solutions to the leather processing industry across South Asian markets.

- In November 2024, Stahl, a global specialty chemicals company, divested its wet-end leather chemicals business to Syntagma Capital, with the transaction encompassing manufacturing sites in Italy and India and a workforce of approximately 428 employees. The deal, which was subject to regulatory approval and expected to close in early 2025, reflects a strategic repositioning by Stahl toward specialty coatings and sustainable chemistry innovation.

India Leather Chemicals Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Biocides, Surfactants, Chromium Sulphate, Polyurethane Resins, Sodium Bicarbonate, Others |

| Processes Covered | Tanning and Dyeing, Beamhouse Chemicals, Finishing Chemicals |

| Applications Covered | Footwear, Upholstery, Leather Goods, Garments |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Leather Chemicals Market Report

The India leather chemicals market size was valued at USD 539.50 Million in 2025.

The India leather chemicals market is expected to grow at a compound annual growth rate of 4.70% from 2026-2034 to reach USD 868.73 Million by 2034.

Polyurethane resins dominated the market with a share of 30.5%, driven by their superior flexibility, water resistance, durability, and adaptability across finishing and coating applications in premium leather processing, serving key end-use sectors such as footwear, upholstery, and garments.

Key factors driving the India leather chemicals include government support through the IFLDP and export promotion schemes, growing footwear and leather goods exports, rising domestic demand for premium leather products, and advancements in sustainable tanning and finishing chemical formulations across India's tannery clusters.

Major challenges include stringent environmental compliance requirements for tannery effluent management, raw material price volatility affecting chemical production costs, competition from synthetic leather alternatives reducing natural leather processing volumes, and limited adoption of advanced chemical technologies among small-scale tanning units.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)