India Legal Services Market Size, Share, Trends and Forecast by Service, Mode, End User, and Region, 2026-2034

India Legal Services Market Size, Share, Trends & Forecast (2026-2034)

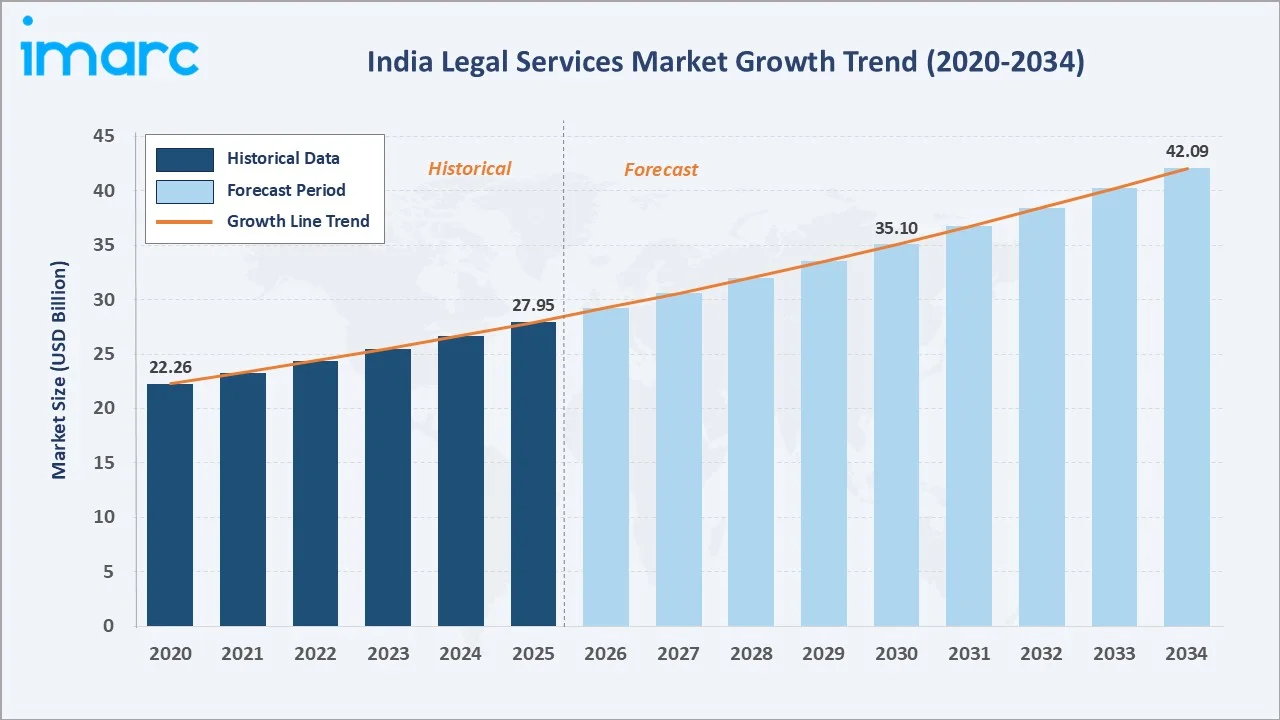

The India legal services market reached USD 27.95 Billion in 2025 and is projected to reach USD 42.09 Billion by 2034, growing at a CAGR of 4.66% during 2026-2034. India's accelerating GDP toward a USD 5 Trillion economy, PLI-scheme-driven M&A and FDI activity, legaltech platform adoption, rising judicial awareness across SME and private consumer segments, and India's pending court cases collectively anchor the market's sustained growth through 2034. Offline legal services dominate at 72.3%. Large businesses lead the end-user at 26.8%. North India commands 31.6% of market revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 27.95 Billion |

|

Forecast Market Size (2034) |

USD 42.09 Billion |

|

CAGR (2026-2034) |

4.66% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Mode |

Offline Legal Services (72.3%, 2025) |

|

Largest End User |

Large Businesses (26.8%, 2025) |

|

Leading Region |

North India (31.6%, 2025) |

The market expanded from USD 22.26 Billion in 2020 to USD 27.95 Billion in 2025, anchored at USD 35.10 Billion in 2030, and forecast to reach USD 42.09 Billion by 2034. COVID-19 permanently transformed India's legal service delivery, virtual hearings, online document filing, and digital legal research platforms established the infrastructure backbone for online legal services that has sustained post-pandemic growth above the pre-COVID trajectory.

To get more information on this market, Request Sample

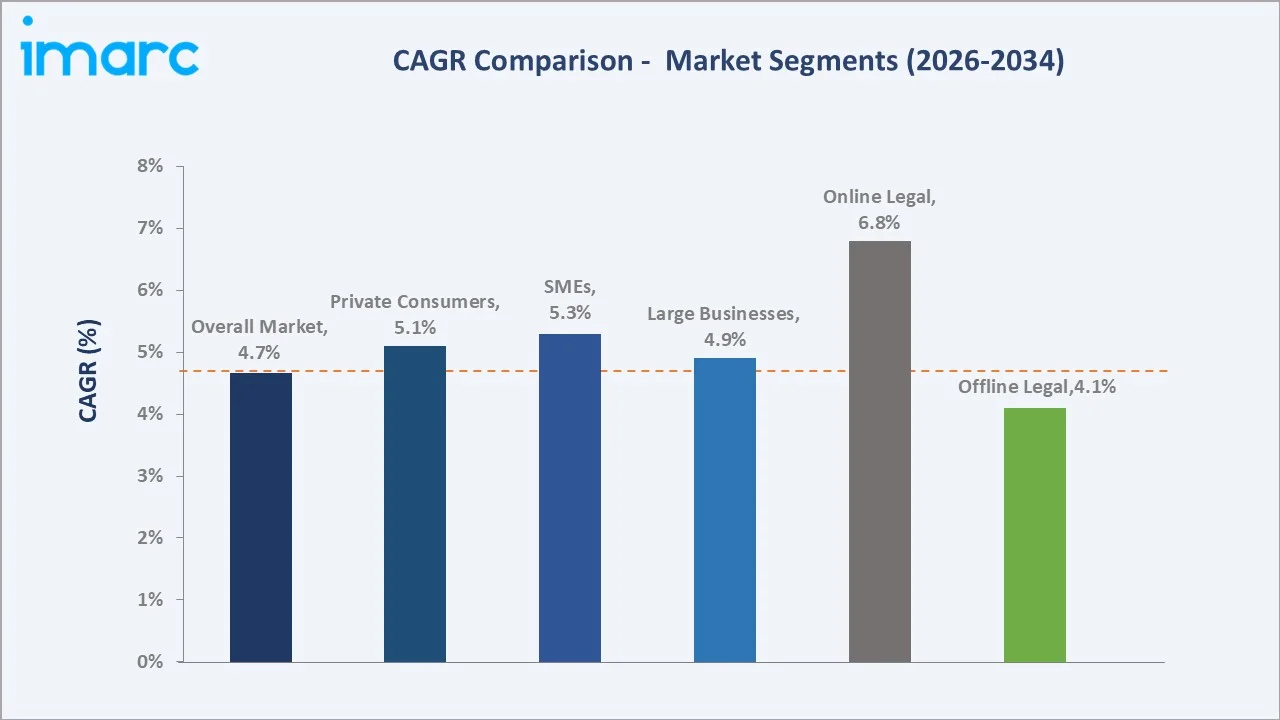

Online legal services grow fastest at ~6.8% CAGR (2026-2034), driven by legaltech platforms serving SME and private consumer demand for accessible, affordable, technology-enabled legal services. SMEs grow at ~5.3% CAGR as India's 63 Million MSME enterprises increasingly require formal legal structuring for GST compliance, employment contracts, intellectual property protection, and e-commerce platform agreements, creating an addressable legal services market.

Executive Summary

The India legal services market reached USD 27.95 Billion in 2025, positioning India as one of Asia's largest legal services markets and one of the world's most dynamic legal services ecosystems by complexity and growth potential. India's common law heritage, enrolled advocates, Supreme Court as the world's most litigated constitutional court, and the simultaneous co-existence of a world-class tier-1 M&A law firm ecosystem alongside massive unmet rural legal access needs define a market of extraordinary breadth and structural complexity. The market is projected to reach USD 42.09 Billion by 2034 at 4.66% CAGR.

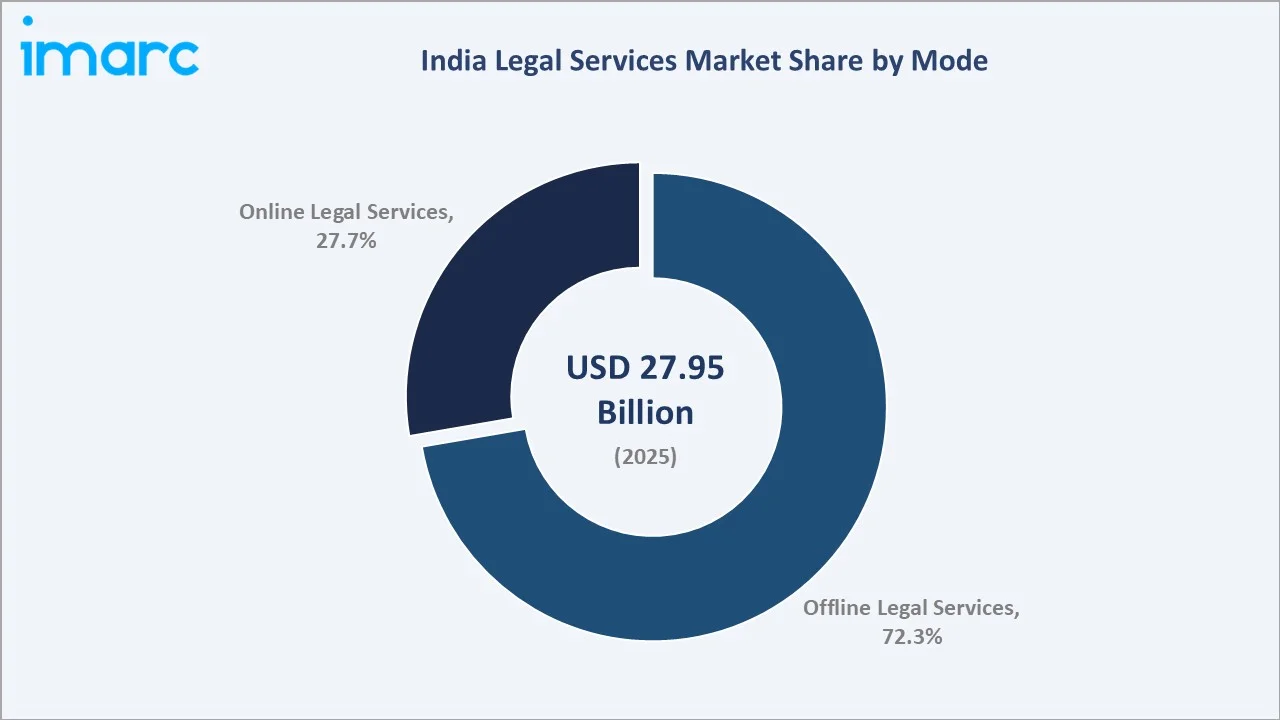

Offline legal services command 72.3% market share (2025), reflecting the inherently personal, relationship-driven, and procedurally complex nature of Indian legal practice, particularly in litigation, real estate transactions, family law, and criminal defense where physical court appearances, document registration at sub-registrar offices, and face-to-face client consultation remain legally or practically mandatory. North India at 31.6% leads through Delhi's concentration of India's Supreme Court, national regulatory tribunals, and all top-tier law firms' national headquarters.

Key Market Insights

|

Insight |

Data |

|

Dominant Mode |

Offline Legal Services - 72.3% share (2025) |

|

Largest End User |

Large Businesses - 26.8% market share (2025) |

|

Leading Region |

North India - 31.6% market share (2025) |

Key Analytical Observations Supporting The Above Data:

- Offline at 72.3% reflecting India's legally mandated physical proceedings and relationship-intensive service culture: Despite COVID-19's digital acceleration, India's legal system retains substantial physical proceeding requirements, particularly in family law, criminal defense, and property disputes, and remains deeply relationship-driven, with senior client trust requiring face-to-face consultation that online platforms cannot replicate for complex, sensitive, or high-stakes matters.

- Large businesses at 26.8% driven by India's M&A boom and complex regulatory compliance requirements: India transactions requiring legal advisory across due diligence, regulatory approvals, documentation, and post-merger integration compliance.

- North India at 31.6% anchored by Delhi NCR's regulatory tribunal concentration and Supreme Court jurisdiction: Delhi NCR is India's undisputed legal epicenter, creating India's highest legal services demand concentration in a single geography and requiring all tier-1 law firms to maintain flagship Delhi offices for regulatory practice.

India Legal Services Market Overview

India's legal services market encompasses all professional advisory, representation, documentation, and dispute resolution services provided by advocates enrolled under the Advocates Act 1961, legal entities registered under BCI regulations, and increasingly legaltech platforms delivering AI-augmented or technology-facilitated legal services. The market spans litigation, transactional legal services, regulatory advisory, intellectual property, taxation, employment and labor law, and alternative dispute resolution.

The ecosystem integrates individual advocates, law firms ranging from premier tier-1 firms through mid-tier regional firms to small neighborhood practices, the judiciary, legaltech platforms, legal aid institutions, and end-user clients spanning the entire economy from global multinationals to individual rural litigants. Macroeconomic factors include strong economic growth, rising foreign direct investment, expanding corporate activity, infrastructure development, and increasing cross-border trade.

Market Dynamics

To evaluate market opportunities, Request Sample

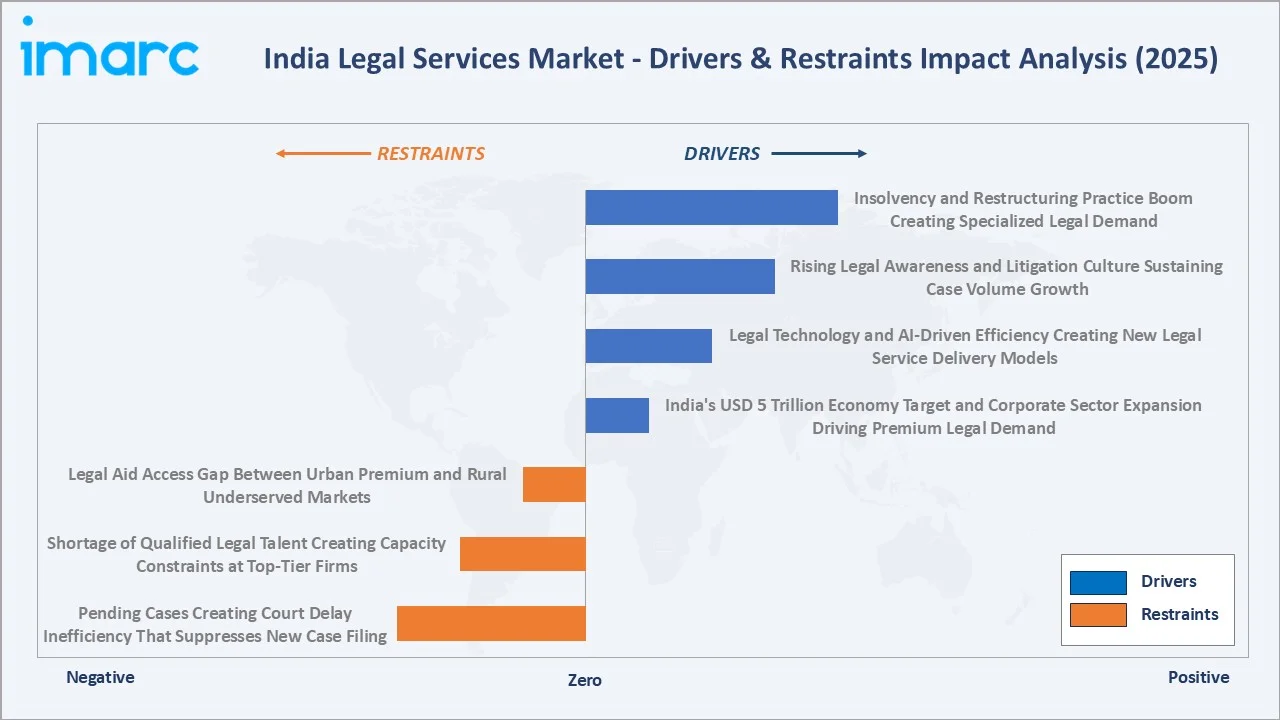

Market Drivers

- India's USD 5 Trillion Economy Target and Corporate Sector Expansion Driving Premium Legal Demand: India’s Minister for Commerce & Industry, Mr. Piyush Goyal, stated that the country is “on track to achieve a $5 trillion economy by 2027. This economic expansion is generating unprecedented corporate legal demand.

- Legal Technology and AI-Driven Efficiency Creating New Legal Service Delivery Models: India's legal technology ecosystem is generating both new client segments and operational efficiency improvements within law firms. AI tools are creating a paradox, improving lawyer efficiency while simultaneously generating new legal demand from the AI governance, data privacy, and algorithmic accountability regulatory landscape.

- Rising Legal Awareness and Litigation Culture Sustaining Case Volume Growth: India's court system receives a high number of new cases annually despite already having pending cases, reflecting a population that increasingly asserts legal rights through litigation.

Market Restraints

- Pending Cases Creating Court Delay Inefficiency That Suppresses New Case Filing: India's 5.6 crore pending court cases create a rational disincentive for potential litigants to initiate court proceedings when commercial resolution will outlast the business dispute's relevance. The pendency also constrains the legal services market's expansion; each pending case represents a legal services engagement that should be a completed matter, generating new case engagements.

- Shortage of Qualified Legal Talent Creating Capacity Constraints at Top-Tier Firms: India's National Law Universities (NLUs) produce very few qualified graduates annually for the premium legal services market. This supply is structurally insufficient for the junior associate positions, and their peers collectively need to fill annually. This talent scarcity constrains tier-1 firm revenue growth to their training and absorption capacity rather than client demand, representing a structural market growth ceiling.

Market Opportunities

- Insolvency and Restructuring Practice Boom Creating Specialized Legal Demand: Each large insolvency requires legal teams of 20-50 lawyers across due diligence, creditor representation, and resolution plan documentation, creating high-fee, long-duration mandates that represent the legal market's highest-growth practice segment at 15%+ annually.

- Data Privacy and Technology Law Creating Entirely New Legal Practice Areas: Data privacy and technology law are creating strong market opportunities as businesses increasingly require legal support for data protection, cybersecurity, AI governance, fintech regulations, digital contracts, and platform compliance. With India’s evolving digital regulatory framework and rising technology adoption, law firms are expanding specialized practices around privacy audits, breach response, cross-border data transfers, and compliance advisory.

Market Challenges

- Legal Aid Access Gap Between Urban Premium and Rural Underserved Markets: The legal aid access gap is a major challenge as premium legal services remain concentrated in urban centers, while rural and low-income populations often lack affordable, qualified, and timely legal support. This creates uneven market penetration, limits formal legal service adoption, and increases dependence on informal dispute resolution or under-resourced public legal aid systems.

- Regulatory Uncertainty Around Legaltech AI and Unauthorized Practice of Law: Regulatory uncertainty around legaltech AI, unclear rules on AI-generated legal advice, liability, confidentiality, and data handling, can slow adoption among law firms and clients. Concerns over unauthorized practice of law may also restrict how legaltech platforms operate, limiting innovation, scalability, and investor confidence in AI-driven legal services.

Emerging Market Trends

1. Legaltech Platform Ecosystem Maturing Beyond Document Automation

Legaltech platforms in India are maturing beyond basic document automation by offering integrated solutions for e-discovery, contract lifecycle management, compliance tracking, legal research, dispute resolution, and workflow management. This trend is reshaping the legal services market as law firms and corporate legal teams adopt technology to improve efficiency, reduce turnaround time, manage large case volumes, and deliver more scalable client services.

2. International Arbitration Hub Ambition Driving India Seat Arbitration Growth

India’s ambition to become an international arbitration hub is driving growth in India-seated arbitration as businesses seek faster, cost-effective, and locally enforceable dispute resolution alternatives. Government support for institutional arbitration, rising cross-border commercial disputes, and improved arbitration infrastructure are encouraging law firms to build stronger arbitration and dispute resolution practices.

3. Foreign Law Firm Entry Opening New Competition and Partnership Dynamics

In January 2026, Malaysian law firm Skrine launched a dedicated India desk to support the growing cross-border business activity between India and Malaysia. The platform is designed to assist Indian companies operating in Malaysia and Malaysian firms with interests in India by bringing together the firm’s expertise in corporate transactions, M&A, energy, projects, dispute resolution, and regulatory advisory. This creates partnership opportunities between Indian and global law firms, helping clients access broader international expertise while pushing domestic firms to strengthen specialization and service quality.

4. In-House Legal Department Expansion Changing Law Firm Revenue Mix

In-house legal department expansion is changing India’s law firm revenue mix as large corporates increasingly handle routine contracts, compliance, and advisory work internally. This is pushing law firms toward higher-value services such as complex litigation, M&A, regulatory strategy, arbitration, investigations, and specialized cross-border advisory.

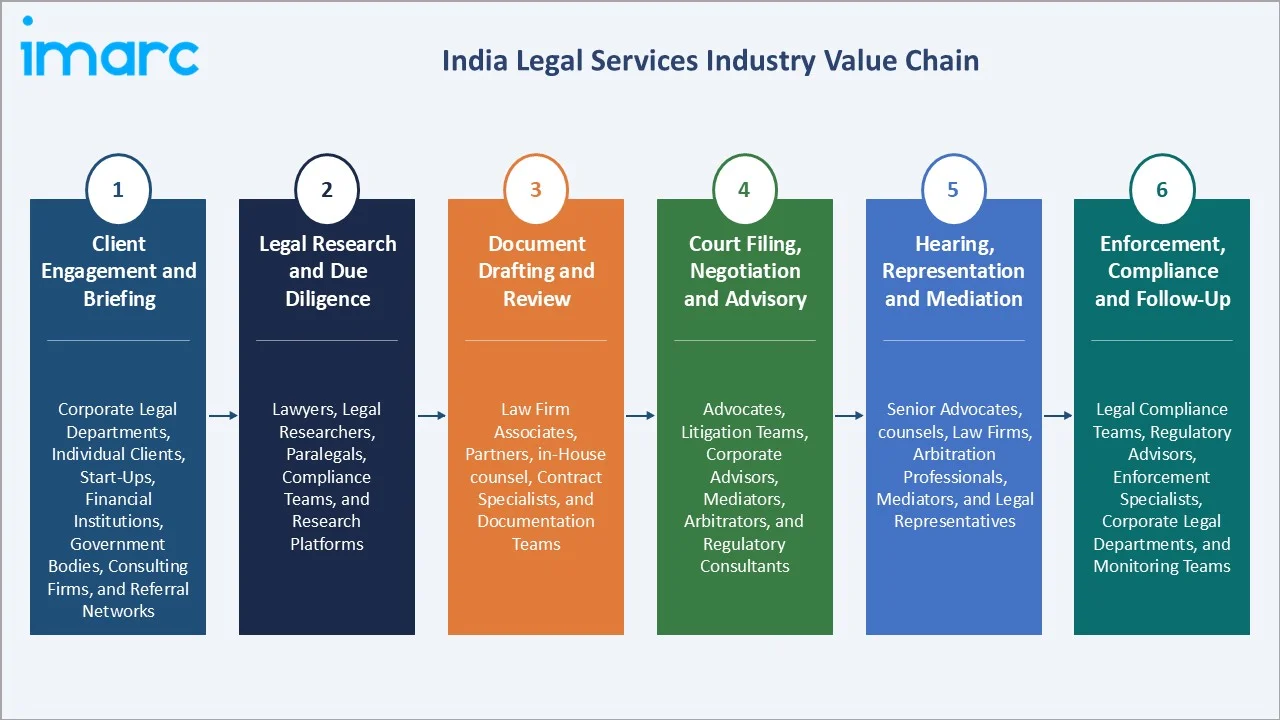

Industry Value Chain Analysis

India's legal services value chain integrates client engagement through legal research, document drafting, regulatory filing, hearing representation, and enforcement compliance, with each stage generating distinct revenue streams and requiring different professional competencies.

|

Stage |

Key Participants |

|

Client Engagement & Briefing |

Corporate legal departments, individual clients, start-ups, financial institutions, government bodies, consulting firms, and referral networks |

|

Legal Research & Due Diligence |

Lawyers, legal researchers, paralegals, compliance teams, and research platforms |

|

Document Drafting & Review |

Law firm associates, partners, in-house counsel, contract specialists, and documentation teams |

|

Court Filing, Negotiation & Advisory |

Advocates, litigation teams, corporate advisors, mediators, arbitrators, and regulatory consultants |

|

Hearing, Representation & Mediation |

Senior advocates, counsels, law firms, arbitration professionals, mediators, and legal representatives |

|

Enforcement, Compliance & Follow-Up |

Legal compliance teams, regulatory advisors, enforcement specialists, corporate legal departments, and monitoring teams |

The court filing, negotiation, and advocacy tier is India's legal value chain's most relationship-intensive segment. Access to skilled senior advocates is a genuine competitive advantage for law firms whose client relationships include senior advocate panel access.

Technology Landscape in the India Legal Services Industry

AI-Powered Contract Review and Management Platforms

AI-powered contract review and management platforms automate clause extraction, risk flagging, obligation tracking, and contract lifecycle workflows. These tools help law firms and in-house legal teams reduce manual review time, improve accuracy, manage high contract volumes, and deliver faster advisory support for corporate, compliance, and transaction-related matters.

Legal Research and Case Analytics Platforms

Legal research and case analytics platforms enabling faster access to statutes, judgments, precedents, regulatory updates, and court records through advanced search and data analytics. These platforms help lawyers assess case trends, judge behavior, litigation risks, and likely outcomes, improving research efficiency, advisory quality, and litigation strategy.

E-Court and Online Dispute Resolution Infrastructure

E-court and online dispute resolution infrastructure enabling digital case filing, virtual hearings, electronic records, and remote dispute resolution. These platforms improve access to justice, reduce procedural delays, lower litigation costs, and create new service opportunities for law firms, mediators, arbitrators, and legaltech providers.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Service | 🔒 | 🔒 | 2025 |

| Mode | Offline Legal Services | 72.3% | 2025 |

| End User | Large Businesses | 26.8% | 2025 |

| Region | North India | 31.6% | 2025 |

By Mode

Offline legal services lead at 72.3% market share (2025). This segment encompasses all legal services delivered through traditional in-person channels such as law firm office consultations, court appearances, document execution at registrar offices, in-person negotiations, and physical filing of court applications.

To access detailed market analysis, Request Sample

Online legal services at 27.7% grow fastest at ~6.8% CAGR, driven by legaltech platforms expanding access, virtual hearings institutionalized post-COVID, online document execution, and AI-powered legal research reducing turnaround time. Online legal services command lower per-matter fees but serve larger client volumes exponentially. This volume-versus-value dynamic sustains the online segment's market size growth despite lower per-engagement revenue.

By End User

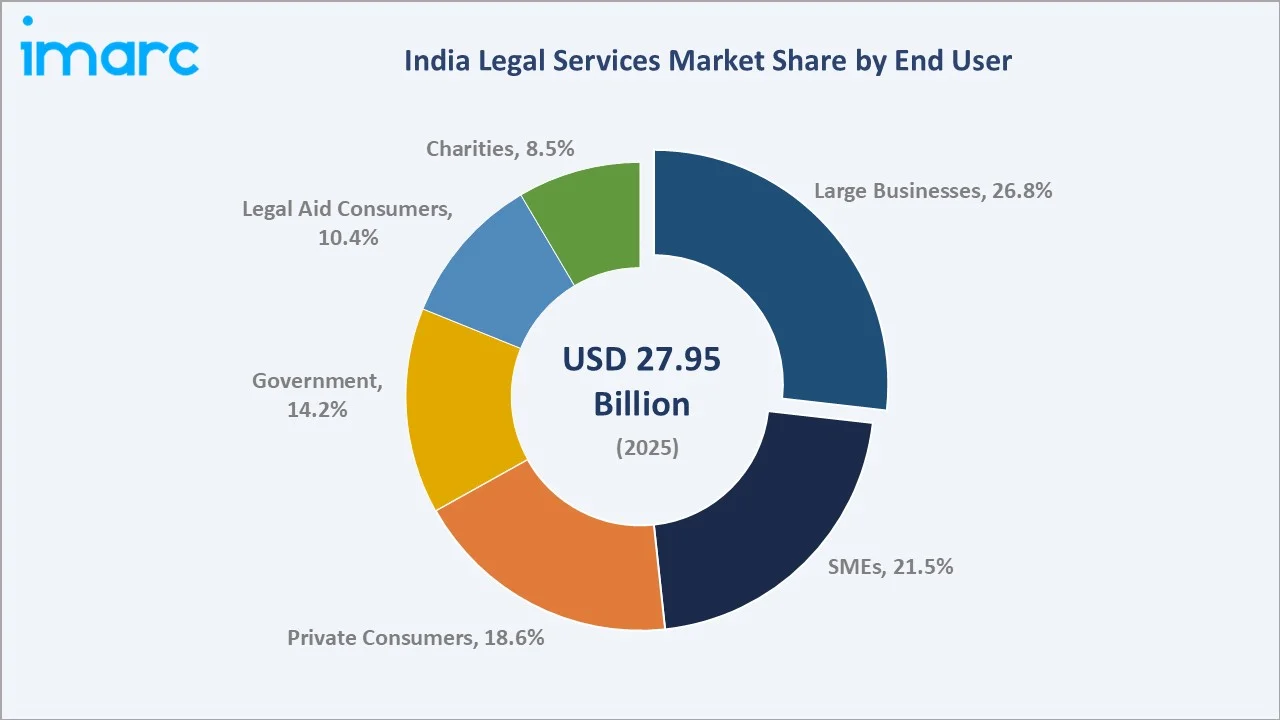

Large businesses lead at 26.8% market share (2025). This segment encompasses listed corporates, MNC subsidiaries, PE-backed unicorns, and private conglomerates requiring full-spectrum legal services across corporate governance, M&A, capital markets, regulatory compliance, employment, IP, and dispute resolution.

SMEs at 21.5% grow fastest at ~5.3% CAGR as 63 Million Indian MSMEs formalize legal processes. Private consumers at 18.6% serve individual legal needs across property disputes, matrimonial law, criminal defense, and consumer protection. Government at 14.2% encompasses Central and State government legal advisory and Law Officers' panel engagements. Legal aid consumers at 10.4% represent facilitated legal aid, with government and court welfare fund subsidization. Charities at 8.5% serve NGOs, trusts, religious institutions, and charitable organizations requiring property, compliance, and registration legal advisory.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

North India |

31.6% |

Strong concentration of courts, tribunals, regulatory bodies, government institutions, public sector enterprises, and corporate headquarters supports steady demand for litigation, compliance, policy advisory, arbitration, taxation, and corporate legal services. |

|

West India |

27.8% |

Presence of financial hubs, capital markets activity, large corporate groups, start-ups, real estate development, ports, and industrial corridors drive demand for M&A advisory, banking and finance law, securities compliance, commercial disputes, and transaction-related legal services. |

|

South India |

24.3% |

Expanding technology, IT services, fintech, manufacturing, healthcare, and start-up ecosystems create strong demand for intellectual property, data privacy, employment law, contract management, regulatory advisory, and corporate legal support. |

|

East India |

16.3% |

Industrial development, mining, infrastructure projects, ports, logistics activity, public sector presence, and regional commercial disputes support demand for environmental law, land and property matters, labor compliance, regulatory advisory, and litigation services. |

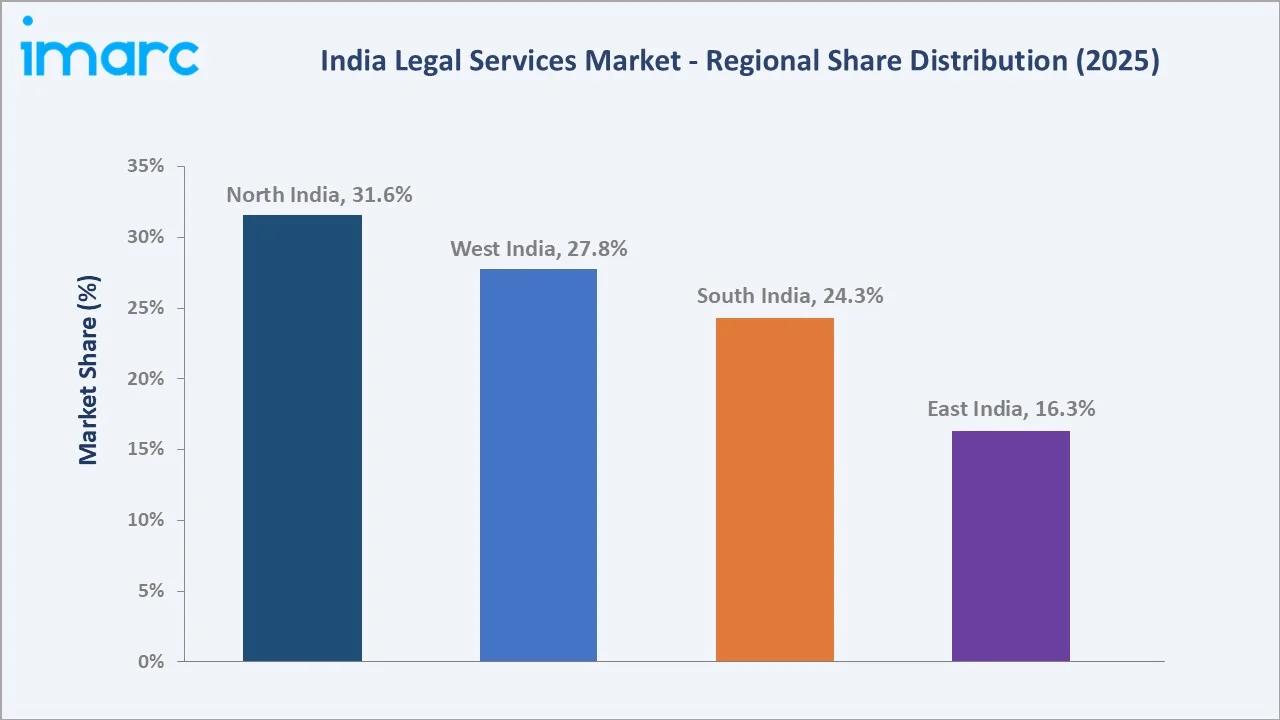

North India's 31.6% dominance reflects the strong presence of the Supreme Court, Delhi High Court, major tribunals, regulatory bodies, government ministries, and public sector institutions concentrated in Delhi NCR. The region also has a high volume of corporate litigation, policy advisory, compliance work, arbitration, taxation, and regulatory matters, making it a key hub for high-value legal services.

West India's 27.8% reflects Mumbai's financial capital status, generating India's highest-value transactional legal mandates. South India's 24.3% is growing fastest as Bengaluru's technology and startup ecosystem, Hyderabad's pharmaceutical sector, and Tamil Nadu's manufacturing corridor create specialized legal practice demand. East India's 16.3% represents Kolkata's traditional commercial law heritage and Odisha-Jharkhand's natural resources legal market.

Competitive Landscape

India's legal services market is highly fragmented. This extreme fragmentation reflects the Advocates Act’s prohibition on law firm corporate structures and the inherently personal, relationship-driven nature of Indian legal practice, where individual advocate reputation drives client selection more than institutional brand.

|

Company Name |

Services |

Market Position |

Core Strength |

|

Cyril Amarchand Mangaldas |

Corporate, Finance, Dispute Resolution |

Market Leader |

With 1000+ lawyers, six pan-India locations, the company is India’s leading full-service law firm, staying ahead of the curve with its ability to provide future-focussed, end-to-end solutions, through both domestic and international collaborations. |

|

AZB & Partners |

Banking & Finance, Competition / Antitrust, Corporate / Mergers & Acquisitions, Data Privacy & Protection, Employment / Labour & Benefits |

Market Leader |

AZB & Partners recognized as a leading Indian Law Firm in 8 Practice Areas with 27 Individual Rankings by the prestigious Chambers and Partners in their Global Rankings, 2026. |

|

Shardul Amarchand Mangaldas & Co |

General Corporate, Private Equity, Banking & Finance, Insolvency & Restructuring, Competition Law, Dispute Resolution |

Strong Challenger |

Committed to investing in the brightest legal talent, the Firm has 800+ lawyers, with 188 partners, who offer solutions across diverse practice areas for industries, the central government and states, regulatory bodies, industry chambers and non-profit organizations. |

|

Khaitan & Co. |

Banking and Finance, Competition / Antitrust, Corporate and Commercial, Corporate Governance, Corporate Restructuring |

Strong Challenger |

More than a century of experience in practising Indian law has lent the company’s rich experience to offer end-to-end legal solutions, in diverse practice areas, for clients across the globe. |

|

JSA |

Corporate, Finance, Disputes |

Established Player |

JSA is a leading national law firm in India with over 700 professionals operating out of 10 offices located in Ahmedabad, Bengaluru, Chennai, Gurugram, Hyderabad, Mumbai and New Delhi. |

The competitive landscape is bifurcating between elite tier-1 full-service firms and emerging specialized boutiques that compete on depth rather than breadth. Legaltech platforms are creating a third competitive tier serving SME and consumer segments at scale through technology-enabled service delivery that traditional law firms cannot economically replicate.

Key Company Profiles

Cyril Amarchand Mangaldas

Cyril Amarchand Mangaldas (CAM) is India's largest law firm by revenues and lawyer headcount, with 1000+ lawyers, six pan-India locations, an office in IFSC (Gift City), Singapore and Abu Dhabi.

- Services: Corporate, Finance, Dispute Resolution

- Recent Developments: In May 2026, Cyril Amarchand Mangaldas elevated 18 lawyers to partnership, effective across its corporate, disputes, finance, and capital markets practices. The promotions highlight the firm’s ongoing expansion, focus on building senior leadership capabilities, and efforts to strengthen its legal expertise and pan-India market presence.

- Strategic Focus: Strengthening high-value corporate, M&A, disputes, finance, capital markets, regulatory, and pan-India advisory capabilities.

Khaitan & Co.

Khaitan & Co. is India's most profitable law firm on a per-partner basis and one of India's oldest and most prestigious full-service firms.

- Services: Banking and Finance, Competition / Antitrust, Corporate and Commercial, Corporate Governance, Corporate Restructuring.

- Recent Developments: In April 2026, Khaitan & Co announced the elevation of 49 members to leadership positions, with 17 members promoted to Partner and 32 to Counsel.

- Strategic Focus: Expanding corporate transactions, M&A, private equity, banking and finance, disputes, tax, intellectual property, and technology-focused advisory services for domestic and global clients.

Market Concentration Analysis

India's legal services market remains structurally fragmented due to restrictions on law firm incorporation as companies, prohibition on non-lawyer investment in law firms, and BCI's regulation of advocate advertising. Top-tier law firms collectively generate high annual revenues from their premier corporate advisory practices.

Market concentration varies dramatically by practice segment; the premium M&A and capital markets legal advisory market is highly concentrated among 6-8 tier-1 firms. The general corporate and SME advisory market is moderately fragmented, with mid-tier firms. The litigation and district court market is extremely fragmented among enrolled advocates. Legaltech platforms are creating the first genuinely scalable and potentially consolidating business models in India's legal market. Regulatory constraints limit concentration. These structural constraints will moderate concentration increases regardless of market growth, sustaining India's uniquely fragmented legal services market structure through 2034.

Investment & Growth Opportunities

Fastest Growing Segments

Online legal services (~6.8% CAGR), SMEs (~5.3% CAGR), IBC insolvency practice (~15%+ within litigation), data privacy and technology law (nascent but growing at 20%+ from a small base), and international arbitration India-seat (~10%+ annually) represent India's highest-growth legal services investment vectors.

Emerging Market Opportunities

India's legal aid market represents the most underserved segment in India's legal services market. Technology-enabled legal aid could serve 10-20x NALSA's current beneficiary count at marginal cost, unlocking a social impact opportunity that also represents a high addressable legal access market currently served by government subsidy and NGO programs.

Investment Themes

- Legaltech platform investment for SME and consumer legal services: India's 63 Million MSMEs represent an addressable legal services market underserved by conventional law firm business models. SaaS-based legal compliance platforms, subscription legal advisory services for SMEs, and AI-powered document automation platforms can serve this market at volumes and price points that create venture-scale technology businesses while expanding legal services market penetration.

- International arbitration infrastructure development: India's ambition to become an international arbitration hub requires investment in infrastructure, case management technology, arbitrator panel development, and legal framework alignment with international best practices.

Future Market Outlook (2026-2034)

The India legal services market is projected to grow from USD 27.95 Billion in 2025 to USD 42.09 Billion by 2034, delivering a 4.66% CAGR over the forecast period. The market's anchor value of USD 35.10 Billion in 2030 represents a fundamentally transformed legal services landscape where online delivery accounts for 35%+ of revenues, AI tools are deployed in 80%+ of tier-1 law firm practices, and India's insolvency process has established the country as Asia's leading restructuring jurisdiction, attracting international creditor advisory mandates to domestic law firms.

Three structural forces define India's legal services market trajectory with exceptional predictability through 2034: India's GDP growth generating proportional corporate and commercial legal advisory demand as economic complexity, regulatory compliance requirements, and transactional activity all scale with economic output; the online legal services disruption reaching inflection point as legaltech platforms achieve the scale, trust, and regulatory clarity needed to serve millions of SME and consumer legal needs at technology-enabled price points that traditional law firms cannot match; and India's potential foreign law firm liberalization creating a competitive transformation of the premium M&A legal market if BCI accepts full liberalization, accelerating premium market growth and quality improvement while intensifying competition for top domestic firms.

Research Methodology

Primary Research

Primary research comprised structured interviews with 60+ industry stakeholders (2025), including Managing Partners from market players; General Counsel executives from BSE-listed companies, PE-backed unicorns, and MNC India subsidiaries; BCI and State Bar Council officers; NALSA program managers; legaltech startup founders; NDIAC and MCIA arbitration center officials; and law school placement officers at NLSIU Bengaluru, NLS Mumbai, and NUJS Kolkata tracking graduate placement trends.

Secondary Research

Secondary research encompassed National Judicial Data Grid (NJDG) pendency statistics 2025, BCI enrollment data (2020-2025), NASSCOM India Legaltech Market Report 2024, SEBI Annual Report 2024-25, NCLT case disposal statistics, NALSA Legal Aid Annual Report 2024, Chambers Asia Pacific India rankings 2025, Legal500 India rankings 2025, IFLR1000 India rankings 2025, ALB Asia Law Awards India 2024-2025, company revenue disclosures from law firm press releases and news, MCA company registration data, DPIIT FDI statistics, and India M&A league table data. Over 100 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up segment models calibrated against GDP-to-legal-spend regression analysis using India's historical data, NCLT/NCLAT case value data for insolvency segment projection, SEBI enforcement action count trends for corporate compliance advisory projection, DPIIT FDI statistics for cross-border legal advisory projection, and legaltech platform user growth models for online segment trajectory. Key inputs include India's IMF GDP growth projections, NJDG case filing growth rates, DPDP Act implementation timeline, foreign law firm liberalization scenario modeling, and BCI enrollment data for supply-side legal talent capacity constraint modeling.

India Legal Services Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Services Covered | Taxation, Real Estate, Litigation, Bankruptcy, Labor/Employment, Corporate, Others |

| Modes Covered | Online Legal Services, Offline Legal Services |

| End Users Covered | Legal Aid Consumers, Private Consumers, SMEs, Charities, Large Businesses, Government |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Cyril Amarchand Mangaldas, AZB & Partners, Shardul Amarchand Mangaldas & Co, Khaitan & Co., JSA, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India legal services market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India legal services market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India legal services industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Legal Services Market Report

The India legal services market reached USD 27.95 Billion in 2025, driven by India's GDP growth toward USD 5 Trillion, PLI-scheme M&A and FDI legal demand, pending court cases sustaining litigation legal services, legaltech platform expansion, and DPDP Act compliance, creating new regulatory legal advisory demand.

The market grows at 4.66% CAGR during 2026-2034, reaching USD 42.09 Billion by 2034, driven by corporate sector expansion, online legal services growth, SME legal formalization, IBC insolvency practice growth, and India's technology regulatory advisory market expansion.

Offline legal services lead at 72.3% through mandatory physical court proceedings, document registration requirements, and relationship-driven professional engagement.

Large businesses lead at 26.8%, served by tier-1 law firms on retainers for M&A, capital markets, and regulatory advisory.

North India leads at 31.6%, anchored by Delhi NCR's Supreme Court, national regulatory tribunals, and all tier-1 law firms' flagship regulatory practice offices concentrated in commercial districts.

Leading law firms include Cyril Amarchand Mangaldas, AZB & Partners, Shardul Amarchand Mangaldas & Co, Khaitan & Co., and JSA, among others.

The market is projected to reach approximately USD 35.10 Billion by 2030, with the growth of online legal services, IBC insolvency practice, and foreign law firms establishing a partial presence.

IBC insolvency practice has become a major growth driver for India’s legal services market by creating steady demand for insolvency resolution, restructuring, creditor advisory, distressed asset transactions, litigation, and tribunal representation.

India's 63 Million MSMEs are growing at ~5.3% CAGR as GST compliance, startup ecosystem, e-commerce platform agreements, and employment law formalization create legal service demand at volumes impossible to serve through traditional offline law firm models, driving legaltech platform adoption.

Online legal services grow at ~6.8% CAGR through legaltech platforms expanding India's legal services addressable market beyond the top-tier law firm clients to millions of SMEs and consumers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade