India Life Insurance Market Size, Share, Trends and Forecast by Type, Premium Type, Premium Range, Provider, Mode of Purchase, and Region, 2026-2034

India Life Insurance Market Size & Forecast 2026-2034

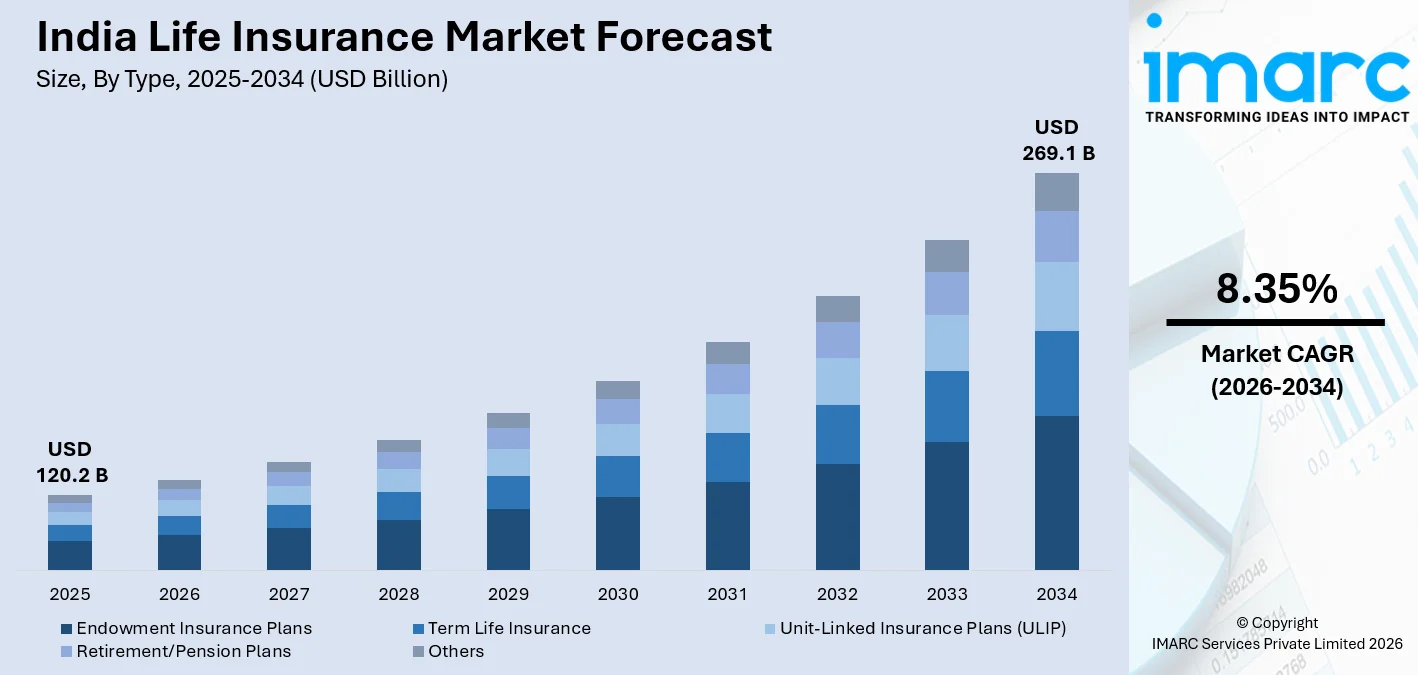

India life insurance market size stood at USD 120.2 Billion in 2025, and it is expected to reach USD 269.1 Billion by 2034, with a compound annual growth rate of 8.35% during 2026-2034. The life insurance market in India is experiencing a constant growth rate due to factors like financial literacy, increase in income levels of the middle-class population, and favourable government initiatives that are enhancing insurance penetration. The government has introduced initiatives like “Insurance for All by 2047” that are helping to enhance life insurance penetration across India. Moreover, favourable taxation policies are also contributing to life insurance market growth. However, despite the growth opportunities, life insurance penetration is still low in India. For example, life insurance penetration was at 2.7% in India during FY 2025.

To get more information on this market Request Sample

India Life Insurance Industry Analysis: Key Insights

- Endowment insurance plans accounted for 36.7% market share by type, in 2025, due to the dual advantage of offering both life cover and guaranteed savings, which is most appealing to risk-averse Indian families who prioritize disciplined long-term saving and wealth creation.

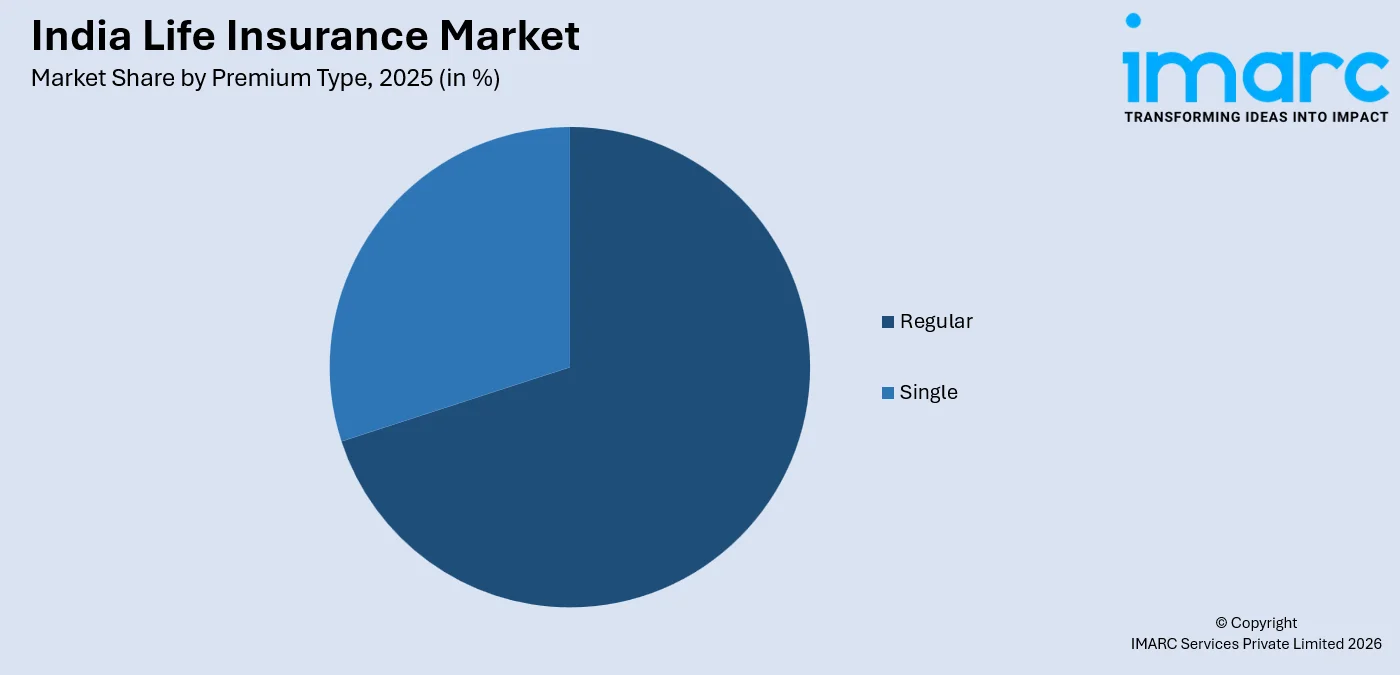

- Regular policies held the largest market share of 68.4% by premium type, in the market in 2025, due to the low premium outflow and the flexibility of paying premiums in regular instalments over the policy term, which is most appealing to Indian families that follow monthly income patterns and prioritize disciplined saving and spending.

- The medium range accounted for the highest market share by premium range, accounting for 44.2% in the market in 2025, due to the dual advantage of being affordable and offering substantial policy benefits, which is most appealing to the growing Indian middle-class population that prioritizes adequate policy benefits without incurring significant premium outflow as policy expenses.

- Insurance companies accounted for the largest market share of 62.5% by provider in 2025, due to their well-established distribution networks and the trust factor that Indian customers place on established insurance brands and their extensive network of insurance agents and bancassurance partners.

- Offline purchase accounted for the largest market share of 71.3% by mode of purchase in 2025, due to the trust factor that Indian customers place on insurance agents and the role of insurance agents in the decision-making process of buying an insurance policy.

- South India remained the leader in the region with a share of 33.8% in 2025, thanks to the high levels of financial literacy and insurance awareness. Major insurance companies and bancassurance networks are present in the region comprising the states of Tamil Nadu, Karnataka, and Kerala.

India Life Insurance Market Trends and Dynamic 2026:

Market Trends

Rapid Digitalisation of Distribution Channels

The Indian life insurance market is witnessing a rapid digitalisation of distribution channels, with many insurance companies opting for online platforms, mobile apps, and digital policy issuance as a means of expansion and cost reduction. Digitalisation of policy purchases through online methods such as online policy issuance, e-KYC, and video-based customer verification has made it easier for young consumers in urban areas to purchase insurance policies. Increased savings and a major shift to digitalisation have propelled India's life insurance industry to surpass $1 trillion in assets under management. Further, the online insurance market is expected to expand rapdily, thus showing a robust growth rate in the adoption of technology for insurance distribution.

Premium Income Growth and Expanding Policy Volumes

Premium income growth and increase in policy volumes indicate an increase in market maturity, and this is seen to be consistent in the life insurance segment. The total premium income earned by life insurance companies in India is around ₹8.86 lakh crore in FY2024-25, growing at around 6.7% annually. On the other hand, private sector life insurance has seen a higher growth rate of around 12% due to aggressive product innovation and expansion. New business premiums are being driven by strong bancassurance partnerships and agency networks. With an increase in participation from private sector players and better product diversity such as ULIPs, term insurance, and retirement products, the market is gradually shifting to a more competitive ecosystem.

Regulatory Liberalization and Increased Foreign Investment

With liberalization and increase in investments, the capital base is being consolidated for the industry, and insurers are able to expand their business and bring in product innovations. The Indian government has announced its intentions to raise the foreign direct investment (FDI) limit to 100% from the existing 74% in the insurance sector to attract global players in the industry. This move is likely to boost investments in infrastructure, increase solvency ratios, and promote technology adoption in the industry. Higher investments from abroad will help bring international standards in risk management and product underwriting, which will improve the overall competitiveness and growth prospects for the life insurance industry in India.

Growth Drivers

The relatively lower levels of insurance penetration and the sizeable uninsured population provide: a substantial structural growth opportunity, making the Indian market one of the most promising for the life insurance segment. While the population size is favorable for the Indian market, the penetration levels for the life insurance segment were recorded at 2.7% penetration in FY 2025. This is relatively lower when compared to the levels in developed markets, which are above 5-7%. With a population of over 1.4 billion people, a considerable segment of the population remains uninsured. With the increasing awareness of the importance of financial planning after the pandemic, people are increasingly preferring to take up life insurance products for risk protection and saving.

The strong economic growth and increase in disposable income: are creating a larger customer potential for life insurance products, especially for the growing middle class in India. India’s GDP growth is among the highest in the world, and with an increase in household income levels, people are in a position to direct more resources towards financial protection and savings products. According to industry estimates, India’s life insurance market has the potential to grow at an average rate of 10.5% between 2025 and 2035, driven by increasing urbanization and financial inclusion. As more and more people enter the formal financial system, the requirement for life insurance products as a means for wealth preservation and protection is on the rise.

Rising Financial Awareness and Protection: Growing awareness of financial security and income protection is one of the major factors contributing to the growth of life insurance in India. This awareness grew manifold after the COVID-19 pandemic hit the country and highlighted the need for financial preparedness among people.

- Rise in Risk Awareness after the COVID-19 Outbreak: The COVID-19 crisis led to a heightened awareness of the risks of mortality among people. As a result, people have begun buying life insurance policies to ensure financial protection.

- Rise in Financial Literacy: Financial literacy programs initiated by insurance companies and financial institutions have led to an increase in life insurance policies among first-time buyers.

- Rise in Income Level of the Middle Class: A growing middle class with a high-income level has helped people purchase life insurance policies and engage in savings schemes.

Market Restraints

Low Insurance Awareness in Rural and Informal Segments: A significant percentage of the Indian population, especially in rural and informal segments of the market, is still unaware of the importance of life insurance. This low financial literacy among the population is likely to continue inhibiting the growth of the market, even as insurance companies expand their presence in rural and semi-urban areas.

Complex Product Structures and Mis-selling Issues: Many insurance products carry complex benefit structures and offer varying returns on investment. This has led to confusion among the population regarding the purchase of insurance products. There have also been instances of mis-selling of insurance products by insurance agents. This has led to low consumer confidence in investing in insurance products.

High Policy Lapse Rates: A significant percentage of policyholders tend to discontinue their insurance plans due to financial constraints. This has led to low policy persistency ratios for insurance companies and has inhibited the growth of the market.

India Life Insurance Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

|

Type |

Endowment Insurance Plans |

36.7% |

2025 |

|

Premium Type |

Regular |

68.4% |

2025 |

|

Premium Range |

Medium |

44.2% |

2025 |

|

Provider |

Insurance Companies |

62.5% |

2025 |

|

Mode of Purchase |

Offline |

71.3% |

2025 |

|

Region |

South India |

33.8% |

2025 |

Type Insights

Endowment Insurance Plans- 36.7% market share (2025) | Leading Type

Endowment insurance products continue to hold the top position in the life insurance segment in India because of the twin benefit of savings and protection of the policyholder's family. It targets the risk-averse households in the country who are working towards securing a high financial goal in life in a gradual manner. The Indian market is benefiting from the growing middle-class population of over 300 million people and the continued dominance of traditional players in the segment, including the Life Insurance Corporation of India. Additionally, the tax advantage under Section 80C of the Income Tax Act, which allows a deduction of ₹1.5 lakh in a financial year on premium payments, helps sustain the demand for savings products.

|

Segment Breakdown Endowment Insurance Plans (36.7%) · Term Life Insurance · Unit-Linked Insurance Plans (ULIP) · Retirement/Pension Plans · Others |

Premium Type Insights

Access the comprehensive market breakdown Request Sample

Regular - 68.4% market share (2025) | Leading Premium Type

The regular premium plans form the foundation of India's life insurance market. These plans are in line with the manner in which people earn and spend their money on a monthly basis. It also helps in inculcating a habit of saving money in the long term. By spreading the premium over a period of 10-25 years, the premium appears manageable compared to paying a lump sum amount at one go. It also helps insurance companies retain customers through regular premium payments through agents, banc assurance channels, or digital platforms such as UPI Autopay. Major players in the industry, including HDFC Life and ICICI Prudential, largely offer protection and savings products based on premium payment structures.

|

Segment Breakdown Regular (68.4%) · Single |

Premium Range Insights

Medium - 44.2% market share (2025) | Leading Premium Range

The mid-range premium segment is the leader in this regard as it offers a balance between cost and reliable coverage for the burgeoning middle-income class in India. The coverage ranges from ₹5 lakh to ₹25 lakh under these policies, making them accessible to salaried employees, small business owners, and first-timers. With an estimated middle class of over 300 million people in India, there is a clear move towards financial security and tax-saving instruments. Insurers such as SBI Life Insurance and Max Life Insurance are working hard to launch mid-tier products to cater to this huge base through agency and bancassurance routes.

|

Segment Breakdown Medium (44.2%) · Low · High |

Provider Insights

Insurance Companies- 62.5% market share (2025) | Leading Provider

The licensed Insurers are at the forefront in terms of market share in the provider space in India, and that is due to the regulations and guidelines provided by the Insurance Regulatory and Development Authority of India. They need robust solvency margins, product approvals, and policyholder protections. Currently, there are multiplr life insurance companies in India, and at the forefront is Life Insurance Corporation of India, which alone has over 250 million policyholders. These Insurers have massive agency networks, with over 1 million agents across the country, and they’re supplemented with bancassurance partnerships with some of the biggest banks in the country. This provides distribution and brand trust with the Indian consumer who wants long-term products.

|

Segment Breakdown Insurance Companies (62.5%) · Insurance Agents/Brokers · Others |

Mode of Purchase Insights

Offline- 71.3% market share (2025) | Leading Mode of Purchase

Offline remains the dominant distribution channel in the market as purchasing a life insurance product in India is essentially about relationships and advice. Most purchases are made through agents, bank branches, or insurance advisors. There are over a million licensed life insurance agents in the country, including those from big players such as Life Insurance Corporation of India and HDFC Life Insurance. Bancassurance partnerships with banks such as State Bank of India add to this lead.

|

Segment Breakdown Offline (71.3%) · Online |

Regional Insights

South India- 33.8% market share (2025) | Leading Region

South India dominates the life insurance market due to higher financial literacy levels, better insurance awareness, and a robust financial services infrastructure. States like Tamil Nadu, Karnataka, and Kerala are reported to have some of the highest levels of insurance penetration in India. These states are followed by a higher per capita income and a savings culture. The region is also home to major life insurance business centers like Chennai and Bengaluru, where several life insurance companies have large operational and customer service centers.

|

Metric

|

Details

|

|---|---|

| Market Share in 2025 | 33.8% |

| Major States | Karnataka, Tamil Nadu, Andhra Pradesh, Telangana, Kerala |

| Key Growth Drivers | High financial literacy, strong savings culture, dense bancassurance and agency networks, high salaried workforce in IT and services sectors |

| Outlook | Strong growth anchored by major insurance operations and distribution hubs in Chennai and Bengaluru |

|

Regional Breakdown South India (33.8%) · North India · West India · East India |

North India:

The North Indian market presents an expanding life insurance market with a high population density and an increase in financial inclusion in states like Uttar Pradesh, Punjab, and Haryana. Metropolises like Delhi and Chandigarh form the hubs of life insurance policy sales with a strong network of agents and a growing need for employment in corporate sectors.

|

Metric

|

Details

|

|---|---|

| Major States | Uttar Pradesh, Punjab, Haryana, Rajasthan, Uttarakhand |

| Key Growth Drivers | Large population base, increasing financial inclusion, expanding bank and insurance distribution networks, rising middle-class income levels |

| Outlook | Growth driven by high policy demand from urban centers including Delhi and Chandigarh |

West India:

The life insurance market in West India is a major market due to a robust industrial base, a high level of urbanization, and a large financial services infrastructure. States like Maharashtra and Gujarat are reported to have a high level of life insurance penetration due to a higher per capita income and a large salaried population.

|

Metric

|

Details

|

|---|---|

| Major States | Maharashtra, Gujarat, Rajasthan, Goa |

| Key Growth Drivers | Strong industrial economy, high urbanization, strong banking and financial services ecosystem, corporate employment concentration |

| Outlook | Stable growth supported by financial services concentration and high insurance awareness in Mumbai |

East India:

The East Indian market presents a developing yet promising life insurance market with a high potential due to an increase in financial awareness and financial inclusion drives of the government in states like West Bengal, Odisha, and Bihar. Cities in these states are gradually growing in terms of insurance penetration, with cities like Kolkata acting as hubs for life insurance companies looking to penetrate tier-2 and tier-3 cities.

|

Metric

|

Details

|

|---|---|

| Major States | West Bengal, Odisha, Bihar, Jharkhand, Assam |

| Key Growth Drivers | Expanding financial inclusion programs, increasing rural insurance awareness, government-backed insurance initiatives, growing penetration of banking services |

| Outlook | Emerging growth region supported by insurance distribution expansion from the regional financial hub of Kolkata. |

Market Outlook (2026-2034)

What is the future outlook of the India life insurance market?

The India Life Insurance market is expected to sustain steady revenue growth through 2034

The future outlook for the India life insurance market is very promising, and it is expected that the market will continue to grow with a steady revenue growth rate up to 2034. The growth of the market will be due to increased financial awareness, growth of middle-class income levels, and increased demand for protection and retirement products. The government's vision of attaining universal insurance coverage by 2047 and the various initiatives taken by the Insurance Regulatory and Development Authority of India will further boost the growth of the market. There will be an increase in the availability of online platforms and insurtech partners, thereby enhancing the availability of life insurance products in tier-2 and tier-3 cities. Moreover, the increased participation of private players and growth of foreign investments will further boost the market growth of the India life insurance market. As the population becomes more financially inclusive and focuses more on risk protection and wealth creation, the India life insurance market is expected to grow with increased demand for protection and savings-related policy segments.

India Life Insurance Market: Leading Key Players

The competitive scenario in the India life insurance industry is marked by a strong presence of a public sector company along with other private sector players who are trying to outperform each other through product development strategies, expansion of distribution networks, and digital transformation strategies. The competition is mainly driven through bancassurance partnerships, distribution networks, and online sales strategies that help achieve operational efficiency. There is a focus on product development strategies such as protection-based, savings-based, and retirement-based insurance policies to cater to changing financial planning needs. On the other hand, the regulatory environment is well managed by the Insurance Regulatory Development Authority of India to ensure high standards of compliance while encouraging product development strategies to promote transparency and participation in the industry.

| Company | Leading Brands/Products | Highlights |

|---|---|---|

|

Life Insurance Corporation of India |

Jeevan Umang, New Endowment Plan, Tech Term | Market leader with the largest policyholder base and extensive nationwide agency network; strong presence in traditional savings-linked life insurance products and deep penetration across rural and semi-urban markets |

|

HDFC Life Insurance |

Click 2 Protect Life, Sanchay Plus, HDFC Life Pension Plans |

Leading private life insurer with strong digital distribution capabilities and diversified portfolio across protection, savings, and retirement solutions supported by bancassurance partnerships |

|

SBI Life Insurance |

Smart Bachat, eShield Next, Saral Pension | Strong growth driven by bancassurance distribution through a large public sector banking network and expanding customer base across urban and semi-urban markets |

Some other major key players in the India Life Insurance market are ICICI Prudential Life Insurance Co. Ltd., Bajaj Allianz Life Insurance Co. Ltd., Reliance Nippon Life Insurance Company Limited, Aditya Birla Sun Life Insurance Company Limited, Max Life Insurance Company Limited, Kotak Mahindra Life Insurance Company Limited, and Aviva Life Insurance Company India Ltd.

Latest Development & News:

- In December 2025, Life Insurance Corporation of India (LIC) launched two new products: 'Protection Plus,' also known as 'Plan 886,' and 'Bima Kavach,' which is 'Plan 887.' These products are intended to deliver flexible life insurance solutions with long-term financial security. The products were announced by the Managing Director and CEO of LIC, R Doraiswamy.

- In November 2025, Manulife Financial Corporation and Mahindra & Mahindra Ltd. (M&M) have announced a new 50/50 joint venture in the life insurance segment. This is dependent on the approval from the relevant authorities. This partnership will help the companies enhance their presence in the Indian market and further solidify their commitment to helping customers improve their financial well-being in one of the fastest-growing economies in the world.

- In July 2025, the Axis Max Life Insurance Limited, formerly Max Life Insurance Company Limited, has launched the Axis Max Life app. The app is designed to simplify the process of managing life insurance and enhance the customer experience. It now includes a wellness benefit for a healthy lifestyle. It is available on both Android and iOS.

India Life Insurance Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Term Life Insurance, Unit-Linked Insurance Plans (ULIP), Endowment Insurance Plans, Retirement/Pension Plans, Others |

| Premium Types Covered | Regular, Single |

| Premium Ranges Covered | Low, Medium, High |

| Providers Covered | Insurance Companies, Insurance Agents/Brokers, Others |

| Mode of Purchase Covered | Online, Offline |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India life insurance market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India life insurance market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India life insurance industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Life Insurance Market Report

The India life insurance market was valued at USD 120.2 Billion in 2025.

The India life insurance market is anticipated to reach a value of USD 269.1 Billion by 2034.

Endowment insurance plans dominate the India life insurance market with a share of 36.7% in 2025, as these products combine life protection with guaranteed savings benefits. Their popularity is driven by the preference of Indian households for low-risk financial instruments that support long-term goals such as children’s education, marriage planning, and retirement savings while also offering life coverage.

Regular policies dominate the market with a share of 68.4% in 2025, primarily because they allow policyholders to spread premium payments over long durations. This structure aligns with monthly income patterns of salaried individuals and helps improve policy affordability while encouraging long-term savings discipline.

The medium premium range dominates the market with a share of 44.2% in 2025, as it offers a balance between affordability and meaningful coverage. These policies are widely preferred by middle-income households seeking moderate protection and savings benefits without committing to high premium payments.

Insurance companies dominate the market with a share of 62.5% in 2025, supported by their established distribution networks, regulatory compliance frameworks, and strong brand credibility. Their extensive agency forces and bancassurance partnerships enable wide coverage across urban as well as semi-urban markets.

Offline purchase channels dominate the market with a share of 71.3% in 2025, as most policyholders prefer guidance from agents or financial advisors before committing to long-term insurance products. Personal interaction helps customers understand policy benefits, tax advantages, and long-term financial implications.

South India dominates the market with a share of 33.8% in 2025, supported by higher financial literacy levels, stronger insurance awareness, and a well-developed banking and financial services ecosystem across states such as Tamil Nadu, Karnataka, and Kerala.

Market growth is supported by rising financial awareness, expanding middle-class income levels, and increasing demand for long-term protection and retirement solutions. Government initiatives promoting insurance coverage, digital distribution platforms, and tax incentives on insurance premiums are also encouraging policy adoption across urban and semi-urban populations.

Some of the major participants in the India life insurance market include Life Insurance Corporation of India, HDFC Life Insurance, SBI Life Insurance, ICICI Prudential Life Insurance, Max Life Insurance, Kotak Mahindra Life Insurance, Bajaj Allianz Life Insurance, Tata AIA Life Insurance, Aditya Birla Sun Life Insurance, and PNB MetLife India Insurance.

The market faces several challenges, including relatively low insurance penetration in rural and informal employment segments. Limited financial literacy, complex product structures, and policy lapse issues also affect adoption levels. In addition, maintaining customer trust and improving long-term policy persistency remain important concerns for insurers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)