India Lighting Market Size, Share, Trends and Forecast by Type, Application, End User, and Region, 2026-2034

India Lighting Market Size, Share, Trends & Forecast (2026-2034)

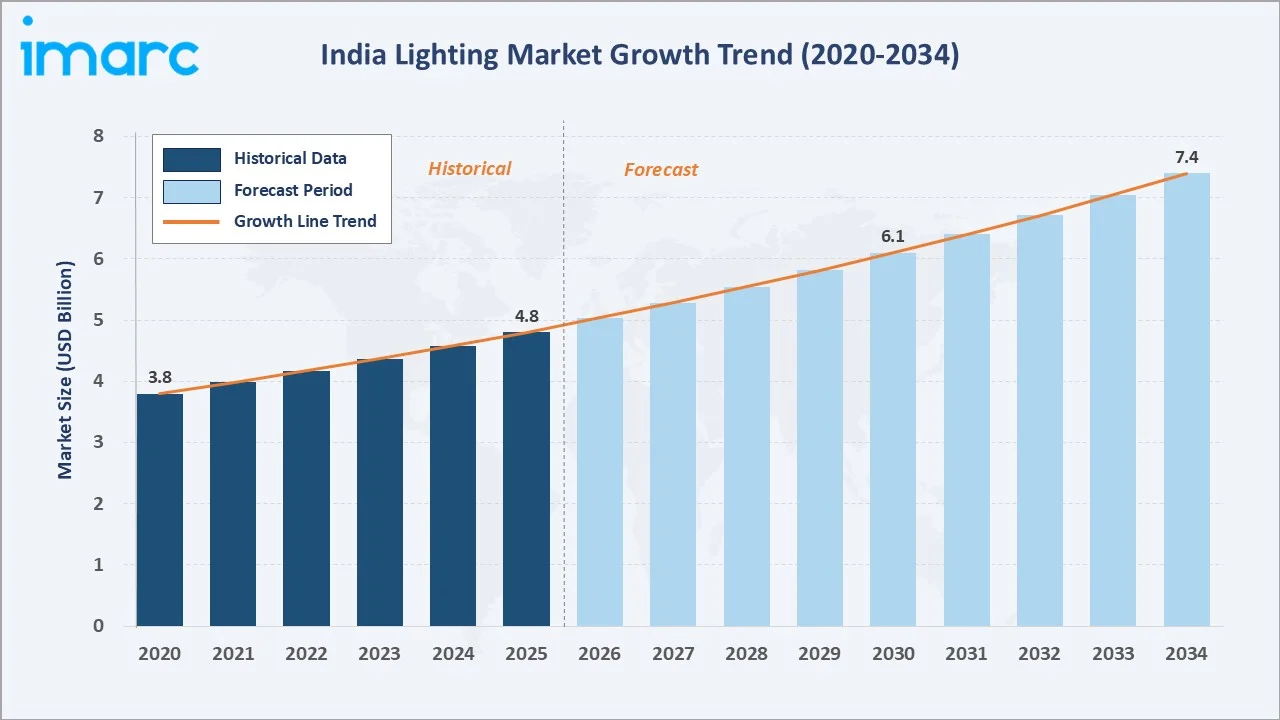

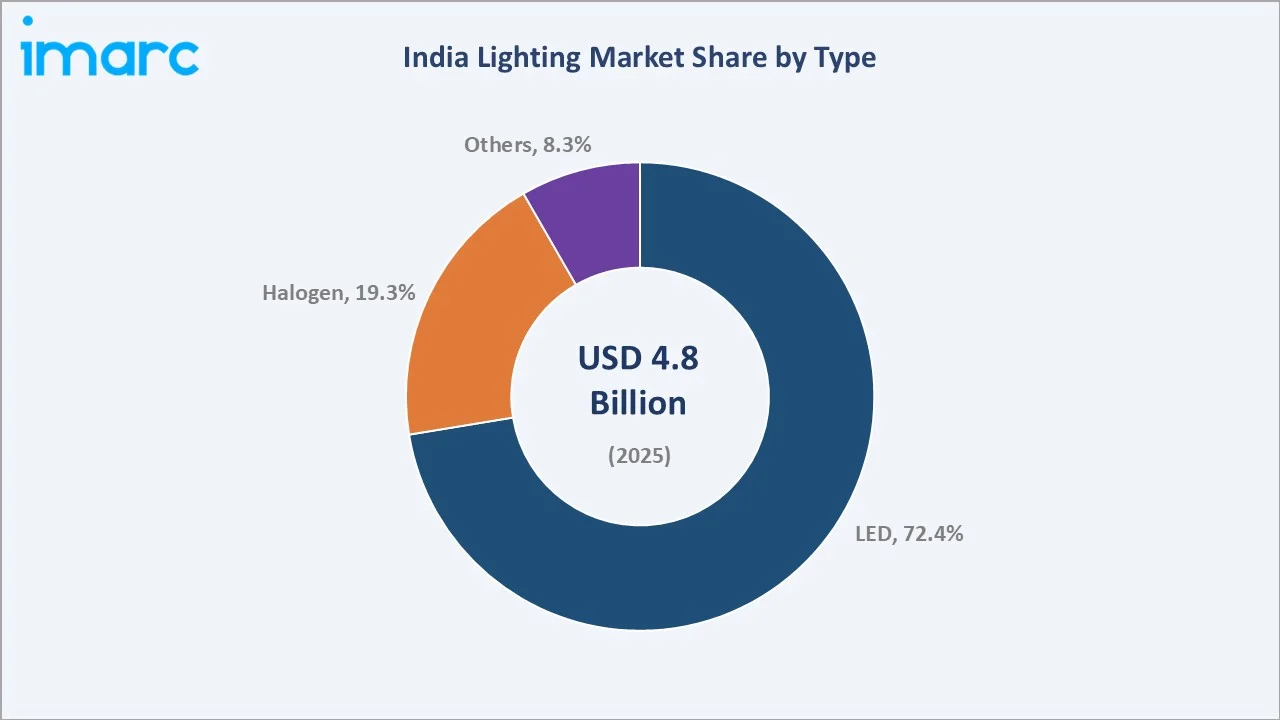

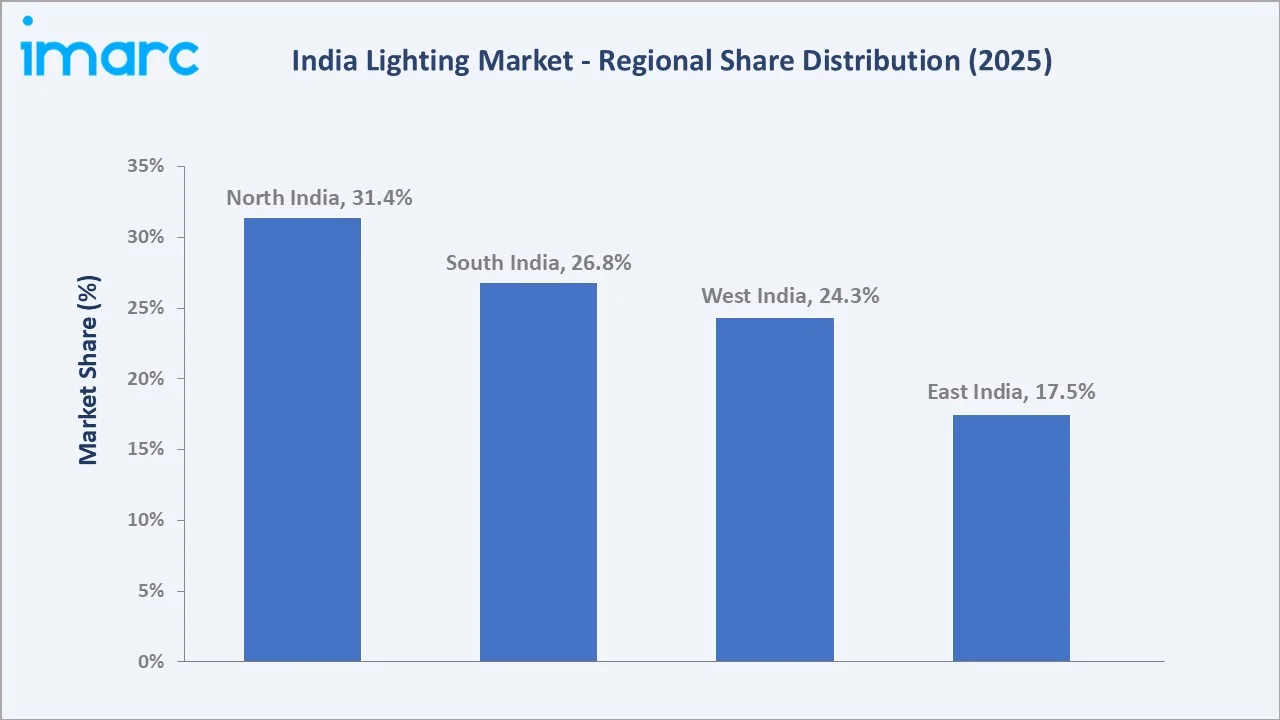

The India lighting market size was valued at USD 4.8 Billion in 2025 and is projected to reach USD 7.4 Billion by 2034, exhibiting a CAGR of 4.70% during the forecast period 2026-2034. Government-led energy-efficiency mandates, rapid urbanisation, and the nationwide success of the UJALA LED scheme are the primary forces driving India lighting market growth. LED lighting dominates with a commanding 72.4% share in 2025, while indoor applications account for 61.7% of demand. North India leads regionally at 31.4%, anchored by high construction activity and government infrastructure spending in Delhi NCR and Uttar Pradesh.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.8 Billion |

|

Forecast Market Size (2034) |

USD 7.4 Billion |

|

CAGR (2026-2034) |

4.70% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (31.4% share, 2025) |

|

Fastest Growing Region |

South India (Rapid urbanisation & smart city projects) |

|

Leading Segment (by Type) |

LED (72.4%, 2025) |

|

Leading Segment (by Application) |

Indoor (61.7%, 2025) |

To get more information on this market, Request Sample

The India lighting market growth trajectory from 2020 through 2034 reflects a sustained expansion curve powered by LED adoption, BEE energy-star mandates, smart-city deployments, and rising residential and commercial construction activity across all four regions.

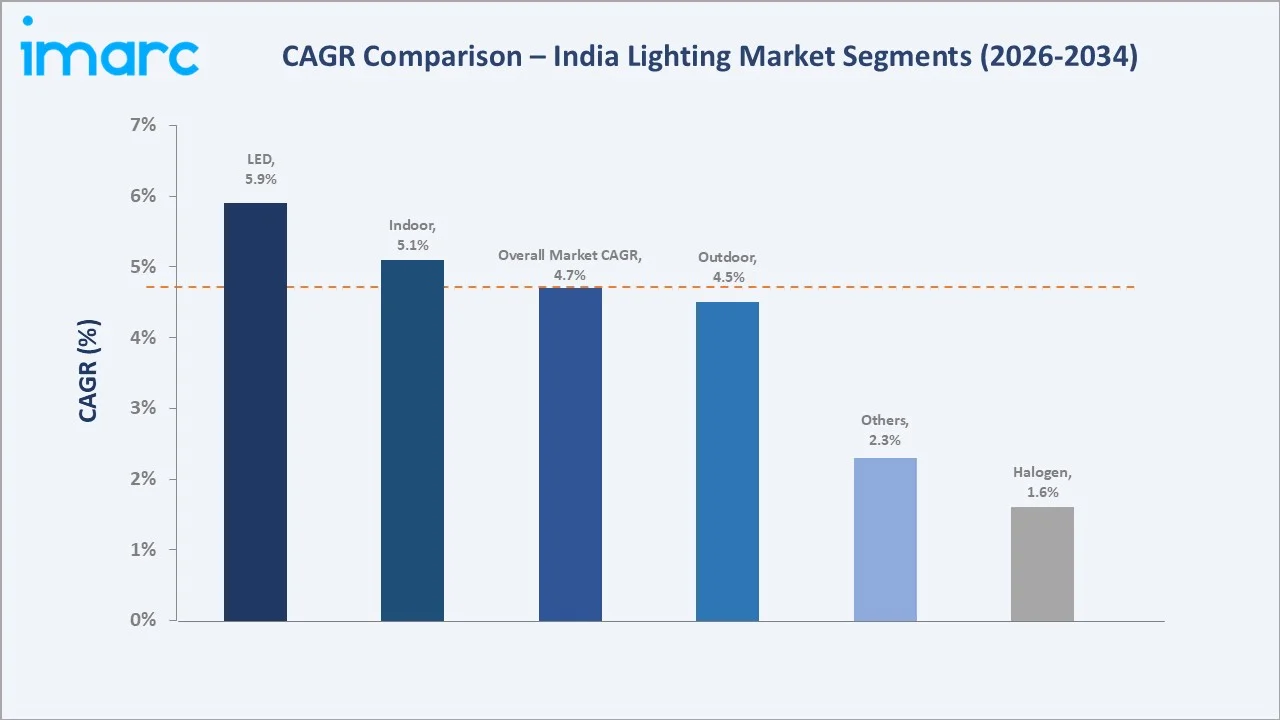

Segment-level CAGR comparisons highlight LED and indoor application categories as the fastest-growing sub-segments within the India lighting market forecast through 2034, driven by declining LED fixture costs and rising smart building adoption.

Executive Summary

The India lighting market is undergoing a structural, technology-driven transformation. Valued at USD 4.8 Billion in 2025, it is forecast to reach USD 7.4 Billion by 2034 at a CAGR of 4.70%. The UJALA scheme, the world's largest domestic LED replacement programme, distributed over 36.8 Crore LED bulbs by 2024, achieving annual energy savings and reducing household electricity costs by approximately INR 19,153 Crore annually, fundamentally restructuring the market toward LED-centric demand.

LED lighting holds a dominant 72.4% market share in 2025, reflecting rapid mass-market penetration across residential, commercial, and government segments. Halogen lighting retains a 19.3% share in 2025, primarily in decorative, automotive, and industrial niche applications where LED replacements are technically constrained. Indoor applications represent 61.7% of the market, driven by residential renovation activity and India's commercial real estate expansion, with 97.4 million sq. ft. of commercial space delivered in 2024.

North India commands 31.4% of the market, underpinned by dense residential construction and government institutional procurement. South India, with 26.8%, is the fastest-growing region, driven by technology-sector commercial buildouts in Bangalore, Hyderabad, and Chennai. The India lighting market outlook remains positive as smart lighting, human-centric lighting, and Li-Fi-enabled infrastructure investments converge through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

LED – 72.4% share (2025) |

|

Second Segment (Type) |

Halogen – 19.3% share (2025) |

|

Largest Application |

Indoor – 61.7% share (2025) |

|

Fastest Growing Application |

Outdoor – Expanding at ~4.5% CAGR (2026-2034) |

|

Leading Region |

North India – 31.4% revenue share (2025) |

|

Fastest Growing Region |

South India – ~5.5% CAGR driven by IT/commercial boom |

|

Top Companies |

Havells India, Signify India (Philips), Crompton Greaves Consumer Electricals, Bajaj Electricals, Syska LED Lights, Wipro Lighting, Surya Roshni, Orient Electric, Panasonic India, and Osram India |

|

Market Opportunity |

Smart LED & IoT lighting convergence through Smart Cities Mission |

Key Analytical Observations:

- LED's 72.4% dominance in 2025 reflects a price decline of over 85% in LED fixture costs since 2014, with a standard 9W LED bulb retailing at INR 70-90 in 2025 versus INR 600+ in 2013, making LED the default replacement across all income segments.

- Halogen's 19.3% residual share is sustained by decorative and specialty lighting applications in hospitality, automotive showrooms, and industrial facilities, where spectral quality requirements and retrofit costs still favour halogen technology.

- Indoor application's 61.7% lead is driven by India's residential housing boom, with 8.5 lakh housing units under the PMAY Urban scheme completed in FY 2024-25, each unit consuming an average of 14 LED fixtures across living, kitchen, and utility spaces.

- Outdoor lighting at 38.3% is expanding rapidly, powered by Smart Cities Mission streetlight replacement projects covering 100 cities, and the National Highways Authority's LED highway lighting upgradation programme.

- North India's 31.4% regional leadership is anchored by Delhi NCR's commercial construction boom and Uttar Pradesh's government-led infrastructure spending, which allocated INR 22,000 Crore to power and infrastructure projects in FY 2024-25.

- South India is the fastest-growing region, driven by 18+ million sq. ft. of Grade-A commercial office space under construction in Bangalore and Hyderabad in 2025, all specifying LED and smart lighting as standard.

India Lighting Market Overview

The India lighting market encompasses the design, manufacture, and distribution of light-emitting products across LED, halogen, fluorescent, incandescent, and emerging smart-lighting technologies. Applications span residential, commercial, industrial, institutional, and infrastructure segments, addressing both indoor and outdoor illumination requirements. The India lighting industry operates at the intersection of energy policy, real estate development, smart-city infrastructure, and consumer electronics trends.

Macro-economic drivers underpinning the market include India's accelerating urbanisation rate in 2025, sustained GDP growth of 6.5-7.0%, and government fiscal commitments to energy efficiency under the Bureau of Energy Efficiency's (BEE) Standards & Labelling programme. The BEE's mandatory star-rating requirement for LED luminaires, effective 2024, and MoHUA's Smart Cities Mission with INR 48,000 Crore in committed spending collectively shape the India lighting market trends and demand architecture.

Market Dynamics

To evaluate market opportunities, Request Sample

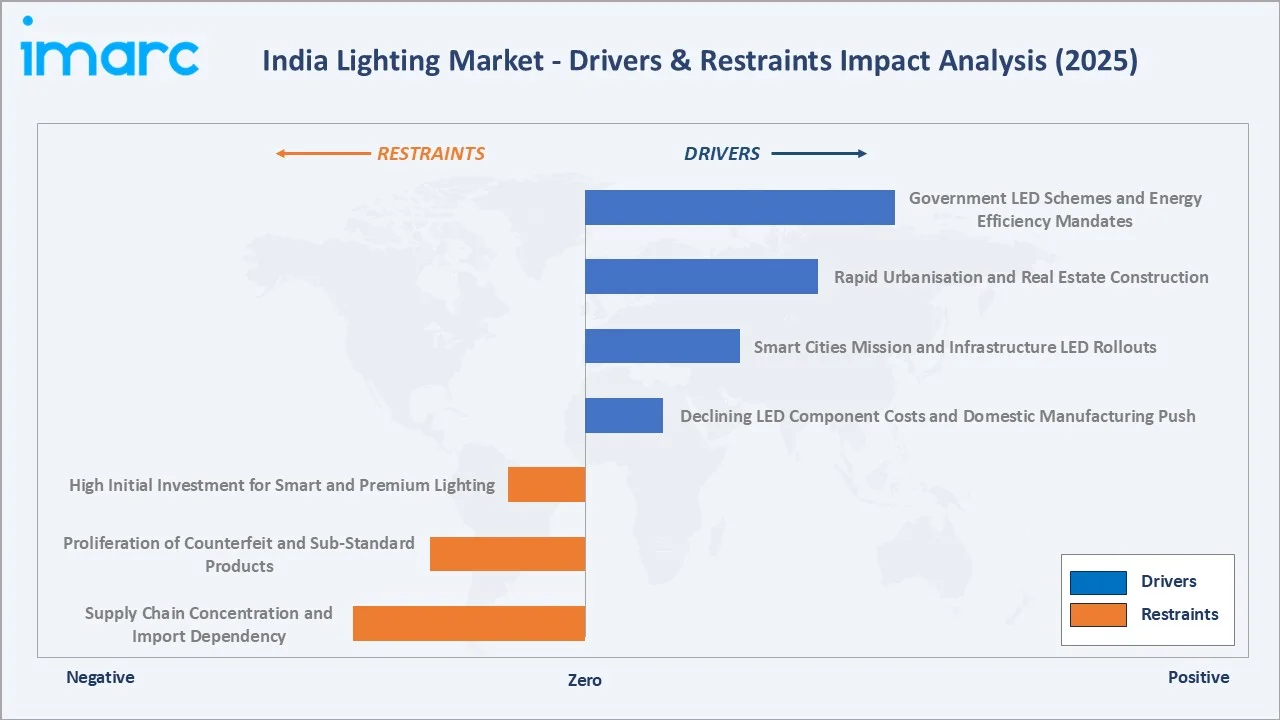

Market Drivers

- Government LED Schemes and Energy Efficiency Mandates: The UJALA scheme distributed 36.8 Crore LED bulbs through 2025, generating 47 billion kWh of annual energy savings and reducing CO2 emissions by 38.5 million tonnes annually. The BEE's expanded ECBC (Energy Conservation Building Code) 2024 mandates LED-only installations in all new commercial buildings exceeding 500 sq. m., directly encoding LED procurement into India's construction supply chain.

- Rapid Urbanisation and Real Estate Construction: India's residential real estate market delivered 4.35 lakh housing units across top-7 cities in 2024, a 21% year-on-year increase per Anarock data. The commercial sector delivered 97.4 million sq. ft. of Grade-A office space. Each new residential or commercial unit represents a structured demand point for LED fixtures, smart controls, and emergency lighting systems.

- Smart Cities Mission and Infrastructure LED Rollouts: MoHUA's Smart Cities Mission, covering 100 cities with INR 48,000 Crore in committed project spending, has initiated LED streetlight replacement projects in 85+ cities as of 2025. The NITI Aayog estimates that nationwide LED streetlight adoption could save INR 5,500 Crore annually in municipal electricity expenditure, creating a recurring procurement pipeline for LED outdoor luminaires and smart control systems.

- Declining LED Component Costs and Domestic Manufacturing Push: The PLI scheme for White Goods (including LED components), with a government incentive outlay of INR 6,238 Crore, is incentivising domestic LED chip, driver, and phosphor manufacturing. The LED Chip manufacturing PLI linked to ESDM has catalysed INR 8,337 Crore in committed capital investments through 2026, progressively reducing India's import dependence on Chinese LED components.

Market Restraints

- High Initial Investment for Smart and Premium Lighting: While basic LED retrofit costs have fallen sharply, premium smart lighting systems with IoT controls, occupancy sensors, and DALI interfaces cost 4-6x more than standard LED alternatives. This price premium significantly constrains adoption in the residential mass market and small commercial segments operating on tight fit-out budgets.

- Proliferation of Counterfeit and Sub-Standard Products: Counterfeit and sub-standard LED products, often sourced through informal import channels, suppress average selling prices, erode consumer confidence, and create unfair competition for compliant domestic manufacturers.

- Supply Chain Concentration and Import Dependency: India imports 65-70% of LED chips and approximately 80% of phosphor materials from China as of 2025. Geopolitical tensions, logistics disruptions, and currency fluctuations create supply chain vulnerability for Indian luminaire manufacturers, potentially constraining production capacity and inflating input costs.

Market Opportunities

- Smart Lighting and IoT Integration: India's smart lighting market is projected to grow exponentially through 2030, driven by Smart Cities Mission deployments, smart home adoption, and commercial building automation. Networked LED streetlight systems with remote monitoring, dimming, and fault-detection capabilities are being deployed in 50+ cities, representing a multi-year procurement opportunity through 2030.

- Human-Centric Lighting (HCL) for Commercial and Healthcare: The growing awareness of lighting's impact on circadian rhythms, productivity, and wellbeing is driving HCL adoption in premium offices, hospitals, schools, and senior living facilities. India’s healthcare infrastructure expansion represents a significant high-value HCL procurement pipeline.

- Li-Fi Technology and Lighting-as-a-Service (LaaS): Li-Fi, which uses light waves for wireless data transmission, is gaining pilot deployments in Indian tech parks and hospitals. LaaS subscription models are gaining traction among commercial real estate operators seeking zero-capital, managed lighting solutions, creating recurring revenue streams for lighting manufacturers and service providers.

Market Challenges

- Intensifying Competition from Low-Cost Chinese Imports: Despite BIS mandatory certification requirements for LED products, low-cost Chinese imports continue to exert significant pricing pressure. India's LED luminaire import value from China reached USD 123.67 million in FY 2025, challenging domestic manufacturers' margins and market share, particularly in the mass-residential and price-sensitive commercial segments.

- Technology Obsolescence and Product Lifecycle Compression: The rapid pace of LED technology evolution, with lumen-per-watt efficiency doubling approximately every 3-4 years, creates significant inventory risk for distributors and compresses product lifecycle economics for manufacturers, requiring continuous R&D investment to maintain product competitiveness.

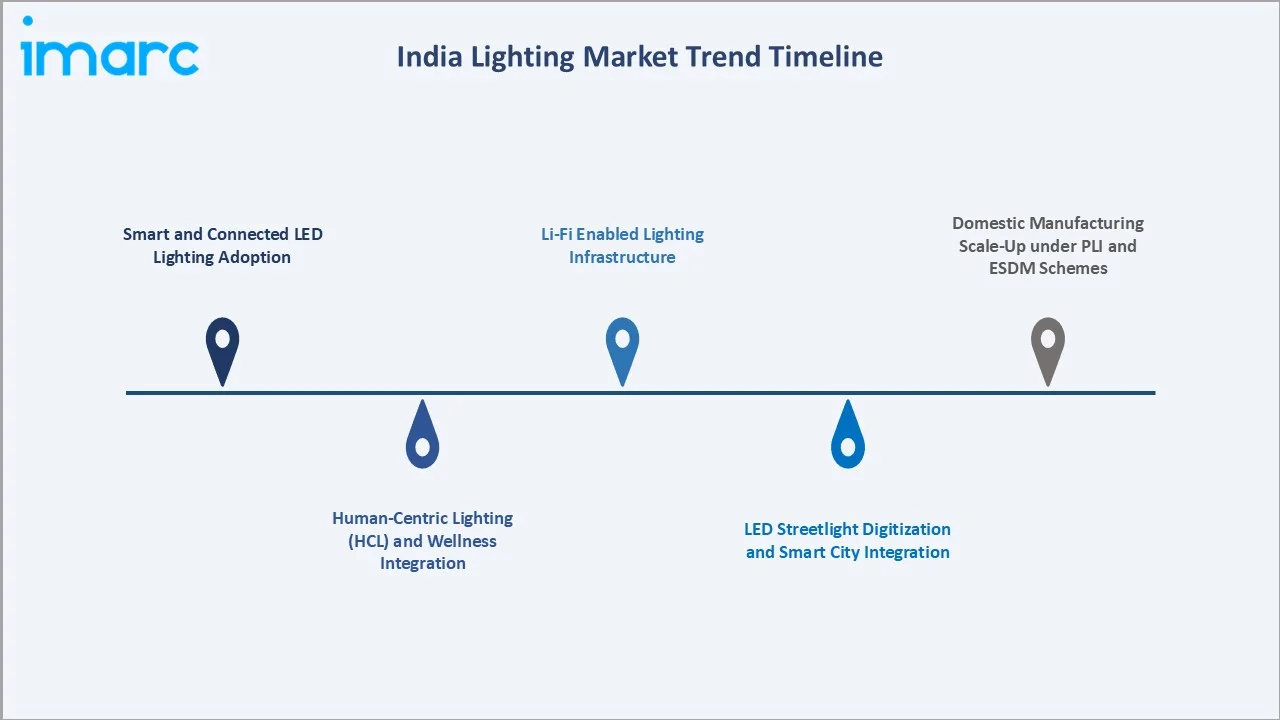

Emerging Market Trends

1. Smart and Connected LED Lighting Adoption

IoT-enabled LED lighting systems, integrating wireless protocols such as Zigbee, Z-Wave, and Bluetooth Mesh, are transitioning from premium niche to mainstream commercial adoption in India. This trend is being institutionalized through BEE's ECBC 2024 mandate for automated lighting controls in large commercial buildings, creating a structural demand inflection point.

2. Human-Centric Lighting (HCL) and Wellness Integration

India's premium office and healthcare sectors are increasingly specifying tunable-white LED systems that dynamically adjust color temperature and intensity to support circadian health. India's Grade-A office market, spanning 780 million sq. ft. in 2025, represents the largest near-term HCL adoption pipeline, with an estimated 15% of new premium office fit-outs specifying HCL-capable systems in 2025.

3. LED Streetlight Digitization and Smart City Integration

India's Smart Cities Mission has funded LED streetlight replacements across 85+ cities, with advanced smart-pole deployments including embedded CCTV, Wi-Fi hotspots, and environmental sensors. The National Street Lighting Programme (SLNP) managed by EESL has installed 29.47 Lakh streetlights with LED systems, with the next phase targeting 5G-integrated smart poles across 500+ cities through 2030.

4. Li-Fi Enabled Lighting Infrastructure

Li-Fi technology, which transmits data through LED light modulation at speeds up to 224 Gbps, is gaining pilot deployments in Indian IT campuses and healthcare facilities. Companies including signify India and startups such as NavInfo are conducting commercial Li-Fi trials in Bangalore and Hyderabad tech parks. Government interest in Li-Fi as a secure, interference-free connectivity solution for defence, hospitals, and sensitive infrastructure is creating early-stage institutional procurement demand.

5. Domestic Manufacturing Scale-Up under PLI and ESDM Schemes

India's Production Linked Incentive (PLI) scheme for White Goods and the ESDM programme are catalysing large-scale domestic LED component manufacturing. Havells, Syska, and Wipro Lighting are expanding Indian manufacturing footprints, targeting reduction of LED chip import dependency by 2030. This domestic supply chain deepening will structurally improve cost competitiveness for Indian manufacturers while reducing currency and logistics risk.

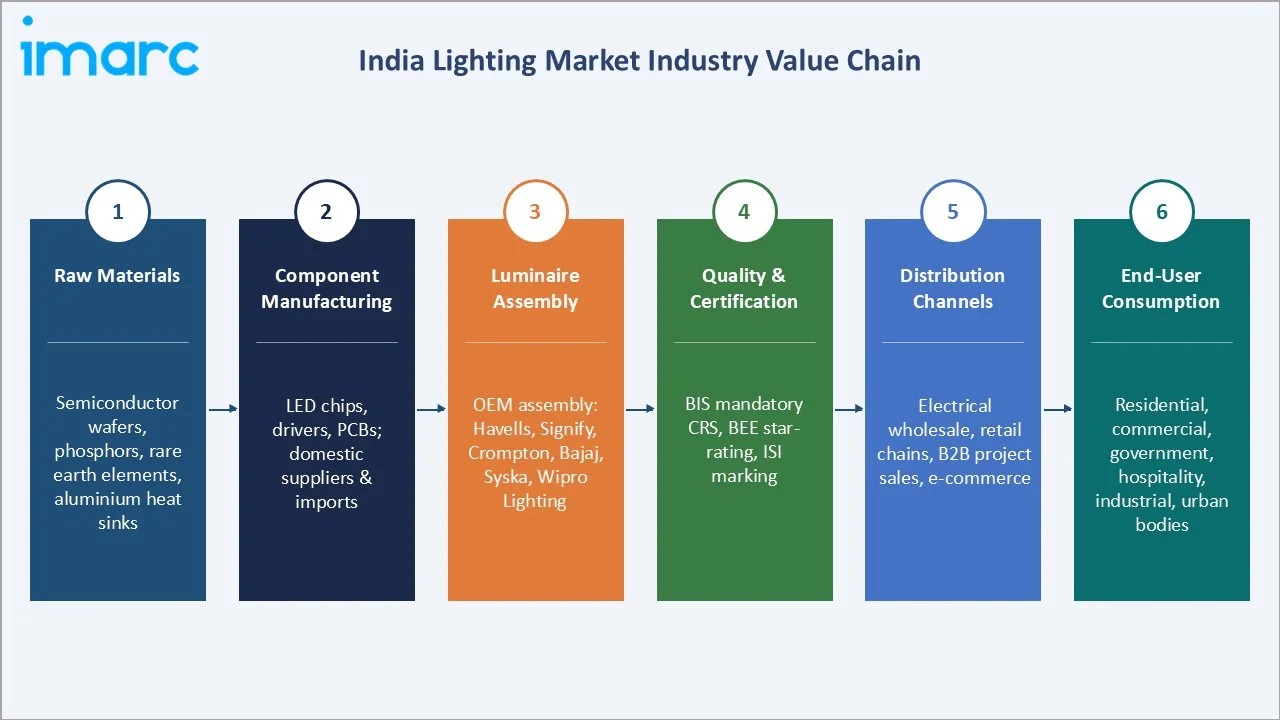

Industry Value Chain Analysis

The India lighting industry value chain spans six integrated stages from raw material sourcing through end-consumer installation. Each stage presents distinct competitive dynamics, margin profiles, and policy intervention points relevant to the overall India lighting market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Semiconductor wafers, phosphors, rare earth elements, aluminium heat sinks, polycarbonate lenses, glass envelopes – predominantly imported from China, Japan, and Taiwan |

|

Component Manufacturing |

LED chips (CSP, COB, SMD), LED drivers (SMPS), PCBs, heat sinks – domestic suppliers; imports from Osram, Nichia |

|

Luminaire Assembly |

OEM assembly by Havells, Signify India, Crompton, Bajaj Electricals, Syska, Wipro Lighting – full product assembly, thermal management, optical design, BIS/BEE certification |

|

Quality & Certification |

BIS mandatory CRS certification, BEE star-rating, ISI marking, third-party testing by NABL-accredited labs |

|

Distribution Channels |

Electrical wholesale distributors (Havells Galaxy), retail chains (D-Mart, Reliance Digital), B2B project sales, e-commerce (Amazon, Flipkart) |

|

End-User Consumption |

Residential homeowners, commercial real estate operators, government institutions, hospitality, healthcare, industrial facilities, and urban local bodies (ULBs) for streetlighting |

OEM manufacturers hold the highest strategic value by integrating component supply, thermal engineering, optical design, and BEE-certified performance into certified luminaire products. The e-commerce channel's growing share in LED retail is reshaping distribution dynamics, enabling manufacturers to bypass traditional electrical wholesale networks and command higher direct-to-consumer margins.

Technology Landscape in the India Lighting Industry

LED Technology Evolution and Efficacy Advances

Modern LED luminaires in India achieve efficacy levels of 140-180 lumens per watt (lm/W) in 2025, up from 80-100 lm/W in 2018, driven by chip-scale package (CSP) and chip-on-board (COB) technology advances. Domestic manufacturers including Havells and Syska are deploying 3rd-generation mid-power LED arrays with colour rendering index (CRI) values exceeding 90, enabling premium decorative and retail lighting applications previously dominated by halogen technology.

Smart Controls and IoT Integration

DALI-2 (Digital Addressable Lighting Interface), BACnet, and wireless Bluetooth Mesh protocols are becoming standard in commercial LED lighting deployments. Smart lighting control systems enabling occupancy-based dimming, daylight harvesting, and remote energy monitoring are achieving additional energy savings beyond basic LED replacement.

Human-Centric Lighting Technology

Tunable-white LED systems using dual-channel CCT (correlated color temperature) control enabling dynamic lighting environments that shift from cool white (6500K) for productive daytime work to warm white (2700K) for evening relaxation. Spectrally optimized LED systems for horticulture, healthcare, and education are emerging as high-value technology sub-segments, with wavelength-specific red/blue LED arrays for indoor agriculture gaining rapid adoption across India's controlled-environment agriculture sector.

Thermal Management and Driver Technology

Advanced thermal interface materials (TIMs), copper-core aluminum PCBs, and vapor-chamber heat spreaders are enabling higher power density LED arrays without compromising lumen maintenance (L70 lifespan). Intelligent LED driver technologies with adaptive current control, power factor correction exceeding 0.9, and THD below 10% are becoming standard in BEE 5-star rated luminaires, meeting increasingly stringent power quality requirements from industrial and commercial grid operators.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the India lighting market, along with forecasts from 2026 to 2034. The market has been analyzed based on Type and Application.

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

LED |

72.4% |

2025 |

|

Application |

Indoor |

61.7% |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

North India |

31.4% |

2025 |

By Type

To access detailed market analysis, Request Sample

LED lighting dominates the India lighting market with a 72.4% share in 2025, up from approximately 41% in 2019. This structural shift has been driven by the UJALA scheme's 36.8 Crore LED bulb distribution, mandatory BEE star-rating enforcement, and a cumulative price decline of 85%+ since 2014. LED's lumen maintenance advantage (L70 lifespan of 25,000-50,000 hours versus 2,000-3,000 hours for halogen) and lower total cost of ownership are permanently displacing incumbent technologies.

Halogen lighting holds 19.3% market share in 2025, primarily concentrated in decorative accent lighting, automotive showroom spotlights, and industrial heat lamps where halogen's spectral characteristics, instant-on capability, and focusable beam remain advantageous. However, BEE's phase-out roadmap for halogen lamps exceeding 25W, aligned with EU regulations, will progressively erode this segment.

Others segment at 8.3% comprises fluorescent (T5/T8 tubes), metal halide, high-pressure sodium, and emerging OLED panels. Industrial and sports stadium applications continue to consume high-pressure sodium and metal halide for high-mast illumination. OLED lighting panels are gaining traction in premium hospitality and architectural applications, though high price points constrain mass adoption.

By Application

Indoor applications lead with 61.7% market share in 2025. Residential indoor lighting represents the largest sub-segment, propelled by India's residential construction completing 4.35 lakh units in 2024 across top-7 cities. The average new residential unit in India deploys 14 LED fixtures, creating 6.1 million fixture demand units from new construction alone in FY 2024-25.

Outdoor lighting accounts for 38.3% of the India lighting market in 2025. The Smart Cities Mission's LED streetlight replacement programme across 100 cities, NHAI's national highway LED upgrade, and the growing deployment of smart stadium floodlighting for IPL venues and state sports infrastructure collectively drive this segment. Industrial outdoor lighting for logistics parks, SEZs, and manufacturing campuses is the fastest-growing outdoor sub-segment as India's goods and services exports scale.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

31.4% |

Delhi NCR commercial construction, UP infrastructure spending, government institutional lighting procurement, EESL project rollouts in Rajasthan and Haryana |

|

South India |

26.8% |

Bangalore IT corridor Grade-A office buildout, Hyderabad pharma and tech campus expansion, Chennai industrial zone lighting, smart city LED deployments in 15+ southern cities |

|

West India |

24.3% |

Mumbai commercial real estate, Pune IT and auto industry campuses, Gujarat industrial and port lighting, Maharashtra Smart Cities Mission LED rollouts across Nagpur and Pune |

|

East India |

17.5% |

Kolkata residential construction, Odisha industrial corridor lighting, government PMAY housing projects in West Bengal, EESL LED streetlight deployments in smaller eastern cities |

North India commands 31.4% of the India lighting market in 2025. Delhi NCR's combined residential and commercial construction pipeline development under various stages in 2025, creates a sustained demand base for LED fixtures. The Government of India's institutional procurement through EESL and CPWD, headquartered in New Delhi, concentrates significant LED procurement spend in the region. Uttar Pradesh's infrastructure budget of INR 25,308 Crore in FY 2024-25 and Rajasthan's 50-city smart LED streetlight programme further reinforce North India's regional dominance.

South India holds 26.8% and is the fastest-growing region, powered by Bangalore's 50+ million sq. ft. of Grade-A office space under construction, Hyderabad's 14 million sq. ft. of new commercial additions in 2024, and a dense concentration of technology multinationals and pharmaceutical giants specifying premium LED and smart lighting in their campuses.

West India represents 24.3%, with Mumbai's Bandra Kurla Complex and Lower Parel commercial zones driving premium commercial LED demand. Gujarat's GIFT City financial district and expanding industrial corridors along the Delhi-Mumbai Industrial Corridor (DMIC) are generating sustained institutional and industrial lighting demand. Maharashtra's Smart Cities Mission LED streetlight deployments in Nagpur, Pune, and Aurangabad supplement the commercial demand base.

East India accounts for 17.5%, the smallest regional share, but is gradually gaining momentum through government-led housing schemes. West Bengal progressed in allocation of PMAY Urban housing units in FY 2024-25, each incorporating basic LED lighting under BEE's affordable housing standards. Odisha's Paradip and Kalinganagar industrial corridor expansions and the North East Industrial Development Scheme (NEIDS) are slowly catalysing commercial and industrial LED demand in the eastern belt.

Competitive Landscape

|

Company Name |

Key Brand / Division |

Market Position |

Core Strength |

|

Havells India Ltd. |

Havells |

Leader |

Pan-India distribution, integrated manufacturing, smart lighting R&D |

|

Signify India Ltd. |

Philips, Interact |

Leader |

Global technology leadership, Interact IoT platform, premium segment dominance |

|

Crompton Greaves Consumer Electricals Limited |

Crompton |

Leader |

Mass-market LED penetration, cost leadership, wide retail network |

|

Bajaj Electricals Ltd. |

Bajaj |

Leader |

Strong B2B project business, government EESL partnerships, EPC capability |

|

Syska LED Lights Pvt. Ltd. |

Syska |

Leader |

Aggressive pricing, high consumer recall, e-commerce and modern retail focus |

|

Wipro Lighting |

Wipro Lighting |

Challenger |

Premium architectural lighting, B2B commercial focus, smart controls expertise |

|

Surya Roshni Ltd. |

Surya |

Challenger |

Domestic manufacturing scale, LED tubes leadership, rural distribution strength |

|

Orient Electric Ltd. |

Orient |

Challenger |

Smart LED fans and lights integration, B2C innovation, growing e-commerce share |

|

Panasonic India Pvt. Ltd. |

Panasonic |

Niche |

Japanese technology quality, industrial and commercial lighting focus |

|

Osram India Pvt. Ltd. |

Osram |

Niche |

Premium horticultural, automotive, and speciality lighting applications |

The India lighting market's competitive landscape is moderately concentrated at the premium tier but highly fragmented in the mass-market LED segment. The top five players – Havells, Signify, Crompton, Bajaj, and Syska. The remaining market share is distributed across 200+ domestic manufacturers, regional assemblers, and organised importers. Strategic priorities across leading players include PLI-aligned domestic manufacturing expansion, smart lighting platform development, and direct-to-consumer e-commerce channel investment.

Key Company Profiles

Havells India Ltd.

Havells India is the country's leading electrical equipment manufacturer, headquartered in Noida, Uttar Pradesh. Founded in 1958, Havells reported revenues of INR 21,745.81 Crore in FY 2024-25, with its lighting and luminaires division contributing approximately INR 1,653 Crore. The company operates 8 manufacturing plants across India and distributes through 110,000+ retail touchpoints.

- Product Portfolio: Havells offers a comprehensive LED portfolio spanning panel lights, downlights, strip lights, battens, streetlights, and smart home lighting under the Havells brand, alongside premium architectural lighting through its Havells Norisys range.

- Recent Developments: In March 2025, Havells commissioned a new LED luminaire manufacturing facility in Sri City, Andhra Pradesh, with an annual capacity of 15 million units, strengthening its South Indian supply chain. In FY 2024-25, Havells expanded its Havells Galaxy dealer network to 7500 direct dealers and 1 lakh retailers.

- Strategic Focus: Havells' strategy centres on PLI-driven component localisation, smart home lighting integration, and premium architectural segment expansion.

Signify India Ltd. (Philips Lighting)

Signify India, the Indian subsidiary of Signify NV (formerly Philips Lighting), is headquartered in Gurugram, Haryana. Signify India reported revenues of approximately INR 3143 Crore in FY 2024-25. It leads India's premium commercial and smart lighting segments through its Philips brand and Interact IoT platform.

- Product Portfolio: Signify India's portfolio includes Philips LED panels, troffers, highbays, streetlights, Interact City smart streetlight management systems, TrueForce industrial LED retrofits, and Hue smart home lighting.

- Recent Developments: In January 2025, Signify India expanded its Interact City smart streetlight platform to 12 additional Indian cities. In FY 2024-25, the Philips HUE ecosystem launched modern retail outlets, doubling smart home lighting retail presence.

- Strategic Focus: Signify India focuses on Interact IoT platform expansion, Li-Fi pilot deployments in Indian tech parks, and human-centric lighting adoption in premium healthcare and office segments.

Crompton Greaves Consumer Electricals Limited

Crompton Greaves Consumer Electricals, headquartered in Mumbai, is one of India's largest consumer electricals companies with revenues of INR 7,932 Crore in FY 2025. Its lighting division, contributing approximately INR 1,020 Crore, leads India's mass-market LED segment through aggressive pricing and wide retail penetration.

- Product Portfolio: Crompton's lighting portfolio spans LED bulbs, battens, panels, CFLs, and ceiling lights, available through retail touchpoints across India. Its Silver Shield anti-bacterial LED range targets post-pandemic hygiene-conscious residential buyers.

- Recent Developments: In 2025, Crompton launched its Aura+ smart ceiling light range, integrating BLE-based voice and app control at price points below competitive smart lighting alternatives, targeting aspirational tier-2 city consumers.

- Strategic Focus: Crompton's strategy centres on capturing the affordable smart lighting segment in tier-2 and tier-3 cities, deepening its e-commerce channel presence, and expanding its B2B project business through EPC partnerships.

Market Concentration Analysis

The India lighting market exhibits moderate concentration at the organized branded segment, with the top five players – Havells, Signify, Crompton, Bajaj, and Syska. The remaining market share is distributed across Wipro Lighting, Surya Roshni, Orient Electric, Panasonic, Osram India, and over 200 regional assemblers and importers.

The market is experiencing a bifurcated consolidation trend. At the premium and smart lighting tier, consolidation is occurring around IoT platform capabilities, BEE 5-star certification, and brand equity. Concurrently, in the mass-market LED commodity segment, persistent pricing pressure from unorganized domestic assemblers and low-cost import channels is fragmenting market share and compressing margins for branded players. PLI incentives are enabling domestic manufacturers to narrow the cost gap with imports, potentially triggering a consolidation wave among mid-tier regional brands through 2027-2030.

Strategic M&A activity is increasing: Havells' acquisition of Lloyd's consumer appliances division (including smart home ecosystem integration) and Bajaj Electricals' EPC business expansion represent the two dominant consolidation themes, with lighting positioned as the nexus of smart home and energy efficiency value chains.

Investment & Growth Opportunities

Fastest-Growing Segments

LED smart lighting is the highest-growth product sub-segment at approximately 12% CAGR through 2030. Outdoor LED streetlights with smart management capabilities are expanding, driven by Smart Cities Mission and NHAI highway LED programmes. Human-centric lighting for healthcare and premium commercial offices represents the highest revenue-per-unit growth opportunity, with average selling prices 8-12x standard LED alternatives.

Emerging Market Expansion

India's tier-2 and tier-3 city markets – covering 400+ cities with populations between 100,000 and 1 million – represent a significantly underpenetrated LED and smart lighting opportunity. Government PMAY housing construction in these cities, combined with rising consumer aspirations and BEE's energy labelling enforcement, is structurally expanding LED demand beyond the top-10 metropolitan areas. The Northeast India LED infrastructure opportunity, backed by the NEIDS scheme and Digital North East programme, is an emerging early-mover advantage zone.

Venture and Strategic Investment Trends

PLI scheme commitments in LED components exceeded INR 3,516 Crore through 2024. Venture and private equity investments in Indian smart lighting and Li-Fi technology with key deals including Signify's Trulifi commercial deployments and a series of seed and Series A rounds for Indian smart home lighting app developers. EESL's PPP model for SLNP Phase 2, covering additional LED streetlights.

Future Market Outlook (2026-2034)

The India lighting market forecast projects expansion from USD 4.8 Billion in 2025 to USD 7.4 Billion by 2034 at a CAGR of 4.70%, with an intermediate milestone of USD 6.1 Billion by 2030. LED technology will further consolidate its share toward 79-82% by 2034 as smart LEDs progressively replace the remaining halogen and fluorescent installed base. Outdoor lighting will gain share relative to indoor as Smart Cities Mission Phase 2 and NHAI LED highway programmes accelerate.

Technological disruptions shaping the market through 2034 include: Li-Fi commercialisation in enterprise and institutional settings, enabling LED infrastructure to double as high-speed data transmission networks; AI-driven adaptive lighting systems that autonomously optimise illumination for energy, circadian health, and security without manual programming; and solid-state lighting advances including OLED and micro-LED panel lighting achieving cost parity with premium LED luminaires by 2030.

India's Net Zero by 2070 commitment and the National Mission for Enhanced Energy Efficiency's (NMEEE) accelerated targets are structurally embedding energy-efficient LED and smart lighting into building codes, procurement standards, and financial incentive frameworks through 2034. This policy tailwind, combined with India's sustained 6%+ GDP growth trajectory and rapid urbanisation, supports a positive and structurally reinforced India lighting market outlook through the forecast period.

Research Methodology

Primary Research

Primary research involved structured interviews and expert consultations with LED luminaire product managers, procurement heads at major real estate developers, BEE energy auditors, government officials at EESL and MoHUA Smart Cities Mission, and distribution channel executives at leading electrical wholesalers. Primary inputs validated market sizing, segment growth trajectories, competitive positioning, and emerging trend prioritisation.

Secondary Research

Secondary research drew upon BEE Standards & Labelling annual reports, MoHUA Smart Cities Mission project data, EESL SLNP procurement statistics, Ministry of Commerce import/export trade data for LED products, Anarock and CBRE commercial real estate reports, NASSCOM IT campus construction data, industry associations including ELCOMA (Electric Lamp and Component Manufacturers Association), and company annual reports for all profiled competitors.

Forecasting Models

Market size forecasts were developed through bottom-up aggregation of segment-level revenues by type and application, cross-validated with top-down macro-economic indicators including India GDP growth, construction sector output, BEE certification issuance volume, and EESL procurement tender data. A base-case CAGR of 4.70% was derived through triangulation of multiple data inputs with scenario analysis across optimistic, base, and conservative growth paths through 2034.

India Lighting Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | LED, Halogen, Others |

| Applications Covered | Indoor, Outdoor |

| End Users Covered | Residential, Industrial, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Havells India Ltd., Signify India Ltd., Crompton Greaves Consumer Electricals Limited, Bajaj Electricals Ltd., Syska LED Lights Pvt. Ltd., Wipro Lighting, Surya Roshni Ltd., Orient Electric Ltd., Panasonic India Pvt. Ltd., Osram India Pvt. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India lighting market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India lighting market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India lighting industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Lighting Market Report

The India lighting market was valued at USD 4.8 Billion in 2025 and is projected to reach USD 7.4 Billion by 2034, growing at a CAGR of 4.70% during 2026-2034.

The market is projected to expand at a CAGR of 4.70% from 2026 to 2034, driven by LED technology dominance, BEE mandates, Smart Cities LED deployments, and rising residential and commercial construction activity.

LED lighting leads with a dominant 72.4% market share in 2025, up from ~41% in 2019, supported by UJALA scheme distribution of 368 million LED bulbs and BEE mandatory certification enforcement.

Indoor applications hold 61.7% market share in 2025, driven by residential housing construction completing 4.35 lakh units in 2024 and Grade-A commercial office space delivery of 97.4 million sq. ft.

North India leads with 31.4% market share in 2025, anchored by Delhi NCR's commercial construction pipeline, UP government infrastructure spending, and EESL institutional procurement headquartered in the region.

South India is the fastest-growing region at an estimated 5.5% CAGR, driven by Bangalore's 50+ million sq. ft. of office construction, Hyderabad's tech campus expansion, and dense smart lighting project activity.

Key drivers include the UJALA LED scheme, BEE energy-efficiency mandates, Smart Cities Mission LED streetlight rollouts, PLI-driven domestic LED manufacturing, rapid urbanisation, and rising residential and commercial construction.

Key players include Havells India, Signify India (Philips), Crompton Greaves Consumer Electricals, Bajaj Electricals, Syska LED Lights, Wipro Lighting, Surya Roshni, Orient Electric, Panasonic India, and Osram India.

The India lighting market is forecast to reach USD 6.1 Billion by 2030, supported by Smart Cities Mission Phase 2, NHAI highway LED programmes, and continued mass-market LED penetration in tier-2 and tier-3 cities.

The UJALA scheme distributed 368 million LED bulbs through 2024, saving 47 billion kWh annually and reducing CO2 emissions by 38.5 million tonnes, fundamentally restructuring the market to LED-centric demand.

BEE's mandatory star-rating programme for LED luminaires, ECBC 2024 LED-only mandate for commercial buildings, and energy performance standards are the primary regulatory frameworks driving LED adoption and quality standards.

Key opportunities include smart LED and IoT-integrated systems, human-centric lighting for healthcare and offices, Li-Fi-enabled LED infrastructure, horticultural LED for indoor farming, and Lighting-as-a-Service subscription models for commercial real estate.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)