India Masterbatch Market Size, Share, Trends and Forecast by Type, Polymer Type, Application, and Region, 2026-2034

India Masterbatch Market Summary:

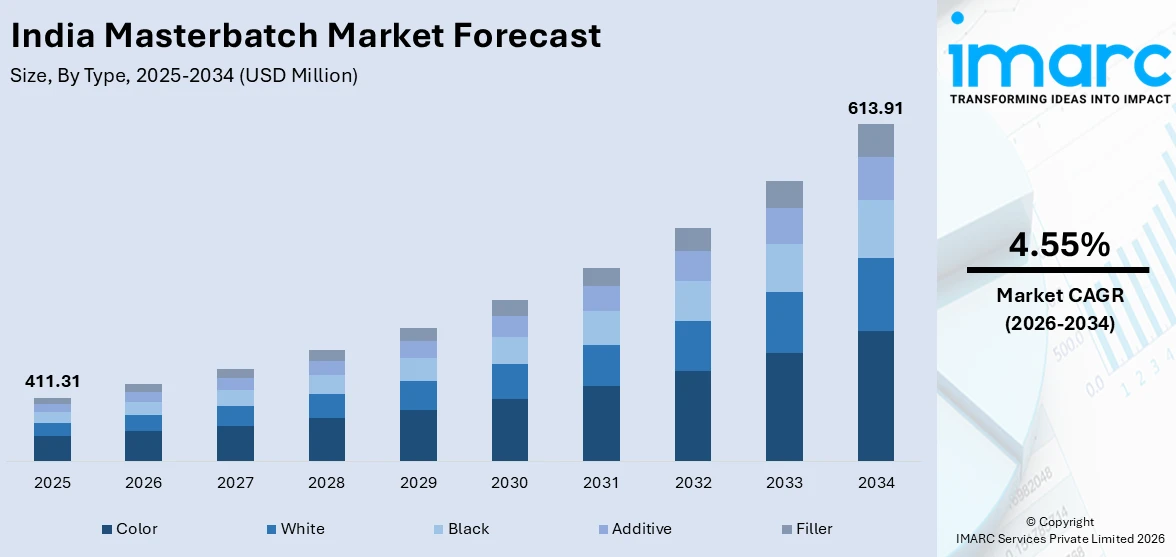

The India masterbatch market size was valued at USD 411.31 Million in 2025 and is projected to reach USD 613.91 Million by 2034, growing at a compound annual growth rate of 4.55% from 2026-2034.

The India masterbatch market is expanding steadily, driven by surging demand from the packaging, automotive, and construction sectors. Rapid urbanization, increasing consumption of processed and packaged goods, and the expansion of e-commerce logistics are intensifying the need for high-quality, aesthetically appealing plastic products. Advances in polymer processing technologies and growing adoption of additive and functional masterbatches are enabling manufacturers to meet diverse end-use requirements. Government-led infrastructure programs, favorable industrial policies, and rising investments in plastics processing capabilities are further strengthening the India masterbatch market share.

Key Takeaways and Insights:

- By Type: Color dominates the market with a share of 42% in 2025, driven by widespread demand for vibrant, consistent coloring across packaging, consumer goods, and automotive applications requiring brand differentiation.

- By Polymer Type: PP leads the market with a share of 30% in 2025, owing to its versatility, cost-effectiveness, and extensive usage in flexible packaging, woven sacks, and automotive components.

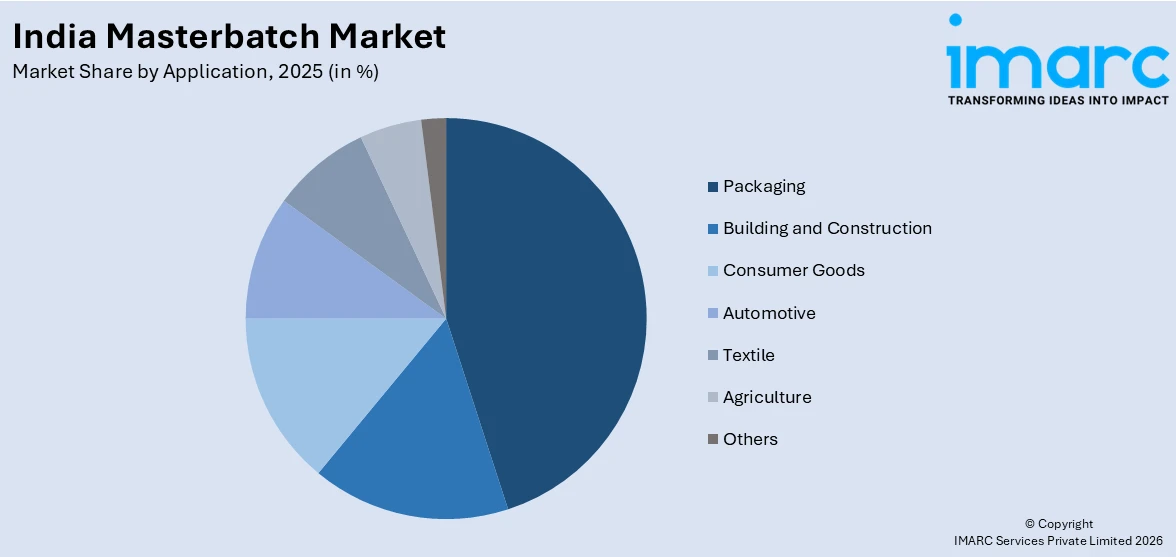

- By Application: Packaging represents the largest segment with a market share of 44% in 2025, supported by the rapid expansion of food processing, FMCG distribution, and e-commerce fulfillment requiring durable and attractive packaging solutions.

- Key Players: The India masterbatch market exhibits a moderately competitive landscape, with established domestic manufacturers and multinational companies investing in capacity expansion, product innovation, and sustainable formulations to strengthen their presence across diverse application segments.

To get more information on this market Request Sample

The India masterbatch market is undergoing a transformative phase, shaped by the convergence of industrial growth, regulatory developments, and technological innovation. The India plastic packaging market size reached USD 13.2 Billion in 2025. The market is expected to reach USD 17.3 Billion by 2034, growing at a CAGR of 3.10% from 2026-2034. The automotive industry is increasingly incorporating lightweight plastic components enhanced with color and additive masterbatches to improve durability, performance, and aesthetic quality. At the same time, manufacturers are placing greater emphasis on sustainable and circular material solutions to align with evolving environmental standards. Supportive industrial policies and ongoing infrastructure initiatives are further stimulating demand across construction, agriculture, and consumer goods segments, collectively reinforcing growth opportunities for masterbatch applications in diverse end-use industries.

India Masterbatch Market Trends:

Rising Adoption of Sustainable and Bio-Based Masterbatch Formulations

Environmental awareness and regulatory pressures are accelerating the shift toward sustainable masterbatch solutions in India. Manufacturers are increasingly developing bio-based and recyclable formulations to comply with stringent Plastic Waste Management Rules and Extended Producer Responsibility (EPR) guidelines that mandate recycled content in packaging. The government’s ban on single-use plastics is pushing processors toward biodegradable alternatives. In February 2025, Chief Minister Yogi Adityanath inaugurated India’s first biopolymer manufacturing unit in Lakhimpur, Uttar Pradesh, a project valued at INR 2,880 crore, signaling growing commitment to sustainable polymer production that strengthens demand for compatible eco-friendly masterbatches.

Growing Integration of Functional and Additive Masterbatches

The demand for performance-enhancing additive masterbatches is rising rapidly as industries seek advanced functional properties in plastic products. UV stabilizers, flame retardants, antimicrobial agents, and antistatic additives are gaining traction across healthcare, agriculture, and electronics applications. This trend supports the India masterbatch market growth as manufacturers invest in specialized formulations. In January 2025, Copperprotek developed a copper-containing masterbatch for the interior layer of food packaging, leveraging the antimicrobial properties of copper ions to extend product shelf life and reduce food waste in supply chains.

Expansion of Lightweight Plastic Applications in the Automotive Sector

India’s automotive industry is increasingly substituting metal components with engineered plastic parts to reduce vehicle weight and improve fuel efficiency, driving significant masterbatch consumption. Color and additive masterbatches enhance the aesthetics, UV resistance, and thermal stability of interior and exterior automotive components. The transition toward electric vehicles is further intensifying demand for high-performance plastic materials. India’s plastic industry, projected to grow from USD 44.28 billion in 2025 to USD 60.11 billion by 2030, underscores the expanding opportunity for automotive-grade masterbatch solutions that meet stringent performance specifications.

Market Outlook 2026-2034:

The India masterbatch market is poised for sustained expansion over the forecast period, supported by robust growth in end-use industries and increasing investments in domestic manufacturing capacity. The packaging sector will continue to be the primary demand driver, bolstered by the expansion of organized retail, quick-commerce platforms, and pharmaceutical packaging requirements. Advances in polymer processing and the rising adoption of sustainable masterbatch formulations will further broaden application opportunities. The market generated a revenue of USD 411.31 Million in 2025 and is projected to reach a revenue of USD 613.91 Million by 2034, growing at a compound annual growth rate of 4.55% from 2026-2034.

India Masterbatch Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Color |

42% |

|

Polymer Type |

PP |

30% |

|

Application |

Packaging |

44% |

Type Insights:

- Color

- White

- Black

- Additive

- Filler

Color dominates with a market share of 42% of the total India masterbatch market in 2025.

Color masterbatch is the cornerstone of India’s plastics coloring industry, enabling manufacturers to achieve consistent, vibrant hues across a wide spectrum of applications. The segment’s leadership reflects the strong demand for brand differentiation in packaging, consumer goods, and automotive interiors, where visual appeal directly influences purchasing decisions. Color masterbatches offer precise pigment dispersion and compatibility with multiple polymer carriers, simplifying production while ensuring uniform quality in high-volume manufacturing environments.

The expanding consumer goods and FMCG sectors are intensifying the need for custom color solutions that meet specific aesthetic and regulatory standards. Indian manufacturers are increasingly investing in advanced color-matching technologies and expanding their product portfolios to serve diverse industry requirements. For instance, Plastiblends India Limited, headquartered in Mumbai with an annual production capacity exceeding 130,000 metric tonnes across facilities in Daman, Roorkee, and Palsana, exports masterbatches to over 60 countries and has been recognized by the Plastics Export Promotion Council for highest export performance in FY 2022-23.

Polymer Type Insights:

- PP

- LDPE/LLDPE

- HDPE

- PVC

- PUR

- PET

- PS

- Others

PP leads with a share of 30% of the total India masterbatch market in 2025.

Polypropylene is the most widely used carrier polymer in India’s masterbatch industry due to its excellent mechanical strength, chemical resistance, and cost-effectiveness. PP-based masterbatches are extensively utilized in flexible packaging, woven sacks, automotive trim, and appliance housings, reflecting the polymer’s versatility across both commodity and engineering applications. The segment’s dominance is reinforced by India’s substantial PP production capacity and its alignment with the country’s manufacturing priorities.

The use of polypropylene in India is increasing along with the development in packaging and infrastructure industries. The focus of the government on programs like Jal Jeevan Mission and Smart Cities Mission creates a long-term demand for PP-based pipes, fittings, and construction materials that would demand the special masterbatch formulations. The Production-Linked Incentive scheme is also directing capital into the Jamnagar-Dahej petrochemical corridor in Gujarat, which reinforced the domestic supply chain of PP as well as contributed to the further growth of the consumption of the PP-based masterbatches.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Packaging

- Building and Construction

- Consumer Goods

- Automotive

- Textile

- Agriculture

- Others

Packaging represent the largest share, accounting for 44% of the total India masterbatch market in 2025.

The packaging sector’s dominance in masterbatch consumption reflects the fundamental role of plastic packaging in India’s FMCG, food processing, pharmaceutical, and e-commerce industries. Masterbatches enable packaging manufacturers to achieve vibrant colors, UV protection, antimicrobial properties, and enhanced barrier characteristics that are essential for product preservation and consumer appeal. The rapid growth of quick-commerce and organized retail is further intensifying demand for functional and visually differentiated packaging solutions.

India’s plastic packaging industry continues to witness strong expansion, driven by the rapid growth of e-commerce and the rising popularity of quick-commerce delivery platforms. Increasing parcel volumes are encouraging innovation in packaging formats, particularly in tamper-evident pouches and moisture-resistant films designed to ensure product safety and durability during transit. These evolving requirements are prompting packaging manufacturers to develop advanced material solutions that combine functionality, protection, and convenience to meet the changing needs of retailers and consumers. For instance, in May 2025, Chemco Group and Kandoi Group announced a joint venture investing INR 450 crore to establish two greenfield PET recycling facilities in Gujarat, capable of recycling over 10 million PET bottles daily, underscoring the growing convergence of sustainable packaging and masterbatch demand.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

North India derives strength from its closeness to major industrial centers and well-established plastics processing clusters. These integrated ecosystems support consistent demand for masterbatch products, particularly across packaging and fast-moving consumer goods applications, ensuring stable consumption driven by ongoing manufacturing and distribution activities in the region.

West and Central India account for the highest regional consumption, supported by a strong presence of petrochemical complexes, packaging converters, and automotive production facilities. The concentration of integrated manufacturing operations in these states sustains significant masterbatch usage across diverse industrial and consumer-oriented applications.

South India is steadily emerging as a high-growth region, fueled by expanding manufacturing hubs in key cities. Rising investments in plastics processing, automotive components, and electronics production are creating new avenues for masterbatch demand, strengthening the region’s role in the evolving industrial landscape.

East and Northeast India represent developing markets where infrastructure expansion, agricultural modernization, and improving consumer goods distribution networks are gradually stimulating masterbatch consumption. As industrial activities expand and supply chains mature, the region is expected to witness progressive growth in plastics and related material demand.

Market Dynamics:

Growth Drivers:

Why is the India Masterbatch Market Growing?

Expanding Packaging Industry Driven by E-Commerce and Organized Retail Growth

The rapid expansion of India’s packaging sector is the primary catalyst for masterbatch demand growth. Rising consumer preference for packaged food, beverages, personal care products, and pharmaceuticals is creating sustained requirements for color, additive, and white masterbatches that enhance packaging aesthetics and functionality. The explosive growth of e-commerce and quick-commerce platforms is generating unprecedented demand for durable secondary packaging materials including tamper-evident pouches, stretch films, and protective liners. The India e-commerce market size was valued at USD 129.72 Billion in 2025 and is projected to reach USD 651.10 Billion by 2034, growing at a compound annual growth rate of 19.63% from 2026-2034. The government’s Extended Producer Responsibility guidelines enacted in 2024 are further driving innovation in recyclable packaging solutions that depend on specialized masterbatch formulations.

Government Infrastructure Programs and Construction Sector Expansion

India’s ambitious infrastructure development agenda is generating significant demand for masterbatch-enhanced plastic products used in construction and utilities. Large-scale government programs including Jal Jeevan Mission for universal piped water supply, Smart Cities Mission for urban modernization, and Pradhan Mantri Awas Yojana for affordable housing are driving consumption of PP and PVC pipes, fittings, cables, and roofing materials that require specialized masterbatch formulations. The construction sector’s growing preference for lightweight, corrosion-resistant, and durable plastic building materials over traditional alternatives is expanding the application scope for color, UV-stabilizer, and filler masterbatches. The government’s allocation of INR 11.11 lakh crore for capital expenditure on infrastructure in the 2024-25 Union Budget reinforces the sustained demand trajectory for construction-grade plastic products.

Automotive Lightweighting and Electric Vehicle Transition

The Indian automotive industry is also moving more to lightweight plastic parts, and it is pushing up the demand for masterbatches used in both traditional and electric vehicle systems. Enterprises are substituting the old metal components with engineered plastics in the form of bumpers, dashboard, door panels, and under-the-hood systems to minimize the total weight of the vehicle and improve efficiency. The use of color and additive masterbatches is crucial in providing the required aesthetic look, UV stability, heat resistance, and flame-retardant features needed by automotive-grade materials. Supportive mobility initiatives and broader industry development strategies are further stimulating the need for high-performance plastics. As the domestic plastics industry continues to advance, the automotive segment remains a significant growth avenue for value-added masterbatch solutions.

Market Restraints:

What Challenges the India Masterbatch Market is Facing?

Volatility in Raw Material Prices

Fluctuations in the prices of petroleum-derived raw materials, pigments, and carrier resins create cost uncertainties for masterbatch manufacturers. Rising naphtha and polymer feedstock prices compress margins and complicate pricing strategies. This volatility discourages long-term investment planning and affects the profitability of smaller producers who lack the scale to absorb cost fluctuations effectively.

Stringent Environmental Regulations on Conventional Plastics

Increasingly strict regulations targeting plastic waste and single-use plastics are constraining certain segments of masterbatch demand. While these policies promote sustainable alternatives, compliance costs increase production expenses for conventional masterbatch formulations. Manufacturers must invest significantly in reformulating products to meet evolving environmental standards, creating transitional challenges for the industry.

Competition from Alternative Coloring and Additive Technologies

The emergence of alternative technologies such as liquid colorants and pre-colored polymers poses competitive challenges to traditional masterbatch products. These alternatives offer advantages including improved pigment dispersion, reduced processing time, and lower waste generation. As some processors adopt these solutions for specific applications, conventional masterbatch manufacturers face pressure to innovate and demonstrate superior value.

Competitive Landscape:

The India masterbatch market features a moderately fragmented competitive landscape characterized by the coexistence of established domestic manufacturers and global players. Companies are investing in capacity expansion, product diversification, and research and development to strengthen their competitive positioning. Domestic producers leverage their understanding of local market requirements and cost advantages, while multinational companies bring advanced technologies and global quality standards. Strategic partnerships, technology licensing agreements, and geographic expansion into underserved regions are key competitive strategies. Sustainability has emerged as a critical differentiator, with leading manufacturers developing recyclable, bio-based, and circular economy-compliant masterbatch solutions to meet evolving regulatory requirements and customer preferences.

India Masterbatch Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Color, White, Black, Additive, Filler |

| Polymer Types Covered | PP, LDPE/LLDPE, HDPE, PVC, PUR, PET, PS, Others |

| Applications Covered | Packaging, Building and Construction, Consumer Goods, Automotive, Textile, Agriculture, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Masterbatch Market Research Report and Industry Forecast Report

The India masterbatch market size was valued at USD 411.31 Million in 2025.

The India masterbatch market is expected to grow at a compound annual growth rate of 4.55% from 2026-2034 to reach USD 613.91 Million by 2034.

Color masterbatch, holding the largest share of 42% in 2025, dominates the India masterbatch market due to its critical role in enabling consistent, vibrant coloring for packaging, consumer goods, automotive, and textile applications that require precise brand differentiation.

Key factors driving the India masterbatch market include expanding packaging demand fueled by e-commerce and organized retail growth, government infrastructure development programs, automotive lightweighting trends, rising adoption of sustainable plastic formulations, and increasing investments in domestic manufacturing capacities.

Major challenges include volatility in petroleum-derived raw material prices, stringent environmental regulations on conventional plastics, competition from alternative coloring technologies, supply chain disruptions affecting pigment and additive availability, and compliance costs associated with evolving sustainability standards.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)