India Material Handling Equipment Market Size, Share, Trends and Forecast by Product, Application, and Region, 2026-2034

India Material Handling Equipment Market Size, Share, Trends & Forecast (2026-2034)

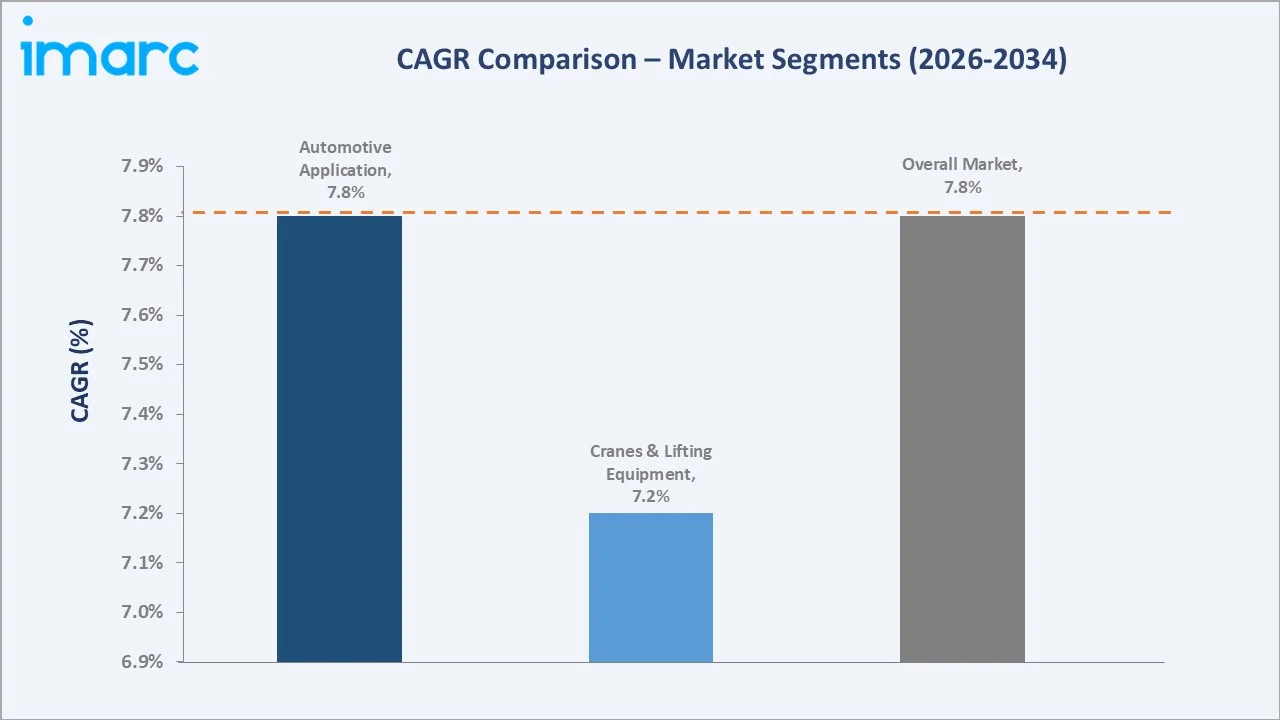

The India material handling equipment market size reached USD 11.42 Billion in 2025 and is projected to reach USD 23.30 Billion by 2034, exhibiting a CAGR of 7.83% during 2026-2034. Rapid industrialization, expanding manufacturing activities, PLI scheme investments, rising e-commerce logistics, and advanced automation adoption are the primary forces driving this market.

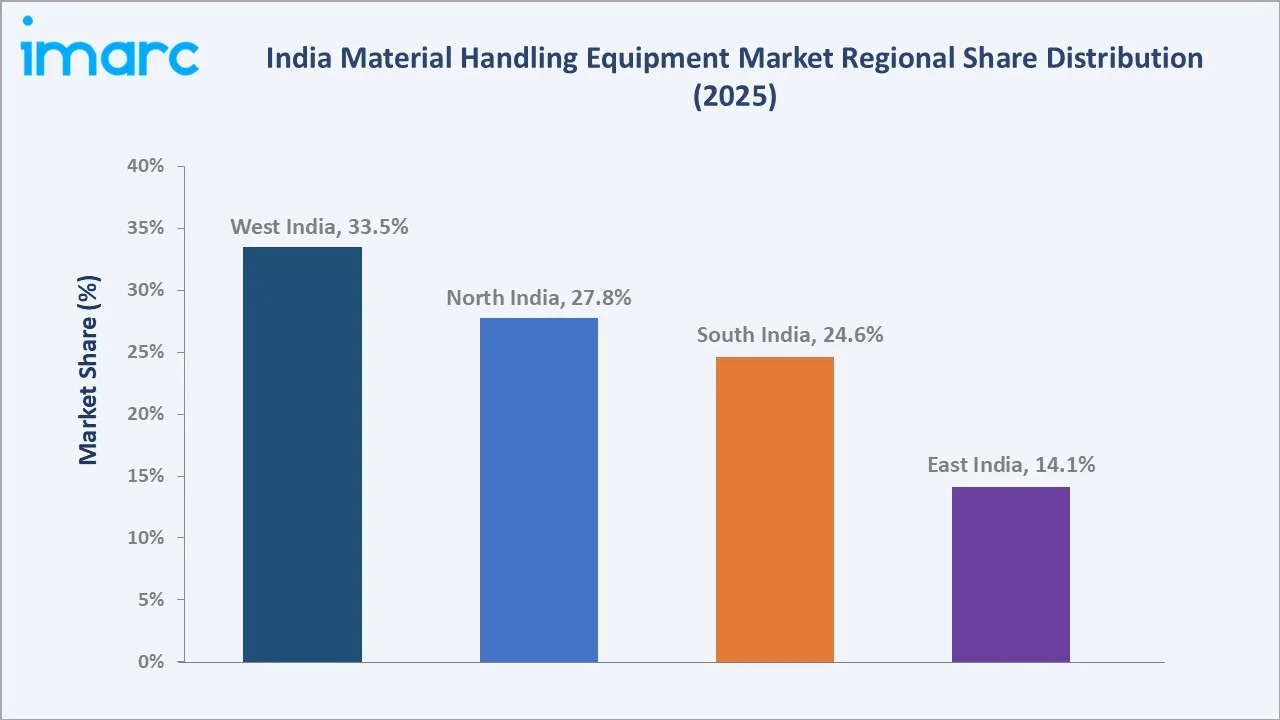

Industrial trucks dominate the product mix at 34.8% in 2025, while e-commerce leads the application segment at 21.4%. West India commands a 33.5% regional share in 2025, reflecting the concentration of manufacturing, logistics, and port infrastructure across Gujarat and Maharashtra.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 11.42 Billion |

|

Forecast Market Size (2034) |

USD 23.30 Billion |

|

CAGR (2026-2034) |

7.83% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West India (33.5% share, 2025) |

|

Second Largest Region |

North India (27.8% share, 2025) |

|

Leading Product |

Industrial Trucks (34.8%, 2025) |

|

Leading Application |

E-commerce (21.4%, 2025) |

The market growth trajectory from 2020 through 2034, with historical expansion to USD 11.42 Billion in 2025, reflects consistent infrastructure-driven demand. The forecast to USD 23.30 Billion captures accelerating automation investment, Gati Shakti-linked logistics build-out, and industrial corridor expansion.

To get more information on this market, Request Sample

The CAGR trajectories across key product and application sub-segments, with continuous handling equipment at ~9.1% CAGR and e-commerce applications at ~10.2% CAGR, are the fastest-growing categories within the India material handling equipment industry through 2034.

Executive Summary

The India material handling equipment market is on a sustained growth trajectory from USD 11.42 Billion in 2025 to USD 23.30 Billion by 2034. Material handling equipment, essential for transporting, storing, and controlling goods across manufacturing, logistics, and warehousing operations, benefits from India's non-discretionary industrial demand.

Industrial trucks dominate the product mix at 34.8% in 2025, driven by broad deployment across e-commerce fulfillment centers, automotive plants, and general manufacturing. Cranes and lifting equipment (28.6%) are critical for construction, port operations, and heavy manufacturing, growing with National Infrastructure Pipeline investments.

West India leads with 33.5% in 2025, anchored by Gujarat's manufacturing and JNPT port traffic, and Maharashtra's automotive and pharmaceutical corridors. North India (27.8%) and South India (24.6%) follow, driven by industrial clusters around Delhi-NCR and Chennai-Bengaluru respectively.

Key Market Insights

|

Insight |

Data |

|

Leading Product |

Industrial Trucks – 34.8% share (2025) |

|

Second Product |

Cranes & Lifting Equipment – 28.6% share (2025) |

|

Leading Application |

E-commerce – 21.4% share (2025) |

|

Second Application |

Automotive – 18.7% share (2025) |

|

Leading Region |

West India – 33.5% share (2025) |

|

Key Companies |

Action Construction Equipment Ltd., Godrej Enterprises, KION Group AG, Toyota, Konecranes, Daifuku Co., Ltd., Beumer Group |

Key Analytical Observations Expanding on the Above Data:

- Industrial trucks at 34.8% in 2025 dominate due to their versatility across forklifts, pallet jacks, and AGVs in e-commerce fulfillment, automotive assembly, and cold-chain logistics across India.

- E-commerce at 21.4% in 2025 leads applications because India's rapidly expanding online retail market demands automated sortation, conveying, and storage systems capable of handling high SKU counts and rapid throughput.

- West India's 33.5% dominance reflects Gujarat's export-oriented manufacturing concentration, JNPT port traffic, and Maharashtra's dense automotive and pharmaceutical manufacturing ecosystem.

- The PLI scheme covering 14 key sectors is creating large-scale capital goods procurement for advanced intralogistics, automated racking, and conveying systems in newly constructed manufacturing plants.

India Material Handling Equipment Market Overview

Material handling equipment (MHE) encompasses mechanical, electromechanical, and automated systems designed to move, store, control, and protect materials, goods, and products throughout manufacturing, distribution, and disposal processes. Product configurations range from manual pallet trucks and hand-operated cranes to fully automated AS/RS and robotic picking systems.

.webp)

The India ecosystem integrates domestic manufacturers, multinational subsidiaries, EPC contractors, steel and component suppliers, automation software developers, and diverse end-use industries spanning e-commerce, automotive, food processing, chemicals, pharmaceuticals, aviation, and semiconductors.

Market Dynamics

To evaluate market opportunities, Request Sample

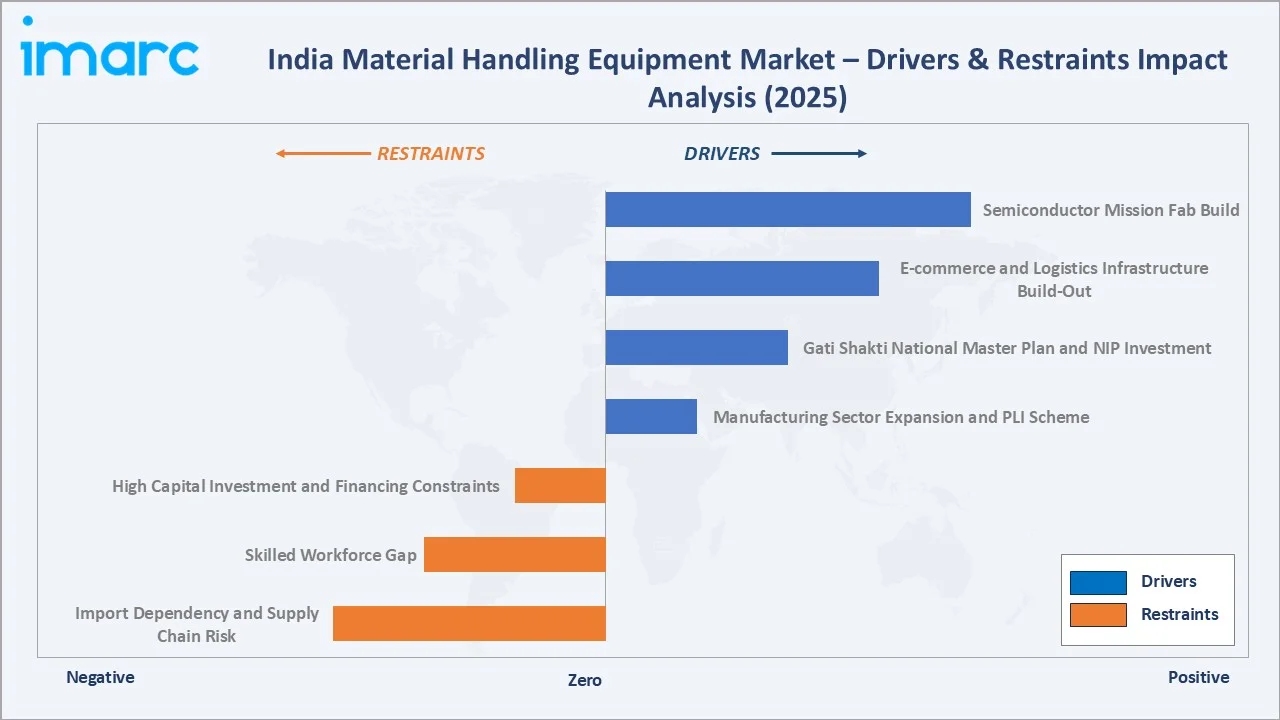

Market Drivers

- Manufacturing Sector Expansion and PLI Scheme: India's Annual Survey of Industries (ASI) 2021–22 reported a 26.6% surge in manufacturing GVA. The PLI scheme across 14 sectors generates large-scale MHE procurement to manage elevated production volumes and reduce operational cycle times.

- E-commerce and Logistics Infrastructure Build-Out: India’s e-commerce sector is expanding rapidly and is expected to reach a substantial market size in the near term. This growth is driving large-scale development of warehousing and fulfillment infrastructure. As a result, there is rising demand for material handling and storage solutions, including conveyor systems, automated sorting technologies, advanced racking structures, and efficient industrial transport equipment.

- Gati Shakti National Master Plan and NIP Investment: The USD 1.4 Trillion National Infrastructure Pipeline accelerates port, airport, highway, and industrial corridor construction, each requiring cranes, lifting systems, and heavy-capacity handling equipment.

Market Restraints

- High Capital Investment and Financing Constraints: Advanced automated material handling equipment (MHE) systems require substantial upfront capital, with large-scale automated storage and retrieval system (AS/RS) installations involving multi-million-dollar investments per facility. Small and medium-sized enterprises (SMEs) often face limited access to financing, which restricts their ability to adopt advanced automation solutions.

- Skilled Workforce Gap: Operating and maintaining advanced automated handling systems requires specialized technical skills. India's shortage of certified MHE technicians constrains adoption of higher-automation solutions, particularly in Tier-2 and Tier-3 industrial cities.

Market Opportunities

- Cold Chain Expansion: India’s cold chain logistics sector is witnessing steady growth, driving the need for temperature-controlled storage and handling infrastructure. This includes increased demand for automated cold storage systems, specialized conveying solutions, and refrigerated racking across industries such as food, pharmaceuticals, and agriculture.

- Semiconductor and Electronics Manufacturing: India's emerging semiconductor ecosystem, with investments exceeding USD 15 Billion under the India Semiconductor Mission, requires precision handling, clean-room compatible automated systems, and specialized lifting equipment.

Market Challenges

- Import Dependency and Supply Chain Risk: India remains significantly reliant on imports for advanced material handling equipment (MHE) components such as precision drives, PLC controllers, and robotic systems. This dependence exposes the sector to external risks, including currency fluctuations and global supply chain disruptions, leading to cost volatility for end-users.

- Regulatory Fragmentation: Varying BIS certification requirements and state-specific GST compliance obligations create complexity for national MHE deployments, adding lead time and compliance cost to multi-state projects.

Emerging Market Trends

.webp)

1. IoT and Industry 4.0 Integration Transforming Warehouse Operations

IoT sensor-enabled forklifts, smart racking with weight monitoring, and AI-powered warehouse management systems are being adopted at scale. Integration with ERP platforms reduces inventory errors by 40–60% and improves asset utilization in multi-facility operations across India.

2. Electric and Green MHE Adoption Accelerating

India's push for net-zero manufacturing is driving adoption of lithium-ion battery-powered forklifts and electric cranes. In August 2024, Godrej & Boyce introduced India's first lithium-ion battery-operated forklift, offering 15% improved run time and zero-emission operations at LogiMAT India 2025.

3. Automated Guided Vehicles (AGVs) and AMRs Scaling Up

E-commerce fulfillment centers and automotive plants are deploying AGVs and autonomous mobile robots (AMRs) to replace manual pallet movement. India's AMR adoption rate is growing at over 35% CAGR, supported by falling hardware costs and improving navigation software.

4. Rental and Leasing Models Unlocking SME Demand

In July 2025, SILA collaborated with Nilkamal to introduce a rental model for electric MHE in India. This lowers adoption barriers for SMEs and warehousing startups, significantly expanding the addressable market for electric trucks and automated systems.

Industry Value Chain Analysis

The India MHE value chain spans six stages from raw material input through end-use deployment. Fabrication, automation software integration, and after-market service capture the highest value-add margins, while distribution and project customization generate significant working capital requirements.

The Indian material handling equipment market value chain is becoming more integrated, with increasing localization of manufacturing and stronger supplier networks reducing dependency on imports. Demand is driven by rapid growth in e-commerce, warehousing, and infrastructure, pushing OEMs to innovate in automation and cost efficiency. Overall, competitive advantage is shifting toward players who can optimize end-to-end solutions, after-sales service, and technology integration.

|

Stage |

Description |

|

Raw Material Supply |

Steel, aluminum, and precision components from domestic and imported sources |

|

MHE Fabrication |

OEM manufacturing of trucks, cranes, conveyors, and storage systems |

|

Automation & Controls |

PLC, sensors, drives, and warehouse management software integration |

|

Distribution & Stocking |

Dealer networks, regional distributors, and service centres |

|

Project Installation |

EPC contractors and OEM teams for commissioning and deployment |

|

End-Use Industries |

E-commerce, Automotive, Food & Beverages, Chemicals, Pharmaceuticals, Aviation |

Technology Landscape in the India MHE Industry

Automation: AGVs, AS/RS, and Robotics

Automated Storage and Retrieval Systems (AS/RS) with mini-load and unit-load configurations are being deployed in pharmaceutical and e-commerce warehouses across NCR and Bengaluru. These systems achieve throughput rates of 400–1,200 pallet moves per hour with 99.9% inventory accuracy.

Digital Twin and Simulation Technology

Leading MHE OEMs are adopting digital twin platforms to simulate material flow, identify bottlenecks, and optimize warehouse layout before physical deployment. KION Group's partnership with NVIDIA and Accenture to implement Physical AI represents the frontier of this technology in India.

Electric Power Train and Battery Technology

Lithium-ion battery technology is displacing lead-acid batteries across industrial truck segments. Lithium-ion forklifts offer 3–4x longer service life, opportunity charging capability, and 20–30% total cost of ownership reduction over 10-year fleet lifecycles.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Industrial trucks |

34.8% |

2025 |

|

Application |

E-commerce |

21.4% |

2025 |

|

Region |

West India |

33.5% |

2025 |

By Product

Industrial trucks command a 34.8% majority share in 2025 owing to their fundamental versatility and broad deployment across India's rapidly expanding logistics, e-commerce, and manufacturing sectors. Counterbalanced forklifts, reach trucks, pallet stackers, and electric tow tractors are the core product types driving volume demand.

To access detailed market analysis, Request Sample

Cranes and lifting equipment at 28.6% in 2025 are indispensable for construction, port operations, and process plant maintenance. The National Infrastructure Pipeline is sustaining multi-year demand for overhead cranes, mobile cranes, and hoists. Continuous handling equipment (20.7%) serves automated conveying and sortation in high-throughput e-commerce and food processing facilities, growing fastest at ~9.1% CAGR. Racking and storage equipment (15.9%) supports dense storage in newly built warehousing and cold-chain facilities.

By Application

E-commerce at 21.4% in 2025 leads all application segments, reflecting India's world-leading e-commerce growth rate and consequent multi-billion-dollar investment in automated fulfillment infrastructure. Amazon, Flipkart, Meesho, and Reliance Retail's logistics buildouts are generating large-scale MHE procurement across all product categories.

Automotive at 18.7% in 2025 represents a structurally important segment as India's passenger vehicle and EV manufacturing expansion generates high-volume MHE procurement for body shops, assembly lines, and paint shops. Food and Beverages (14.6%) demand specialized hygienic conveying and automated palletizing. Semiconductor and Electronics (12.3%) is the fastest-growing application at ~12.5% CAGR, driven by India Semiconductor Mission fab investments.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

West India |

33.5% |

JNPT port logistics; Gujarat manufacturing SEZs; Maharashtra automotive & pharma clusters |

|

North India |

27.8% |

Delhi-NCR warehousing; UP-Haryana industrial corridors; Ludhiana manufacturing |

|

South India |

24.6% |

Chennai automotive hub; Bengaluru technology & aerospace; Hyderabad pharma & data centers |

|

East India |

14.1% |

Kolkata port; Odisha and Jharkhand mining and steel; emerging warehousing in Patna |

West India's 33.5% market dominance in 2025 is driven by the Dedicated Freight Corridor connecting Dadri to JNPT, Gujarat's 34 special economic zones, and Maharashtra's concentration of automotive OEMs and Tier-1 suppliers, all generating high-volume MHE procurement.

North India at 27.8% benefits from the Delhi-Mumbai Industrial Corridor, the National Capital Region's position as India's largest e-commerce fulfillment hub, and Haryana and UP warehouse clusters serving Amazon, Flipkart, and Meesho distribution networks.

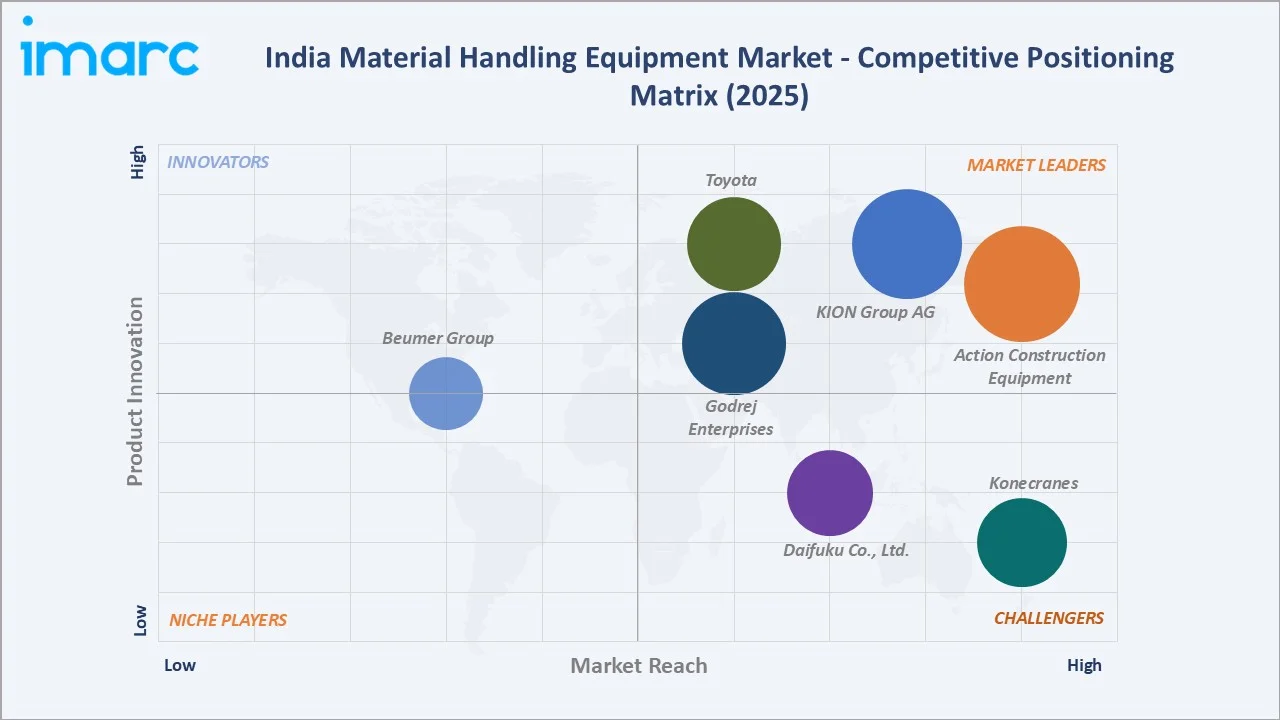

Competitive Landscape

The India material handling equipment market is moderately fragmented, with domestic leaders holding strong positions in industrial trucks and cranes, while global MNCs compete in automation and specialized segments. The PLI scheme is attracting new multinational entrants establishing local manufacturing.

|

Company |

Key Products |

Position |

Strategic Focus |

|

Action Construction Equipment Ltd. |

Mobile Cranes, Tower Cranes, Forklifts |

Leader |

Largest domestic crane OEM; infrastructure & construction |

|

Godrej Enterprises |

Electric Forklifts, Forklifts, Reach Trucks, Stackers |

Leader |

Pioneer in lithium-ion MHE; green logistics focus |

|

KION Group AG |

Linde Forklifts, Warehouse Trucks |

Leader |

Premium intralogistics; warehouse automation; EV forklifts |

|

Toyota |

Electric Counterbalance Trucks, Powered Pallet Trucks, Powered Stackers, Reach Trucks, Articulated Counterbalance Trucks |

Leader |

JIT supply chain; automotive sector dominance |

|

Konecranes |

Industrial Cranes, Hoists |

Challenger |

Smart crane technology; IoT-enabled predictive maintenance |

|

Daifuku Co., Ltd. |

Conveyors, AS/RS, Sortation Systems |

Challenger |

Airport logistics & advanced automation; Hyderabad plant |

|

Beumer Group |

Conveyors, Sortation, Palletizing |

Emerging |

Airport & distribution; bulk materials & parcel logistics |

Key players include Action Construction Equipment Ltd., Godrej Enterprises, KION Group AG, Toyota, Konecranes, Daifuku Co., Ltd., Beumer Group, and others.

Key Company Profiles

Action Construction Equipment Ltd.

Action Construction Equipment Ltd. is India's largest domestic manufacturer of construction and material handling equipment, headquartered in Faridabad, Haryana. ACE holds leading positions in mobile cranes, tower cranes, and forklifts with distribution across 500+ touch points nationally.

- Product Portfolio: Mobile Cranes, Tower Cranes, Forklifts

- Recent Developments: In February 2023, ACE unveiled India's first fully electric mobile crane at Bauma Conexpo 2023, aligning with Make in India and sustainable technology goals.

- Strategic Focus: ACE's strategy leverages its domestic manufacturing cost advantage and wide distribution network to capture infrastructure-linked crane demand under the NIP, while expanding its electric MHE portfolio to meet sustainability mandates across logistics and manufacturing sectors.

KION Group AG

KION Group is the world's second-largest industrial truck manufacturer and a leading provider of supply chain automation solutions globally.

- Product Portfolio: Linde Forklifts, Warehouse Trucks

- Strategic Focus: KION India focuses on premium intralogistics automation for large-format e-commerce, automotive, and pharmaceutical warehouses, where its integrated truck-automation-software offering commands significant pricing power over standalone equipment providers.

Daifuku Co., Ltd.

Daifuku operates across airport baggage handling, automotive assembly, and general warehouse automation markets across India.

- Product Portfolio: Conveyors, AS/RS, Sortation Systems

- Recent Developments: In April 2025, Daifuku Co., Ltd. inaugurated a new manufacturing plant in Hyderabad, India to meet growing demand for material handling systems.

- Strategic Focus: Daifuku India's strategy focuses on airport modernization projects, automotive production line automation, and large-scale e-commerce AS/RS deployments, leveraging its parent's global engineering capabilities and project execution experience across India.

Market Concentration Analysis

The India material handling equipment market is moderately fragmented at the national level, with no single company holding more than 8–12% of total market revenue. Domestic leaders like ACE and TIL hold concentrated positions in cranes, while multinational brands like KION and Toyota dominate premium industrial truck segments.

Consolidation through strategic partnerships is emerging. The Godrej-KION competition dynamic, Daifuku's new Hyderabad plant, and Jungheinrich's bundled racking-plus-truck offerings reflect a shift toward integrated solution providers capturing higher-value automation project revenue across India.

Investment & Growth Opportunities

Fastest-Growing Segments

Continuous handling equipment at ~9.1% CAGR through 2034 is the highest-growth product segment, driven by e-commerce sortation, food processing conveying, and automated pharmaceutical dispensing. Semiconductor and electronics applications at ~12.5% CAGR represent the highest-growth application vertical.

Emerging Markets

East India at ~8.5% CAGR is the fastest-growing region for MHE through 2034. Odisha's industrial corridor, Bengal's logistics park expansion, and Bihar-Jharkhand mining infrastructure investments are creating significant MHE procurement from a currently undersupplied region.

Venture & Investment Trends

Private equity interest in India-focused intralogistics automation is accelerating. Domestic AMR start-ups have attracted USD 200+ Million in venture funding since 2022. Rental model platforms for electric MHE, following SILA-Nilkamal's 2025 collaboration, are lowering entry barriers and expanding the addressable market.

Future Market Outlook (2026-2034)

The India material handling equipment market is forecast to expand from USD 11.42 Billion in 2025 to USD 23.30 Billion by 2034 at a CAGR of 7.83%, adding USD 11.88 Billion in incremental annual market value over the forecast period. This sustained growth reflects India's infrastructure-investment-linked, non-discretionary demand characteristics.

Three structural forces will most significantly shape the India MHE industry through 2034: India Semiconductor Mission fab construction generating precision handling procurement; Gati Shakti-linked freight corridor and port automation; and the transition of organized retail and FMCG to fully automated distribution centers with AI-driven warehouse management.

Research Methodology

Primary Research

Primary research encompassed structured interviews with India MHE industry stakeholders, including senior commercial managers at domestic OEMs, EPC procurement specialists, warehouse automation engineers, logistics park developers, and operations heads at major e-commerce and automotive companies across India.

Secondary Research

Key secondary sources include Annual Survey of Industries (ASI) 2021–22, Index of Industrial Production (IIP), National Logistics Policy 2022 documentation, Ministry of Commerce PLI scheme notifications, DPIIT FDI statistics, CII Logistics Council reports, and trade publications including Materials Handling World, Indian Infrastructure, and Logistics Insider.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, industrial production indices, manufacturing GVA data, e-commerce GMV projections, and historical market evolution patterns.

India Material Handling Equipment Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Cranes and Lifting Equipment, Industrial Trucks, Continuous Handling Equipment, Racking and Storage Equipment |

| Applications Covered | Automotive, Food and Beverages, Chemical, Semiconductors and Electronics, E-Commerce, Aviation, Pharmaceutical, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Action Construction Equipment Ltd., Godrej Enterprises, KION Group AG, Toyota, Konecranes, Daifuku Co., Ltd., Beumer Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India material handling equipment market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India material handling equipment market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India material handling equipment industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Material Handling Equipment Market Report

The India material handling equipment market reached USD 11.42 Billion in 2025, driven by rapid industrialization, PLI scheme-linked manufacturing expansion, and e-commerce fulfillment infrastructure investment across India.

The market is projected to reach USD 23.30 Billion by 2034, growing at a CAGR of 7.83% during 2026-2034, driven by Gati Shakti logistics build-out, semiconductor manufacturing investments, and automation adoption.

Industrial trucks lead with a 34.8% product share in 2025, valued for their versatility across forklifts, AGVs, and pallet systems serving the logistics, automotive, and general manufacturing sectors.

E-commerce leads at 21.4% in 2025, representing the most dynamic demand driver as Amazon, Flipkart, and Meesho build large-scale automated fulfillment infrastructure across India's top logistics clusters.

West India commands a dominant 33.5% market share in 2025, driven by JNPT port volumes, Gujarat's export manufacturing SEZs, and Maharashtra's dense automotive and pharmaceutical industrial base.

Semiconductor and electronics are the fastest-growing application at ~12.5% CAGR through 2034, driven by India Semiconductor Mission investments creating entirely new precision handling requirements.

Leading companies include Action Construction Equipment Ltd., Godrej Enterprises, KION Group AG, Toyota, Konecranes, Daifuku Co., Ltd., Beumer Group, and others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)