India Meat Market Size, Share, Trends and Forecast by Type, Product, Distribution Channel, and Region, 2026-2034

India Meat Market Size, Share, Trends & Forecast (2026-2034)

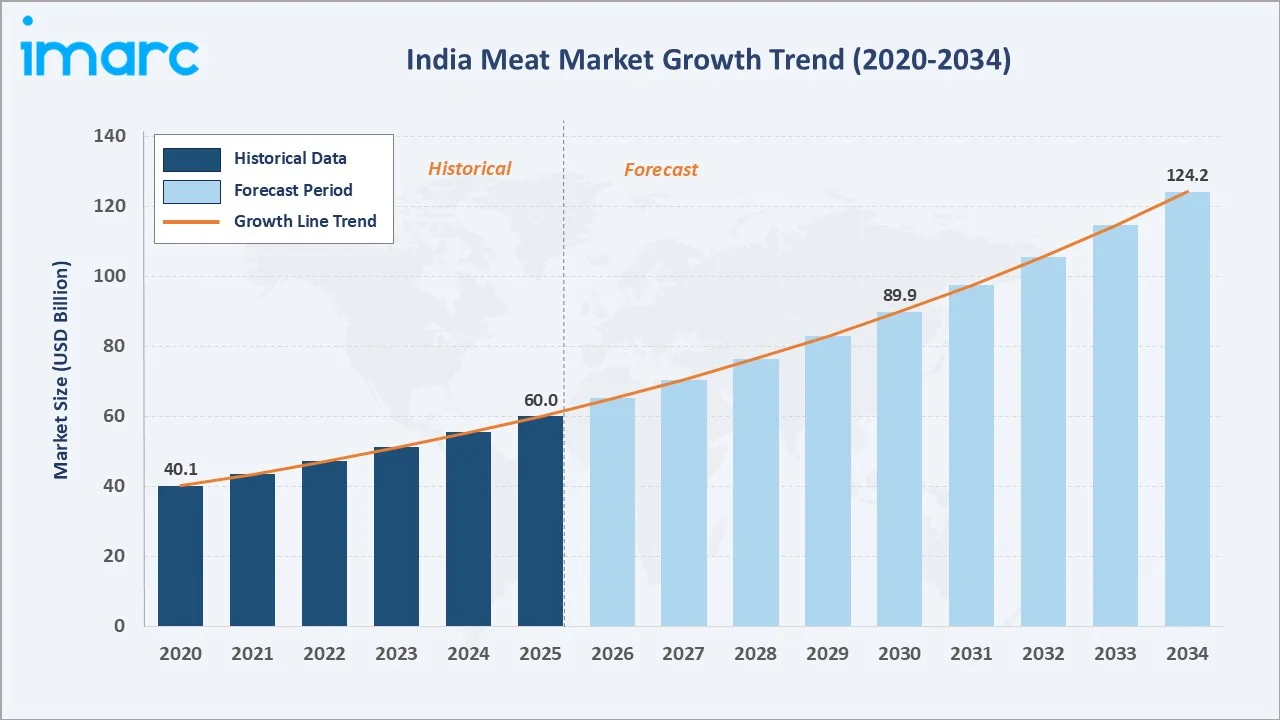

The India meat market was valued at USD 60.0 Billion in 2025 and is projected to reach USD 124.2 Billion by 2034, exhibiting a CAGR of 8.42% during 2026-2034. Rising urbanization, increasing disposable incomes, and expansion of cold chain and e-commerce delivery platforms are the primary drivers shaping the market growth. According to the Economic Survey 2023-24, it is projected that over 40% of India's population will reside in urban regions by 2030.

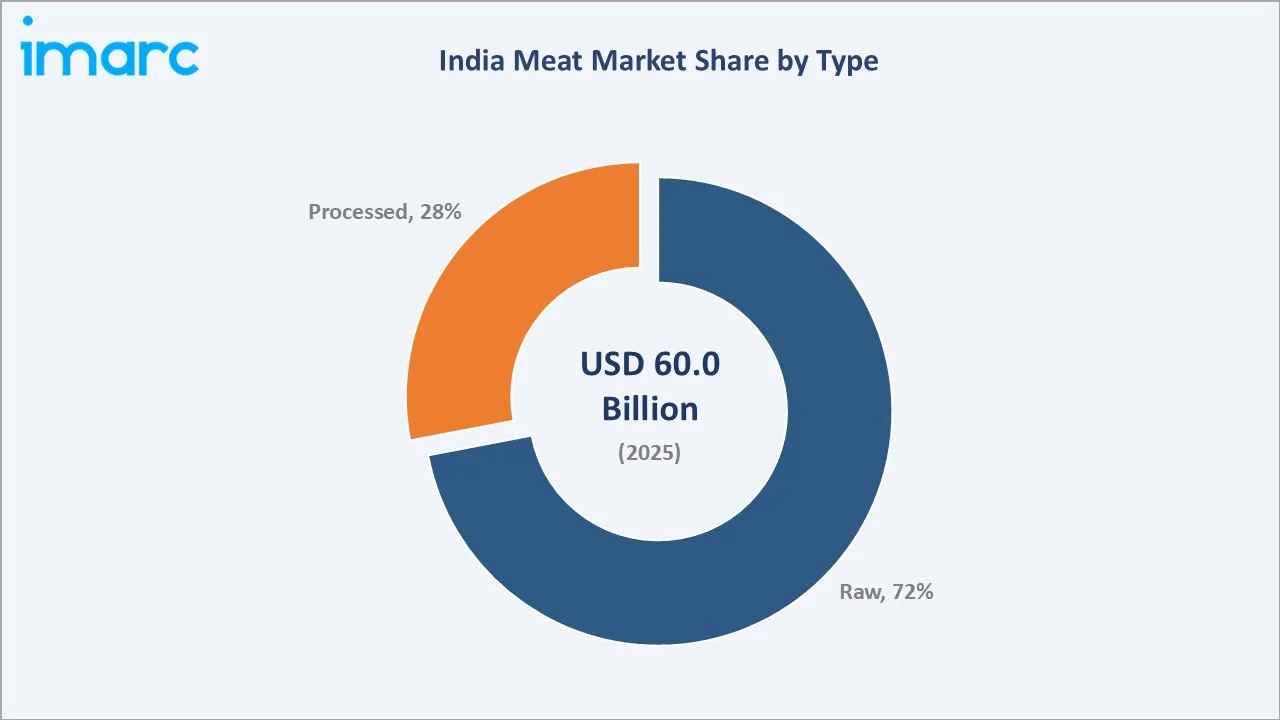

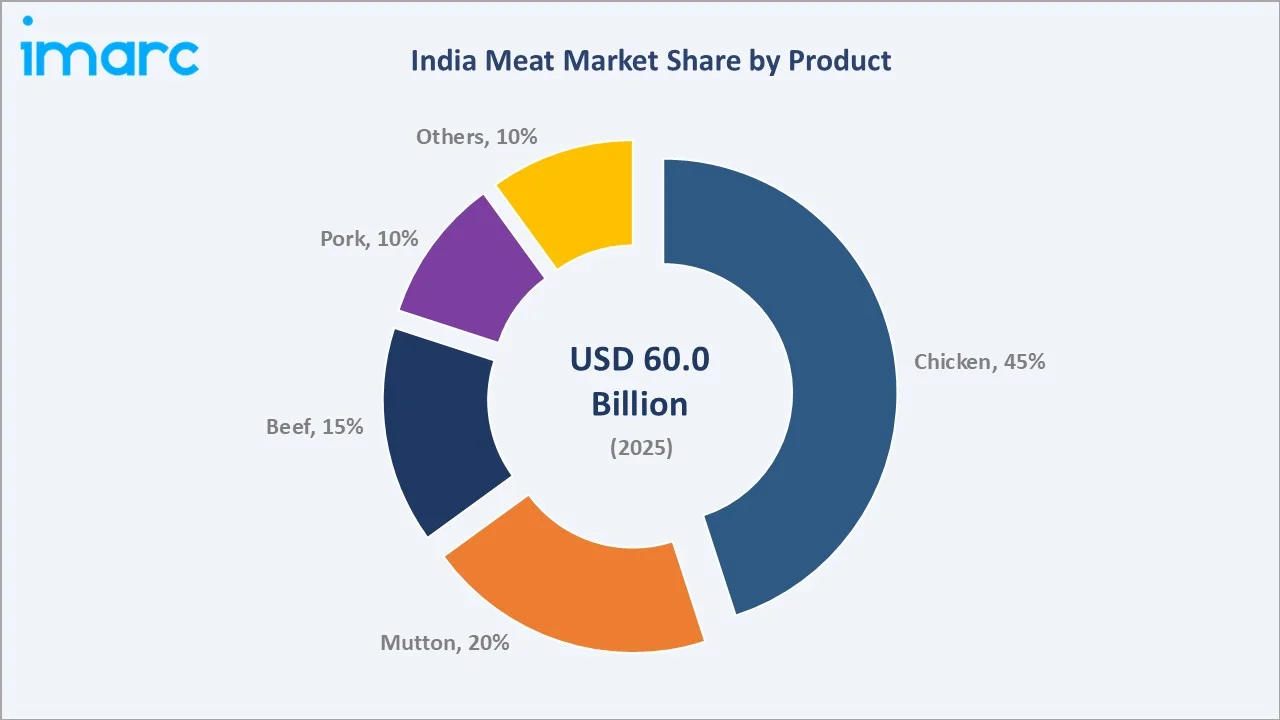

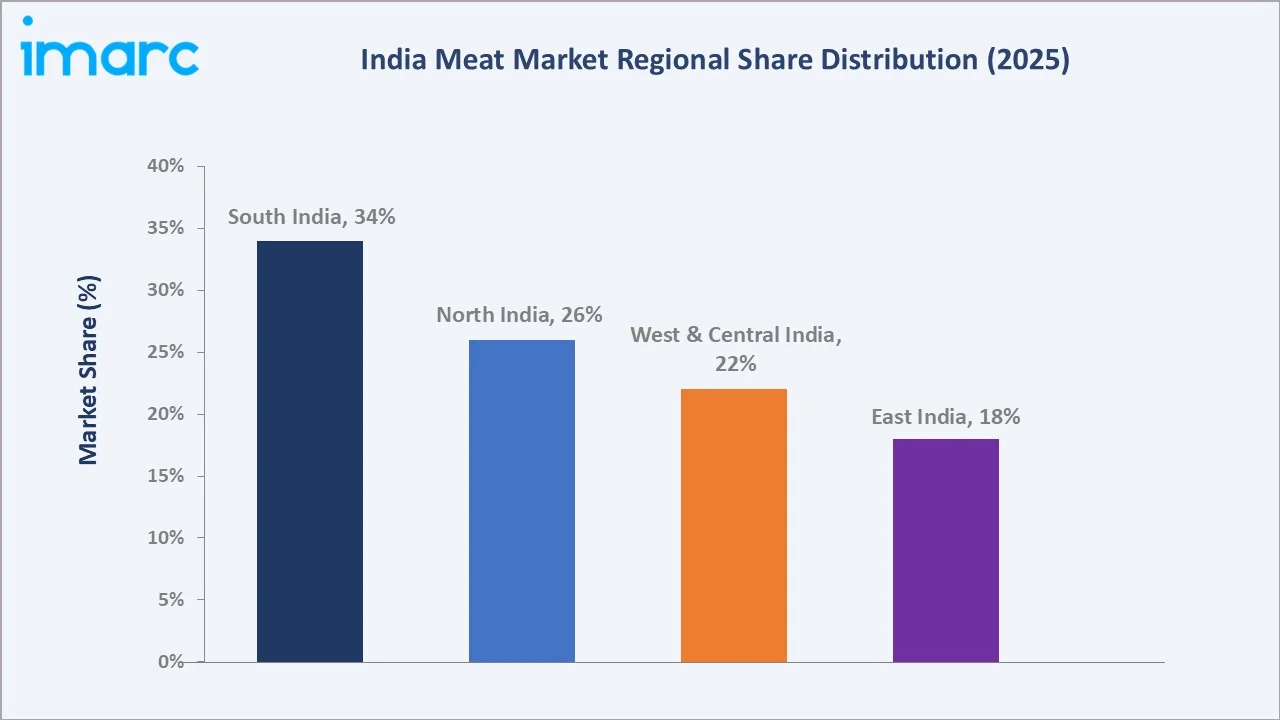

Raw leads the type segment at 72%, chicken dominates the product segment at 45%, and South India commands 34% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 60.0 Billion |

|

Forecast Market Size (2034) |

USD 124.2 Billion |

|

CAGR (2026-2034) |

8.42% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South India (34%, 2025) |

|

Fastest Growing Region |

East India (18%, 2025) |

|

Leading Type |

Raw (72%, 2025) |

|

Leading Product |

Chicken (45%, 2025) |

The India meat market expanded from USD 40.1 Billion in 2020 to USD 60.0 Billion in 2025, driven by rising household protein consumption, expanding organized retail, and government livestock development programs. Anchored at USD 89.9 Billion in 2030, the forecast to USD 124.2 Billion by 2034 is supported by urbanization-led dietary shifts and processed meat adoption.

To get more information on this market, Request Sample

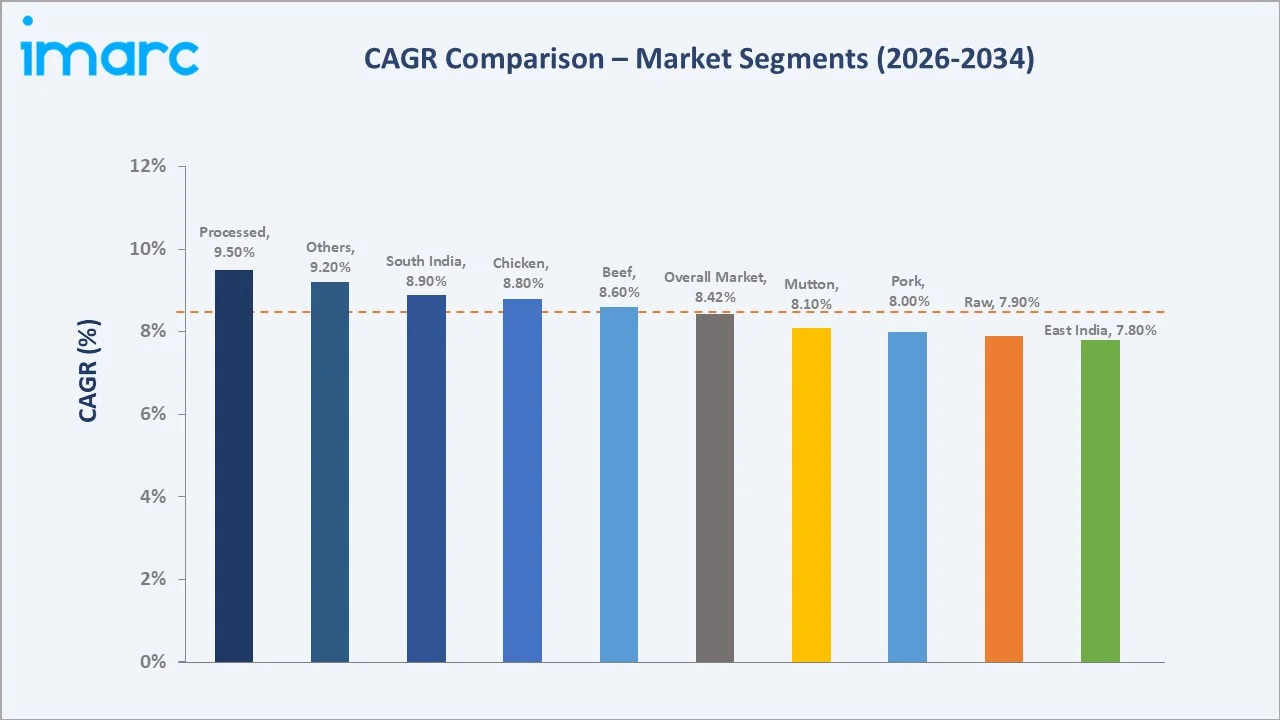

CAGR trajectories across type and product sub-segments show processed and chicken expanding faster than the overall 8.42% market CAGR, driven by convenience food adoption and affordability advantages.

Executive Summary

The India meat market is on a strong growth path from USD 40.1 Billion in 2020 to USD 124.2 Billion by 2034. Meat consumption in India is shifting from a traditional wet-market model toward organized retail and digital delivery. Falling cold-storage costs and rising health awareness are encouraging households to consume more protein-rich diets. Government livestock missions and food-safety regulations are further supporting the organized meat supply chain.

Raw dominates the type segment at 72% in 2025, supported by strong consumer preference for fresh cuts purchased from local markets and expanding retail ecosystem. In February 2025, Licious, the Indian online meat retailer backed by Temasek, announced plans to go public in 2026, targeting a valuation of USD 2 Billion. Chicken leads the product segment at 45%, fueled by affordability and cultural acceptance across most regions. South India commands 34% regional share, led by high per-capita poultry consumption in Tamil Nadu, Andhra Pradesh, and Telangana.

Key Market Insights

|

Insight |

Data |

|

Leading Type |

Raw - 72% share (2025) |

|

Second Type |

Processed - 28% share (2025) |

|

Leading Product |

Chicken - 45% share (2025) |

|

Second Product |

Mutton - 20% share (2025) |

|

Leading Region |

South India - 34% share (2025) |

|

Fastest Growing Region |

East India - 18% share (2025) |

|

Top Companies |

Godrej Industries Group, IB Group, Allanasons Pvt Ltd, ITC, Delightful Gourmet Pvt Ltd. |

Key Analytical Observations Expanding on the Data Above:

- Raw dominance at 72% is supported by strong consumer preference for freshly cut meat purchased through traditional butcher shops and wet markets. Daily consumption habits and trust in fresh sourcing continue to favor unprocessed meat formats across urban and rural areas.

- Processed at 28% is expanding steadily with the growth of modern retail, frozen food availability, and rising demand for convenience-oriented protein options among working consumers and younger households. As per IMARC Group, the Indian frozen foods market size was valued at INR 216.59 Billion in 2025.

- Chicken leadership at 45% is driven by affordability, widespread cultural acceptance, and shorter production cycles that ensure stable supply availability across the country. Its versatility across cuisines further strengthens household demand.

- Mutton at 20% maintains a significant position due to strong consumption during festivals, family gatherings, and regional culinary preferences, particularly across markets in North and South India, where premium meat demand remains resilient.

- South India share at 34% leads the regional landscape owing to high per-capita poultry consumption, well-developed poultry farming infrastructure, and strong integration of organized meat retail networks across states, such as Tamil Nadu, Andhra Pradesh, and Telangana.

India Meat Market Overview

Meat remains an important source of dietary protein in India, with consumption patterns influenced by regional cuisines, cultural preferences, and household income levels. The India meat market encompasses the production, processing, distribution, and sale of animal-derived protein products, including poultry, mutton, beef (predominantly buffalo meat), and pork. The domestic ecosystem integrates livestock farmers, feed suppliers, slaughterhouses, cold-chain operators, modern retailers, and e-commerce platforms, together enabling farm-to-fork supply across urban and rural India.

Macroeconomic factors, such as rising urbanization, a growing middle class, and increasing internet penetration, are reshaping consumption patterns. Government initiatives under the National Livestock Mission are supporting cold-chain infrastructure development and processing capacity expansion. Growing preference for hygienic packaging, traceable sourcing, and doorstep delivery services is also accelerating the transition toward organized meat retail channels.

Market Dynamics

To evaluate market opportunities, Request Sample

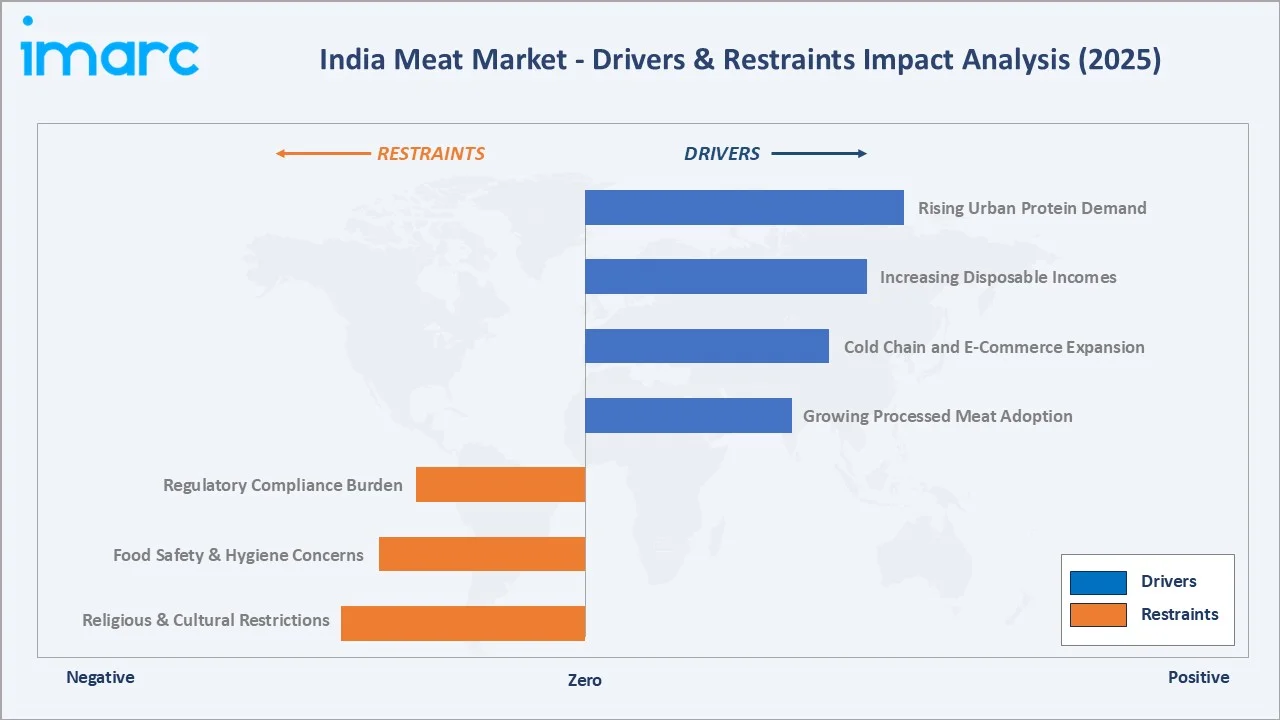

Market Drivers

- Rising Urban Protein Demand: Rapid urbanization and growing health consciousness are driving higher per-capita meat consumption among Indian households. Younger demographics and dual-income families are increasingly incorporating protein-rich diets into daily meals.

- Increasing Disposable Incomes: India's expanding middle class is willing to spend more on quality animal protein. Premium cuts, branded meat products, and hygienically packaged offerings are gaining traction in metropolitan and Tier-2 cities.

- Cold Chain and E-Commerce Expansion: The proliferation of quick-commerce meat delivery platforms is improving access. In July 2025, the Indian government allocated an additional INR 1,920 Crore under the Pradhan Mantri Kisan Sampada Yojana. Approval encompassed INR 500 Crore to assist in establishing 50 Multi Product Food Irradiation Units as part of the component scheme - Integrated Cold Chain and Value Addition Infrastructure (ICCVAI).

- Growing Processed Meat Adoption: Demand for ready-to-cook, frozen, and marinated meat products is rising steadily across urban India, supported by modern retail expansion and changing consumer lifestyles.

Market Restraints

- Religious and Cultural Restrictions: Meat consumption varies significantly across regions and communities. Periodic bans on slaughter during religious festivals and state-level regulations on specific meat types constrain market growth in certain geographies.

- Food Safety and Hygiene Concerns: Inconsistent sanitation practices across traditional slaughterhouses and wet markets continue to raise concerns regarding contamination and product quality. Consumer awareness regarding hygienic meat handling is increasing pressure on suppliers to modernize processing facilities.

- Regulatory Compliance Burden: Meat processors and slaughterhouses face increasing pressure to comply with food safety, animal welfare, and environmental regulations. Smaller unorganized operators often struggle to meet licensing, waste disposal, and hygiene requirements, limiting modernization across the sector.

Market Opportunities

- Online Meat Retail Expansion: Quick-commerce platforms are rapidly onboarding meat categories, enabling 15-30 minute delivery of fresh protein products. This channel is broadening accessibility and trust in hygienically sourced meat among urban consumers.

- Export Market Growth: India remains a leading exporter of buffalo meat globally. Rising demand from the Middle East, Southeast Asia, and Africa presents opportunities for processors to scale export-grade operations and value-added products.

- Value-Added and Processed Meat Demand: Urban consumers are increasingly adopting ready-to-cook and marinated meat products due to convenience and changing lifestyles. Expanding freezer availability and modern retail penetration are supporting wider acceptance of packaged meat formats.

Market Challenges

- Feed Cost Volatility: Fluctuations in maize and soybean meal prices directly impact poultry and livestock production costs, compressing processor margins and creating pricing instability across the domestic supply chain.

- Fragmented and Unorganized Supply Chain: A significant share of the India meat market remains unorganized, with local butchers and wet markets dominating distribution. This fragmentation creates inconsistencies in quality, hygiene, and traceability standards.

- Disease Outbreak Risks: Periodic outbreaks of avian influenza and livestock diseases disrupt supply chains and temporarily weaken consumer confidence in meat consumption. Such incidents often trigger transportation restrictions and precautionary culling measures across affected regions.

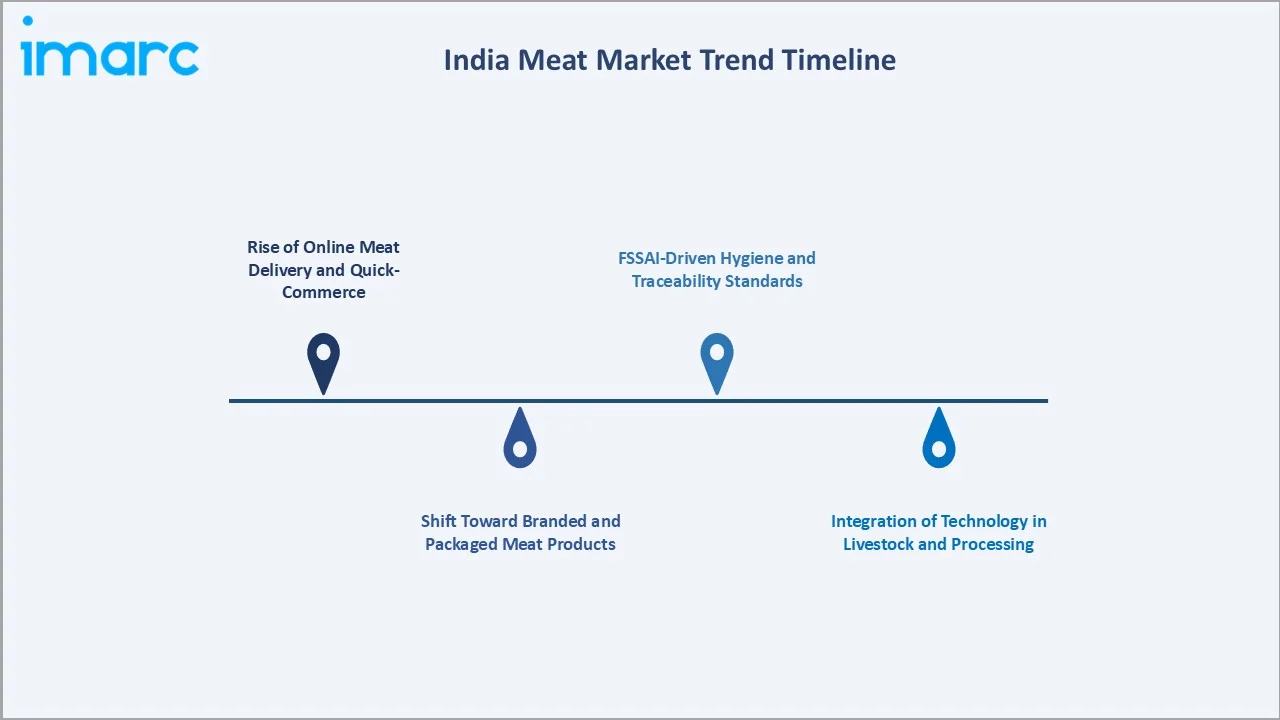

Emerging Market Trends

1. Rise of Online Meat Delivery and Quick-Commerce

Direct-to-consumer (D2C) meat platforms are transforming how urban households purchase protein. Brands have pioneered cold-chain-integrated delivery models with 15-30 minute delivery windows. This shift is driving transparency in sourcing and improving consumer trust in packaged meat.

2. Shift Toward Branded and Packaged Meat Products

Consumers are increasingly moving from loose, unpackaged meat to branded, hygienically packaged alternatives. Retail chains and FMCG companies are expanding ready-to-cook and marinated product lines to capture growing demand for convenience.

3. FSSAI-Driven Hygiene and Traceability Standards

Regulatory tightening by the Food Safety and Standards Authority of India is accelerating the formalization of meat processing. Mandatory compliance requirements are creating a competitive advantage for organized players with modern processing infrastructure.

4. Integration of Technology in Livestock and Processing

Internet of Things (IoT)-based livestock monitoring, automated processing lines, and blockchain-enabled traceability are being adopted by leading meat processors. These technologies are improving yield, reducing waste, and enhancing product quality across the value chain. As per DAHD, India achieved a historic milestone of 10.25 Million Tons of meat production in 2023-24, positioning India as the fourth-largest meat producer globally.

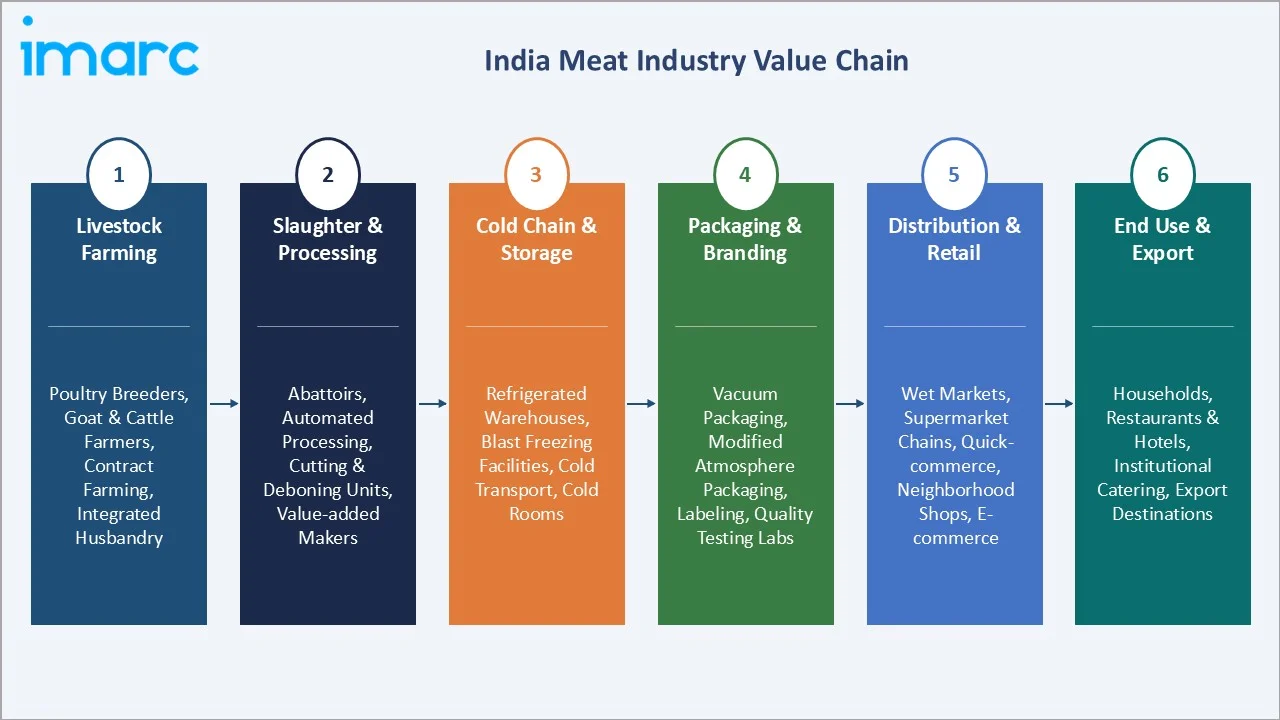

Industry Value Chain Analysis

The India meat market value chain spans six stages from livestock farming through end-consumer delivery. Slaughter and processing capture the highest value-add, while distribution and retail networks generate downstream competitive advantages in this perishable product category.

|

Stage |

Key Players / Examples |

|

Livestock Farming |

Poultry breeders, goat and cattle farmers, contract farming enterprises, and integrated animal husbandry operations |

|

Slaughter & Processing |

Abattoirs, automated processing facilities, meat cutting and deboning units, and value-added product manufacturers |

|

Cold Chain & Storage |

Refrigerated warehouses, blast freezing facilities, temperature-controlled transport fleet operators, and cold room providers |

|

Packaging & Branding |

Vacuum packaging, modified atmosphere packaging providers, labeling and branding agencies, and quality testing laboratories |

|

Distribution & Retail |

Wet markets, supermarket chains, quick-commerce platforms, neighborhood meat shops, and e-commerce delivery networks |

|

End Use & Export |

Households, restaurants and hotels, institutional catering, and international export destinations |

Players with vertically integrated operations spanning breeding, feed production, processing, and branded retail tend to achieve stronger cost efficiency and supply reliability, while standalone processors remain more exposed to fragmented sourcing and raw material volatility.

Technology Landscape in the India Meat Industry

Cold Chain and Preservation Innovation

Advanced blast-freezing systems, modified atmosphere packaging, and GPS-enabled temperature-monitored logistics are becoming standard for organized processors. These technologies extend shelf life, reduce post-harvest losses, and enable safe long-distance distribution across India's diverse geography.

Automated Processing and Robotics

Automated cutting, deboning, and portioning lines are replacing manual labor in large-scale meat processing plants. Leading companies are investing in robotic processing to increase throughput, improve yield, and maintain consistent hygiene standards.

Digital Platforms and Farm-to-Fork Traceability

QR-code-based traceability, blockchain-enabled supply chain tracking, and IoT sensor integration in farms and cold rooms are improving transparency. Online meat platforms are leveraging these technologies to build consumer trust through visible sourcing and quality assurance.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Raw |

72% |

2025 |

|

Product |

Chicken |

45% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

South India |

34% |

2025 |

By Type

Raw commands a 72% majority share in 2025, driven by deep-rooted consumer preference for fresh, unprocessed cuts from wet markets and local butcher shops. This segment benefits from widespread availability through informal retail channels and the cultural tradition of purchasing freshly cut meat for daily household cooking.

To access detailed market analysis, Request Sample

Processed at 28% in 2025 is expanding rapidly through ready-to-cook, frozen, and marinated products. Urban consumers are driving this shift, seeking convenience, extended shelf life, and consistent quality from branded offerings.

By Product

Chicken dominates with 45% share in 2025, reflecting its affordability, cultural acceptability, and the strength of vertically integrated poultry operations. India's large-scale poultry companies ensure steady supply and competitive pricing, making chicken the most accessible animal protein across income segments.

Mutton holds 20% share, driven by strong demand during festive seasons and cultural preference in North India and parts of South India. Premium pricing and strong preference for freshly cut goat meat continue to support stable consumption across traditional household and foodservice channels.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South India |

34% |

High per-capita poultry consumption, strong presence of integrated processors, and deep cultural tradition of non-vegetarian diets |

|

North India |

26% |

Large population base, strong demand for mutton and poultry, expanding modern retail penetration, and rising urban meat consumption |

|

West & Central India |

22% |

Growing urbanization, increasing processed meat adoption, expanding cold-chain networks, and rising demand from the foodservice sector |

|

East India |

18% |

Expanding poultry farming, rising disposable incomes, growing awareness of protein-rich diets, and improving distribution infrastructure |

South India at 34% in 2025 leads the national market, driven by high poultry consumption across Tamil Nadu, Andhra Pradesh, Telangana, and Kerala. Strong presence of integrated poultry processors and a well-established cold-chain network further support the region's dominant position.

East India at 18% is the fastest-growing region through 2034. Expanding poultry farming capacity in West Bengal, Odisha, and Bihar, combined with rising incomes and improving retail infrastructure, is driving regional growth.

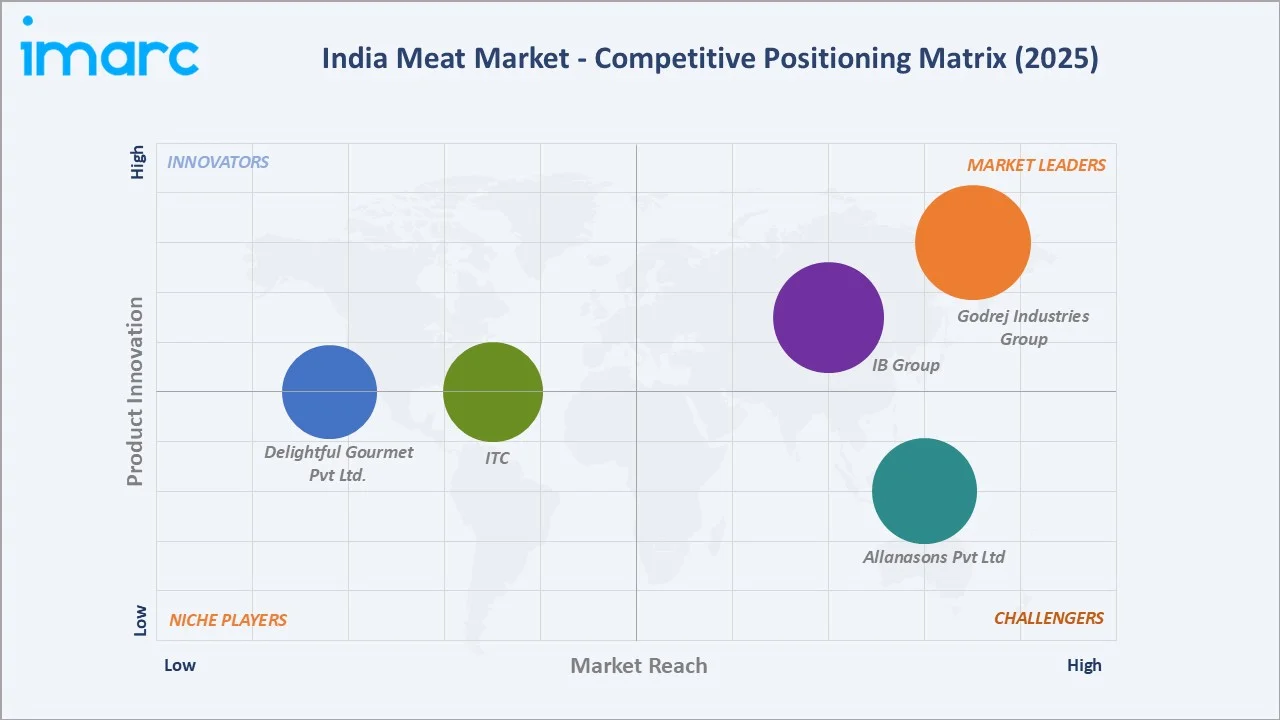

Competitive Landscape

The India meat market is moderately fragmented, with a small number of organized processors leading brand recognition and distribution while a large unorganized sector serves local and rural markets. Vertical integration, cold-chain depth, and digital retail capabilities form the key competitive moats.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Godrej Industries Group |

Yummiez, Real Good |

Leader |

Operating through Godrej Foods, Branded frozen and processed meat; strong modern retail distribution |

|

IB Group |

ABIS Laziz |

Leader |

Diversified protein portfolio; livestock feed production; multi-state farmer network |

|

Allanasons Pvt Ltd |

Sheep Carcass, Goat Carcass, and Buffalo Leg |

Challenger |

Leading meat exporter in India; buffalo meat processing; global trade network |

|

ITC |

ITC Master Chef, Meatigo, Parsuma |

Emerging |

Frozen ready-to-cook meat products; strong FMCG distribution reach |

|

Delightful Gourmet Pvt Ltd. |

Licious |

Emerging |

D2C fresh meat and seafood platform; omnichannel expansion; cold-chain-integrated quick delivery |

Key players include Godrej Industries Group, IB Group, Allanasons Pvt Ltd, ITC, and Delightful Gourmet Pvt Ltd., among others.

Key Company Profiles

IB Group

IB Group is India's leading protein-centric agri-business conglomerate, headquartered in Rajnandgaon, Chhattisgarh. The group has evolved into a diversified business spanning poultry, livestock feed, edible oil, FMCG, dairy, and pet food, with a robust presence across several states.

- Product Portfolio: ABIS Laziz branded fresh chilled chicken for retail; livestock feed for poultry, fish feed, and shrimp feed.

- Recent Developments: The company has been strengthening its meat processing and poultry distribution network to support growing demand for hygienically processed protein products. It is also expanding branded fresh chicken offerings and cold-chain capabilities across key regional markets.

- Strategic Focus: Vertically integrated protein operations across several states; backward and forward integration from breeding and feed to processed food and retail.

Allanasons Pvt Ltd

Allanasons Pvt Ltd is one of the oldest and largest food processing and meat export companies in India. Established in 1865 and headquartered in Mumbai, the company is the undisputed leader in India's buffalo meat export sector. The company operates integrated processing facilities and exports frozen meat products to multiple international markets across the Middle East, Southeast Asia, and Africa.

- Product Portfolio: Frozen boneless buffalo meat, including sheep carcass, goat carcass, and buffalo leg; chilled vacuum-packed buffalo meat, frozen lamb carcasses, and processed meat products for export.

- Strategic Focus: Dominant position in buffalo meat export with global distribution across multiple countries.

ITC

ITC is one of India's largest FMCG conglomerates with a growing presence in the frozen and processed meat segment through its ITC Master Chef brand. The company leverages its deep distribution infrastructure, institutional relationships, and culinary expertise to deliver quality frozen meat products.

- Product Portfolio: ITC Master Chef branded frozen ready-to-cook products; Meatigo, Parsuma; non-vegetarian frozen food offerings across retail and foodservice channels.

- Recent Developments: In October 2025, ITC Master Chef expanded its frozen foods portfolio with the launch of Chicken Malai Seekh Kebab and Piri Piri French Fries. These kebabs could be made in just a few minutes, whether using the microwave, oven, or tawa, delivering restaurant-quality kebabs right at home.

- Strategic Focus: Leveraging ITC's extensive FMCG distribution reach; expanding frozen meat product range; targeting modern retail, quick-commerce, and institutional foodservice channels.

Market Concentration Analysis

The India meat market is moderately concentrated in the organized segment, with the top five companies (Godrej Industries Group, IB Group, Allanasons Pvt Ltd, ITC, and Delightful Gourmet Pvt Ltd.) estimated to hold approximately 20-25% of the organized market revenue share in 2025.

Barriers to entry in the organized segment include FSSAI compliance, cold-chain investment requirements, multi-year farmer-relationship building, and the brand development needed to gain consumer trust. Consolidation is accelerating through acquisitions, vertical integration, and digital retail expansion.

Scale advantages in farming, processing, distribution, and branded retail are reinforcing the competitive position of established players. Increasing consumer preference for hygienically processed meat is expected to shift market share from unorganized to organized channels over the forecast period.

Investment & Growth Opportunities

Fastest-Growing Segments

Processed at 28% is expanding faster than the overall 8.42% market CAGR through 2034, driven by urbanization, convenience demand, and rising modern retail penetration. Chicken at 45% leads product growth as integrated poultry companies scale operations and retail distribution.

Emerging Markets

East India at 18% is the fastest-growing region, with West Bengal, Odisha, and Bihar leading expansion. Tier-2 and Tier-3 cities across India represent the largest untapped opportunities as improving cold-chain infrastructure and rising incomes unlock mass-market organized meat adoption.

Venture & Investment Trends

Venture capital is concentrated in online meat delivery platforms, cold-chain logistics startups, and branded processed food companies. Investment is also expanding into farm automation, traceability technology, and sustainable livestock practices that address growing consumer expectations around food safety and quality.

Future Market Outlook (2026-2034)

The India meat market is forecast to expand from USD 60.0 Billion in 2025 to USD 124.2 Billion by 2034 at a CAGR of 8.42%, adding roughly USD 64.2 Billion in incremental market value over the forecast period.

Four forces will shape the market through 2034: cold-chain infrastructure expansion; digital retail penetration into Tier-2 and Tier-3 cities; regulatory-driven formalization of the unorganized sector; and growing consumer preference for branded, processed meat products.

By 2034, organized retail is expected to capture a significantly larger share of meat distribution. Processed meat will emerge as a mainstream product category, and vertically integrated companies with digital-first retail strategies will dominate the competitive landscape.

Research Methodology

Primary Research

Primary research included interviews with senior executives at leading meat processors, poultry farm operators, cold-chain logistics providers, online meat platform founders, and industry association representatives, validating market sizing, regional demand, segmentation splits, and competitive dynamics.

Secondary Research

Secondary sources included DAHD Basic Animal Husbandry Statistics, USDA India Livestock Reports, FSSAI regulatory publications, APEDA trade data, and annual reports, press releases, and investor presentations from listed companies.

Forecasting Models

Market forecasts used top-down and bottom-up models combining per-capita meat consumption trends, livestock production data, cold-chain penetration rates, organized retail expansion, and regional dietary pattern analysis. Scenario analysis addressed feed-cost volatility and regulatory impact variation.

India Meat Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Raw, Processed |

| Products Covered | Chicken, Beef, Pork, Mutton, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Departmental Stores, Specialty Stores, Online Stores, Others |

| Regions Covered | South India, North India, West & Central India, East India |

| Companies Covered | Godrej Industries Group, IB Group, Allanasons Pvt Ltd, ITC, Delightful Gourmet Pvt Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India meat market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the India meat market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India meat industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Meat Market Report

The India meat market was valued at USD 60.0 Billion in 2025, driven by rising protein demand, urbanization, and cold-chain expansion.

The market is projected to grow at 8.42% CAGR from 2026 to 2034, reaching USD 124.2 Billion by 2034.

Raw leads at 72% in 2025, driven by consumer preference for fresh cuts. Traditional wet markets and neighborhood butcher shops continue to dominate purchasing behavior, particularly in tier-2 and rural regions where freshly slaughtered meat is strongly preferred.

Chicken dominates at 45% in 2025, supported by affordability, cultural acceptance, and strong vertically integrated poultry supply chains.

South India commands 34% in 2025, led by Tamil Nadu and Andhra Pradesh, due to high poultry consumption, established livestock infrastructure, and strong penetration of organized meat retail networks. East India at 18% is the fastest-growing region.

Leading players include Godrej Industries Group, IB Group, Allanasons Pvt Ltd, ITC, and Delightful Gourmet Pvt Ltd.

Rising urbanization, convenience-seeking lifestyles, modern retail expansion, and growing consumer trust in branded, hygienically packaged meat products.

Online meat platforms are driving transparency, hygiene standards, and accessibility in urban and semi-urban markets. Faster doorstep delivery and digital payment convenience are further strengthening consumer adoption.

IoT-based farm monitoring, automated processing, blockchain traceability, and quick-commerce delivery are modernizing the entire value chain.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)