India Medical Equipment Market Size, Share, Trends and Forecast by Product Type, Application, End User, and Region, 2026-2034

India Medical Equipment Market Summary:

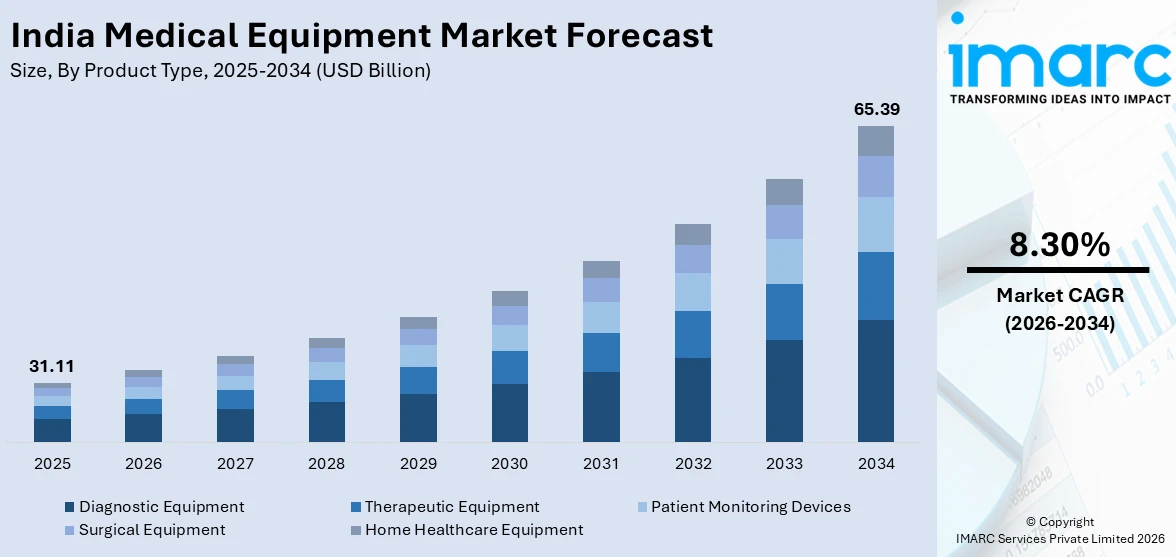

The India medical equipment market size was valued at USD 31.11 Billion in 2025 and is projected to reach USD 65.39 Billion by 2034, growing at a compound annual growth rate of 8.30% from 2026-2034.

The India medical equipment market is experiencing growth driven by expanding healthcare infrastructure, rising chronic disease prevalence, and strong government manufacturing initiatives. The convergence of demographic shifts, technological innovation, and heightened health awareness is reshaping the landscape across urban and rural settings. The growing investments in hospital networks and diagnostic capabilities are creating substantial opportunities for market participants throughout the value chain.

Key Takeaways and Insights:

- By Product Type: Diagnostic equipment represents the largest segment with a market share of 42.6% in 2025, driven by the growing demand for early disease detection and widespread hospital investments in advanced imaging and laboratory systems.

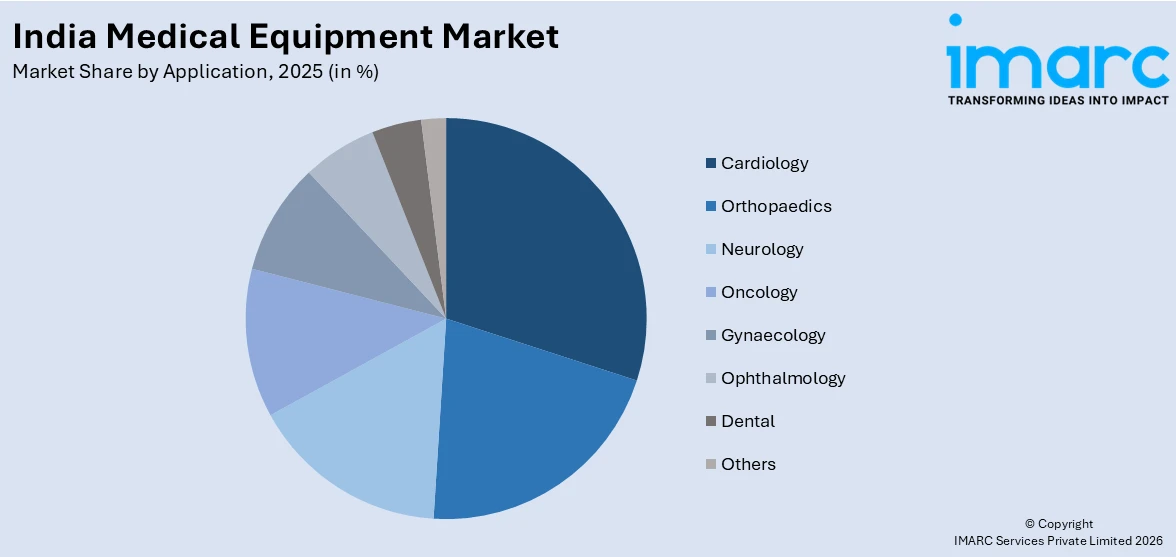

- By Application: Cardiology dominates the market with a share of 26.3% in 2025, reflecting India's growing cardiovascular disease burden, expanded cardiac care facilities, and rising adoption of interventional and monitoring devices.

- By End User: Hospitals lead the market with a share of 48.2% in 2025, driven by high patient volumes, substantial capital procurement budgets, and comprehensive requirements spanning diagnostic, therapeutic, and surgical equipment categories.

- By Region: South India represents the largest segment with a market share of 34.5% in 2025, supported by advanced healthcare clusters in Chennai and Bengaluru, strong medical tourism activity, and mature diagnostic infrastructure.

- Key Players: The India medical equipment market features intense competition among multinational corporations and domestic manufacturers, with players focused on innovation, product localization, and strategic partnerships to expand their market footprint.

To get more information on this market Request Sample

The Indian medical devices market is witnessing growth, fueled by rising healthcare demands, advancements in technology, and encouraging government policies. Factors like the increasing incidence of chronic illnesses, a growing elderly population, and advancements in healthcare systems are driving significant demand for sophisticated diagnostic, imaging, and treatment devices. Moreover, the increasing health consciousness and expanded insurance options are facilitating better access to modern medical technologies in both urban and rural settings. Government assistance is crucial in enhancing the local ecosystem. For example, in 2025, the Indian Council of Medical Research (ICMR) called upon start-ups, research organizations, and NGOs to participate in test-batch production of medical devices and diagnostics, which encompassed software as a medical device. This initiative enabled creators to enhance prototypes, guarantee adherence to regulatory requirements, and optimize production, thus encouraging innovation and advancing independence in healthcare technology.

India Medical Equipment Market Trends:

Collaborative Innovation Accelerating Medical Technology

Collaborative research and development (R&D) between domestic and international firms is a key factor accelerating the creation of advanced medical devices. These partnerships leverage complementary expertise to reduce development cycles and ensure regulatory compliance. A vital example is Tata Elxsi’s 2025 launch of the Bayer Development Centre in Radiology in Pune. The center focuses on molecular imaging, combining Tata Elxsi’s engineering expertise with Bayer’s domain knowledge to co-develop cutting-edge radiology devices. This collaboration facilitated faster design, development, and validation, exemplifying how joint innovation drives technological advancement in India’s medical device market and positions the country as a hub for globally competitive healthcare solutions.

Rise of At-Home Diagnostics

The rise of at-home diagnostic services reflects a growing trend of patient-centric healthcare, where convenience, accessibility, and timely results are prioritized. These services reduce hospital visits, enable early detection, and integrate seamlessly with digital health platforms. For example, in 2025, Amazon India launched Amazon Diagnostics in partnership with Orange Health Labs, offering at-home sample collection in six cities with results delivered digitally within six hours. Users can access over 800 diagnostic tests through the Amazon app, complemented by teleconsultation and pharmacy services. This evidences how home-based diagnostic solutions are expanding healthcare access, streamlining end-to-end patient experiences, and driving the adoption of digital health solutions in India.

Domestic Manufacturing Driving Self-Reliance

Expanding local manufacturing capabilities is a critical factor influencing the India medical equipment sector by promoting self-reliance, reducing import dependence, and strengthening healthcare supply chains. Industrial parks and government support encourage domestic production of essential medical devices. For instance, Krish Biomedicals inaugurated its first manufacturing facility in 2025 at the YEIDA Medical Device Park, Uttar Pradesh. The plant produced ultra-low temperature freezers, centrifuges, and vaccine storage equipment, benefiting from Make in India incentives and shared infrastructure. This example illustrates how domestic manufacturing initiatives accelerate innovation, enhance availability of critical healthcare devices, and contribute to India’s broader goal of becoming self-sufficient in the medical technology industry.

Market Outlook 2026-2034:

The India medical equipment market is projected to experience strong growth in the coming years, driven by rising healthcare demand, increasing investments, and rapid technological advancements. Expanding healthcare infrastructure, supportive government initiatives, and the growing awareness are accelerating adoption. The market generated a revenue of USD 31.11 Billion in 2025 and is projected to reach a revenue of USD 65.39 Billion by 2034, growing at a compound annual growth rate of 8.30% from 2026-2034. Improved access to financing and innovation in medical technologies are further expected to enhance efficiency, strengthen service delivery, and boost overall market growth nationwide.

India Medical Equipment Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product Type |

Diagnostic Equipment |

42.6% |

|

Application |

Cardiology |

26.3% |

|

End User |

Hospitals |

48.2% |

|

Region |

South India |

34.5% |

Product Type Insights:

- Diagnostic Equipment

- Therapeutic Equipment

- Patient Monitoring Devices

- Surgical Equipment

- Home Healthcare Equipment

Diagnostic equipment dominates with a market share of 42.6% of the total India medical equipment market in 2025.

Diagnostic equipment represents the largest segment driven by the rising demand for early and accurate disease detection across the healthcare ecosystem. Increasing prevalence of chronic and lifestyle-related conditions is significantly driving the need for advanced diagnostic solutions. Hospitals and diagnostic centers are investing in modern imaging and testing technologies to improve clinical outcomes and efficiency. Government initiatives promoting preventive healthcare and screening programs are further supporting demand, while the growing awareness among patients about timely diagnosis is accelerating the adoption of diagnostic equipment across both urban and semi-urban regions nationwide.

The dominance of diagnostic equipment is also supported by continuous technological advancements that improve speed, accuracy, and usability in clinical procedures. Integration of digital technologies, automation, and data-driven tools enhances workflow efficiency and supports faster clinical decision-making. In 2025, Hyderabad’s Niloufer Hospital introduced Amruth Swasth Bharath, India’s first AI-powered, non-invasive diagnostic blood test developed by Quick Vitals. Utilizing Remote Photoplethysmography (PPG), it delivered key health metrics, including blood pressure, oxygen saturation, hemoglobin, and cholesterol, in under a minute without needles. This innovation enabled safer, faster, and more accessible diagnostics, particularly benefiting children, pregnant women, and patients in remote regions.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Cardiology

- Orthopaedics

- Neurology

- Oncology

- Gynaecology

- Ophthalmology

- Dental

- Others

Cardiology leads with a market share of 26.3% of the total India medical equipment market in 2025.

Cardiology holds the biggest market share because of the rising burden of cardiovascular conditions and the growing need for timely diagnosis and intervention. Increasing awareness about heart health and preventive care is encouraging early screening and regular monitoring. Healthcare providers are expanding cardiac care capabilities by investing in advanced equipment to enhance treatment outcomes and patient safety. The growing number of specialized cardiac centers and improvements in healthcare access are further driving the demand. These factors collectively support the widespread adoption of cardiology equipment across diverse healthcare settings nationwide.

The cardiology segment’s leadership is reinforced by rapid technological advancements that enhance accuracy, efficiency, and clinical decision-making in cardiac care. Integration of digital platforms and data analytics enables better patient monitoring and streamlined workflows. In 2025, Terumo India launched the FineCross™ M3 Coronary Micro-Guide Catheter, improving guidewire support, navigability, and crossing ability in complex PCI procedures. Designed to enhance safety and predictability for treating coronary artery disease, India’s leading cause of death, this innovation underscores ongoing investment in infrastructure and quality care, driving the continued dominance of cardiology equipment in India’s evolving medical technology market.

End User Insights:

- Hospitals

- Ambulatory Surgical Centers

- Clinics

- Home Healthcare Settings

- Diagnostic Laboratories

Hospitals exhibit a clear dominance with a 48.2% share of the total India medical equipment market in 2025.

Hospitals are the leading segment in the market attributed to the rising demand for advanced healthcare services and increasing patient volumes. Expansion of multi-specialty and tertiary care facilities, along with modernization of existing hospitals, drives the adoption of comprehensive medical equipment. Investment in advanced infrastructure enables hospitals to provide high-quality care, improve clinical outcomes, and streamline operations. Government initiatives promoting healthcare accessibility and private sector participation further accelerate the procurement of modern equipment.

The dominance of hospitals as end users is also supported by continuous technological advancements that enhance efficiency, safety, and treatment accuracy. Integration of digital platforms, automated systems, and patient monitoring solutions enables optimized workflows and improved care quality. In 2025, Hospkart Healthique Pvt Ltd launched Hospkart.com, India’s first AI-powered B2B medical marketplace, designed to streamline procurement by connecting verified manufacturers with hospitals and clinics, providing automated sourcing, transparent pricing, and real-time product availability. By reducing intermediaries, the platform ensured faster deliveries, cost efficiency, and better access to medical equipment, further strengthening hospitals’ adoption of modern healthcare technologies.

Regional Insights:

- North India

- South India

- East India

- West India

South India dominates with a market share of 34.5% of the total India medical equipment market in 2025.

South India leads the market due to its sophisticated healthcare facilities and a large number of multi-specialty hospitals and diagnostic centers. The area gains from robust private sector involvement, well-established urban healthcare systems, and growing patient knowledge regarding advanced medical therapies. Increasing investments in hospital expansion, advanced diagnostic centers, and preventive health programs promote the use of advanced medical devices. Moreover, favorable state policies, increased healthcare expenditure, and improved access to tertiary care services further bolster South India's role as a leading regional market for medical equipment across the country.

The area is also supported by strong infrastructure, technology usage, and a proficient workforce, drawing investment and encouraging innovation in healthcare production. Hospitals and diagnostic facilities are progressively utilizing advanced imaging technologies, digital health innovations, and automated patient monitoring systems, enhancing clinical results and operational effectiveness. In 2025, Andhra Pradesh established the 500-acre Medical Devices Manufacturing Zone 2.0 in Visakhapatnam to enhance the production of diagnostic tools, imaging technologies, and critical medical equipment, attracting both domestic and international firms, thereby fortifying the region's leadership and competitive edge in India's medical equipment industry.

Market Dynamics:

Growth Drivers:

Why is the India Medical Equipment Market Growing?

Mobile Services Enhancing Diagnostic Accuracy

The rise of mobile healthcare and device services is progressively enhancing access and quality in India's medical equipment sector, especially in remote or resource-constrained regions. Mobile units decrease the necessity for costly travel, minimize downtime, and guarantee that medical equipment is regularly calibrated and dependable, directly enhancing patient care. A prime illustration is IIT Madras' 2024 initiation of India's inaugural mobile medical devices calibration facility. This cutting-edge device was dispatched to hospitals across the country, including remote areas, facilitating accurate calibration of diagnostic tools. By minimizing expenses and travel duration, it guaranteed dependable test outcomes, improved treatment precision, and supported SDG-3 for health and wellness, showcasing how mobile technologies are revolutionizing diagnostic benchmarks nationwide.

Smart Devices and Digital Workflow Integration

The adoption of smart medical devices integrated with digital workflows is shaping modern healthcare delivery, enabling real-time monitoring, better data management, and improved operational efficiency in hospitals. These systems support critical-care environments by providing timely insights that enhance patient outcomes. For instance, BPL Medical Technologies, at ISACON 2025, launched ExcelSign E12/E17 patient monitors, Relife 1000 defibrillators, and OT charting software. This combination of reliable hardware and intelligent software allowed ICUs, operating theatres, and emergency units to track patient vitals continuously, manage records digitally, and optimize workflows. The initiative evidences a market shift toward connected, intelligent devices that enhance hospital efficiency while delivering safer and faster patient care.

Digital Regulatory Platforms Simplifying Compliance

Digital regulatory platforms are transforming medical device approvals by streamlining processes, increasing transparency, and aligning with international standards. These tools help manufacturers classify devices, ensure compliance, and reduce time-to-market, fostering innovation in India’s medical equipment sector. A concrete example is the CDSCO’s 2025 online risk classification module for medical devices (excluding IVDs). This system allowed manufacturers to categorize devices from low to high risk under the Medical Device Rules, 2017, simplifying licensing procedures and ensuring regulatory adherence. By digitizing the classification process, it provides a faster, more predictable approval pathway, demonstrating the impact of digital governance on enhancing efficiency and reliability in India’s medical device industry.

Market Restraints:

What Challenges the India Medical Equipment Market is Facing?

High Capital Costs Limiting Equipment Access for Smaller Healthcare Providers

The substantial upfront acquisition cost of advanced medical equipment represents a significant barrier for smaller hospitals, clinics, and diagnostic centers across India’s healthcare ecosystem. Facilities in Tier-II and Tier-III cities often face tight budgets that hinder procurement of high-end imaging systems and advanced diagnostic platforms, while weak reimbursement structures and limited financing options further constrain adoption nationwide growth overall significantly.

Heavy Import Dependence and Supply Chain Vulnerabilities

Despite progress in domestic manufacturing initiatives, India’s medical equipment market still depends heavily on imports of advanced diagnostic and therapeutic technologies. This reliance exposes the sector to geopolitical risks, currency volatility, and global supply chain disruptions, raising costs and delaying procurement. Shortages of key components like semiconductors, sensors, and specialized materials further strain availability and challenge healthcare budgeting nationwide.

Shortage of Skilled Healthcare Professionals Limiting Equipment Utilization

The effective utilization of advanced medical equipment is constrained by a persistent shortage of trained medical professionals, particularly in rural and Tier-III markets across the country. This workforce gap relative to global benchmarks results in underutilization of sophisticated technologies and infrastructure, limiting operational efficiency, reducing returns on investment, and ultimately constraining the overall growth potential of the healthcare market nationwide.

Competitive Landscape:

The India medical equipment market is characterized by a moderately concentrated competitive landscape, featuring multinational healthcare corporations alongside a growing cohort of domestic manufacturers gaining prominence through government-backed manufacturing incentives. Leading global players leverage established brand recognition, extensive research and development capabilities, and broad product portfolios to serve large hospital networks and specialty institutions. The competitive environment is increasingly shaped by strategic product localization, technology partnerships, and digital health integrations. Distribution network strength, after-sales service quality, and regulatory compliance capabilities are emerging as critical differentiators, particularly as market expansion extends into Tier-II and Tier-III markets where reliable service infrastructure carries significant weight in procurement decisions.

Recent Developments:

- March 2026: India is launching its first dedicated MedTech investment fund, MedArtha Capital, with a corpus of INR 1,000 Crore to boost domestic medical technology innovation and manufacturing. The fund will support growth-stage companies developing advanced healthcare devices, reducing dependence on imports. This initiative aims to scale indigenous medtech solutions, strengthen local manufacturing, and accelerate India’s healthcare technology ecosystem.

- February 2026: ECDS announced plans to set up its first medical equipment manufacturing unit in Ujjain with an initial investment of INR 780 Crore, in partnership with three South Korean firms. The facility, scheduled to start production by April 2027, will manufacture diagnostic kits for diseases like cancer, kidney disorders, and diabetes using advanced nanofiber and biomass polymer technologies. The project aims to generate around 500 jobs in its first phase and strengthen India’s domestic medical device manufacturing capabilities.

- January 2026: Prime Minister Narendra Modi e-inaugurated a 336-acre medical device park in Rajkot, designed to support India’s growing MedTech sector with end-to-end facilities from R&D to global exports. The park offers plug-and-play infrastructure, efficient logistics, and utilities to attract high-value manufacturing investments. This initiative strengthens Gujarat’s leadership in sunrise industries and enhances India’s medical device manufacturing capabilities.

India Medical Equipment Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Diagnostic Equipment, Therapeutic Equipment, Patient Monitoring Devices, Surgical Equipment, Home Healthcare Equipment |

| Applications Covered | Cardiology, Orthopaedics, Neurology, Oncology, Gynaecology, Ophthalmology, Dental, Others |

| End Users Covered | Hospitals, Ambulatory Surgical Centers, Clinics, Home Healthcare Settings, Diagnostic Laboratories |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Medical Equipment Market Report

The India medical equipment market size was valued at USD 31.11 Billion in 2025.

The India medical equipment market is expected to grow at a compound annual growth rate of 8.30% during 2026-2034 to reach USD 65.39 Billion by 2034.

Diagnostic equipment accounted for the largest revenue share of 42.6% in 2025, driven by the growing demand for early disease detection and widespread hospital investments in advanced imaging and laboratory diagnostic systems.

Key factors driving the India medical equipment market include collaborative R&D between domestic and international firms, which accelerates innovation and reduces development cycles. A notable example is Tata Elxsi’s 2025 Bayer Development Centre in Pune, co-developing advanced radiology devices with molecular imaging expertise.

Major challenges include high capital costs limiting access for smaller healthcare providers, heavy dependence on imported advanced technologies creating supply chain vulnerabilities, and a shortage of skilled healthcare professionals that limits effective utilization of sophisticated medical equipment across rural and semi-urban markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)