India Medical Plastics Market Size, Share, Trends and Forecast by Material, Application, and Region, 2026-2034

India Medical Plastics Market Summary:

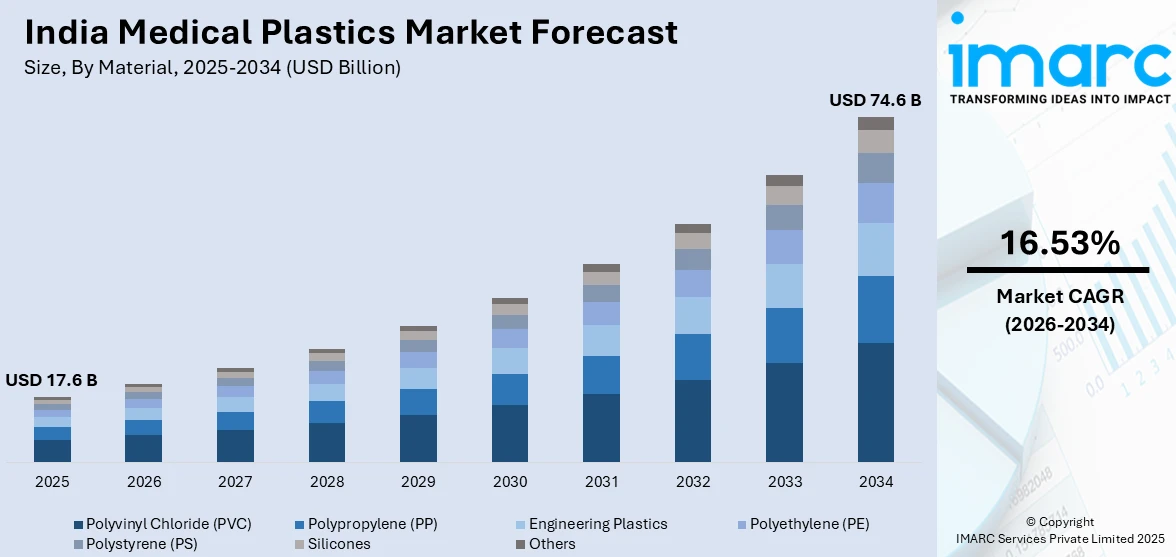

The India medical plastics market size was valued at USD 17.6 Billion in 2025 and is projected to reach USD 74.6 Billion by 2034, growing at a compound annual growth rate of 16.53% from 2026-2034.

The India medical plastics market is experiencing robust expansion as the healthcare sector undergoes rapid modernization and infrastructure development. Increasing demand for disposable medical supplies, diagnostic instruments, and drug delivery systems is accelerating polymer consumption across hospitals and clinics. Government-led initiatives to strengthen domestic manufacturing, combined with rising healthcare accessibility in urban and rural areas, are reshaping the competitive landscape and expanding the India medical plastics market share.

Key Takeaways and Insights:

- By Material: Polyvinyl chloride (PVC) dominates the market with a share of 39.5% in 2025, because of its exceptional chemical resistance, biocompatibility, and affordability, which make it essential for producing blood tubing, intravenous bags, and catheter parts for India's growing healthcare system.

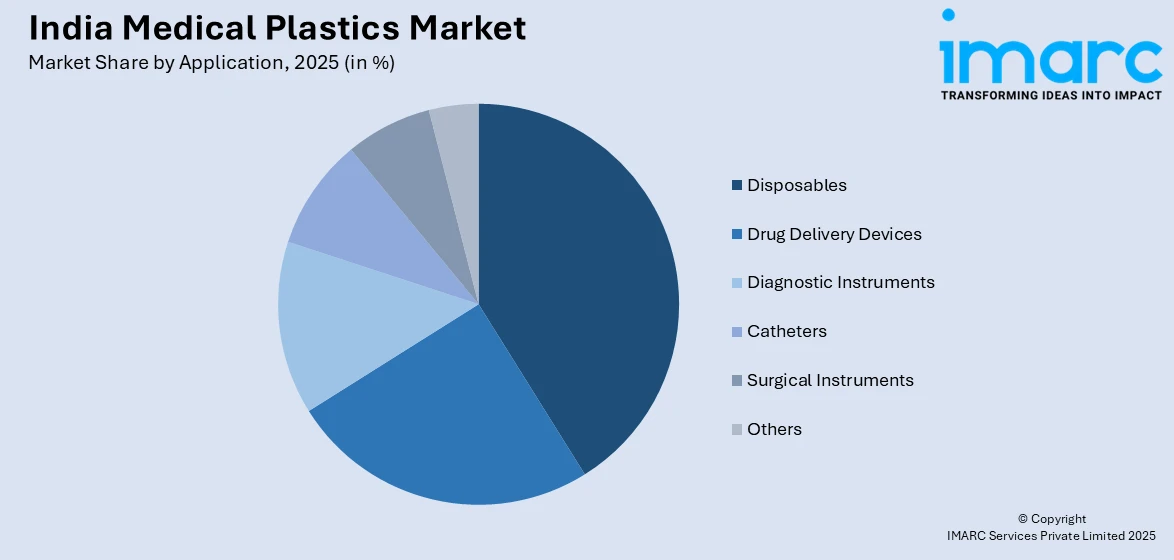

- By Application: Disposables lead the market with a share of 41.2% in 2025, driven by heightened infection control protocols, increasing surgical volumes, and the nationwide shift toward single-use medical products that ensure patient safety and reduce cross-contamination risks.

- By Region: West India is the largest region with 33.7% share in 2025, supported by the concentration of medical device manufacturing clusters in Gujarat and Maharashtra, established pharmaceutical ecosystems, and strong port-linked export infrastructure.

- Key Players: Key players drive the India medical plastics market by expanding manufacturing capacities, investing in advanced polymer processing technologies, strengthening nationwide distribution networks, and forging strategic partnerships with healthcare providers to accelerate adoption of high-performance medical-grade plastics across diverse clinical applications.

To get more information on this market Request Sample

The India medical plastics market is advancing as healthcare infrastructure scales rapidly under government-led modernization programs and rising private sector investments. Expanding hospital networks, growing outpatient care facilities, and increasing penetration of advanced diagnostic services are creating sustained demand for medical-grade polymers across diverse clinical applications. The Union Budget 2025-26 allocated Rs 99,858 Crore (approximately USD 11.48 Billion) to the healthcare sector, reflecting a strong governmental commitment to strengthening medical infrastructure and public health systems nationwide. This substantial budgetary push is directly fueling procurement of plastic-based disposable supplies, drug delivery systems, surgical instruments, and diagnostic equipment at public and private healthcare facilities. Simultaneously, the domestic manufacturing ecosystem is maturing, supported by production-linked incentive schemes that are attracting fresh investments into polymer processing and medical device fabrication. Rising awareness around infection prevention, expanding insurance coverage through programs such as Ayushman Bharat, and the proliferation of tier-two and tier-three city hospitals are broadening the addressable market. Technological innovations in biocompatible and sustainable plastics are further diversifying application possibilities across the entire healthcare value chain.

India Medical Plastics Market Trends:

Expansion of Domestic Manufacturing Under Government Initiatives

India is rapidly scaling its medical plastics manufacturing base through targeted policy interventions and infrastructure investments. The Production-Linked Incentive scheme for medical devices has catalyzed greenfield facility development nationwide. In March 2024, Union Minister Mansukh Mandaviya inaugurated 27 greenfield bulk drug park projects and 13 new manufacturing plants under the scheme. A significant number of these projects have since been commissioned with production commenced for multiple products, generating substantial cumulative eligible sales. This manufacturing push is strengthening domestic supply chains for medical-grade polymers and reducing import dependence.

Rising Adoption of Sustainable and Bio-based Medical Plastics

Environmental sustainability is gaining prominence in India's medical plastics sector as manufacturers transition toward eco-friendly polymer alternatives and circular economy practices. Healthcare facilities and device makers are increasingly prioritizing recyclable, bio-based, and reduced-carbon-footprint materials to align with global environmental standards. Berry Global's healthcare manufacturing facility in Bangalore received International Sustainability and Carbon Certificate Plus accreditation in April 2023, allowing it to produce certified sustainable packaging and plastic components while obtaining approximately 90% of its electricity from renewable solar and wind energy sources. This trend is driving India medical plastics market growth through innovation in green polymer technologies.

Growth in Single-Use Medical Products Driven by Infection Control Priorities

Heightened infection prevention awareness and regulatory mandates are accelerating the shift toward disposable plastic-based medical products across Indian healthcare settings. Hospital-acquired infections remain a critical concern, with studies indicating that affected patients experience hospital stays extending nearly 12 days beyond standard durations. This challenge is driving procurement of single-use syringes, gloves, drapes, and surgical kits fabricated from medical-grade polymers. In March 2024, Hindustan Syringes and Medical Devices launched the Dispojekt indigenous safety needle syringe, committing INR 70 Crore in first-phase investment targeting annual production capacity of 200 Million Units.

Market Outlook 2026-2034:

The India medical plastics market is positioned for sustained expansion over the forecast period, underpinned by converging factors including accelerating healthcare infrastructure development, rising chronic disease burden, and deepening government commitment to self-reliant medical device manufacturing. The proliferation of tier-two and tier-three city hospitals, expanding insurance coverage, and growing surgical volumes are generating consistent demand for medical-grade polymers. The market generated a revenue of USD 17.6 Billion in 2025 and is projected to reach a revenue of USD 74.6 Billion by 2034, growing at a compound annual growth rate of 16.53% from 2026-2034. Continued policy support through the Production-Linked Incentive scheme, establishment of dedicated medical device parks, and increasing private sector investments in polymer processing technologies will drive capacity expansion. Advancements in biocompatible materials, sustainable plastics, and precision-molded components for advanced diagnostic and therapeutic devices are expected to create new growth avenues, positioning India as a significant global hub for medical plastics manufacturing and innovation.

India Medical Plastics Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Material |

Polyvinyl Chloride (PVC) |

39.5% |

|

Application |

Disposables |

41.2% |

|

Region |

West India |

33.7% |

Material Insights:

- Polyvinyl Chloride (PVC)

- Polypropylene (PP)

- Engineering Plastics

- Polyethylene (PE)

- Polystyrene (PS)

- Silicones

- Others

Polyvinyl chloride (PVC) dominates with a market share of 39.5% of the total India medical plastics market in 2025.

Polyvinyl chloride remains the most extensively utilized polymer in India's medical plastics sector, valued for its exceptional combination of chemical resistance, biocompatibility, flexibility, and sterilization compatibility. The material is fundamental to manufacturing critical healthcare products including intravenous fluid bags, blood collection and transfusion tubing, urinary catheters, endotracheal tubes, and dialysis equipment. Its ability to be compounded with various plasticizers enables precise customization of rigidity and flexibility to match diverse clinical requirements. India's expanding hospital network is generating sustained procurement demand for PVC-based medical consumables and devices across both public and private healthcare systems.

The growing emphasis on affordable healthcare delivery in India further reinforces the prominence of polyvinyl chloride, as it offers significant cost advantages over alternative medical-grade polymers while meeting stringent regulatory quality standards. Domestic manufacturers are increasingly investing in medical-grade PVC compounding facilities to reduce dependence on imported raw materials and finished components. Government production-linked incentive programmes are accelerating domestic manufacturing of medical devices that rely on PVC as a primary input material. Additionally, advancements in phthalate-free PVC formulations are addressing safety concerns while maintaining performance characteristics, further strengthening its market position in sensitive healthcare applications.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Disposables

- Drug Delivery Devices

- Diagnostic Instruments

- Catheters

- Surgical Instruments

- Others

Disposables lead with a share of 41.2% of the total India medical plastics market in 2025.

Disposable medical products represent the largest application segment in India's medical plastics market, driven by the imperative for infection prevention and patient safety across healthcare facilities. Single-use items including syringes, examination gloves, surgical drapes, specimen collection containers, and infusion sets constitute the bulk of plastic consumption in hospitals and clinics. The enormous scale of demand is generated by immunization programmes, routine clinical procedures, and expanding outpatient care services. The nationwide adoption of safety-engineered devices following needlestick injury prevention guidelines is further accelerating demand for advanced disposable products.

The expanding scope of government healthcare programmes is reinforcing the growth trajectory of disposable medical plastics in India. Flagship public health insurance initiatives are enabling millions of additional beneficiaries to access hospital-based treatments that require substantial volumes of single-use medical supplies. Enhanced budgetary allocations toward healthcare coverage schemes are significantly broadening the insured patient base and driving institutional procurement of disposable products. This insurance-driven demand is complemented by rising private sector hospital expansion, with major healthcare chains adding new facilities across tier-two and tier-three cities where disposable product penetration is growing rapidly. Manufacturers are responding by scaling production capacities and introducing cost-optimized product lines tailored to diverse clinical settings.

Regional Insights:

- North India

- South India

- East India

- West India

West India holds the largest share with 33.7% of the total India medical plastics market in 2025.

West India commands the leading position in the medical plastics market, anchored by the concentrated presence of medical device manufacturing infrastructure in Gujarat and Maharashtra. Gujarat hosts the highest concentration of licensed medical device manufacturing sites nationwide, establishing the state as a critical hub for healthcare product fabrication. The region benefits from established pharmaceutical ecosystems, robust port-linked export logistics through major western coastal ports, and proximity to petrochemical complexes that supply essential polymer raw materials for medical-grade plastic production.

The region's dominance is further reinforced by strategic government investments in dedicated medical device manufacturing zones and industrial corridors. West India hosts a significant share of the country's designated medical device clusters, reflecting sustained policy focus on building localized manufacturing ecosystems. Maharashtra's leadership in imaging systems and surgical instrument manufacturing, combined with Gujarat's emerging specialization in diagnostic kits and consumables, creates a diversified production base that drives consistent demand for medical plastics. Strong academic institutions and research centres in key western cities provide skilled workforce availability and innovation support, further consolidating the region's competitive advantage.

Market Dynamics:

Growth Drivers:

Why is the India Medical Plastics Market Growing?

Government Healthcare Expenditure and Infrastructure Development

The Indian government's sustained increase in healthcare spending is creating a powerful demand catalyst for medical plastics across the country. Expanding hospital networks, upgrading primary health centres, and establishing new specialty care facilities require massive volumes of plastic-based medical supplies, instruments, and devices. Annual union budget allocations to the healthcare sector have grown substantially, encompassing significant provisions for the National Health Mission and flagship public health insurance programmes. A large number of sub-health centres and primary health centres have been upgraded to health and wellness centres nationwide, each requiring stocking of essential disposable supplies, diagnostic equipment, and medical devices manufactured from various plastic polymers. This infrastructure-driven demand is extending medical plastics consumption beyond metropolitan areas into semi-urban and rural healthcare settings, significantly broadening the addressable market for domestic manufacturers and importers.

Production-Linked Incentive Scheme for Medical Devices

The government's Production-Linked Incentive scheme for medical devices is catalysing domestic manufacturing of plastic-based medical products and reducing dependence on imports. The scheme carries a substantial budgetary outlay with a multi-year incentive period, directly encouraging investment in manufacturing infrastructure for medical-grade polymer components. The government has progressively scaled up budgetary allocations for the medical devices sector, enabling local production of advanced equipment including imaging systems and diagnostic devices that incorporate substantial plastic components. Dedicated medical device parks have been approved across multiple states, providing specialised infrastructure for medical plastics manufacturers. These parks are attracting investment from both domestic and international companies seeking to establish production bases for exportable medical plastic products, strengthening the country's position as an emerging hub for medical device manufacturing and polymer processing.

Rising Prevalence of Chronic Diseases and Expanding Patient Pool

India's growing chronic disease burden is generating increasing demand for medical plastic products used in diagnosis, treatment, and long-term patient management. The country faces a rising incidence of lifestyle-related conditions that require continuous use of plastic-based medical consumables, monitoring devices, and therapeutic equipment. Diabetes cases in India are projected to jump from 77 Million in 2019 to 134 Million by 2045, substantially magnifying demand for glucose monitors, insulin delivery devices, and dialysis supplies fabricated from medical-grade polymers. Cardiovascular conditions are likewise increasing, driving wider deployment of catheterization products, stent delivery systems, and interventional cardiology devices that rely heavily on precision-molded plastic components. The expanding elderly population, growing surgical volumes, and rising health awareness among middle-income demographics are collectively broadening the patient pool that consumes medical plastic products on a recurring basis, ensuring sustained market demand.

Market Restraints:

What Challenges the India Medical Plastics Market is Facing?

High Import Dependence and Supply Chain Vulnerabilities

India continues to import approximately 70 to 80% of its medical devices, creating significant supply chain vulnerabilities that impact the medical plastics sector. This heavy reliance on imported finished devices and critical polymer components exposes manufacturers and healthcare providers to currency fluctuation risks, logistics disruptions, and extended lead times. Geopolitical uncertainties and global supply chain bottlenecks can trigger shortages of essential medical plastic products, affecting healthcare delivery and raising procurement costs for hospitals and distributors across the country.

Healthcare Waste Management and Environmental Compliance Challenges

The rapid increase in disposable medical plastic consumption is creating substantial healthcare waste management challenges across India. Inadequate biomedical waste processing infrastructure, particularly in semi-urban and rural areas, raises environmental and public health concerns regarding the disposal of single-use plastic medical products. Tightening regulatory requirements around biomedical waste segregation, treatment, and disposal are increasing compliance costs for healthcare facilities and medical plastics manufacturers. These environmental pressures are compelling the industry to invest in sustainable alternatives and recycling technologies, adding to production costs.

Stringent Regulatory Compliance and Quality Certification Requirements

Medical plastics manufacturers in India face increasingly complex regulatory frameworks governing product quality, safety, and biocompatibility standards. Compliance with regulations mandated by the Central Drugs Standard Control Organisation and the Bureau of Indian Standards requires substantial investment in testing infrastructure, quality management systems, and documentation processes. The requirement for premium-grade polymer specifications that meet international standards such as ISO 13485 and USP Class VI increases production costs and creates barriers for smaller manufacturers. Prolonged regulatory approval timelines can delay market entry for new medical plastic products and technologies.

Competitive Landscape:

The India medical plastics market features a dynamic competitive landscape characterized by the presence of both established multinational corporations and emerging domestic manufacturers. Competition is intensifying as companies invest in expanding production capacities, upgrading polymer processing technologies, and developing specialized medical-grade formulations. Players are focusing on backward integration into raw material sourcing, forward integration into device assembly, and securing quality certifications to access export markets. Strategic collaborations between polymer suppliers and medical device manufacturers are fostering innovation in product design and manufacturing efficiency. The government's emphasis on domestic manufacturing through incentive schemes is encouraging new market entrants and driving competitive differentiation through cost optimization, product quality enhancement, and geographic distribution network expansion.

India Medical Plastics Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Materials Covered |

Polyvinyl Chloride (PVC), Polypropylene (PP), Engineering Plastics, Polyethylene (PE), Polystyrene (PS), Silicones, Others |

|

Applications Covered |

Disposables, Drug Delivery Devices, Diagnostic Instruments, Catheters, Surgical Instruments, Others |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Medical Plastics Market Research Report and Industry Forecast Report

The India medical plastics market size was valued at USD 17.6 Billion in 2025.

The India medical plastics market is expected to grow at a compound annual growth rate of 16.53% from 2026-2034 to reach USD 74.6 Billion by 2034.

Polyvinyl chloride (PVC), holding the largest revenue share of 39.5%, remains the dominant material in India's medical plastics market due to its biocompatibility, chemical resistance, sterilization compatibility, and cost-effectiveness for high-volume medical device manufacturing.

Key factors driving the India medical plastics market include rising government healthcare expenditure, production-linked incentive schemes for medical devices, increasing chronic disease prevalence, expanding hospital infrastructure, and growing demand for disposable medical products.

Major challenges include high import dependence on medical devices, healthcare waste management concerns, stringent regulatory compliance requirements, rising raw material costs, and limited domestic production capacity for specialized medical-grade polymers

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)