India Medical Tubing Market Size, Share, Trends and Forecast by Product, Structure, Application, End User, and Region, 2026-2034

India Medical Tubing Market Summary:

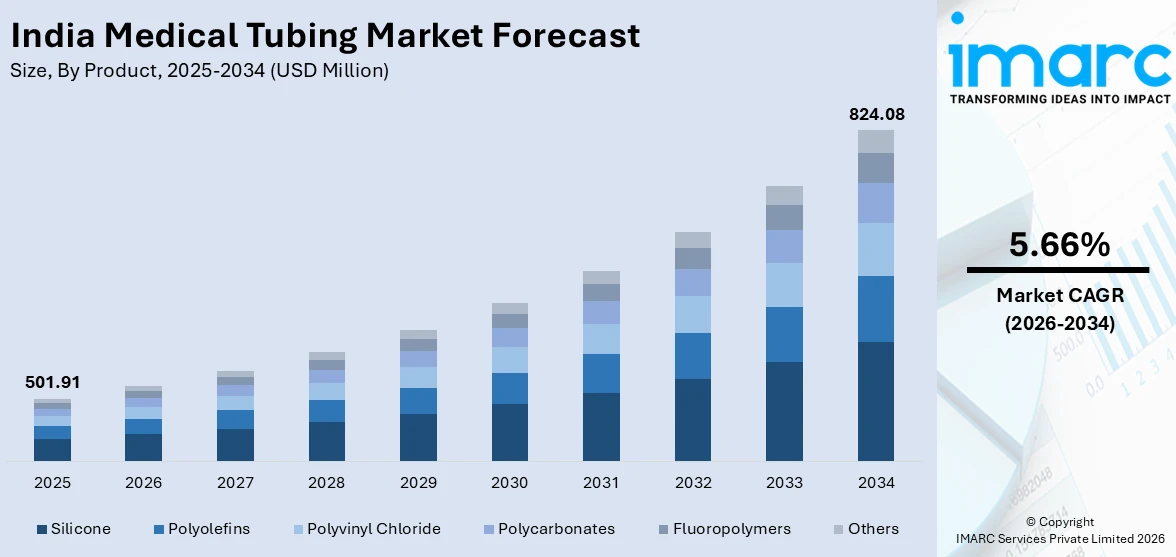

The India medical tubing market size was valued at USD 501.91 Million in 2025 and is projected to reach USD 824.08 Million by 2034, growing at a compound annual growth rate of 5.66% from 2026-2034.

The India medical tubing market is witnessing growth driven by the rapid modernization of healthcare infrastructure, rising surgical procedure volumes, and the increasing adoption of advanced medical devices across the country. The growing government investment in public health systems, expanding hospital networks into tier-two and tier-three cities, and the rising prevalence of chronic diseases requiring continuous medical intervention are collectively boosting the demand for high-quality medical tubing solutions. The convergence of domestic manufacturing initiatives, material science innovations, and rising healthcare expenditure is strengthening the India medical tubing market share.

Key Takeaways and Insights:

- By Product: Silicone leads the market with a share of 25% in 2025, driven by its superior biocompatibility, flexibility, and suitability for high-precision medical applications, including catheters, drug delivery systems, and implantable devices across India’s expanding healthcare ecosystem.

- By Structure: Single-lumen represents the largest segment with a market share of 40% in 2025, owing to its widespread utilization in standard intravenous therapy, fluid management, and drainage applications that constitute the majority of routine medical procedures in Indian hospitals.

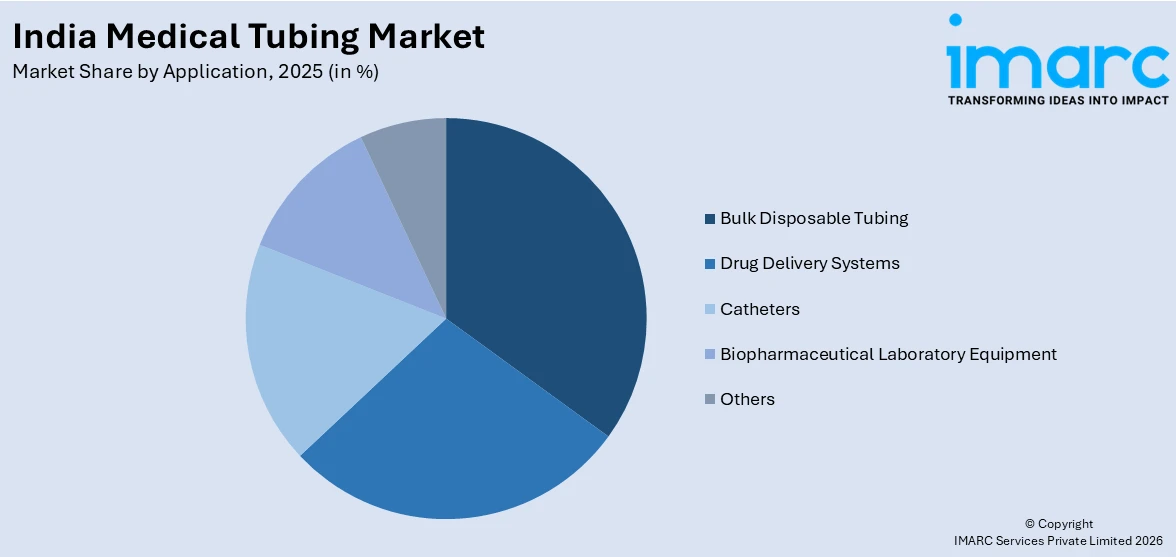

- By Application: Bulk disposable tubing dominates the market with a share of 33% in 2025, supported by rising infection control protocols, increasing adoption of single-use sterile devices, and the growing hospital admissions requiring disposable fluid transfer solutions.

- By End User: Hospitals and clinics lead the market with a share of 50% in 2025, reflecting their central role in delivering surgical, diagnostic, and therapeutic procedures that demand diverse and high-volume medical tubing solutions.

- Key Players: The India medical tubing market features a competitive mix of multinational specialty chemical companies and domestic manufacturers, with players focusing on capacity expansion, material innovation, and strategic partnerships to strengthen market positioning.

To get more information on this market Request Sample

The medical tubing market in India is advancing steadily as the country’s healthcare sector undergoes substantial transformation, supported by expanded government expenditure and rising private investment in hospitals, diagnostics, and medical device manufacturing. Growth in healthcare infrastructure across urban and semi-urban regions is increasing the demand for high-quality tubing used in fluid management, respiratory care, and minimally invasive procedures. Higher disposable incomes are also strengthening patient access to advanced treatments and elective procedures. According to the Ministry of Statistics (MoSPI), per capita Net National Income increased to INR 2,05,324 in FY2024–25 from INR 1,88,892 in FY2023–24, indicating improved purchasing power and healthcare spending capacity. In addition, the growing burden of chronic diseases, expansion of health insurance coverage, and policy initiatives promoting domestic medical device production are reinforcing demand for precision-engineered tubing solutions, thereby supporting the market growth.

India Medical Tubing Market Trends:

Rising Prevalence of Chronic Diseases

The growing incidence of chronic diseases, such as cardiovascular disorders, diabetes, respiratory ailments, and renal conditions, is significantly contributing to the demand for medical tubing products. This prevalence is supported by the data provided by the International Diabetes Federation, which stated that India’s adult population with diabetes reached 89.8 million in 2024. These conditions often require long-term treatment involving catheters, intravenous lines, dialysis equipment, and respiratory devices that depend on high-quality tubing. An aging population and changing lifestyles are further increasing the patient pool requiring continuous medical intervention. As the burden of non-communicable diseases expands, healthcare providers are utilizing more advanced and durable tubing materials designed to ensure patient safety, thereby driving sustained employment within the market.

Expansion of Healthcare Infrastructure

Rising investments in hospitals, specialty clinics, diagnostic centers, and ambulatory care facilities are generating sustained demand for medical-grade components used in fluid management, respiratory support, and minimally invasive procedures. Expanding public and private sector expenditure, particularly across tier II and tier III cities, is improving access to advanced treatment infrastructure and increasing the need for reliable, sterile, and application-specific tubing solutions. Reflecting this commitment, in 2024 the Prime Minister of India launched and inaugurated health sector projects worth over INR 12,850 Crore, including new AIIMS facilities, medical colleges, and critical care blocks, while also expanding Ayushman Bharat coverage and supporting medical device manufacturing under the PLI scheme. Such large-scale infrastructure and policy initiatives are reinforcing long-term growth prospects for the India medical tubing market.

Growing Geriatric Population and Age-Related Healthcare Needs

The steady increase in India’s elderly population is emerging as a factor influencing the medical tubing market. Aging individuals typically require more frequent medical interventions, including long-term therapies, hospitalization, and management of chronic conditions like cardiovascular and respiratory disorders. These treatments often depend on devices incorporating medical-grade tubing for fluid delivery, catheterization, dialysis, and respiratory support. According to government projections, India’s senior citizen population is expected to reach approximately 230 million by 2036, accounting for nearly 15% of the total population. This demographic shift is likely to increase demand for age-specific healthcare services and medical consumables. As the burden of age-related ailments rises, healthcare providers will require reliable and high-quality tubing solutions, thereby contributing to the market demand.

Market Outlook 2026-2034:

The India medical tubing market is positioned for notable growth throughout the forecast period, driven by sustained healthcare infrastructure development, rising chronic disease prevalence, and increasing surgical procedure volumes. The market generated a revenue of USD 501.91 Million in 2025 and is projected to reach a revenue of USD 824.08 Million by 2034, growing at a compound annual growth rate of 5.66% from 2026-2034. Strengthening domestic manufacturing capacity, government policy support for medical device localization, and expanding hospital networks are expected to drive higher revenue streams and foster a more competitive, innovation-driven medical tubing landscape across the country.

India Medical Tubing Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product |

Silicone |

25% |

|

Structure |

Single-Lumen |

40% |

|

Application |

Bulk Disposable Tubing |

33% |

|

End User |

Hospitals and Clinics |

50% |

Product Insights:

- Silicone

- Polyolefins

- Polyvinyl Chloride

- Polycarbonates

- Fluoropolymers

- Others

Silicone dominates with a market share of 25% of the total India medical tubing market in 2025.

Silicone holds the biggest market share because of its superior biocompatibility, flexibility, and thermal stability. Silicone tubing is widely utilized in applications requiring prolonged patient contact, including catheters, drainage systems, peristaltic pumps, and respiratory devices. Its non-reactive nature reduces the risk of adverse tissue reactions, making it suitable for sensitive medical procedures. Additionally, silicone maintains structural integrity across a broad temperature range and withstands repeated sterilization cycles without compromising performance. These characteristics make it a preferred material in both short-term and long-term clinical applications, contributing to sustained demand across hospitals, specialty clinics, and medical device manufacturing facilities.

The material’s dominance is further reinforced by its durability and adaptability to complex medical requirements. Silicone tubing offers high flexibility and kink resistance, enabling smooth fluid transfer even in demanding clinical settings. Its transparency also allows healthcare professionals to monitor fluid flow with ease, enhancing procedural accuracy and patient safety. Manufacturers benefit from silicone’s compatibility with advanced extrusion techniques, enabling production in varied dimensions and configurations. As healthcare providers increasingly prioritize safety, longevity, and performance in medical consumables, silicone continues to secure a leading share within the India medical tubing market across multiple therapeutic and diagnostic applications.

Structure Insights:

- Single-Lumen

- Co-Extruded

- Multi-Lumen

- Tapered or Bump Tubing

- Braided Tubing

Single-lumen leads with a market share of 40% of the total India medical tubing market in 2025.

Single-lumen dominates the market driven by its broad applicability across standard medical procedures and fluid transfer systems. This structure, consisting of a single internal channel, is widely used in intravenous lines, catheters, drainage systems, and oxygen delivery devices. Its relatively simple design allows for cost-effective manufacturing while ensuring consistent flow performance and ease of sterilization. Healthcare providers often prefer single-lumen configurations for routine applications where multiple channels are not required. High patient volumes in hospitals and clinics further contribute to sustained demand, as this tubing type is commonly utilized in day-to-day therapeutic and diagnostic interventions.

The dominance of single-lumen is also supported by its compatibility with a wide range of medical devices and treatment settings. Its straightforward construction enhances reliability, reduces the risk of blockage, and simplifies integration into existing equipment systems. Manufacturers are able to produce single-lumen tubing in various diameters and material compositions to meet diverse clinical needs. In addition, the growing demand for disposable and short-term use products aligns well with single-lumen designs, which are easier to mass-produce and distribute. As healthcare infrastructure expands and procedural volumes increase, single-lumen tubing continues to maintain a leading position in the market.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Bulk Disposable Tubing

- Drug Delivery Systems

- Catheters

- Biopharmaceutical Laboratory Equipment

- Others

Bulk disposable tubing exhibits a clear dominance with a 33% share of the total India medical tubing market in 2025.

Bulk disposable tubing represents the largest segment owing to its widespread use across routine medical procedures and high patient turnover environments. Hospitals, clinics, and diagnostic centers rely heavily on disposable tubing for intravenous therapy, fluid transfer, suction systems, and enteral feeding applications. The growing emphasis on infection prevention and patient safety has accelerated the shift toward single-use products that minimize cross-contamination risks. Bulk procurement practices adopted by large healthcare institutions further support demand, as disposable tubing is required in significant volumes for daily operations. Cost-effectiveness, ease of handling, and compliance with sterilization standards reinforce its dominant application segment.

The segment’s leadership is also driven by operational efficiency considerations within healthcare facilities. Disposable tubing eliminates the need for reprocessing and sterilization infrastructure, reducing labor requirements and turnaround time between procedures. In high-demand settings like ICUs, emergency wards, and operating theaters, ready-to-use tubing ensures uninterrupted clinical workflows. Increasing awareness about hospital-acquired infections and stricter regulatory oversight regarding hygiene standards are strengthening preference for disposable solutions. Moreover, expanding public healthcare programs and rising hospitalization rates are increasing the usage of consumable medical components.

End User Insights:

- Hospitals and Clinics

- Ambulatory Surgical Centers

- Medical Labs

- Others

Hospitals and clinics dominate with a market share of 50% of the total India medical tubing market in 2025.

Hospitals and clinics lead the market due to their central role in delivering primary, secondary, and tertiary healthcare services. These facilities handle a high volume of surgical procedures, emergency treatments, critical care interventions, and long-term therapies that require dependable medical-grade tubing. Applications, such as intravenous infusion, catheterization, dialysis, respiratory support, and surgical drainage, rely extensively on precision-engineered tubing components. The presence of specialized departments, including cardiology, oncology, and intensive care units, further increases usage. Continuous patient inflow and expanding bed capacity across public and private hospitals sustain consistent procurement of sterile and application-specific tubing products.

The dominance of hospitals and clinics is also supported by ongoing infrastructure expansion and technological upgrades across India’s healthcare network. Investments in advanced diagnostic equipment, minimally invasive surgical systems, and life-support devices are increasing the need for high-performance tubing that meets strict safety and regulatory standards. Large multispecialty hospitals often establish long-term supply agreements with medical consumable manufacturers to ensure uninterrupted availability. Additionally, the growing adoption of infection control protocols encourages the use of disposable tubing solutions within inpatient and outpatient settings. As institutional healthcare delivery continues to expand, hospitals and clinics are expected to maintain their leading position in the market.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

North India represents a significant market for medical tubing, supported by the concentration of major public and private healthcare institutions across states, including Delhi, Uttar Pradesh, Rajasthan, and Punjab. The region benefits from established medical tourism corridors and ongoing investments in hospital modernization and capacity expansion in both metropolitan and emerging urban centers.

West and Central India is a key growth region for medical tubing, driven by the robust healthcare ecosystems in Maharashtra, Gujarat, and Madhya Pradesh. The presence of leading pharmaceutical manufacturing clusters and medical device production hubs in this region creates complementary demand for high-quality tubing products used in biopharmaceutical applications and clinical settings.

South India commands a prominent position in the medical tubing market, anchored by the advanced healthcare infrastructure in Karnataka, Tamil Nadu, Kerala, and Andhra Pradesh. The region’s growing medical device manufacturing ecosystem is strengthening local production capacity and supply chain capabilities.

East and Northeast India is an emerging market for medical tubing, driven by government initiatives to improve healthcare access in underserved areas. The region is experiencing accelerated hospital construction and healthcare facility upgrades that are gradually increasing institutional demand for medical tubing products and consumables.

Market Dynamics:

Growth Drivers:

Why is the India Medical Tubing Market Growing?

Growth in Medical Device Manufacturing

India’s robust medical device manufacturing sector is generating significant demand for domestically produced medical tubing. Policy measures aimed at reducing import dependence and promoting local production are encouraging investments in precision component manufacturing. As multinational and domestic companies scale up operations within the country, consistent supply of specialized tubing for infusion systems, ventilators, and diagnostic equipment is becoming more important. In 2024, Union Minister Dr. Mansukh Mandaviya inaugurated 27 greenfield bulk drug park projects and 13 greenfield medical device manufacturing plants under the PLI scheme, including facilities producing imaging systems, stents, dialysis equipment, and catheter tubing for cardiovascular and neurovascular applications. Such initiatives are strengthening backward integration, enhancing self-reliance in advanced medical devices, and supporting the growth of the India medical tubing market.

Technological Advancements in Materials

Continuous advancements in polymer science and extrusion technologies are significantly improving the functional performance of medical tubing products in India. The introduction of advanced biocompatible materials, kink-resistant configurations, and multi-layer constructions is enhancing flexibility, tensile strength, and resistance to chemicals and temperature variations. These improvements enable tubing to maintain structural integrity under demanding clinical conditions. Manufacturers are also aligning product development with stringent sterilization protocols and regulatory requirements, ensuring safety and reliability without substantially increasing production costs. Enhanced material formulations support specialized uses, including minimally invasive surgical procedures and high-pressure fluid management systems. Such technological progress is strengthening product differentiation and encouraging wider adoption of high-performance medical tubing solutions across diverse healthcare applications.

Urbanization and Healthcare Access Expansion

Rapid urbanization in India is contributing significantly to the growth of the medical tubing market by increasing the concentration of hospitals and specialty care centers in metropolitan and emerging urban regions. Improved transportation infrastructure and rising health awareness are enabling patients to access advanced treatments that rely on sophisticated medical devices incorporating precision tubing components. Urban healthcare facilities are more likely to adopt critical care systems, minimally invasive surgical technologies, and high-end diagnostic equipment, all of which require reliable tubing solutions. According to World Bank data, India’s urban population represented approximately 36.87% of the total population in 2024, reflecting a substantial and growing urban base. This demographic shift is supporting higher procedural volumes and sustained demand for specialized medical tubing across modern healthcare settings.

Market Restraints:

What Challenges the India Medical Tubing Market is Facing?

Raw Material Price Volatility and Supply Chain Dependencies

Fluctuating prices of key raw materials including specialty polymers, silicone, and medical-grade plastics create cost pressures for medical tubing manufacturers in India. The dependency on imported raw materials for high-performance medical-grade tubing exposes manufacturers to global supply chain disruptions, currency fluctuations, and geopolitical uncertainties that can impact production costs and pricing stability.

Stringent Regulatory Compliance and Quality Certification Requirements

Meeting rigorous international quality standards and obtaining necessary regulatory certifications for medical tubing products requires substantial investment in testing, quality management systems, and compliance infrastructure. Smaller domestic manufacturers often face challenges in achieving ISO 13485 certification and meeting biocompatibility testing requirements, which can limit their ability to compete in premium market segments.

Limited Advanced Manufacturing Capabilities Among Domestic Producers

While India’s medical tubing manufacturing base is expanding, many domestic producers still lack advanced extrusion capabilities required for producing multi-lumen, braided, and specialty tubing products. This technology gap results in continued import dependence for high-precision tubing applications, limiting the domestic industry’s ability to capture the full value chain and constraining overall market development.

Competitive Landscape:

The India medical tubing market exhibits a moderately competitive structure, with established global specialty material providers operating alongside a growing base of domestic manufacturers. Companies are focusing on expanding production capacities, enhancing material performance, and forming strategic partnerships to strengthen their market position. Competitive intensity is influenced by localization efforts aligned with national manufacturing initiatives, encouraging companies to increase domestic production and reduce import dependence. Investments in advanced extrusion technologies and cleanroom manufacturing facilities are improving product quality and regulatory compliance. Additionally, manufacturers are developing application-specific tubing solutions tailored to the evolving needs of hospitals, diagnostic centers, and medical device producers across India’s expanding healthcare sector.

Recent Developments:

- July 2025: Varex Imaging launched its second manufacturing facility at Andhra Pradesh MedTech Zone (AMTZ), expanding its footprint in India’s medical imaging sector. The new plant planned to introduce India’s first local manufacturing lines for Cesium Iodide coating and medical-grade glass tubes used in X-ray and CT systems. The expansion strengthened domestic production of critical imaging components and supports India’s goal of becoming a global MedTech manufacturing hub.

- November 2024: Lubrizol announced a partnership with Polyhose to establish a medical tubing manufacturing plant in Chennai, India. The facility will produce tubing for neurovascular and cardiovascular applications using medical-grade thermoplastic polymers and is expected to begin operations in 2026. The project supports Lubrizol’s broader investment strategy in India to expand local manufacturing and reduce reliance on imports for medical device components.

India Medical Tubing Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Silicone, Polyolefins, Polyvinyl Chloride, Polycarbonates, Fluoropolymers, Others |

| Structures Covered | Single-Lumen, Co-Extruded, Multi-Lumen, Tapered or Bump Tubing, Braided Tubing |

| Applications Covered | Bulk Disposable Tubing, Drug Delivery Systems, Catheters, Biopharmaceutical Laboratory Equipment, Others |

| End Users Covered | Hospitals and Clinics, Ambulatory Surgical Centers, Medical Labs, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Medical Tubing Market Research Report and Industry Forecast Report

The India medical tubing market size was valued at USD 501.91 Million in 2025.

The India medical tubing market is expected to grow at a compound annual growth rate of 5.66% from 2026-2034 to reach USD 824.08 Million by 2034.

Silicone holds the largest market share at 25% in 2025, driven by its superior biocompatibility, flexibility, and suitability for high-precision medical applications including catheters, drug delivery systems, and implantable devices.

Key factors driving the India medical tubing market include the rising prevalence of chronic diseases such as cardiovascular disorders, diabetes, respiratory ailments, and renal conditions; notably, India had 89.8 million adults living with diabetes in 2024, increasing demand for catheters, dialysis systems, and respiratory tubing solutions.

Major challenges include raw material price volatility and import dependency, stringent regulatory compliance and quality certification requirements, limited advanced manufacturing capabilities among domestic producers, and supply chain disruptions affecting medical-grade polymer availability.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)