India Menswear Market Size, Share, Trends and Forecast by Product Type, Season, Distribution Channel, and Region, 2026-2034

India Menswear Market Size, Share, Trends & Forecast (2026-2034)

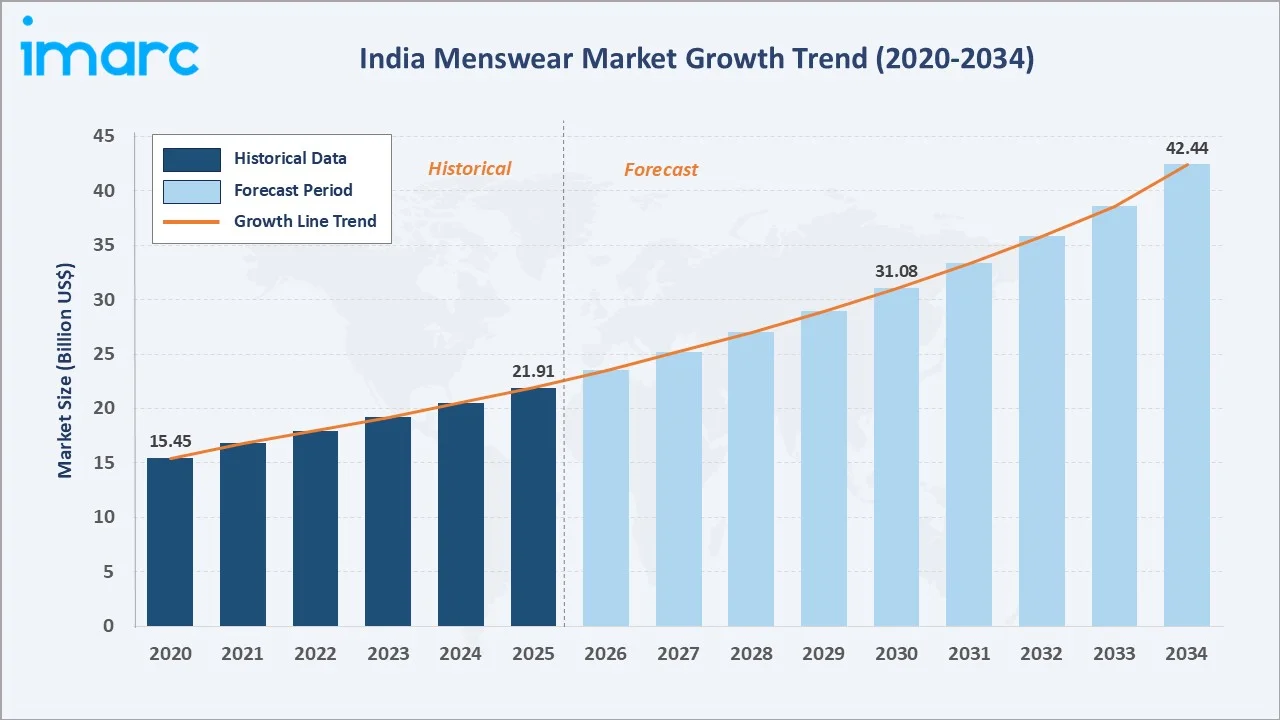

The India menswear market reached USD 21.91 Billion in 2025 and is projected to reach USD 42.44 Billion by 2034, growing at a CAGR of 7.24% during 2026-2034. The market is driven by rising disposable incomes, rapid urbanization, changing fashion trends, and e-commerce expansion.

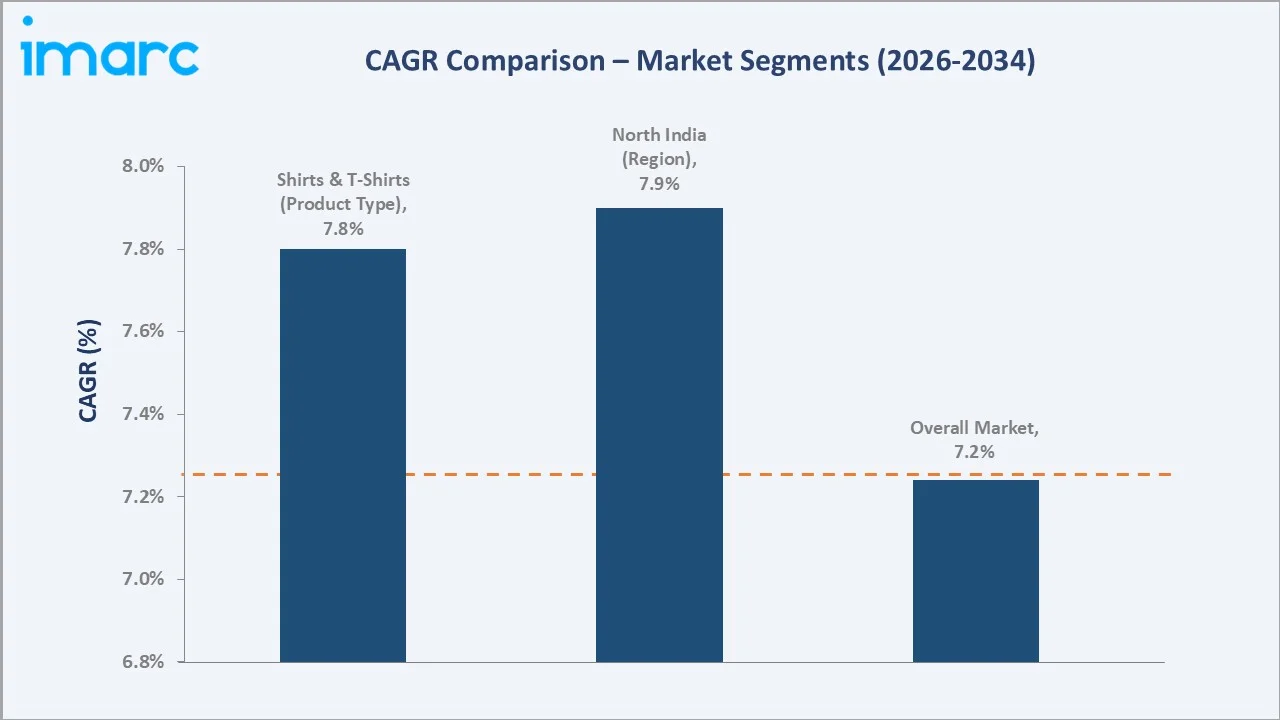

India's growing urban middle class, increasing brand consciousness, and expanding organized retail are structurally accelerating menswear demand. Shirts & T-Shirts lead at 34.0%, All-Season Wear dominates at 46.0%, and North India commands 29.0% of the regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 21.91 Billion |

|

Forecast Market Size (2034) |

USD 42.44 Billion |

|

CAGR (2026-2034) |

7.24% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Shirts & T-Shirts (34.0%, 2025) |

|

Leading Season |

All-Season Wear (46.0%, 2025) |

|

Leading Region |

North India (29.0%, 2025) |

The market expanded steadily over the historical period 2020-2025, anchored by post-pandemic casualwear adoption and rising fashion consciousness. Growing premiumization, ethnic wear revival, and digital commerce are compounding growth through 2034.

To get more information on this market, Request Sample

Shirts & T-Shirts grow at approximately 7.8% CAGR driven by casualization of dress codes and rising branded casual demand. All-Season Wear grows at approximately 7.5% CAGR. North India leads regional CAGR at approximately 7.9% through strong urban fashion consumption.

Executive Summary

The India menswear market reached USD 21.91 Billion in 2025, representing one of the fastest-growing fashion markets globally, driven by India's young demography, urban expansion, and rising male fashion consciousness. The market is projected to reach USD 42.44 Billion by 2034.

Shirts & T-Shirts at 34.0% dominate through versatile everyday wear appeal across formal and casual occasions. All-Season Wear at 46.0% leads through utility and year-round demand. North India at 29.0% reflects high consumer spending and Delhi NCR's fashion retail concentration.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Shirts & T-Shirts – 34.0% share (2025) |

|

Leading Season |

All-Season Wear – 46.0% market share (2025) |

|

Leading Region |

North India – 29.0% market share (2025) |

|

Market Opportunity |

Premiumization; sustainable fabrics; D2C brands; ethnic wear revival; e-commerce expansion |

Key Analytical Observations Supporting the Above Data:

- Shirts & T-Shirts at 34.0%: The shirts and T-shirts segment dominates as it encompasses the highest-frequency everyday wear for Indian men across all occasions, income groups, and geographies, spanning formal dress shirts, casual shirts, polo shirts, and graphic T-shirts.

- All-Season Wear at 46.0%: All-season wear leads as it offers versatile, everyday utility not restricted to seasonal purchase cycles, enabling year-round consistent demand. Cotton-blend fabrics, stretch trousers, and casual shirts designed for India's warm climate drive sustained all-season consumption.

- North India at 29.0%: North India leads through Delhi NCR's high concentration of fashion-forward consumers, strong organized retail presence, and established tradition of both western and ethnic menswear consumption across diverse occasions.

India Menswear Market Overview

The India menswear market encompasses the design, manufacture, distribution, and retail of all clothing specifically tailored for men, including formal wear, casualwear, ethnic wear, innerwear, activewear, and outerwear across all price segments and distribution channels.

The ecosystem integrates raw material suppliers, textile mills, garment manufacturers, branded apparel companies, retail distributors including exclusive stores, MBOs, and e-commerce platforms, and regulatory bodies governing textile safety standards. Rising incomes, urbanization, and social media-driven fashion adoption are key macroeconomic drivers.

Market Dynamics

To evaluate market opportunities, Request Sample

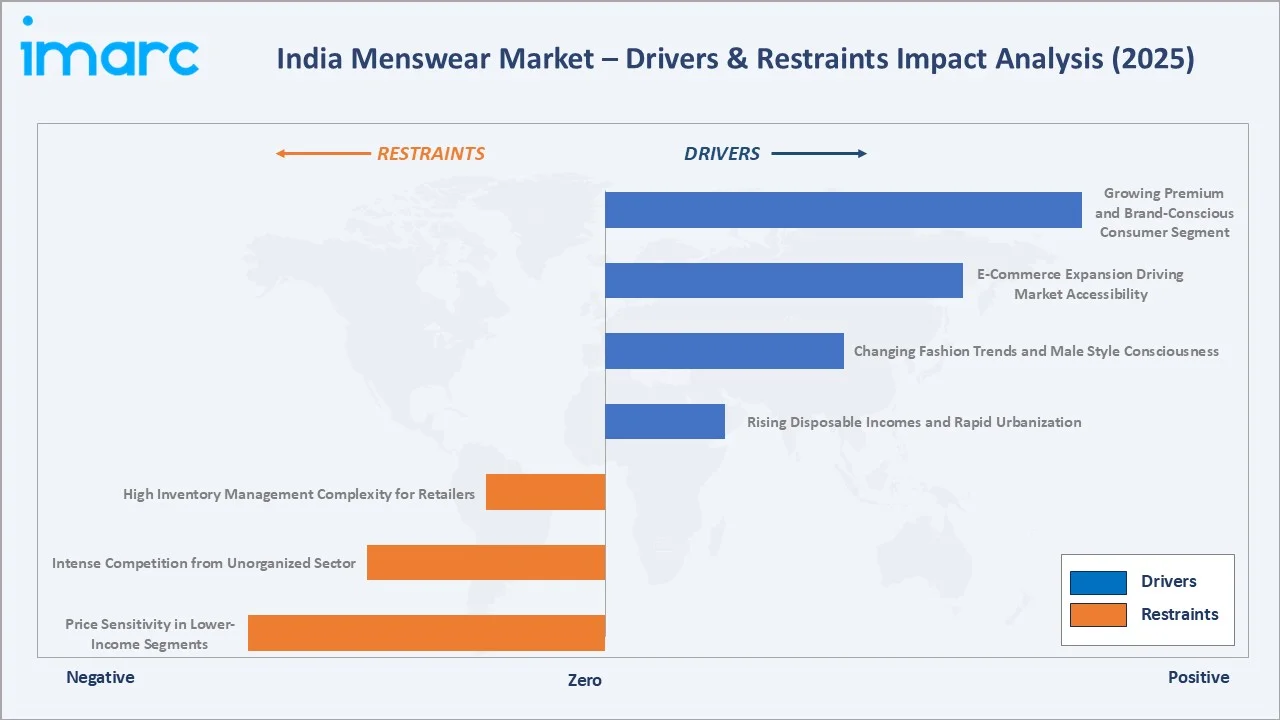

Market Drivers

- Rising Disposable Incomes and Rapid Urbanization: India's rising per-capita income and accelerating urbanization are expanding the addressable menswear consumer base. Urban males are allocating higher wallet share to branded apparel, premiumization is accelerating across tier-1 and tier-2 cities, and organized retail expansion is enabling brand access beyond metropolitan centers.

- Changing Fashion Trends and Male Style Consciousness: Increasing social media penetration, celebrity endorsements, and fashion media are driving higher style consciousness among Indian men. Consumers are actively upgrading wardrobes, embracing athleisure and workwear fusion trends, and demonstrating a growing preference for branded over unbranded alternatives.

- E-Commerce Expansion Driving Market Accessibility: Rapid growth of fashion e-commerce platforms is enabling branded menswear access across Tier-2 and Tier-3 cities previously underserved by organized retail. Virtual try-on technology, easy returns, and targeted recommendations are accelerating online apparel conversion rates.

- Growing Premium and Brand-Conscious Consumer Segment: India's expanding affluent middle class is driving structural premiumization in menswear. Consumers are actively trading up from value-tier to mid-premium and premium branded alternatives, driven by rising incomes, fashion awareness, and social aspiration.

Market Restraints

- Price Sensitivity in Lower-Income Segments: A significant proportion of India's male consumer base remains price-sensitive, particularly in rural and semi-urban markets. The unorganized sector's low-cost alternatives constrain branded manufacturers' market penetration and limit premiumization potential in mass-market segments.

- Intense Competition from Unorganized Sector: India's menswear market remains significantly fragmented, with the unorganized sector capturing the maximum share of total market volume. This competition limits pricing power for organized brands and makes channel management challenging in traditional retail formats.

- High Inventory Management Complexity for Retailers: Menswear's diverse product range across sizes, colors, fabrics, and seasonal variants creates significant inventory complexity. Overstocking or understocking leads to markdown requirements and margin compression, particularly at the mid-market tier.

Market Opportunities

- Ethnic and Fusion Menswear Premiumization: Growing demand for branded ethnic and fusion menswear across wedding, festive, and celebration occasions is creating a significant market opportunity. Brands investing in premium kurtas, sherwanis, and Indo-western styles can capture high-value per-transaction purchases.

- Sustainable and Eco-Friendly Fabric Innovation: Rising environmental consciousness among urban Indian consumers is creating demand for organic cotton, recycled polyester, and sustainably sourced fabrics. Brands with transparent sustainability credentials can command premium pricing and build loyalty among eco-conscious consumers.

Market Challenges

- Counterfeit and Grey Market Product Proliferation: Premium and aspirational menswear brands face persistent challenges from counterfeit products mimicking their designs and brand identifiers, damaging brand equity and reducing consumer confidence in authentic premium products.

- Rising Raw Material and Production Cost Pressures: Volatility in cotton prices, polyester feedstock costs, and labor expenses creates margin pressure for menswear manufacturers. Cost increases are difficult to fully pass through to price-sensitive consumers without volume impact.

Emerging Market Trends

1. Casualisation and Work-from-Anywhere Fashion Shift

The post-pandemic shift toward hybrid work models and casual dress codes is structurally expanding the smart-casual menswear segment. Premium T-shirts, chinos, and casual shirts are gaining share at the expense of traditional formal suits, driving new product category growth.

2. E-Commerce and D2C Brand Proliferation

Direct-to-consumer menswear brands born on digital platforms are rapidly gaining market share, leveraging data-driven personalization, targeted social media marketing, and agile product development cycles. Digital-native brands are disrupting established players in casualwear and ethnic menswear.

3. Ethnic and Occasion Wear Premiumization

Branded ethnic and occasion menswear is experiencing structural demand growth driven by India's large wedding market and increasing consumer preference for premium celebration wear. Brands offering end-to-end ethnic menswear solutions are capturing high-value per-occasion spend.

4. Sustainable Fabric and Conscious Fashion Adoption

Urban Indian consumers are increasingly gravitating toward menswear brands with credible environmental credentials. Organic cotton, recycled fabrics, and carbon-neutral production claims are becoming meaningful differentiators among younger, premium-segment male consumers.

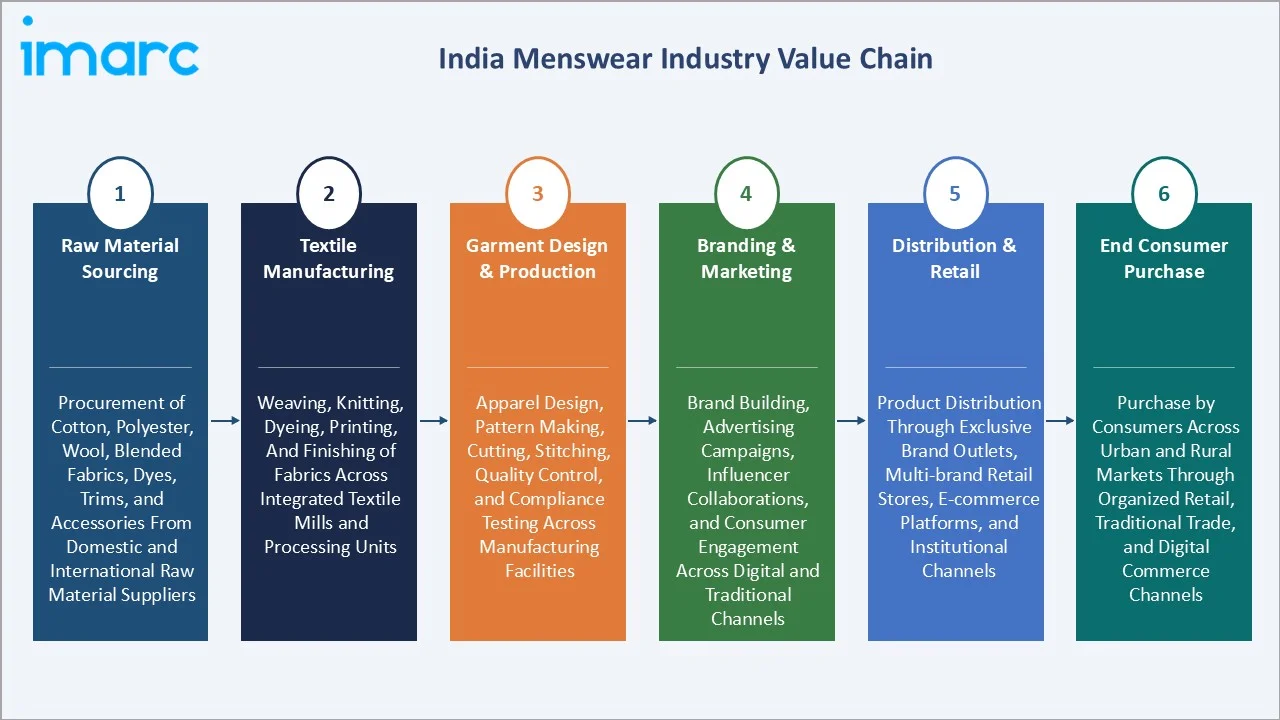

Industry Value Chain Analysis

The India menswear value chain integrates raw material and fabric procurement, textile manufacturing, garment design and production, brand building, multi-channel distribution, and end consumer sales across organized retail, e-commerce, and traditional trade formats.

|

Stage |

Key Activities |

|

Raw Material Sourcing |

Procurement of cotton, polyester, wool, blended fabrics, dyes, trims, and accessories from domestic and international raw material suppliers |

|

Textile Manufacturing |

Weaving, knitting, dyeing, printing, and finishing of fabrics across integrated textile mills and processing units |

|

Garment Design & Production |

Apparel design, pattern making, cutting, stitching, quality control, and compliance testing across manufacturing facilities |

|

Branding & Marketing |

Brand building, advertising campaigns, influencer collaborations, and consumer engagement across digital and traditional channels |

|

Distribution & Retail |

Product distribution through exclusive brand outlets, multi-brand retail stores, e-commerce platforms, and institutional channels |

|

End Consumer Purchase |

Purchase by consumers across urban and rural markets through organized retail, traditional trade, and digital commerce channels |

The garment design, branding, and e-commerce distribution stages hold the highest value creation potential through product differentiation, brand equity, and digital consumer engagement. Vertical integration from fabric to finished garment is being adopted by leading players to improve quality and margin capture.

Technology Landscape in the India Menswear Industry

AI-Driven Personalization and Recommendation Technology

AI-powered size recommendation, style personalization, and virtual try-on technologies are reducing online fashion return rates and improving conversion. Machine learning models analyzing consumer purchase history and browsing behavior enable hyper-personalized menswear recommendations, enhancing digital channel economics.

Sustainable and Technical Fabric Technology

Advanced fabric technologies including moisture-wicking, anti-odor, UV-protection, and wrinkle-resistant finishes are creating functional performance menswear premium segments. Sustainable fabric innovations including lyocell, recycled polyester, and organic cotton are enabling brands to address eco-conscious consumer demand.

Omnichannel Retail Technology

RFID-based inventory management, buy-online-pick-up-in-store capabilities, and real-time inventory visibility across channels are enabling integrated omnichannel experiences. These technologies reduce stockouts, minimize overstock markdowns, and improve same-store sales productivity for organized menswear retailers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Shirts and T-Shirts |

34.0% |

2025 |

|

Season |

All-Season Wear |

46.0% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

North India |

29.0% |

2025 |

By Product Type

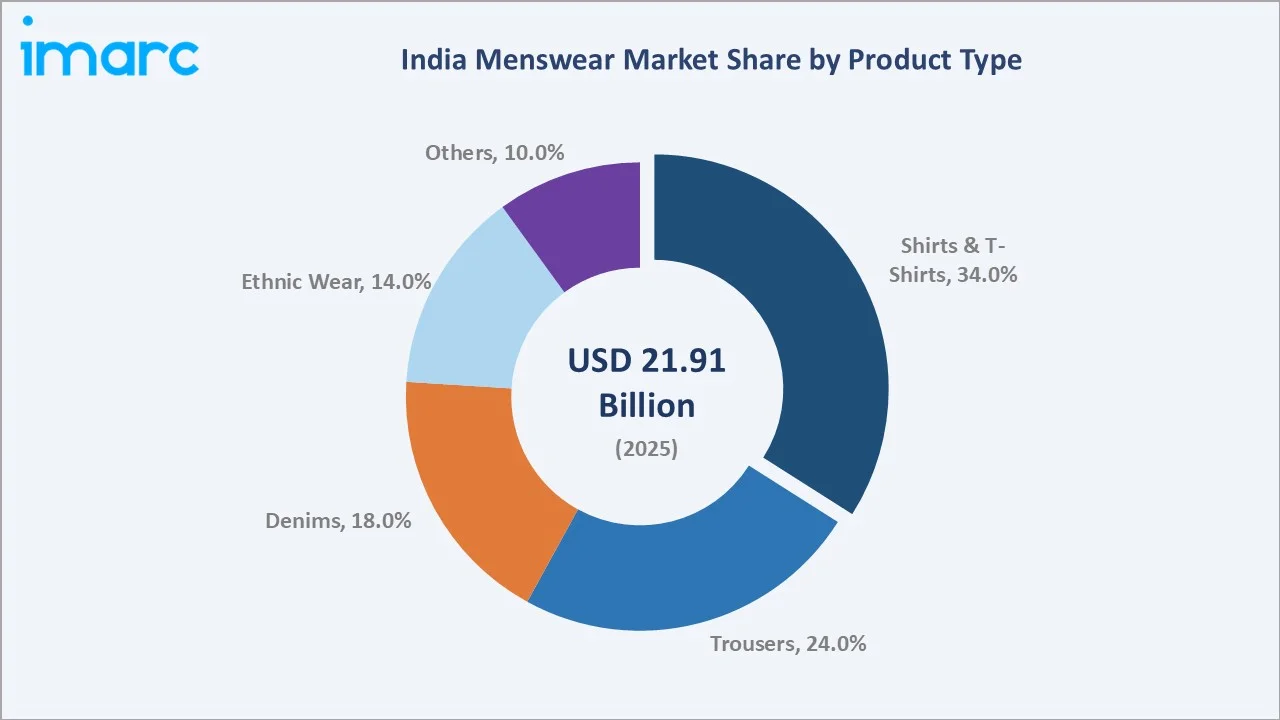

Shirts & T-Shirts lead at 34.0% in 2025, encompassing formal dress shirts, casual shirts, polo shirts, and graphic T-shirts across all price segments. This segment's dominance reflects its highest purchase frequency, versatile usage across formal and casual occasions, and broad consumer demographics.

To access detailed market analysis, Request Sample

Trousers at 24.0% capture formal trousers, chinos, and casual pants demand. Denims at 18.0% benefit from sustained casualization trends. Ethnic Wear at 14.0% is the fastest-growing sub-segment driven by branded kurtas, sherwanis, and festive occasion wear. Others at 10.0% includes activewear, innerwear, and outerwear.

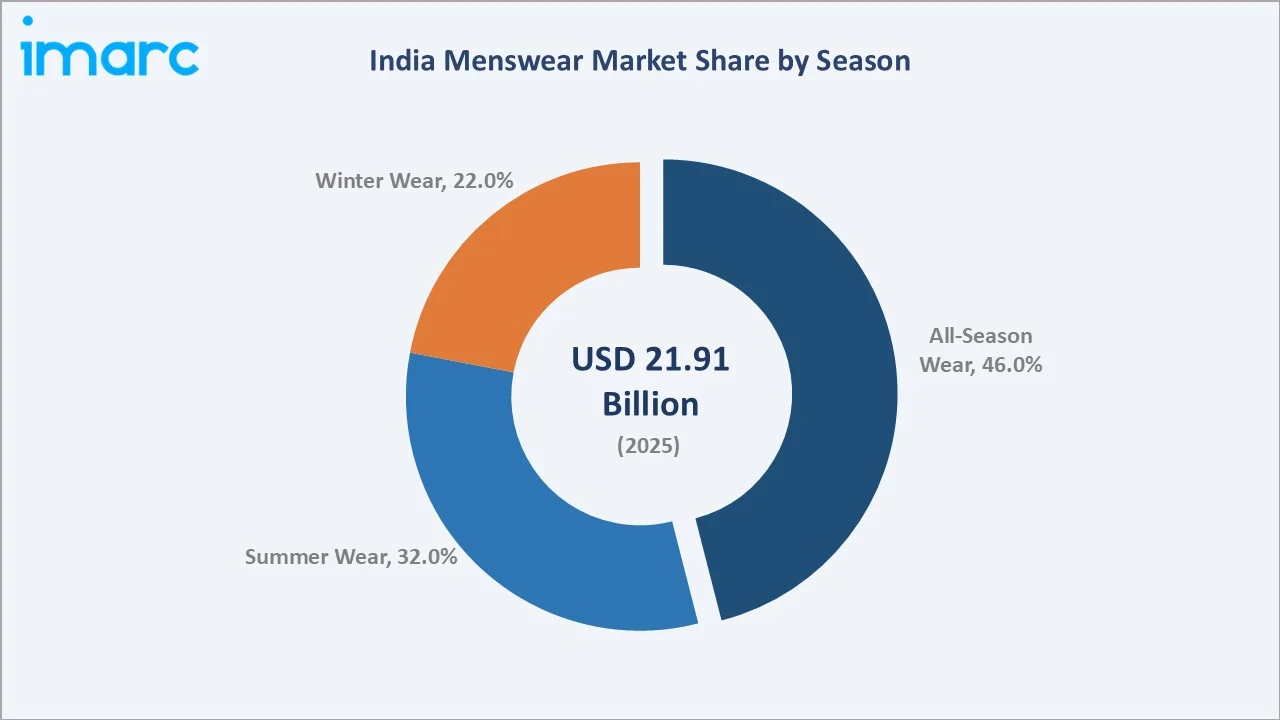

By Season

All-Season Wear leads at 46.0% through year-round utility across cotton-blend fabrics, everyday shirts, and casual trousers not restricted to seasonal purchase cycles. India's predominantly warm climate sustains high all-season demand, and organized brands increasingly develop trans-seasonal collections.

Summer Wear at 32.0% captures high-volume T-shirt and lightweight shirt demand during peak summer months. Winter Wear at 22.0% represents the premium segment opportunity, with consumers willing to pay premium prices for quality woollens, jackets, and outerwear during colder months.

Regional Market Insights

|

Region |

Share (2025) |

Key Market Drivers & Characteristics |

|

North India |

29.0% |

Driven by high consumer spending, strong urban fashion consciousness, and dense organized retail infrastructure across major metropolitan and tier-2 city markets |

|

South India |

27.0% |

Supported by rising disposable incomes, strong brand adoption in metro cities, and growing consumer preference for both formal and casual branded menswear |

|

West & Central India |

26.0% |

Driven by fashion-forward consumer bases in major urban centers, growing e-commerce penetration, and expanding organized retail formats across the region |

|

East India |

18.0% |

Emerging growth driven by rising incomes, increasing urbanization, expanding organized retail infrastructure, and growing fashion awareness in tier-2 and tier-3 cities |

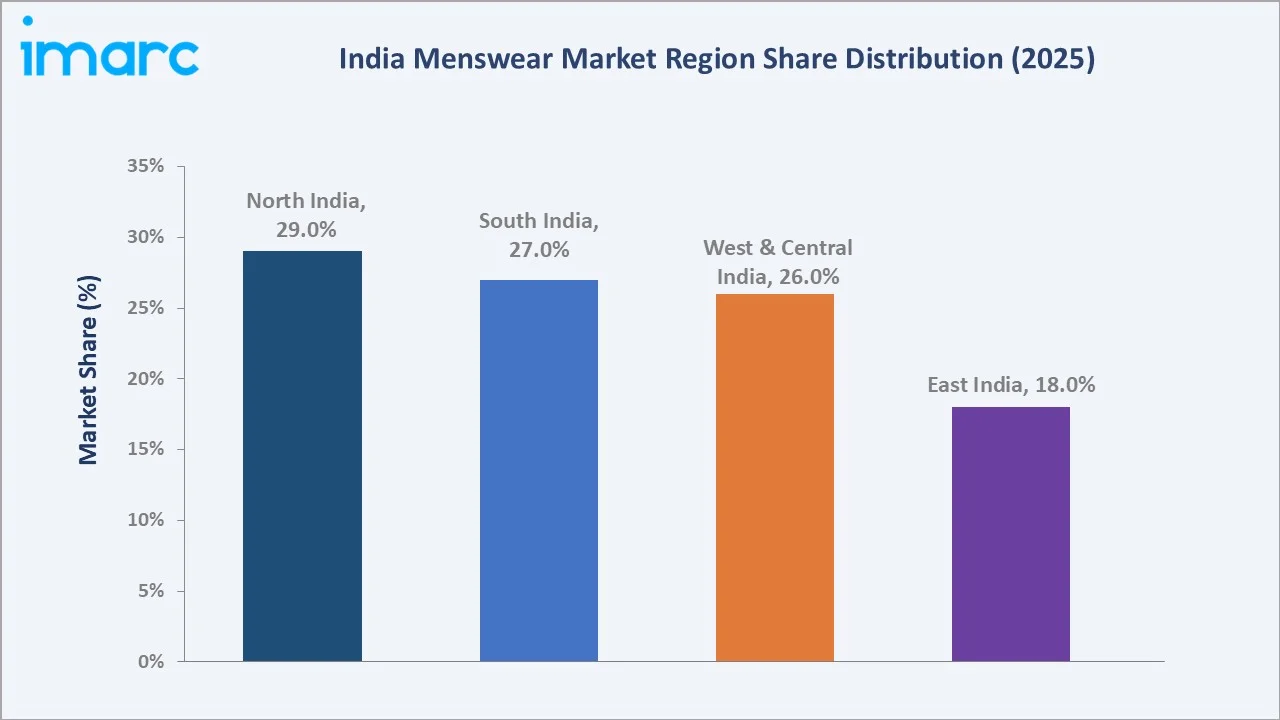

North India, at 29.0%, leads through Delhi NCR's massive urban fashion consumer base, high per-capita spending on branded menswear, and strong organized retail infrastructure spanning premium malls to large-format value retailers.

South India, at 27.0%, reflects high brand adoption in Chennai, Bengaluru, and Hyderabad. West & Central India, at 26.0%, benefits from Mumbai's fashion-forward consumer culture. East India, at 18.0%, is the fastest-growing region driven by Kolkata's expanding organized retail.

Competitive Landscape

The India menswear market's competitive landscape is moderately concentrated, led by diversified branded apparel conglomerates alongside strong single-category specialists and fast-growing ethnic wear players. Competition centers on brand equity, multi-channel distribution, product portfolio breadth, and pricing strategy.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Raymond Limited |

Raymond Suits, Park Avenue, ColorPlus, Parx, Ethnix |

Market Leader |

Raymond Limited leads India's menswear market with an iconic brand legacy spanning suiting, formal wear, and readymade garments across premium and mid-market segments. |

|

Page Industries Ltd. |

Jockey Innerwear, Activewear, T-Shirts, Loungewear |

Strong Challenger |

Page Industries Limited leads India's premium innerwear and activewear segment with strong brand equity and national retail distribution. |

|

Vedant Fashions Ltd. |

Manyavar, Mohey, Manthan, Twamev |

Niche Player |

Vedant Fashions Limited is India's largest branded ethnic menswear company, dominating the wedding and celebration wear segment through its Manyavar brand. |

Key players include Raymond Limited, Page Industries Ltd., Vedant Fashions Ltd., and others.

Key Company Profiles

Raymond Limited

Raymond is India's most iconic menswear brand, operating across premium suiting fabrics, branded readymade garments, and ethnic menswear with a legacy spanning over nine decades and a pan-India retail presence.

- Key Products: Raymond Suits, Park Avenue, ColorPlus, Parx, Ethnix

- Recent Developments: In April 2026, Raymond launched its premium menswear destination, Chairman’s Collection, in Mumbai’s Bandra, marking the brand’s expansion into luxury fashion retail. The new format offers couture menswear, bespoke tailoring, and personalized styling in an appointment-led setting.

- Strategic Focus: Expanding branded readymade garment revenues through premiumization, growing the Ethnix ethnic wear franchise, and strengthening e-commerce and omnichannel distribution capabilities.

Page Industries Ltd.

Page Industries is India's leading premium innerwear and athleisure manufacturer, operating as the exclusive licensee of Jockey International Inc. (USA) with a pan-India distribution.

- Key Products: Jockey Innerwear, Activewear, T-Shirts, Loungewear

- Recent Developments: In October 2025, the company launched its 1,500th exclusive brand store in India, further strengthening its nationwide footprint. The new outlet reflects Jockey’s focus on reaching younger and style-conscious consumers through a refreshed retail format and a wider portfolio spanning innerwear, apparel, and athleisure for men, women, and children.

- Strategic Focus: Strengthening omnichannel retail through dedicated Regional Distribution Centres, expanding exclusive brand stores in urban and semi-urban markets, and driving athleisure and women's innerwear category growth to diversify beyond men's innerwear.

Market Concentration Analysis

The India menswear market is moderately fragmented. The top five organized players collectively account for approximately 25-35% of the organized branded menswear market revenue.

The unorganized sector retains an estimated 40-50% of total market volume through low-cost garments sold through local tailors, unbranded wholesale markets, and traditional retail formats. Market concentration is expected to increase as organized brands expand into Tier-2 and Tier-3 cities.

Investment & Growth Opportunities

Highest Growth Segments

Ethnic and occasion menswear (~10-12% CAGR), premium athleisure (~12%+ CAGR), D2C casual brands (~15% CAGR), e-commerce fashion channel (~18% CAGR), and sustainable menswear (~20%+ CAGR from small base) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

India's large and growing wedding market represents the menswear market's highest per-transaction value opportunity. Branded ethnic menswear companies capturing wedding occasion spending demonstrate significantly above-market revenue growth rates and high customer lifetime value.

Investment Themes

- Premiumization and Branded Upgrade Investment: India's rising middle class is structurally trading up from unbranded to mid-premium and premium branded menswear. Investments in strong brand equity, premium retail formats, and premium product development represent high-return opportunities as per-capita income growth sustains premiumization through 2034.

- E-Commerce and Omnichannel Infrastructure: Building robust digital commerce, virtual try-on, and omnichannel fulfillment capability represents structural competitive advantage. Fashion e-commerce is growing at over 18% annually and enabling premium brand access across previously unreachable Tier-2 and Tier-3 consumer bases.

Future Market Outlook (2026-2034)

The India menswear market is projected to grow from USD 21.91 Billion in 2025 to USD 42.44 Billion by 2034, delivering a 7.24% CAGR. Growth is underpinned by India's young demography, accelerating urbanization, rising fashion consciousness, and expanding organized retail infrastructure.

Three structural forces define market growth through 2034. India's expanding urban middle class creates compounding demand for branded menswear as consumers trade up from unorganized channels. Casualization trends are creating new premium casualwear sub-categories. E-commerce expansion unlocks branded fashion access across Tier-2 and Tier-3 markets previously dominated by unbranded supply.

Research Methodology

Primary Research

Primary research comprised structured interviews with 45+ industry stakeholders (2025), including menswear brand managers, retail channel executives, fabric and raw material suppliers, e-commerce category managers, and fashion trend analysts.

Secondary Research

Secondary research encompassed company annual reports, Textile Ministry publications, organized retail industry data, IMARC Group fashion market tracking, and regulatory filings. Over 50 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using a consumer spending-based demand model incorporating urban household formation rates, per-capita menswear spending trends, premiumization trajectories, and channel-level distribution expansion assumptions across organized trade and e-commerce.

India Menswear Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Trousers, Denims, Shirts and T-Shirts, Ethnic Wear, Others |

| Seasons Covered | Summer Season, Winter Season, All-Season Wear |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Exclusive Stores, Multi-Brand Retail Outlets, Online Stores, Others |

| Regions Covered | South India, North India, West & Central India, East India |

| Companies Covered | Raymond Limited, Page Industries Ltd., Vedant Fashions Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India menswear market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the India menswear market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India menswear industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Menswear Market Report

The India menswear market reached USD 21.91 Billion in 2025, driven by Shirts & T-Shirts dominant at 34.0%, All-Season Wear leading at 46.0%, and North India commanding 29.0% regional market share through high consumer spending and strong organized retail infrastructure.

The India menswear market grows at 7.24% CAGR during 2026-2034, reaching USD 42.44 Billion by 2034. Growth reflects rising disposable incomes, urban fashion consciousness, e-commerce expansion, ethnic wear premiumization, and growing branded menswear penetration in Tier-2 and Tier-3 markets.

Shirts & T-Shirts lead at 34.0%, capturing everyday formal and casual wear requirements across all income groups and geographies. The segment grows at approximately 7.8% CAGR through casualization of dress codes and rising branded casual demand among urban and semi-urban male consumers.

All-Season Wear dominates at 46.0% through the year-round utility of cotton-blend everyday shirts, trousers, and casual wear. India's predominantly warm climate sustains all-season demand at approximately 7.5% CAGR, making it the highest-revenue and most consistent demand segment.

North India leads at 29.0% through Delhi NCR's high per-capita fashion spending, strong organized retail density, and established tradition of both western and ethnic menswear consumption across diverse consumer demographics and occasions.

Leading companies include Raymond Limited, Page Industries Ltd., Vedant Fashions Ltd., and others.

The India menswear market is projected to reach approximately USD 31.08 Billion by 2030, driven by continued urbanization, premiumization of shirts and casualwear segments, ethnic wear branded expansion, and e-commerce channel growth accelerating organized brand penetration.

Three priority investment opportunities: branded ethnic and occasion menswear capturing India's large wedding market, e-commerce and omnichannel infrastructure investment enabling premium brand access across Tier-2 and Tier-3 cities, and premiumization plays targeting India's expanding aspirational middle-class male consumer segment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)