India mHealth Market Size, Share, Trends and Forecast by Component, Service, Participants, and Region, 2026-2034

India mHealth Market Size and Share:

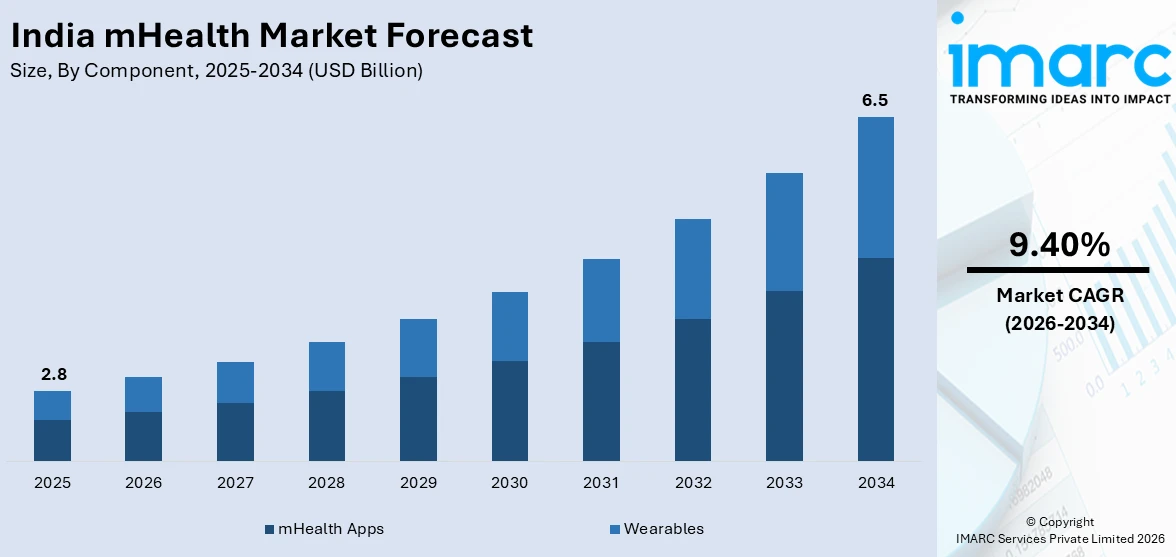

The India mHealth market size was valued at USD 2.8 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 6.5 Billion by 2034, exhibiting a CAGR of 9.40% during 2026-2034. North India currently dominates the market, holding a significant market share of 32.3% in 2025. Growing use of smartphones, improved internet access, and increasing preference for digital health tools are supporting the rise of mobile-based healthcare in India. Demand for remote consultations, self-monitoring, and health apps continues to expand. This upward trend is strengthening the India mHealth market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 2.8 Billion |

| Market Forecast in 2034 | USD 6.5 Billion |

| Market Growth Rate (2026-2034) | 9.40% |

The rapid growth in smartphone ownership has significantly contributed to the adoption of mobile health services in India. Affordable data plans and widespread internet availability have made it easier for people to access healthcare tools through their phones. This shift is especially visible in semi-urban and rural regions, where physical healthcare infrastructure often falls short. Users now prefer mobile apps for doctor consultations, medicine orders, health monitoring, and wellness tips, offering convenience and time savings. In the second half of 2024, several telecom companies launched bundled health services with mobile recharge plans, targeting tier-2 and tier-3 cities. This move attracted first-time users to try mobile health platforms. Additionally, the launch of basic-feature mobile health apps by government bodies allowed low-income users to receive primary care updates, vaccination alerts, and maternal health information.

To get more information on this market Request Sample

Policy support and digital health schemes have played a strong role in advancing the mHealth market in India. Government initiatives are encouraging the use of mobile platforms to improve healthcare access, reduce patient wait times, and streamline administrative tasks. Programs that support teleconsultation, e-prescriptions, and remote diagnostics are pushing healthcare providers to adopt mobile-based services. During 2024, the Ayushman Bharat Digital Mission added new features for integrating mobile apps with health records, boosting ease of use for patients and doctors. Public hospitals in several states started using mobile dashboards for patient tracking and appointment scheduling.

India mHealth Market Trends:

Push for Integrated Digital Infrastructure

India’s mHealth sector is experiencing steady expansion, largely supported by national efforts to build a connected digital ecosystem in healthcare. One of the most prominent trends is the prioritization of infrastructure that unifies patient data, streamlines service delivery, and promotes secure digital interactions. With increased smartphone usage and internet penetration, the need for centralized digital health systems has grown stronger, particularly to bridge the service divide between rural and urban regions. A turning point came in January 2025 when the Ayushman Bharat Digital Mission advanced these goals by launching Health IDs, the Unified Health Interface (UHI), and comprehensive digital registries for facilities and professionals. These features created a foundation for safe and efficient data exchange, remote consultations, and improved clinical coordination. The impact has been visible in expanded telemedicine reach, better care continuity, and faster diagnostics, especially in underserved areas. As this infrastructure matures, private players are also aligning their platforms to national standards, fostering interoperability across systems. The emphasis on system-level integration reflects a clear trend where government-led infrastructure is not just supporting policy goals, but actively shaping mHealth innovation. The push for digital uniformity has emerged as a strong growth driver, increasing institutional adoption and boosting user confidence in digital health tools.

Focus on Public Accessibility and Convenience

An important trend driving the India mHealth market growth is the increasing focus on enhancing public accessibility and simplifying everyday healthcare interactions. As patients seek faster, more transparent ways to interact with healthcare systems, digital solutions that improve user experience are gaining popularity. A clear example emerged in April 2025 when the Kerala government introduced an mHealth mobile app in state-run hospitals. This app provided users with access to treatment histories, lab reports, and prescriptions on their mobile devices, while also enabling online outpatient bookings and a scan-to-book system using hospital-displayed QR codes. These features removed the need for physical queueing, making healthcare more convenient for both patients and hospital staff. The rollout, especially in facilities under the public health department, demonstrated how localized innovation can significantly increase the use of mHealth platforms in real-world settings. This trend of prioritizing end-user simplicity, through mobile integration, fewer touchpoints, and quick digital transactions, is helping mHealth services expand beyond early adopters to reach a wider demographic. As more people experience the practical benefits of digital access in their local hospitals, the demand for similar tools across other states is likely to rise. The broader shift reflects a market increasingly driven by the value of convenience in care delivery.

Surge in Mobile-Driven Health Solutions

The market is rapidly expanding, driving a shift in how healthcare services are accessed and delivered through mobile and wireless technologies. As a key segment of electronic health (eHealth), mHealth is improving patient engagement, expanding access to services, and supporting better health outcomes. Its uses include remote health monitoring, streamlined communication between patients and doctors, and enhanced medication compliance. It also contributes to supply chain tracking, diagnostic support, and chronic disease management. Non-communicable diseases remain a major health challenge in India, responsible for over half of all deaths and a significant share of lost healthy years, according to the Ministry of Science and Technology. In response, mHealth tools are helping raise awareness and empower individuals with real-time health data. Under the Ayushman Bharat Digital Mission, more than 76 Crore people have registered for ABHA IDs, and over 51 Crore digital health records are now linked, based on National Health Authority data. Rising smartphone usage and improved internet connectivity are strengthening this trend. IDC reports that India shipped 29 million 5G smartphones in Q1 2025, with 5G devices making up 88% of shipments. As mobile platforms offer services like booking appointments and tailored health advice, the market is set to grow even further.

India mHealth Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the India mHealth market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on component, service, and participants.

Analysis by Component:

- Wearables

- Blood Pressure Monitors

- Blood Glucometer

- Pulse Oximeter

- Neurological Monitors

- Others

- mHealth Apps

- Medical Apps

- Fitness Apps

In 2025, the mHealth apps segment led the market, accounting for 77.8% of the total market share, driven by the popularity of mHealth apps in India, which is growing steadily due to their ease of use, multilingual features, and integration with everyday smartphones. Apps that offer doctor consultations, medication reminders, fitness tracking, and mental health support have gained wide acceptance. In 2024, several Indian startups introduced lightweight apps suited for low-end phones, increasing rural outreach. Growing public trust, improved digital literacy, and partnerships with hospitals and insurance firms continue to expand their role in the national healthcare ecosystem. The India mHealth market forecast suggests continued industrial growth, fueled by increasing adoption rates and ongoing innovation in mobile healthcare solutions.

Analysis by Service:

Access the comprehensive market breakdown Request Sample

- Monitoring Services

- Diagnosis Services

- Healthcare Systems Strengthening Services

- Treatment Services

- Others

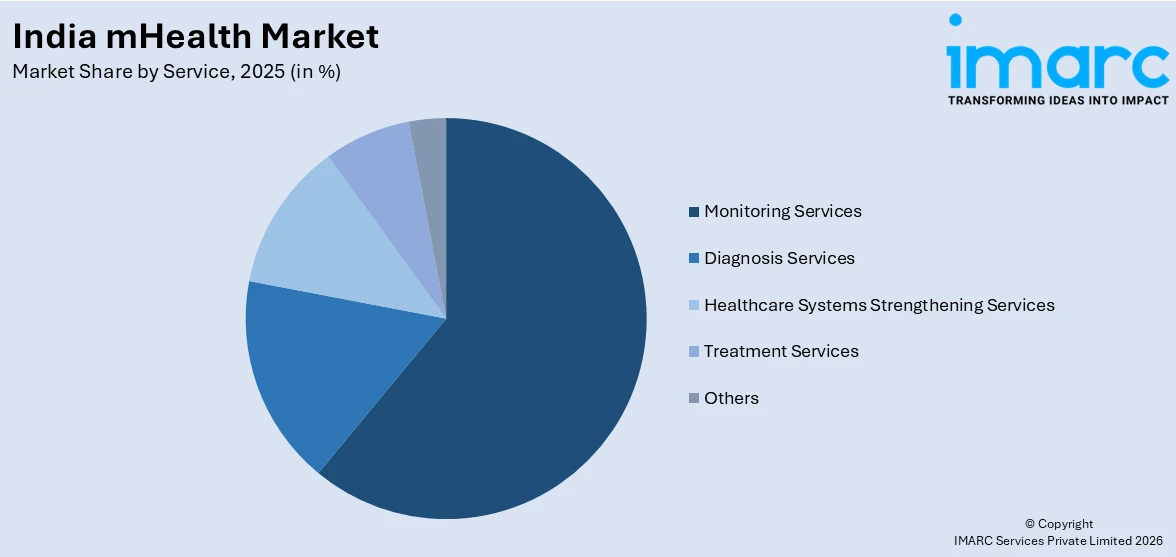

In 2025, monitoring services segment led the Indian mHealth market, accounting for 61.2% of the total market share. Mobile-based monitoring services are driving patient engagement by enabling real-time tracking of vital signs and chronic conditions. Diabetics, heart patients, and senior citizens increasingly rely on these tools for regular updates. In India, telemonitoring gained ground during the COVID-19 pandemic and continues to expand through app-device integration. Healthcare providers are using mobile dashboards for managing patient alerts and data. Improved connectivity and reduced device costs are supporting large-scale adoption, especially in tier-2 and tier-3 cities.

Analysis by Participants:

- mHealth Application Companies

- Pharmaceuticals Companies

- Hospitals

- Health Insurance Companies

- Others

In 2025, mHealth application companies led the Indian mHealth market, as these companies play a crucial role by creating solutions tailored for local needs, including regional language support, low-data modes, and integration with UPI for payments. These firms partner with hospitals, insurers, and governments to expand reach. In 2024, several companies received funding to develop AI-driven diagnostic apps. Strong user demand, regulatory support, and investor interest continue to drive innovation and competition in this space, helping the overall mHealth market grow rapidly and sustainably. Digital outreach allows them to engage directly with chronic disease patients and caregivers. In 2024, several firms launched branded mobile apps for prescription reminders and therapy monitoring. This shift supports better outcomes and builds loyalty. As more pharma players digitize their patient services, their involvement is becoming a key factor driving the mHealth market’s development and credibility.

Regional Analysis:

- North India

- West and Central India

- South India

- East and Northeast India

According to the India mHealth market outlook, in 2025, North India led the market, accounting for 32.3% of the total market share. North India is seeing a surge in mHealth adoption due to improved mobile infrastructure and rising digital literacy. Urban centers like Delhi and Chandigarh are leading in teleconsultation, while rural districts benefit from state-run health apps offering maternal care and disease monitoring. In 2024, partnerships between private app developers and public hospitals expanded access to remote diagnosis. High population density, combined with a growing burden of chronic diseases, is pushing demand for digital health tools. Supportive state health departments and targeted awareness campaigns are further driving mHealth integration across both metro and non-metro areas in the region.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Latest News and Developments:

- April 2025: RED Health launched FLASH, an AI-powered mHealth app offering rapid medical assistance in Hyderabad. Utilizing real-time tracking and advanced routing, FLASH dispatches ambulances within eight minutes, providing services like IV medication, vaccinations, and post-surgical care.

- February 2025: Gurugram-based Lifesigns secured strategic investment from Healthcare Capital, the investment arm of Kauvery Hospital Group. The funding aims to advance Lifesigns' AI-powered patient monitoring platform, featuring USFDA-approved hardware and predictive analytics, to enhance real-time healthcare delivery across hospitals, ambulances, and home care settings.

- February 2025: The World Economic Forum launched the India Digital Health Activator to accelerate digital health adoption, including mHealth, AI, and interoperability. The initiative aims to create regional hubs, promote secure health data exchange, and support telemedicine and mobile health innovations through public-private collaboration aligned with India’s digital health goals.

- January 2025: Cipla introduced CipAir, an AI-driven mHealth application designed for initial asthma screening in India. The app guides users through three exhalations aimed at extinguishing a virtual candle, analyzing the sounds to detect asthma indicators.

- October 2024: Health tech startup sehatUP launched an integrated digital health clinic, blending modern medicine with Ayurveda and homeopathy. Supporting the "One Nation One Health System" vision, the mHealth platform offers personalized wellness plans, sexual and weight care, free consultations, and discreet delivery for holistic, mobile-based healthcare access.

- July 2024: Hyundai Motor India Foundation launched mobile health units under its Sparsh Sanjeevani initiative in Nagpur and Sambhajinagar, Maharashtra. Equipped with doctors, diagnostics, and medicines, these units aim to deliver free primary healthcare to underserved rural areas.

India mHealth Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered |

|

| Services Covered | Monitoring Services, Diagnosis Services, Healthcare Systems Strengthening Services, Treatment Services, Others |

| Participants Covered | mHealth Application Companies, Pharmaceuticals Companies, Hospitals, Health Insurance Companies, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India mHealth market from 2020-2034.

- The India mHealth market research report provides the latest information on the market drivers, challenges, and opportunities in the regional market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key markets within the region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India mHealth industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India mHealth Market Report

The mHealth market in India was valued at USD 2.8 Billion in 2025.

The India mHealth market is projected to exhibit a CAGR of 9.40% during 2026-2034, reaching a value of USD 6.5 Billion by 2034.

Key factors driving the India mHealth market include growing smartphone and internet penetration, rising demand for remote healthcare, increased chronic disease burden, supportive government digital health initiatives, and the expansion of telemedicine platforms offering affordable, accessible, and real-time medical services across urban and rural regions.

In 2025, North India dominated the India mHealth market holding a significant market share of 32.3%, driven by increasing smartphone penetration, growing health awareness, and government initiatives supporting digital health services. The region also benefits from a large, tech-savvy population and expanding healthcare infrastructure.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade