India Military Drone Market Size, Share, Trends and Forecast by Type, Operation Mode, Range, Application, Maximum Takeoff Weight, End Use, and Region, 2026-2034

India Military Drone Market Size, Share, Trends & Forecast (2026-2034)

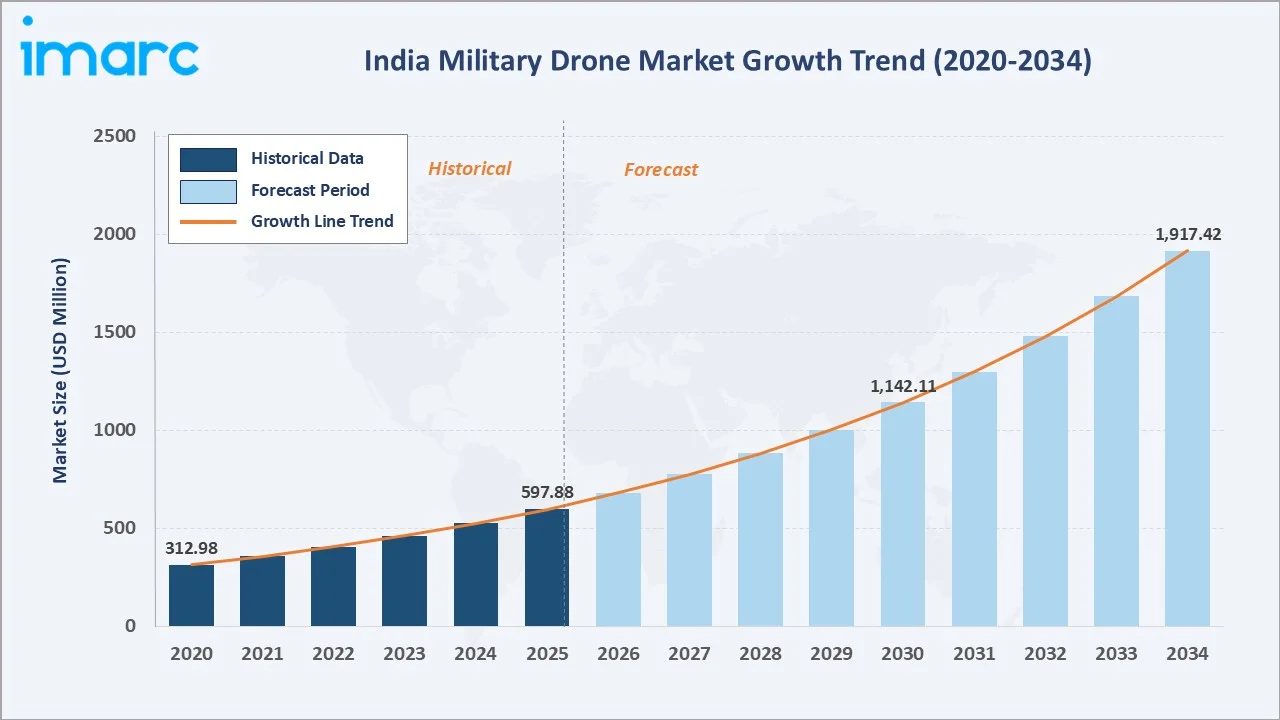

The India military drone market size reached USD 597.88 Million in 2025 and is projected to reach USD 1,917.42 Million by 2034, exhibiting a CAGR of 13.82% during 2026-2034. Rising geopolitical tensions, robust government defense modernization, and the Make in India initiative are the primary forces driving India military drone market growth.

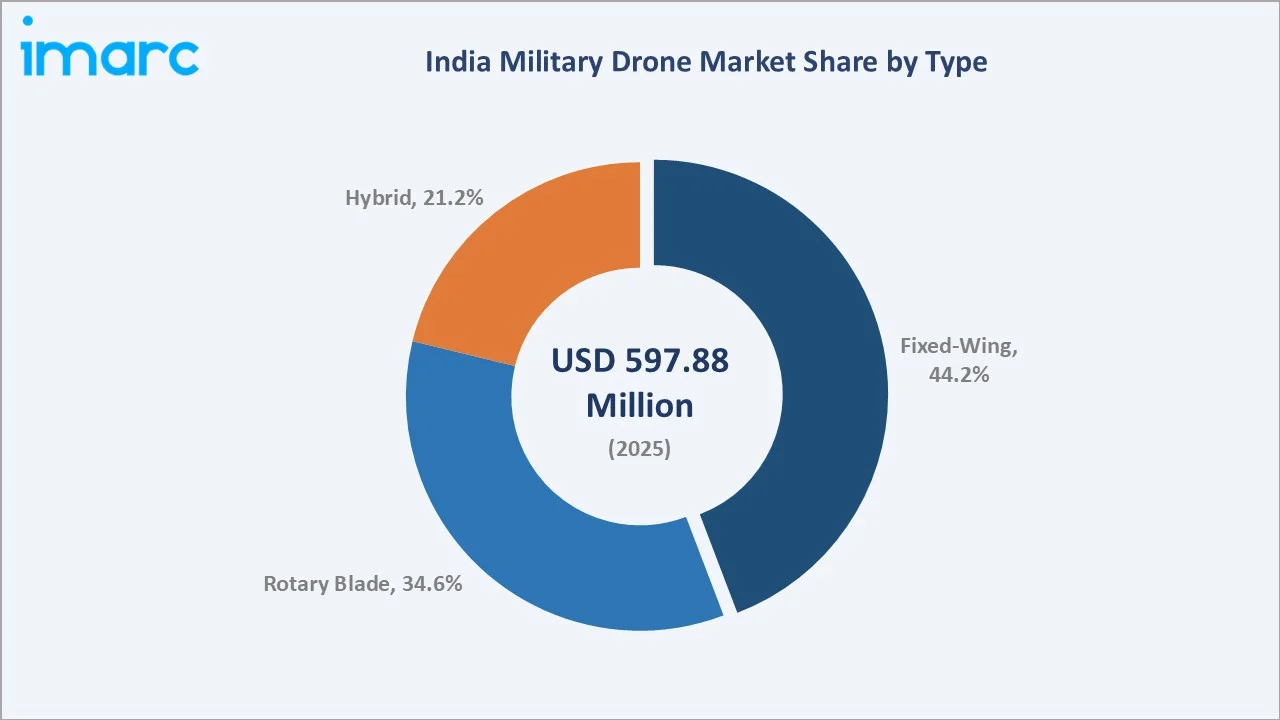

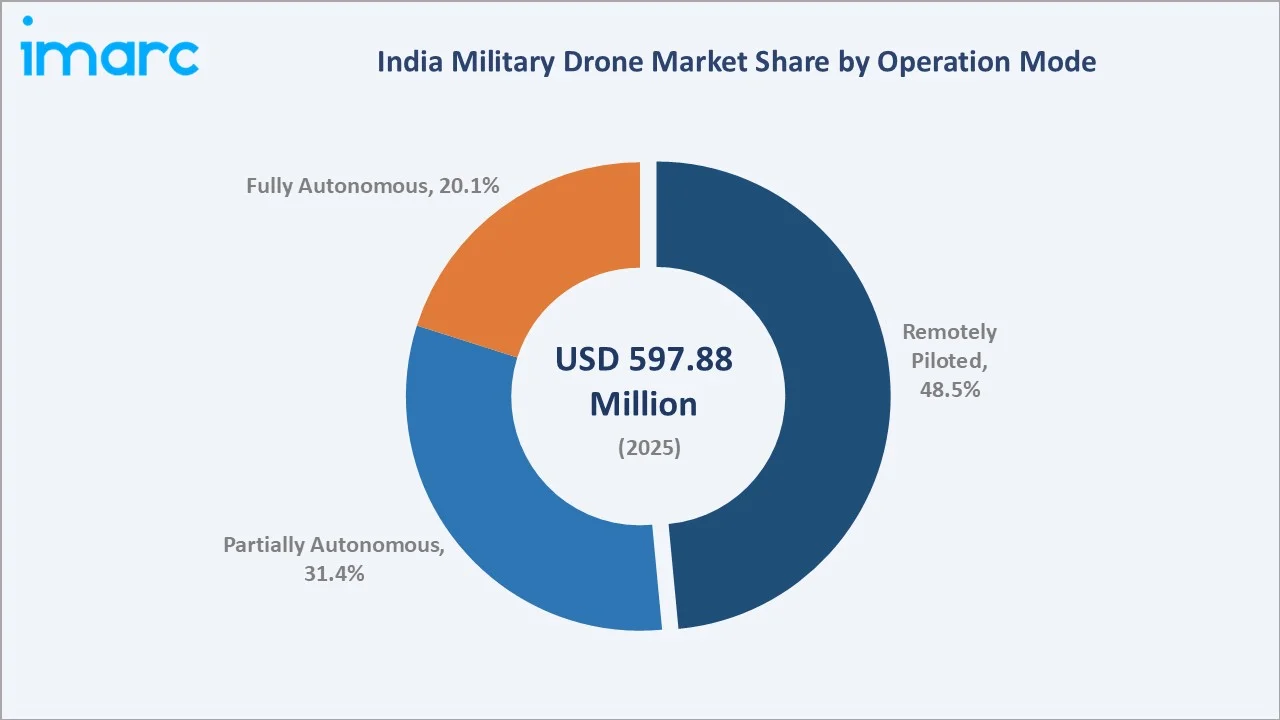

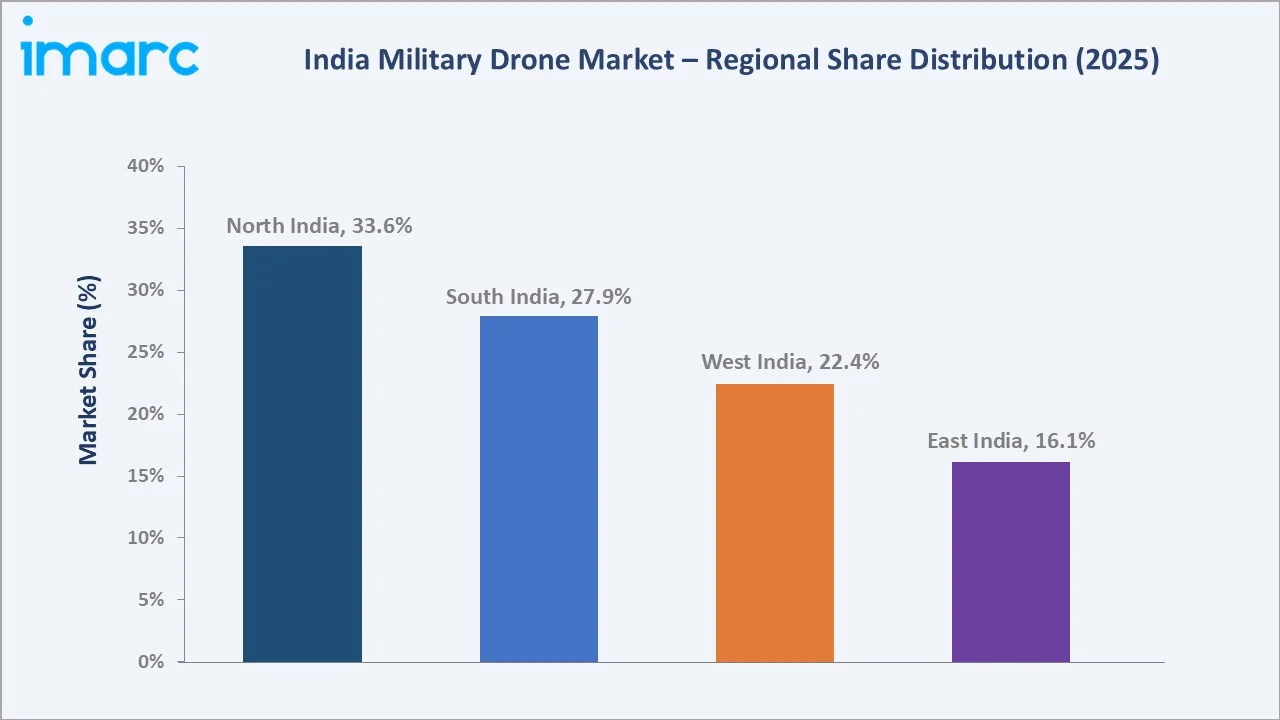

Fixed-wing drones dominate the type segment at 44.2% in 2025, while Remotely Piloted drones lead the operation mode at 48.5%. North India commands the largest regional share at 33.6% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 597.88 Million |

|

Forecast Market Size (2034) |

USD 1,917.42 Million |

|

CAGR (2026-2034) |

13.82% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (33.6% share, 2025) |

|

Second Largest Region |

South India (27.9% share, 2025) |

|

Leading Type |

Fixed-Wing Drone (44.2%, 2025) |

|

Leading Operation Mode |

Remotely Piloted (48.5%, 2025) |

The India military drone market growth trajectory from 2020 through 2034, with historical expansion to USD 597.88 Million in 2025, reflects accelerating defense procurement, while the forecast to USD 1,917.42 Million captures AI-driven autonomy investment, indigenous manufacturing scale-up, and border security imperatives.

To get more information on this market, Request Sample

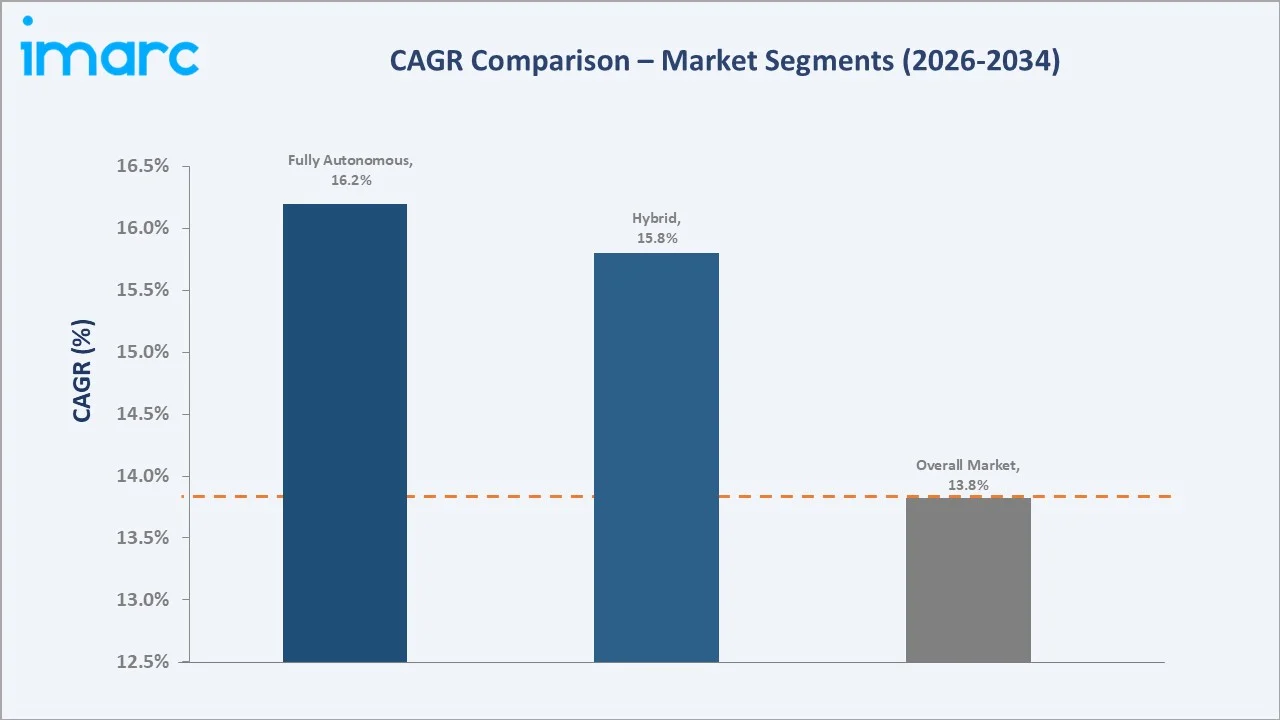

The CAGR trajectories across key type, operation mode, and regional sub-segments, with Fully Autonomous drones at ~16.2% CAGR and Hybrid drones at ~15.8% CAGR, are the fastest-growing categories within the India military drone industry analysis through 2034.

Executive Summary

The India military drone market is on a sustained growth trajectory from USD 597.88 Million in 2025 to USD 1,917.42 Million by 2034. Military drones, essential UAV platforms deployed across surveillance, reconnaissance, combat, and logistics missions, benefit from non-discretionary defense budget allocations and active border security requirements.

Fixed-wing drones dominate the type segment at 44.2% in 2025, owing to superior endurance and area coverage capabilities suited to long-range border surveillance and ISR missions. Hybrid drones (21.2%) represent the fastest-growing type at ~15.8% CAGR, combining VTOL flexibility with fixed-wing endurance for high-altitude multi-terrain operations.

Remotely Piloted systems lead operation mode at 48.5% in 2025, serving established tactical doctrine requirements. Fully Autonomous drones (20.1%) are the fastest-growing mode at ~16.2% CAGR, propelled by AI advances and the Indian Army's drive to reduce personnel exposure in high-threat border zones across the LAC and LoC.

North India dominates regionally at 33.6% in 2025, anchored by active border deployments across Ladakh, Jammu & Kashmir, Punjab, and Rajasthan. South India (27.9%) and West India (22.4%) follow, driven by naval maritime surveillance and coastal security drone procurement across the Indo-Pacific region.

Key Market Insights

|

Insight |

Data |

|

Largest Drone Type |

Fixed-Wing – 44.2% share (2025) |

|

Leading Operation Mode |

Remotely Piloted – 48.5% share (2025) |

|

Leading Region |

North India – 33.6% share (2025) |

|

Second Largest Region |

South India – 27.9% share (2025) |

|

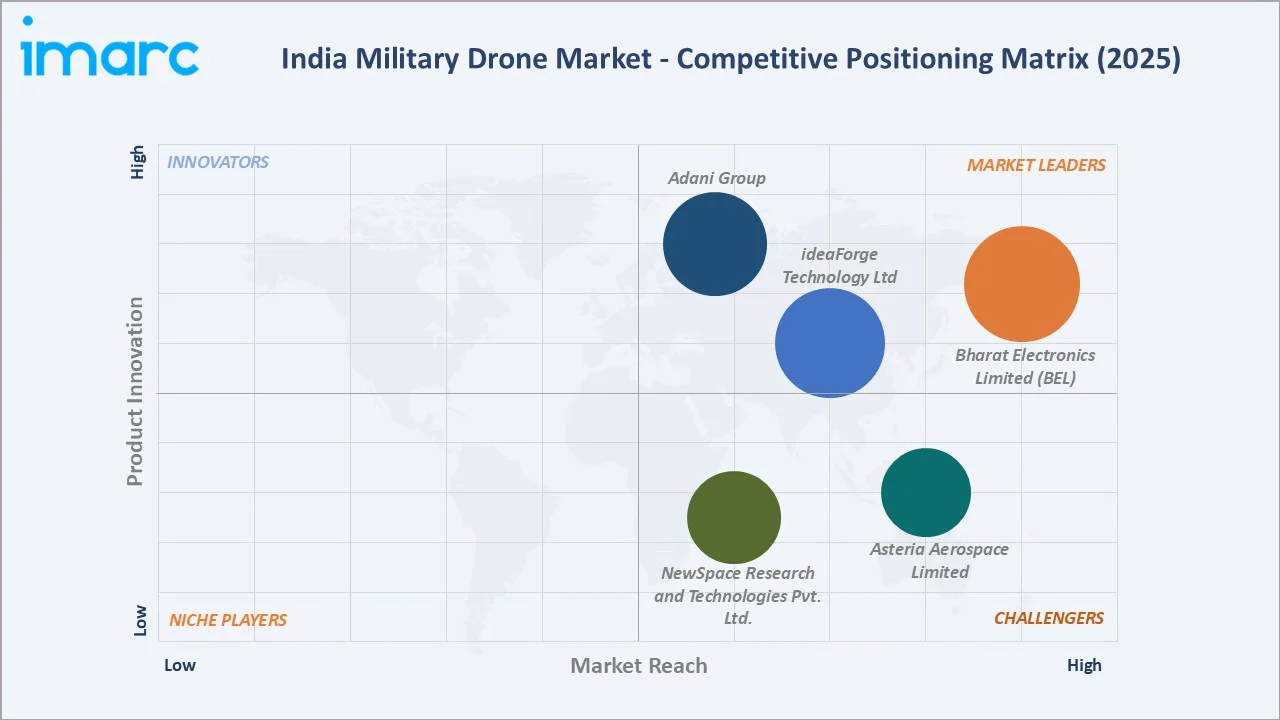

Top Companies |

Bharat Electronics Limited (BEL), ideaForge Technology Ltd, Adani Group, NewSpace Research and Technologies Pvt. Ltd., Asteria Aerospace Limited |

Key Analytical Observations Expanding on the Above Data:

- Fixed-wing drones, with 44.2% in 2025, dominate because of their superior endurance and range profile. For most border surveillance missions along the LAC with China and LoC with Pakistan, fixed-wing platforms maintain 12-24 hour loiter capability at altitudes up to 5,000 metres, making them operationally irreplaceable.

- Remotely Piloted systems, with 48.5% in 2025, lead operation mode because established military doctrine, radio-frequency link infrastructure, and trained operator cadres favor human-in-the-loop control for current Indian Army and Air Force tactical and strategic UAV deployments.

- North India's 33.6% dominance in 2025 reflects multiple structural forces: active deployment of drones along the Ladakh sector, Punjab border security, and Rajasthan desert surveillance, all generating large and sustained military procurement demand from the Northern and Western Army Commands.

- South India, with 27.9% in 2025, benefits from Indian Navy's Indo-Pacific maritime drone procurement, the expanding Southern Naval Command drone fleet, and coastal surveillance operations along the 7,500-kilometre peninsular coastline and Lakshadweep Islands.

India Military Drone Market Overview

A military drone is an unmanned aerial vehicle operated by armed forces for surveillance, reconnaissance, intelligence gathering, combat strike, logistics, and electronic warfare missions. Product configurations span fixed-wing MALE and HALE platforms, rotary-blade tactical UAVs, and hybrid VTOL systems with varying payload capacities and operational ranges.

India's military drone ecosystem integrates DRDO research laboratories, defense public sector undertakings, private indigenous manufacturers, global OEM technology transfer partners, ground control station developers, payload integrators, certification authorities, and MRO service providers, underpinned by government policy frameworks including PLI, iDEX, and the Defense Acquisition Policy 2020.

Market Dynamics

To evaluate market opportunities, Request Sample

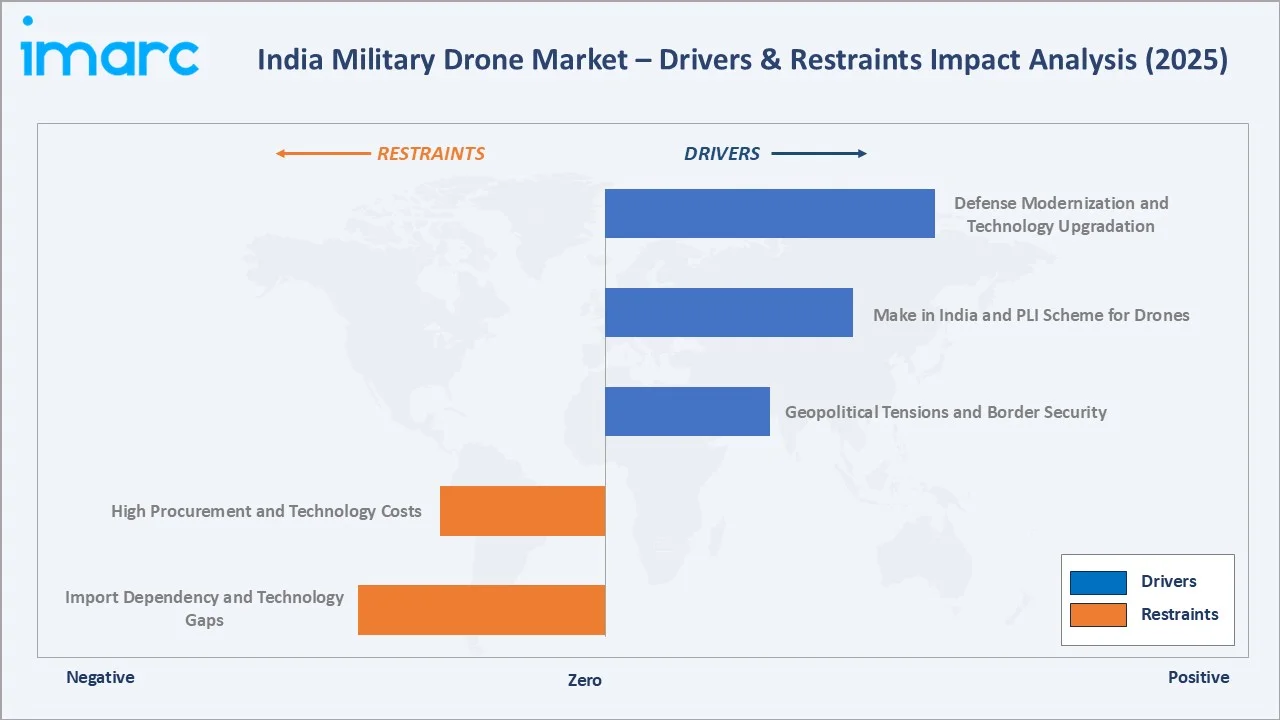

Market Drivers

- Geopolitical Tensions and Border Security: Persistent confrontations along the Line of Actual Control with China and the Line of Control with Pakistan drive sustained procurement of surveillance and combat UAVs. India's defense budget exceeded INR 6.21 trillion in FY2024-25, with dedicated UAV procurement allocations rising each year.

- Make in India and PLI Scheme for Drones: The Production Linked Incentive scheme provides a 20% incentive on incremental sales for drone manufacturers, accelerating domestic production capacity. The iDEX program with INR 498.78 Crore in cumulative funding through 2026 supports defense startup-led innovation across tactical UAV sub-systems.

- Defense Modernization and Technology Upgradation: The Indian Armed Forces' Technology Perspective and Capability Roadmap mandates integration of AI-enabled autonomous UAVs across all three services by 2030, driving procurement of next-generation platforms with swarm capability, BVLOS range, and AI-powered targeting.

Market Restraints

- High Procurement and Technology Costs: Advanced military drones, particularly MALE and HALE platforms requiring indigenous propulsion, advanced sensors, and secure data links, involve high per-unit costs of USD 2-15 Million, placing pressure on defense capital expenditure budgets despite rising overall allocations.

- Import Dependency and Technology Gaps: India remains dependent on foreign suppliers for critical drone sub-systems including advanced aero-engines, electro-optical and infrared sensors, and satellite communication terminals, creating supply chain vulnerability and limiting full indigenous MALE drone production timelines.

Market Opportunities

- AI-Powered Autonomous Drone Development: DRDO's earmarked INR 450 Crore for swarm drone technology and the Indian Army's active trials of AI-integrated tactical UAVs signal massive investment in next-generation autonomous platforms, creating high-value opportunities for domestic AI-defense technology companies.

- Export Potential Under Defense Export Policy: India's defense export target of INR 50,000 Crore by 2028-29 and the approved Drone Export Policy create opportunities for indigenous military drone manufacturers to address demand from friendly nations in Southeast Asia, Africa, and the Middle East.

Market Challenges

- Cybersecurity and Electronic Warfare Vulnerabilities: Military drones face growing risks from GPS jamming, signal spoofing, and cyber-intrusion by adversary electronic warfare systems, requiring expensive encrypted data links and anti-jamming navigation redundancy to maintain mission integrity in contested airspace environments.

- Skilled Workforce Gap in Drone Operations and MRO: India's rapid military drone expansion is constrained by a shortage of trained UAV operators, sensor analysts, and MRO-certified technicians across Army Aviation Corps and Navy drone squadrons, requiring substantial training infrastructure investment across all three services.

Emerging Market Trends

1. Swarm Drone Technology and Multi-UAV Operations

India has conducted 25+ official swarm drone trials, including multi-UAV operations covering 150 sq km in a single Ladakh mission. DRDO's INR 450 Crore swarm program is driving development of AI-coordinated autonomous multi-drone formations for saturation attack, distributed ISR coverage, and decoy operations.

2. BVLOS Operations and Extended Range Platforms

DGCA's issuance of BVLOS approvals for defense applications is enabling long-range drone operations beyond the visual line of sight for border patrol, maritime patrol, and deep reconnaissance missions. Rustom-II and TAPAS BH-201 represent India's indigenous MALE-class BVLOS platforms currently under phased induction.

3. AI Integration and Mission Autonomy Enhancement

Armed forces are integrating AI algorithms for real-time target recognition, path planning, and threat avoidance into tactical UAV mission computers. AI-powered EO/IR sensor fusion is enabling drones to operate in GPS-denied environments, as demonstrated in Operation Sindoor drone deployments in May 2025.

4. Indigenous Manufacturing Scale-Up Under PLI

Domestic drone manufacturing surged 35% YoY in 2024 under the PLI scheme. Companies like ideaForge, Garuda Aerospace, and Asteria Aerospace are scaling production facilities to fulfill large military tenders, reducing India's import dependence from approximately 70% in 2020 toward 40% by 2025.

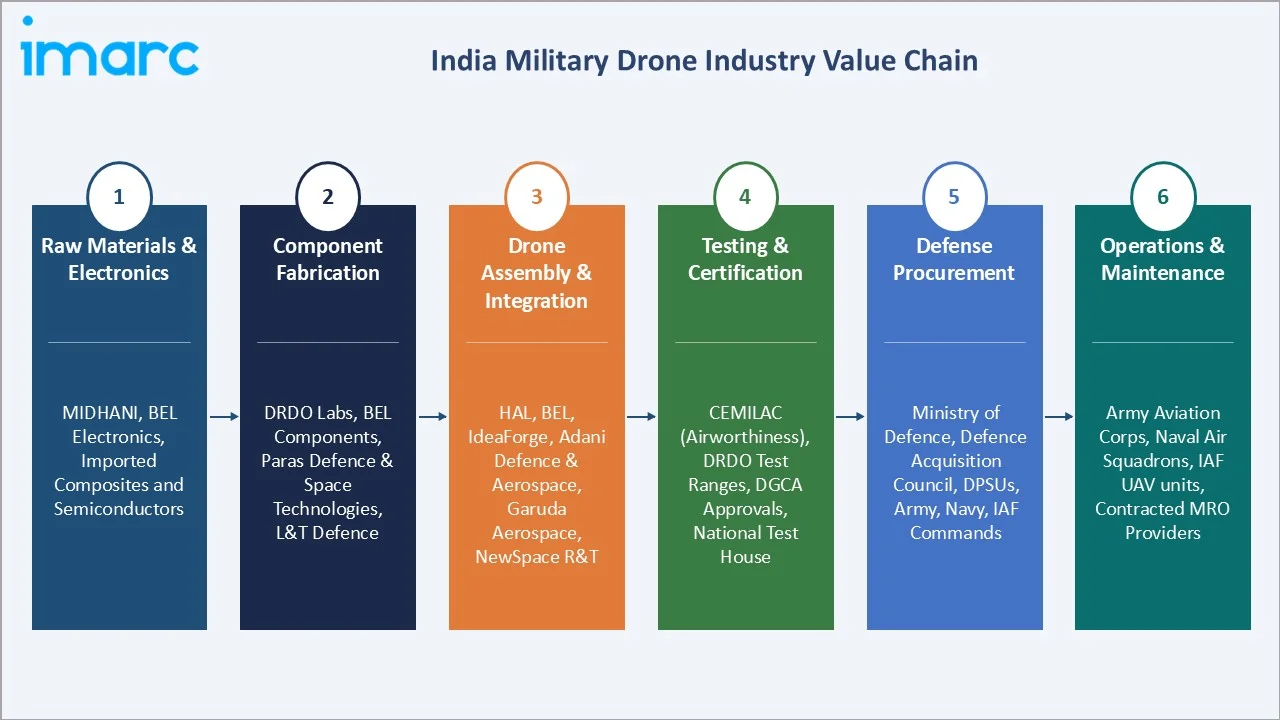

Industry Value Chain Analysis

The India military drone value chain spans six stages from raw materials through operational maintenance. Systems integration and AI software capture the highest value-add margins, while DRDO-driven R&D and government defense procurement generate the largest volume of strategic capital investment across the ecosystem.

|

Stage |

Key Players / Examples |

|

Raw Materials & Electronics |

MIDHANI, BEL Electronics, imported composites and semiconductors |

|

Component Fabrication |

DRDO production labs, BEL components division, Paras Defence & Space Technologies Limited, L&T Defence |

|

Drone Assembly & Integration |

HAL, BEL, ideaForge, Adani Defence & Aerospace, Garuda Aerospace, NewSpace R&T |

|

Testing & Certification |

CEMILAC (airworthiness), DRDO test ranges, DGCA approvals, National Test House |

|

Defense Procurement |

Ministry of Defence, Defence Acquisition Council, DPSUs, Army, Navy, IAF Commands |

|

Operations & Maintenance |

Army Aviation Corps, Naval Air Squadrons, IAF UAV units, contracted MRO providers |

Vertically integrated defense manufacturers like BEL, with captive PCB assembly and systems integration capabilities, achieve lower procurement risk than integrators relying entirely on imported sub-systems. Government offset policy mandates 30% indigenization in defense contracts, driving domestic supply chain development.

Technology Landscape in the India Military Drone Industry

Propulsion Technology: Electric, Hybrid, and Turboprop Platforms

Electric propulsion dominates small tactical drones for low acoustic signature and low operational cost. Turboprop engines power MALE-class platforms like Rustom-II. Hybrid propulsion systems combining fuel cells with lithium-polymer batteries are gaining specification for extended-endurance covert ISR platforms operating across the Himalayan high-altitude theatre.

Sensor and Payload Technology: EO/IR and SAR Integration

Modern military drones integrate multi-spectral electro-optical and infrared turrets with laser rangefinders and designators. Synthetic Aperture Radar payloads enable all-weather, day-night ground surveillance. India's DRDO has developed the PAWAN multi-mission sensor suite specifically designed for indigenous UAV platform integration.

Data Link and Communication: Encrypted and Anti-Jamming Systems

Military-grade encrypted data links with frequency-hopping spread spectrum technology protect drone command and control from jamming. Satellite communication data links enable BVLOS operations at extended ranges. DRDO's Software Defined Radio programs aim to indigenize secure data link sub-systems for all DRDO UAV platforms by 2027.

AI and Autonomy: Machine Learning for Target Recognition

Deep learning neural networks running on embedded GPU platforms enable real-time object detection, vehicle classification, and human activity recognition from drone-mounted EO/IR feeds without ground-link dependency. Operation Sindoor demonstrated GPS-denied autonomous navigation capability in contested electronic warfare environments.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Fixed-wing | 44.2% | 2025 |

| Operation Mode | Remotely Piloted | 48.5% | 2025 |

| Range | 🔒 | 🔒 | 2025 |

| Application | 🔒 | 🔒 | 2025 |

| Maximum Takeoff Weight | 🔒 | 🔒 | 2025 |

| End Use | 🔒 | 🔒 | 2025 |

| Region | North India | 33.6% | 2025 |

By Type

Fixed-wing drones command a 44.2% majority share in 2025 owing to their fundamental endurance and range advantage. Their operational profile makes them the default procurement specification for border surveillance, strategic reconnaissance, and maritime patrol missions across all three Indian Armed Forces services.

To access detailed market analysis, Request Sample

Rotary Blade drones at 34.6% in 2025 are irreplaceable in applications requiring vertical takeoff and precision hover for rapid deployment from forward operating bases, urban area surveillance, and ship-deck launch-and-recovery operations.

By Operation Mode

Remotely piloted drones dominate the operation mode segment at 48.5% in 2025, representing the largest installed base of UAVs operating under established human-in-the-loop doctrine across Army, Navy, and IAF tactical and strategic UAV squadrons with trained operator cadres.

Partially autonomous drones, with 31.4% in 2025, provide automatic takeoff, landing, and waypoint navigation with human override, reducing operator workload for long-duration ISR missions.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

33.6% |

LAC/LoC border deployments; Ladakh, J&K, Punjab active procurement |

|

South India |

27.9% |

Indo-Pacific surveillance; coastal security |

|

West India |

22.4% |

Rajasthan desert borders; Gujarat coastal patrol; Western Naval Command |

|

East India |

16.1% |

Northeast insurgency monitoring; Myanmar border; Bay of Bengal patrol |

North India's 33.6% market dominance in 2025 is driven by the most operationally intense combination of border threat intensity, terrain complexity, and large-scale military procurement activity. Following the 2020 Galwan Valley conflict, India accelerated drone procurement for the Ladakh sector, with swarm drone trials covering 150 sq km in a single mission.

South India, with 27.9% in 2025, is experiencing pronounced naval drone expansion. The Indian Navy's Maritime Domain Awareness initiatives, Indo-Pacific patrol commitments, and Lakshadweep and Andaman Island surveillance requirements generate sustained MALE-class drone procurement from the Southern and Eastern Naval Commands.

Competitive Landscape

The India military drone market is moderately fragmented, with DPSUs holding strong positions in large platform procurement, while private sector innovators dominate small tactical UAV supply under iDEX and COTS procurement pathways. The government's Make in India mandate is progressively shifting procurement toward domestic manufacturers.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Bharat Electronics Limited (BEL) |

Archer UAV |

Leader |

DPSU; full-spectrum UAV integration; systems integration |

|

ideaForge Technology Ltd |

Q6 V2 UAV, Q6 V2 GEO, NETRA 5, SWITCH V2, ZOLT, SWITCH |

Leader |

India's largest tactical UAV manufacturer |

|

Adani Group |

Vibhram, Alakh |

Leader |

Adani-Elbit JV; growing MALE-class capability |

|

NewSpace Research and Technologies Pvt. Ltd. |

Beluga, Nimbus, Mackerel, Nimbus-Scope |

Challenger |

iDEX winner; swarm autonomy specialization |

|

Asteria Aerospace Limited |

A200-XT, AT-15 |

Challenger |

Surveillance focus |

Key players include Bharat Electronics Limited (BEL), ideaForge Technology Ltd, Adani Group, NewSpace Research and Technologies Pvt. Ltd., Asteria Aerospace Limited, and others.

Key Company Profiles

Bharat Electronics Limited (BEL)

Bharat Electronics Limited is India's largest defense electronics DPSU, headquartered in Bengaluru. BEL integrates UAV platforms, ground control stations, EO/IR payloads, and data link systems, serving all three Indian Armed Services as the primary systems integrator for military drone programs.

- Product Portfolio: Archer UAV

- Recent Developments: In November 2022, Bharat Electronics Limited entered a memorandum of understanding with Aerosense Technologies Pvt Ltd to collaborate on the development and commercialization of drone and anti-drone systems. The partnership is aimed at leveraging the complementary strengths of both companies to jointly design and develop advanced unmanned aerial and soft-kill anti-drone solutions.

- Strategic Focus: BEL's drone strategy leverages its established DPSU defense contract relationships and systems integration expertise to position as the prime integrator for large-format military drone programs, while expanding its AI-enabled payload portfolio for next-generation ISR mission applications.

ideaForge Technology Ltd

ideaForge Technology is India's largest domestic drone manufacturer, specializing in tactical military and paramilitary UAVs. The company's drones are deployed by the Indian Army, CRPF, and state police forces for surveillance, border security, and disaster response operations nationwide.

- Product Portfolio: Q6 V2 UAV, Q6 V2 GEO, NETRA 5, SWITCH V2, ZOLT, SWITCH, and others

- Recent Developments: In August 2025, ideaForge Technology Limited received DGCA Type Certification for its SWITCH unmanned aerial system, marking a significant milestone that enables the deployment of its military-grade drone capabilities across civil, paramilitary, and enterprise applications. The certification validates the platform’s compliance with stringent safety and performance standards, supporting broader adoption among government bodies and commercial users.

- Strategic Focus: ideaForge focuses on scale manufacturing of certified tactical UAV platforms under PLI scheme benefits, targeting both Indian defense procurement and export opportunities to friendly nations across Southeast Asia and the Middle East, leveraging its DGCA-certified indigenous design advantage.

Adani Group

Adani Group operates via Adani Defence and Aerospace, bringing Israeli UAV technology into Indian manufacturing under Make in India mandate. The company is rapidly scaling its drone production capability to address Indian military MALE-class and combat drone procurement requirements.

- Product Portfolio: Vibhram, Alakh

- Recent Developments: In May 2025, The Adani Group strengthened India’s defense capabilities through the deployment of SkyStriker loitering munitions, marking a significant advancement in indigenous military technology. Developed under a collaboration between Adani Defence’s Alpha Design Technologies and Israel’s Elbit Systems, these drones were successfully used in a major military operation "Operation Sindoor", demonstrating precision strike capabilities and operational effectiveness.

- Strategic Focus: Adani Defense's strategy differentiates on large-scale manufacturing and capability in loitering munitions and armed UAV systems, targeting the higher-value combat drone segment where technology transfer from Elbit Systems provides a competitive advantage over purely indigenous competitors.

Market Concentration Analysis

The India military drone market is moderately fragmented, with DPSUs holding dominant positions in large-platform strategic procurement, while no single company holds more than 15-20% of total market revenue across all drone categories and procurement segments from the Ministry of Defense.

Consolidation at the tactical drone level is more advanced, with ideaForge commanding the largest share of small-format military UAV procurement under COTS and emergency procurement channels. The iDEX program has fragmented the competitive landscape by enabling 50+ defense startups to enter the military drone value chain as niche specialists.

Investment & Growth Opportunities

Fastest-Growing Segments

Fully Autonomous drones at ~16.2% CAGR through 2034 represent the highest-growth operation mode, driven by DRDO swarm drone programs and AI-integration investment. Hybrid-type drones at ~15.8% CAGR are the fastest-growing type segment, suited to high-altitude, multi-terrain operational requirements across all three services.

Emerging Markets

South India and East India represent the fastest-growing regions within the market. The Indian Navy's Indo-Pacific expansion, including the Andaman & Nicobar Command drone fleet build-up and Eastern Naval Command maritime patrol expansion, is generating rapidly growing procurement from these geographies through the forecast period.

Venture & Investment Trends

Venture capital and strategic investment in Indian defense drone startups reached record levels in 2024. iDEX DISC grants of up to INR 10 Crore and SPARK framework funding are catalyzing IP-driven startups in swarm AI, counter-UAV, and high-altitude drone systems. The defense export target is creating export-driven valuation upside for scale-ready manufacturers.

Future Market Outlook (2026-2034)

The India military drone market is forecast to expand from USD 597.88 Million in 2025 to USD 1,917.42 Million by 2034 at a CAGR of 13.82%, adding USD 1,319.54 Million in incremental annual market value over the forecast period. This robust growth reflects the market's defense-budget-linked, non-discretionary demand characteristics.

Three strategic forces will most significantly shape India's military drone industry through 2034: full indigenization of MALE-class drone platforms, AI-enabled autonomous swarm doctrine adoption, and the emergence of India as a defense drone exporter. DRDO's next-generation MALE UAV programs and HAL's CATS Warrior UCAV will define the high-value platform landscape.

Research Methodology

Primary Research

Primary research encompassed structured interviews with India military drone industry stakeholders, including defense procurement officials, UAV program managers at DPSUs, private manufacturer executives, DRDO scientists, and defense analysts. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include Ministry of Defense Annual Reports (2020-2025), DRDO Technology Focus publications, SIPRI Military Expenditure Database, DGCA drone regulation documentation, iDEX grant disclosures, Defense Acquisition Council procurement notices, and defense publications including Jane's Defence Weekly, Force India, and SP's MAI.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models incorporating India's defense budget growth trajectory, UAV procurement pipeline analysis, indigenization policy mandates, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed.

India Military Drone Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Fixed-wing, Rotary Blade, Hybrid |

| Operation Modes Covered | Remotely Piloted, Partially Autonomous, Fully Autonomous |

| Ranges Covered | Visual Line of Sight (VLOS), Extended Visual Line of Sight (EVLOS), Beyond Visual Line of Sight (BVLOS) |

| Applications Covered | Intelligence, Surveillance and Reconnaissance (ISR), Logistics and Supply, Others |

| Maximum Takeoff Weights Covered | <150 Kg, 150 - 1000 Kg, >1000 Kg |

| End Uses Covered | Air Force, Army, Navy |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Bharat Electronics Limited (BEL), ideaForge Technology Ltd, Adani Group, NewSpace Research and Technologies Pvt. Ltd., Asteria Aerospace Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India military drone market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India military drone market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India military drone industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Military Drone Market Report

The India military drone market reached USD 597.88 Million in 2025, reflecting consistent demand driven by geopolitical tensions, rising defense budget allocations, and the Make in India initiative accelerating indigenous UAV procurement.

The market is projected to reach USD 1,917.42 Million by 2034, growing at a CAGR of 13.82% during 2026-2034, driven by AI-enabled autonomous drone platforms, swarm technology investment, and multi-service UAV fleet expansion programs.

Fixed-wing drones lead the type segment with a 44.2% share in 2025, valued for their superior endurance and range, serving the majority of border surveillance, strategic reconnaissance, and maritime patrol missions across the Indian Armed Forces.

Remotely Piloted drones dominate with a 48.5% share in 2025, reflecting established human-in-the-loop military doctrine, trained operator infrastructure, and radio-frequency link investments across Army, Navy, and Air Force tactical UAV squadrons.

North India commands the dominant 33.6% market share in 2025, driven by active deployments along the Ladakh LAC with China and the J&K LoC with Pakistan, generating large-scale and sustained tactical and surveillance drone procurement from northern commands.

Hybrid drones are the fastest-growing type segment at ~15.8% CAGR through 2034, driven by the Indian military's demand for platforms combining VTOL flexibility with fixed-wing endurance for high-altitude multi-terrain operations, particularly in the Ladakh and northeastern theatres.

Leading companies include Bharat Electronics Limited (BEL), ideaForge Technology Ltd, Adani Group, NewSpace Research and Technologies Pvt. Ltd., Asteria Aerospace Limited, and others.

AI integration is enabling real-time target recognition, autonomous path planning, and GPS-denied navigation in tactical UAVs. DRDO's swarm drone program and Indian Army trials of AI-integrated platforms are accelerating autonomy adoption across ISR, strike, and logistics drone missions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)