India Mobile Accessories Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Region, 2026-2034

India Mobile Accessories Market Size, Share, Trends & Forecast (2026-2034)

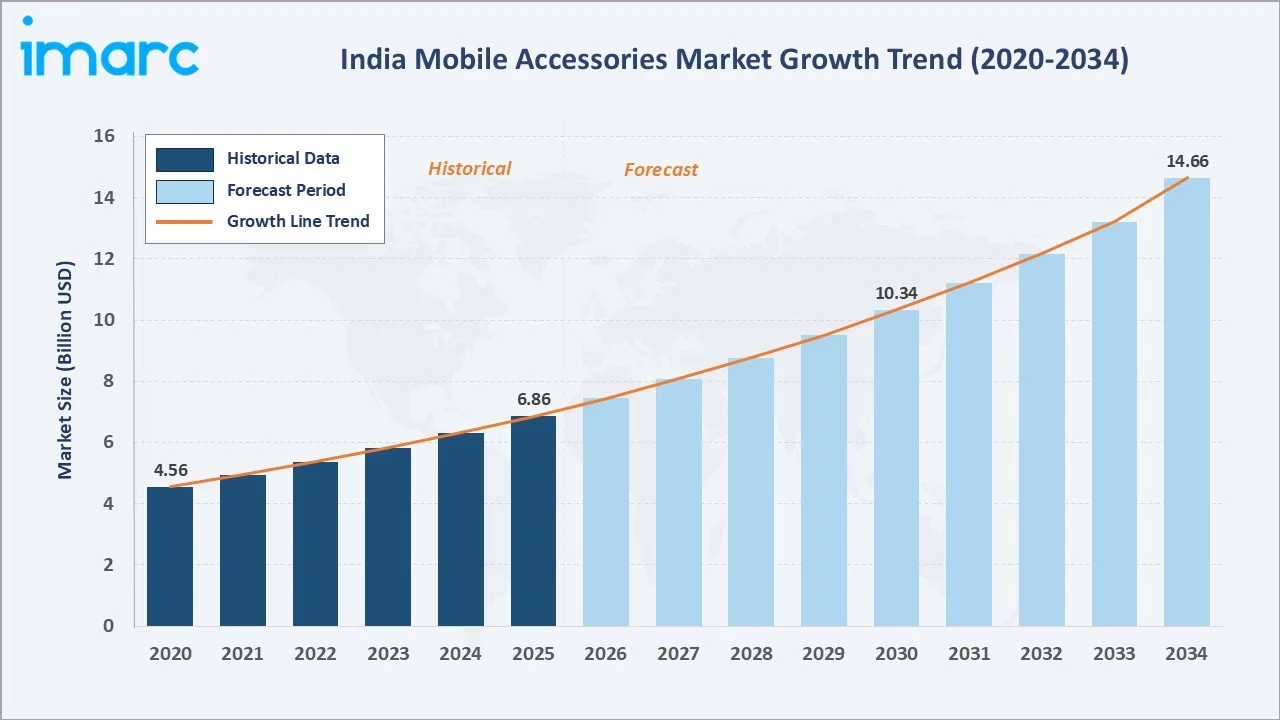

The India mobile accessories market reached USD 6.86 Billion in 2025 and is projected to reach USD 14.66 Billion by 2034, growing at a CAGR of 8.54% during 2026-2034. India's 1 billion smartphone user base by the end of 2026, 5G network rollout driving TWS headphone upgrade cycles, PLI scheme boosting domestic accessory manufacturing, rising disposable income fueling premiumization, and Flipkart-Amazon e-commerce penetrating Tier-2/3 cities anchor the market's sustained growth. Headphones lead the product type at 32.8%. Online channel leads at 58.4%. North India commands 29.7% of market revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.86 Billion |

|

Forecast Market Size (2034) |

USD 14.66 Billion |

|

CAGR (2026-2034) |

8.54% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Headphones (32.8%, 2025) |

|

Dominant Distribution Channel |

Online (58.4%, 2025) |

|

Leading Region |

North India (29.7%, 2025) |

The market expanded from USD 4.56 Billion in 2020 to USD 6.86 Billion in 2025, anchored at USD 10.34 Billion in 2030, and forecast to reach USD 14.66 Billion by 2034. COVID-19 lockdowns were transformative, forced work-from-home and online education, which created India's largest-ever single-year TWS headphone demand surge, while remote work power bank adoption and device protection case demand permanently elevated the market baseline.

To get more information on this market, Request Sample

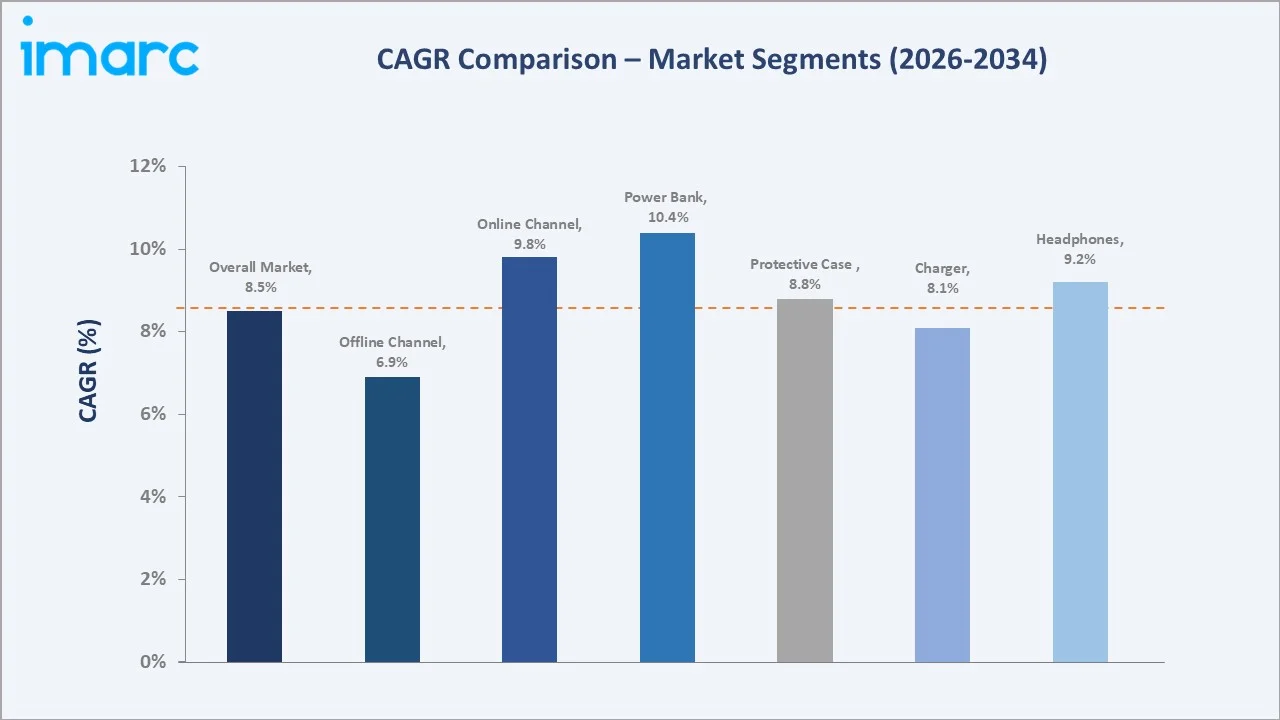

Power banks grow fastest at ~10.4% CAGR (2026-2034) as India's power infrastructure gaps in Tier-2/3 cities and rural areas create structural mobile power backup demand, the rural internet adoption creates first-time buyers of power banks, and fast-charging GaN power banks create premium upgrade cycles for existing power bank owners. Online channel grows at ~9.8% CAGR through Amazon and Flipkart's next-day delivery expansion to Tier-3 cities, social commerce reaching rural buyers, and quick commerce creating impulse purchase occasions for accessories in metro markets.

Executive Summary

The India mobile accessories market reached USD 6.86 Billion in 2025, establishing India as one of Asia's largest mobile accessories markets and the world's fastest-growing major accessories market by absolute demand addition. India's accessories market is structurally differentiated from mature markets, simultaneously serving the world's largest first-time buyer cohort, a rapidly premiumizing upgrade market, and India's emerging premium lifestyle segment. The market is projected to reach USD 14.66 Billion by 2034 at 8.54% CAGR.

Headphones at 32.8% lead as the market's highest-growth, highest-visibility product category. Online channel at 58.4% reflects India's digital commerce transformation, where Amazon's mobile accessories category and Flipkart's electronics leadership have created the most competitive consumer electronics marketplace in Asia. North India at 29.7% leads through Delhi NCR's wholesale hub and UP's massive consumer base.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Headphones - 32.8% share (2025) |

|

Dominant Distribution Channel |

Online - 58.4% market share (2025) |

|

Leading Region |

North India - 29.7% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Headphones at 32.8% driven by India becoming the world's third-largest TWS earphone market through disruptive value pricing: boAt's Airdopes, India's best-selling TWS earphone model, represents a market-creating product that made True Wireless Stereo (TWS) technology accessible at a price point below any comparable global market.

- Online at 58.4%, reflecting India's digital commerce dominance in electronics that exceeds any comparable major market: India's online mobile accessories channel has achieved a channel dominance unique among major consumer electronics markets globally. This dominance reflects India's specific retail evolution: limited organized offline electronics retail, a vast local mobile phone shop network that lacks the premium product range consumers seek, and Amazon/Flipkart's aggressive accessories category investment.

- North India at 29.7% anchored by Delhi's wholesale hub and UP-Rajasthan's massive first-time buyer market: Delhi's Nehru Place distributes mobile accessories to retail outlets across North, East, and Central India, making Delhi the logistical epicenter of India's offline accessories market.

India Mobile Accessories Market Overview

India's mobile accessories market encompasses all supplementary products and peripherals that enhance, protect, power, or extend the functionality of mobile smartphones. The market spans five primary categories: headphones and earphones, chargers, protective cases, power banks, and others (USB cables, screen protectors, car mounts, selfie sticks, gaming controllers, Pop Sockets).

The ecosystem integrates component manufacturers, India-based PLI assembly partners, domestic brands, international brands' India operations, BIS certification laboratories, a multi-tier distribution network, e-commerce platforms, and end consumers across Indian cities and towns served by delivery networks. Macroeconomic factors include rising smartphone penetration, expanding middle-class consumer spending, rapid growth of e-commerce platforms, increasing digital connectivity, and government support for electronics manufacturing.

Market Dynamics

To evaluate market opportunities, Request Sample

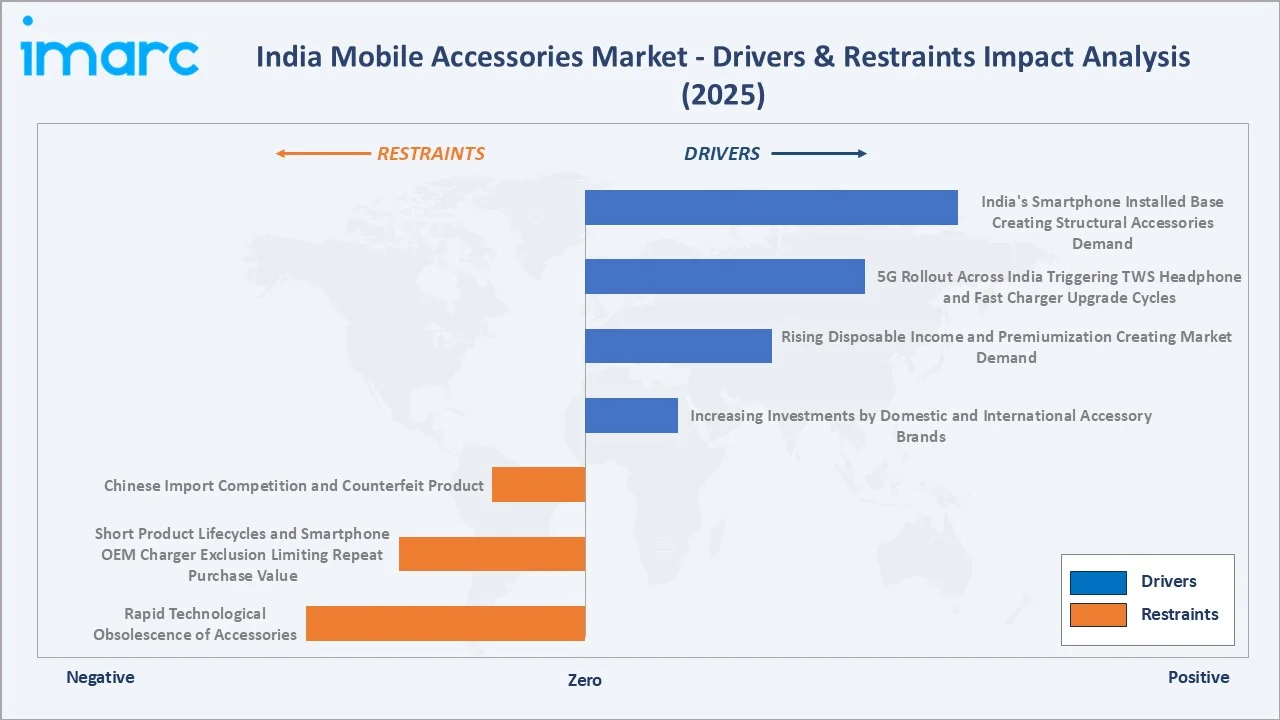

Market Drivers

- India's Smartphone Installed Base Creating Structural Accessories Demand: India's smartphone installed base is projected to reach 1 billion by the end of 2026, one of the world's largest smartphone user bases. Each incremental smartphone user requires a minimum accessories basket: charger, USB cable, and typically a protective case within the first 3 months of smartphone ownership. The upgrade cycle creates additional demand, creating a structural first-time accessories buyer market growing at above-market rates.

- 5G Rollout Across India Triggering TWS Headphone and Fast Charger Upgrade Cycles: India's 5G deployment is creating two distinct accessories upgrade waves. First, 5G smartphones eliminate the 3.5mm headphone jack, forcing users of wired earphones to transition to TWS or USB-C earphones, accelerating the TWS adoption curve. Second, 5G devices drain batteries 20-30% faster than 4G, creating urgent demand for fast-charging chargers and high-capacity power banks.

- Rising Disposable Income and Premiumization Creating Market Demand: India's per-capita GDP growth is creating a massive premiumization wave in mobile accessories, where consumers who began with basic accessories are progressively upgrading to feature-rich products. The corporate gifting market generates high annual branded accessories purchases, creating a premium demand channel independent of individual consumer purchasing.

Market Restraints

- Chinese Import Competition and Counterfeit Products: India's mobile accessories market faces sustained competitive pressure from Chinese imports. Chinese OEM accessories priced at INR 80-300 (earphones), INR 100-250 (chargers), and INR 50-150 (cases) compete in India's largest volume segment, where BIS certification is theoretically mandatory, but enforcement is inconsistent.

- Short Product Lifecycles and Smartphone OEM Charger Exclusion Limiting Repeat Purchase Value: India's smartphone OEM practice of removing box chargers creates a market opportunity but simultaneously commoditizes the charger category as consumers purchase third-party replacements rather than premium OEM chargers.

Market Opportunities

- Gaming Accessories Market as India's Fastest-Growing Mobile Accessories Sub-Category: India has become the world's most downloaded mobile gaming market with 8.45 billion downloads in FY2024-25, generating explosive demand for gaming-specific accessories that premium accessory brands are beginning to address.

- Corporate Gifting and Branded Merchandise Market Creating High-Margin B2B Accessories Revenue: India's corporate gifting market has adopted mobile accessories, particularly branded TWS earphones, branded power banks, and premium phone cases, as among India's most preferred corporate gifts for the festival season (Diwali), employee recognition, and client appreciation.

Market Challenges

- BIS Certification Enforcement Gap Allowing Substandard Products to Compete with Certified Brands: Bureau of Indian Standards (BIS) mandatory certification for chargers, power banks, and earphones in the Indian market is imperfectly enforced, an estimated 35-40% of mobile accessories sold through local mobile phone shops and small online sellers operate without proper BIS certification, creating unfair competition where uncertified products avoid the 5-8% compliance cost premium that BIS certification imposes on organized brands.

- E-Commerce Return Rates and Fake Review Ecosystem Undermining Consumer Trust in Online Channel: India's online mobile accessories channel faces a structural quality assurance challenge have created consumer trust deficits that 30-35% of Indian online shoppers cite as a concern when purchasing accessories from unfamiliar brands.

Emerging Market Trends

1. True Wireless Stereo Revolution Democratizing Premium Audio Across Income Segments

The rapid adoption of true wireless stereo (TWS) devices is emerging as affordable pricing, improved sound quality, and feature-rich offerings make premium audio experiences accessible across multiple income groups. Domestic and global brands are launching budget-friendly TWS earbuds with noise cancellation, gaming modes, and voice assistant integration, accelerating mass-market penetration in both urban and semi-urban regions. In January 2026, boAt Lifestyle expanded its affordable audio portfolio with the introduction of the Nirvana Crown TWS earbuds, featuring a charging case equipped with Sonic A.R.C (Advanced Rotational Crown) technology. The system integrates a rotating control dial with haptic feedback, multifunction controls, and customizable RGB lighting features to enhance the user experience.

2. GaN Fast Charging Technology Transforming Charger Premium Market

Gallium Nitride (GaN) fast charging technology enables compact, energy-efficient, and high-speed charging solutions for smartphones, laptops, and wearable devices. In February 2026, Xiaomi expanded its charging accessories portfolio in India with the introduction of the compact 45W Mini-GaN Charger, strengthening its presence in the fast-charging solutions segment. Consumers are increasingly shifting toward premium multi-device fast chargers with higher power output, portability, and advanced thermal efficiency, encouraging brands to expand their GaN-based charging portfolios across online and retail channels.

3. Protective Cases Evolving from Protection to Personal Expression

Protective smartphone cases in India are increasingly evolving from basic safety accessories into fashion and lifestyle products that reflect personal identity and style preferences. Consumers, particularly younger demographics, are driving demand for customized, designer, transparent, rugged, and themed cases featuring premium materials, artistic designs, and influencer-led aesthetics, encouraging brands to expand personalization-focused product offerings.

4. TWS and Headphone Ecosystem Extension - Smart Wearables Integration

India's leading audio accessory brands are evolving beyond standalone products toward health-integrated smart devices. boAt's smartwatch ecosystem is cross-selling with boAt TWS through ecosystem app integration. This ecosystem extension creates accessory replacement bundling (consumers upgrading both TWS and smartwatch simultaneously) that will sustain higher average transaction values and cross-category purchase frequency through 2034.

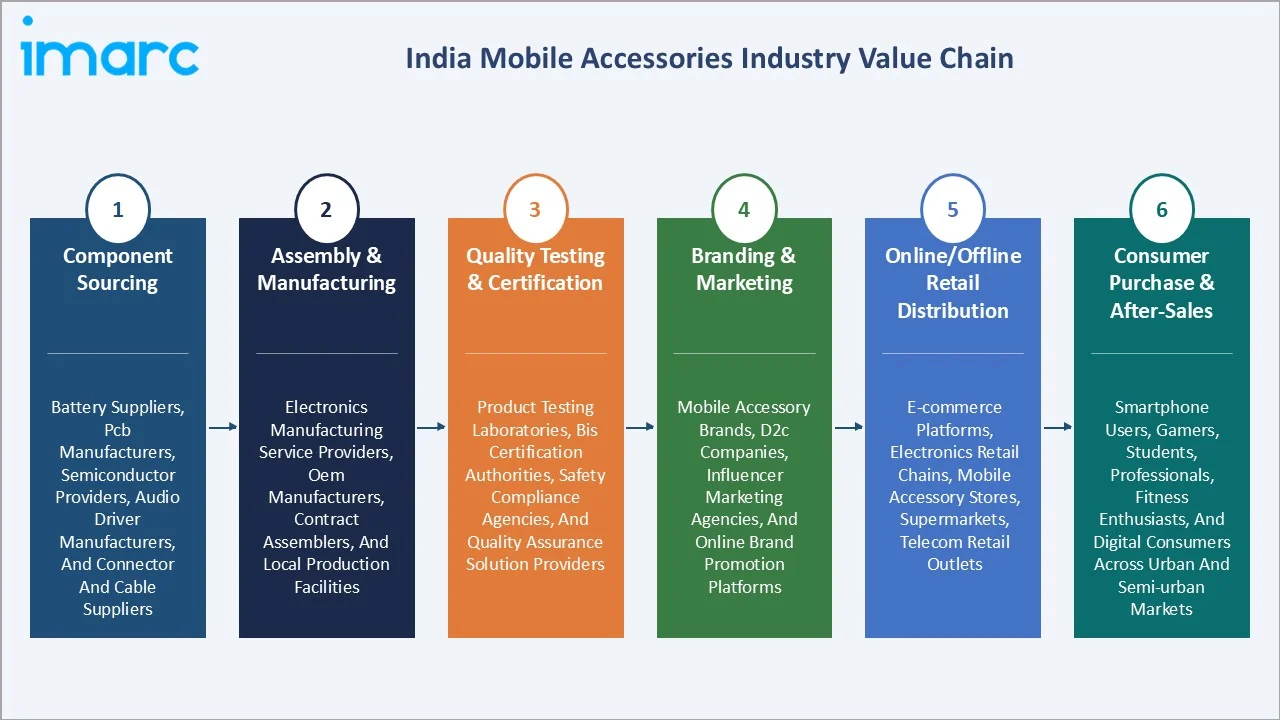

Industry Value Chain Analysis

India's mobile accessories value chain integrates component sourcing from China and emerging India manufacturing, quality certification, brand and marketing development, multi-channel distribution, and end consumer purchase with after-sales service. Branded domestic manufacturers earn 35-50% gross margins on products where brand premium justifies pricing above manufacturing cost. International premium brands earn 45-60% gross margins.

|

Stage |

Key Participants |

|

Component Sourcing |

Battery suppliers, PCB manufacturers, semiconductor providers, audio driver manufacturers, and connector and cable suppliers |

|

Assembly & Manufacturing |

Electronics manufacturing service providers, OEM manufacturers, contract assemblers, and local production facilities |

|

Quality Testing & Certification |

Product testing laboratories, BIS certification authorities, safety compliance agencies, and quality assurance solution providers |

|

Branding & Marketing |

Mobile accessory brands, D2C companies, influencer marketing agencies, and online brand promotion platforms |

|

Online/Offline Retail Distribution |

E-commerce platforms, electronics retail chains, mobile accessory stores, supermarkets, telecom retail outlets |

|

Consumer Purchase & After-Sales |

Smartphone users, gamers, students, professionals, fitness enthusiasts, and digital consumers across urban and semi-urban markets |

The brand and marketing tier is India's mobile accessories value chain's most competitively dynamic element. This marketing investment is disproportionate relative to global accessories markets, reflecting India's extreme brand-building sensitivity, where a single IPL cricket broadcast spot generates the brand recall of equivalent FMCG advertising, making India's accessories market more brand-driven than any comparable emerging market.

Technology Landscape in the India Mobile Accessories Industry

Bluetooth SoC Technology Evolution in TWS Earphones

Bluetooth System-on-Chip (SoC) technology evolution enables TWS earphones with improved connectivity, lower power consumption, enhanced audio processing, and AI-powered features. Advanced Bluetooth chipsets are supporting functionalities such as active noise cancellation, low-latency gaming modes, spatial audio, and seamless multi-device pairing, driving innovation across premium and affordable audio segments.

GaN (Gallium Nitride) Semiconductor Revolution in Charging Technology

GaN (Gallium Nitride) semiconductor technology enables smaller, faster, and more energy-efficient charging devices. The adoption of GaN-based chargers is supporting high-power fast charging, multi-device compatibility, reduced heat generation, and compact portable designs, encouraging brands to expand premium charging accessory portfolios across the Indian market.

ANC (Active Noise Cancellation) Technology Democratization

The democratization of Active Noise Cancellation (ANC) technology is making premium audio experiences accessible across mid-range and budget TWS and headphone segments. In February 2026, Samsung Electronics launched Galaxy Buds4 Pro and Galaxy Buds4 in India for pre-orders, introducing advanced hi-fi audio capabilities and improved everyday comfort. The Galaxy Buds4 Pro features a newly designed wider woofer, enhanced Active Noise Cancellation (ANC), and an upgraded Adaptive Equalizer (EQ) to deliver audio performance closer to the original sound recording.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Headphones |

32.8% |

2025 |

|

Distribution Channel |

Online |

58.4% |

2025 |

|

Region |

North India |

29.7% |

2025 |

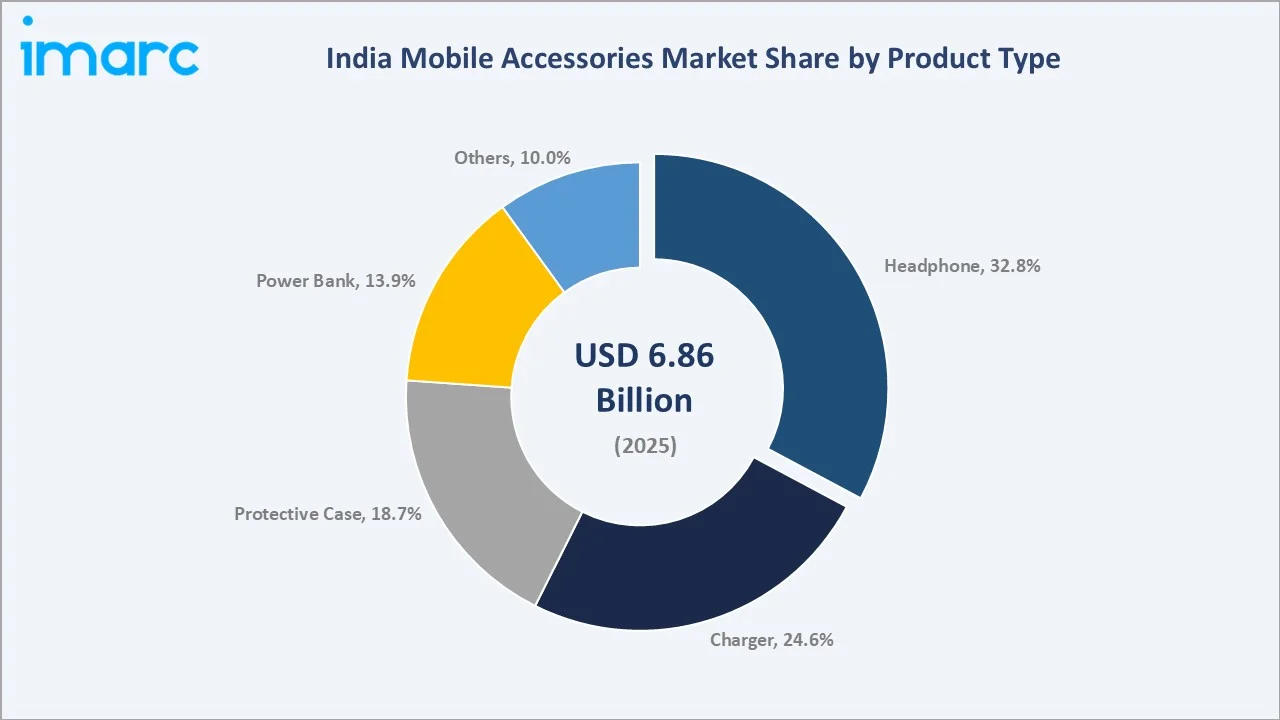

By Product Type

Headphones lead at 32.8% market share (2025). India's headphone market spans five sub-categories: TWS earphones, wired earphones, neckband wireless, over-ear wireless, and gaming headphones. India's TWS earphone shipments are making India the world's third-largest TWS market after China and the USA.

To access detailed market analysis, Request Sample

Chargers at 24.6% serve every new smartphone sale through bundled and replacement purchases. Protective cases at 18.7% represent India's most volume-intensive accessory category. Power banks at 13.9% grow fastest at ~10.4% CAGR through rural infrastructure-driven demand and urban fast-charging upgrades. Others at 10.0% encompasses USB cables, screen protectors, car mounts, gaming controllers, smartwatch bands, and wireless charging pads.

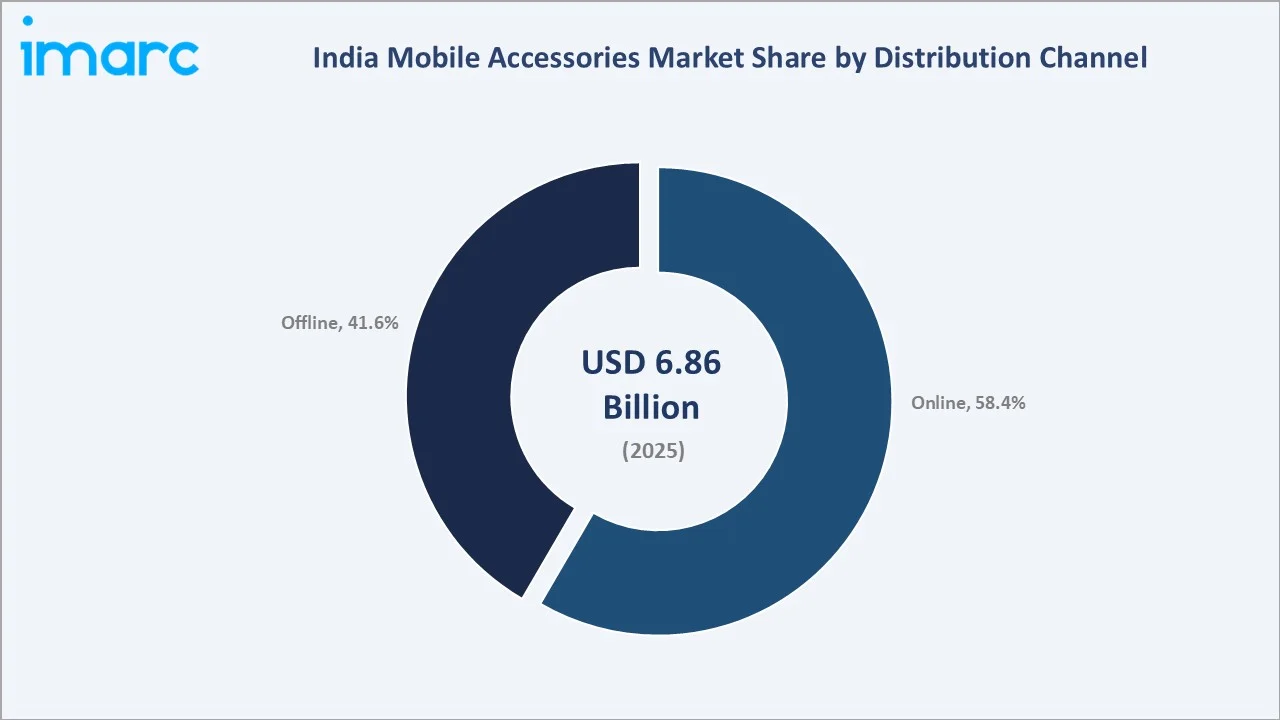

By Distribution Channel

Online channel leads at 58.4% market share (2025). Amazon India and Flipkart collectively account for 45-48% of India's total mobile accessories revenues, an online channel concentration unprecedented in any major consumer electronics market globally. Amazon India's mobile accessories category benefits from Prime delivery, Amazon's Choice certification for best-in-class accessories, and A+ content pages enabling brand storytelling that drives premium purchase conversion. Flipkart's Big Billion Days and Amazon Great Indian Festival each generate high sales in accessories in 5-7 day events.

Offline channel at 41.6% encompasses India's local mobile phone accessory shops, modern trade electronics chains, brand exclusive stores, telecom retail stores, and D-Mart/Big Bazaar basic accessories sections.

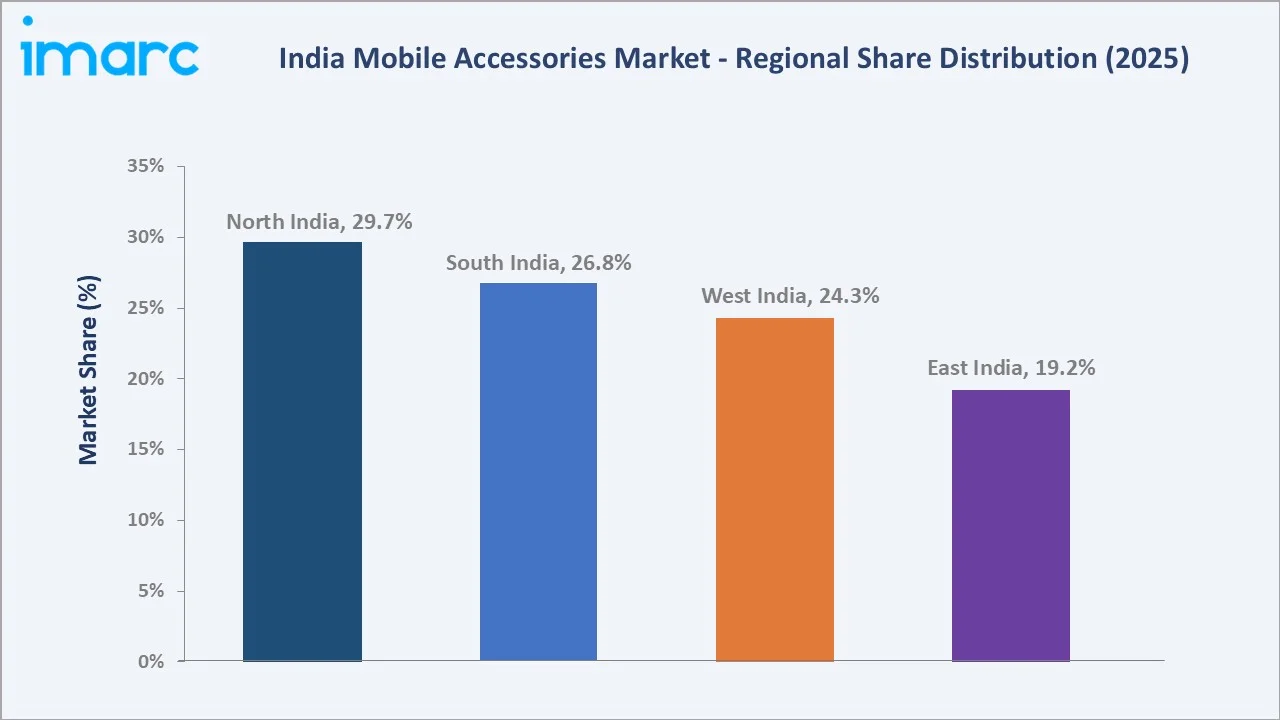

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

North India |

29.7% |

High smartphone penetration, strong retail distribution networks, expanding e-commerce adoption, and large urban consumer bases across major metropolitan cities. |

|

South India |

26.8% |

Driven by high digital literacy, strong technology sector presence, premium consumer spending patterns, and rising adoption of smart audio and wearable accessories. |

|

West India |

24.3% |

Strong urbanization, growing organized retail infrastructure, rising disposable incomes, and increasing demand for premium mobile and gaming accessories. |

|

East India |

19.2% |

Supported by expanding internet connectivity, rising smartphone adoption in tier-2 and tier-3 cities, and increasing affordability of mobile accessories. |

North India's 29.7% market leadership is structurally anchored by Delhi's dual role as India's largest accessories wholesale hub and one of India's highest per-capita digital consumer markets. Delhi's wholesale markets supply accessories to retailers across North and Central Indian states, making North India's logistics infrastructure the de facto supply chain backbone for India's offline accessories market.

South India's 26.8% reflects Bengaluru's premium consumer density and Tamil Nadu-Kerala's high consumer electronics literacy. West India's 24.3% is anchored by Mumbai's financial capital consumer base and Maharashtra-Gujarat's corporate gifting demand. East India's 19.2%, while the lowest, is growing fastest at 12%+ annually as Kolkata's wholesale hub expands distribution across East India's population, Jio's rural 4G penetration drives smartphone adoption, and social commerce reaches accessory buyers in villages and small towns that organized retail and e-commerce have not previously served.

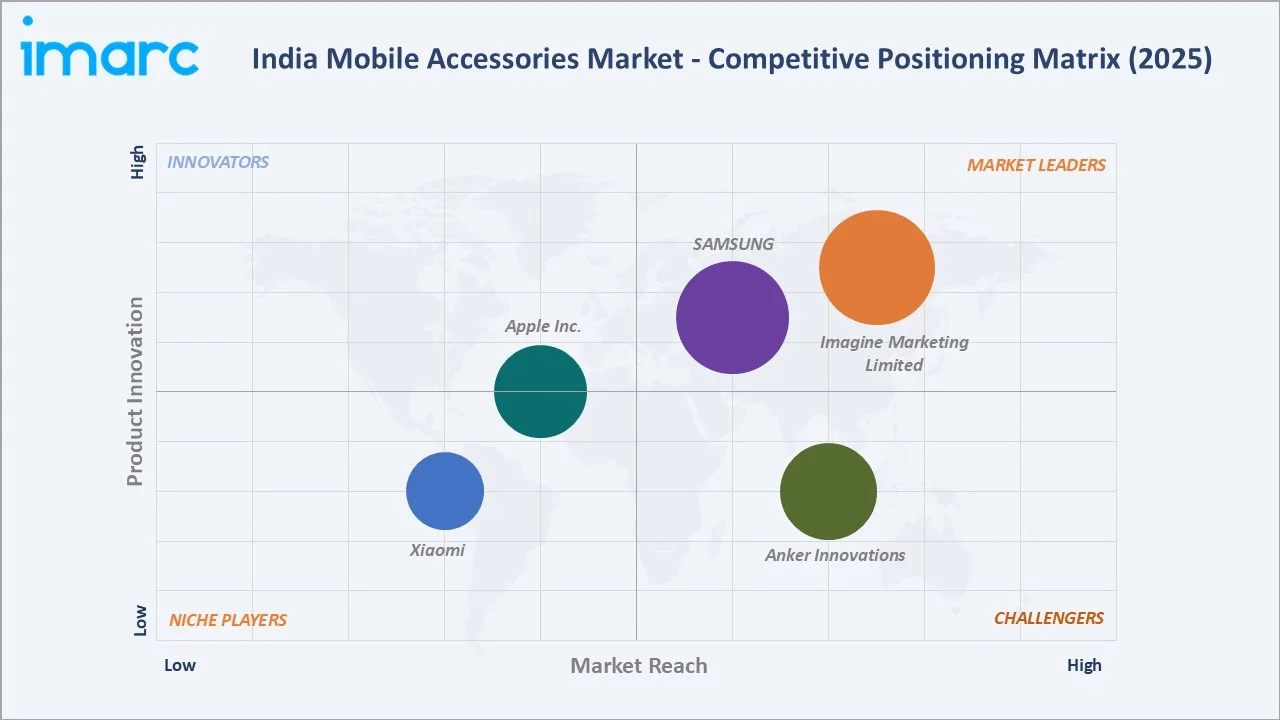

Leading Mobile Accessories Companies in India

India's mobile accessories market exhibits moderate concentration at the brand level with very high concentration in specific categories. boAt and Samsung together command approximately 45-50% of India's TWS earphone market. Chargers are more fragmented. Protective cases are the most fragmented category with no single brand holding more than 10% market share in a market where 1,000+ brands, from premium Casetify to unbranded local manufacturers, compete.

|

Company Name |

Key Brands |

Market Position |

Core Strength |

|

Imagine Marketing Limited |

boAt |

Market Leader |

boAt is a leading Indian consumer electronics and mobile accessories brand known for its affordable audio products, wearables, chargers, and lifestyle-focused smart accessories. |

|

SAMSUNG |

Samsung |

Market Leader |

Samsung is offering premium and mid-range audio devices, chargers, wearables, and ecosystem-integrated smartphone accessories. |

|

Anker Innovations |

Anker, soundcore |

Strong Challenger |

Anker Innovations is a global smart hardware technology company driven by ultimate innovation. |

|

Apple Inc. |

Apple |

Established Player |

Ecosystem-integrated products, such as AirPods, MagSafe chargers, Apple Watch accessories, and premium protective cases among high-end smartphone consumers. |

|

Xiaomi |

Redmi, Xiaomi |

Niche Player |

Founded in April 2010 as a consumer electronics and smart manufacturing company with smartphones and smart hardware connected by an IoT platform at its core. |

The competitive landscape is defined by India's unique brand phenomenon. boAt's rise from startup to India's #1 wearable audio brand demonstrates India's ability to build globally competitive consumer electronics brands through digital-native D2C marketing, supply chain optimization, and celebrity association.

Key Company Profiles

Imagine Marketing Limited

Imagine Marketing Limited is the parent entity of boAt, a leading Indian consumer electronics and lifestyle brand specializing in audio devices, wearables, chargers, and mobile accessories. boAt is India's undisputed #1 mobile accessories brand, transforming from a Kickstarter-style startup to India's most-recognized consumer electronics brand in less than a decade.

- Brands: boAt

- Recent Developments: In August 2024, boAt announced that its cumulative production of ‘Made in India’ products surpassed the 5-crore milestone, doubling from the previously reported 2.5 crore locally manufactured units.

- Strategic Focus: Expanding affordable premium audio and wearable products, strengthening local manufacturing, enhancing AI-driven audio innovation, and building ecosystem-based smart accessories for India’s digitally connected consumers.

SAMSUNG

Samsung India Electronics is India's largest consumer electronics company and the country's #2 mobile accessories brand, with the structural advantage of selling accessories to Indian smartphone users who are already in Samsung's ecosystem.

- Brands: Samsung

- Recent Developments: In December 2025, Samsung expanded its partnership with Swiggy Instamart in India for the ultra-fast doorstep delivery option for Galaxy devices, including chargers, smartwatches, tablets, and wireless earbuds.

- Strategic Focus: Expanding its ecosystem-driven mobile accessories portfolio through premium audio devices, wearable integration, fast-charging technologies, and AI-enhanced connected consumer experiences in India.

Market Concentration Analysis

India's mobile accessories market exhibits category-specific concentration patterns with an overall moderate Herfindahl-Hirschman Index (HHI) reflecting both branded and unbranded competition coexisting. TWS earphones show the highest concentration, driven by effective brand building and e-commerce optimization that created switching costs through ecosystem apps and consumer brand loyalty. Power banks show moderate concentration with a significant unbranded segment. Chargers are the least concentrated organized market due to commodity perception and certification enforcement, creating a level playing field among certified brands, while unbranded, uncertified products compete on price.

The market's concentration at the D2C digital brand level disguises significant fragmentation at the product supply level. This means that the barriers to creating a new competing brand are lower than boAt's apparent market dominance suggests. International brand concentration at the premium tier creates a two-tier concentration structure, domestic brands dominating the mid-market while international brands defend premium market share through technological differentiation that India's domestic brands are progressively but not yet fully matching.

Investment & Growth Opportunities

Fastest Growing Segments

Power banks (~10.4% CAGR), headphones (~9.2% CAGR), online channel (~9.8% CAGR), gaming accessories sub-category (~35%+ CAGR from small base), ANC TWS mid-premium segment (~25% CAGR within headphone category), East India regional market (~12%+ CAGR), and premium GaN chargers (~30%+ CAGR within charger category) represent India's highest-growth mobile accessories investment vectors through 2034.

Emerging Market Opportunities

India's rural power bank market represents the most underserved accessories opportunity. Rural smartphone users experiencing power outages have a structural need for mobile power backup. A BIS-certified, affordable power bank brand targeting India's rural market through social commerce and retail networks could build high revenues in the rural power bank market with no organized branded competitor.

Investment Themes

- Gaming accessories as India's next D2C brand creation opportunity: India's mobile gamers represent a dedicated accessories buyer segment requiring specialized products (gaming controllers, low-latency TWS gaming earphones, gaming power banks with pass-through charging, gaming chairs with headphone integration) that no current India brand serves comprehensively.

- East India wholesale and distribution expansion: Kolkata's Fancy Market and SP Mukherjee Road wholesale ecosystem serves East India's accessories market with significantly less organized distribution investment than North India's Nehru Place ecosystem. An organized accessories distributor establishing C&F networks across West Bengal, Odisha, Jharkhand, Assam, and Northeast India can capture first-mover distribution advantages in India's fastest-growing regional accessories market, where organized penetration currently lags 3-5 years behind North and South India distribution infrastructure.

Future Market Outlook (2026-2034)

The India mobile accessories market is projected to grow from USD 6.86 Billion in 2025 to USD 14.66 Billion by 2034, delivering an 8.54% CAGR over the forecast period. The market's anchor value of USD 10.34 Billion in 2030 represents an Indian mobile accessories industry where TWS headphone penetration is high in India's active smartphone users, ANC technology has become standard at the lower price point rather than premium, and PLI-enabled domestic manufacturing has shifted 40-50% of accessories production from import-dependent to India-assembled, establishing India as one of the Asia's largest mobile accessories manufacturing base.

Three structural forces define India's mobile accessories market growth through 2034 with high confidence: India's smartphone installed base creates a proportional accessories market expansion; the premiumization wave converting India's existing accessory buyers from INR 200-500 average spend to INR 800-2,500 average spend as 5G adoption, rising incomes, and brand education systematically upgrade accessory quality expectations; and India's domestic brand ecosystem building globally competitive brands that capture value within India's accessories market rather than remitting it to Chinese OEM manufacturers.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including VP Sales and Product Directors; category buyers from Amazon India (Mobile Accessories), Flipkart (Electronics), and Croma (Infiniti Retail); BIS certification officials; CEAMA (Consumer Electronics and Appliances Manufacturers Association) industry data; distribution network representatives from North (Delhi Nehru Place), South (Chennai SP Road), West (Mumbai Heera Panna), and East (Kolkata Fancy Market) wholesale markets; and consumer interviews with 150+ mobile accessories buyers across Tier-1, Tier-2, and Tier-3 cities.

Secondary Research

Secondary research encompassed IDC India Quarterly Mobile Accessories Tracker Q4 2025, GfK India Consumer Electronics Market Share Data 2025, Amazon India Best Seller lists (Mobile Accessories category, 12-month analysis), Flipkart Electronics Category Report 2025, company annual reports, BIS Quality Control Order notifications for mobile accessories, Ministry of Electronics and IT PLI scheme disbursement reports, Meesho Seller Report 2025, CMIE Consumer Expenditure Survey mobile accessories data, and India Wireless Headphone Market report (IDC). Over 75 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up product type and distribution channel models calibrated against IDC India mobile accessories quarterly tracker data, Amazon and Flipkart category GMV growth rates, BEE certification volume data for chargers and power banks, India smartphone shipment data (IDC India Quarterly Smartphone Tracker), and income elasticity models for accessories spending based on Indian household consumption survey data. Key inputs include India smartphone installed base growth projections, 5G subscriber adoption curve (TRAI data), PLI scheme manufacturing capacity addition timelines, e-commerce penetration growth in Tier-2/3 cities (India Internet Report 2025), and premium accessories market growth correlation with per-capita income growth in India's top-100 urban centers.

India Mobile Accessories Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Headphone, Charger, Power Bank, Protective Case, Others |

| Distribution Channels Covered | Online, Offline |

| Regions Covered | North India, South India, East India, West India |

| Companaies Covered | Imagine Marketing Limited, SAMSUNG, Anker Innovations, Apple Inc., Xiaomi, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India mobile accessories market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India mobile accessories market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India mobile accessories industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Mobile Accessories Market Report

The India mobile accessories market reached USD 6.86 Billion in 2025, driven by India's smartphone user base, boAt's category-creating TWS earphone market, Amazon and Flipkart's e-commerce accessories leadership, PLI scheme domestic manufacturing expansion, and rising urban consumer premiumization.

The market grows at 8.54% CAGR during 2026-2034, reaching USD 14.66 Billion by 2034, driven by India's smartphone installed base, 5G adoption triggering TWS headphone and fast-charger upgrades, ANC democratization creating a mass premium headphone market, East India's rapidly growing market, and PLI manufacturing enabling domestic brand margin improvement.

Headphones lead at 32.8% through boAt's high TWS market share, India becoming the world's 3rd-largest TWS market, and the INR 999-2,999 TWS segment's mass adoption.

Online leads at 58.4% through Amazon India and Flipkart, commanding 45-48% of total accessory revenues, India's highest-in-Asia e-commerce accessories penetration, and Big Billion Days/Great Indian Festival generating high accessories sales.

North India leads at 29.7%, anchored by Delhi's Nehru Place wholesale hub, UP-Bihar's massive first-time smartphone buyer market, Gurugram-Noida IT workforce premium accessory demand, and North India's concentration of both B2C premium buyers and wholesale distribution infrastructure.

Leading companies include Imagine Marketing Limited, SAMSUNG, Anker Innovations, Apple Inc., and Xiaomi, among others.

The market is projected to reach approximately USD 10.34 Billion by 2030, with the TWS headphone market growth, ANC democratization at mass premium adoption, PLI manufacturing shifting 40%+ of organized accessories to India-assembled production, gaming accessories emerging as a standalone category, and East India's rapid market growth closing the regional market share gap.

5G creates two accessory upgrade waves: TWS earphones and fast chargers. India's 5G subscriber base growth represents a strong upgrade cycle concentrated in India's highest-spending urban demographics.

Gaming accessories, India's mobile gamers requiring specialized gaming controllers, gaming TWS, and gaming power banks; ANC TWS mid-premium segment (~25% CAGR within headphones) as ANC democratizes to INR 2,999; GaN chargers (~30% CAGR within chargers) as USB-C standardization and fast-charging adoption accelerate; and rural power banks (~15-20% CAGR) as rural India's power infrastructure drives first-time mobile power backup adoption.

Three priority opportunities: PLI manufacturing investment for organized brands to eliminate import duties and improve gross margins; gaming accessories brand creation targeting India's mobile gamers with specialized low-latency controllers and gaming headsets; and East India wholesale distribution network building to capture the regional market's fastest-growing CAGR trajectory as organized distribution infrastructure lags 3-5 years behind North and South India.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)