India Mobile Payment Market Size, Share, Trends and Forecast by Mode of Transaction, Application, and Region, 2026-2034

India Mobile Payment Market Summary:

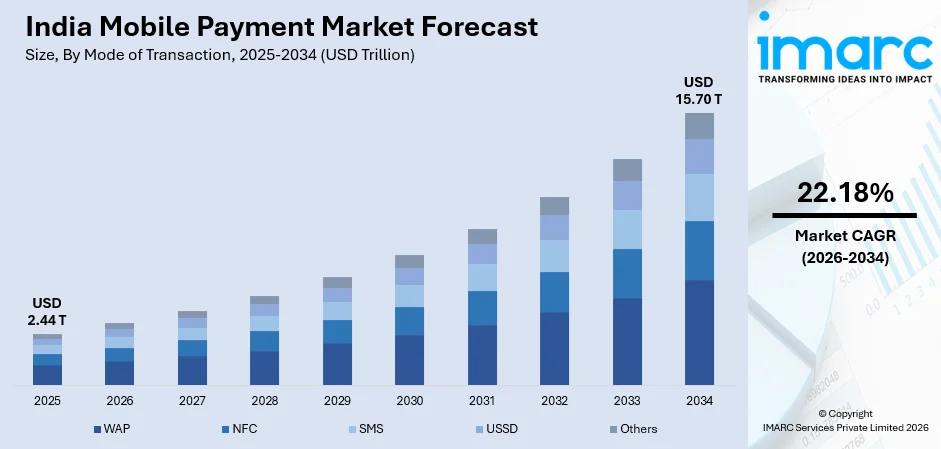

The India mobile payment market size was valued at USD 2.44 Trillion in 2025 and is projected to reach USD 15.70 Trillion by 2034, growing at a compound annual growth rate of 22.18% from 2026-2034.

India's mobile payment landscape is undergoing a structural transformation driven by ubiquitous smartphone penetration, rapid expansion of real-time payment infrastructure, and a digitally aspirational consumer base. The widespread integration of mobile applications and web-based transaction platforms has redefined how individuals and enterprises conduct everyday commerce, utility settlements, and cross-sector financial activities. Intensifying government-led digital inclusion mandates, growing merchant acceptance networks, and advancements in payment security frameworks are collectively reinforcing adoption across urban and semi-urban geographies, further consolidating the India mobile payment market share.

Key Takeaways and Insights:

- By Mode of Transaction: WAP dominates the market with a share of 97.0% in 2025, reflecting the overwhelming preference for app-based and mobile web interfaces, including UPI apps, mobile wallets, and browser-based payment gateways, as the primary channel for digital transactions across India.

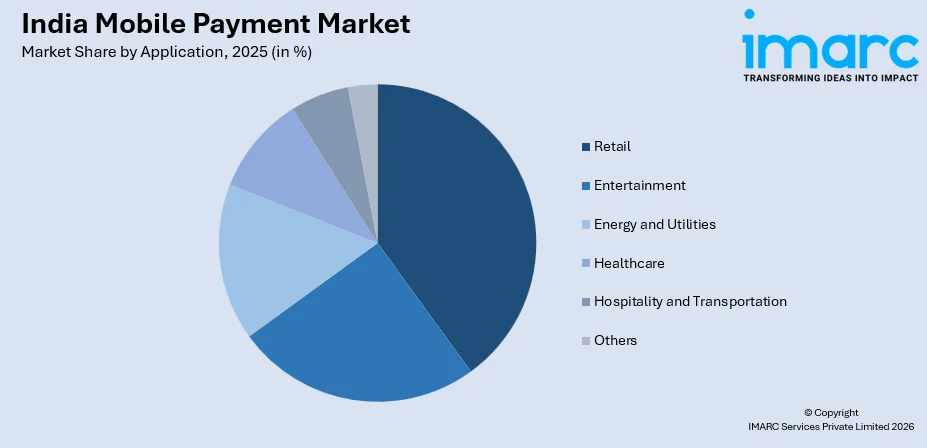

- By Application: Retail leads the market with a share of 34.0% in 2025, driven by surging in-app purchases, QR code-based merchant transactions, e-commerce checkout adoption, and the accelerating shift of kirana stores and formal retailers toward digital payment acceptance.

- By Region: North India represents the largest regional segment with a market share of 32.7% in 2025, underpinned by high urban density in the Delhi National Capital Region, robust fintech infrastructure, and concentrated commercial activity across Uttar Pradesh, Rajasthan, and Haryana.

- Key Players: The India mobile payment market features a competitive mix of domestic fintech leaders, global technology platforms, and bank-affiliated digital wallets. Major players compete on transaction speed, security, user experience, and ecosystem breadth to capture market share across diverse consumer and merchant segments.

To get more information on this market Request Sample

India's mobile payment market has emerged as one of the fastest-evolving digital financial ecosystems globally, propelled by the National Payments Corporation of India's Unified Payments Interface (UPI) infrastructure. UPI processed over 228 billion transactions in 2025, processing daily averages exceeding 698 million transactions, a testament to the platform's deep entrenchment in daily commerce. Person-to-merchant transactions have become a major component of the UPI ecosystem, reflecting the growing acceptance of digital payments among small retailers, local shops, and neighborhood merchants. Government initiatives aimed at encouraging merchant adoption of digital payment platforms are further strengthening this trend, particularly for everyday low-value transactions. These efforts are helping expand mobile payment usage across rural and semi-urban markets where digital acceptance is steadily improving. At the same time, major fintech and technology platforms are witnessing broad consumer engagement with UPI services, with significant participation emerging from smaller cities and developing urban centers, highlighting the widening reach of India’s mobile payment ecosystem.

India Mobile Payment Market Trends:

Accelerating Dominance of UPI-Integrated Mobile App Transactions

The convergence of mobile applications and the UPI infrastructure has entrenched WAP and app-based channels as the defining modality of India's mobile payment ecosystem. Person-to-merchant UPI transactions grew 37% year-on-year in the first half of 2025, reaching 67 billion transactions, driven by broader merchant digitization extending even to micro-retailers. India's UPI QR acceptance network expanded to 678 million endpoints by June 2025, a 111% increase since January 2024, enabling seamless tap-scan-pay experiences across the formal and informal economy. For instance, in April 2025, Razorpay became the first payment gateway to integrate with NPCI's UPI plugin, enabling native in-app payment flows for businesses and significantly reducing checkout friction for mobile commerce operators.

Growing Integration of NFC and Contactless Payment Technologies

Near Field Communication technology is progressively complementing app-based transactions, particularly in urban transit and organized retail. India recorded approximately 700 million NFC-capable smartphone users in 2024, and digital payment volumes grew by nearly 40% during the year, reflecting strong preference for tap-based solutions. Contactless payment methods are gaining strong momentum in in-store transactions as regulatory adjustments simplify the authentication process for small-value NFC payments. By reducing friction at checkout, these measures encourage faster and more convenient transactions through mobile devices. Additionally, the expansion of the National Common Mobility Card program across multiple cities is integrating contactless payments into public transportation systems, enabling commuters to use mobile and NFC-based payment solutions in everyday travel and retail environments.

Expansion of Digital Payment Adoption Across Tier-II and Tier-III Cities

The expansion of mobile payments beyond major metropolitan areas is significantly influencing the growth pattern of the market. Increasing digital commerce adoption in smaller cities and emerging urban centers is driving broader participation in mobile payment ecosystems. As online shopping and digital financial services gain popularity in these regions, mobile payment platforms are experiencing rising user engagement and deeper market penetration outside traditional urban hubs. Behavioral data from UPI shows a declining average ticket size—from ₹1,478 in 2024 to ₹1,348 in 2025, driven by routine low-value purchases such as groceries and daily provisions, indicating normalized digital payment habits in smaller markets. The proliferation of affordable 5G connectivity and vernacular-language UPI interfaces, including BHIM's support for over 13 regional languages, is further lowering adoption barriers in linguistically diverse regions.

Market Outlook 2026-2034:

India's mobile payment market is poised for sustained double-digit expansion throughout the forecast period, supported by deepening digital financial infrastructure, rising smartphone ownership, and ongoing regulatory facilitation of real-time transactions. Innovations including credit-on-UPI, biometric authentication, and AI-assisted fraud prevention are broadening the addressable user base while improving transactional security. The integration of mobile payments into sectors such as healthcare, energy utilities, and public transportation will further diversify application demand beyond retail. The market generated a revenue of USD 2.44 Trillion in 2025 and is projected to reach a revenue of USD 15.70 Trillion by 2034, growing at a compound annual growth rate of 22.18% from 2026-2034.

India Mobile Payment Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Mode of Transaction |

WAP |

97.0% |

|

Application |

Retail |

34.0% |

|

Region |

North India |

32.7% |

Mode of Transaction Insights:

- WAP

- NFC

- SMS

- USSD

- Others

WAP dominates with a market share of 97.0% of the total India mobile payment market in 2025.

The WAP segment leads the India mobile payment market largely because it enables users to complete transactions through mobile web interfaces without requiring dedicated applications. This accessibility allows a wide range of consumers, including those who may not frequently download multiple financial apps, to perform digital payments directly through mobile browsers. Payment gateways integrated with banking platforms and merchant websites often support WAP-based transaction flows, enabling services such as bill payments, ticket bookings, and online purchases through simple browser-based interfaces. This convenience supports widespread usage across various digital commerce platforms.

Another factor supporting the dominance of the WAP segment is its compatibility with a broad range of mobile devices and operating systems. Unlike app-based solutions that require installation and regular updates, WAP-based payment interfaces function through standard mobile internet access, making them accessible even in situations with limited device storage or varying device capabilities. Financial institutions, e-commerce platforms, and service providers commonly integrate browser-based payment gateways to support seamless transactions. This flexibility helps expand digital payment reach across diverse user groups and contributes to the continued relevance of WAP-based payment channels in India’s evolving digital economy.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Entertainment

- Energy and Utilities

- Healthcare

- Retail

- Hospitality and Transportation

- Others

Retail leads with a share of 34.0% of the total India mobile payment market in 2025.

The retail segment holds the leading position in the India mobile payment market, propelled by accelerating merchant digitization, the proliferation of QR code acceptance points, and the normalization of mobile checkout across organized retail and informal commerce. The India retail market size reached USD 1,124.2 Billion in 2025. The market is expected to reach USD 3,505.4 Billion by 2034, exhibiting a growth rate (CAGR) of 12.80% during 2026-2034. A significant behavioral shift among small and micro-merchants toward UPI-based payment acceptance is transforming India’s retail payment landscape. Neighborhood kirana stores and local retailers are increasingly adopting mobile payment solutions for everyday transactions.

The expansion of digital payment infrastructure and supportive government initiatives are further strengthening mobile payment adoption in the retail sector. Programs promoting cashless transactions, along with simplified onboarding processes for merchants, are encouraging retailers to integrate mobile payment platforms into their daily operations. In addition, the growing penetration of smartphones and affordable internet services is enabling both consumers and merchants to access digital payment ecosystems with greater ease. As a result, retailers are increasingly leveraging mobile payments to enhance transaction efficiency, reduce cash-handling risks, and improve the overall customer checkout experience.

Regional Insights:

- North India

- West and Central India

- South India

- East India

North India exhibits a clear dominance with a 32.7% share of the total India mobile payment market in 2025.

North India's leading position in the mobile payment market is anchored by the Delhi National Capital Region's dense urban commercial ecosystem, which serves as the country's largest concentration of both fintech enterprises and high-frequency digital payment users. States including Uttar Pradesh, India's most populous state with over 240 million residents, Rajasthan, Haryana, and Punjab collectively generate substantial mobile payment volumes across retail, transportation, and utility verticals. The region benefits from extensive 4G/5G infrastructure coverage, high smartphone penetration in urban corridors, and significant government-sector digital payment adoption driven by direct benefit transfer programs and public utility digitization.

Additionally, North India’s strong mobile payment adoption is supported by the rapid expansion of organized retail chains, food delivery platforms, ride-hailing services, and e-commerce marketplaces across major cities such as Delhi, Noida, Gurugram, and Lucknow. These urban centers act as digital commerce hubs where QR code–based payments and UPI transactions are widely accepted by both large retailers and small merchants. Furthermore, government initiatives promoting cashless transactions, along with increasing fintech collaborations with local banks and payment service providers, are accelerating the integration of mobile payment solutions across both urban and semi-urban consumer segments.

Market Dynamics:

Growth Drivers:

Why is the India Mobile Payment Market Growing?

Robust Expansion of UPI Infrastructure and Digital Public Infrastructure

India's Unified Payments Interface has evolved from a simple payment mechanism into a comprehensive digital financial infrastructure that underpins the country's entire mobile payment ecosystem. The architecture's open, interoperable design allows over 80 UPI applications to serve 641 connected banks through a single payment rail, enabling near-universal accessibility for both consumers and merchants. The National Payments Corporation of India has progressively enhanced the platform through innovations such as UPI Lite for offline low-value transactions, UPI 123PAY for feature phone users, and credit-on-UPI that extends formal credit access through the payment interface. The Union Cabinet's approval of a ₹1,500 crore incentive program in March 2025 to accelerate BHIM-UPI adoption among rural and small merchants directly expands the addressable market. Aadhaar-linked e-KYC streamlines user onboarding while India's entry into Project Nexus—the Bank for International Settlements cross-border real-time payments initiative in 2024—is extending UPI's utility to international corridors in Southeast Asia and beyond, broadening the revenue opportunity for India's mobile payment ecosystem.

Accelerating Smartphone Penetration and Affordable Mobile Internet Access

The democratization of smartphone access and low-cost mobile internet connectivity has created an unprecedented base of potential and active mobile payment users across India's diverse socioeconomic landscape. The widespread availability of smartphones and affordable mobile data has significantly improved access to app-based payment platforms across diverse income groups in India. Expanding high-speed mobile network infrastructure is enhancing transaction reliability and connectivity, particularly in previously underserved regions. At the same time, the growing availability of NFC-enabled smartphones is supporting the adoption of contactless payment methods among a broader consumer base. The increasing use of wearable devices such as smartwatches and fitness trackers is further diversifying digital payment options. Additionally, multilingual mobile applications are helping make digital payment services more accessible across India’s linguistically diverse population.

Government-Led Financial Inclusion and Digital Economy Initiatives

India's policy framework has been a powerful structural catalyst for mobile payment market expansion, embedding digital transactions into government service delivery, welfare disbursements, and regulatory mandates. The Digital India initiative has connected over 2.5 lakh Gram Panchayats to broadband infrastructure, while the Jan Dhan-Aadhaar-Mobile trinity has brought hundreds of millions of previously unbanked citizens into the formal financial system. Government-led digital initiatives are encouraging greater adoption of mobile payments by directing subsidies and welfare benefits into bank accounts linked to digital platforms, familiarizing beneficiaries with electronic financial transactions. At the same time, evolving regulatory frameworks are simplifying customer verification processes and merchant onboarding requirements. Policy measures that enable additional banking services through digital payment systems, along with standardized payment mechanisms across financial institutions, are further strengthening the role of mobile payments in everyday financial and institutional transactions.

Market Restraints:

What Challenges the India Mobile Payment Market is Facing?

Rising Cybersecurity Threats and Digital Payment Fraud

Rising cybercrime and digital payment fraud are undermining consumer confidence in mobile payment platforms, particularly among new users. Increasing incidents of identity theft, phishing, and unauthorized transactions require stronger security frameworks and regulatory oversight. At the same time, evolving digital threats and gaps in legal provisions create compliance complexities for payment service providers and slow innovation within the digital payments ecosystem.

Digital Literacy Gaps and Adoption Barriers in Rural and Semi-Urban Areas

Although digital infrastructure and internet connectivity have expanded significantly, digital literacy remains uneven across rural and semi-urban regions. Many households lack the skills required to independently access and use digital financial services. This knowledge gap increases vulnerability to fraud and slows the adoption of mobile payment platforms, limiting the pace of market expansion in less digitally experienced populations.

Zero-MDR Regime and Revenue Sustainability Challenges for Ecosystem Players

The zero Merchant Discount Rate framework for certain digital payment transactions has reduced an important revenue source for payment service providers. Limited monetization opportunities can restrict investments in infrastructure, cybersecurity, and service innovation. Over time, the absence of sustainable revenue models may affect the ability of ecosystem participants to scale operations and support long-term growth of the digital payments market.

Competitive Landscape:

India's mobile payment market exhibits high competitive intensity, characterized by a stratified structure comprising domestic fintech leaders, global technology platforms, telecom-backed payment services, and bank-affiliated digital wallets. The market is highly concentrated at the transaction volume level, with a small number of dominant platforms capturing many UPI flows. Competition centers on user experience quality, transaction success rates, merchant onboarding efficiency, and ecosystem breadth encompassing financial services, commerce, and utility integrations. The competitive landscape is further shaped by regulatory requirements under the Reserve Bank of India's payment aggregator licensing framework, which has rationalized entry and raised compliance standards. Technology investments in AI-driven fraud detection, API integration capabilities, and feature phone compatibility are emerging as key differentiators as platforms compete to serve India's vast underserved segments.

Recent Developments:

- April 2025: Resilient Payments Private Limited, a subsidiary of a leading domestic fintech, received final approval from the Reserve Bank of India to operate as an online payment aggregator. This regulatory clearance positions the company as one of the few entities holding a payment aggregator license alongside an NBFC license and bank ownership, enabling it to scale integrated digital payments, lending, and investment offerings within a single regulated platform.

- January 2025: A prominent domestic digital wallet provider, in partnership with the Reserve Bank of India and a private sector bank, launched a full-scale Central Bank Digital Currency (e-Rupee) wallet, becoming the country's first digital wallet provider to offer complete e-₹ production capabilities to Android users. This development marks a significant milestone in India's digital currency adoption trajectory.

- September 2024: A leading UPI platform introduced a feature enabling primary users to manage payment authorizations for family members or trusted contacts without bank-linked accounts, allowing dependents to transact using their own UPI IDs while the primary account holder retains oversight of spending limits and transaction history. This innovation directly broadens the addressable user base within household payment ecosystems.

India Mobile Payment Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Trillion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Mode of Transactions Covered | WAP, NFC, SMS, USSD, Others |

| Applications Covered | Entertainment, Energy and Utilities, Healthcare, Retail, Hospitality and Transportation, Others |

| Region Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Mobile Payment Market Report

The India mobile payment market size was valued at USD 2.44 Trillion in 2025.

The India mobile payment market is expected to grow at a compound annual growth rate of 22.18% from 2026-2034 to reach USD 15.70 Trillion by 2034.

WAP held the largest India mobile payment market share at 97.0% in 2025, driven by the dominant role of UPI-integrated mobile applications and browser-based payment gateways as the primary channel for digital transactions across consumers and merchants nationwide.

Key factors driving the India mobile payment market include the robust expansion of the UPI digital payment infrastructure, rapid smartphone and affordable internet penetration, government-led financial inclusion programs such as Digital India and BHIM-UPI incentives, rising merchant digitization across Tier-II and Tier-III cities, and growing adoption of NFC-enabled contactless payment technologies.

Major challenges facing the India mobile payment market include escalating cybersecurity threats and digital payment fraud with growing financial losses, persistent digital literacy gaps in rural and semi-urban populations limiting independent adoption, the zero-MDR policy framework that constrains revenue sustainability for payment ecosystem participants, and interoperability limitations across platforms and devices that restrict seamless user experiences

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade