India Modular Kitchen Market Size, Share, Trends and Forecast by Product, Distribution Channel, End-User, and Region, 2026-2034

India Modular Kitchen Market Size, Share, Trends & Forecast (2026-2034)

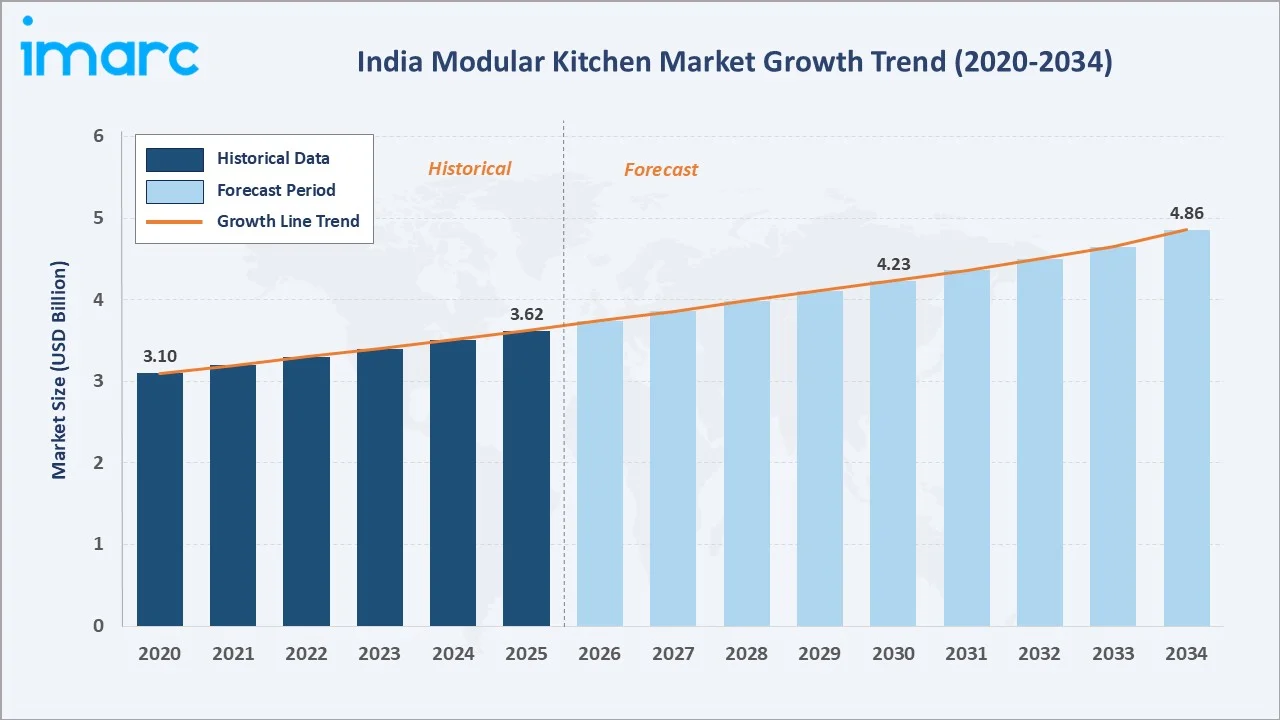

The India modular kitchen market was valued at USD 3.62 Billion in 2025 and is projected to reach USD 4.86 Billion by 2034, exhibiting a CAGR of 3.16% during 2026-2034. Rising urban household formation, an active residential construction pipeline supported by PMAY-Urban under which a total of 1.18 Crore houses were sanctioned cumulatively as per the Economic Survey 2024-2025, growing nuclear family share, expanding organized retail networks, and steady premiumization in metro and tier-2 markets are the primary drivers shaping market growth.

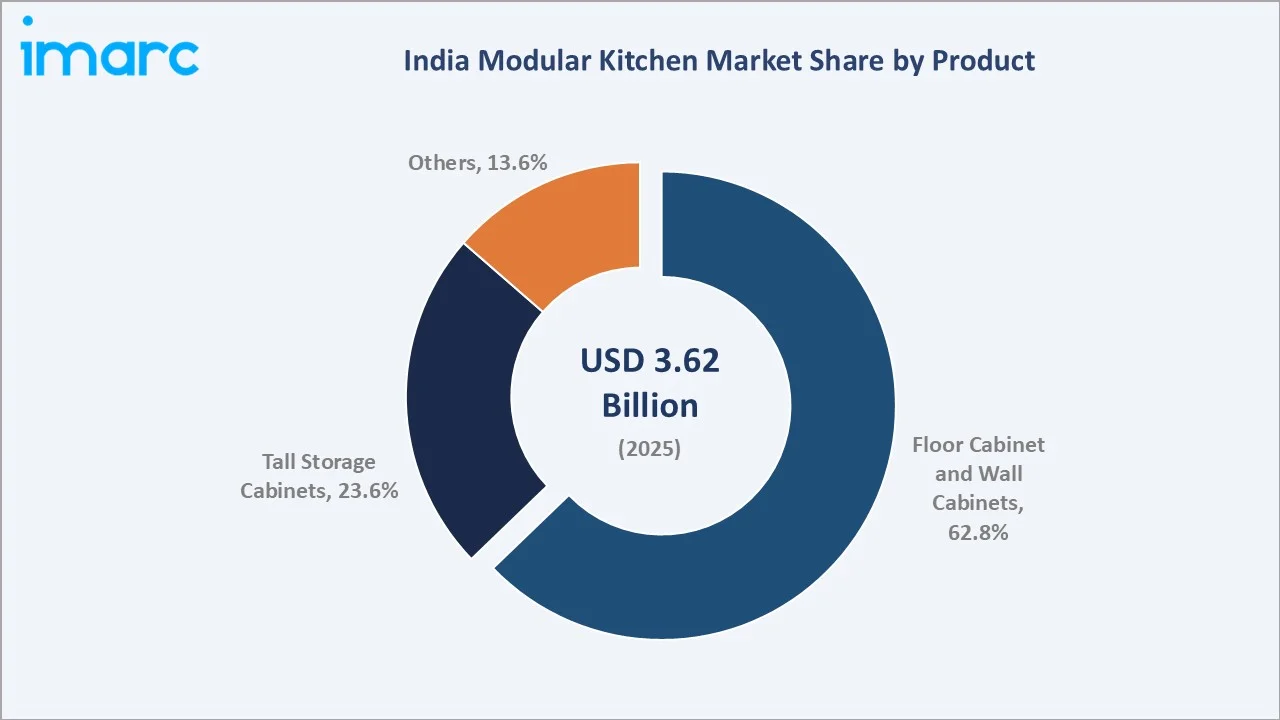

Floor cabinet and wall cabinets lead the product segment at 62.8%, residential dominates the end user segment at 78.6%, and North India commands 31.7% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.62 Billion |

|

Forecast Market Size (2034) |

USD 4.86 Billion |

|

CAGR (2026-2034) |

3.16% |

|

Base Year |

2025 |

|

Historical Period |

2026-2034 |

|

Forecast Period |

2020-2025 |

|

Largest Region |

North India (31.7%, 2025) |

|

Leading Product |

Floor Cabinet and Wall Cabinets (62.8%, 2025) |

|

Leading End User |

Residential (78.6%, 2025) |

The India modular kitchen market expanded from USD 3.10 Billion in 2020 to USD 3.62 Billion in 2025, supported by faster urbanization, rising disposable incomes, and standardized housing handovers. Anchored at USD 4.23 Billion in 2030, the forecast to USD 4.86 Billion by 2034 is supported by accelerating tier-2 city demand and brand-led organized expansion.

To get more information on this market, Request Sample

CAGR trajectories across product and end user sub-segments show that others, residential, and North India grow faster than the overall 3.16% market CAGR, supported by aspirational demand, premiumization, and rapid metro housing handovers.

.webp)

Executive Summary

The India modular kitchen market is on a steady growth path, expanding from USD 3.10 Billion in 2020 toward USD 4.86 Billion by 2034. Modular kitchens have moved from an aspirational metro upgrade to a near-default fitment in new urban apartments. Rising household incomes, smaller home footprints, and demand for hygienic, low-maintenance interiors are reshaping kitchen design choices. Brand-led design studios and online configurators are also bringing organized solutions to many tier-2 households for the first time.

Floor cabinet and wall cabinets dominate at 62.8% in 2025, supported by their role as the structural core of every modular kitchen layout. Residential leads end user demand at 78.6%, fueled by apartment handovers and the growing share of nuclear families across metros. IKEA India reported 10% year-on-year growth for the financial year ending August 2025, reflecting steadily widening demand for organized home and kitchen solutions across the country. North India commands 31.7%, led by the Delhi-NCR cluster, Lucknow, and Chandigarh, supported by large-format housing pipelines.

Key Market Insights

|

Insight |

Data |

|

Leading Product |

Floor Cabinet and Wall Cabinets - 62.8% share (2025) |

|

Second Product |

Tall Storage Cabinets - 23.6% share (2025) |

|

Leading End User |

Residential - 78.6% share (2025) |

|

Second End User |

Commercial - 21.4% share (2025) |

|

Leading Region |

North India - 31.7% share (2025) |

|

Top Companies |

Asian Paints Ltd., Häfele, Spacewood Furnishers Pvt. Ltd., Homevista Decor and Furnishings Private Limited, Livspace |

Key Analytical Observations Expanding on the Data Above:

- Floor cabinet and wall cabinets at 62.8% dominate because they form the structural core of nearly every kitchen layout, covering counter storage, base utility, and overhead crockery storage. Demand here is closely linked to apartment handovers and renovation cycles.

- Tall storage cabinets at 23.6% are gaining ground in metro homes where compact carpet area pushes households toward vertical storage that absorbs pantry items, larger appliances, and brooms in a single unit.

- Residential leadership at 78.6% reflects the structural reality that modular kitchen demand is shaped largely by individual homeowners and apartment buyers, with developer tie-ups now bundling kitchens into new project handovers.

- Commercial at 21.4% is sustained by cloud kitchens, café chains, hotel pantries, and serviced apartments where standardized, hygienic, and quickly installable kitchen units are essential to multi-site rollouts. As per IMARC Group, the India cloud kitchen market size was valued at USD 1,236.5 Million in 2025.

- North India at 31.7% leads the regional mix on the strength of the Delhi-NCR cluster, Lucknow, Jaipur, and Chandigarh. Strong urban housing demand and rising preference for space-optimized, premium interiors continue to drive modular kitchen adoption across Tier 1 and emerging Tier 2 cities in the region.

India Modular Kitchen Market Overview

Modular kitchens are factory-engineered, prefabricated kitchen units assembled on-site, typically combining floor and wall cabinets, tall storage units, countertops, and integrated appliances into a single coordinated layout.

.webp)

The Indian ecosystem brings together MDF and plywood manufacturers, hardware and fitting suppliers, appliance makers, design studios, builder partnerships, and organized showroom networks, working in coordination to deliver factory-finished kitchens to homeowners and developers across metros and growing tier-2 cities.

Market Dynamics

To evaluate market opportunities, Request Sample

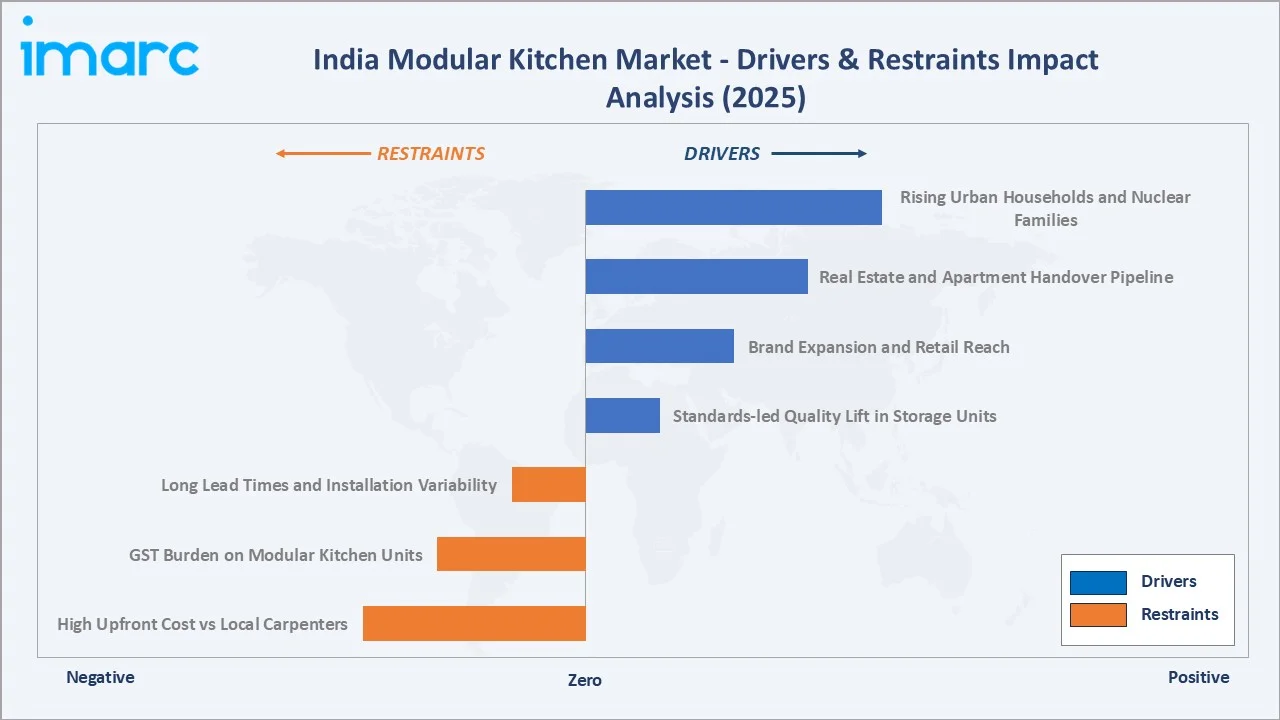

Market Drivers

- Rising Urban Households and Nuclear Families: Faster urbanization and the growing share of nuclear households are reshaping kitchen needs, with smaller carpet areas and dual-income lifestyles favoring organized, easy-to-clean modular formats over traditional masonry kitchens. Urban population (% of total population) in India was recorded at 36.87% in 2024, according to the World Bank collection of development indicators.

- Real Estate and Apartment Handover Pipeline: Sustained launches and possessions in Tier-1 and emerging Tier-2 cities are translating into a stable base of new kitchen fitouts, especially in mid-segment apartments where modular formats are increasingly the default.

- Brand Expansion and Retail Reach: Organized brands are scaling design studios, dealer networks, and online configurators, making modular kitchens accessible to households that earlier relied only on local carpenters for built-in storage.

- Standards-led Quality Lift in Storage Units: The implementation of quality guidelines by the Bureau of Indian Standards for domestic kitchen storage units is raising expectations around materials, hardware, and durability, helping organized brands gain share over informal, carpentry-led offerings.

Market Restraints

- High Upfront Cost vs Local Carpenters: Branded modular kitchens carry a meaningful price premium over traditional carpenter-built setups, limiting penetration in price-sensitive Tier-3 cities and large parts of semi-urban India where local craft economics still dominate.

- GST Burden on Modular Kitchen Units: As of 2025, modular kitchen furniture in India was taxed at a Goods and Services Tax (GST) rate of 18%, which adds materially to the final delivered price for end consumers and discourages first-time buyers from upgrading from open or semi-fitted layouts to fully modular configurations.

- Long Lead Times and Installation Variability: Order-to-install cycles can stretch across several weeks because of customization, on-site measurement reworks, and dependence on skilled fitters, occasionally pushing buyers toward off-the-shelf alternatives or local providers.

Market Opportunities

- Tier-2 and Tier-3 City Penetration: Cities, such as Indore, Jaipur, Coimbatore, Lucknow, and Bhubaneswar, are emerging as significant growth pockets, supported by housing handovers and rising aspirations among younger homeowners.

- Builder-Developer Bundling: Real estate developers are increasingly offering modular kitchens as part of project handovers, opening a steady project-channel pipeline for brands willing to standardize SKUs and provide predictable installation.

Market Challenges

- Fragmented Unorganized Competition: Local carpenters and small fabricators continue to hold significant share, particularly in renovation projects, creating persistent price competition that constrains volume conversion for organized players.

- Skilled Installation Workforce Gap: Quality installation requires trained fitters who can handle precise measurements, hardware tuning, and finishing work, but availability of such skilled workforce remains uneven across cities and seasons.

Emerging Market Trends

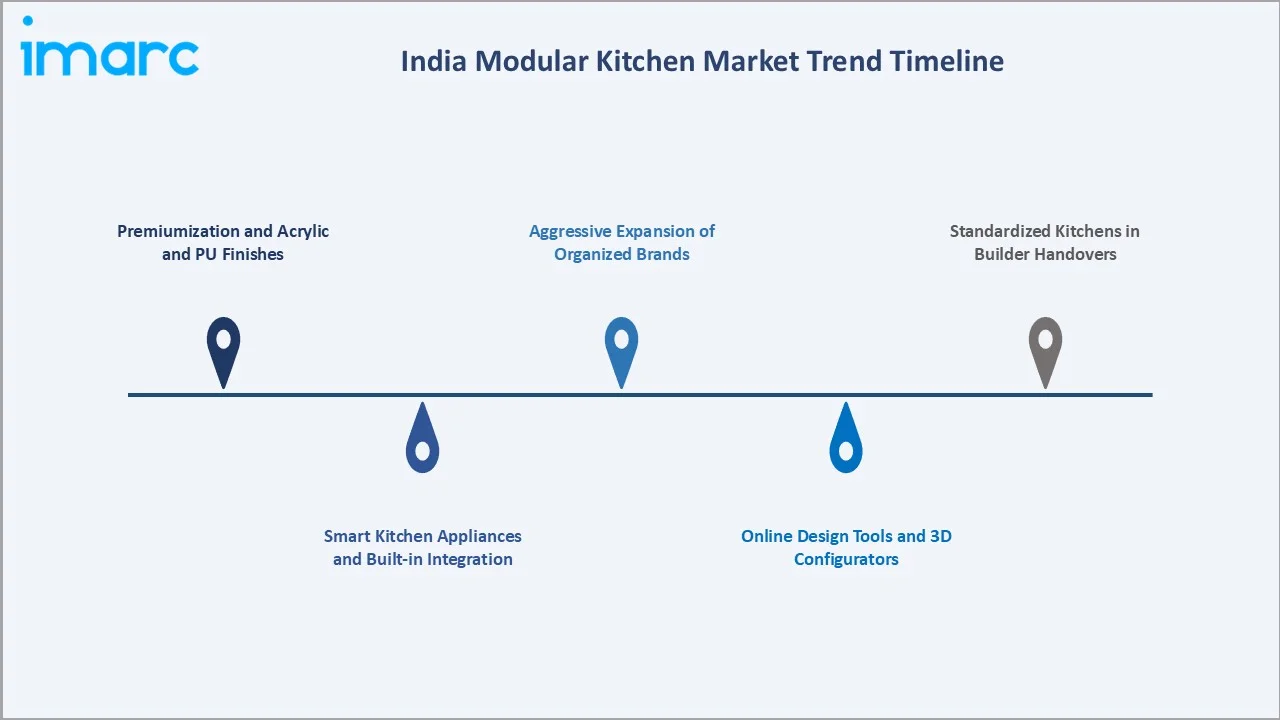

1. Premiumization and Acrylic and PU Finishes

Acrylic, polyurethane, and lacquered glass shutters are gaining share over basic laminates in metro premium projects. Buyers increasingly favor scratch-resistant, glossy, easy-to-clean finishes that hold up to long-term Indian cooking conditions and align with contemporary interior themes.

2. Smart Kitchen Appliances and Built-in Integration

Built-in hobs, chimneys, microwaves, and dishwashers are increasingly integrated into the cabinetry footprint. Hidden hinges, soft-close drawers, and motion-sensor lighting are becoming standard expectations rather than upgrade options in mid-segment projects.

3. Aggressive Expansion of Organized Brands

Global and domestic players are accelerating physical retail rollouts to capture rising organized demand. Notably, in November 2025, IKEA India announced plans to open four to five new stores annually across major metros, reflecting structural confidence in the country's home and kitchen demand pipeline beyond the existing Hyderabad, Mumbai, and Bengaluru footprint.

4. Online Design Tools and 3D Configurators

Brands are leaning on 3D design configurators, virtual showrooms, and remote consultations. These tools shorten decision cycles, reduce showroom dependency, and enable brand-led penetration in cities without dense physical retail.

5. Standardized Kitchens in Builder Handovers

Mid- and premium-segment housing projects are increasingly bundling modular kitchens into possession-stage handovers. This shifts the buying decision from individual homeowners to developers, generating steady project-channel demand for organized brands.

Industry Value Chain Analysis

The Indian modular kitchen value chain spans six stages, from raw material sourcing through installation and after-sales service. System integration, design, and last-mile installation capture the highest value addition, while organized brand-driven distribution provides downstream control over the customer experience.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of MDF, plywood, particleboard, laminates, and steel sheets, along with edge banding and adhesive providers supporting cabinet-grade material production |

|

Cabinet & Component Manufacturing |

Cabinet makers producing carcass, shutters, drawers, and fascia panels, including large facilities focused on dimensional accuracy and finishing quality |

|

Brand & System Integration |

OEMs and national brands assembling cabinets and integrating hardware, hobs, chimneys, and lighting into complete modular kitchen systems |

|

Compliance & Standards |

BIS specifications for domestic storage units, fire-safety norms, and emission standards governing materials, formaldehyde levels, and finishes |

|

Distribution & Installation |

Organized brand showrooms, franchise studios, online configurators, and trained installers providing site-specific measurement, fitment, and handover services |

|

End Use & After-sales |

Homeowners, builder-developer projects, cloud kitchens, hotels, and serviced apartments supported by warranty, repair, and refurbishment services |

Vertically integrated players that combine in-house design, captive cabinet manufacturing, and exclusive franchise studios achieve stronger control over quality, lead times, and customer experience compared to assemblers reliant on third-party panel sourcing.

Technology Landscape in the India Modular Kitchen Industry

Materials and Engineered Boards

Marine-grade plywood and high-density MDF remain the most common cabinet substrates, while moisture-resistant boards and acrylic laminates are increasingly preferred in metro homes for durability against humid kitchen conditions and frequent cleaning.

Hardware and Soft-Close Mechanisms

Tandem drawer systems, soft-close hinges, lift-up flap fittings, and pull-out tall units are becoming standard in mid-segment kitchens. Indian operations of global hardware specialists are pushing locally produced hardware up the value curve.

Smart Connectivity and Appliance Integration

Built-in chimneys, induction hobs, ovens, dishwashers, and warming drawers are increasingly factored into cabinet planning from the outset. Connected appliance ecosystems and motion-sensor lighting are slowly entering premium urban kitchens.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product | Floor Cabinet and Wall Cabinets | 62.8% | 2025 |

| Distribution Channel | 🔒 | 🔒 | 2025 |

| End-User | Residential | 78.6% | 2025 |

| Region | North India | 31.7% | 2025 |

By Product

Floor cabinet and wall cabinets command a 62.8% majority share in 2025, driven by their role as the structural backbone of every modular kitchen layout. They typically include base storage, sink units, hob counters, and overhead cabinets that serve as the daily-use core of the kitchen.

To access detailed market analysis, Request Sample

Tall storage cabinets at 23.6% in 2025 are gaining traction in compact urban apartments where carpet area is constrained. These cabinets enable vertical storage of pantry items, large appliances, and bulky utensils within a single integrated unit, freeing counter and base space for active use.

By End User

Residential dominates with a 78.6% share in 2025, reflecting the structural fact that modular kitchen demand is shaped largely by individual homeowners, apartment buyers, and renovation projects. Builder-developer bundling of standardized modular kitchens into new project handovers further reinforces this dominance.

.webp)

Commercial at 21.4% is supported by cloud kitchens, quick-service café chains, hotel pantries, hostel kitchens, and serviced apartment operators. These end users prioritize standardized layouts, quick installation cycles, and easy maintenance, making modular formats well-suited to multi-site rollouts.

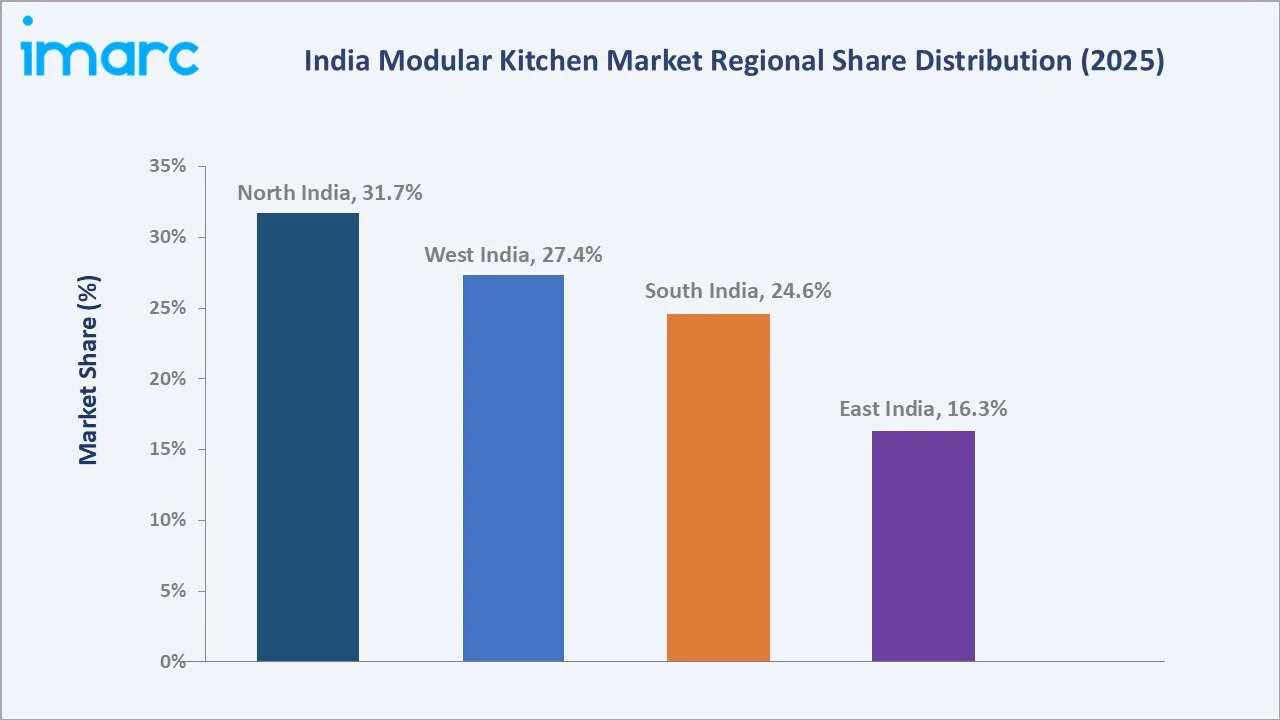

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

31.7% |

Large apartment handover pipeline, strong organized retail penetration, and growing aspirational demand across the metro and tier-2 belt |

|

West India |

27.4% |

Premium urban housing stock, compact carpet areas favoring smart storage, and a mature design and dealer ecosystem |

|

South India |

24.6% |

Established IT-driven urban incomes, high apartment ownership, and steady premiumization in modern home interiors |

|

East India |

16.3% |

Emerging tier-2 demand, growing organized retail reach, and rising adoption among first-time apartment buyers |

North India at 31.7% in 2025 leads the regional mix, anchored by the Delhi-NCR cluster along with Lucknow, Chandigarh, and Jaipur. A robust apartment delivery pipeline, deep dealer networks, and strong organized brand activity in the region together sustain its leadership in the modular kitchen category.

West India at 27.4% follows closely, with Mumbai, Pune, Ahmedabad, and Surat driving demand. Compact apartment formats in this belt naturally favor smart, space-saving cabinet configurations and premium finishes, supporting steady value growth alongside volume.

Competitive Landscape

The India modular kitchen market is moderately fragmented. Organized brands dominate the metro and tier-1 retail conversation, while a long tail of regional brands and local carpenters continue to hold significant share in renovation and tier-3 demand pockets. Brand-owned design studios, dealer depth, and project channel relationships form the key competitive moats.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Asian Paints Ltd. |

Sleek |

Leader |

Branded studios; full kitchen plus wardrobe portfolio; broad multi-city reach |

|

Häfele |

VS SUB Side base cabinet pull-out |

Challenger |

Premium fittings; integrated kitchen and appliance design studios |

|

Spacewood Furnishers Pvt. Ltd. |

Adele Modular Kitchen Design, Amelia Modular Kitchen Design |

Challenger |

Pan-India dealer network; large-scale manufacturing capacity; broad modular kitchen and home furniture portfolio |

|

Homevista Decor and Furnishings Private Limited |

HomeLane, HomeLane Luxe |

Emerging |

Online-first interior design; tier-2 expansion; modular kitchen as anchor offer |

|

Livspace |

Vinciago |

Emerging |

Digital-first home interior platform; strong design configurator focus |

Key players include Asian Paints Ltd., Häfele, Spacewood Furnishers Pvt. Ltd., Homevista Decor and Furnishings Private Limited, and Livspace, among others.

.webp)

Key Company Profiles

Asian Paints Ltd.

Asian Paints Ltd. operates the Sleek brand, positioned as one of India's leading organized modular kitchen brands. The company leverages its strong distribution network, brand equity, and expanding home décor portfolio to strengthen its presence in the modular kitchen segment.

- Product Portfolio: Sleek modular kitchens, kitchen accessories, wardrobes, hardware fittings, and built-in appliances spanning entry, mid, and premium price tiers, distributed through company-owned and franchise studios across metros and tier-2 cities.

- Recent Developments: The company continues to expand its footprint through new experience centers and strengthened channel partnerships, while enhancing digital design tools and customer engagement platforms. It is also focusing on product innovation and operational efficiencies to support growth in the modular kitchen and home interiors segment.

- Strategic Focus: Leveraging Asian Paints' deep retail and dealer ecosystem, focused expansion of branded modular kitchen studios, and integration with the broader home décor portfolio of the parent group.

Häfele

Häfele is a global specialist in furniture fittings, architectural hardware, and integrated kitchen solutions, with India operations spanning premium kitchen fittings, appliances, and complete kitchen design studios across metros and tier-2 cities.

- Product Portfolio: Premium kitchen fittings, including the VS SUB Side base cabinet pull-out, integrated kitchen appliances, sinks, faucets, kitchen surfaces, and hardware solutions for cabinets and storage units.

- Recent Developments: In April 2026, Häfele expanded its modular kitchen offerings with Häfele Islene – Aluminum Profiles for Modular Island Systems, aimed at improving the aesthetic and structural integrity of contemporary kitchen islands.

- Strategic Focus: Premium fittings leadership, integrated kitchen and appliance design studios, and deep partnerships with architects, designers, and modular kitchen brands across India.

Homevista Decor and Furnishings Private Limited

Homevista Decor and Furnishings Private Limited operates the HomeLane and HomeLane Luxe brands, providing end-to-end interior design and modular kitchen solutions through experience centers and digital design tools across India.

- Product Portfolio: HomeLane offers full-home interiors with modular kitchens, wardrobes, and storage units as anchor categories, while HomeLane Luxe delivers a premium, personalized interior design service for high-end residential projects.

- Recent Developments: Homevista Decor and Furnishings Private Limited, continues to expand its footprint across key urban markets while strengthening its technology-driven design and project execution capabilities. HomeLane reported revenue of around INR 700+ Crore for FY25, with 22% year-on-year growth, supported by its acquisition of Design Cafe.

- Strategic Focus: Online-first interior design with 3D visualization, expansion into tier-2 cities through experience centers, and modular kitchen as the anchor category for full-home interior conversions.

Market Concentration Analysis

The India modular kitchen market is moderately concentrated at the organized end and highly fragmented overall. Leading players, such as Asian Paints Ltd., Häfele, Spacewood Furnishers Pvt. Ltd., Homevista Decor and Furnishings Private Limited, and Livspace, together hold a meaningful share of the organized segment, while local carpenters and small fabricators continue to serve a large portion of overall kitchen fitouts, especially in renovation projects.

Barriers to entry for organized players include showroom and dealer network build-out, quality and finish consistency at scale, BIS-aligned product engineering, and trained installation workforce. These structural requirements favor well-capitalized incumbents with manufacturing depth and brand recall.

Consolidation is gradually advancing as paint and home décor majors, large furniture brands, and global retailers strengthen their modular kitchen capabilities. Scale advantages in design tools, sourcing, and after-sales service are progressively reinforcing the position of leading organized players.

Investment & Growth Opportunities

Fastest Growing Segments

Others at 13.6%, residential at 78.6%, and the floor cabinet and wall cabinets at 62.8% are expected to grow faster than the overall 3.16% market CAGR through 2034, supported by premiumization, rising apartment handovers, and standardized cabinet integration in new homes.

Emerging Markets

North India at 31.7% remains the largest as well as fastest-growing region, while tier-2 cities, such as Lucknow, Indore, Coimbatore, Bhubaneswar, and Visakhapatnam, represent the most attractive untapped opportunities as housing handovers and aspirational demand expand.

Investment Trends

Investment activity is concentrated in design-led organized brands, online interior platforms, hardware manufacturing capacity expansion, and showroom rollouts in tier-2 cities. Builder-developer bundling and bank-led home interior financing are also opening newer go-to-market models.

Future Market Outlook (2026-2034)

The India modular kitchen market is forecast to expand from USD 3.62 Billion in 2025 to USD 4.86 Billion by 2034 at a CAGR of 3.16%, adding roughly USD 1.24 Billion in incremental annual market value over the forecast period.

Four forces will shape the market through 2034: a sustained urban housing pipeline, organized brand expansion into tier-2 and tier-3 cities, premiumization through smart appliances and high-end finishes, and gradual replacement of carpenter-built kitchens with branded modular systems.

By 2034, modular kitchens are likely to become the default fitment in new urban apartments across leading Indian cities, with builder-bundled configurations and brand-led design studios anchoring most household kitchen decisions in the country's organized segment.

Research Methodology

Primary Research

Primary research included structured interviews with senior product managers at leading modular kitchen brands, retail and franchise partners, real estate developers, hardware suppliers, and homeowners, validating market sizing, regional demand, product mix, and end user behavior.

Secondary Research

Secondary sources included Bureau of Indian Standards specifications, Reserve Bank of India and Ministry of Statistics and Program Implementation publications, Pradhan Mantri Awas Yojana progress dashboards, company annual reports, investor presentations, and verified industry news from leading business publications.

Forecasting Models

Market forecasts combine top-down and bottom-up approaches, factoring in urban housing handovers, organized brand penetration rates, average ticket size per kitchen, regional mix, and renovation cycles. Scenario analysis addresses interest-rate-led housing cycle variations and raw material cost movements.

India Modular Kitchen Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Floor Cabinet and Wall Cabinets, Tall Storage Cabinets, Others |

| Distribution Channels Covered |

|

| End-Users Covered | Residential, Commercial |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Asian Paints Ltd., Häfele, Spacewood Furnishers Pvt. Ltd., Homevista Decor and Furnishings Private Limited, Livspace, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India modular kitchen market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India modular kitchen market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India modular kitchen industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Modular Kitchen Market Report

The India modular kitchen market was valued at USD 3.62 Billion in 2025, supported by urban housing handovers, organized brand expansion, and rising aspirational demand.

The market is projected to grow at 3.16% CAGR from 2026 to 2034, reaching USD 4.86 Billion, driven by tier-2 city expansion and premiumization trends.

Floor cabinet and wall cabinets lead at 62.8% in 2025, forming the structural core of every kitchen layout. Tall storage cabinets at 23.6% are gaining ground.

Residential dominates at 78.6% in 2025, fueled by apartment handovers and nuclear families. Commercial at 21.4% is supported by cloud kitchens and hotel pantries.

North India commands 31.7% in 2025, led by Delhi-NCR, Lucknow, and Chandigarh, and remains the fastest-growing region through 2034. Rising urbanization and strong demand for modern, space-efficient housing solutions continue to reinforce the region’s market leadership.

Leading players include Asian Paints Ltd., Häfele, Spacewood Furnishers Pvt. Ltd., Homevista Decor and Furnishings Private Limited, and Livspace.

Urbanization, nuclear families, apartment handovers, organized brand expansion, smart appliance integration, and rising household income levels are key demand drivers.

Builder-developer bundling of modular kitchens into apartment handovers is creating a steady project channel pipeline and shifting purchase decisions upstream.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)