India Molecular Diagnostics Point of Care Market Size, Share, Trends and Forecast by Product and Service, Technology, Application, End User, and Region, 2026-2034

India Molecular Diagnostics Point of Care Market Summary:

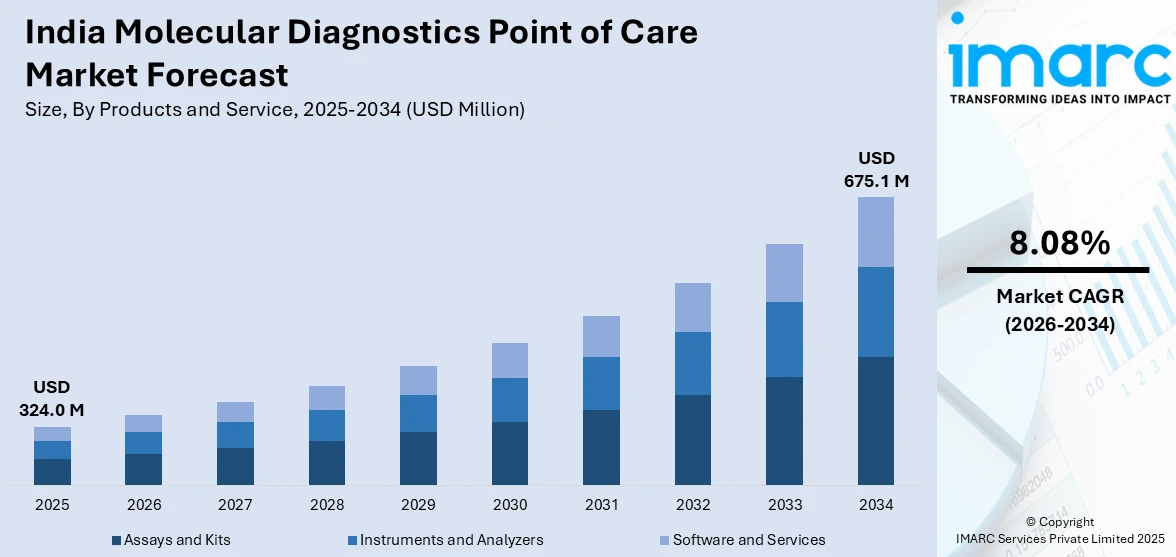

The India molecular diagnostics point of care market size was valued at USD 324.0 Million in 2025 and is projected to reach USD 675.1 Million by 2034, growing at a compound annual growth rate of 8.08% from 2026-2034.

The India molecular diagnostics point of care market is expanding as healthcare delivery shifts toward decentralized and rapid testing models. Growing demand for near-patient molecular testing, government emphasis on strengthening primary healthcare infrastructure, and advancements in portable diagnostic platforms are accelerating adoption. Rising focus on early disease detection and precision medicine is further reinforcing the India molecular diagnostics point of care market share.

Key Takeaways and Insights:

- By Product and Service: Assays and kits dominate the market with a share of 47.1% in 2025, driven by rising demand for ready-to-use molecular testing solutions enabling rapid pathogen detection at decentralized healthcare settings.

- By Technology: Polymerase chain reaction (PCR) held the largest market share of 43.5% in 2025, owing to its established sensitivity and accuracy for infectious disease detection across national disease surveillance programmes.

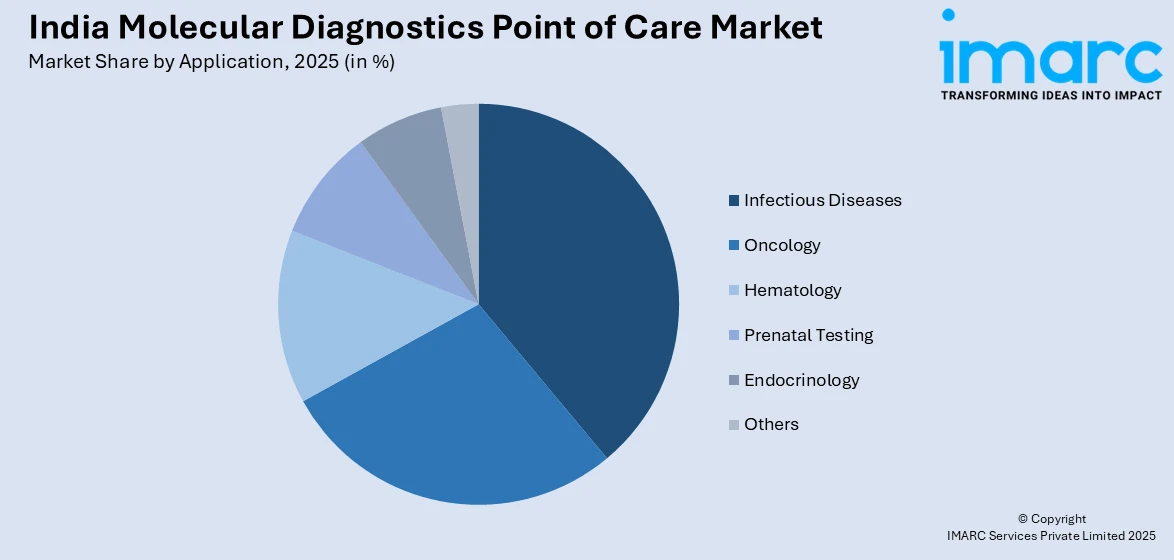

- By Application: Infectious diseases lead the market with a share of 38.9% in 2025, reflecting the persistent burden of tuberculosis, hepatitis, dengue, and other communicable diseases requiring rapid molecular detection.

- By End User: Physicians’ offices held the largest market share of 41.6% in 2025, supported by growing availability of compact molecular diagnostic devices enabling real-time clinical decision-making during patient consultations.

- By Region: West India dominated the market with a share of 35.2% in 2025, driven by the concentration of advanced healthcare facilities, diagnostic laboratories, and pharmaceutical infrastructure in the region.

- Key Players: The India molecular diagnostics point of care market exhibits dynamic competitive intensity, with domestic innovators and global diagnostic corporations expanding product portfolios, strengthening distribution networks, and investing in research and development.

To get more information on this market Request Sample

The India molecular diagnostics point of care market is progressing as healthcare delivery transitions toward rapid, decentralized, and patient-centric testing models. The growing prevalence of infectious and chronic diseases continues to drive demand for molecular diagnostic solutions that deliver accurate results within clinical consultation windows. In June 2024, Roche Diagnostics expanded access to its cobas Liat point-of-care molecular testing platform in India, enabling faster on-site detection of respiratory infections and supporting quicker clinical decision-making in hospitals and emergency settings. Government initiatives aimed at strengthening primary healthcare infrastructure and expanding diagnostic access in rural and semi-urban areas are playing a pivotal role in market expansion. Technological innovation in portable testing platforms and microfluidic devices is enabling molecular-level testing outside traditional laboratory environments. The integration of digital health frameworks with molecular diagnostics is further enhancing disease surveillance, treatment monitoring, and public health preparedness across the country, supporting the broader transition toward universal health coverage.

India Molecular Diagnostics Point of Care Market Trends:

Expansion of Multiplex Testing Capabilities at Near-Patient Settings

Multiplex molecular diagnostic platforms are gaining traction by enabling simultaneous detection of multiple pathogens from a single sample at the point of care. These systems significantly reduce testing time, conserve resources, and improve diagnostic accuracy, particularly for respiratory and febrile illnesses where symptom overlap makes clinical differentiation challenging without molecular confirmation. Moreover, BioFire Diagnostics (a bioMérieux company) expanded global deployment of its FilmArray multiplex PCR system, improving rapid clinical decision-making in emergency and primary care settings. The growing adoption of cartridge-based multiplex solutions at primary care facilities is streamlining workflows and supporting more effective patient management.

Integration of Artificial Intelligence with Molecular Diagnostic Platforms

Artificial intelligence and machine learning algorithms are being increasingly embedded into point-of-care molecular devices to enhance result interpretation and reduce operator dependency. AI-powered analytics enable automated quality control, predictive disease insights, and real-time data integration with public health surveillance systems. In May 2025, Diagnostics.ai launched the industry’s first CE-IVDR-certified transparent AI platform for real-time PCR molecular diagnostics, enabling laboratories and clinicians to trace exactly how AI-generated diagnostic results are produced while improving accuracy and regulatory compliance. This integration is particularly significant for resource-limited settings where trained laboratory personnel are scarce, allowing non-specialist healthcare workers to conduct complex molecular tests with greater confidence and diagnostic reliability.

Rising Adoption of Isothermal Amplification Technologies

Isothermal nucleic acid amplification technologies are emerging as viable alternatives to conventional thermal cycling methods for near-patient molecular diagnostics. These approaches enable rapid DNA amplification at constant temperatures without requiring sophisticated instrumentation, making them particularly suitable for rural health centres, community clinics, and mobile diagnostic units across underserved regions. According to reports, Abbott highlighted that its ID NOW platform leverages isothermal amplification at a constant temperature to deliver rapid molecular results within minutes, significantly reducing equipment complexity and enabling faster infectious disease detection in decentralized care settings. Their inherent simplicity, cost-effectiveness, and minimal infrastructure requirements are broadening molecular diagnostic access and supporting decentralized healthcare delivery models throughout the country.

Market Outlook 2026-2034:

The India molecular diagnostics point of care market is positioned for sustained expansion, supported by healthcare decentralization, rising disease burden, and continuous innovation in portable testing technologies. Growing government investment in primary healthcare, expanding insurance coverage, and rising public awareness about early disease detection are expected to accelerate adoption across urban, semi-urban, and rural settings. The convergence of digital health integration, miniaturized platforms, and expanded test menus will further strengthen the market trajectory over the forecast period. The market generated a revenue of USD 324.0 Million in 2025 and is projected to reach a revenue of USD 675.1 Million by 2034, growing at a compound annual growth rate of 8.08% from 2026-2034.

India Molecular Diagnostics Point of Care Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product and Service |

Assays and Kits |

47.1% |

|

Technology |

Polymerase Chain Reaction (PCR) |

43.5% |

|

Application |

Infectious Diseases |

38.9% |

|

End User |

Physicians’ Offices |

41.6% |

|

Region |

West India |

35.2% |

Products and Service Insights:

- Assays and Kits

- Instruments and Analyzers

- Software and Services

The assays and kits dominate with a market share of 47.1% of the total India molecular diagnostics point of care market in 2025.

Assays and kits represent the largest product segment, as healthcare facilities increasingly adopt ready-to-use molecular testing solutions for rapid and accurate pathogen detection. The growing availability of disease-specific assay kits designed for portable diagnostic platforms is expanding testing capabilities at primary healthcare centres, outpatient clinics, and rural health facilities across the country. According to reports, India’s Department of Biotechnology (DBT) supported the large-scale deployment of indigenous molecular diagnostic kits under its Biotechnology Industry Research Assistance Council (BIRAC) programs, strengthening domestic production and public-sector access to standardized RT-PCR and infectious disease test kits. Their standardized formulations and pre-configured reagent compositions further ensure consistent diagnostic performance across diverse clinical environments and operator skill levels.

The preference for assay kits is further supported by their ease of use, minimal training requirements, and compatibility with compact point-of-care instruments that enable sample-to-result workflows. Continuous development of multiplex assay panels covering respiratory infections, tropical febrile illnesses, and sexually transmitted diseases is broadening the diagnostic scope of near-patient molecular testing. The increasing availability of room temperature-stable reagent kits is also enhancing storage and distribution feasibility in regions with limited cold chain infrastructure, reinforcing this segment's leadership.

Technology Insights:

- Polymerase Chain Reaction (PCR)

- Hybridization

- DNA Sequencing

- Microarray

- Isothermal Nucleic Acid Amplification Technology (INAAT)

- Others

The polymerase chain reaction (PCR) leads with a share of 43.5% of the total India molecular diagnostics point of care market in 2025.

Polymerase chain reaction technology holds the largest share owing to its established reputation for high sensitivity, specificity, and reliability in detecting infectious and genetic disorders at the point of care. The miniaturization of PCR systems into portable, battery-operated devices has enabled real-time molecular testing at primary health centres and district hospitals beyond traditional laboratory settings. The widespread availability of validated PCR-based assay protocols for nationally prioritized diseases further strengthens adoption across both public and private healthcare networks.

The continued dominance of PCR technology is reinforced by endorsements from national and international health authorities for critical disease detection programmes. Ongoing advancements in micro-PCR chip technology, rapid thermal cycling, and automated sample preparation are further enhancing the speed, portability, and cost-effectiveness of PCR-based point-of-care solutions across diverse clinical settings. The development of integrated sample-to-result PCR cartridges requiring minimal hands-on time is also accelerating deployment among non-specialist operators at decentralized healthcare facilities throughout the country.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Infectious Diseases

- Oncology

- Hematology

- Prenatal Testing

- Endocrinology

- Others

The infectious diseases dominates with a market share of 38.9% of the total India molecular diagnostics point of care market in 2025.

Infectious diseases dominate the market reflecting the country's substantial burden of communicable diseases including tuberculosis, hepatitis, dengue, malaria, and respiratory infections. The persistent need for rapid and accurate pathogen identification at the patient site has made molecular diagnostics indispensable for timely clinical decision-making, infection control, and public health surveillance. The rising focus on antimicrobial resistance detection is further expanding the role of molecular testing in guiding targeted treatment strategies across healthcare settings.

The segment's prominence is further reinforced by national disease elimination programmes that prioritize molecular testing for early detection and drug resistance profiling. The deployment of portable molecular platforms across primary health centres and community health facilities is enabling faster diagnosis and treatment initiation, reducing disease transmission and improving patient outcomes. The growing integration of molecular diagnostic data with digital health reporting systems is also strengthening epidemiological monitoring and enabling more coordinated public health responses across endemic regions.

End User Insights:

- Physicians’ Offices

- Hospitals and ICUs

- Research Institutes

- Others

The physicians’ offices leads with a share of 41.6% of the total India molecular diagnostics point of care market in 2025.

Physicians' offices represent the largest end-user segment, driven by growing availability of compact, automated molecular testing devices enabling clinicians to obtain actionable diagnostic results during patient consultations. The ability to conduct molecular-level testing without referral to centralized laboratories is transforming clinical workflows and enabling same-visit diagnosis and treatment initiation. The rising patient expectation for immediate diagnostic clarity is further motivating physicians to integrate advanced molecular testing capabilities within their practice settings.

The increasing preference for near-patient molecular diagnostics in physicians' offices is supported by the development of simple, cartridge-based platforms requiring minimal technical expertise and infrastructure investment. As healthcare delivery models shift toward outpatient and community-based care, physicians are integrating point-of-care molecular testing into routine clinical practice, improving diagnostic turnaround times and overall patient satisfaction. The expanding reimbursement frameworks and growing awareness of molecular diagnostic benefits among primary care practitioners are also contributing to sustained adoption and utilization growth across this end-user segment.

Regional Insights:

- North India

- South India

- East India

- West India

West India exhibits a clear dominance with a 35.2% share of the total India molecular diagnostics point of care market in 2025.

West India commands the largest regional share, underpinned by well-established healthcare infrastructure, a high concentration of diagnostic laboratories, and a robust pharmaceutical and biotechnology ecosystem. States in this region benefit from strong urban healthcare networks, advanced medical research institutions, and progressive government health programmes supporting adoption of innovative diagnostic technologies. The presence of major industrial corridors and economic zones further attracts investment in healthcare innovation, creating a conducive environment for the deployment and scaling of advanced molecular diagnostic solutions.

The region's leadership is further strengthened by significant private sector investment in healthcare facilities, the expansion of organized diagnostic chains into smaller cities, and growing awareness of early disease detection among the population. The concentration of manufacturing and distribution hubs for diagnostic products facilitates faster market penetration and broader accessibility of point-of-care molecular testing solutions. Additionally, strong academic and clinical research collaborations within the region are driving innovation in diagnostic methodologies and supporting the validation and commercialization of indigenous molecular testing platforms.

Market Dynamics:

Growth Drivers:

Why is the India Molecular Diagnostics Point of Care Market Growing?

Rising Burden of Infectious and Chronic Diseases Driving Diagnostic Demand

The escalating prevalence of infectious diseases, including tuberculosis, hepatitis, dengue, malaria, and respiratory infections, combined with the growing incidence of chronic conditions such as diabetes, cardiovascular disorders, and cancer, is creating substantial demand for rapid diagnostic solutions at the point of care. In support of faster and more decentralized testing, the Government of India expanded the deployment of Molbio Diagnostics’ Truenat molecular testing platform under the National Tuberculosis Elimination Program to strengthen near-patient TB detection, improving access in remote and underserved regions. The need for immediate pathogen identification and disease marker detection to facilitate timely treatment decisions is compelling healthcare providers to adopt molecular diagnostic technologies that deliver laboratory-grade precision in near-patient environments. The expanding disease burden across urban, semi-urban, and rural populations is intensifying the requirement for decentralized testing capabilities, as centralized laboratory infrastructure alone cannot meet the rising diagnostic volumes and geographic distribution of patient needs across the country.

Government Initiatives Strengthening Primary Healthcare and Diagnostic Infrastructure

The government’s sustained investment in strengthening primary healthcare infrastructure through national health missions, digital health initiatives, and insurance coverage programmes is creating a supportive ecosystem for point-of-care molecular diagnostics adoption. Recent initiatives, including the inauguration of the National Virus Research & Diagnostic Laboratory Conclave 2025 and the launch of a national in-vitro diagnostics validation portal, further reinforce India’s commitment to enhancing diagnostic innovation, regulatory efficiency, and disease surveillance. The establishment and operationalization of health and wellness centres integrated public health laboratories, and district-level diagnostic facilities is expanding the network of healthcare touchpoints equipped to deliver advanced diagnostic services. Policy frameworks that prioritize decentralized testing for disease surveillance, elimination programmes, and pandemic preparedness are driving the deployment of portable molecular diagnostic platforms at the grassroots level, ensuring broader access to quality diagnostics in previously underserved regions and reducing dependence on overburdened centralized laboratory networks.

Technological Advancements in Portable and Automated Molecular Testing Platforms

Rapid advancements in diagnostic technology, including the miniaturization of polymerase chain reaction systems, development of microfluidic lab-on-chip devices, and introduction of isothermal amplification platforms, are significantly expanding the feasibility and scope of molecular testing at the point of care. These innovations are enabling battery-operated, sample-to-result diagnostic workflows that require minimal technical expertise and infrastructure, making molecular-level diagnostics accessible at primary health centres, physician offices, and field settings. The continuous expansion of test menus covering infectious, oncological, and genetic conditions, along with the integration of connectivity features for data management and disease reporting, is enhancing the clinical utility and adoption of point-of-care molecular solutions.

Market Restraints:

What Challenges the India Molecular Diagnostics Point of Care Market is Facing?

High Cost of Molecular Diagnostic Instruments and Consumables

The relatively high upfront cost of molecular diagnostic devices and the recurring expense of proprietary reagent cartridges and test kits present a significant barrier to widespread adoption, particularly in resource-constrained healthcare settings. Many primary healthcare facilities and smaller physician offices face budget limitations that restrict procurement and maintenance of advanced molecular testing platforms, slowing market penetration in rural and semi-urban areas where cost sensitivity remains high.

Limited Availability of Trained Healthcare Personnel for Molecular Testing

Despite advancements in automation and user-friendly device design, the effective operation and quality assurance of molecular point-of-care diagnostics requires baseline technical competence that remains scarce across many healthcare facilities. The shortage of trained laboratory technicians and healthcare workers with molecular diagnostics proficiency, particularly at peripheral health centres and underserved regions, hampers optimal utilization of deployed testing equipment and affects the reliability of diagnostic results.

Regulatory and Quality Standardization Challenges

The evolving regulatory landscape for in vitro diagnostic devices and the limited extent of laboratory accreditation across decentralized testing sites create challenges for ensuring consistent quality standards. Variations in regulatory approval timelines, absence of uniform proficiency testing requirements for point-of-care settings, and gaps in post-market surveillance mechanisms can affect the credibility of molecular diagnostic solutions deployed outside established laboratory networks.

Competitive Landscape:

The India molecular diagnostics point of care market is characterized by a dynamic competitive environment, with both domestic innovators and established multinational diagnostic corporations vying for market share. The competitive landscape is shaped by continuous product innovation, with participants focusing on developing portable, battery-operated, and fully automated molecular testing platforms capable of operating effectively in resource-limited environments. Strategic investments in research and development are driving the expansion of test menus across infectious diseases, oncology, and genetic testing applications. Market participants are actively pursuing partnerships with government health programmes, international public health agencies, and private healthcare networks to broaden distribution reach and accelerate device deployment. Pricing strategies, localized manufacturing capabilities, after-sales service networks, and regulatory compliance are emerging as critical competitive differentiators. The market is witnessing increasing focus on expanding geographic coverage into underserved areas, with participants strengthening last-mile distribution and training infrastructure to support broader adoption across primary healthcare settings.

Recent Developments:

-

In December 2025, CoSara Diagnostics, a joint venture between Co-Diagnostics and Ambalal Sarabhai Enterprises, advanced its point-of-care PCR platforms for tuberculosis and HPV into Phase II preclinical studies. The company is preparing for clinical validation in India, focusing on portable, decentralized molecular diagnostics to improve testing access in resource-limited healthcare settings.

India Molecular Diagnostics Point of Care Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Products and Services Covered |

Assays and Kits, Instruments and Analyzers, Software and Services |

|

Technologies Covered |

Polymerase Chain Reaction (PCR), Hybridization, DNA Sequencing, Microarray, Isothermal Nucleic Acid Amplification Technology (INAAT), Others |

|

Applications Covered |

Infectious Diseases, Oncology, Hematology, Prenatal Testing, Endocrinology, Others |

|

End Users Covered |

Physicians’ Offices, Hospitals and ICUs, Research Institutes, Others |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Molecular Diagnostics Point of Care Market Research Report Report

The India molecular diagnostics point of care market size was valued at USD 324.0 Million in 2025.

The India molecular diagnostics point of care market is expected to grow at a compound annual growth rate of 8.08% from 2026-2034 to reach USD 675.1 Million by 2034.

Assays and kits held the largest share of 47.1%, driven by widespread adoption of ready-to-use molecular testing solutions for rapid pathogen detection and compatibility with portable point-of-care diagnostic platforms across diverse healthcare settings.

Key factors driving the India molecular diagnostics point of care market include rising prevalence of infectious and chronic diseases, government healthcare infrastructure expansion, technological innovation in portable molecular platforms, and increasing demand for decentralized diagnostic testing solutions.

Major challenges include high instrument and consumable costs limiting adoption in resource-constrained settings, shortage of trained healthcare personnel for molecular testing, regulatory standardization gaps, infrastructure constraints in rural areas, and supply chain dependencies for imported reagents and components.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)