India Movie and Entertainment Market Size, Share, Trends and Forecast by Product, and Region, 2026-2034

India Movie and Entertainment Market Summary:

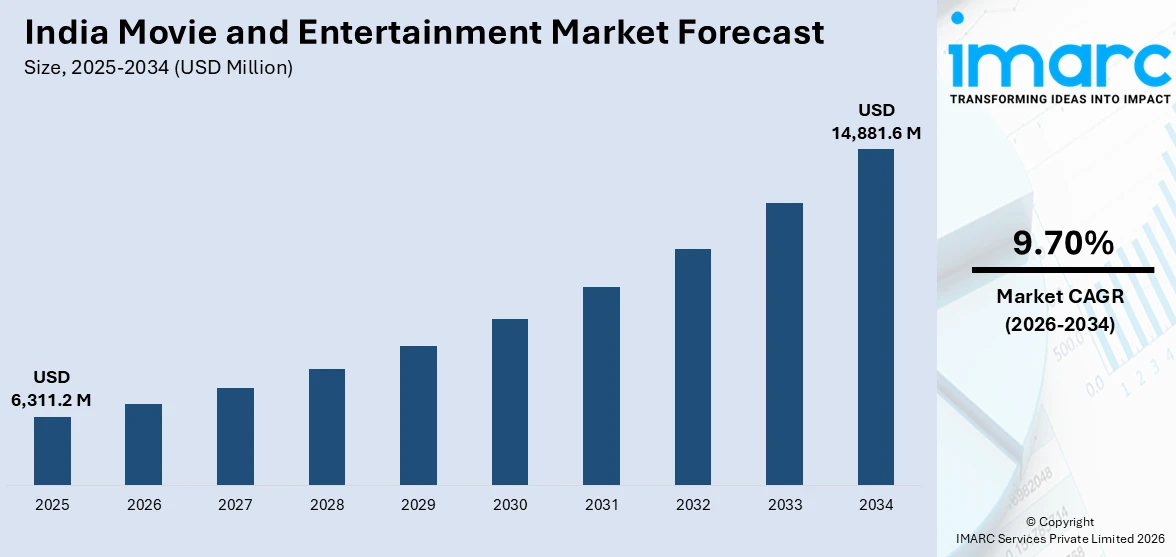

The India movie and entertainment market size was valued at USD 6,311.2 Million in 2025 and is projected to reach USD 14,881.6 Million by 2034, growing at a compound annual growth rate of 9.70% from 2026-2034.

The market is driven by increasing digital content consumption, expanding multiplex infrastructure, rising disposable incomes, and growing demand for diverse regional language content across the country. The proliferation of over-the-top streaming platforms, coupled with evolving consumer preferences for premium cinematic experiences, is further accelerating industry expansion. Additionally, favorable government initiatives supporting film production and entertainment ecosystem development are contributing to sustained momentum, reinforcing India movie and entertainment market share.

Key Takeaways and Insights:

-

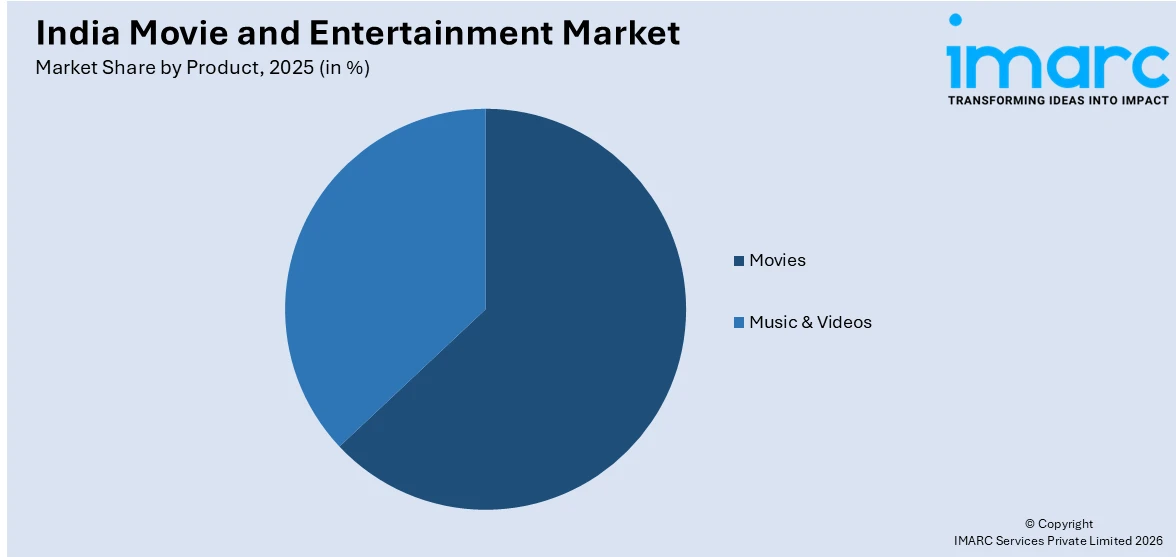

By Product: Movies dominate the market with a share of 62.8% in 2025, driven by cinema's deep cultural significance, robust theatrical release pipelines across multiple regional film industries, and rising investments in high-production-value content.

-

By Region: South India leads the market with a share of 35.6% in 2025, owing to the prolific output of Telugu, Tamil, Kannada, and Malayalam film industries, a deeply engaged moviegoing audience base, and expanding multiplex penetration.

-

Key Players: The India movie and entertainment market exhibits a highly competitive landscape, with established production houses competing alongside emerging independent content creators and global streaming platforms across theatrical, digital, and television segments.

To get more information on this market Request Sample

The India movie and entertainment market is experiencing robust growth underpinned by several converging demand-side and supply-side factors. Rapid urbanization and a burgeoning middle class are expanding the consumer base for premium entertainment experiences, including multiplexes and digital streaming subscriptions. The country's demographic advantage, characterized by a large and youthful population with increasing digital literacy, is fueling content consumption across platforms. As per sources, in 2025, Indian streaming giant JioHotstar committed approximately ₹4,000 crore ($445 million) to invest in South India’s creative economy over the next five years, reflecting major platform‑led content expansion and regional diversification efforts. Furthermore, the growing internationalization of Indian cinema, particularly regional language films gaining global recognition, is opening new revenue streams. Government policy support through production incentives and infrastructure development, along with advancements in filmmaking technology, is enabling higher-quality content creation and broader distribution capabilities across domestic and international markets.

India Movie and Entertainment Market Trends:

Rise of Regional Content as a Pan-India Phenomenon

Regional language films and entertainment content are increasingly transcending traditional geographic and linguistic boundaries to achieve pan-India appeal. Audiences across the country are embracing content from diverse film industries, driven by dubbing, subtitling, and digital distribution capabilities. According to reports, in 2025, platforms have doubled down on regionalisation, with nearly 50% of Zee5’s viewership coming from non‑Hindi content and titles and Identity gaining traction even among Hindi viewers, highlighting how regional storytelling now drives national consumption. This cultural shift is reshaping content commissioning strategies, with producers investing in stories rooted in regional authenticity that carry universal narrative appeal.

Premiumization of the Cinematic Experience

The Indian entertainment landscape is witnessing a marked shift toward premium viewing formats and immersive theatrical experiences. Audiences are increasingly willing to pay for enhanced offerings such as large-format screens, advanced sound systems, luxury seating, and dine-in cinema concepts. In November 2025, PVR INOX launched its luxury Cinemagic multiplex in Delhi, featuring gaming zones, nail bars, perfumery corners, and gourmet dining, aiming to transform cinemas into lifestyle destinations. This premiumization trend is particularly prominent in metropolitan and tier-one cities, where entertainment spending patterns are evolving toward quality over quantity.

Integration of Technology in Content Creation and Distribution

Advanced technologies are fundamentally reshaping how entertainment content is produced, distributed, and consumed in India. Virtual production techniques, visual effects capabilities, and artificial intelligence-driven tools are enabling filmmakers to achieve cinematic quality previously associated only with international productions. In February 2026, Invideo partnered with Google Cloud to launch enterprise‑grade AI filmmaking tools at the India AI Film Festival, integrating generative and cloud technologies to streamline production pipelines for studios and creators. Simultaneously, data analytics and algorithmic recommendation engines are transforming content distribution by enabling platforms to personalize viewer experiences and optimize content acquisition strategies.

Market Outlook 2026-2034:

The India movie and entertainment market is poised for sustained revenue expansion through the forecast period, supported by rising consumer spending on entertainment, accelerating digital infrastructure development, and increasing content monetization opportunities across theatrical, streaming, and ancillary revenue channels. The proliferation of affordable internet connectivity and smartphone penetration is expected to unlock significant demand from semi-urban and rural populations. Strategic investments in content libraries, regional film ecosystems, and immersive entertainment technologies are anticipated to drive revenue diversification. The market generated a revenue of USD 6,311.2 Million in 2025 and is projected to reach a revenue of USD 14,881.6 Million by 2034, growing at a compound annual growth rate of 9.70% from 2026-2034.

India Movie and Entertainment Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product |

Movies |

62.8% |

|

Region |

South India |

35.6% |

Product Insights:

Access the comprehensive market breakdown Request Sample

- Movies

- Music & Videos

Movies dominate with a market share of 62.8% of the total India movie and entertainment market in 2025.

The movies command the largest share of the India movie and entertainment market, reflecting cinemas deeply embedded cultural role in Indian society. Theatrical releases across Hindi, Telugu, Tamil, and other regional industries generate substantial box office revenue, supported by a vast network of single screens and rapidly expanding multiplex chains. According to reports, Dhurandhar crossed the 1000 crore India gross milestone, becoming the first single‑language Hindi film to achieve this domestic theatrical record, highlighting the enduring appeal of major pan‑India releases.

In addition, the film industry is undergoing a shift with the changing nature of revenue streams that go beyond the conventional window periods. The digital distribution rights, satellite broadcasting rights, and international theatrical releases are opening up new revenue streams for film producers. The trend of releasing films in multiple languages at the same time is increasing the reach of individual films, and the rising production costs are allowing filmmakers to produce content that is spectacle-driven, thus emphasizing the theatrical experience as a distinct form of entertainment that is different from home viewing.

Regional Insights:

- North India

- South India

- East India

- West India

South India leads with a market share of 35.6% of the total India movie and entertainment market in 2025.

South India leads the regional segmentation of the India movie and entertainment market, driven by the exceptionally prolific output and commercial success of the Telugu, Tamil, Kannada, and Malayalam film industries. The region benefits from a deeply ingrained moviegoing culture, with high per-capita cinema attendance and strong audience loyalty to regional stars and storytelling traditions. Expanding multiplex infrastructure across southern cities is further supporting premium ticket pricing and improved revenue realization per screen across both established metropolitan centers and rapidly growing tier-two urban markets.

The preeminence of South India is further supported by the fact that the region has been at the forefront of innovation and technology adoption in the Indian film industry. The southern film industry has always been at the forefront of visual effects integration, genre innovation, and story innovation, thereby creating content that is increasingly appealing to the masses. The success of dubbed and subtitled southern films in the Hindi-speaking market has opened up new avenues of revenue and has firmly established South India as the driving force behind the growth of the industry as a whole.

Market Dynamics:

Growth Drivers:

Why is the India Movie and Entertainment Market Growing?

Expanding Digital Infrastructure and Internet Penetration

The rapid expansion of affordable broadband and mobile internet connectivity across India is fundamentally transforming entertainment consumption patterns. Increasing smartphone adoption, particularly in semi-urban and rural areas, is creating vast new audiences for digital entertainment content. According to reports, India had 958 million active internet users, with rural areas accounting for 57% (approximately 548 million), and 61% of users consuming short-video content, highlighting expanding digital engagement. This infrastructure buildout enables content platforms to reach previously underserved populations, dramatically expanding the total addressable market.

Rising Disposable Incomes and Evolving Consumer Spending Priorities

India's expanding middle class, characterized by growing disposable incomes and evolving lifestyle aspirations, is driving increased expenditure on entertainment and leisure activities. Consumers are increasingly prioritizing experiential spending, including premium cinema visits, subscription-based streaming services, and live entertainment events. In 2025, Big Tree Entertainment, operating BookMyShow, posted ₹192 crore net profit, driven by strong growth in ticketing and live events, including concerts and music festivals. This shift in spending priorities is particularly pronounced among younger demographics who view entertainment as an integral component of their lifestyle.

Government Policy Support and Institutional Investment Framework

The Indian government's proactive stance in supporting the film and entertainment sector through favorable policies is creating a conducive environment for sustained industry growth. Initiatives including production subsidies, tax incentives for theatrical infrastructure development, and single-window clearance mechanisms for film shooting permissions are reducing operational barriers and encouraging investment. State-level film policies offering financial incentives for productions shot within their jurisdictions are stimulating regional content ecosystems. The granting of industry status to the film sector has further improved access to institutional financing, enabling producers to undertake ambitious large-scale projects.

Market Restraints:

What Challenges the India Movie and Entertainment Market is Facing?

Content Piracy and Intellectual Property Challenges

Unauthorized distribution and digital piracy remain significant impediments to revenue realization within the Indian entertainment industry. The widespread availability of pirated content through illicit websites and messaging platforms erodes legitimate revenue streams across theatrical and digital windows. Despite ongoing enforcement efforts, the scale and technological sophistication of piracy operations continue to outpace regulatory mechanisms, resulting in substantial revenue leakage.

Fragmented Distribution and Infrastructure Gaps

Significant disparities in entertainment infrastructure between urban and rural regions constrain overall market potential. While metropolitan areas benefit from modern multiplex facilities and reliable digital connectivity, large portions of semi-urban and rural India lack adequate theatrical screens and consistent internet bandwidth. This infrastructure fragmentation limits the addressable audience for premium content offerings and creates uneven revenue distribution across geographies.

High Content Production Costs and Financial Risk

The entertainment industry inherently involves substantial financial risk due to the unpredictable nature of audience reception and content performance. Rising production costs driven by talent compensation, technology adoption, and marketing expenditure are increasing financial stakes associated with each project. The hit-driven nature of the business means a significant proportion of releases fail to recover investments, discouraging independent production ventures.

Competitive Landscape:

The India movie and entertainment market is characterized by a dynamic and intensely competitive environment featuring a diverse mix of established conglomerates, regional production powerhouses, independent studios, and global streaming platforms. Competition spans multiple dimensions including content quality, talent acquisition, distribution reach, and technological capabilities. The market exhibits a layered competitive structure where large integrated entities with theatrical, digital, and broadcasting assets compete alongside agile, content-focused independent players. Strategic investments in original content libraries, exclusive talent partnerships, and technology-driven distribution are key competitive differentiators. The growing convergence of theatrical and digital ecosystems is intensifying competitive dynamics, as traditional players expand into streaming while digital-first platforms explore theatrical distribution, creating a fluid competitive landscape.

Recent Developments:

-

In February 2026, Almighty Motion Picture launched a new vertical, Almighty All In LLP, to create high-end legacy documentaries, premium brand films, and advertiser-funded programming. The initiative aims to enhance cinematic storytelling for Indian and global audiences, strengthen brand engagement, and integrate AI tools for historical and mythological narratives.

India Movie and Entertainment Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Products Covered |

Movies, Music & Videos |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Movie and Entertainment Market Report

The India movie and entertainment market size was valued at USD 6,311.2 Million in 2025.

The India movie and entertainment market is expected to grow at a compound annual growth rate of 9.70% from 2026-2034 to reach USD 14,881.6 Million by 2034.

Movies held the largest India movie and entertainment market share, driven by cinema's deep cultural significance, prolific regional film industry output across multiple languages, strong box office performance fueled by star-driven releases, and rapidly expanding multiplex infrastructure nationwide.

Key factors driving the India movie and entertainment market include expanding digital infrastructure and internet penetration, rising disposable incomes fueling premium entertainment demand, supportive government policies, growing regional content appeal, and increasing content monetization opportunities.

Major challenges include widespread content piracy undermining revenue realization, fragmented distribution infrastructure between urban and rural areas, high production costs with unpredictable returns, intense competition across platforms, and evolving regulatory frameworks governing digital content.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)