India Music Streaming Market Size, Share, Trends and Forecast by Revenue Model, Service, Platform, and Region, 2026-2034

India Music Streaming Market Summary:

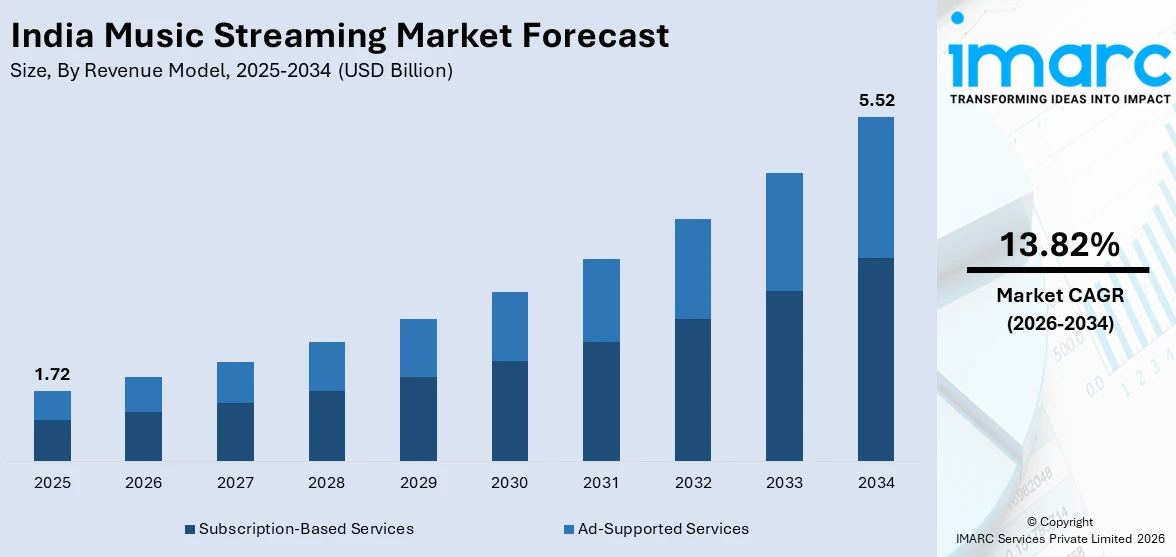

The India music streaming market size was valued at USD 1.72 Billion in 2025 and is projected to reach USD 5.52 Billion by 2034, growing at a compound annual growth rate of 13.82% from 2026-2034.

The market is fueled by the widespread use of smartphones, affordable mobile data plans, and the rapidly growing digital consumer base that favors on-demand audio entertainment. The rise of regional language content and vernacular music libraries is also expanding the base of listeners across various demographics and geographies. Moreover, the use of artificial intelligence for personalized recommendations and playlists is also improving user retention and stickiness, thus fueling the growing India music streaming market share.

Key Takeaways and Insights:

- By Revenue Model: Subscription‑based services dominate the market with a share of 67% in 2025, driven by growing consumer preference for ad-free listening, offline access, and premium audio quality features.

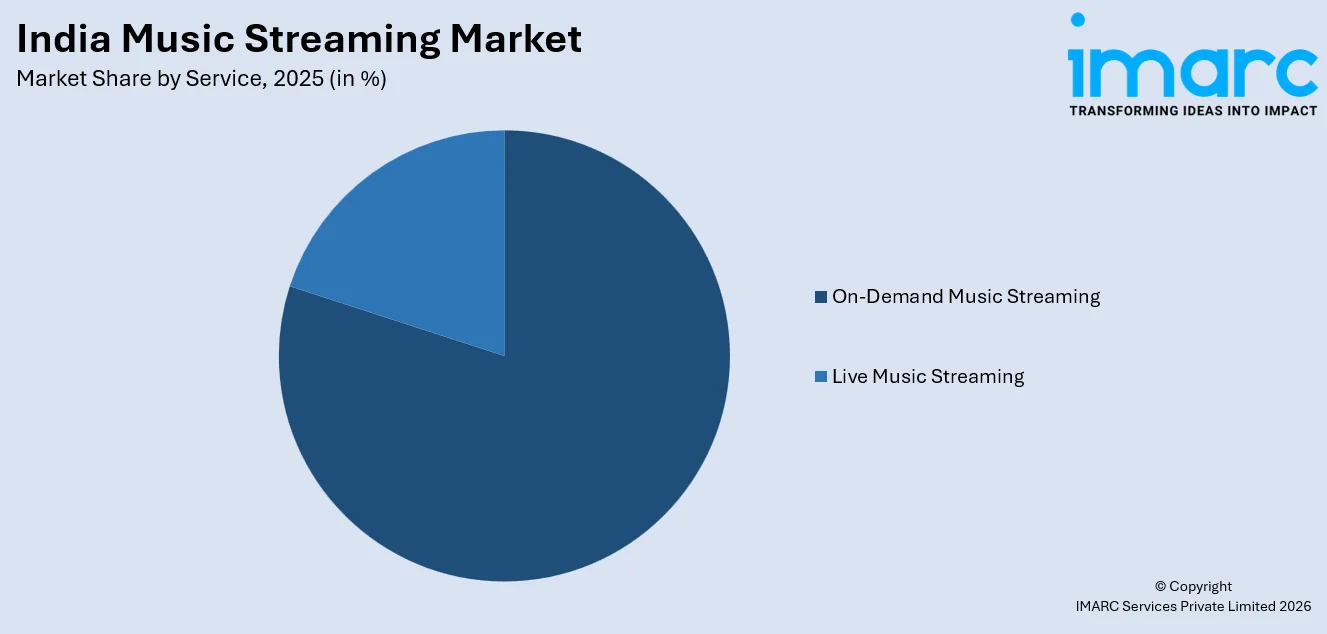

- By Service: On‑demand music streaming leads the market with a share of 80% in 2025, owing to its flexibility in track selection, personalized playlists, and multilingual catalogue access.

- By Platform: Application based represents the largest segment with a market share of 81% in 2025, driven by widespread smartphone adoption, intuitive mobile interfaces, and seamless device ecosystem integration.

- Key Players: The India music streaming market exhibits a highly competitive landscape, with global technology conglomerates vying alongside homegrown digital entertainment platforms across freemium and premium tiers. Strategic content licensing agreements, exclusive artist partnerships, and telco bundling strategies define competitive positioning.

To get more information on this market Request Sample

The India music streaming market is experiencing robust expansion fueled by a confluence of technological, demographic, and cultural factors. Rising internet penetration, particularly through affordable mobile data plans, has democratized access to digital music across urban and semi-urban populations. As per sources, in 2025, JioSaavn reported over 100 million monthly active users and highlighted that Hindi, Telugu, Punjabi, Tamil, and English remained the top five streamed languages, reinforcing the continued dominance of regional and multilingual content consumption across India’s diverse audience. The country’s youthful demographic profile, with a significant proportion of the population under the age of thirty-five, has created a massive base of digitally native consumers who prefer streaming over traditional music formats. The growing popularity of regional and vernacular music content has expanded the addressable audience beyond Hindi and English language listeners, enabling platforms to penetrate previously underserved linguistic markets.

India Music Streaming Market Trends:

Growth of Regional and Vernacular Music Content

The India music streaming market is witnessing a significant surge in demand for regional and vernacular music content as platforms expand their catalogues to cater to linguistically diverse audiences. According to reports, in 2025, Gaana’s mid‑year report highlighted that listeners in India’s metros and tier‑2 cities were increasingly tuning into diverse linguistic and musical styles, with regional artists from Maharashtra, Haryana, Tamil Nadu, and Bihar topping charts and reshaping national listening habits. Listeners across states are increasingly seeking music in their native languages, moving beyond the traditional dominance of Bollywood soundtracks and Hindi-language content.

Integration of Podcasts and Non-Music Audio Content

Music streaming platforms in India are increasingly diversifying their content offerings by integrating podcasts, audiobooks, and spoken‑word programming alongside traditional music libraries to reflect evolving consumer preferences for varied audio entertainment. As per sources, Spotify relaunched its creator programs for podcasters in India, such as the Managed Partner Program and PodStart, boosting support for creators producing content in Hindi, Tamil, and English, and noting that one in every four music listeners on the platform now also consumes podcasts. This strategic expansion extends beyond music to include storytelling, educational content, and conversational shows, with platforms commissioning exclusive podcast series and partnering with independent creators to build differentiated audio ecosystems.

Rise of Social and Collaborative Listening Features

A notable trend shaping the India music streaming market is the growing integration of social and collaborative listening functionalities within streaming applications. Platforms are introducing features that enable users to share playlists, co-listen in real time with friends, and discover music through social feeds and community recommendations. These social engagement tools are particularly resonating with younger demographics who view music consumption as an inherently communal and shareable experience. The incorporation of social elements is driving organic user acquisition through peer recommendations and fostering community-driven content discovery across streaming services.

Market Outlook 2026-2034:

The revenue of the music streaming industry in India is expected to grow significantly over the forecast period, driven by the rising adoption of subscription services, the increasing penetration of the internet in rural areas with the expansion of mobile networks, and the accelerating diversification of content offerings such as podcasts and live audio events. The industry is also driven by the changing monetization models, including tiered pricing and telecommunications partnerships, which are expanding the base of premium subscribers. The market generated a revenue of USD 1.72 Billion in 2025 and is projected to reach a revenue of USD 5.52 Billion by 2034, growing at a compound annual growth rate of 13.82% from 2026-2034.

India Music Streaming Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Revenue Model |

Subscription‑Based Services |

67% |

|

Service |

On‑Demand Music Streaming |

80% |

|

Platform |

Application Based |

81% |

Revenue Model Insights:

- Subscription-Based Services

- Ad-Supported Services

Subscription‑based services dominate with a market share of 67% of the total India music streaming market in 2025.

Subscription-based services lead the India music streaming market as consumers increasingly prioritize ad-free, uninterrupted listening experiences with premium audio quality and offline download capabilities. In October 2025, JioSaavn launched a new annual Pro subscription plan priced at Rs 399 that offers ad‑free music and offline downloads for 12 months, aimed at making premium access more affordable and driving paid user growth in India. The growing digital payments infrastructure across India, including the widespread adoption of unified payments interfaces, has significantly reduced friction in converting free-tier users to paid subscribers.

The rising adoption of the subscription model is also being driven by exclusive content strategies, where the platforms are acquiring first-release rights for popular albums, regional music catalogs, and original audio programming content. This is because exclusivity is offering a compelling value proposition that differentiates the paid offerings from the free ones. Additionally, the adoption of tiered subscription models at various price points is allowing the platforms to monetize various income segments, ranging from students to urban professionals.

Service Insights:

Access the comprehensive market breakdown Request Sample

- On-Demand Music Streaming

- Live Music Streaming

On‑demand music streaming leads with a share of 80% of the total India music streaming market in 2025.

On-demand music streaming dominates the India music streaming market as the preferred service model, offering users complete control over their listening experience with the ability to search, select, and replay specific tracks at any time. As per sources, in December 2025, Spotify revealed through its Wrapped 2025 data that “Raanjhan” by Sachet‑Parampara became the most‑streamed song in India with over 246 million streams, highlighting how on‑demand listening patterns reflect localized and user‑driven preferences.

The on-demand dominance is further strengthened by advancements in streaming technology, such as adaptive bitrate streaming, which allows audio quality to be adjusted according to network conditions, ensuring a smooth experience even on slower mobile networks that are more common in semi-urban and rural areas. The players are also working to enhance their on-demand services with functionalities such as lyrics display, mood-based playlists, and recommendations that are context-specific, based on time of day and user activity.

Platform Insights:

- Application Based

- Web Based

Application based exhibits a clear dominance with a 81% share of the total India music streaming market in 2025.

Application based platforms hold the largest share of the India music streaming market, driven by the country’s massive smartphone user base and the convenience of dedicated mobile applications that provide optimized streaming experiences. In December 2025, Indian artists were streamed 11.2 billion times by new listeners on digital platforms, with nearly two-thirds of royalties in India coming from local artists, highlighting the role of mobile apps in promoting domestic music consumption. These applications leverage device-native functionalities including push notifications, background playback, widget controls, and integration with vehicle infotainment systems to deliver seamless and accessible music consumption.

The application based platform advantage is further strengthened by the ecosystem integrations that mobile applications enable, including social media sharing capabilities, voice assistant compatibility, and smartwatch connectivity. Platforms continuously optimize their mobile applications for performance on entry-level and mid-range smartphones that constitute the majority of devices in the Indian market, ensuring broad accessibility across different hardware configurations. Regular feature updates, personalized home screens, and data-efficient streaming modes designed for users with limited data plans contribute to the sustained dominance of application-based platforms in the Indian music streaming landscape.

Regional Insights:

- North India

- South India

- East India

- West India

North India represents a significant share of the India music streaming market, driven by high population density across Uttar Pradesh, Delhi, Rajasthan, and Punjab. Well-developed urban digital infrastructure in metropolitan centers like Delhi-NCR supports strong smartphone penetration. The region's vibrant musical traditions spanning Punjabi pop, Bollywood soundtracks, and devotional genres sustain diverse streaming demand.

South India is a rapidly growing contributor to the India music streaming market, fueled by strong affinity for language-specific content in Tamil, Telugu, Kannada, and Malayalam. Thriving regional film industries in Chennai, Hyderabad, and Bengaluru generate popular soundtracks driving streaming consumption, positioning the region as a key growth engine for vernacular content.

East India presents emerging growth opportunities in the music streaming market, with West Bengal, Odisha, Bihar, and Jharkhand gradually increasing their digital consumption footprint. The region's rich cultural heritage in Bengali music, Odia folk traditions, and Bhojpuri popular music creates distinct content demand, supported by expanding mobile internet coverage across tier-two cities.

West India constitutes a major market for music streaming, anchored by the commercial and entertainment hub of Mumbai along with digitally active urban centers across Gujarat, Maharashtra, and Goa. The presence of the Bollywood film industry in Mumbai generates a constant flow of popular Hindi film music dominating national streaming charts.

Market Dynamics:

Growth Drivers:

Why is the India Music Streaming Market Growing?

Expanding Smartphone Penetration and Affordable Mobile Data Access

The India music streaming market is experiencing sustained growth driven by the rapid expansion of smartphone ownership across both urban and rural demographics. As per sources, average monthly data usage per Indian reached 27.5 GB, while 5G traffic surged threefold, supported by 271 million active 5G devices, boosting digital content and streaming adoption. The availability of affordable smartphones at multiple price points has made digital content consumption accessible to millions of new users who previously relied on traditional media formats. Simultaneously, the dramatic reduction in mobile data costs has made streaming economically viable for price-sensitive consumers.

Rising Preference for Personalized and On-Demand Entertainment

The growing need for personalized and on-demand entertainment experiences among consumers is one of the key drivers of the music streaming market in India. Indian music enthusiasts, especially the younger generation, are increasingly seeking personalized music experiences that are aligned with their tastes, moods, and contexts, as opposed to the conventional radio or album-based experiences. The music streaming industry is meeting this requirement by employing advanced artificial intelligence and machine learning algorithms that have the ability to analyze the listening patterns of consumers and offer them highly personalized playlists and song recommendations.

Strategic Telecommunications Partnerships and Bundled Service Offerings

Strategic partnerships between music streaming platforms and telecommunications operators represent a significant growth driver for the India music streaming market. These collaborations enable streaming services to reach massive subscriber bases by bundling premium music access with mobile data plans and postpaid packages, effectively reducing standalone subscription costs for consumers. In November 2025, Tata Play partnered with Apple Music to offer subscribers up to four months of free access to Apple Music across its mobile, Binge, and Fiber services, extending the reach of music streaming via telecom‑linked platforms in India.

Market Restraints:

What Challenges the India Music Streaming Market is Facing?

Low Average Revenue Per User and Monetization Challenges

The music streaming market in India is challenged by high levels of monetization difficulties due to very low average revenue per user. The fact that free music streaming services with advertisements are very common and that music content is available for free on video platforms limits the willingness of consumers to pay for music streaming services.

Complex Music Licensing and Rights Management

The fragmented music rights landscape in India presents a persistent restraint for streaming platforms. Negotiating licensing agreements across multiple record labels, independent artists, film production houses, and regional music publishers involves significant legal complexity and high content acquisition costs, creating operational inefficiencies and content availability gaps that limit platform catalogues.

Digital Piracy and Unauthorized Content Distribution

Digital piracy and unauthorized distribution of music content continue to undermine revenue potential in the India music streaming market. Despite growing awareness of intellectual property rights, pirated music remains widely accessible through informal channels, social media file sharing, and unauthorized applications, reducing the perceived value of legitimate streaming subscriptions.

Competitive Landscape:

The India music streaming market is characterized by intense competition among a diverse mix of global technology platforms and domestic digital entertainment services. The competitive landscape features players differentiating through content library depth, regional language coverage, pricing strategies, audio quality, and exclusive content partnerships. Market participants are increasingly leveraging artificial intelligence and machine learning capabilities to enhance personalization and user experience as key competitive differentiators. Strategic partnerships with telecommunications providers, device manufacturers, and content creators serve as critical tools for user acquisition and retention.

Recent Developments:

- In November 2025, Spotify introduced lossless audio streaming in India with a revamped three-tier Premium plan. Starting at Rs 139, the new lineup includes Premium Lite, Standard, and Premium Platinum, with the top tier offering lossless audio, AI-powered playlists, and family sharing, enhancing the music streaming experience for Indian users.

India Music Streaming Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Revenue Models Covered | Subscription-Based Services, Ad-Supported Services |

| Services Covered | On-Demand Music Streaming, Live Music Streaming |

| Platforms Covered | Application-Based, Web-Based |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Music Streaming Market Report

The India music streaming market size was valued at USD 1.72 Billion in 2025.

The India music streaming market is expected to grow at a compound annual growth rate of 13.82% from 2026-2034 to reach USD 5.52 Billion by 2034.

Subscription-based services held the largest share, driven by growing consumer preference for ad-free listening, offline access capabilities, premium audio quality, and competitive pricing strategies including telco-bundled subscription plans that enhance overall user experience.

Key factors driving the India music streaming market include expanding smartphone penetration, affordable mobile data access, rising preference for personalized on-demand entertainment, strategic telco partnerships, and growing demand for regional and vernacular music content.

Major challenges include low average revenue per user, complex music licensing and rights management frameworks, digital piracy and unauthorized content distribution, intense price competition, and the prevalence of free music access through video streaming platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)