India Nanosatellite And Microsatellite Market Size, Share, Trends and Forecast by Satellite Mass, Component, Application, End-Use Sector, and Region, 2026-2034

India Nanosatellite And Microsatellite Market Summary:

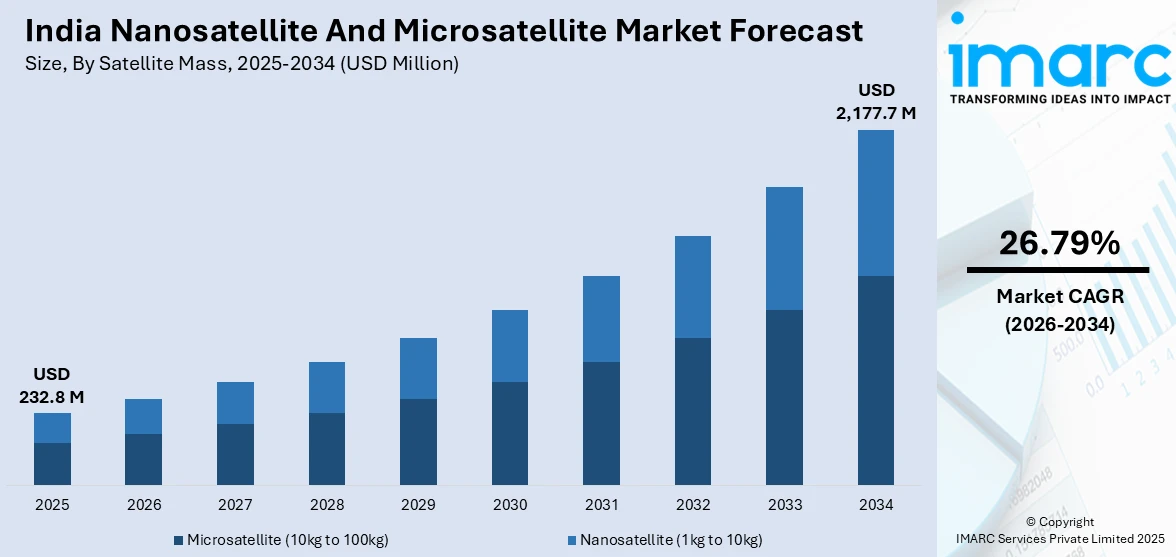

The India nanosatellite and microsatellite market size was valued at USD 232.8 Million in 2025 and is projected to reach USD 2,177.7 Million by 2034, growing at a compound annual growth rate of 26.79% from 2026-2034.

Driven by government initiatives to democratize space access and bolster indigenous satellite manufacturing capabilities, the market is witnessing unprecedented growth. Policy reforms are also catalyzing private sector participation with technology startups. The development of dedicated launch vehicles for small satellites and growing demand for real-time Earth observation data across agriculture, disaster management, and defense sectors are expanding the India nanosatellite and microsatellite market share.

Key Takeaways and Insights:

- By Satellite Mass: Microsatellite 10kg to 100kg dominates the market with 52.4% share in 2025, driven by enhanced payload capacities enabling complex multi-sensor missions and superior performance for defense surveillance and broadband communication applications.

- By Component: Hardware leads the market with 58.7% share in 2025, reflecting strong demand for satellite bus systems, propulsion modules, and onboard subsystems as indigenous manufacturing capabilities expand through public-private partnerships and technology transfer agreements.

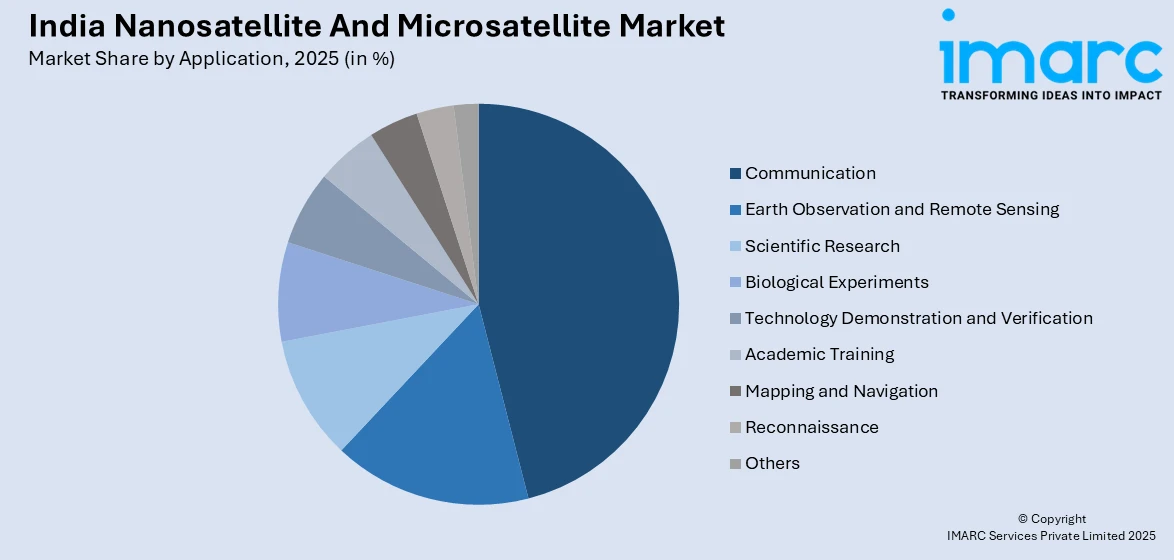

- By Application: Communication accounts for 45.9% market share in 2025, addressing India's rural connectivity challenges where only forty-nine percent of the population has internet access and satellite-based solutions bridge infrastructure gaps in remote terrains.

- By End-Use Sector: Government represents 39.2% market share in 2025, propelled by defense modernization programs, sovereign Earth observation requirements, and strategic investments in intelligence, surveillance, and reconnaissance satellite constellations.

- By Region: South India holds 31.5% market share in 2025, anchored by Bengaluru's concentration of space technology startups, proximity to launch facilities at Sriharikota, and Karnataka's ambitious space policy targeting fifty percent of the national market.

- Key Players: The market exhibits intensifying competition between established aerospace corporations and emerging Indian space technology startups, with international collaboration agreements expanding as domestic players demonstrate satellite platform capabilities alongside global vendors.

To get more information on this market Request Sample

India's small satellite sector represents a strategic convergence of technological advancement and policy enablement, positioning the nation as a cost-competitive hub for satellite manufacturing and launch services. The Indian Space Research Organisation's proven track record of launching 390 foreign satellites since 2014 demonstrates operational reliability, while recent missions showcase indigenous innovation. In January 2024, the Polar Satellite Launch Vehicle successfully deployed Dhruva Space's P-30 nanosatellite platform during the PSLV-C58 mission, validating commercial payload hosting capabilities. This achievement followed the historic February 2017 mission that placed 104 satellites into orbit in a single launch, establishing India's credentials in multi-satellite deployment. The government's allocation of a Rs. 1,000 crore venture capital fund in October 2024 specifically for space sector signals sustained commitment to sector growth, complementing infrastructure investments and regulatory frameworks that enable private entities to design, build, and operate satellite constellations for both domestic and international markets.

India Nanosatellite And Microsatellite Market Trends:

Government-Led Space Sector Liberalization

India's regulatory landscape transformation is catalyzing unprecedented private sector participation in small satellite development and deployment. The National Space Promotion and Authorisation Centre announced plans for 25 small satellite launches via three fully operational small satellite launch vehicle (SSLVs) annually during 2025, representing a significant acceleration from the historical average of three annual launches. This expansion includes dedicated missions for the Small Satellite Launch Vehicle, an Indian Space Research Organisation rocket specifically engineered for the nanosatellite and microsatellite market. The liberalized policy framework permits private companies to access government launch facilities, ground stations, and testing infrastructure, eliminating traditional barriers to entry that previously confined space activities to state-run organizations.

Indigenous Constellation Development Through Public-Private Partnerships

Commercial satellite constellation programs are reshaping India's Earth observation capabilities through innovative partnership models between government agencies and private enterprises. In 2025, the Indian National Space Promotion and Authorization Centre awarded a consortium led by Pixxel, alongside strategic partners Dhruva Space, PierSight, and SatSure, a contract valued at Rs. 1,200 crore for India's first fully indigenous Earth observation satellite constellation comprising twelve satellites. This landmark public-private partnership mandates domestic manufacturing, Indian rocket launches, and ground control within national boundaries, advancing data sovereignty objectives while demonstrating commercial viability of small satellite constellations for delivering sub-meter resolution imagery, synthetic aperture radar capabilities, and hyperspectral sensing for precision agriculture, infrastructure monitoring, and disaster response applications.

Regional Manufacturing Hubs and Technology Ecosystem Development

Karnataka state's Draft Space Technology Policy 2024-2029 exemplifies regional initiatives driving manufacturing infrastructure development and talent cultivation for the small satellite sector. The policy envisions capturing 50% of India's national space market and 5% of the global space economy, establishment of specialized manufacturing clusters, and support for over 500 startups and medium-sized enterprises with funding assistance, intellectual property development, and quality certification programs. These regional ecosystems are complementing national initiatives, with Tata Advanced Systems establishing facilities capable of producing low Earth orbit satellites annually, while Bengaluru's concentration of space technology companies creates synergies between satellite design firms, component manufacturers, and service providers that accelerate innovation cycles and reduce development costs.

Market Outlook 2026-2034:

The India nanosatellite and microsatellite market demonstrates robust expansion potential driven by converging factors including defense modernization requirements, commercial Earth observation demand, and satellite communication infrastructure development. The market generated a revenue of USD 232.8 Million in 2025 and is projected to reach a revenue of USD 2,177.7 Million by 2034, growing at a compound annual growth rate of 26.79% from 2026-2034. Government commitments to invest in space-related contract awards over the coming years, coupled with private sector deployment of constellation networks for broadband connectivity and imaging services, position India among the fastest-growing regional markets globally. The maturation of indigenous launch capabilities through the Small Satellite Launch Vehicle program reduces dependency on foreign launch providers while lowering mission costs, enabling more frequent satellite deployments across government, commercial, and academic sectors.

India Nanosatellite And Microsatellite Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Satellite Mass |

Microsatellite (10kg to 100kg) |

52.4% |

|

Component |

Hardware |

58.7% |

|

Application |

Communication |

45.9% |

|

End-Use Sector |

Government |

39.2% |

|

Region |

South India |

31.5% |

Satellite Mass Insights:

- Nanosatellite (1kg to 10kg)

- Microsatellite (10kg to 100kg)

Microsatellite (10kg to 100kg) dominates with a market share of 52.4% of the total India nanosatellite and microsatellite market in 2025.

The microsatellite segment's market leadership reflects its optimal balance between payload capacity, mission complexity, and cost efficiency for India's diverse space applications. These platforms accommodate multiple sensors, advanced communication systems, and extended operational lifetimes that nanosatellites cannot support, making them essential for defense surveillance requiring high-resolution optical and radar imaging, telecommunications missions demanding significant transponder power, and scientific experiments needing substantial onboard processing capabilities. The Indian Space Research Organisation's proven microsatellite platforms serve as foundation for commercial variants, while private sector development of standardized bus architectures reduces manufacturing timelines and enables customization for specific mission requirements without complete redesign efforts.

Defense and intelligence agencies particularly favor microsatellites for strategic reconnaissance and secure communications, as larger form factors permit encryption hardware, maneuvering propulsion, and radiation-hardened electronics necessary for military specifications. The segment benefits from government contracts prioritizing indigenous manufacturing, with specifications often requiring satellite masses in the microsatellite range to accommodate mission payloads. Commercial operators deploying broadband communication constellations similarly select microsatellite platforms for their ability to carry high-throughput Ka-band transponders and phased array antennas that deliver competitive data rates, while Earth observation companies leverage the additional capacity for hyperspectral sensors and synthetic aperture radar systems that generate premium-value data products for agriculture, mining, and infrastructure monitoring applications.

Component Insights:

- Hardware

- Software and Data Processing

- Space Services

- Launch Services

Hardware leads with a share of 58.7% of the total India nanosatellite and microsatellite market in 2025.

Hardware components form the foundation of satellite functionality, encompassing structural platforms, power systems, attitude control mechanisms, propulsion modules, and payload instruments that collectively determine mission performance and reliability. India's expanding manufacturing capabilities in satellite hardware benefit from technology transfer agreements, joint ventures with international aerospace firms, and investments in domestic production facilities that reduce import dependencies while building local expertise. Companies are establishing assembly lines for satellite structures, while specialized manufacturers produce solar panels, reaction wheels, and thermal management systems that meet international quality standards, creating supply chains that support both government programs and commercial ventures.

The hardware segment captures value across satellite bus platforms, subsystem integration, and payload development, with government initiatives promoting indigenous content requirements that mandate minimum percentages of domestically manufactured components in publicly funded missions. This policy environment stimulates investments in manufacturing infrastructure, quality testing facilities, and component certification processes that enhance India's competitive position in global satellite supply chains. Private sector startups are developing modular satellite platforms that allow rapid configuration for different mission profiles, reducing non-recurring engineering costs while enabling volume production that brings economies of scale. The emphasis on hardware extends to ground segment equipment including satellite control systems, telemetry receivers, and data processing stations that complete the end-to-end value chain, particularly as private operators establish ground networks to support their constellation operations without relying exclusively on government facilities.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Communication

- Earth Observation and Remote Sensing

- Scientific Research

- Biological Experiments

- Technology Demonstration and Verification

- Academic Training

- Mapping and Navigation

- Reconnaissance

- Others

Communication exhibits a clear dominance with a 45.9% share of the total India nanosatellite and microsatellite market in 2025.

Communication applications drive substantial market demand as satellite-based connectivity addresses India's persistent infrastructure challenges in connecting remote, rural, and geographically challenging regions where terrestrial networks prove economically unviable. With the population having internet access and deployment costs in remote areas running higher than urban zones, satellite communication emerges as the most practical solution for bridging the digital divide. The government's Digital India initiative, Smart Cities mission, and rural broadband programs align with satellite capabilities, while commercial operators view India's underserved markets as opportunities for high-throughput satellite services that can deliver broadband connectivity, video distribution, and enterprise networking solutions.

Small satellites in communication applications support diverse use cases including maritime vessel tracking through automatic identification systems, aircraft connectivity during oceanic flights, internet of things networks for asset monitoring across agriculture and logistics sectors, and emergency communications during natural disasters when terrestrial infrastructure fails. The rise of low Earth orbit constellations provides lower latency compared to geostationary satellites, making real-time applications feasible while reducing ground terminal costs through smaller antenna requirements. Indian operators are developing regional constellation architectures optimized for domestic coverage, leveraging the nation's geographical position and orbital slots to deliver competitive services. The segment benefits from regulatory clarity on spectrum allocation and licensing procedures, with the Indian National Space Promotion and Authorisation Centre streamlining approval processes for satellite communication operators while maintaining national security oversight through appropriate safeguards and monitoring mechanisms.

End-Use Sector Insights:

- Government

- Civil

- Commercial

- Defense

- Energy and Infrastructure

- Others

Government leads with a share of 39.2% of the total India nanosatellite and microsatellite market in 2025.

Government agencies constitute the dominant end-user segment through sustained investments in Earth observation, communications, and scientific missions that fulfill strategic priorities including border surveillance, disaster management, agricultural monitoring, and space exploration. The Indian Space Research Organisation operates extensive satellite programs supporting multiple government departments, while defense forces increasingly deploy dedicated military satellites for secure communications, electronic intelligence gathering, and real-time battlefield surveillance. The government's commitment to developing indigenous capabilities rather than relying on foreign satellite data or services drives procurement of domestically manufactured small satellites, creating stable demand that supports industry development and technology advancement.

Recent policy directions emphasize expanding satellite capacity across government functions, with the Ministry of Defence announcing plans to establish intelligence, surveillance, and reconnaissance satellite constellations equipped with optical and hyperspectral sensors to reduce dependency on international sources. The gap between India's military satellites and major powers operating hundreds of such assets motivates modernization programs that favor small satellite approaches for rapid deployment, constellation resilience, and cost-effective capacity expansion. Government applications extend beyond defense to include the Ministry of Agriculture's crop monitoring programs, Ministry of Earth Sciences' weather forecasting and ocean observation missions, and various state governments' infrastructure development monitoring, all benefiting from the rapid revisit times and specialized sensor capabilities that small satellite constellations provide compared to traditional large satellite architectures.

Regional Insights:

- North India

- South India

- East India

- West India

South India exhibits a clear dominance with a 31.5% share of the total India nanosatellite and microsatellite market in 2025.

South India's market leadership stems from the region's concentration of aerospace infrastructure, technology talent, and research institutions centered in Bengaluru, which hosts over sixty percent of India's space technology startups. The city's ecosystem includes satellite design firms, component manufacturers, software development companies, and service providers that form integrated value chains supporting satellite development from concept through operations. Proximity to the Satish Dhawan Space Centre in Sriharikota provides logistical advantages for payload integration, pre-launch testing, and mission operations, while reducing transportation costs and timeline risks associated with moving sensitive equipment across long distances.

Karnataka state's proactive space technology policy reinforces South India's advantages through targeted incentives for manufacturing investments, research and development funding, and workforce training programs that produce engineers and scientists with specialized space systems expertise. The policy's ambition to capture fifty percent of India's national space market by 2029 includes establishing dedicated manufacturing zones with appropriate infrastructure for clean rooms, vibration testing, thermal vacuum chambers, and other specialized facilities required for satellite production. The region benefits from established aerospace supply chains originally developed for aircraft manufacturing, which provide precision machining, composite materials fabrication, and electronic assembly capabilities that readily transfer to satellite applications. Academic institutions including the Indian Institute of Science and Indian Institute of Space Science and Technology contribute fundamental research, graduate education, and collaborative projects with industry partners that advance technical capabilities while creating talent pipelines that sustain ecosystem growth.

Market Dynamics:

Growth Drivers:

Why is the India Nanosatellite And Microsatellite Market Growing?

Expanding Earth Observation Requirements Across Multiple Sectors

The proliferation of Earth observation applications across agriculture, disaster management, urban planning, and environmental monitoring creates sustained demand for satellite imagery and geospatial analytics that small satellite constellations uniquely deliver through frequent revisit times and specialized sensor capabilities. Agriculture alone presents substantial opportunities, with India's farming sector employing approximately 45% of the workforce and government programs promoting precision agriculture techniques that require regular satellite monitoring of crop health, soil moisture, and irrigation efficiency. The Ministry of Agriculture's crop insurance schemes increasingly incorporate satellite data for yield estimation and loss assessment, while commercial agribusiness firms subscribe to Earth observation services for supply chain planning and commodity trading decisions.

Cost Advantages and Rapid Deployment Timelines for Small Satellites

Small satellites offer compelling economic advantages compared to traditional large satellite systems, with development costs typically representing ten to twenty percent of conventional platforms while achieving comparable mission objectives through constellation architectures that distribute functionality across multiple units. Manufacturing timelines compress from five to seven years for traditional satellites to twelve to eighteen months for small satellites, enabling faster response to emerging requirements and technology insertion of latest components that would be obsolete by the time traditional programs reach launch. The modular design approaches employed in small satellite platforms allow configuration customization without extensive redesign, reducing non-recurring engineering expenses while supporting volume production that brings economies of scale.

Defense Modernization and Strategic Satellite Capability Development

India's defense sector is pursuing comprehensive satellite capability expansion to address strategic requirements for communications, surveillance, and navigation that cannot depend on foreign systems potentially subject to access restrictions during conflicts or geopolitical tensions. The gap between India's current inventory of military satellites and major powers operating hundreds of such assets motivates modernization programs emphasizing indigenous development and rapid deployment capabilities that small satellite approaches inherently provide. Rs 1.80 lakh crore set aside in the Armed Forces' Capital Budget; Modernization is a primary emphasis; Rs 1.12 lakh crore designated for purchases from local industries. The Chief of Defence Staff's articulation of requirements for intelligence, surveillance, and reconnaissance satellite constellations equipped with optical and hyperspectral sensors reflects institutional recognition that space-based assets are essential for modern military operations.

Market Restraints:

What Challenges the India Nanosatellite And Microsatellite Market is Facing?

Limited Payload Capacity Constraining Mission Complexity

The fundamental size and mass constraints of nanosatellites and microsatellites impose significant trade-offs in payload accommodation, power generation, and operational capabilities that limit their suitability for certain demanding applications. These platforms cannot support the large aperture optical telescopes required for highest-resolution imaging, high-power radar systems for all-weather surveillance, or extensive communication transponders needed for broadcasting applications. The restricted volume available for payload integration forces mission designers to prioritize specific capabilities while sacrificing others, potentially necessitating constellation approaches that employ multiple specialized satellites rather than single multifunctional platforms, thereby increasing overall mission costs and operational complexity despite individual satellite economies.

Technology Transfer Dependencies And Component Import Requirements

Despite growing indigenous manufacturing capabilities, India's small satellite sector retains dependencies on imported components for critical subsystems including star trackers for attitude determination, reaction wheels for satellite orientation control, high-efficiency solar cells, and specialized radiation-hardened processors designed for space environments. These technology areas represent highly specialized markets dominated by established international suppliers with significant intellectual property protections and export control restrictions that limit technology transfer even when components are commercially available. The reliance on foreign sources creates supply chain vulnerabilities including delivery delays, price escalations, and potential access restrictions during geopolitical tensions.

Ground Infrastructure And Operational Support System Gaps

The proliferation of small satellite constellations requiring frequent communications for data downlink, command upload, and health monitoring creates demands for ground station networks that exceed current infrastructure availability. While government facilities operated by the Indian Space Research Organisation provide capabilities for major missions, commercial operators and private satellite owners face limitations in accessing these resources or find capacity constraints during peak demand periods. Establishing private ground station networks requires significant capital investments in antenna systems, tracking mechanisms, radio frequency equipment, and site infrastructure including power supply and environmental controls.

Competitive Landscape:

The India nanosatellite and microsatellite market exhibits a dynamic competitive environment characterized by collaboration between established international aerospace corporations and emerging domestic space technology startups, with government agencies playing dual roles as customers and capability enablers through technology transfer, infrastructure access, and procurement policies. International players bring decades of satellite heritage, established supply chains, and proven platform designs that serve large-scale government programs and commercial operators requiring high reliability and performance guarantees. These companies increasingly establish partnerships with Indian firms to access the domestic market while complying with indigenous content requirements and technology localization mandates.

India Nanosatellite And Microsatellite Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Satellite Masses Covered |

Nanosatellite (1kg to 10kg), Microsatellite (10kg to 100kg) |

|

Components Covered |

Hardware, Software and Data Processing, Space Services, Launch Services |

|

Applications Covered |

Communication, Earth Observation and Remote Sensing, Scientific Research, Biological Experiments, Technology Demonstration and Verification, Academic Training, Mapping and Navigation, Reconnaissance, Others |

|

End-Use Sectors Covered |

Government, Civil, Commercial, Defense, Energy and Infrastructure, Others |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Nanosatellite And Microsatellite Market Research Report and Industry Forecast Report

The India nanosatellite and microsatellite market size was valued at USD 232.8 Million in 2025.

The India nanosatellite and microsatellite market is expected to grow at a compound annual growth rate of 26.79% from 2026-2034 to reach USD 2,177.7 Million by 2034.

Microsatellite (10kg to 100kg) dominated the market with 52.4% share, driven by its optimal balance between payload capacity and cost efficiency. These platforms accommodate multiple sensors, advanced communication systems, and extended operational lifetimes essential for defense surveillance, telecommunications, and complex Earth observation missions requiring high-resolution optical and radar imaging capabilities.

Key factors driving the India nanosatellite and microsatellite market include expanding Earth observation requirements across agriculture, disaster management, and urban planning sectors; cost advantages and rapid deployment timelines compared to traditional satellites; and defense modernization programs requiring indigenous satellite capabilities for communications, surveillance, and navigation applications with strategic importance for national security.

Major challenges include limited payload capacity constraining mission complexity and sensor capabilities; technology transfer dependencies requiring imported components for critical subsystems like star trackers and radiation-hardened processors; and ground infrastructure gaps in station networks and data processing facilities needed to support growing constellation operations and deliver competitive analytics services.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)