India Natural Gas Market Size, Share, Trends and Forecast by Type and Region, 2026-2034

India Natural Gas Market Size, Share, Trends & Forecast (2026-2034)

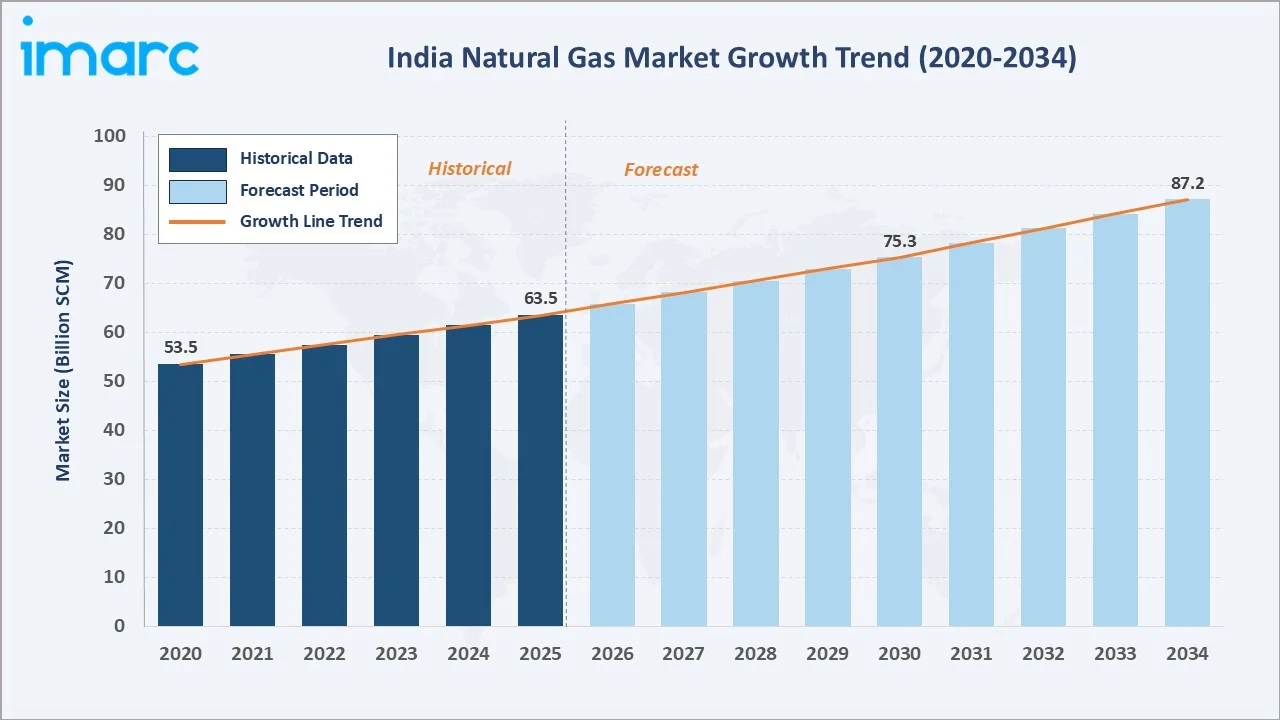

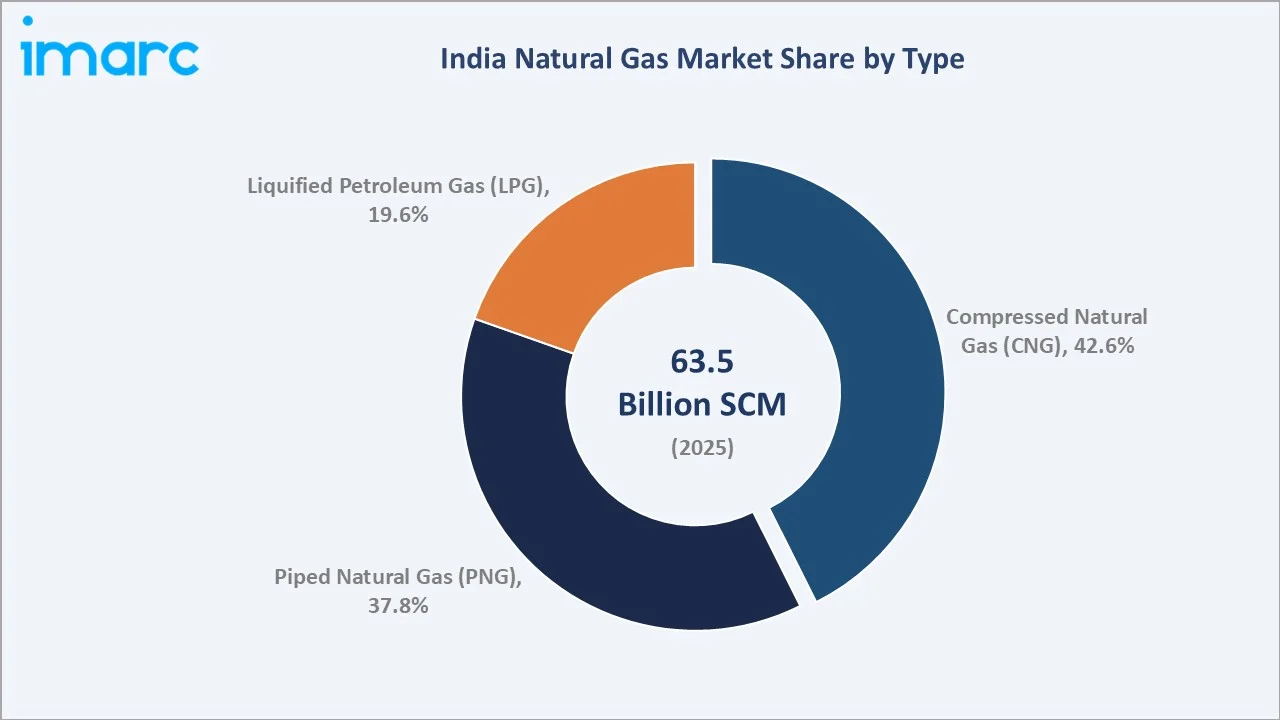

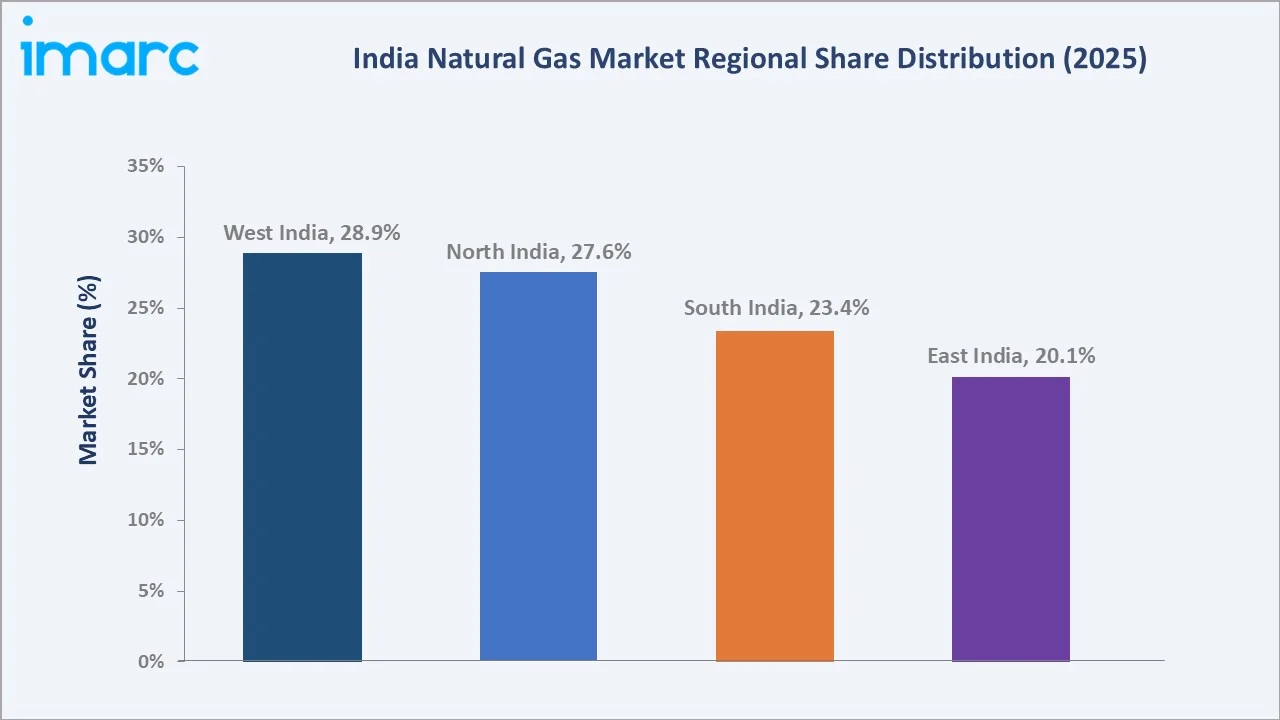

The India natural gas market reached 63.50 Billion Standard Cubic Meters (BSCM) in 2025 and is projected to reach 87.17 Billion Standard Cubic Meters by 2034, growing at a CAGR of 3.48% during 2026-2034. The market is driven by expanding city gas distribution networks, pipeline infrastructure growth, and rising integration in hydrogen production. Compressed Natural Gas (CNG) dominates at 42.6%. West India leads regional share at 28.9%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

63.50 Billion Standard Cubic Meters |

|

Forecast Market Size (2034) |

87.17 Billion Standard Cubic Meters |

|

CAGR (2026-2034) |

3.48% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Compressed Natural Gas – CNG (42.6%, 2025) |

|

Leading Region |

West India (28.9%, 2025) |

The India natural gas market expanded from 53.53 BSCM in 2020 to 63.50 BSCM in 2025, anchored at 75.33 BSCM in 2030, and forecast to reach 87.17 BSCM by 2034. Sustained government investment in city gas distribution and pipeline connectivity, alongside rising urban energy demand, has driven consistent above-baseline growth across the historical period.

To get more information on this market, Request Sample

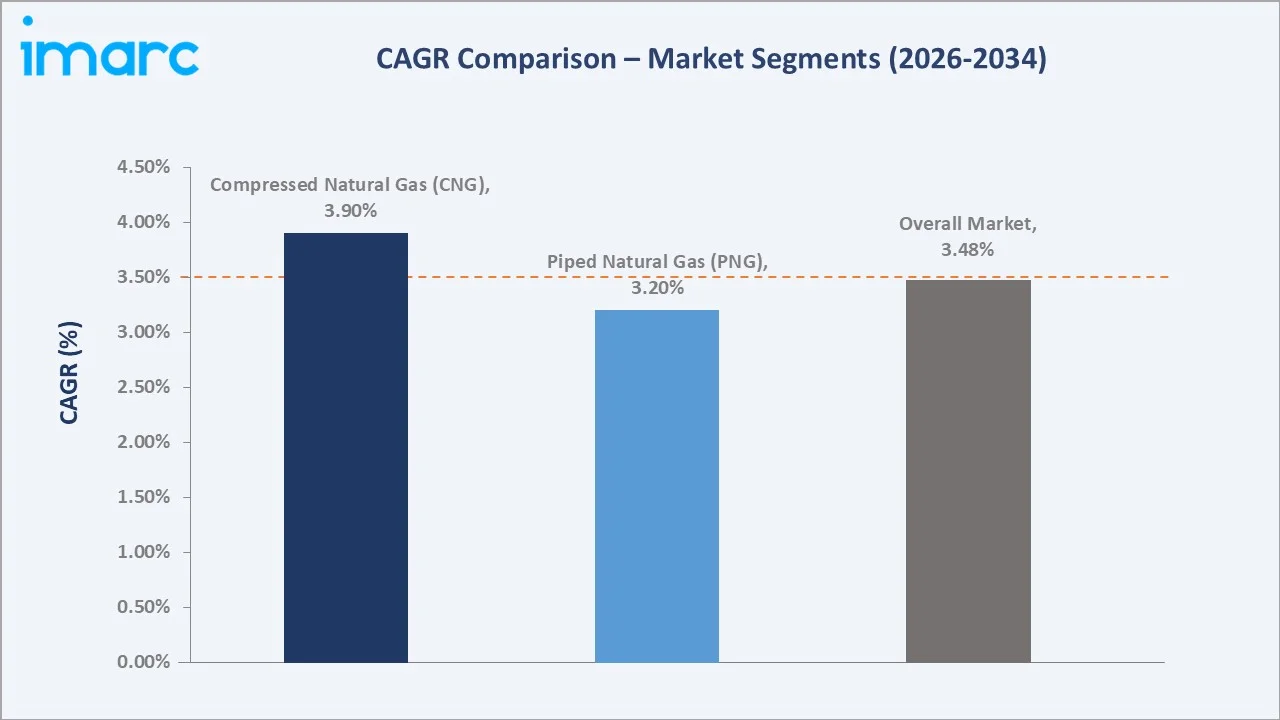

CNG segment grows fastest driven by urban fleet conversion programs and expanding dispensing station networks. PNG segment grows steadily through progressive city gas distribution rollout and new residential connections. The overall market CAGR of 3.48% reflects a stable and policy-supported demand growth trajectory through 2034.

Executive Summary

The India natural gas market reached 63.50 Billion Standard Cubic Meters (BSCM) in 2025, representing one of Asia's most strategically significant energy transitions. The market encompasses domestic production, LNG import, pipeline transmission, city gas distribution, and end-user applications across residential, commercial, industrial, and transportation sectors.

Compressed Natural Gas (CNG) at 42.6% dominates through rapid urban vehicle adoption and government-mandated fleet conversion programs. West India at 28.9% leads through Gujarat's established pipeline infrastructure and Maharashtra's large industrial and residential gas demand base.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Compressed Natural Gas (CNG) – 42.6% share (2025) |

|

Second Segment |

Piped Natural Gas (PNG) – 37.8% market share (2025) |

|

Leading Region |

West India – 28.9% market share (2025) |

|

Market Opportunity |

CGD greenfield expansion; LNG for heavy transport; blue hydrogen; industrial gas substitution; smart metering infrastructure |

Key Analytical Observations Supporting The Above Data:

- Compressed Natural Gas (CNG) at 42.6%: CNG dominates India's natural gas consumption through rapid urban transportation adoption, government-mandated bus and auto-rickshaw fleet conversions, and expanding CNG station networks in PNGRB-licensed geographies across Indian cities.

- Piped Natural Gas (PNG) at 37.8%: PNG leads residential and industrial penetration through city gas distribution network expansion, driven by PNGRB's mandatory minimum connection targets and favorable economics versus LPG cylinders for household cooking applications.

- West India at 28.9%: West India leads through Gujarat's decades-long gas infrastructure advantage, Dahej LNG terminal proximity, and Maharashtra's large industrial and residential consumer base in the country's most gas-mature region.

India Natural Gas Market Overview

The India natural gas market encompasses exploration and production, LNG import and regasification, pipeline transmission, and city gas distribution serving residential, commercial, industrial, and transportation end-uses. Regulatory bodies PNGRB and MoPNG govern market structure, licensing, and pricing across the full value chain.

Macroeconomic factors include rapid urbanization, industrial growth, and national energy security imperatives. The government's ambition of a gas-based economy targeting 15% natural gas share in the primary energy mix by 2030 underpins long-term demand growth and infrastructure investment across the country.

Market Dynamics

To evaluate market opportunities, Request Sample

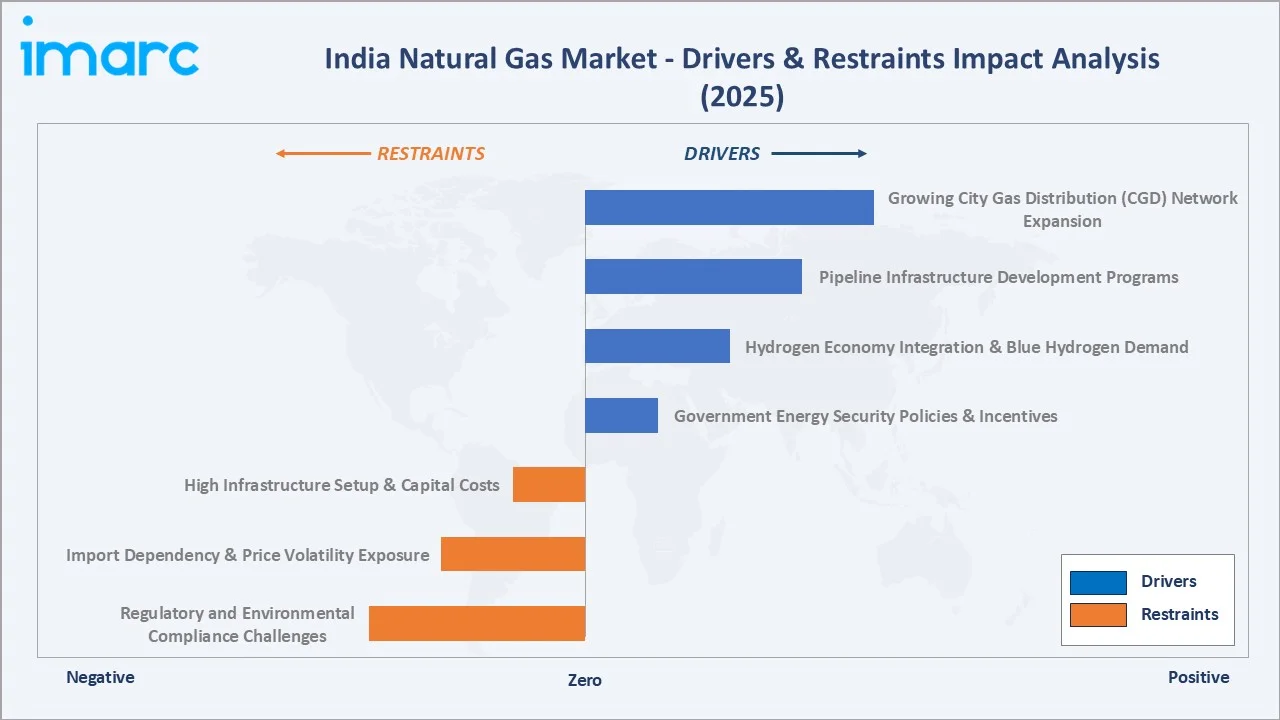

Market Drivers

- Growing City Gas Distribution (CGD) Network Expansion: Increasing government support for expanding piped natural gas access to households and compressed natural gas for transportation is accelerating infrastructure buildout. Rising consumer awareness and favorable fuel economics are supporting rapid uptake across urban and semi-urban areas nationwide.

- Pipeline Infrastructure Development Programs: The rapid expansion of the national gas pipeline network is improving supply reliability and regional connectivity. Investment in new interstate pipelines and compressor stations is enabling gas access in previously underserved areas, supporting both residential and industrial demand growth.

- Hydrogen Economy Integration and Blue Hydrogen Demand: Rising emphasis on hydrogen as a future energy carrier is creating new demand for natural gas through blue hydrogen production via steam methane reforming. Growing policy support and strategic partnerships are accelerating investments in gas-derived hydrogen technologies across industrial sectors.

- Government Energy Security Policies and Incentives: National policies targeting a gas-based economy, combined with PNGRB licensing reforms and supportive pricing mechanisms, are creating a favorable regulatory environment for sustained investment and consumption growth across all natural gas market segments.

Market Restraints

- High Infrastructure Setup and Capital Costs: Establishing city gas distribution networks, transmission pipelines, and LNG regasification facilities requires substantial upfront capital. Long payback periods and financing constraints restrict expansion into price-sensitive markets and limit the pace of infrastructure rollout in smaller cities.

- Import Dependency and Price Volatility Exposure: Growing reliance on LNG imports exposes the market to international pricing fluctuations and supply disruptions. Volatility in global gas markets can significantly impact domestic affordability and the competitive position of natural gas versus alternative fuels for end consumers.

- Regulatory and Environmental Compliance Challenges: Complex multi-jurisdictional regulatory requirements, land acquisition issues for pipelines, and evolving environmental compliance standards create project delays and increase development costs, slowing the overall pace of natural gas infrastructure expansion across regions.

Market Opportunities

- City Gas Distribution Greenfield Expansion: A large number of geographic areas licensed under successive PNGRB bidding rounds represent significant greenfield investment opportunities. Rising urban populations and government targets for increasing natural gas's share in the energy mix present substantial long-term demand potential for CGD operators.

- Industrial Gas Substitution from Coal and Oil: Growing environmental awareness and corporate emission reduction commitments are driving fuel switching from coal and oil to natural gas in manufacturing sectors. This structural transition in industrial energy demand creates sustained volume growth opportunities for natural gas suppliers and distributors.

Market Challenges

- Last-Mile Connectivity in Smaller Cities: Extending city gas distribution networks profitably to Tier 2 and Tier 3 cities with lower population density and purchasing power remains operationally and economically challenging. High per-connection costs and limited industrial anchor demand complicate network economics in these developing markets.

- Natural Gas Pricing Competitiveness Against Renewables: The rapid decline in solar and wind power costs is increasing competition for natural gas in power generation applications. Maintaining the economic competitiveness of gas in this segment requires efficient pricing mechanisms and supportive energy policies from regulatory authorities.

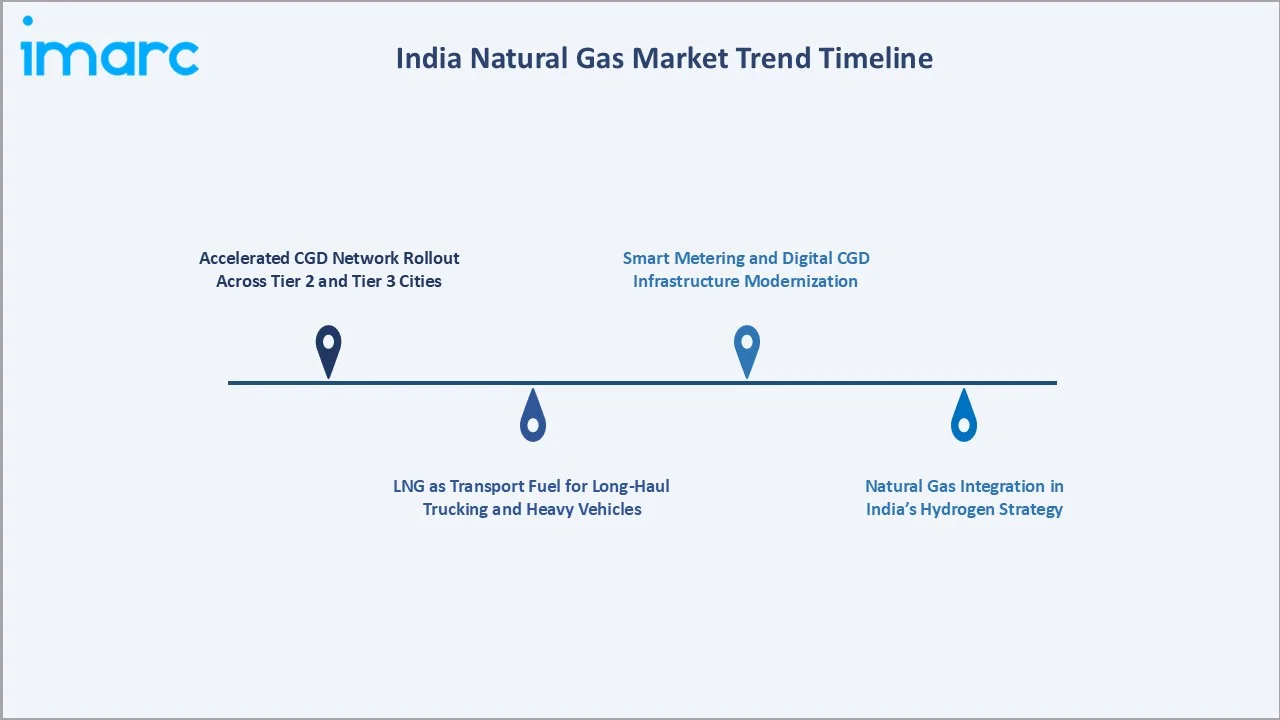

Emerging Market Trends

1. Accelerated CGD Network Rollout Across Tier 2 and Tier 3 Cities

PNGRB-licensed operators are aggressively expanding piped natural gas and CNG infrastructure beyond major metropolitan areas into smaller cities and semi-urban regions. Regulatory support and mandatory work program commitments ensure sustained capital expenditure deployment, while growing consumer awareness of PNG economics versus LPG is accelerating residential connection growth.

2. LNG as Transport Fuel for Long-Haul Trucking and Heavy Vehicles

Liquefied natural gas is emerging as a viable clean fuel for long-haul road freight given economic advantages over diesel. LNG truck adoption, supported by the development of highway corridor LNG dispensing infrastructure, is creating a new consumption segment that complements existing CNG-dominated urban transport applications and expands overall gas demand.

3. Natural Gas Integration in India's Hydrogen Strategy

India's National Hydrogen Mission positions blue hydrogen produced from natural gas with carbon capture as a transitional energy pathway. Ongoing investments in steam methane reforming capacity, supported by government incentives and strategic partnerships, are creating incremental natural gas demand from the emerging hydrogen economy alongside traditional consumption sectors.

4. Smart Metering and Digital CGD Infrastructure Modernization

City gas distribution operators are deploying smart metering, IoT-enabled monitoring, and automated billing platforms to improve operational efficiency and reduce commercial losses. These digital infrastructure investments are improving network reliability and enabling data-driven demand forecasting, benefiting both operators and end consumers across distribution networks.

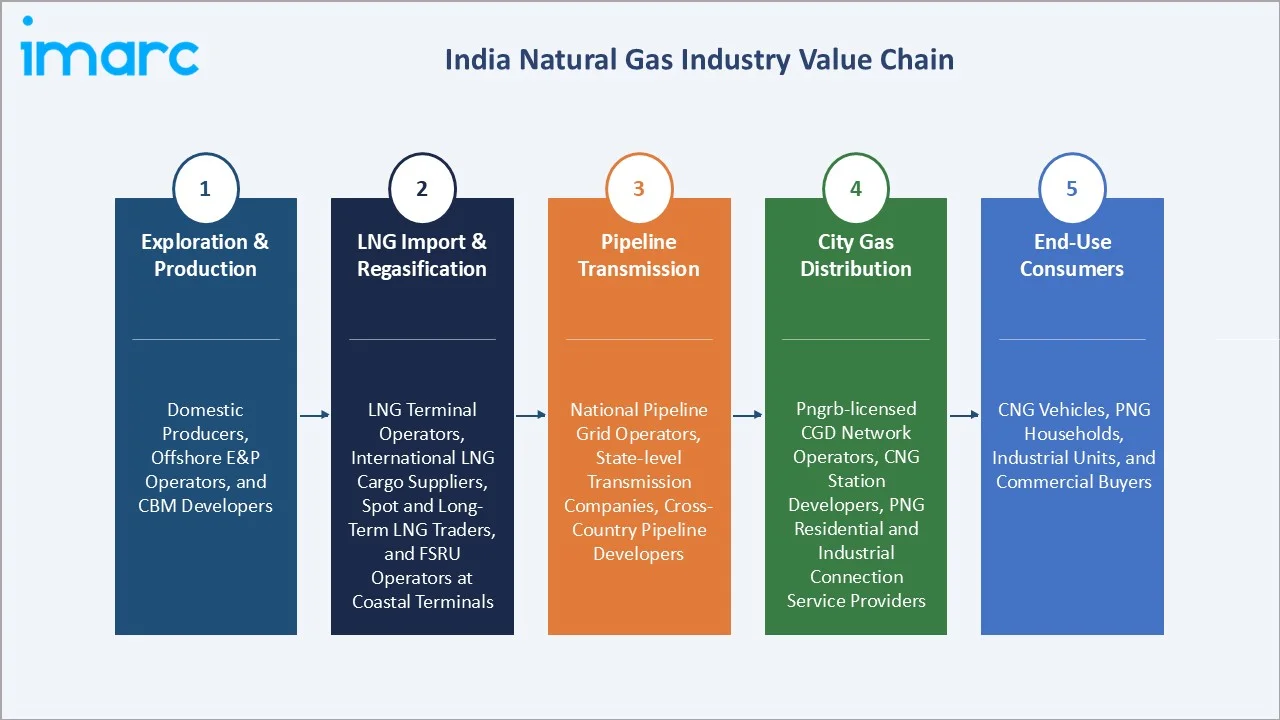

Industry Value Chain Analysis

The India natural gas value chain integrates upstream exploration and production, LNG import and regasification, national pipeline transmission, city gas distribution, and end-user applications across residential, commercial, industrial, and transportation segments.

|

Stage |

Key Participants |

|

Exploration & Production |

Domestic upstream producers, offshore and onshore E&P operators, coalbed methane developers, and independent gas field companies supplying indigenous gas to the national grid |

|

LNG Import & Regasification |

LNG terminal infrastructure operators, international LNG cargo suppliers, spot and long-term LNG traders, FSRU operators, and regasification service providers at coastal terminals |

|

Pipeline Transmission |

National pipeline grid operators, state-level gas transmission companies, cross-country pipeline developers, and compressor station infrastructure management and operations teams |

|

City Gas Distribution |

PNGRB-licensed CGD network operators, CNG station developers and operators, PNG residential and industrial connection service providers, and last-mile distribution infrastructure companies |

|

End-Use Consumers |

CNG vehicle operators, residential PNG households, industrial manufacturing units, commercial establishments, fertilizer plants, and gas-based power generation facility procurement teams |

The pipeline transmission stage is the most strategically critical segment of the value chain, with the national gas grid forming the supply backbone for downstream distribution. The CGD layer creates the direct consumer interface, with licensed operators delivering final customer value through PNG connections and CNG dispensing infrastructure.

Technology Landscape in the India Natural Gas Industry

City Gas Distribution (CGD) Technology

Advanced SCADA systems, smart pressure regulators, and advanced metering infrastructure are transforming CGD network management. Real-time leak detection, predictive maintenance, and automated pressure control systems are reducing operational losses and improving safety compliance across city gas distribution networks in India.

LNG Regasification and Storage Technology

Floating storage and regasification units are enabling faster LNG import capacity additions at lower capital cost compared to conventional land-based terminal construction. Advanced cryogenic storage systems, boil-off gas recovery, and improved send-out efficiency are enhancing terminal economics and supply reliability for Indian LNG importers.

CNG Compression and Dispensing Technology

Next-generation cascade compression systems and fast-fill dispensing stations are improving CNG station throughput and reducing vehicle refueling times. Mobile CNG and virtual pipeline technologies are enabling gas supply to areas without direct pipeline connectivity, extending the market reach of city gas distribution operators.

Market Segmentation Analysis

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Compressed Natural Gas (CNG) |

42.6% |

2025 |

|

Region |

West India |

28.9% |

2025 |

By Type

Compressed Natural Gas (CNG) leads at 42.6% (2025). The CNG segment encompasses urban vehicle fleets, public transport buses, auto-rickshaws, and private automobiles across PNGRB-licensed geographic areas. CNG dominates through government-mandated vehicle fleet conversions, competitive fuel economics, and the expanding dispensing station network across Indian cities.

Piped Natural Gas (PNG) at 37.8% encompasses residential household connections and industrial consumers within city gas distribution network coverage areas. PNG growth is driven by mandatory minimum connection targets and favorable economics versus bottled LPG for household cooking. Liquified Petroleum Gas (LPG) at 19.6% serves areas outside PNG coverage and is expected to decline as CGD networks expand.

Regional Market Insights

|

Region |

Share (2025) |

Key India Natural Gas Market Drivers & Characteristics |

|

West India |

28.9% |

Driven by Gujarat's established gas infrastructure, proximity to the largest LNG import terminal, and Maharashtra's large industrial and residential gas demand representing the country's most mature natural gas market. |

|

North India |

27.6% |

Driven by the dominant city gas distribution network in the National Capital Region, Rajasthan's expanding gas network, and Uttar Pradesh's large industrial and residential consumer base supported by growing pipeline connectivity. |

|

South India |

23.4% |

Driven by expanding city gas distribution networks in major cities, national pipeline grid connectivity, and growing industrial demand from petrochemicals, pharmaceuticals, and manufacturing sectors across the southern states. |

|

East India |

20.1% |

Driven by domestic gas production assets in the region, ongoing pipeline expansion programs, and increasing CGD rollout in Odisha, West Bengal, and northeastern states with growing urban natural gas demand. |

West India's 28.9% market leadership is anchored by decades of gas infrastructure development in Gujarat and proximity to the country's largest LNG regasification terminal. North India's 27.6% reflects strong CGD network penetration in the National Capital Region and expanding pipeline-based coverage in adjacent states.

South India's 23.4% encompasses rapidly growing city gas distribution networks in major southern cities, supported by national pipeline connectivity and rising industrial gas adoption. East India at 20.1% represents the highest growth potential region through ongoing pipeline expansion programs and new CGD licensing across underserved geographies.

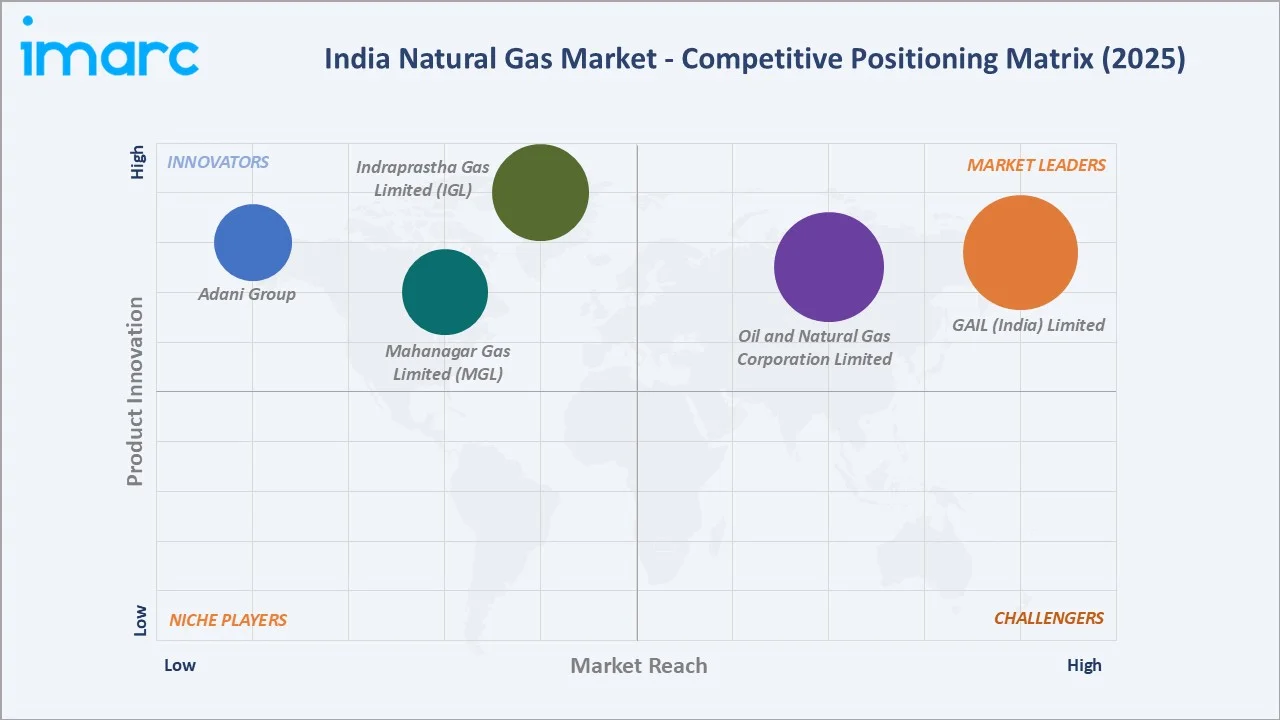

Competitive Landscape

The India natural gas market competitive landscape encompasses upstream exploration and production companies, LNG import and regasification infrastructure operators, national pipeline transmission operators, and city gas distribution companies serving different segments of the gas value chain.

|

Company Name |

Key Products/Services |

Market Position |

Core Strength |

|

GAIL (India) Limited |

Gas transmission, CGD, LNG marketing, petrochemicals |

Market Leader |

Operates India's most extensive natural gas pipeline network; dominant role across transmission, marketing, and distribution spanning all major consuming regions |

|

Oil and Natural Gas Corporation Limited |

Domestic E&P, offshore and onshore gas production |

Market Leader |

India's largest domestic natural gas producer with significant offshore and onshore field operation capabilities and extensive proven hydrocarbon reserves |

|

Indraprastha Gas Limited (IGL) |

CNG dispensing, PNG household and commercial supply |

Established Player |

Dominant city gas distribution operator in India's largest urban market with an extensive CNG station network and large residential and commercial PNG customer base |

|

Mahanagar Gas Limited (MGL) |

CNG, PNG distribution in Mumbai Metro Region |

Established Player |

Key CGD operator in the Mumbai Metropolitan Region with an extensive CNG and PNG distribution network serving residential, commercial, and industrial consumers |

|

Adani Group |

City gas distribution, CNG, PNG across licensed GAs |

Established Player |

Expanding multi-geography CGD operations across numerous PNGRB-licensed geographic areas with strong infrastructure development and execution capabilities |

Market concentration is increasing at the CGD segment through consolidation, as established operators acquire additional PNGRB-licensed geographic areas. The transmission segment maintains high concentration through the dominant national pipeline network position, which remains strategically central for all downstream market participants.

Key Company Profiles

GAIL (India) Limited

GAIL (India) Limited is India's flagship natural gas processing and distribution company, operating the country's most extensive pipeline transmission network and participating across the entire natural gas value chain from production to retail city gas distribution across India.

- Key Products: Natural gas transmission services, city gas distribution through GAIL Gas, LNG marketing, petrochemicals, and liquid hydrocarbons across India.

- Recent Developments: In 2025, Cummins Accelera and GAIL (India) Limited announced a strategic partnership to collaborate on green hydrogen and zero-emission technologies, focusing on hydrogen production, blending, transportation, and storage across transportation, energy, and steel manufacturing sectors.

- Strategic Focus: Expanding pipeline transmission capacity, growing the CGD subsidiary network, developing hydrogen infrastructure, and diversifying into renewable energy alongside core natural gas operations.

Indraprastha Gas Limited (IGL)

Indraprastha Gas Limited (IGL) is the dominant city gas distribution operator in India's largest urban market, established as a joint venture serving the National Capital Region through an extensive network of CNG stations and piped natural gas connections.

- Key Products: Compressed Natural Gas (CNG) for vehicles, Piped Natural Gas (PNG) for residential and commercial consumers, and industrial natural gas supply across Delhi-NCR and adjacent cities.

- Recent Developments: In November 2025, Indraprastha Gas Limited (IGL) signed a strategic alliance with Saudi Arabia-based MASAH Construction Company to jointly develop and operate natural gas distribution networks in industrial cities across the Kingdom of Saudi Arabia. The partnership focuses on leveraging IGL's expertise in planning, designing, and operating city gas networks, while MASAH contributes regulatory, engineering, procurement, construction, and local stakeholder capabilities. The collaboration marks IGL's first international expansion and aims to promote cleaner energy solutions and cross-border knowledge sharing.

- Strategic Focus: Geographic expansion into new licensed cities, CNG station network densification, smart metering deployment, and capitalizing on government mandates for fleet conversion to grow distribution volumes.

Market Concentration Analysis

The India natural gas market exhibits moderate to high concentration at the transmission tier, where the dominant national pipeline operator holds a commanding share of total gas transmission volumes. The city gas distribution sector shows increasing concentration as established operators acquire additional PNGRB-licensed geographic areas through M&A activity.

Upstream production remains concentrated among a small number of state-owned producers accounting for the majority of domestic gas supply. LNG import infrastructure concentration is gradually decreasing through new terminal projects and floating regasification unit deployments that are expanding India's overall regasification capacity.

Investment & Growth Opportunities

Highest Growth Segments

CGD network expansion in Tier 2 and Tier 3 cities, LNG for long-haul road transport, industrial gas substitution from coal, blue hydrogen production from natural gas, smart metering and digital CGD infrastructure, and pipeline capacity additions in underserved eastern and northeastern regions represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

India's government-mandated CGD expansion across a large number of licensed geographic areas represents the largest near-term structured investment opportunity. Operators establishing preferred positions in high-potential licensed areas before competitive market entry are positioned for above-market volume growth as network density increases.

Investment Themes

- CGD Network Infrastructure Investment: Investors establishing city gas distribution infrastructure in high-growth licensed areas can capture first-mover advantages through pipeline asset ownership, creating long-duration regulated returns from India's structural energy transition away from coal and bottled LPG.

- LNG Heavy Transport Infrastructure: LNG adoption in long-haul road freight creates structured demand for highway corridor dispensing infrastructure. Companies investing in LNG dispensing networks along major national freight corridors are positioned to benefit from the decarbonization transition in India's road transport sector.

Future Market Outlook (2026-2034)

The India natural gas market is projected to grow from 63.50 BSCM in 2025 to 87.17 BSCM by 2034, delivering a 3.48% CAGR over the forecast period. The anchor value of 75.33 BSCM in 2030 reflects expected milestones in PNGRB CGD network targets, national pipeline expansion programs, and LNG import capacity additions reaching full operational scale.

Three structural forces define India natural gas market growth through 2034 with high confidence. Government policy targeting a gas-based economy creates mandated regulatory demand for infrastructure investment. India's ongoing urbanization trajectory creates structural residential demand growth for PNG. Corporate emission reduction commitments across major Indian industries are driving coal-to-gas fuel switching in manufacturing sectors, creating sustained volume growth independent of residential and transportation demand.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 50 industry stakeholders in 2025, including regulatory officials, city gas distribution company executives, pipeline operators, LNG terminal management, and market specialists across India's major natural gas consuming regions and growth corridors.

Secondary Research

Secondary research encompassed government ministry publications, regulatory body annual reports, company annual reports and investor presentations, international energy agency data, and industry association reports. Over 60 secondary sources were reviewed, validated, and incorporated into the analysis.

Forecasting Models

Market volume forecasts were developed using a segment bottom-up model combining CGD network rollout projection, industrial demand substitution modeling, LNG import terminal capacity scheduling, domestic production decline assessment, and macroeconomic demand factor integration across all regional and segment dimensions.

India Natural Gas Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion Standard Cubic Meters |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Compressed Natural Gas, Piped Natural Gas, Liquified Petroleum Gas |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | GAIL (India) Limited, Oil and Natural Gas Corporation Limited, Indraprastha Gas Limited (IGL), Mahanagar Gas Limited (MGL), Adani Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India natural gas market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India natural gas market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India natural gas industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Natural Gas Market Report

The India natural gas market reached 63.50 Billion Standard Cubic Meters (BSCM) in 2025, driven by rapid city gas distribution network expansion, government energy transition policies, and growing adoption of compressed natural gas in vehicle transportation across urban centers in India.

The market grows at a CAGR of 3.48% during 2026-2034, reaching 87.17 BSCM by 2034. The CNG segment drives above-average growth through urban transportation fleet conversion, while PNG growth follows city gas distribution network rollout velocity across newly licensed geographic areas.

Compressed Natural Gas (CNG) leads at 42.6% through urban transportation dominance, government mandates on fleet conversion, and extensive CNG station network development by PNGRB-licensed city gas distribution operators across Indian metropolitan and Tier 2 cities.

West India leads at 28.9% through established pipeline infrastructure, LNG terminal proximity, and large industrial and residential consumer bases. North India at 27.6% reflects strong CGD penetration in the National Capital Region and expanding pipeline coverage in adjacent states.

Leading companies include GAIL (India) Limited, Oil and Natural Gas Corporation Limited, Indraprastha Gas Limited (IGL), Mahanagar Gas Limited (MGL), and Adani Group, among others in the competitive landscape.

The market is projected to reach approximately 75.33 BSCM by 2030, with city gas distribution coverage achieving significant operational maturity, LNG terminal capacity expanding, and industrial gas adoption accelerating across manufacturing and fertilizer production sectors.

India's National Hydrogen Mission creates incremental natural gas demand through blue hydrogen production via steam methane reforming. Strategic partnerships and government incentives position natural gas as a critical transitional hydrogen feedstock, supporting demand through the forecast period.

Key challenges include last-mile connectivity economics in smaller cities, LNG import price volatility exposure, pipeline land acquisition complexity, and increasing competition from renewable energy in power generation applications across the natural gas demand base.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)