India Next Generation Sequencing Market Size, Share, Trends and Forecast by Sequencing Type, Product Type, Technology, Application, End User, and Region, 2026-2034

India Next Generation Sequencing Market Summary:

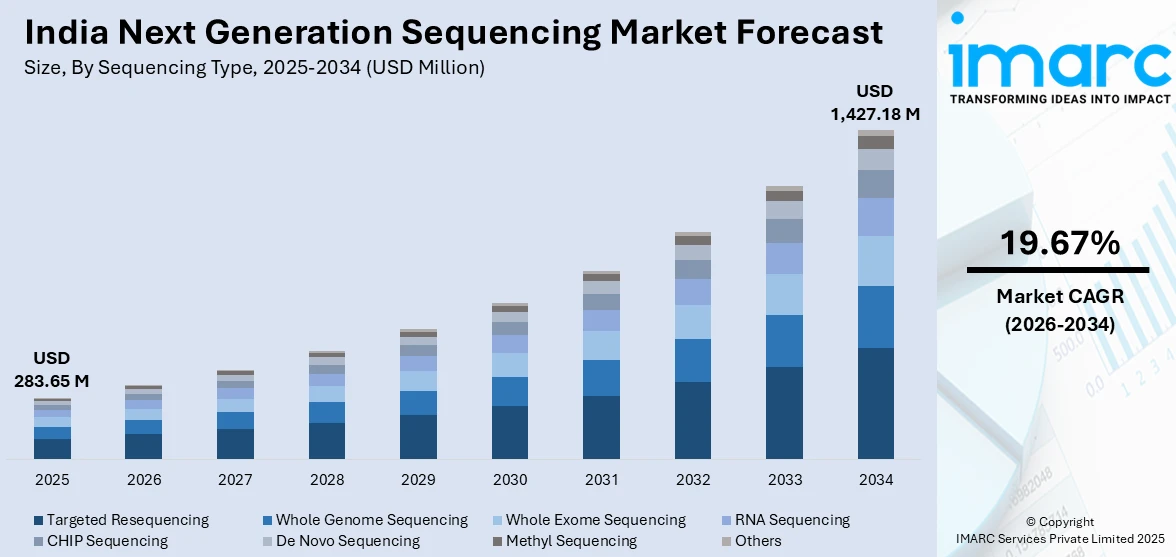

The India next generation sequencing market size was valued at USD 283.65 Million in 2025 and is projected to reach USD 1,427.18 Million by 2034, growing at a compound annual growth rate of 19.67% from 2026-2034.

The Indian market is experiencing transformative growth as national genomic initiatives gain momentum and precision medicine adoption accelerates across healthcare institutions. Government-supported initiatives in population genomics and biotechnology infrastructure development are strengthening the ecosystem for advanced sequencing technologies. Technological advancements in bioinformatics, increasing cancer diagnostics demand, and growing agricultural genomics applications are expanding the India next generation sequencing market share.

Key Takeaways and Insights:

- By Sequencing Type: Targeted resequencing leads the market with 36.8% share in 2025, driven by cost-effectiveness in clinical applications and widespread adoption in oncology diagnostics where focused gene panel sequencing provides actionable insights.

- By Product Type: Reagents and consumables dominate the market with 49.6% share in 2025, supported by high recurring demand from sequencing workflows and continuous consumption across research and diagnostic laboratories nationwide.

- By Technology: Sequencing by synthesis dominates with 63.4% share in 2025, benefiting from established platform ecosystems, superior accuracy in base calling, and extensive validation in clinical and research applications.

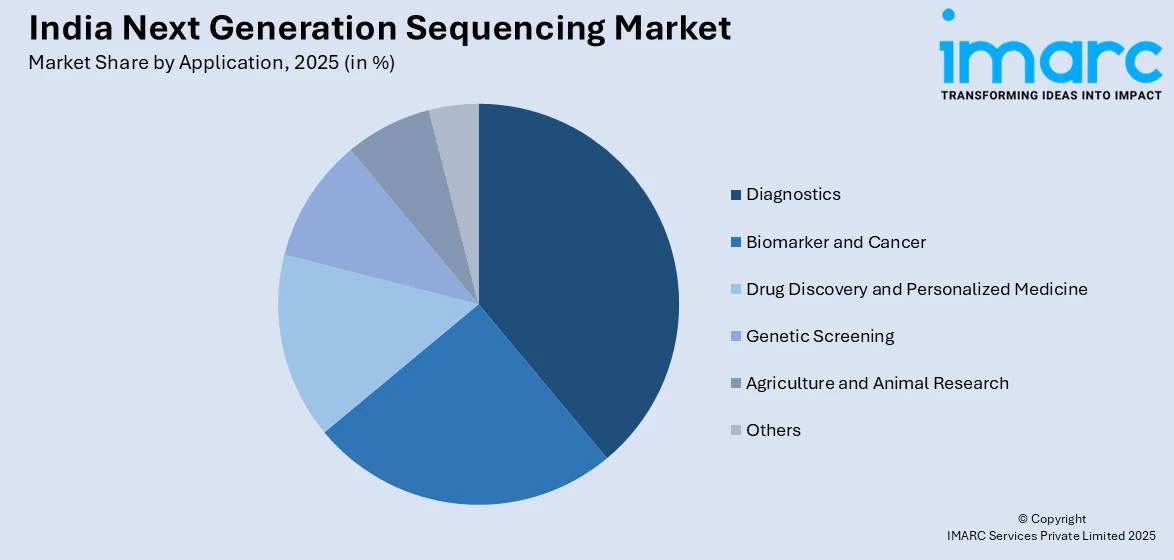

- By Application: Diagnostics leads with 38.9% share in 2025, fueled by expanding precision medicine adoption, cancer genomics applications, and increasing demand for genetic disease identification in clinical settings.

- By End User: Academic institutes & research centers account for 41.7% share in 2025, driven by government-funded genome projects, expanding research infrastructure, and collaborative initiatives advancing genomic science.

- By Region: West India dominates with 33.8% share in 2025, leveraging concentration of biotechnology hubs, research institutions, and healthcare infrastructure in metropolitan areas supporting advanced genomics adoption.

- Key Players: The India next generation sequencing market exhibits moderate competitive intensity, with international sequencing technology providers competing alongside emerging domestic genomics service companies across clinical and research segments.

To get more information on this market Request Sample

The market is propelled by government-led genomic initiatives creating robust data infrastructure for precision medicine development. Declining costs of whole-genome sequencing are democratizing access to advanced diagnostics across tertiary care hospitals and specialized research facilities. Rising cancer burden combined with growing awareness of genetic testing is accelerating clinical adoption of targeted sequencing panels. Technological advancements in bioinformatics platforms are enabling faster data interpretation and expanding clinical utility. Integration of artificial intelligence in genomic analysis is enhancing accuracy while reducing turnaround times for diagnostic applications. Agricultural genomics adoption is opening new application areas for crop improvement and breeding programs. Collaborative partnerships between international technology providers and domestic institutions are strengthening local capabilities and expanding service accessibility nationwide. In 2025, Gujarat has emerged as the first Indian State to introduce a genome sequencing program specifically aimed at tribal populations. During a significant consultation led by State Tribal Development Minister Kuber Dindor, the Tribal Genome Sequencing Project was unveiled to identify genetic health risks and promote precision healthcare for tribal communities. The project will analyze the genomes of 2,000 people from tribal groups in 17 districts within the State.

India Next Generation Sequencing Market Trends:

Expansion of Government-Led Genomic Infrastructure

Government-supported population genomics initiatives are establishing comprehensive genetic databases serving as foundational resources for precision medicine development. National programs focusing on ethnic diversity mapping are creating reference genomes specific to Indian populations, addressing underrepresentation in global databases. Collaborative frameworks involving academic institutions are accelerating data generation and standardization efforts across research networks. In 2024, the Department of Biotechnology announced completion of the Genome India Project, which sequenced whole genomes of 10,000 individuals from 99 diverse communities representing major linguistic and social groups. The project generated 8 petabytes of data stored at the Indian Biological Data Centre in Faridabad, India's first national repository for life science data. Translational research grants up to Rs 50 lakhs were announced for focused multi-institutional projects utilizing GenomeIndia data for developing cost-effective diagnostic tools and understanding population-specific genetic risk factors.

Integration of Artificial Intelligence (AI) in Data Analysis

Artificial intelligence and machine learning platforms are revolutionizing genomic data interpretation by enabling rapid variant annotation and clinical significance assessment. Automated bioinformatics workflows are reducing analysis complexity and accelerating time from sequencing to actionable insights for clinicians. Cloud-based computational infrastructure is expanding accessibility to advanced analytical capabilities across smaller laboratories previously limited by computing resources. MedGenome operates South Asia's largest CAP-accredited multiomics laboratory equipped with proprietary analytics platforms that have served over 1 million patients since 2013. The company's AI-driven clinical annotation platform translates NGS data from cancer testing gene panels into actionable insights for clinicians treating rare diseases, oncology, and reproductive healthcare conditions. Integration of deep learning algorithms is improving variant classification accuracy and enabling discovery of novel genomic associations relevant to Indian populations.

Rising Adoption in Agricultural Genomics

Agricultural research institutions are increasingly deploying next generation sequencing for crop improvement programs targeting drought resistance, pest tolerance, and yield optimization. Genome editing technologies combined with comprehensive sequencing are accelerating development of climate-resilient crop varieties addressing food security challenges. Government funding for agricultural biotechnology research is supporting infrastructure development and capacity building in agrigenomics. In May 2025, India became the world's first country to approve genome-edited rice for cultivation when Union Agriculture Minister Shivraj Singh Chouhan launched DRR Rice 100 (Kamala) and Pusa DST Rice 1, developed by the Indian Council of Agricultural Research. These varieties demonstrate enhanced drought, salinity, and climate stress tolerance, with DRR Rice 100 delivering 19% yield increase and 20% reduction in greenhouse gas emissions while saving 7,500 million cubic meters of irrigation water annually.

Market Outlook 2026-2034:

The India Next Generation Sequencing market is positioned for robust expansion throughout the forecast period, driven by converging technological, regulatory, and healthcare delivery advancements. Declining sequencing costs below USD 500 per whole genome are enabling population-scale screening programs previously economically unfeasible for public health systems. The market generated a revenue of USD 283.65 Million in 2025 and is projected to reach a revenue of USD 1,427.18 Million by 2034, growing at a compound annual growth rate of 19.67% from 2026-2034. Government initiatives targeting 10 million genome sequences will establish comprehensive genetic diversity databases supporting precision medicine development across oncology, rare diseases, and pharmacogenomics applications. Clinical integration of liquid biopsy panels for early cancer detection and treatment monitoring is expanding commercial diagnostic applications beyond research settings. Agricultural genomics adoption for crop improvement and livestock breeding programs is diversifying market applications beyond healthcare.

India Next Generation Sequencing Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Sequencing Type |

Targeted Resequencing |

36.8% |

|

Product Type |

Reagents and Consumables |

49.6% |

|

Technology |

Sequencing by Synthesis |

63.4% |

|

Application |

Diagnostics |

38.9% |

|

End User |

Academic Institutes & Research Centers |

41.7% |

|

Region |

West India |

33.8% |

Sequencing Type Insights:

- Whole Genome Sequencing

- Targeted Resequencing

- Whole Exome Sequencing

- RNA Sequencing

- CHIP Sequencing

- De Novo Sequencing

- Methyl Sequencing

- Others

Targeted resequencing dominates with a market share of 36.8% of the total India next generation sequencing market in 2025.

Targeted resequencing leads the market by offering cost-effective solutions for clinical diagnostics where focused analysis of specific genomic regions provides sufficient information for medical decision-making. This approach is particularly prevalent in oncology applications where gene panels covering actionable mutations guide targeted therapy selection, delivering clinical utility at substantially lower costs compared to whole genome approaches. The segment benefits from established validation protocols and regulatory acceptance in clinical settings, facilitating adoption across diagnostic laboratories. Cancer gene panels ranging from 50 to 500 genes are widely deployed across tertiary care hospitals for tumor profiling, enabling identification of therapeutic targets and resistance markers guiding treatment strategies. Hereditary disease testing panels focusing on known pathogenic variants represent another major application area, supporting carrier screening and prenatal diagnostics across reproductive healthcare settings.

Targeted resequencing workflows are optimized for high sample throughput and rapid turnaround times, meeting clinical diagnostic requirements better than comprehensive sequencing approaches. The technology's compatibility with formalin-fixed paraffin-embedded tissue samples expands applicability to archived clinical specimens commonly encountered in oncology diagnostics. Academic research institutions utilize targeted approaches for focused investigation of specific biological pathways or disease-associated gene families, maximizing cost efficiency in hypothesis-driven studies. Infectious disease applications including drug resistance profiling in tuberculosis and viral genotyping represent emerging use cases where targeted sequencing provides actionable information for public health interventions. The segment's cost structure aligns well with reimbursement frameworks and patient affordability considerations, supporting broader clinical adoption across India's diverse healthcare ecosystem.

Product Type Insights:

- Instruments

- Reagents and Consumables

- Software and Services

Reagents and consumables lead with a share of 49.6% of the total India next generation sequencing market in 2025.

Reagents and consumables generate the largest revenue share through recurring demand across all sequencing workflows, from sample preparation through library construction to sequencing reactions. The consumable-intensive nature of Next Generation Sequencing creates sustained demand across installed instrument base, with sequencing reagents representing the highest-value component consumed per sample processed. Library preparation kits encompassing DNA fragmentation, end-repair, adapter ligation, and amplification reagents constitute significant recurring expenditure for laboratories performing routine sequencing. Quality control reagents and standards used throughout workflow stages contribute to segment growth, ensuring data quality and regulatory compliance in clinical applications.

Sequencing flow cells and chemistry cartridges represent major consumable investments that scale directly with sample throughput, driving proportional revenue growth as sequencing volumes expand. Target enrichment reagents used in capture-based workflows for exome and targeted sequencing applications add specialized consumable requirements beyond basic sequencing chemistry. The segment benefits from platform lock-in dynamics where instruments require proprietary consumables from manufacturers, creating predictable recurring revenue streams. Growing adoption of sequencing in clinical diagnostics is expanding consumables demand beyond traditional research applications, with quality-controlled reagents meeting regulatory requirements commanding premium pricing. Domestic manufacturing initiatives are emerging to develop cost-competitive alternatives to imported consumables, potentially expanding market accessibility while maintaining revenue growth through volume expansion.

Technology Insights:

- Sequencing by Synthesis

- Ion Semiconductor Sequencing

- Single-Molecule Real-Time Sequencing

- Nanopore Sequencing

- Others

Sequencing by synthesis exhibits a clear dominance with a 63.4% share of the total India next generation sequencing market in 2025.

Sequencing by synthesis technology dominates through established accuracy benchmarks, comprehensive validation in clinical applications, and extensive infrastructure of supporting reagents, protocols, and analysis pipelines. The technology's base-calling precision exceeds 99.9% accuracy for individual reads, meeting stringent requirements for clinical diagnostics where false positives and negatives carry significant consequences. Scalable throughput ranging from benchtop systems processing dozens of samples to production instruments handling thousands enables technology deployment across diverse laboratory settings. Robust ecosystem of library preparation kits, quality control tools, and bioinformatics solutions reduces implementation barriers and operational complexity for new adopters.

Clinical validation data accumulated over two decades of technology deployment supports regulatory approvals and reimbursement coverage for diagnostic applications, accelerating clinical adoption. The technology's read length characteristics are well-matched to common applications including targeted sequencing, whole exome analysis, and transcriptome profiling in oncology and genetic disease diagnostics. Established operator training programs and technical support infrastructure facilitate technology transfer to laboratories expanding sequencing capabilities. Academic research institutions benefit from extensive literature and protocols optimized for sequencing by synthesis platforms, enabling rapid implementation of new applications. Compatibility with multiplexing approaches enables cost-effective processing of multiple samples per sequencing run, improving laboratory economics and supporting clinical diagnostics scalability.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Biomarker and Cancer

- Drug Discovery and Personalized Medicine

- Genetic Screening

- Diagnostics

- Agriculture and Animal Research

- Others

Diagnostics leads with a share of 38.9% of the total India next generation sequencing market in 2025.

Diagnostics applications lead market growth through expanding precision oncology adoption where tumor genomic profiling guides targeted therapy selection and treatment monitoring. Cancer diagnostics represent the largest clinical application segment, with comprehensive genomic profiling enabling identification of actionable mutations, pathway alterations, and resistance mechanisms across solid tumors and hematologic malignancies. Hereditary cancer risk assessment using multi-gene panels supports prevention strategies through early detection screening and prophylactic interventions in high-risk individuals. Rare disease diagnostics benefit from whole exome sequencing capabilities identifying causative variants in genetically heterogeneous conditions previously undiagnosable through traditional approaches.

Prenatal and neonatal screening applications are expanding beyond traditional single-gene disorders to comprehensive chromosomal microarray and exome analysis, improving diagnostic yields in suspected genetic conditions. Pharmacogenomic testing integrating germline variants affecting drug metabolism and response is emerging in clinical practice, supporting dose optimization and adverse event prevention. Infectious disease diagnostics including pathogen identification and antimicrobial resistance profiling are growing applications in public health surveillance and outbreak management. Liquid biopsy approaches detecting circulating tumor DNA enable non-invasive cancer screening, minimal residual disease monitoring, and treatment response assessment, expanding diagnostic utility beyond tissue-based testing. Clinical laboratories are developing specialized workflows and validated pipelines meeting regulatory requirements for diagnostic applications, supporting transition from research to clinical implementation.

End User Insights:

- Academic Institutes & Research Centers

- Hospitals & Clinics

- Pharmaceutical & Biotechnology Companies

- Others

Academic institutes & research centers exhibit a clear dominance with a 41.7% share of the total India next generation sequencing market in 2025.

Academic institutes and research centers lead market utilization through government-funded genome projects, basic research programs, and translational studies bridging discovery science to clinical applications. National genomic initiatives including the Genome India Project are concentrated in academic research institutions with sequencing infrastructure and computational resources supporting large-scale data generation. Basic research programs investigating disease mechanisms, evolutionary biology, and functional genomics drive sustained sequencing demand across university and government research laboratories nationwide. Collaborative research networks linking multiple institutions enable pooling of resources and expertise for ambitious sequencing projects addressing complex biological questions.

Research centers serve as training grounds for next generation of genomics researchers and bioinformaticians, creating skilled workforce supporting broader market ecosystem development. Technology evaluation and method development activities concentrated in academic settings generate evidence supporting clinical translation and commercial adoption of sequencing applications. Government research funding through agencies including Department of Biotechnology and Indian Council of Medical Research provides sustained support for sequencing infrastructure and operational costs. Academic medical centers combining research capabilities with clinical care facilitate translational research integrating genomic discoveries into patient care pathways. Collaborative partnerships between academic institutions and industry enable technology access, validation studies, and commercialization of research findings into diagnostic products.

Regional Insights:

- North India

- South India

- East India

- West India

West India leads with a share of 33.8% of the total India next generation sequencing market in 2025.

West India leads market concentration through high density of biotechnology companies, research institutions, and specialty hospitals in metropolitan areas including Mumbai, Pune, and Ahmedabad. The region hosts major pharmaceutical and biotechnology clusters with research and development capabilities driving demand for sequencing services supporting drug discovery and development programs. Academic research institutions contribute significant sequencing capacity supporting basic and translational research initiatives. Healthcare infrastructure concentration in tier-one cities provides patient populations and clinical expertise supporting diagnostic sequencing adoption in oncology and genetic disease specialties.

Venture capital availability and entrepreneurial ecosystems in western metropolitan areas support genomics startup development, expanding service provider landscape and driving competitive innovation. Government biotechnology initiatives and industrial parks in Maharashtra and Gujarat provide infrastructure supporting sequencing facility establishment and operations. Proximity to international connectivity through major airports and ports facilitates import of sequencing reagents and instruments, reducing supply chain complexities affecting market operations. Skilled workforce availability through engineering and life science educational institutions supports laboratory operations and bioinformatics analysis requirements. The region's established diagnostic laboratory networks are expanding sequencing capabilities to meet growing clinical demand for genomic testing across specialty care settings.

Market Dynamics:

Growth Drivers:

Why is the India Next Generation Sequencing Market Growing?

Government Support for Precision Medicine Initiatives

Government-led population genomics programs are establishing comprehensive genetic databases supporting precision medicine development and personalized healthcare delivery across India's diverse populations. National initiatives focusing on ethnic diversity mapping are addressing underrepresentation of Indian genomes in global databases, creating reference resources specific to regional populations and enabling discovery of population-specific disease variants. Substantial public funding through the Department of Biotechnology supports infrastructure development, research grants, and collaborative programs linking academic institutions, research centers, and healthcare providers. Regulatory frameworks are evolving to support genomic data sharing while protecting privacy, facilitating research collaboration and clinical implementation of genomic findings. The Genome India Project's completion provides foundational data resources enabling translational research projects developing diagnostic tools, therapeutic targets, and disease risk prediction models relevant to Indian populations. In 2025, Government announcements targeting sequencing of 10 million genomes demonstrate sustained commitment to building genomic infrastructure supporting long-term precision medicine goals. Translational research funding programs encourage utilization of population genomic data for developing cost-effective screening tools, pharmacogenomic applications, and rare disease diagnostics addressing unmet clinical needs. Public-private partnership models are emerging to leverage government data resources and private sector technology capabilities, accelerating clinical translation and commercial development of genomic applications.

Declining Sequencing Costs and Technology Advancement

Dramatic reductions in sequencing costs over the past decade have democratized access to genomic technologies previously limited to well-funded research institutions and specialty clinical programs. Whole genome sequencing costs falling below USD 500 per sample enable population-scale screening programs and research studies previously economically unfeasible within public health budgets. Technological improvements delivering higher throughput, increased accuracy, and simplified workflows reduce operational complexity and expand feasibility of sequencing adoption across smaller laboratories and healthcare facilities. Benchtop sequencing systems with lower capital costs and operational requirements enable distributed testing models bringing genomic capabilities closer to patients in regional medical centers. Reagent cost reductions driven by competition and manufacturing efficiencies are making recurring operational expenses more affordable, supporting sustained utilization growth across existing installed base. Bioinformatics platform improvements automating analysis workflows reduce computational expertise requirements and enable broader adoption by clinicians and laboratory professionals without specialized training. IMARC Group predicts that the India bioinformatics market is projected to attain USD 2,534.8 Million by 2033.

Increasing Cancer Burden Driving Diagnostics Demand

Rising cancer incidence across India is creating urgent demand for advanced diagnostic capabilities enabling early detection, precise classification, and personalized treatment selection. The frequency of cancer cases is estimated to increase by 12.8 per cent in 2025 as compared to 2020 and cancer cases in India may rise 67% by 2045. Genomic profiling of tumors provides actionable information guiding targeted therapy selection, predicting treatment response, and monitoring disease progression beyond capabilities of traditional diagnostic approaches. Liquid biopsy applications detecting circulating tumor DNA offer non-invasive monitoring alternatives to tissue biopsies, enabling serial testing throughout treatment courses for dynamic assessment of therapeutic efficacy. Expanding availability of targeted therapies and immunotherapies approved based on genomic biomarkers creates clinical utility for comprehensive tumor profiling in treatment decision-making. Cancer gene panel testing is becoming standard of care in major oncology centers for lung, breast, colorectal, and hematologic malignancies where actionable mutations guide therapy selection. Government healthcare initiatives establishing day care cancer centers expand treatment infrastructure requiring supporting diagnostic capabilities including genomic testing for precision oncology implementation. Growing awareness among oncologists and patients regarding personalized medicine benefits is driving referrals for genomic testing, supported by evidence demonstrating improved outcomes with biomarker-guided therapy selection. Insurance coverage and reimbursement frameworks are gradually expanding to include genomic testing for appropriate clinical indications, reducing financial barriers to patient access.

Market Restraints:

What Challenges the India Next Generation Sequencing Market is Facing?

Shortage of Skilled Bioinformatics Professionals

Limited availability of trained bioinformatics specialists and computational biologists capable of analyzing complex genomic datasets constrains market expansion and quality of insights derived from sequencing data. The gap between sequencing data generation capacity and analytical workforce availability creates bottlenecks in translating raw sequence information into clinically actionable insights. Academic training programs have not scaled proportionally with market growth, resulting in insufficient pipeline of qualified professionals entering genomics workforce. Competition for skilled talent among research institutions, diagnostic laboratories, and biotechnology companies drives compensation inflation and retention challenges. International migration of trained professionals to higher-paying markets reduces domestic workforce availability despite significant training investments. Interdisciplinary expertise requirements spanning molecular biology, statistics, programming, and clinical sciences create high barriers to rapid workforce development through traditional education pathways. Limited continuing education and professional development opportunities constrain upskilling of existing laboratory personnel to meet evolving technical requirements.

High Initial Platform Costs and Infrastructure Requirements

Substantial capital investments required for sequencing instrumentation, supporting laboratory equipment, and computational infrastructure present barriers to market entry for smaller healthcare facilities and research institutions. Supporting infrastructure including sample preparation equipment, quality control instruments, and high-performance computing systems add significant costs beyond primary sequencing platforms. Facility requirements for controlled environments, reliable power supply, and temperature regulation necessitate infrastructure investments particularly challenging in tier-two and tier-three cities. Ongoing maintenance costs, service contracts, and reagent inventory management create operational expense burdens requiring sustained utilization volumes for economic viability. Limited equipment financing options and absence of shared facility models in many regions constrain access to sequencing capabilities for smaller institutions. High upfront investments create risks for early adopters uncertain about utilization volumes and revenue generation potential from emerging clinical applications.

Regulatory Complexities in Genomic Data Handling

Evolving regulatory frameworks for genetic testing, data privacy, and clinical validation create uncertainties affecting commercial development and clinical implementation of sequencing-based diagnostics. Absence of clear guidelines for laboratory-developed tests using sequencing platforms complicates regulatory pathways for clinical implementation, particularly for novel applications. Genetic data privacy regulations and consent requirements add operational complexity and potential liability concerns for laboratories handling patient genomic information. International data transfer restrictions complicate collaborative research and commercial service models involving cross-border data flows for analysis or storage. Quality standards and proficiency testing requirements for genomic testing laboratories are still developing, creating uncertainties about compliance expectations and validation requirements. Lack of standardization across sequencing platforms and analysis pipelines complicates establishing consistent quality benchmarks and inter-laboratory comparability. Regulatory capacity limitations within oversight agencies create approval delays and unpredictable timelines for new test implementations. Ethical considerations regarding incidental findings, data ownership, and result disclosure require careful navigation affecting clinical workflow complexity.

Competitive Landscape:

The India next generation sequencing market features diverse competitive dynamics with international sequencing technology providers, global genomics service companies, and emerging domestic players operating across research and clinical segments. International platform manufacturers maintain dominant positions through established technology ecosystems, comprehensive reagent portfolios, and technical support infrastructure supporting installed instrument base. These players pursue market expansion through local partnership models, training programs, and collaborative initiatives with academic institutions and healthcare providers. Global genomics service providers operate through subsidiaries and partnerships offering comprehensive testing menus spanning oncology, rare diseases, and reproductive genetics supported by accredited laboratory facilities and proprietary analytical platforms. Domestic genomics companies are emerging with specialized capabilities in population genetics, agricultural applications, and cost-competitive testing services targeting underserved market segments. Academic research institutions play dual roles as technology adopters and service providers, offering sequencing capabilities to external researchers while conducting internal programs. Competition centers on factors including technology performance, cost competitiveness, turnaround times, data quality, regulatory compliance, and customer support capabilities. Collaborative partnerships between technology providers and healthcare institutions are common for establishing reference laboratories and clinical validation programs. Market consolidation activity includes acquisitions of domestic companies by international players seeking local market access and specialized capabilities.

India Next Generation Sequencing Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Sequencing Types Covered |

Whole Genome Sequencing, Targeted Resequencing, Whole Exome Sequencing, RNA Sequencing, CHIP Sequencing, De Novo Sequencing, Methyl Sequencing, Others |

|

Product Types Covered |

Instruments, Reagents and Consumables, Software and Services |

|

Technologies Covered |

Sequencing by Synthesis, Ion Semiconductor Sequencing, Single-Molecule Real-Time Sequencing, Nanopore Sequencing, Others |

|

Applications Covered |

Biomarker and Cancer, Drug Discovery and Personalized Medicine, Genetic Screening, Diagnostics, Agriculture and Animal Research, Others |

|

End Users Covered |

Academic Institutes & Research Centers, Hospitals & Clinics, Pharmaceutical & Biotechnology Companies, Others |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Next Generation Sequencing Market Report

The India next generation sequencing market size was valued at USD 283.65 Million in 2025.

The India next generation sequencing market is expected to grow at a compound annual growth rate of 19.67% from 2026-2034 to reach USD 1,427.18 Million by 2034.

Targeted resequencing dominated the market with 36.8% share in 2025, driven by cost-effectiveness in clinical diagnostics and widespread adoption for oncology applications where focused gene panels provide actionable therapeutic insights.

Key factors driving the India next generation sequencing market include government support for precision medicine initiatives through population genomics programs, declining sequencing costs per genome enabling broader accessibility, increasing cancer burden creating demand for genomic diagnostics, and technological advancements in bioinformatics platforms enabling clinical implementation.

Major challenges include shortage of skilled bioinformatics professionals capable of analyzing complex genomic datasets, high upfront capital costs for sequencing platforms and supporting infrastructure exceeding budgets of smaller institutions, regulatory complexities surrounding genetic testing and data privacy creating implementation uncertainties, and limited reimbursement frameworks constraining patient access to genomic testing services.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)