India Non-Dairy Creamer Market Size, Share, Trends and Forecast by Origin, Type, Form, Nature, Distribution Channel, End Use, and Region, 2026-2034

India Non-Dairy Creamer Market Summary:

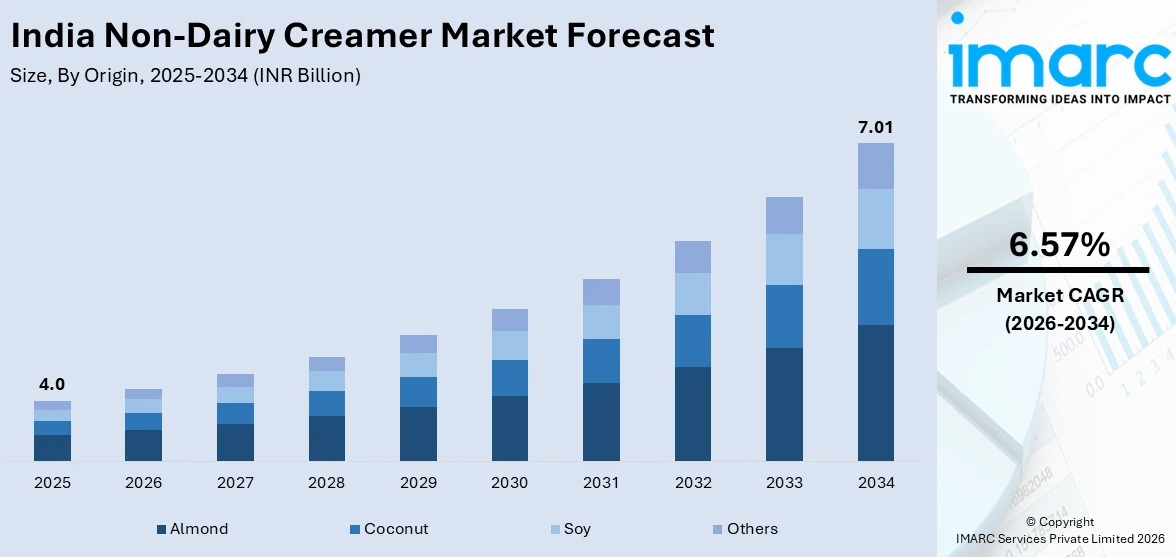

The India non-dairy creamer market size was valued at INR 4.0 Billion in 2025 and is projected to reach INR 7.01 Billion by 2034, growing at a compound annual growth rate of 6.57% from 2026-2034.

The India non-dairy creamer market is gaining strong traction due to rising health consciousness, increasing lactose intolerance awareness, and the growing adoption of plant-based and vegan dietary preferences among urban consumers. Expanding café culture, the booming food and beverage processing industry, and surging demand for convenient, shelf-stable products are further propelling growth. Enhanced digital distribution through e-commerce and quick-commerce platforms has broadened consumer accessibility, reinforcing the India non-dairy creamer market share across urban and semi-urban populations.

Key Takeaways and Insights:

- By Origin: Almond leads the market with a share of 25% in 2025, driven by strong consumer perception of almonds as a health-promoting, nutrient-rich plant base and rising preference for premium plant-based creamer alternatives among health-conscious Indian consumers.

- By Type: Medium fat NDC dominates the market with a revenue share of 40% in 2025, owing to its balanced fat content that delivers ideal creaminess, solubility, and whitening efficiency for diverse beverage and food processing applications.

- By Form: Powdered form represents the largest market share at 68% in 2025, reflecting strong preferences for shelf-stable, easily transportable, and cost-effective creamer formats suited to India's wide-ranging distribution conditions.

- By Nature: Conventional non-dairy creamer dominates the market with a revenue share of 71% in 2025, underpinned by its widespread availability, competitive pricing, and deeply established consumer familiarity in both retail and institutional segments.

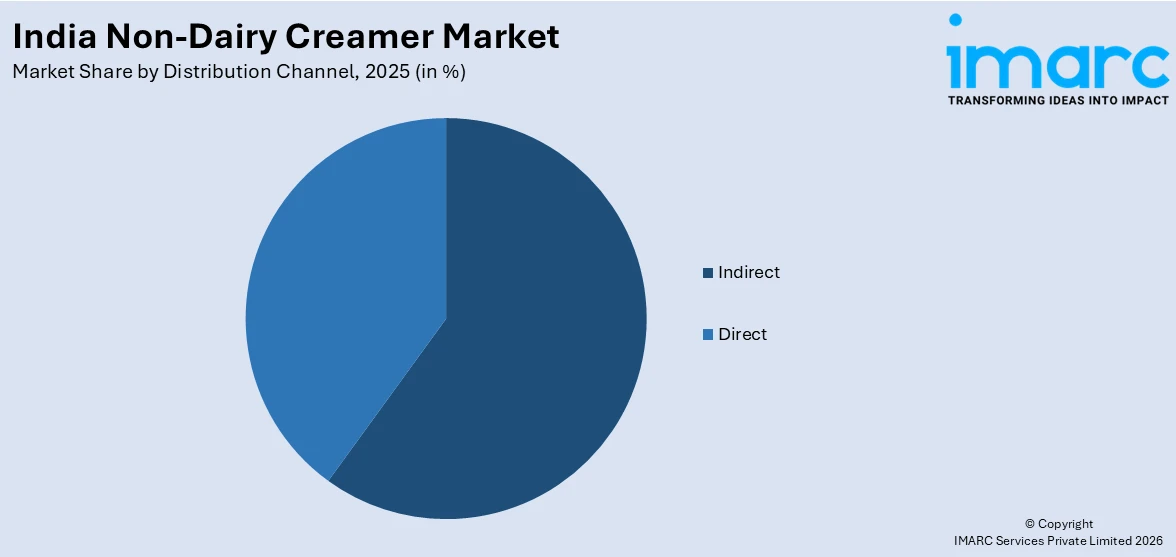

- By Distribution Channel: Indirect channels represent the leading segment with a 58% share in 2025, driven by broad retail access through hypermarkets, supermarkets, online platforms, and departmental stores serving diverse consumer geographies.

- By End Use: Household/retail leads the market with a share of 50% in 2025, reflecting growing at-home beverage consumption and rising consumer awareness of dairy-free alternatives among India's expanding middle class.

- Key Players: The India non-dairy creamer market features a moderately competitive landscape of domestic manufacturers, with players differentiating through product customization, FSSAI-compliant formulations, and vegan-friendly and clean-label creamer variants. Some of the Key players include Amrut International, Drytech Processes (I) Pvt. Ltd., Insta Foods, Krishna Food India, Pruthvi's Foods Private Limited, Venkatesh Natural Extract Pvt. Ltd., and Vinayak Ingredients (INDIA) Pvt. Ltd.

To get more information of this market Request Sample

The India non-dairy creamer market is witnessing robust expansion, underpinned by rising urbanization, evolving dietary preferences, and rapid proliferation of specialty coffee and tea culture. Increasing awareness of lactose intolerance and veganism is reshaping consumption patterns, with consumers actively seeking plant-based alternatives aligned with health, ethical, and sustainability priorities. Manufacturers are investing in product innovation, developing fortified and organic creamer variants enriched with vitamins and minerals to attract health-focused buyers. The food and beverage processing sector remains a substantial end-user, deploying non-dairy creamers across bakery products, soup premixes, beverage mixes, and ready-to-drink formulations. Expanding distribution through quick-commerce and e-commerce platforms is enhancing product availability in both metropolitan areas and tier-2 cities. For instance, in January 2025, Coffee Island, Greece's largest food service chain, launched its inaugural outlet in Gurugram in a partnership with Vita Nova, with plans toopen 20 locations by March 2026, reflecting the accelerating pace of India's café sector growth and the consequent demand for non-dairy creamer products.

India Non-Dairy Creamer Market Trends:

Rising Café Culture and Specialty Coffee Consumption

India’s coffeehouse ecosystem is witnessing strong expansion, fueled by rapid urbanization, rising disposable incomes, and a growing inclination toward premium beverage experiences among younger consumers. Both domestic and international café brands are increasingly entering smaller cities, broadening the organized café footprint beyond metropolitan areas. This shift is generating consistent institutional demand for shelf-stable and high-performance non-dairy creamers used in coffee and specialty beverages. Additionally, rising foreign participation in the café segment is further strengthening the overall supply chain and supporting sustained growth in the non-dairy creamer market.

Expansion of E-Commerce and Quick-Commerce Distribution Channels

The rapid expansion of digital retail platforms is fundamentally reshaping non-dairy creamer distribution in India, significantly improving product access for household consumers, home bakers, and small food businesses. Quick-commerce and online grocery platforms are enlarging product assortment and geographic coverage, enabling high-frequency repurchase behavior for packaged food ingredients. Swiggy Instamart expanded its quick-commerce operations to 100 cities across India in March 2025, making over 30,000 products available for rapid delivery. This accelerating digital distribution ecosystem is lowering purchase friction, encouraging consumer trial of non-dairy creamer variants, and broadening the addressable retail market beyond traditional organized grocery formats.

Growing Preference for Plant-Based and Lactose-Free Alternatives

India's evolving dietary landscape is driving measurable demand for plant-based and lactose-free food products, benefiting non-dairy creamer categories directly. Rising awareness of lactose intolerance and the growing vegan and flexitarian movement, particularly among urban, health-conscious demographics, are prompting consumers to adopt almond, soy, and coconut-based creamer alternatives. In May 2025, the Food Safety and Standards Authority of India (FSSAI) proposed stricter regulations for dairy analogue products, mandating detailed label declarations and restricting manufacturing to licensed businesses. While adding compliance requirements, these regulatory developments are ultimately strengthening consumer trust in non-dairy products, catalyzing greater transparency and long-term adoption in the category.

Market Outlook 2026-2034:

India's non-dairy creamer market is poised for sustained expansion over the forecast period, supported by rising health awareness, growing food service infrastructure, and expanding household consumption patterns. Urban cafés, quick-service restaurants, and food processing businesses will continue driving volume growth, while retail and e-commerce channels further enhance product accessibility across geographies. Innovation in organic, low-fat, and functionally enriched formulations will widen the addressable consumer base. Additionally, increasing regulatory emphasis on labeling transparency and quality standards is expected to further formalize the market and build stronger consumer trust. The market generated a revenue of INR 4.0 Billion in 2025 and is projected to reach a revenue of INR 7.01 Billion by 2034, growing at a compound annual growth rate of 6.57% from 2026-2034.

India Non-Dairy Creamer Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Origin |

Almond |

25% |

|

Type |

Medium Fat NDC |

40% |

|

Form |

Powdered |

68% |

|

Nature |

Conventional |

71% |

|

Distribution Channel |

Indirect |

58% |

|

End Use |

Household/Retail |

50% |

Origin Insights:

- Almond

- Coconut

- Soy

- Others

Almond leads with a market share of 25% of the total India non-dairy creamer market in 2025.

Almond-based non-dairy creamer has emerged as the preferred origin segment, attributable to growing consumer perception of almonds as a health-promoting ingredient naturally rich in proteins, vitamins, and healthy fats. Demand is particularly strong among urban, health-conscious consumers who seek plant-based beverages replicating the creaminess of dairy without associated digestive concerns. Almond-derived creamers command premium positioning across both retail and food service applications, with manufacturers investing in improved emulsification techniques that enhance solubility and texture. As India's plant-based dietary preferences gain further traction, almond-based non-dairy creamers remain central to product innovation strategies and category premiumization.

The almond segment's growth is reinforced by rising adoption of almond-based beverages across specialty café chains and home-brewing consumers. Almond creamers are increasingly featured in nutritional beverage formulations including protein drinks and specialty teas, expanding their utility beyond conventional coffee whitening. Manufacturers are differentiating through fortified variants enriched with calcium and vitamin B12, catering to lactose-intolerant and vegan consumers seeking nutritionally enhanced alternatives. The segment also benefits from growing consumer awareness of its environmental credential as a minimally processed, plant-derived ingredient, aligning with broader sustainability-driven purchasing priorities among younger demographics.

Type Insights:

- Low Fat NDC

- Medium Fat NDC

- High Fat NDC

Medium fat NDC represents the largest share of 40% of the total India non-dairy creamer market in 2025.

Medium-fat non-dairy creamers occupy the dominant position owing to their versatile application profile and balanced sensory characteristics that appeal to both foodservice operators and household users. Their fat content, typically ranging between 20% and 30%, delivers an ideal balance of creaminess, solubility, and whitening efficiency for standard coffee and tea preparations. The segment aligns well with the cost-efficiency objectives of food processing companies and institutional buyers that require consistent product performance across high-volume applications. Expanding usage in instant beverage mixes, soup premixes, and ready-to-drink formulations continues to reinforce its leading position within the India non-dairy creamer market.

From a processing standpoint, medium fat NDC exhibits favorable emulsification and stability properties, making it a preferred ingredient in bakery products, ice cream applications, and convenience foods. Manufacturers favor this category for its broad formulation compatibility and lower raw material costs compared to high-fat variants. Consumer preference for products that replicate dairy creaminess while maintaining moderate fat levels further sustains demand. Increasing research and development (R&D) investments in improving medium fat creamer texture and extending shelf life are expected to widen the application scope and reinforce market share throughout the forecast period.

Form Insights:

- Powdered

- Liquid

Powdered led the highest revenue share at 68% of the total India non-dairy creamer market in 2025.

Powdered non-dairy creamers hold a commanding share primarily due to their extended shelf life, convenience of storage and transportation, and cost-effectiveness compared to liquid alternatives. These advantages make powdered formats particularly well-suited for India's diverse supply chain conditions, including distribution to remote and rural markets where cold-chain infrastructure remains limited. In food and beverage processing, powdered creamers offer precise dosing capabilities and formulation consistency, making them the preferred choice for instant beverage manufacturers, bakery producers, and premix companies operating at scale across the country.

The dominance of the powdered format is further reinforced by household purchase behavior, where consumers prefer bulk-pack creamers for at-home tea and coffee preparation. Quick-dissolving spray-dried powder variants with shelf lives extending to 24 months are particularly valued in the Indian market for minimizing wastage and enabling cost-efficient large-pack purchasing. Institutional and food service buyers also rely on powdered creamers for standardized use in high-volume commercial operations. Product innovation in micro-encapsulated and instant-dissolve powder variants continues to expand application versatility and consumer acceptability within this segment.

Nature Insights:

- Organic

- Conventional

Conventional exhibits a clear dominance with a 71% share of the total India non-dairy creamer market in 2025.

Conventional non-dairy creamers dominate the market due to their widespread availability, cost-competitiveness, and entrenched consumer familiarity. These products are formulated using vegetable oils, corn syrup solids, sodium caseinate, and standard emulsifiers, providing consistent performance across a wide range of food and beverage applications. Price sensitivity among a large segment of Indian consumers, particularly in tier-2 and tier-3 cities, continues to anchor demand for conventional variants. Food processing companies and institutional buyers favor them for bulk procurement due to reliable supply chains, predictable pricing structures, and well-established formulation track records.

While organic alternatives are gaining momentum among health-conscious urban consumers, the conventional segment retains its market share advantage through established manufacturing infrastructure and competitive pricing. Conventional creamers meet the functional requirements of mass-market food processing applications, including premix beverages, bakery, and ice cream, where ingredient cost management is critical to profitability. Manufacturers are innovating within the conventional category by improving nutritional profiles, such as reducing trans-fat content and adding micronutrient fortification, to enhance product appeal without significantly increasing production costs or compromising market accessibility.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Direct

- Indirect

- Hypermarkets/Supermarkets

- Online Stores

- Departmental Stores

- Others

Indirect represent the leading segment with 58% of the total India non-dairy creamer market in 2025.

Indirect distribution channels dominate owing to their broad geographic coverage and ability to reach diverse consumer segments across urban, semi-urban, and emerging markets. Hypermarkets and supermarkets anchor the indirect channel through extensive shelf availability and brand visibility, enabling consumer trial and impulse purchases. As organized retail expands beyond metro cities into tier-2 and tier-3 locations, indirect channels are increasingly serving as the primary point of contact for household and institutional non-dairy creamer buyers seeking product variety and competitive value propositions.

Online stores represent the fastest-growing sub-channel within indirect distribution, driven by the rapid expansion of India's digital grocery platforms. The Indian online grocery market size was valued at USD 14.33 Billion in 2025 and is projected to reach USD 101.99 Billion by 2034, growing at a compound annual growth rate of 24.36% from 2026-2034, significantly improving last-mile accessibility for household non-dairy creamer buyers. Quick-commerce models enable high-frequency repurchase behavior, further strengthening the indirect channel's market position. Departmental stores and specialty food outlets also contribute meaningfully, particularly in catering to premium and organic non-dairy creamer variants across niche urban segments.

End Use Insights:

- HoReCa/Foodservices

- Food and Beverage Processing

- Food Premixes

- Soups and Sauces

- Beverage Mixes

- Bakery Products and Ice Creams

- RTD Beverages

- Infant Food

- Prepared and Packaged Food

- Household/Retail

Household/retail represent the largest share of 50% of the total India non-dairy creamer market in 2025.

The household and retail end-use segment leads the market, reflecting growing at-home consumption of instant beverages, coffee, and tea among India's expanding middle class. Rising health consciousness, coupled with increasing awareness of lactose intolerance and plant-based dietary options, is driving household adoption of non-dairy creamers as a regular pantry staple. The penetration of organized retail and e-commerce platforms has significantly improved product accessibility, enabling consumers in smaller cities and towns to incorporate non-dairy creamers into daily routines previously dominated by traditional dairy additives.

The household segment is further supported by a rising home-brewing culture, particularly in urban areas where specialty coffee consumption is growing at a sustained pace. Single-serve and bulk-pack powdered creamer SKUs are gaining traction among household buyers seeking convenience and cost savings. As disposable incomes rise and consumer exposure to global beverage culture increases, demand for premium, flavored, and organic household creamer variants is expected to expand. Retailers are responding by dedicating shelf space to non-dairy creamer categories, improving brand visibility and consumer engagement within this leading end-use segment.

Regional Insights:

- Maharashtra

- Tamil Nadu

- Uttar Pradesh

- Gujarat

- Karnataka

- West Bengal

- Rajasthan

- Andhra Pradesh

- Telangana

- Madhya Pradesh

- Delhi NCR

- Punjab

- Haryana

- Others

Maharashtra leads the India non-dairy creamer market, driven by its large urban population, concentrated café and food service infrastructure in Mumbai and Pune, and high consumer awareness of plant-based and lactose-free products. The state's advanced organized retail networks further support distribution depth.

Tamil Nadu represents a significant market owing to its strong tea-drinking culture and expanding café sector in Chennai and Coimbatore. Rising health awareness and growing demand for dairy-free alternatives among the urban professional demographic contribute to steady creamer consumption.

Uttar Pradesh is a key volume market due to its large consumer base and expanding food processing industry. Growing urbanization in cities such as Lucknow, Noida, and Kanpur is driving incremental demand for non-dairy creamers in both institutional and household segments.

Gujarat benefits from its well-developed food processing industry and strong entrepreneurial food manufacturing base. Growing preference for convenience food ingredients and the state's prominent dairy industry backdrop make it an important adoption market for non-dairy creamer alternatives.

Karnataka, home to Bengaluru's thriving tech-driven café culture, represents a dynamic market for premium non-dairy creamers. The city's large young professional population and specialty coffee culture drive sustained demand for innovative and plant-based creamer products.

West Bengal's food processing industry and urban demand in Kolkata contribute to consistent non-dairy creamer consumption. Growing adoption of packaged beverage products in retail and foodservice settings supports market expansion in this eastern state.

Rajasthan is an emerging market where expanding organized retail, rising tourism-linked hospitality demand, and increasing health awareness are beginning to drive non-dairy creamer adoption. Tier-2 cities are increasingly becoming growth hotspots for packaged food ingredients.

Andhra Pradesh benefits from a large food processing sector and growing café presence in Visakhapatnam and other urban centers. Increasing consumer familiarity with non-dairy alternatives is gradually expanding market penetration across both retail and institutional channels.

Telangana, anchored by Hyderabad's vibrant food service market, offers strong growth potential. The city's expanding café ecosystem and significant HoReCa sector drive institutional demand for non-dairy creamers used in beverage and food preparation applications.

Madhya Pradesh is witnessing steady growth in non-dairy creamer demand, supported by food manufacturing cluster development and increasing organized retail penetration in cities like Indore and Bhopal that are experiencing rapid urbanization.

Delhi NCR stands among the top-consuming regions, driven by high consumer awareness, premium café culture, and wide-ranging organized retail coverage. The region's large HoReCa sector and fast-growing quick-commerce ecosystem underpin significant non-dairy creamer consumption.

Punjab's food processing industry and growing health-conscious consumer base in Chandigarh and Ludhiana contribute to increasing non-dairy creamer adoption. Expansion of modern retail formats and café chains is progressively enlarging the addressable market in the region.

Haryana, with its proximity to Delhi NCR and growing food processing sector, is an emerging non-dairy creamer market. Rising urbanization and expanding institutional food procurement in the region are supporting incremental consumption growth.

Market Dynamics:

Growth Drivers:

Why is the India Non-Dairy Creamer Market Growing?

Thriving Food and Beverage Processing Industry

India's food and beverage processing industry has emerged as one of the largest end-users of non-dairy creamers, deploying them across an extensive portfolio of applications, including instant beverage mixes, bakery products, soup premixes, ice creams, infant formula, and convenience foods. Non-dairy creamers enhance texture, whitening, and emulsification in processed food products while extending shelf life, which are critical requirements for mass-market manufacturers. The growing proliferation of branded ready-to-drink beverage categories, particularly tea and coffee premixes, is creating sustained incremental demand. India's food processing sector, supported by government investment in infrastructure and cold-chain expansion, is projected to maintain robust output growth, reinforcing consistent demand for specialty food ingredients, including non-dairy creamers, throughout the forecast period.

Rising Urbanization and Expanding Café and HoReCa Sector

India's accelerating urbanization, growing disposable incomes, and evolving consumer lifestyles are driving rapid expansion of the café, restaurant, and hospitality sector, a significant institutional end-user of non-dairy creamers. The proliferation of branded and independent café chains into tier-2 and tier-3 cities is creating new demand hotspots. The India coffee shops/cafes market size reached USD 424.6 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 1,152.1 Million by 2034, exhibiting a growth rate (CAGR) of 11.14% during 2026-2034. HoReCa establishments depend on non-dairy creamers for consistent and cost-effective beverage preparation, making them essential in large-scale food service operations. This growing reliance is driving increased bulk demand for non-dairy creamers and related ingredients.

Growing Health Consciousness, Lactose Intolerance Awareness, and Vegan Adoption

A secular shift in Indian consumer values, driven by rising health consciousness, urbanization, and exposure to global dietary trends, is substantially enlarging the addressable market for non-dairy creamer products. India's large lactose-intolerant population, which includes a significant proportion of the adult demographic, is increasingly seeking plant-based alternatives that provide comparable sensory experiences to dairy without digestive discomfort. Simultaneously, vegan and flexitarian dietary adoption is growing, particularly among urban millennials and Gen Z consumers. Plant-derived creamers, including almond, soy, and coconut variants, benefit directly from these twin demand trends, reinforcing long-term category growth momentum and driving sustained product innovation in the India non-dairy creamer market.

Market Restraints:

What Challenges the India Non-Dairy Creamer Market is Facing?

Competition from Entrenched Dairy-Based Products

Non-dairy creamers face intense competition from conventional dairy whiteners and milk powder, which benefit from deep-rooted consumer loyalty and well-established supply chains. A significant segment of Indian consumers, particularly in rural and semi-urban areas, maintains strong preference for dairy-based products supported by cultural familiarity and trusted taste profiles, limiting non-dairy creamer adoption and constraining market penetration in price-sensitive consumer segments.

Regulatory Uncertainty Around Plant-Based Product Labeling

The evolving regulatory landscape governing dairy analogues in India introduces compliance complexity for non-dairy creamer manufacturers. FSSAI's ongoing deliberations over labeling standards for plant-based and non-dairy products create market uncertainty, potentially affecting product positioning strategies, export credentials, and consumer communication for brands targeting health and wellness segments, imposing additional compliance costs on manufacturers.

Raw Material Price Volatility and Supply Chain Constraints

Non-dairy creamers rely on commodity inputs including vegetable oils, corn syrup solids, sodium caseinate, and stabilizers, whose prices are subject to global market fluctuations. Volatility in palm oil and specialty nut prices can substantially impact production costs, compressing manufacturer margins and complicating long-term pricing strategies across retail and institutional segments, potentially limiting product affordability and market expansion in cost-sensitive channels.

Competitive Landscape:

The India non-dairy creamer market is characterized by a moderately competitive landscape comprising established domestic manufacturers and specialty food ingredient companies. Competitive dynamics are shaped by product quality, formulation customization capabilities, price competitiveness, and distribution reach. Key players are differentiating through investment in spray-drying manufacturing technology, FSSAI-compliant formulations, and expanded vegan and clean-label creamer portfolios designed to capture health-conscious consumer segments. Strategic partnerships with food service chains, institutional buyers, and online grocery platforms are becoming important levers for market share expansion. Companies with large production capacities and strong raw material sourcing networks hold inherent advantages in pricing and supply reliability, enabling them to serve both domestic and export markets effectively. Some of the major market players include:

- Amrut International

- Drytech Processes (I) Pvt. Ltd.

- Insta Foods

- Krishna Food India

- Pruthvi's Foods Private Limited

- Venkatesh Natural Extract Pvt. Ltd.

- Vinayak Ingredients (INDIA) Pvt. Ltd.

India Non-Dairy Creamer Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion INR |

| Origins Covered | Almond, Coconut, Soy, Others |

| Types Covered | Low Fat NDC, Medium Fat NDC, High Fat NDC |

| Forms Covered | Powdered, Liquid |

| Natures Covered | Organic, Conventional |

| Distribution Channels Covered |

|

| End Uses Covered |

|

| Regions Covered | Maharashtra, Tamil Nadu, Uttar Pradesh, Gujarat, Karnataka, West Bengal, Rajasthan, Andhra Pradesh, Telangana, Madhya Pradesh, Delhi NCR, Punjab, Haryana, Others |

| Companies Covered | Amrut International, Drytech Processes (I) Pvt. Ltd., Insta Foods, Krishna Food India, Pruthvi's Foods Private Limited, Venkatesh Natural Extract Pvt. Ltd., Vinayak Ingredients (INDIA) Pvt. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Non-Dairy Creamer Market Report

The India non-dairy creamer market size was valued at INR 4.0 Billion in 2025.

The India non-dairy creamer market is expected to grow at a compound annual growth rate of 6.57% from 2026-2034 to reach INR 7.01 Billion by 2034.

Almond, commanding the largest origin share at 25% in 2025, leads owing to strong consumer perception of almonds as a natural, nutrient-rich plant base and the growing preference for premium, plant-based creamer alternatives among health-conscious Indian consumers.

Key factors driving the India non-dairy creamer market include rising health consciousness, growing lactose intolerance awareness, expanding café and HoReCa sectors, increasing food and beverage processing demand, growing veganism and plant-based dietary adoption, and expanding digital retail distribution channels.

Major challenges include strong competition from established dairy-based products, regulatory uncertainty surrounding plant-based product labeling, raw material price volatility, limited consumer awareness in rural areas, and supply chain constraints affecting ingredient sourcing and cost management.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)