India Non-Ferrous Metals Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

India Non-Ferrous Metals Market Size, Share, Trends & Forecast (2026-2034)

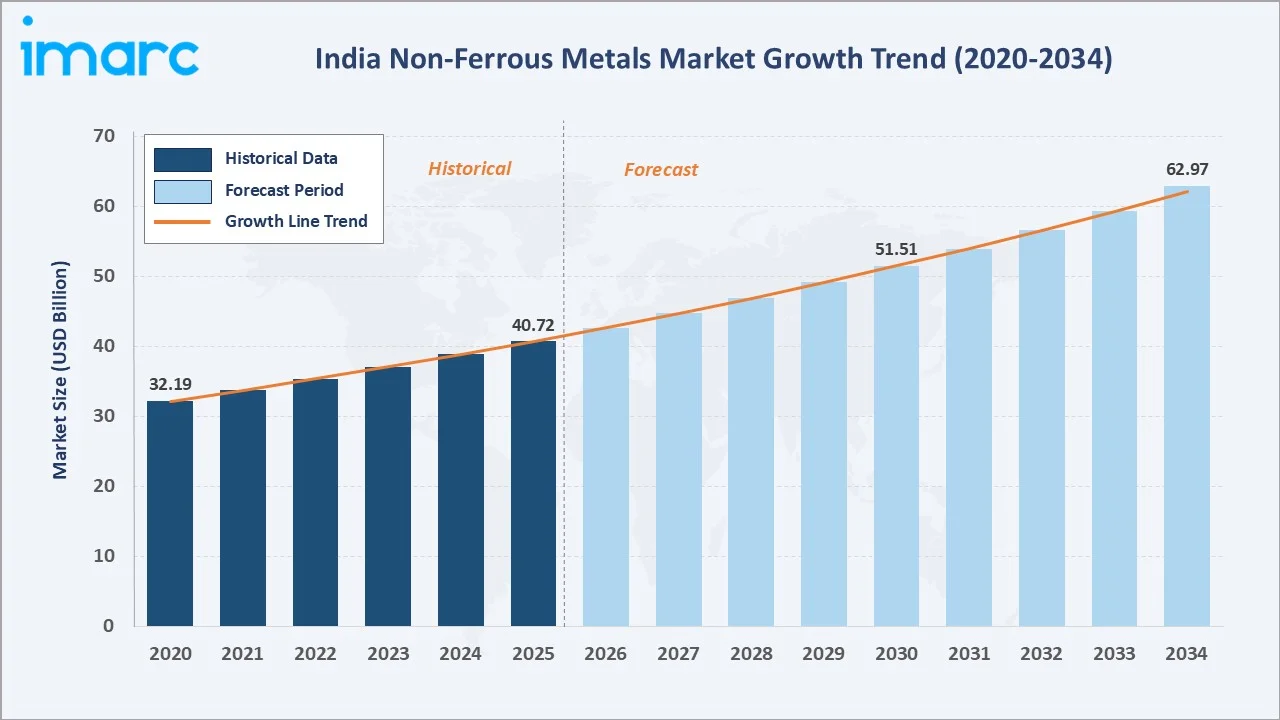

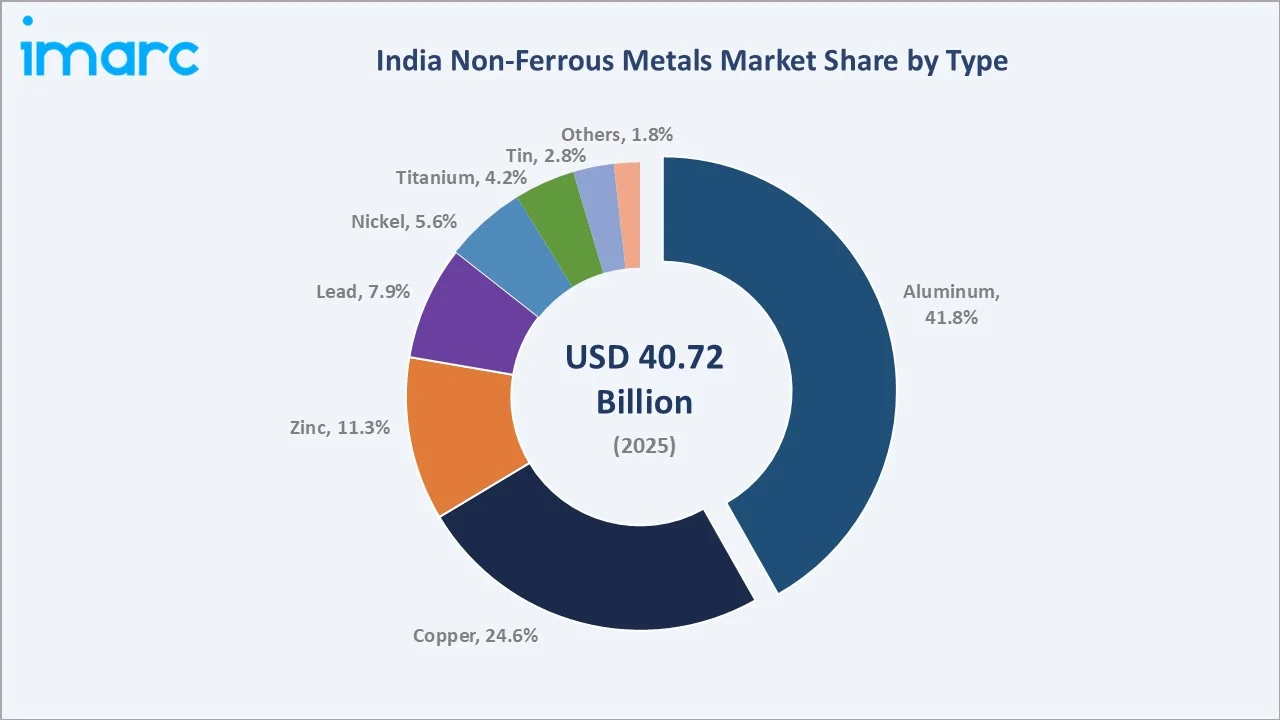

The India non-ferrous metals market reached USD 40.72 Billion in 2025 and is projected to reach USD 62.97 Billion by 2034, growing at a CAGR of 4.81% during 2026-2034. Sustained infrastructure investment under the National Infrastructure Pipeline, rapid electric vehicle adoption requiring copper and aluminum, government initiatives including Make in India and the Production Linked Incentive (PLI) scheme, and India’s expanding construction and electronic power sectors are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 40.72 Billion |

|

Forecast Market Size (2034) |

USD 62.97 Billion |

|

CAGR (2026-2034) |

4.81% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Segment (Type) |

Aluminum – 41.8% share (2025) |

|

Largest Application |

Construction Industry – 36.4% share (2025) |

|

Leading Region |

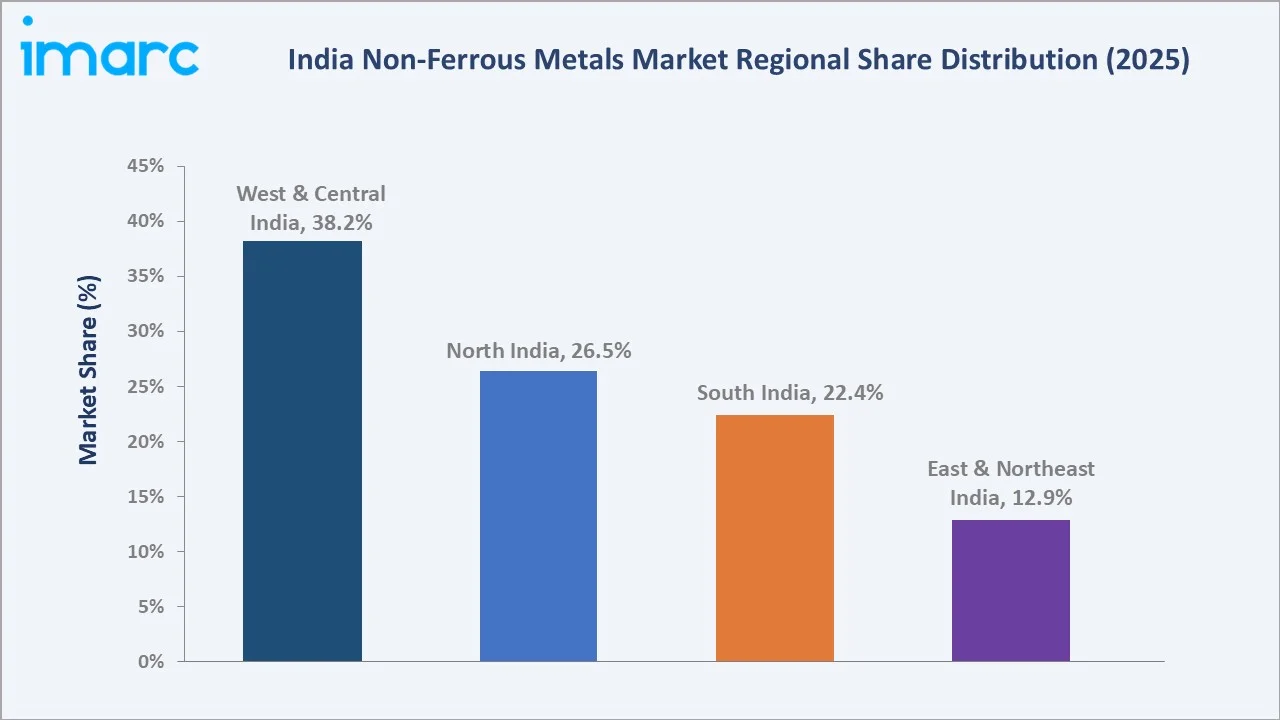

West and Central India – 38.2% share (2025) |

West and Central India lead regionally, holding a 38.2% market share in 2025, anchored by Gujarat’s copper refining clusters, Maharashtra’s automotive demand, and Chhattisgarh’s aluminum smelting base. Aluminum commands the dominant 41.8% share among metal types, reflecting its broad use across construction, transportation, power, and packaging.

To get more information on this market, Request Sample

India’s non-ferrous metals market is underpinned by three structural forces: infrastructure-led industrialization, the green energy and EV transition driving copper and aluminum demand, and the government’s strategic focus on building domestic smelting and refining capacity to reduce import dependency. Each force independently sustains multiple metal categories, collectively supporting above-GDP-growth CAGR through 2034.

Executive Summary

The India non-ferrous metals market is experiencing robust, broad-based expansion driven by the convergence of infrastructure investment, industrial modernization, and the global green energy transition. The market was valued at USD 40.72 Billion in 2025 and is forecast to reach USD 62.97 Billion by 2034, growing at a CAGR of 4.81%. This growth trajectory is anchored by India’s National Infrastructure Pipeline committing over INR 111 lakh crore (USD 1.5 trillion) through 2020 to 2025, driving sustained aluminum and copper consumption across construction, power, and transportation.

Aluminum dominates the type segment with a 41.8% share in 2025, followed by copper at 24.6%, zinc at 11.3%, and lead at 7.9%. The construction industry is the largest application at 36.4%, followed by the automobile industry at 28.7% and the electronic power industry at 24.1%. West and Central India lead regionally at 38.2%, underpinned by Gujarat’s copper processing infrastructure and Maharashtra’s dense automotive manufacturing base.

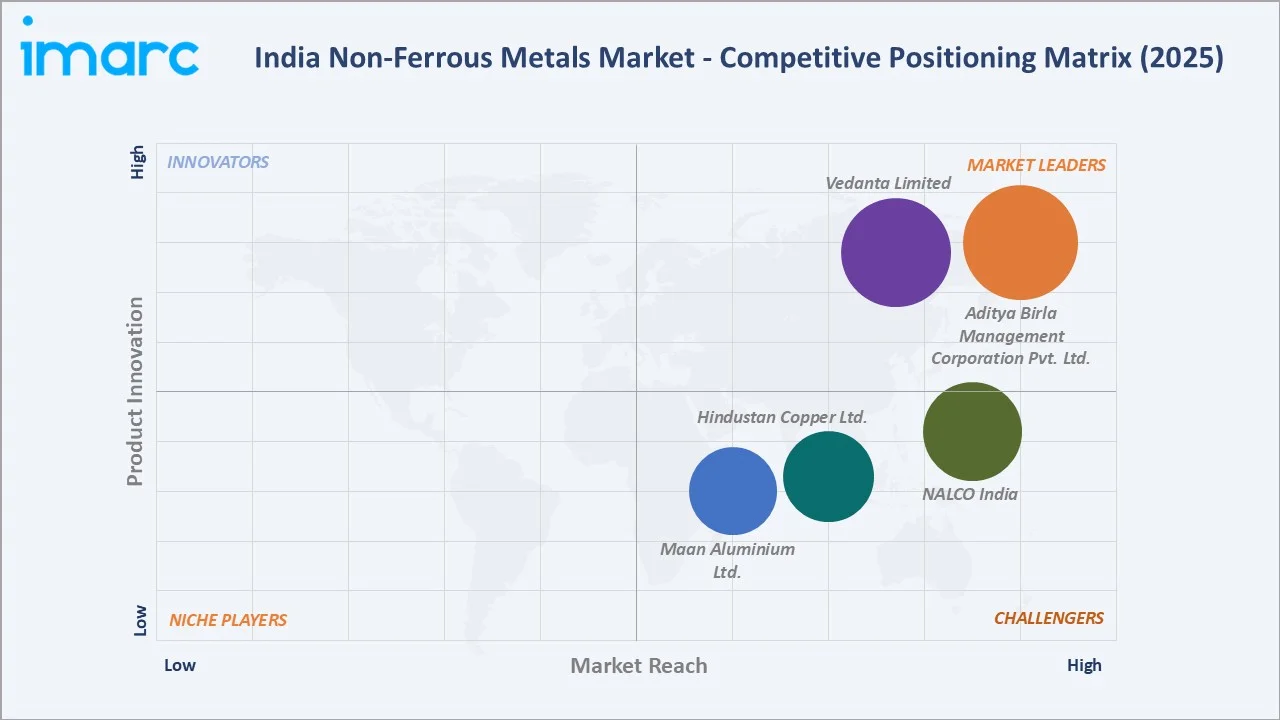

Leading domestic players, including Aditya Birla Management Corporation Pvt. Ltd., Vedanta Limited, NALCO India, Hindustan Copper Ltd., and Maan Aluminium Ltd., collectively account for approximately 65–70% of primary metal production value. India’s strategic priority to reduce metal import dependency through enhanced domestic capacity positions the sector for sustained long-term growth.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Aluminum – 41.8% share (2025) |

|

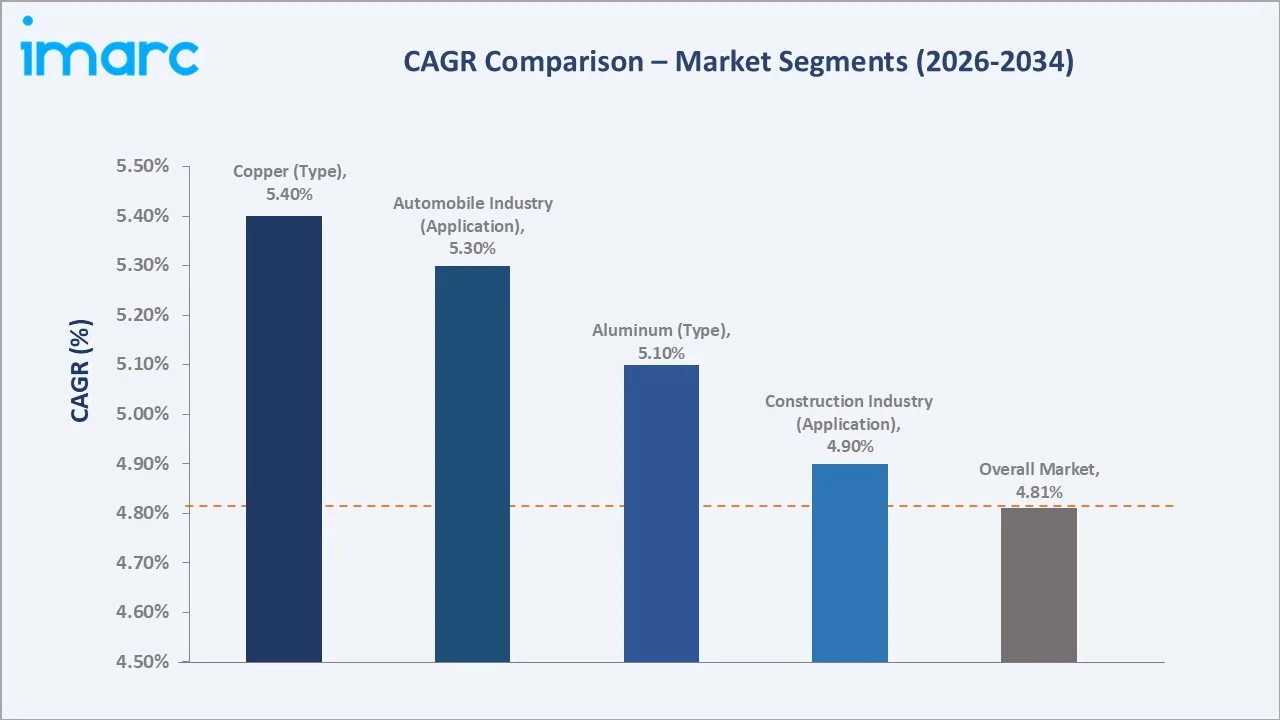

Fastest Growing Type |

Copper – ~5.4% CAGR (2026-2034) |

|

Largest Application |

Construction Industry – 36.4% share (2025) |

|

Fastest Growing Application |

Automobile Industry – ~5.3% CAGR (2026-2034) |

|

Leading Region |

West and Central India – 38.2% share (2025) |

|

Top Companies |

Aditya Birla Management Corporation Pvt. Ltd., Vedanta Limited, NALCO India, Hindustan Copper Ltd., and Maan Aluminium Ltd. |

Key Analytical Observations Supporting the Above Data:

- Aluminum’s 41.8% share reflects its pervasive use across construction (structural profiles, roofing, facades), transportation (automotive panels, rail wagons), packaging (beverage cans, pharmaceutical foil), and power (overhead transmission conductors). India is a significant producer of primary aluminum, contributing 6% to global production, with output projected to increase from 4 million tons (MT) in 2023 to 37 million tons (MT) by 2070.

- Copper at 24.6% remains indispensable for power sector expansion, EV charging infrastructure, and electronics manufacturing. India’s structural copper deficit, with domestic production well below consumption, creates a significant opportunity for capacity additions.

- Construction Industry’s 36.4% share reflects India’s urban housing shortage of approximately 18.78 million units, the PMAY program targets, and commercial real estate expansion across Tier-1 and Tier-2 cities, all requiring aluminum extrusions, copper wiring, and zinc-coated structural components.

- West and Central India’s 38.2% share reflects the region’s concentration of primary smelting facilities, Gujarat’s copper processing ecosystem, and Maharashtra’s dense automotive OEM manufacturing base in Pune and Chakan.

India Non-Ferrous Metals Market Overview

Non-ferrous metals are metallic elements or alloys that do not contain iron as a primary component. These metals are prized for their unique properties, including corrosion resistance, electrical conductivity, malleability, and lightweight characteristics. In India, the market encompasses mining, smelting, refining, and downstream fabrication of aluminum, copper, zinc, lead, nickel, titanium, tin, and specialty metals, serving industries from construction and transportation to electronics and renewable energy.

Macroeconomic drivers include India’s GDP growth averaging 6–7% annually, government capital outlay in infrastructure budgeted at INR 11.21 Lakh Crore in the Union Budget FY26, and the PLI scheme for advanced chemistry cell batteries directly stimulating nickel and lithium demand. India’s position as the world’s third-largest electricity consumer drives sustained copper demand for power transmission network expansion.

Market Dynamics

To evaluate market opportunities, Request Sample

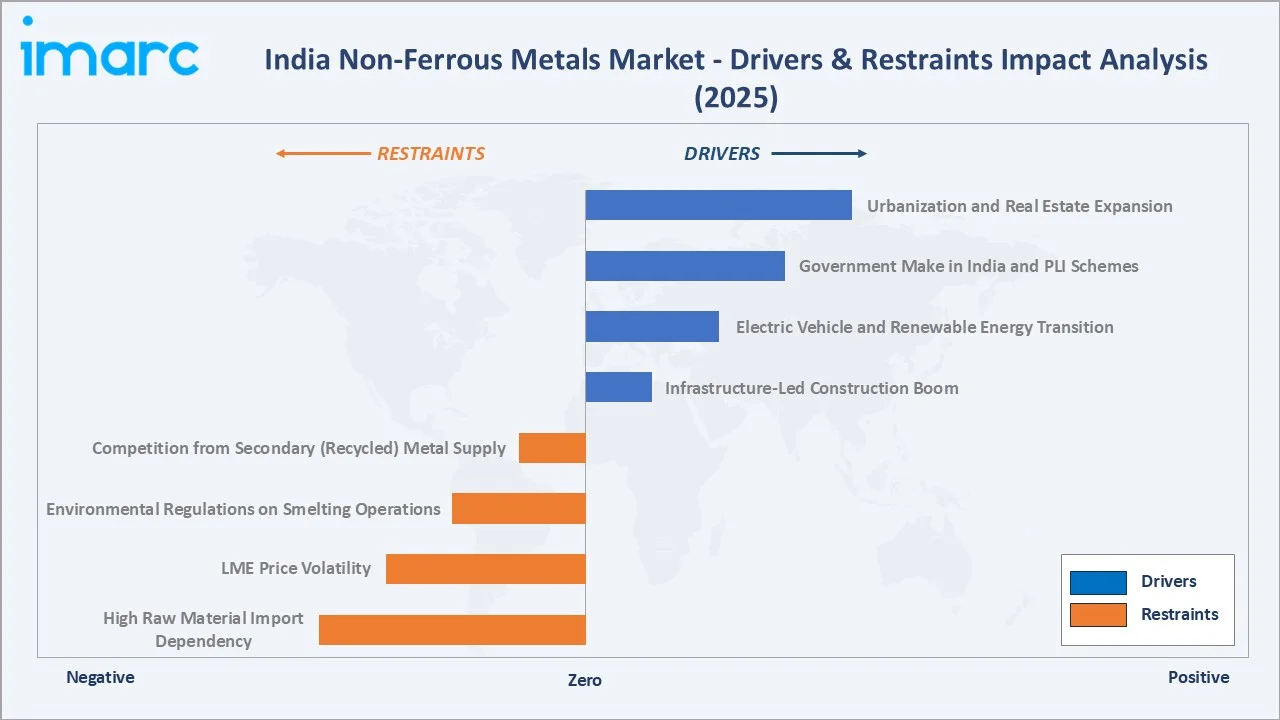

Market Drivers

- Infrastructure-Led Construction Boom: India’s National Infrastructure Pipeline targets USD 1.5 Trillion in investment through 2025, directly driving non-ferrous metals consumption. Each kilometer of metro rail requires approximately 1,200–1,500 metric tons of aluminum and copper; 26-29 operational metro systems represent continuous procurement pipelines.

- Electric Vehicle and Renewable Energy Transition: According to the Federation of Automobile Dealers Associations (FADA), the electric vehicle (EV) industry reached over 2 million registrations by November for the 2025 calendar year, with each EV requiring 60-80 kg of copper for wiring harnesses and traction motors. India’s 500 GW renewable energy target by 2030 also necessitates substantial copper for solar wiring and aluminum for solar panel frames.

- Government Make in India and PLI Schemes: The PLI scheme for specialty steel and advanced chemistry cell batteries, combined with the FAME-II EV incentive, is catalyzing domestic demand for aluminum, copper, nickel, and cobalt. These schemes reduce import-substitution risk and create captive procurement for domestic producers.

- Urbanization and Real Estate Expansion: India’s urban population is projected to reach 600 million by 2031, necessitating 25 million additional housing units. Each new residential unit requires approximately 8–12 kg of copper wiring and 40–80 kg of aluminum doors, windows, and plumbing fixtures.

Market Restraints

- High Raw Material Import Dependency: In FY24, India’s refined copper consumption was 0.844 MT, and copper concentrate imports are expected to reach 91%–97% by 2047, making domestic producers vulnerable to global supply disruptions and currency fluctuations.

- LME Price Volatility: Non-ferrous metal prices are determined on the London Metal Exchange, exposing Indian manufacturers to global commodity price cycles. Copper price swings of 15–25% within a financial year create significant working capital pressure for downstream fabricators.

- Environmental Regulations on Smelting Operations: The National Green Tribunal and Ministry of Environment’s tightening emission norms for SO₂, NOx, and particulate matter from copper and zinc smelting require significant capital investment in flue gas desulphurization and electrostatic precipitator upgrades.

- Competition from Secondary (Recycled) Metal Supply: India is expected to have a shortfall of ~1.6 MT of aluminum production capacity by FY30 and competes directly with primary producers on price. The government’s Scrap Metal Policy 2021 is increasing secondary metal availability, constraining primary producers’ price realization.

Market Opportunities

- Copper Capacity Localization: Adani Enterprises Limited's subsidiary, Kutch Copper Limited, a copper smelter in Gujarat with a 500,000 metric ton per annum capacity, which applied for London Metal Exchange recognition in August 2025, represents the most significant copper capacity addition in two decades, directly reducing India’s refined copper import dependency.

- Battery Metal Value Chain Development: India’s National Battery Policy and PLI scheme for advanced chemistry cells create investment opportunities across nickel, cobalt, manganese, and lithium processing. Companies establishing battery-grade processing in India qualify for a 20% National Programme on Advanced Chemistry Cell (ACC) Battery Storage incentive over five years.

Market Challenges

- Power Cost Disadvantage for Smelting: Primary aluminum smelting consumes 13-15 MWh per metric ton. India’s average industrial electricity tariff of INR 6–8 per kWh creates a significant cost disadvantage versus smelters in regions with lower power costs, limiting India’s competitiveness in commodity-grade aluminum markets.

- Skill Gap in Advanced Metallurgy: India’s sector faces a shortage of qualified metallurgical engineers for advanced smelting and specialty metal processing. Talent availability constraints are particularly acute in titanium, nickel superalloys, and aerospace-grade aluminum quality certification.

Emerging Market Trends

.webp)

1. Aluminum Intensity in Green Building Construction

India’s Energy Conservation Building Code (ECBC) and the Bureau of Energy Efficiency’s star-rating program for commercial buildings are driving adoption of aluminum-intensive building envelopes. High-performance aluminum curtain walls, thermally broken window systems, and reflective roofing panels that improve building energy efficiency by 30–50% are seeing accelerated specification in commercial real estate across major metros.

2. Copper in EV Charging Infrastructure

India’s allocation of INR 2,000 crore under the PM E-DRIVE Scheme for the deployment of EV charging infrastructure nationwide is creating a new copper demand vector beyond traditional power distribution. Each DC fast-charging station requires 50–150 kg of copper for power electronics, cabling, and thermal management.

3. Zinc’s Critical Role in Anti-Corrosion Coatings for Infrastructure

India’s infrastructure durability imperative is driving hot-dip galvanizing adoption across bridge structures, transmission towers, and coastal construction. India's zinc consumption increased at a compound annual growth rate (CAGR) of 8.4% from 2021 to 2025, with infrastructure-related demand projected to sustain this trajectory through 2028.

4. Titanium Adoption in Aerospace and Defense

India’s Defense Acquisition Procedure 2020 and the defense offset policy, requiring 30–50% local content for defense contracts, are driving titanium demand for fighter aircraft, naval vessels, and aerospace structural components. Government-backed metallurgy research programs are creating import-substitution opportunities for India’s titanium sponge and alloy sector.

Industry Value Chain Analysis

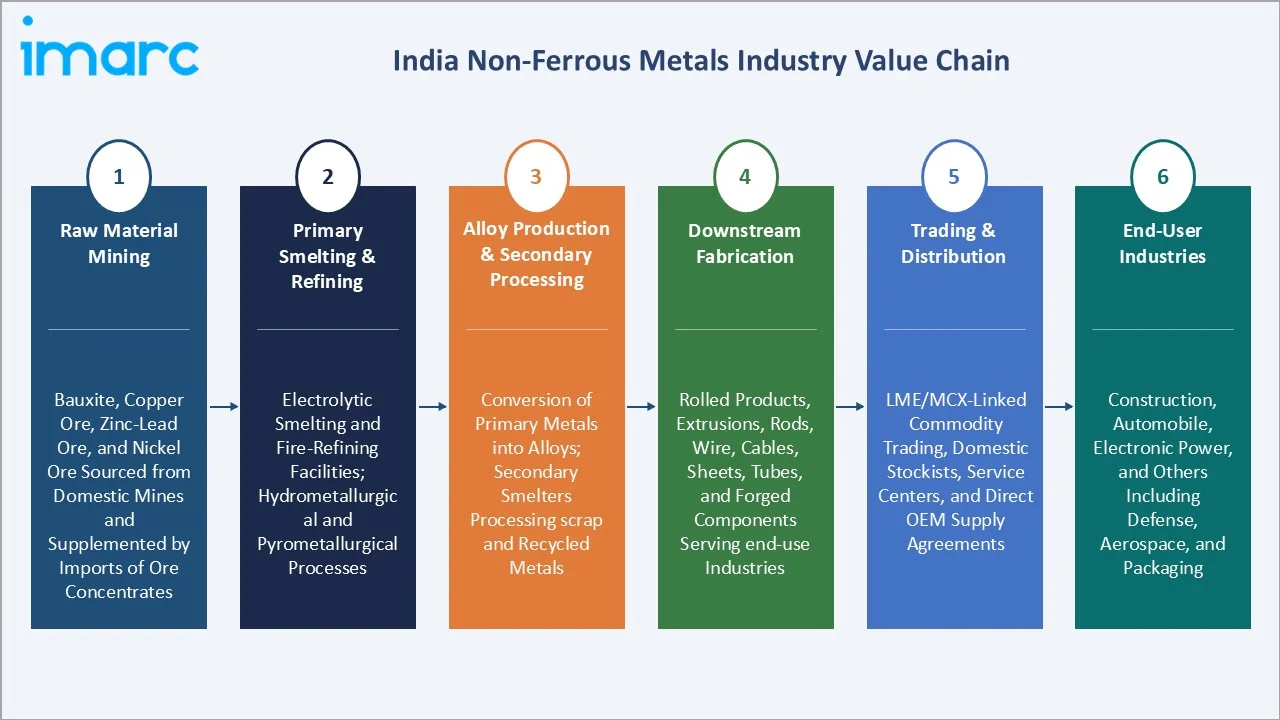

India’s non-ferrous metals value chain spans raw material mining through end-user fabricated product delivery, with each stage characterized by specific competitive dynamics and regulatory environments.

|

Stage |

Description |

|

Raw Material Mining |

Bauxite, copper ore, zinc-lead ore, and nickel ore are sourced from domestic mines and supplemented by imports of ore concentrates. |

|

Primary Smelting & Refining |

Electrolytic smelting and fire-refining facilities convert ore concentrates into primary metal; hydrometallurgical and pyrometallurgical processes. |

|

Alloy Production & Secondary Processing |

Conversion of primary metals into alloys (aluminum alloys, brass, bronze); secondary smelters processing scrap and recycled metals |

|

Downstream Fabrication |

Rolled products, extrusions, rods, wire, cables, sheets, tubes, and forged components serving end-use industries |

|

Trading & Distribution |

LME/MCX-linked commodity trading, domestic stockists, service centers, and direct OEM supply agreements |

|

End-User Industries |

Construction, automobile, electronic power, and others, including defense, aerospace, and packaging |

Technology Landscape in the India Non-Ferrous Metals Industry

Hall-Héroult Electrolytic Aluminum Smelting

Aluminum smelting in India employs the Hall-Héroult electrolysis process, converting alumina to primary aluminum at temperatures exceeding 960 degrees Celsius. India’s most advanced Point Feeder Prebaked (PFPB) anode smelting cells achieve a specific energy consumption of approximately 13-14 kWh per kg of aluminum. New 325 kA cell technology represents the industry’s advancement toward lower-emission, energy-efficient primary production.

Continuous Cast and Roll (CCR) Technology for Copper Rod

Continuous Cast and Roll (CCR) technology is used for copper rod production, producing 8–25 mm rods with consistent electrical conductivity exceeding 100% IACS. CCR achieves 25-50% lower energy consumption versus batch casting and enables real-time quality control through electromagnetic stirring and online surface inspection.

Imperial Smelting Furnace (ISF) and Hydrometallurgical Zinc Processing

India’s integrated zinc-lead smelting complexes combine Imperial Smelting Furnace (ISF) technology for lead-zinc co-production with SHG (Special High Grade) zinc refining through electrolysis. Advanced hydrometallurgical facilities achieve zinc recovery rates exceeding 95%, significantly above the global industry average of 90–92%, through advanced leaching and solvent extraction circuits.

Secondary Aluminum Recycling Technology

India’s secondary aluminum sector is adopting tilt rotary furnaces (TRFs) and oxygen-enriched combustion systems that reduce melting energy consumption by 20–30% versus conventional reverberatory furnaces. Advanced dross processing and fume extraction systems improve metallic recovery from 80–85% to 92–95%, enhancing the economics of scrap-based production.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Aluminum |

41.8% |

2025 |

|

Application |

Construction Industry |

36.4% |

2025 |

|

Region |

West and Central India |

38.2% |

2025 |

By Type

Aluminum dominates the type segment with a 41.8% share in 2025, representing the largest sub-market within India’s non-ferrous metals ecosystem. This dominance reflects aluminum’s broad applicability across construction (structural sections, window frames, roofing), transportation (automotive panels, rail wagons, aircraft structures), packaging (beverage cans, pharmaceutical foil), and power (overhead transmission conductors, busbars).

To access detailed market analysis, Request Sample

Copper, at 24.6%, is the second-largest segment and the fastest-growing among base metals, driven by its indispensable role in EV wiring harnesses, renewable energy systems, and power distribution networks. India’s structural copper deficit makes this the market’s most import-sensitive segment.

By Application

The construction industry commands a 36.4% share in 2025. Aluminum extrusions for facades, windows, and curtain walls, copper wiring for buildings, zinc-coated steel for structural applications, and lead sheets for waterproofing collectively drive sustained metal demand aligned with India’s urbanization trajectory.

.webp)

The automobile industry at 28.7% is the second-largest and fastest-growing application segment, reflecting India’s position as the world’s third-largest automobile market. Each passenger vehicle contains 20-25 kg of aluminum while consuming 14-15 kg of aluminum for every two-wheeler.

Regional Market Insights

West and Central India’s market leadership (38.2%, 2025) reflects the region’s concentration of primary smelting and refining facilities, established metal trading infrastructure, and the largest automotive and construction demand clusters in the country.

|

Region |

Share (2025) |

Key Growth Drivers |

|

West & Central India |

38.2% |

Dominant smelting and refining base, large automotive and construction demand cluster, and established metal trading infrastructure |

|

North India |

26.5% |

Significant zinc-lead operations, power sector copper demand, Delhi NCR construction activity, and government infrastructure investment in major states |

|

South India |

22.4% |

Strong copper demand from electronics and IT hardware manufacturing, the automotive components cluster, and the emerging data center infrastructure |

|

East & Northeast India |

12.9% |

Primary bauxite and copper mining operations, alumina refining capacity, and emerging industrial corridors with government infrastructure investment |

South India, at 22.4%, is experiencing accelerating non-ferrous metals demand, driven by Bengaluru’s electronics manufacturing ecosystem, Tamil Nadu’s established automotive components cluster, and Andhra Pradesh’s emerging industrial corridors. Data center expansion in Hyderabad, requiring copper for power distribution and aluminum for cooling infrastructure, represents a distinct emerging demand vector.

Competitive Landscape

India’s non-ferrous metals market exhibits moderate-to-high concentration, with the top five domestic producers collectively accounting for approximately 65–70% of primary metal production value in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Aditya Birla Management Corporation Pvt. Ltd. |

Eternia, Everlast Structurals, Freshpakk, Freshwrapp, Superwrap |

Market Leader |

Vertically integrated aluminum and copper; the largest Indian non-ferrous company by revenue; global downstream presence through Novelis |

|

Vedanta Limited |

Sterlite Copper, Vedanta Nico, Vedanta Zinc International, Hindustan Zinc, Vedanta Aluminium |

Market Leader |

Diversified metals portfolio; lowest-cost aluminum production; largest zinc producer through Hindustan Zinc subsidiary |

|

NALCO India |

NALCO |

Strong Challenger |

Government Navratna enterprise; integrated bauxite-to-aluminum operations; captive coal and power; Angul complex |

|

Hindustan Copper Ltd. |

HCL (HINDCOPPER) |

Challenger |

Government enterprise; India's only vertically integrated copper producer; copper cathodes, rods, and downstream products |

|

Maan Aluminium Ltd. |

Maan |

Challenger |

India's largest manufacturer and exporter of aluminum extruded profiles, comprising approximately 50% of the country's exports; in-house anodizing and fabrication facilities |

With India being a crucial consumer of non-ferrous metals, especially aluminum, copper, and zinc, the market is also witnessing an influx of investments in production capacity, green technology, and recycling initiatives.

Key Company Profiles

Aditya Birla Management Corporation Pvt. Ltd.

Aditya Birla Management Corporation Pvt. Ltd operates Hindalco Industries Ltd., the largest non-ferrous metals producer in India by consolidated revenue. The company operates across aluminum and copper verticals.

- Product Portfolio: Eternia (aluminium windows/doors), Everlast Structurals (aluminium roofing/structural), Freshpakk (foil containers), Superwrap and Freshwrapp (kitchen foil).

- Recent Developments: In January 2026, Hindalco Industries Ltd. announced a INR 21,000 crore expansion of its aluminum smelter capacity at the Aditya Aluminum complex in Odisha and commissioned new flat‑rolled products (FRP) and battery‑grade aluminum foil facilities.

- Strategic Focus: Value-added aluminum products for EV lightweighting; Novelis automotive body sheet expansion in Europe and North America; green aluminum initiatives targeting 50% renewable energy by 2030 for smelting operations.

Vedanta Limited

Vedanta Limited, headquartered in Mumbai, is India’s most diversified natural resources conglomerate, with significant non-ferrous metals operations spanning zinc-lead-silver and copper. Vedanta’s Jharsuguda aluminum smelter in Odisha is India’s largest single-location smelter.

- Product Portfolio: Sterlite Copper (copper business unit), Vedanta Nico (nickel/cobalt division under Sterlite Copper), Hindustan Zinc (zinc-lead-silver), Vedanta Aluminium (aluminum division), and Zinc International (Vedanta's international zinc operations).

- Recent Developments: In May 2026, Vedanta Limited’s complex completed its demerger, leading to the creation of four new standalone business entities, including Vedanta Aluminium Metal, which is expected to seek stock exchange approvals and begin trading by mid‑June 2026.

- Strategic Focus: Aluminum downstream integration through wire rod and extrusion capacity expansion; Hindustan Zinc’s production doubling plan to 2 million tons with INR 30,000–35,000 Crore investment; operational restart of copper refining capacity.

NALCO India

NALCO India, headquartered in Bhubaneswar, Odisha, is a Navratna public sector enterprise under the Ministry of Mines. NALCO operates India’s largest integrated bauxite mining, alumina refining, and primary aluminum smelting complex, with a coal-based power plant at Angul, Odisha.

- Product Portfolio: Calcined alumina, primary aluminum ingots, billets, wire rods, and rolled products; aluminum fluoride by-products; captive power generation for smelting operations.

- Recent Developments: For 2025-26, NALCO India recorded a 77 lakh ton bauxite excavation and strong growth across alumina, aluminum, and power segments. Aluminum smelting reached a new milestone, with cast metal production hitting 4.72 lakh tons during the financial year.

- Strategic Focus: Alumina refinery capacity expansion from 2.275 million to 3.275 million tons per annum; captive solar power procurement to reduce energy costs; downstream value-added product development for packaging and transportation applications.

Market Concentration Analysis

India’s non-ferrous metals market exhibits moderate-to-high concentration at the primary production level. The zinc market is highly concentrated, while aluminum is moderately concentrated across multiple producers, and copper exhibits the highest import dependency with less concentrated domestic production.

Consolidation at the secondary processing and downstream fabrication levels is occurring through backward integration by large users. Automotive component manufacturers and cable manufacturers are securing long-term supply agreements with primary producers to reduce raw material price exposure and improve supply chain resilience.

Investment & Growth Opportunities

Fastest Growing Segments

Copper for EV and renewable energy applications (~5.4% CAGR), aluminum for green building construction (~5.2% CAGR), battery-grade specialty metals including nickel and cobalt (~8–10% CAGR), and titanium for aerospace and defense (~7% CAGR) represent the highest-growth investment vectors through 2034.

Emerging Market Expansion

Tier-2 and Tier-3 industrial cities including Hosur (automotive), Aurangabad (auto ancillaries), Coimbatore (engineering), and Rajpura (cables) collectively represent an incremental USD 3–4 Billion non-ferrous metals consumption opportunity beyond established metro markets by 2034.

Venture and Institutional Investment Trends

- The government PLI scheme for advanced chemistry cell batteries represents a USD 2.5 Billion incentive pool driving nickel, cobalt, manganese, and lithium processing investments, with companies establishing battery materials supply chains eligible for 18–20% production-linked incentives on incremental domestic sales over five years.

- India’s National Mineral Policy amendments provide composite licenses combining prospecting and mining rights, reducing exploration-to-production timelines from 8–12 years to 5–7 years, improving the economics of greenfield bauxite, copper, and zinc mining projects.

- Green aluminum premiums are emerging as automotive OEMs and FMCG companies commit to low-carbon aluminum procurement, enabling producers with renewable power-sourced smelters to command USD 50–150 per ton premiums over standard LME-linked pricing.

Future Market Outlook (2026-2034)

India’s non-ferrous metals market is positioned for sustained, above-GDP-growth expansion through 2034. From a base of USD 40.72 Billion in 2025, the market is projected to reach USD 62.97 Billion by 2034, representing total incremental value creation of USD 22.25 Billion at a CAGR of 4.81%. This growth is structurally underpinned by India’s irreversible urbanization trajectory and government infrastructure capital expenditure commitments.

The technology transition from fossil-fuel-intensive smelting to renewable energy-powered production will define the market’s sustainability profile by 2034. Producers achieving 50%+ renewable energy in their smelting operations by 2030 will command green metal premiums and gain preferential export access in regions where carbon border adjustment mechanisms will penalize high-emission primary metal imports from 2026 onward.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 130 industry participants in 2024–2025, including mining operators, primary smelters, downstream fabricators, commodity traders, automotive OEM procurement heads, and institutional investors across India, Europe, and Southeast Asia.

Secondary Research

Secondary research encompassed company annual reports, Ministry of Mines annual reports, DGFT import-export data for non-ferrous metals (HS Codes 74, 75, 76, 78, 79, 80), LME/MCX price data, Bureau of Indian Standards specifications, and industry publications including Metal Bulletin, Mining Weekly, and CRU Group reports.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating metal consumption per sector (kg/unit of construction area, kg/vehicle, kg/MW of power capacity), sector output forecasts, domestic production plus net import data, and vendor revenue disclosures. A base-case CAGR of 4.81% reflects consensus estimates validated against announced production expansion pipelines and downstream demand indicators from FY 2020 to FY 2025.

India Non-Ferrous Metals Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Aluminum, Copper, Lead, Tin, Nickel, Titanium, Zinc, Others |

| Applications Covered | Automobile Industry, Electronic Power Industry, Construction Industry, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Aditya Birla Management Corporation Pvt. Ltd., Vedanta Limited, NALCO India, Hindustan Copper Ltd., Maan Aluminium Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India non-ferrous metals market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India non-ferrous metals market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India non-ferrous metals industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Non-Ferrous Metals Market Report

The India non-ferrous metals market reached USD 40.72 Billion in 2025 and is projected to reach USD 62.97 Billion by 2034.

The market is expected to grow at a CAGR of 4.81% during 2026-2034, driven by infrastructure expansion, EV adoption, and renewable energy deployment requiring aluminum and copper.

West and Central India leads with a 38.2% share in 2025, anchored by major smelting and refining infrastructure, Gujarat’s copper processing ecosystem, and Maharashtra’s large automotive and construction demand base.

Aluminum dominates with a 41.8% share in 2025, encompassing primary ingots, extrusions, flat-rolled products, and conductor-grade aluminum for power transmission.

The construction industry holds the largest share at 36.4%, driven by India’s urban housing deficit, commercial real estate expansion, and government-funded infrastructure projects.

Key players include Aditya Birla Management Corporation Pvt. Ltd., Vedanta Limited, NALCO India, Hindustan Copper Ltd., and Maan Aluminium Ltd.

Copper is growing at approximately 5.4% CAGR because EV adoption, renewable energy grid expansion, and data center growth are collectively driving a step-change increase in copper intensity per unit of economic output.

Key challenges include high energy costs for aluminum smelting, dependence on imported copper ore, LME price volatility, tightening environmental regulations on smelting emissions, and competition from growing secondary metal recycling supply.

Copper smelting capacity (to reduce the annual import deficit), battery-grade metal processing for India’s EV supply chain, green aluminum with renewable energy, titanium for aerospace and defense, and downstream fabrication for export markets represent the highest-growth investment opportunities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)