India Nutraceuticals Market Size, Share, Trends and Forecast by Product, Indication, and Region, 2026-2034

India Nutraceuticals Market Size, Share, Trends & Forecast (2026-2034)

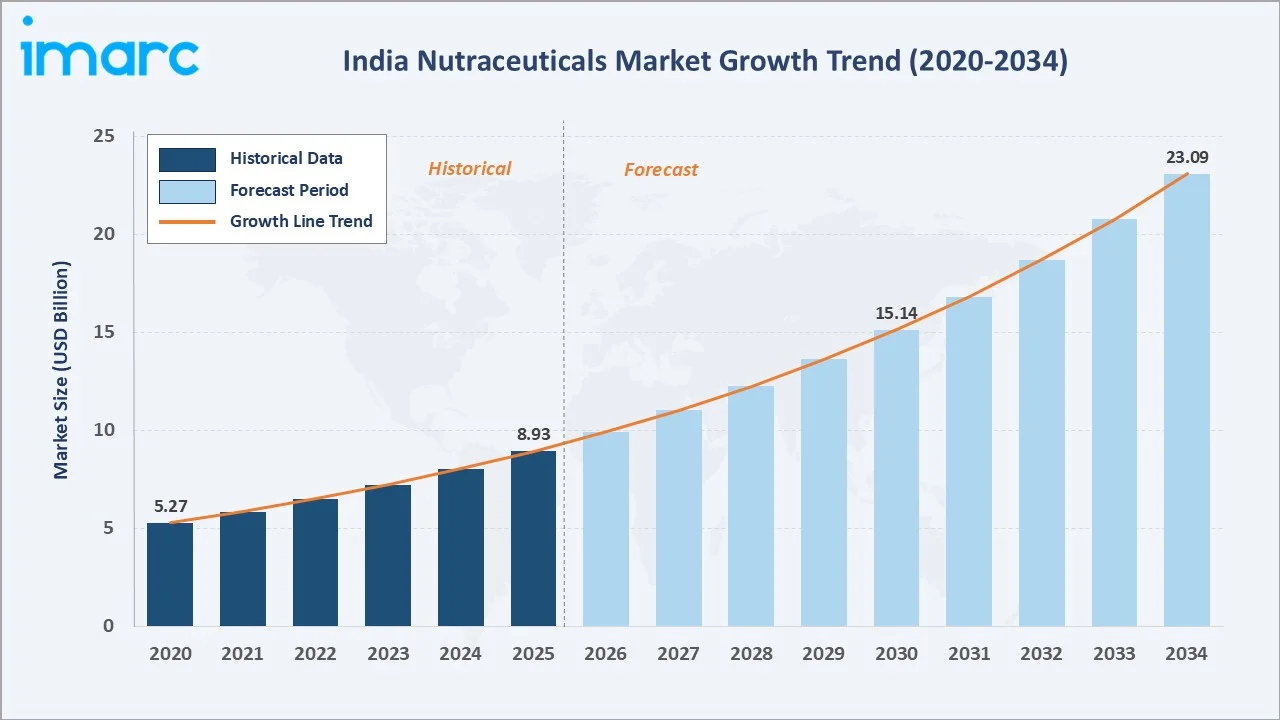

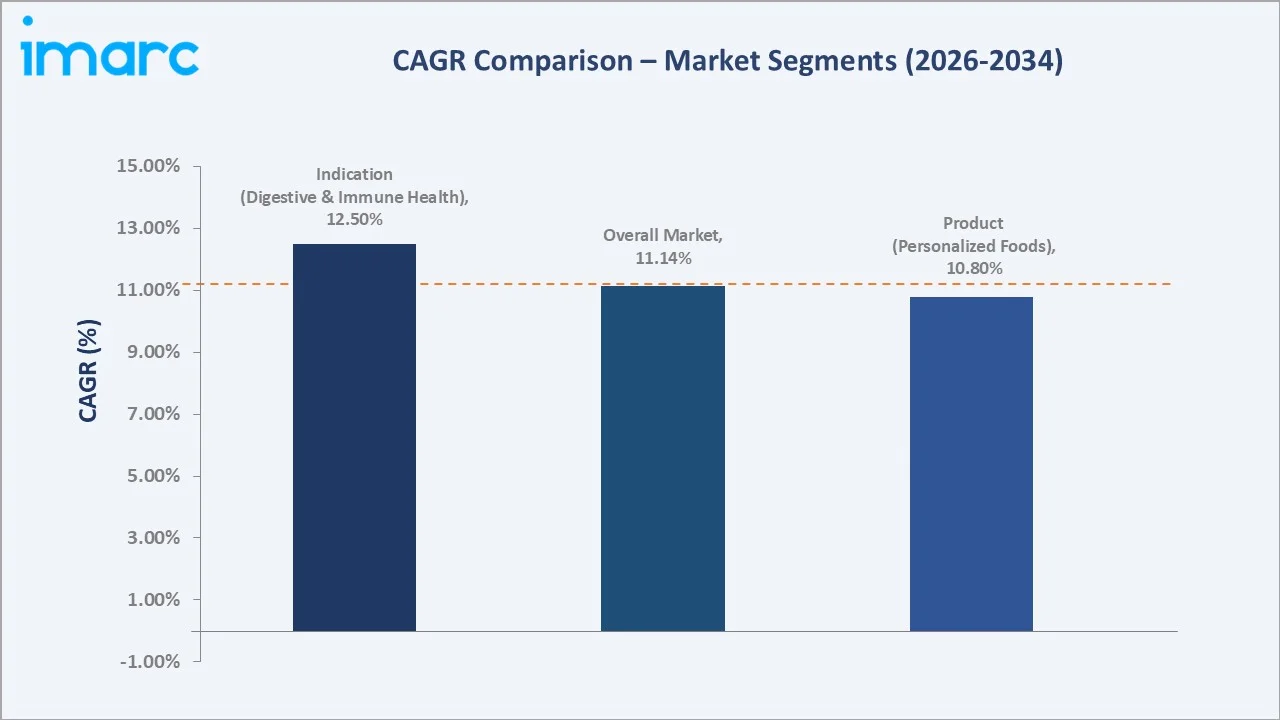

The India nutraceuticals market reached USD 8.93 Billion in 2025 and is projected to reach USD 23.09 Billion by 2034, growing at a CAGR of 11.14% during 2026-2034. Rising health consciousness, increasing adoption of preventive healthcare approaches, growing demand for personalized nutrition, and expanding e-commerce distribution channels are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.93 Billion |

|

Forecast Market Size (2034) |

USD 23.09 Billion |

|

CAGR (2026-2034) |

11.14% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (35.0% share, 2025) |

|

Fastest Growing Region |

South India |

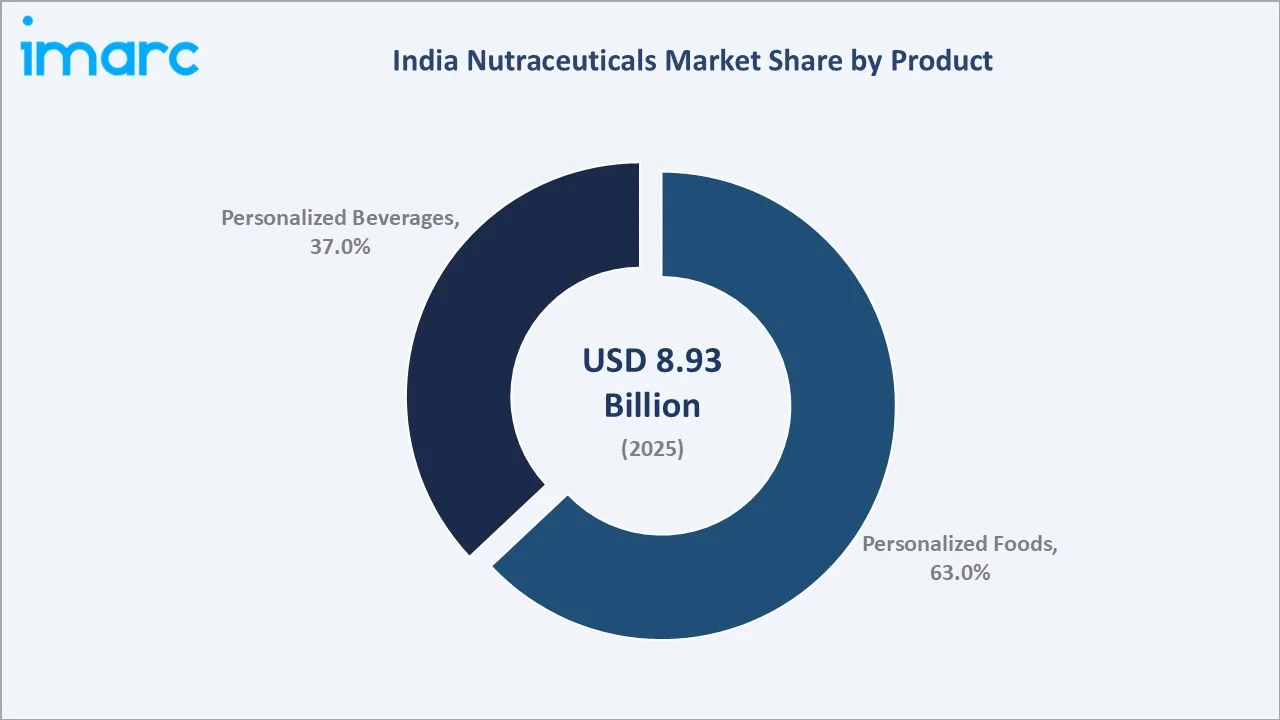

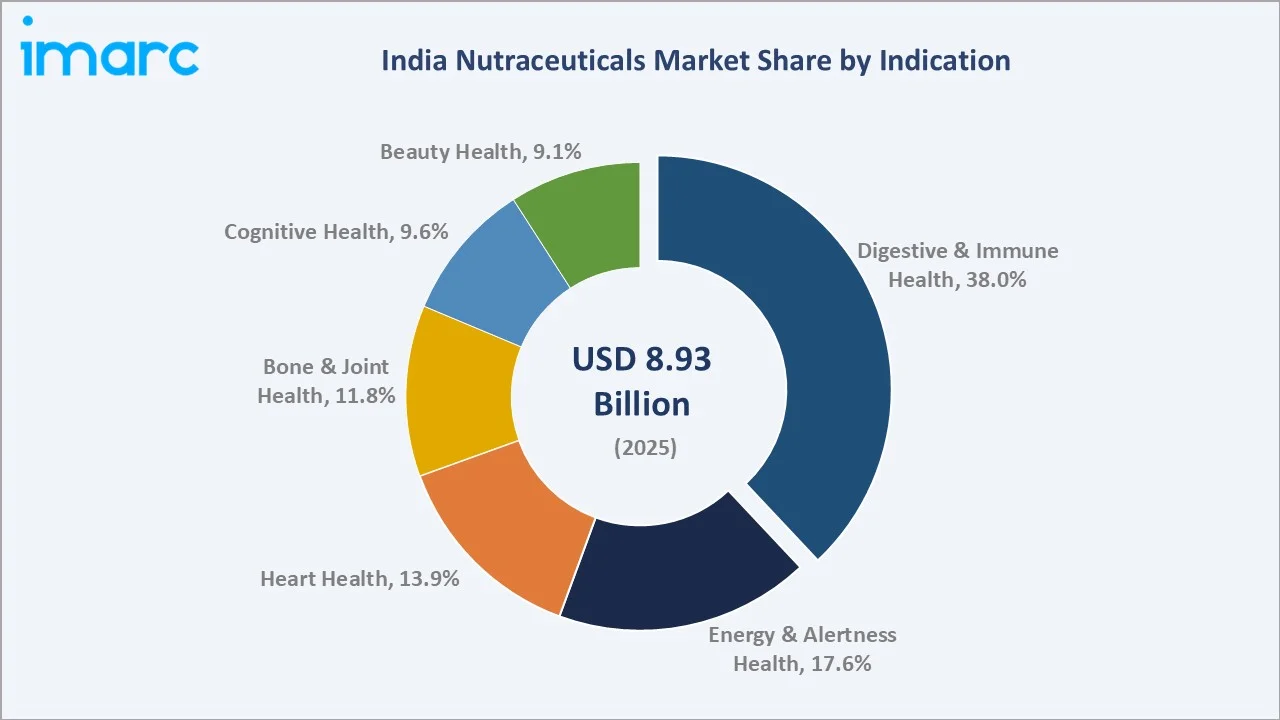

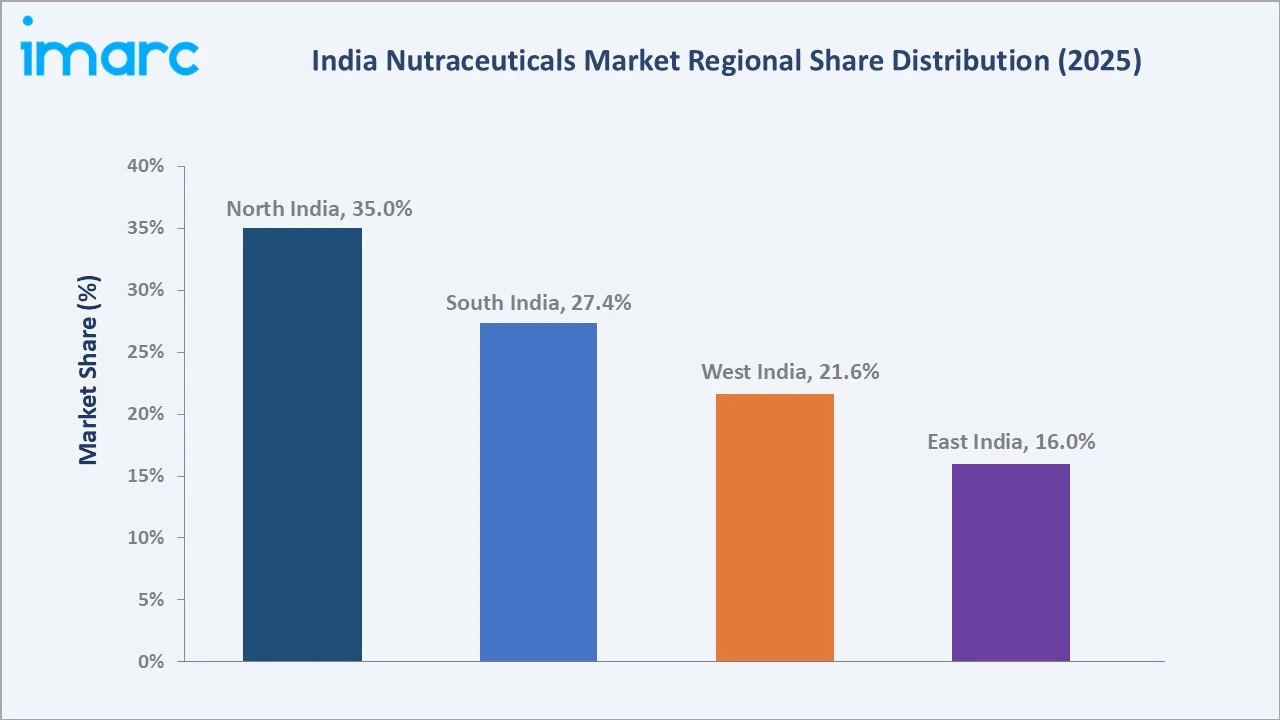

North India dominates, holding a 35.0% market share in 2025, while personalized foods lead product demand at 63.0%. Digestive and immune health remains the dominant indication segment with a 38.0% share. India's nutraceuticals industry offers tremendous advantages, including an extensive base of traditional Ayurvedic knowledge, a rapidly growing health-conscious middle class, and a supportive regulatory framework under the Food Safety and Standards Authority of India (FSSAI), creating a highly conducive environment for both domestic and international nutraceutical enterprises.

To get more information on this market, Request Sample

With applications spanning digestive health, cardiovascular wellness, cognitive performance, beauty nutrition, and bone and joint support, the market is expected to continue expanding at an accelerated pace, supported by technological advancements in personalized nutrition science, increasing digital health awareness, and the integration of artificial intelligence in supplement formulation across India's rapidly evolving nutraceutical ecosystem.

Executive Summary

The India nutraceuticals market is on an accelerated growth trajectory, driven by a fundamental paradigm shift from reactive medical treatment to proactive preventive healthcare across the Indian consumer landscape. The market reached USD 8.93 Billion in 2025 and is forecast to reach USD 23.09 Billion by 2034, reflecting a robust CAGR of 11.14% over the forecast period, one of the fastest growth rates among major nutraceutical markets globally.

North India commands the largest regional share at 35.0% in 2025, driven by high population density, concentration of urban health-conscious consumers, and superior retail and e-commerce infrastructure. South India represents the fastest-growing regional opportunity, with tech-savvy urban populations in Bengaluru, Hyderabad, and Chennai increasingly adopting science-backed nutraceutical solutions.

Personalized foods dominate the product category at 63.0%, while digestive and immune health lead indication demand at 38.0%. Leading players, including Amway Corp., Dabur India Limited, Himalaya Wellness Company, Abbott, and Herbalife International of America, Inc., are investing in Ayurveda-modern science integration and personalized nutrition technology.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Product) |

Personalized Foods – 63.0% share (2025) |

|

Largest Segment (Indication) |

Digestive and Immune Health – 38.0% share (2025) |

|

Leading Region |

North India – 35.0% revenue share (2025) |

|

Fastest Growing Region |

South India (digital-first health adoption) |

|

Top Companies |

Amway Corp., Dabur India Limited, Himalaya Wellness Company, Abbott, and Herbalife International of America, Inc. |

|

Market Opportunity |

Personalized nutrition and AI-driven supplement formulation |

Key Analytical Observations Supporting The Above Data:

- Personalized foods account for 63.0% of India's nutraceuticals market in 2025, driven by growing consumer preference for nutrition tailored to individual health objectives, dietary requirements, and lifestyle choices. Fortified cereals, protein-enriched snacks, and functional dairy products with added vitamins and probiotics are gaining widespread acceptance.

- Digestive and immune health is the dominant indication segment at 38.0% (2025), reflecting heightened consumer awareness about the gut microbiome's impact on overall wellness. The rising incidence of digestive disorders and post-pandemic immunity focus are propelling demand for probiotics, prebiotics, and herbal formulations.

- North India holds 35.0% of the Indian nutraceuticals market in 2025, attributed to high population density, increasing access to health products, strong cultural acceptance of traditional therapeutic systems, and concentration of metropolitan areas with health-conscious urban consumers.

- South India is the fastest-growing region, driven by tech-savvy urban populations in Bengaluru, Hyderabad, and Chennai who are early adopters of digital health platforms, personalized nutrition services, and premium nutraceutical brands.

India Nutraceuticals Market Overview

The India nutraceuticals market encompasses a broad spectrum of products that bridge the gap between conventional food and pharmaceutical medicines. Nutraceuticals, including functional foods, dietary supplements, herbal and botanical products, and fortified beverages, are consumed for their physiological and health benefits beyond basic nutritional needs.

The macroeconomic backdrop is highly favorable. India's GDP growth, rising urban household incomes, and expanding digital infrastructure are collectively enabling greater consumer investment in health and wellness products. As of March 2025, approximately 5.8 million Indians lose their lives annually to non-communicable diseases (NCDs), with approximately one in four Indians at risk of dying from NCDs before age 70, creating demand for preventive nutraceutical interventions.

Market Dynamics

To evaluate market opportunities, Request Sample

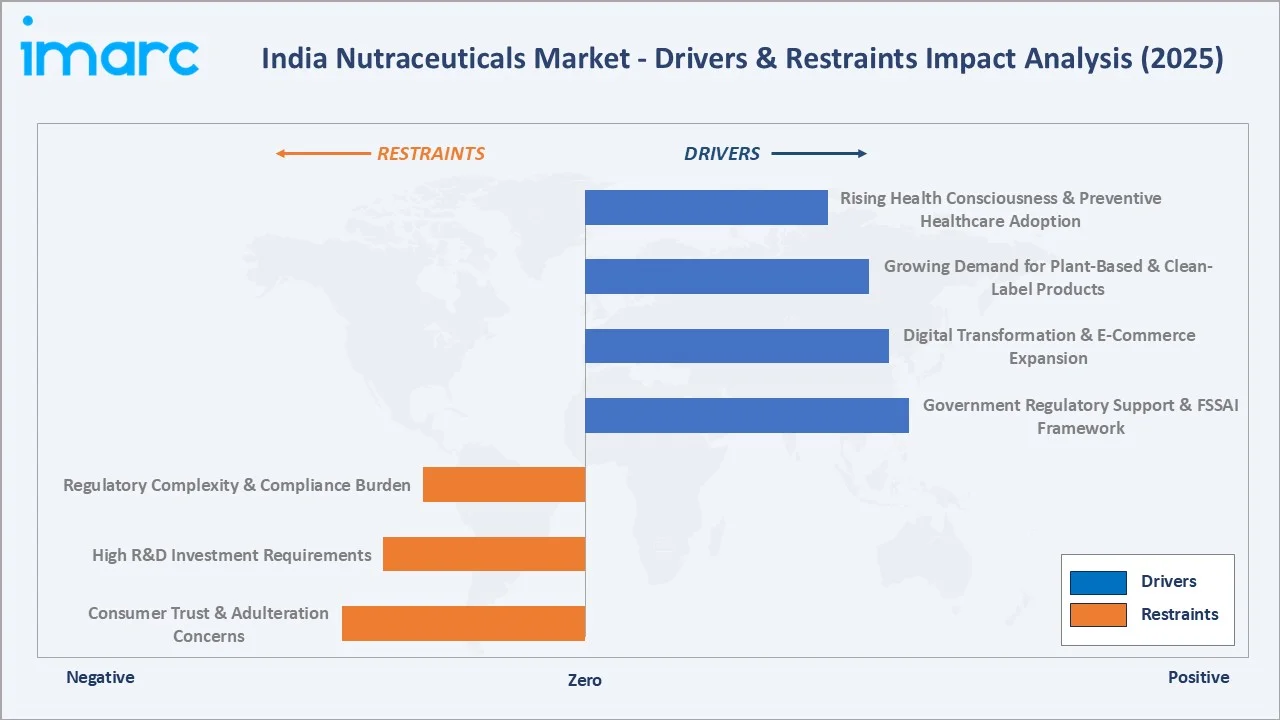

Market Drivers

- Rising Health Consciousness and Preventive Healthcare Adoption: The Indian preventive healthcare sector is estimated at USD 197 billion in 2025, growing at a CAGR of 22%. The rising prevalence of lifestyle diseases is compelling a broader consumer base to adopt nutraceuticals as preventive and supplementary health solutions, creating sustained structural demand across all product categories.

- Growing Demand for Plant-Based and Clean-Label Products: India had the largest proportion of vegans at 9% of its population in 2025. The integration of indigenous botanicals, ashwagandha, turmeric, moringa, brahmi, and amla, into modern supplement formulations reflects evolving consumer expectations for natural, culturally resonant wellness solutions.

- Digital Transformation and E-Commerce Expansion: The India e-commerce market reached USD 129.72 Billion in 2025. Direct-to-consumer (D2C) brands leverage social media marketing, influencer partnerships, and personalized recommendation algorithms to connect with younger demographics in semi-urban and rural areas.

- Government Regulatory Support and FSSAI Framework: The National Nutritional Strategy and supportive FDI policies allowing 100% foreign direct investment in nutraceutical manufacturing have attracted global players and accelerated technology transfer and product innovation across the market.

Market Restraints

- Regulatory Complexity and Compliance Burden: Compliance with FSSAI product approval processes, labeling requirements, and health claim substantiation standards imposes significant time-to-market delays and compliance costs, particularly for smaller domestic producers and new market entrants seeking regulatory approvals.

- High R&D Investment Requirements: Developing clinically validated, science-backed nutraceutical formulations requires substantial investment in research, clinical trials, and quality assurance infrastructure.

- Consumer Trust and Adulteration Concerns: Incidents of adulteration and quality inconsistency in some segments of India's supplement market have undermined consumer confidence, particularly in online channels.

Market Opportunities

- Personalized Nutrition Solutions and AI Integration: Advances in nutritional genomics, microbiome analysis, and artificial intelligence are enabling the development of hyper-personalized nutraceutical formulations. Personalized nutrition platforms leveraging wearable health data, genetic testing, and AI-driven recommendation engines represent a multi-billion-dollar emerging opportunity.

- Rural Market Penetration via Digital Channels: India's rural population of over 900 million represents a largely untapped market for nutraceuticals. Expanding digital infrastructure, smartphone penetration, and regional-language e-commerce platforms are progressively enabling access to health products in Tier 2, Tier 3, and rural markets.

- Export Market Development and Global Positioning: India is positioned to become a global hub for nutraceutical manufacturing and export, leveraging cost-competitive manufacturing, extensive botanical biodiversity, and Ayurveda's growing international credibility.

Market Challenges

- Quality Inconsistency and Adulteration Risk: The fragmented nature of India's nutraceutical supply chain, involving large numbers of small-scale botanical ingredient suppliers, creates persistent quality inconsistency risks. Ensuring standardized potency, purity, and efficacy across complex herbal formulations requires investment in analytical testing infrastructure that many manufacturers lack.

- Price Sensitivity and Affordability Barriers: Despite growing health consciousness, price sensitivity remains a significant constraint on nutraceutical adoption among India's mass-market consumer segments. Premium-positioned imported supplements face affordability barriers, while domestic brands must balance quality improvement investment against competitive retail price points accessible to India's predominantly value-conscious consumer base.

Emerging Market Trends

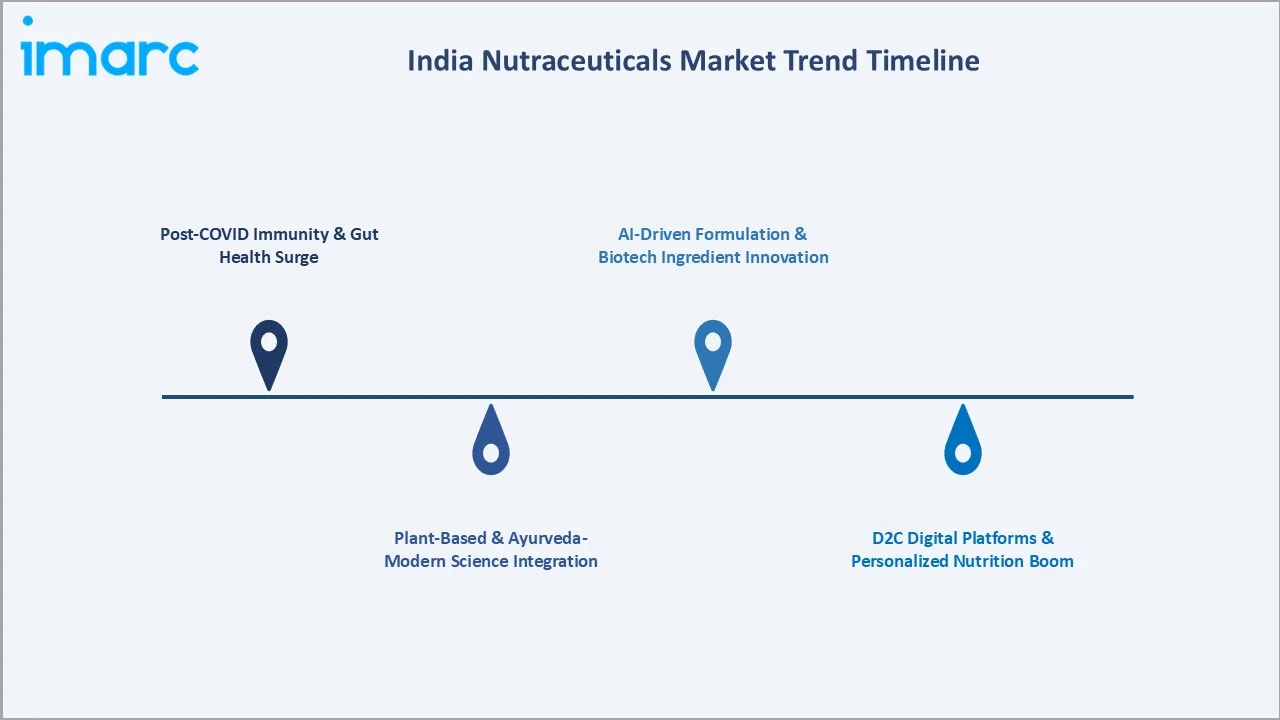

1. Post-COVID Immunity and Gut Health Surge

In 2025, Amway India expanded its immunity-focused range with the launch of Nutrilite Triple Protect, a plant-based supplement delivering 100% RDA of Vitamin C supporting immune, gut, and skin health. Probiotics, elderberry extracts, zinc supplements, and vitamin D formulations have transitioned from specialty health store products to mass-market daily supplements, fundamentally reshaping category volumes.

2. Plant-Based and Ayurveda-Modern Science Integration

In January 2025, Amway India announced active exploration of entering the Ayurveda segment, planning products integrating local traditional herbs within 2-3 years. Companies are investing in clinically substantiated ashwagandha, turmeric, moringa, and brahmi-based formulations targeting stress management, cognitive health, and metabolic wellness, products that resonate deeply with India's culturally embedded herbal wellness tradition.

3. D2C Digital Platforms and Personalized Nutrition Boom

In June 2025, Dabur India launched Siens by Dabur, a premium D2C nutraceutical brand targeting beauty, gut health, and daily wellness through digital-first channels. Mobile health applications, subscription-based supplement services, and AI-driven personalization algorithms are creating new consumption patterns particularly resonant with India's urban Millennial and Gen Z demographics.

4. AI-Driven Formulation and Biotech Ingredient Innovation

In April 2026, Herbalife India collaborated with IIT Madras to launch the Plant Cell Fermentation Technology Lab in Chennai, a CSR-driven initiative developing sustainable, high-quality herbal raw materials for nutraceuticals, bridging demand-supply gaps and aligning with India's bio-manufacturing strategic goals.

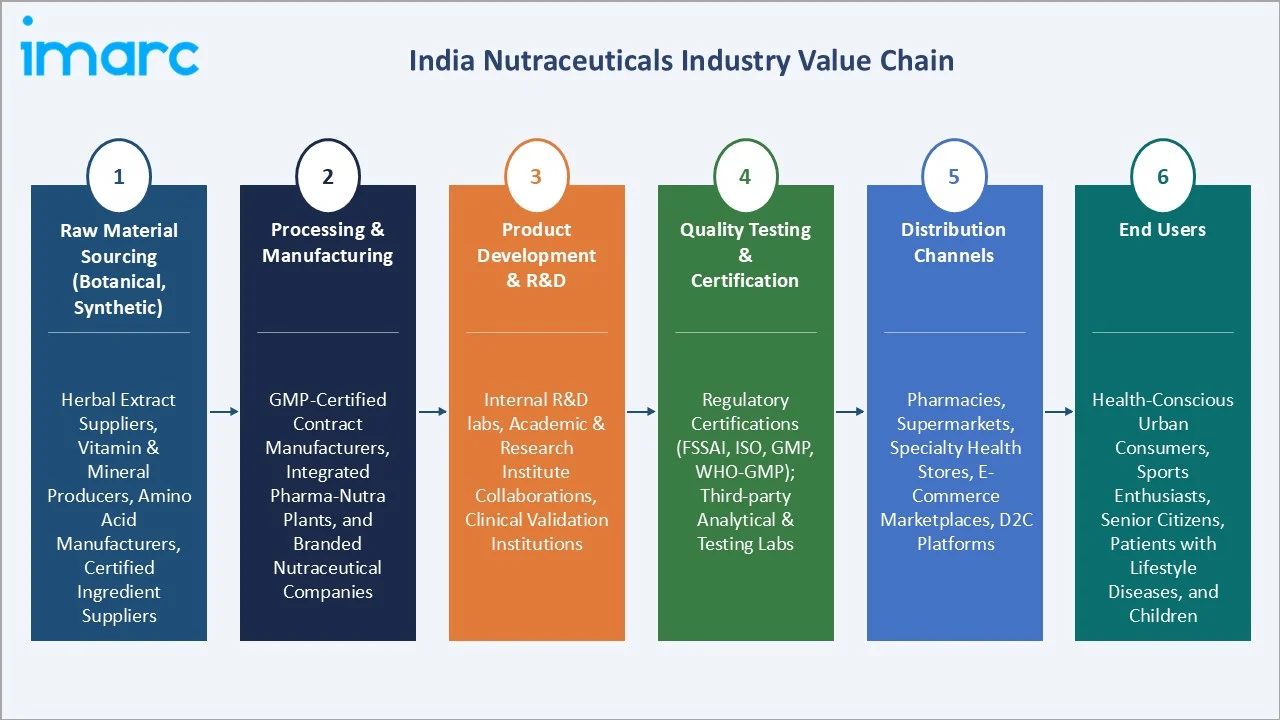

Industry Value Chain Analysis

The India nutraceuticals value chain spans raw botanical and ingredient sourcing through clinical validation, manufacturing, quality certification, multi-channel distribution, and final consumer delivery, each stage populated by specialized operators whose quality performance and regulatory compliance directly influence product efficacy and market credibility.

|

Stage |

Key Players / Examples |

|

Raw Material Sourcing (Botanical, Synthetic) |

Herbal extract suppliers, vitamin & mineral producers, amino acid manufacturers, certified ingredient suppliers |

|

Processing & Manufacturing |

GMP-certified contract manufacturers, integrated pharma-nutra plants, and branded nutraceutical companies. |

|

Product Development & R&D |

Internal R&D labs, academic & research institute collaborations, clinical validation institutions |

|

Quality Testing & Certification |

Regulatory certifications (FSSAI, ISO, GMP, WHO-GMP); third-party analytical & testing labs |

|

Distribution Channels |

Pharmacies, supermarkets, specialty health stores, e-commerce marketplaces, D2C platforms |

|

End Users |

Health-conscious urban consumers, sports enthusiasts, senior citizens, patients with lifestyle diseases, and children |

Technology Landscape in the India Nutraceuticals Industry

Precision Fermentation and Biotechnology-Enabled Ingredients

Herbalife India's collaboration with IIT Madras on a Plant Cell Fermentation Technology Lab (February 2025) exemplifies this trend, targeting sustainable herbal raw material production for large-scale nutraceutical manufacturing aligned with India's bio-manufacturing policy framework.

AI-Powered Personalized Nutrition Platforms

Indian start-ups and established players alike are developing mobile-first personalization platforms that translate individual health assessments into tailored nutraceutical protocols, a convergence of digital health technology and nutritional science that is reshaping consumer engagement and product development across the industry.

Advanced Delivery Systems and Novel Formulation Technology

Gummies, effervescent tablets, ready-to-drink (RTD) formats, nano-encapsulated bioactive compounds, and liposomal delivery systems are gaining significant market traction. These technologies enhance bioavailability, consumer compliance, and product differentiation in an increasingly competitive market landscape.

Blockchain-Based Supply Chain Traceability and Authentication

Given concerns about adulteration and quality inconsistency in India's nutraceutical supply chain, blockchain-based ingredient traceability systems are gaining adoption among premium market players. These platforms enable consumers to verify ingredient origins, quality certifications, and manufacturing provenance from farm to finished product.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product | Personalized Foods | 63.0% | 2025 |

| Indication | Digestive and Immune Health | 38.0% | 2025 |

| Region | North India | 35.0% | 2025 |

By Product

Personalized foods dominate the product segment with a 63.0% share in 2025. This dominance reflects the strong consumer preference for nutrition aligned with individual health objectives and lifestyle choices. Fortified cereals, protein-enriched snacks, functional dairy products enriched with vitamins and probiotics, and specialty bakery products with added health benefits are gaining widespread acceptance across India's urban consumer base.

To access detailed market analysis, Request Sample

Personalized beverages hold the remaining 37.0% share, driven by strong demand for protein shakes, meal replacement beverages, functional energy drinks, fortified juices, and probiotic drinks. The beverages segment is the fastest-growing sub-category, benefiting from the convenience consumption preferences of India's younger urban demographic and the rapid expansion of health-focused beverage brands across digital and modern trade channels.

By Indication

Digestive and immune health leads the indication demand at 38.0% in 2025. This dominance reflects heightened post-pandemic awareness about the gut microbiome's central role in systemic immunity, metabolic health, and mental wellness. Rising incidence of irritable bowel syndrome (IBS), food intolerances, and chronic gut inflammation is propelling demand for probiotics, prebiotics, digestive enzymes, and specialized herbal formulations across India.

Energy and alertness health holds 17.6%, growing rapidly among India's fitness enthusiasts, working professionals, and student population. Heart health commands 13.9%, driven by rising cardiovascular disease prevalence. Bone and joint health accounts for 11.8%, reflecting growing arthritis incidence and aging population demand.

Regional Market Insights

North India's market leadership (35.0%, 2025) reflects high population density, increasing access to health products through both traditional and digital retail channels, strong cultural acceptance of the traditional therapeutic system, and concentration of major metropolitan areas such as Delhi NCR, Chandigarh, Lucknow, and Jaipur.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

35.0% |

High urban density, cultural acceptance of Ayurveda, and strong modern trade infrastructure |

|

South India |

27.4% |

Tech-savvy consumers, D2C digital adoption, high literacy, and health awareness |

|

West India |

21.6% |

Mumbai-Pune financial hub, sports nutrition demand, and premium segment preference |

|

East India |

16.0% |

Growing middle class, Kolkata metro expansion, and traditional medicine awareness |

South India is the fastest-growing region, with Bengaluru's technology sector creating a large base of health-conscious, high-income professionals willing to invest in premium nutraceutical products. The region's high literacy rates, strong digital adoption, and concentration of pharmaceutical and biotechnology companies create a particularly fertile environment for nutraceutical innovation and premium brand adoption.

Competitive Landscape

The India nutraceuticals market exhibits a moderately competitive structure, with multinational corporations competing alongside strong domestic players and emerging D2C brands. The top five players, Amway India, Dabur India, Himalaya Wellness, Abbott India, and Herbalife International India, collectively account for approximately 40–45% of total market revenue in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Amway Corp. |

Nutrilite |

Market Leader |

Global direct-selling leader; science-backed Nutrilite brand; plant-sourced supplements with phytonutrient concentrates |

|

Dabur India Limited |

Dabur Chyawanprash, Siens by Dabur |

Market Leader |

India's largest Ayurvedic FMCG; 120+ country distribution; June 2025 D2C nutra brand launch (Siens) |

|

Himalaya Wellness Company |

Himalaya Liv.52, Quista, Evecare, Himalaya Pure Herbs range |

Strong Challenger |

Bengaluru-based Ayurveda pioneer; extensive R&D-backed herbal formulations; global export presence |

|

Abbott |

Ensure, PediaSure, Similac |

Strong Challenger |

International clinical nutrition expertise; infant and medical nutrition leadership; rigorous R&D standards |

|

Herbalife International of America, Inc. |

Herbalife |

Strong Challenger |

Operating in India as Herbalife International India Pvt. Ltd., Global wellness brand; IIT Madras plant cell fermentation lab partnership (Feb 2025); direct selling model |

Domestic Ayurveda-focused companies, including Patanjali Ayurved and Baidyanath, along with pharmaceutical companies diversifying into nutraceuticals, account for a significant additional share.

Key Company Profiles

Amway Corp.

Amway Corp. (Ada, Michigan, USA) is one of the leading direct-selling nutraceutical companies. Operating through the globally recognized Nutrilite brand, Amway India delivers science-backed nutritional products from plant-based raw materials grown on Amway-owned Nutrilite farms worldwide.

- Product Portfolio: Full-spectrum nutritional supplements including protein powders, multivitamins, herbal supplements, immunity boosters, and skincare nutrition under the Nutrilite brand.

- Recent Developments: In November 2025, Amway India launched Nutrilite Vitamin D Plus Boron, a scientifically designed supplement combining Vitamin D3, Boron, Vitamin K2, Quercetin, and Licorice to support optimal Vitamin D levels, bone strength, and immune health amid widespread deficiency concerns in India.

- Strategic Focus: Expanding science-backed Ayurveda product line; growing digital sales channel; deepening rural market penetration through direct selling model; integrating traditional Indian herbs with Nutrilite's plant-based nutrition science.

Dabur India Limited

Dabur India Limited, founded in 1884 and headquartered in Ghaziabad, is one of India's largest Ayurvedic fast-moving consumer goods (FMCG) companies. Dabur's nutraceutical portfolio spans immunity boosters, digestive health products, herbal formulations, and a rapidly expanding modern supplement range catering to urban health-conscious consumers.

- Product Portfolio: Chyawanprash, herbal digestive formulations, immunity boosters, Real fruit juices with functional ingredients, and Siens by Dabur featuring marine collagen, multivitamin gummies, omega-3 softgels, and probiotic supplements.

- Recent Developments: In June 2025, Dabur India launched Siens by Dabur, a premium digital‑first nutraceutical brand offering science‑backed supplements across beauty, daily wellness, and gut health categories.

- Strategic Focus: D2C digital expansion via Siens brand; premium nutraceutical segment entry targeting urban millennials; global export growth (products available in 120+ countries); integrating modern nutritional science with Ayurvedic heritage.

Himalaya Wellness Company

Himalaya Wellness Company, headquartered in Bengaluru and founded in 1930, is a pioneer in herbal healthcare products that leverages Ayurveda for a broad range of nutraceutical and pharmaceutical offerings.

- Product Portfolio: Liv. 52 (liver health), Himalaya Protein supplements, Himalaya Ashwagandha, Himalaya Chyavanaprasha, herbal digestive and immunity formulations; broad pharma-nutra range spanning multiple therapeutic categories.

- Recent Developments: In November 2025, Himalaya Wellness partnered with Unicommerce, India’s e‑commerce enablement SaaS platform, to integrate and automate its online and offline operations using the Uniware system, aiming to accelerate omnichannel expansion.

- Strategic Focus: D2C growth and digital platform development; global export expansion; advanced R&D in herbal-clinical science integration; entering premium nutraceutical segments with evidence-backed botanical formulations.

Market Concentration Analysis

The India nutraceuticals market exhibits moderate concentration at the branded product level. The top five players, Amway Corp., Dabur India Limited, Himalaya Wellness Company, Abbott, and Herbalife International of America, Inc., account for approximately 40–45% of total market revenue in 2025. A long tail of regional Ayurvedic manufacturers, contract supplement producers, pharmacy private labels, and emerging D2C brands accounts for the remaining balance, ensuring substantial market fragmentation below the top tier.

Consolidation is accelerating, driven by the capital intensity of clinical validation requirements, FSSAI compliance investments, and the digital infrastructure needed to compete in India's rapidly growing e-commerce and D2C nutraceutical segments. Pharmaceutical companies, including Sun Pharmaceutical Industries, Cipla Health, and Zydus Wellness, are aggressively diversifying into nutraceuticals, further intensifying competitive dynamics at the premium branded segment level.

Investment & Growth Opportunities

Fastest Growing Segments

Personalized nutrition platforms (estimated CAGR approximately 18%), AI-driven supplement formulation technology, cognitive health nutraceuticals (approximately 15% CAGR), and biotech-enabled herbal ingredient manufacturing represent the four highest-growth investment vectors through 2034. Together, these niches address a combined total addressable market exceeding USD 4.5 Billion by 2034 within the broader India nutraceuticals ecosystem.

Emerging Market Expansion

Rural India's vast and underserved population of over 900 million, combined with rapidly expanding digital infrastructure and Tier 2/Tier 3 city middle-class growth, collectively represents the largest structural expansion opportunity for nutraceutical market participants. Companies that develop affordable, trusted, culturally resonant products and leverage India's digital public infrastructure for distribution are positioned to capture significant incremental volumes.

Venture and Institutional Investment Trends

- Personalized nutrition genomics platforms combining genetic testing, microbiome analysis, and AI-driven supplement protocol generation.

- D2C nutraceutical brands targeting urban Millennial and Gen Z health consumers with science-backed, clean-label formulations in innovative delivery formats.

- Contract nutraceutical manufacturing platforms catering to the rapidly growing global private-label supplement market with GMP-certified, export-ready production.

- Ayurveda modernization start-ups are developing clinically validated, standardized botanical extracts meeting international regulatory requirements for global market access.

Future Market Outlook (2026-2034)

The India nutraceuticals market is positioned for exceptional, broad-based growth through 2034. From a base of USD 8.93 Billion in 2025, the market is projected to reach USD 23.09 Billion by 2034, representing total incremental value creation of approximately USD 14.16 Billion over the forecast decade at a CAGR of 11.14%.

Three structural macro-themes will define India's nutraceutical trajectory through 2034: the accelerating transition from reactive to preventive healthcare; the digital revolution in health consumer behavior (enabling D2C, personalization, and data-driven product development at scale); and the global rise of Ayurveda and traditional botanical wellness.

Regulatory evolution, particularly FSSAI's progressive strengthening of nutraceutical standards, potential pharmaceutical-nutraceutical convergence frameworks, and emerging personalized nutrition regulations, will drive significant industry professionalization. Companies that invest early in clinical validation, digital infrastructure, and supply chain traceability are positioned to capture disproportionate share as India's nutraceuticals market approaches maturity through the 2030-2034 period.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and consultations with over 130 industry stakeholders in 2024-2025, including nutraceutical manufacturers, pharmaceutical companies diversifying into supplements, Ayurvedic product producers, e-commerce platform representatives, retail pharmacists, regulatory consultants, and health professionals across North, South, West, and East India.

Secondary Research

Secondary research encompassed a systematic review of FSSAI regulatory documentation, IMARC Group proprietary databases, company annual reports and investor presentations, Ministry of Health and Family Welfare data, NFHS survey data, National Nutritional Strategy documentation, industry publications, and publicly available market transaction data.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating India's macroeconomic indicators (GDP growth, urban household income growth, digital penetration rates), disease burden statistics (NCD prevalence trends), consumption pattern analysis, and regulatory environment evolution.

India Nutraceuticals Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered |

|

| Indications Covered | Digestive and Immune Health, Energy and Alertness Health, Heart Health, Bone and Joint, Cognitive Health, Beauty Health |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Amway Corp., Dabur India Limited, Himalaya Wellness Company, Abbott, Herbalife International of America, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Nutraceuticals Market Report

The India nutraceuticals market reached USD 8.93 Billion in 2025 and is projected to reach USD 23.09 Billion by 2034, growing at a CAGR of 11.14% during the forecast period 2026-2034.

The India nutraceuticals market is projected to grow at a CAGR of 11.14% during the forecast period 2026-2034, driven by rising health consciousness, preventive healthcare adoption, expanding e-commerce distribution, and growing demand for personalized nutrition solutions.

North India dominates the India nutraceuticals market with a 35.0% revenue share in 2025, attributed to high population density, strong cultural acceptance of traditional therapeutic systems, and concentration of metropolitan areas with health-conscious urban consumers. South India is the fastest-growing region.

Personalized foods are the dominant product segment with a 63.0% share in 2025, driven by growing consumer preference for nutrition tailored to individual health objectives, dietary requirements, and lifestyle choices, including fortified cereals, protein-enriched snacks, and functional dairy products.

Digestive and immune health is the dominant indication segment at 38.0% in 2025, reflecting heightened awareness about the gut microbiome's impact on overall wellness and sustained post-pandemic demand for probiotics, prebiotics, and immune-supporting herbal formulations.

Key players in the India nutraceuticals market include Amway Corp., Dabur India Limited, Himalaya Wellness Company, Abbott, and Herbalife International of America, Inc.

The India e-commerce market reached USD 129.72 Billion in 2025, with health and wellness products among the fastest-growing categories. D2C brands, digital subscription models, and personalized recommendation platforms are enabling access to nutraceuticals across semi-urban and rural markets previously underserved by conventional retail infrastructure.

Key challenges include regulatory complexity and evolving FSSAI compliance requirements, consumer trust concerns arising from adulteration incidents in some market segments, high R&D investment requirements for clinical validation, and quality inconsistency across fragmented botanical ingredient supply chains.

Key investment opportunities include personalized nutrition genomics platforms, AI-driven supplement formulation technology, D2C nutraceutical brands targeting urban Millennial consumers, GMP-certified contract manufacturing for global private-label markets, and rural market expansion through digital public infrastructure and affordable product development.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)