India Office Furniture Market Size, Share, Trends and Forecast by Product Type, Material Type, Distribution Channel, Price Range, and Region, 2026-2034

India Office Furniture Market Summary:

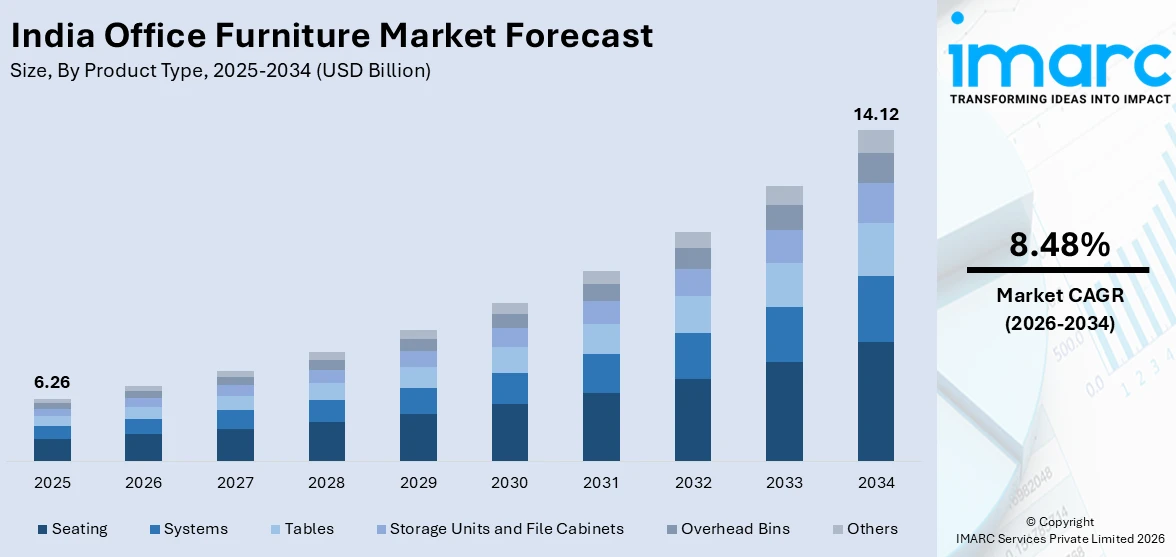

The India office furniture market size was valued at USD 6.26 Billion in 2025 and is projected to reach USD 14.12 Billion by 2034, growing at a compound annual growth rate of 8.48% from 2026-2034.

The India office furniture market is witnessing robust expansion, driven by evolving workplace dynamics, rapid urbanization, and rising corporate investments in employee-centric environments. Increasing adoption of hybrid work models, growing emphasis on ergonomic solutions, and the proliferation of co-working spaces are reshaping demand for modern, adaptable, and sustainable office furniture across commercial and institutional sectors nationwide, reflecting the broader trajectory of India's economic transformation and the India office furniture market share.

Key Takeaways and Insights:

- By Product Type: Seating dominates the market with a share of 38.0% in 2025, owing to the growing emphasis on employee wellness and ergonomic workspace solutions. Rising corporate investments in adjustable, comfort-oriented seating reflect evolving workplace standards and improved productivity outcomes.

- By Material Type: Wood leads the market with a share of 41.0% in 2025, driven by its aesthetic versatility, cultural resonance, and suitability for diverse office environments. Its wide adaptability across contemporary and traditional interior designs supports consistent and diversified demand.

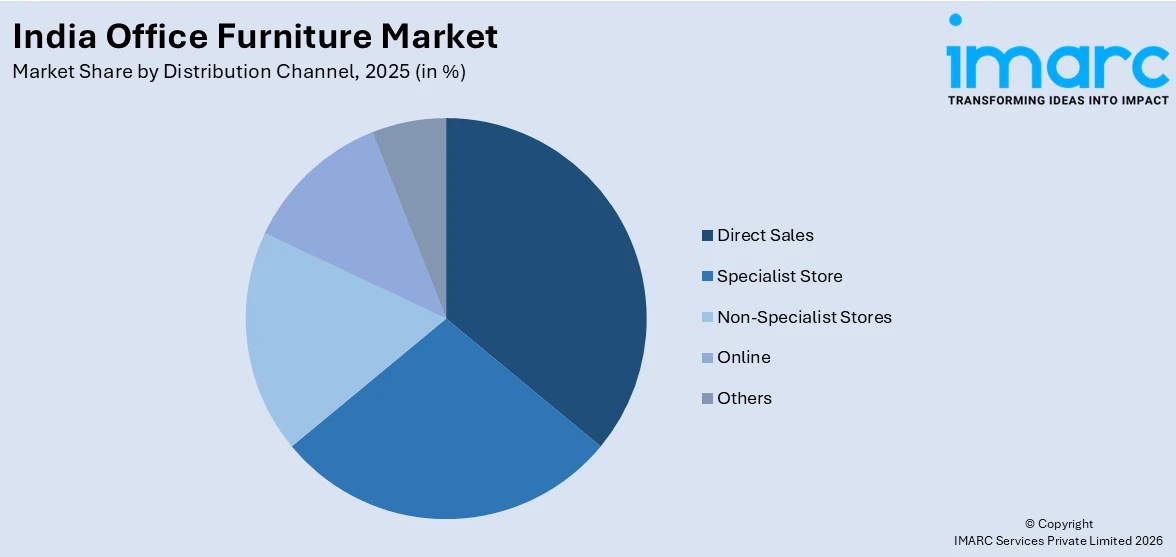

- By Distribution Channel: Direct sales hold the largest segment with a share of 36.0% in 2025, reflecting the sector's project-based procurement model and enterprises' preference for single-window delivery encompassing design consultation, installation, and post-sale support services.

- By Price Range: Medium exhibits a clear dominance in the market with 49.0% share in 2025, balancing quality and affordability for a broad range of corporate buyers, including SMEs and expanding startups seeking functional yet cost-effective workspace solutions.

- By Region: West and Central India represents the largest region with 34.0% share in 2025, driven by the concentration of major commercial hubs, IT corridors, and financial districts in cities such as Mumbai, Pune, and Ahmedabad.

- Key Players: Key players drive the India office furniture market by expanding product portfolios, developing ergonomic and sustainable designs, and strengthening nationwide distribution networks. Their strategic investments in workspace innovation, customization capabilities, and partnerships with corporate clients accelerate adoption and ensure consistent product availability across diverse buyer segments.

To get more information on this market Request Sample

The India office furniture market is influenced by a combination of factors related to corporate growth, infrastructure development, and changing philosophies of work. Companies across various industries are now increasingly focusing on providing a high level of comfort and productivity in the work environment, which in turn creates a consistent demand for office furniture. Additionally, the shift in office furniture demand towards open offices and workspaces is also impacting the market. At the same time, the development of global capability centers and multinational corporate campuses is fueling the demand for high-end office furniture. Initiatives taken by the Indian government, including the Smart Cities Mission and the Make in India initiative, are contributing positively to the development of commercial infrastructure and motivating companies to manufacture in the country, which in turn creates a positive impact on the India office furniture market share in all regions.

India Office Furniture Market Trends:

Rise of Ergonomic and Employee-Centric Workspace Design

The increasing awareness about the relationship between workplace comfort and employee productivity is influencing furniture procurement decisions across India. Organizations in corporate, IT, and service sectors are gradually moving away from traditional rigid office setups and adopting ergonomic seating, adjustable workstations, and supportive accessories that help reduce physical strain during long working hours. This transition is further supported by workplace wellness initiatives that emphasize the importance of a comfortable and supportive work environment. As a result, ergonomics is becoming an important consideration in the evolving demand for modern office furniture solutions in India.

Modular and Flexible Furniture for Hybrid Workspaces

India's corporate sector is rapidly embracing hybrid work models that necessitate dynamic, reconfigurable office layouts, spurring strong demand for modular furniture systems, including mobile desks, foldable partitions, and lightweight storage units. Co-working space operators are at the forefront of this transition, curating interiors that cater to varying occupancy patterns throughout the week. The demand for versatile furniture solutions that maximize space utilization is defining a new standard in Indian office design. Grade-A office leasing exceeded 70 Million sq. ft in 2024, reflecting the scale of commercial space expansion underpinning demand for modular furniture configurations.

Sustainability and Eco-Conscious Manufacturing Practices

Indian businesses and international corporations operating in India are increasingly aligning office furniture procurement with environmental, social, and governance objectives, driving demand for furniture manufactured from sustainably sourced wood, recycled materials, and low-VOC finishes. The growing adoption of green building certifications issued by the Indian Green Building Council is compelling real estate developers and occupants to prioritize eco-certified workspace products. In February 2025, India's DPIIT issued a Furniture Quality Control Order mandating ISI certification for major furniture categories, a regulatory development that is accelerating the shift toward compliant, quality-assured manufacturing within the domestic industry.

Market Outlook 2026-2034:

The office furniture market in India is set for a period of sustained and robust growth, with a number of macroeconomic factors, urbanization, and changing office dynamics all contributing to a positive outlook for the market. The ongoing expansion of commercial real estate, particularly in tier 1 cities and newly emerging technology hubs, continues to provide a significant level of procurement opportunity for office furniture. The alignment of government policy, particularly with regard to infrastructure development and domestic manufacturing incentives, is further enhancing the production landscape, thereby providing a competitive environment. The ongoing and growing adoption of smart office technology, combined with increased awareness of office ergonomics, and the continued expansion of India's startup and information technology industries, are all set to ensure a sustained period of growth for the market. The market generated a revenue of USD 6.26 Billion in 2025 and is projected to reach a revenue of USD 14.12 Billion by 2034, growing at a compound annual growth rate of 8.48% from 2026-2034.

India Office Furniture Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product Type |

Seating |

38.0% |

|

Material Type |

Wood |

41.0% |

|

Distribution Channel |

Direct Sales |

36.0% |

|

Price Range |

Medium |

49.0% |

|

Region |

West and Central India |

34.0% |

Product Type Insights:

- Seating

- Systems

- Tables

- Storage Units and File Cabinets

- Overhead Bins

- Others

Seating dominates with a market share of 38.0% of the total India office furniture market in 2025.

Seating is the leading category of the India office furniture market, and it is driven by fundamental and ongoing need for corporate establishments of all sizes. The category includes a broad array of products, from task chairs with ergonomic designs to visitor chairs, conference chairs, and collaborative soft seating, each of which is designed for specific purposes in the office of today. The widespread adoption of open office and activity-based office concepts has further fueled interest in seating arrangements that facilitate movement, posture correction, and personal comfort. As organizations across industries invest in designing environments that are conducive for productivity, seating has become the primary point of expense for office outfitting, thus cementing its position as the leading category of the overall product landscape of the India office furniture market.

The preponderance of the seating segment is further validated by the fact that, unlike other office furniture, office chairs have a replacement cycle that lasts only a few years. This ensures that there is always a consistent and stable source of revenue. Moreover, with the increased adoption of international ergonomic standards and certification in India's corporate campuses, there has been an improvement in the quality expectations from office seating products. Both global and local players are actively expanding their office seating product offerings, including mesh-back, lumbar support, and posture-adaptive chairs, to meet the increasingly discerning needs of office buyers in India.

Material Type Insights:

- Wood

- Metal

- Plastic and Fiber

- Glass

- Others

Wood leads with a share of 41.0% of the total India office furniture market in 2025.

Wood retains an unassailable lead within the India office furniture material landscape, benefiting from deeply entrenched consumer preference, cultural affinity, and an unmatched capacity for aesthetic versatility. From premium executive desks and conference tables to modular storage solutions and partition systems, wooden furniture spans a wide spectrum of price points and design sensibilities. The material's inherent warmth and formality continue to resonate strongly with Indian corporate buyers who value professional interior aesthetics. Engineered wood variants, including medium-density fiberboard and plywood, have further democratized access to wood-based furniture by offering consistent quality at competitive price points, extending the material's reach to SMEs and budget-conscious organizations across the country.

The enduring dominance of wood in India's office furniture segment is also supported by a robust domestic supply chain and the growing availability of sustainably sourced timber and engineered wood alternatives. Furniture manufacturers are increasingly adopting low-emission adhesives, water-based lacquers, and certified wood inputs in response to corporate sustainability mandates and green building requirements. The versatility of wood in terms of finish options, customization potential, and compatibility with contemporary and traditional interior design schemes gives it a significant edge over competing materials. As compliance with quality control and environmental standards becomes more prominent in institutional procurement, the demand for certified wood-based office furniture is expected to remain a central pillar of market demand.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Direct Sales

- Specialist Store

- Non-Specialist Stores

- Online

- Others

Direct sales represent the leading segment with a 36.0% share of the total India office furniture market in 2025.

Direct sales constitute the predominant distribution mechanism for office furniture in India, reflecting the inherently project-oriented and relationship-driven nature of commercial procurement. Corporate buyers, particularly large enterprises, government institutions, and co-working operators, typically engage furniture suppliers directly to ensure comprehensive service coverage from space planning and product customization through to logistics, installation, and post-sale maintenance. This direct engagement model enables buyers to tailor purchases to specific workspace dimensions, aesthetic requirements, and budgetary constraints, resulting in higher order values and superior alignment with organizational needs. The ability to negotiate long-term annual rate contracts further incentivizes procurement managers to maintain direct relationships with established suppliers who can support multi-location rollouts consistently and efficiently.

The direct sales channel also benefits from the growing complexity of modern workspace procurement, which increasingly involves design consultancy, virtual reality layout planning, and integrated project management services best delivered through dedicated account teams rather than retail intermediaries. Furniture manufacturers and established market participants have invested substantially in direct sales infrastructure, including showrooms, dedicated project teams, and after-sales support capabilities, which reinforce their competitive advantage in large-scale corporate projects. The primacy of the direct channel is linked to the sector's emphasis on service credibility and brand assurance, particularly among multinational corporations and institutional buyers who prioritize vendor reliability, product consistency, and lifecycle support over immediate cost considerations in their procurement decisions.

Price Range Insights:

- Low

- Medium

- High

Medium exhibits a clear dominance with a 49.0% share of the total India office furniture market in 2025.

The medium price range commands the largest share of the India office furniture market, occupying the sweet spot between affordability and quality that appeals to the broadest segment of corporate buyers. This category serves the extensive mid-tier corporate landscape, encompassing technology companies, financial service firms, educational institutions, healthcare providers, and the rapidly expanding cohort of well-funded startups and small to medium enterprises seeking functional yet presentable workspace solutions. Medium-range furniture successfully delivers on key procurement priorities, including adequate ergonomic support, durable construction, aesthetic acceptability, and adherence to basic quality standards, without the cost premium associated with high-end executive or designer collections.

The sustained dominance of medium-priced office furniture reflects India's evolving corporate spending ethos, wherein organizations aim to balance employee welfare investments against fiscal discipline. This segment benefits from a wide variety of product offerings from both domestic manufacturers and international brands, creating a competitive environment that delivers high value to buyers. Furthermore, compliance with quality control orders and increasing standardization within this bracket is gradually squeezing out inferior products while elevating the overall quality benchmark for medium-range furniture. As more enterprises in tier-2 and tier-3 cities formalize their workspaces and transition from unorganized purchases to organized procurement, the medium segment is expected to sustain its leadership through the forecast period.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

West and Central India holds the largest region with a 34.0% share of the total India office furniture market in 2025.

The leading position is held by West and Central India, which comprises major economic centers like Mumbai, Pune, and Ahmedabad. These cities are major financial, industrial, and technology centers that provide a constant demand for modern office furniture from corporate houses. The developed market for commercial real estate in this region and the presence of multinational corporate campuses, capability centers, and co-working spaces ensure a constant demand for modern, ergonomic, and premium quality office furniture from various segments of buyers.

This region is also blessed with a developed manufacturing ecosystem that has a large number of furniture manufacturers, distribution centers, and design showrooms located across Gujarat and Maharashtra. The development of GIFT City as a financial services center in Gujarat and the rapid development of IT parks in cities like Navi Mumbai and Pune are creating a new market for modern office furniture. The investments being made in commercial real estate are also a major boost for this region.

Market Dynamics:

Growth Drivers:

Why is the India Office Furniture Market Growing?

Rapid Expansion of Corporate Offices and Co-working Spaces

India's business landscape is undergoing a profound structural transformation, characterized by the rapid multiplication of corporate office establishments, technology parks, and co-working facilities across major metropolitan areas and emerging tier-2 cities. The growth of the information technology and IT-enabled services sector, combined with the proliferation of startups and the influx of global capability centers established by multinational corporations, is generating unprecedented demand for modern and well-equipped office spaces. As organizations seek to attract and retain top talent in an increasingly competitive labor market, the quality and functionality of physical workspaces have become a critical differentiator in employer branding strategies. This has prompted substantial investments in ergonomic seating, modular workstation systems, and collaborative furniture configurations that align with contemporary workspace philosophies. Co-working space operators, who must balance aesthetic appeal, functional versatility, and cost efficiency across shared environments, represent a particularly active segment of furniture buyers. Their need for durable, adaptable, and visually cohesive furniture solutions has created a specialized demand stream that continues to grow alongside the broader flexible workspace movement in India.

Government Infrastructure Initiatives and Smart City Development

India's national and state governments have launched a series of wide-ranging infrastructure programs that are directly and indirectly stimulating demand for office furniture across commercial and public sector domains. The Smart Cities Mission, which focuses on urban infrastructure development across designated cities, has resulted in the construction and modernization of a significant number of commercial office buildings, government establishments, and public service facilities that require comprehensive furnishing. The Make in India initiative has additionally incentivized domestic manufacturing activity, leading to the establishment of new industrial facilities and business parks that generate additional workspace procurement needs. Infrastructure corridors and special economic zones developed under national programs continue to attract private investments and commercial tenants, resulting in fresh demand for organized workplace solutions. Public sector modernization drives, including digital governance initiatives and the expansion of government office networks into tier-2 and tier-3 cities, are also contributing to growing institutional procurement of quality office furniture, broadening the market's demand base beyond private corporate buyers.

Growing Emphasis on Employee Wellness and Ergonomic Design Standards

The increasing corporate recognition of the direct relationship between workspace quality, employee health, and organizational productivity is reshaping furniture procurement priorities across India's business landscape. Human resource and facilities management teams are now actively specifying ergonomic standards for new office fitouts, including lumbar-supported task chairs, height-adjustable desks, anti-fatigue accessories, and acoustically optimized workstations. This emphasis on ergonomics is being further reinforced by the adoption of occupational health and wellness frameworks within corporate sustainability reporting, making workspace quality a measurable organizational outcome. The intersection of hybrid work trends and ergonomic requirements has also prompted companies to invest in portable and adaptable furniture solutions that maintain comfort standards across different usage patterns and employee rotation schedules. International workspace design standards and green building certification systems that include ergonomic requirements are gaining traction among premium commercial real estate developers and corporate occupants in India, elevating the minimum acceptable specification for office furniture and driving long-term demand growth across seating, desking, and workstation categories.

Market Restraints:

What Challenges the India Office Furniture Market is Facing?

High Raw Material Price Volatility

Fluctuations in the cost of wood, metal, and polymer inputs significantly disrupt operational planning for office furniture manufacturers in India. Rising timber prices, driven by limited sustainable forestry capacity and increasing regulatory compliance requirements, compress profit margins and force price adjustments that challenge manufacturers' competitiveness. Steel and aluminum price movements further add to cost unpredictability, making it difficult for suppliers to maintain stable pricing commitments across long-duration project contracts, particularly in government and institutional procurement channels where fixed-price agreements are standard practice. This volatility limits manufacturers' ability to plan production capacity and invest in product innovation consistently.

Intense Competition from the Unorganized Sector

The India office furniture market continues to face intense pricing pressure from a large and fragmented unorganized sector comprising small workshops and local fabricators. These informal producers operate at significantly lower cost structures by bypassing quality certifications, tax compliance requirements, and formal labor standards, allowing them to underprice organized manufacturers by a considerable margin. While government measures such as quality control orders and GST enforcement are gradually narrowing the competitive gap, the unorganized sector retains a dominant presence in cost-sensitive market segments, creating persistent headwinds for branded, organized players seeking to maintain premium positioning and expand their market share across diverse buyer segments.

Limited Market Penetration in Tier-2 and Tier-3 Cities

Despite rapid urbanization, organized office furniture manufacturers face significant challenges in extending their commercial reach into India's vast network of tier-2 and tier-3 cities, where awareness of branded products, distribution infrastructure, and after-sales service capabilities remain underdeveloped. Corporate buyers in smaller cities frequently default to locally fabricated solutions that offer immediate availability at lower prices. Establishing robust sales networks, installation teams, and customization capabilities in these geographies requires substantial investment and time, creating a meaningful barrier that limits the addressable market for premium and mid-range furniture brands pursuing nationwide expansion strategies.

Competitive Landscape:

The competitive scenario of the India office furniture market comprises a mix of domestic manufacturers with a strong presence in the country, international brands with a subsidiary presence in the country, and the unorganized sector. Companies differentiate themselves in terms of product innovations, ergonomic design expertise, green manufacturing practices, and project management services. International brands bring in international design expertise and high-tech material technology, whereas domestic players have an edge in terms of market understanding, distribution network, and scale of operations. The use of digital technology and virtual showrooms in office furniture is changing the face of customer engagement models. Companies are looking at product portfolio development, collaborations, and acquisitions as new factors in changing the competitive scenario in the industry. The implementation of quality control norms would eventually shift the balance of power in favor of organized players with quality certifications.

India Office Furniture Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Seating, Systems, Tables, Storage Units and File Cabinets, Overhead Bins, Others |

| Material Types Covered | Wood, Metal, Plastic and Fiber, Glass, Others |

| Distribution Channels Covered | Direct Sales, Specialist Store, Non-Specialist Stores, Online, Others |

| Price Ranges Covered | Low, Medium, High |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Office Furniture Market Report

The India office furniture market size was valued at USD 6.26 Billion in 2025.

The India office furniture market is expected to grow at a compound annual growth rate of 8.48% from 2026-2034 to reach USD 14.12 Billion by 2034.

Seating dominated the market with a share of 38.0%, driven by widespread corporate investment in ergonomic and wellness-oriented seating solutions that enhance employee comfort, productivity, and adherence to evolving workplace health and safety standards.

Key factors driving the India office furniture market include rapid corporate office expansion, growing co-working space proliferation, rising ergonomic awareness, government infrastructure initiatives, and increasing demand for sustainable and modular workspace solutions.

Major challenges include high raw material price volatility, intense competition from the unorganized sector, limited penetration in tier-2 and tier-3 cities, and the ongoing difficulty of maintaining consistent quality standards across a fragmented and geographically dispersed supply chain.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)