India Offshore Wind Turbine Market Size, Share, Trends and Forecast by Location of Deployment, Foundation Type, Capacity, Component, application, and Region 2026-2034

India Offshore Wind Turbine Market Summary:

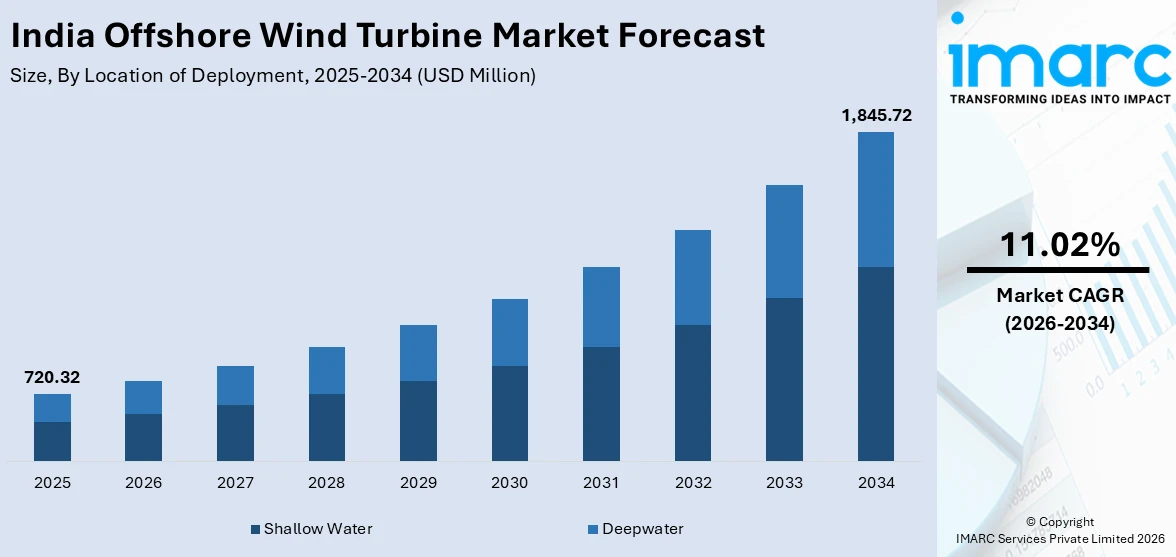

The India offshore wind turbine market size reached USD 720.32 Million in 2025. The market is projected to reach USD 1,845.72 Million by 2034, growing at a CAGR of 11.02% during 2026-2034. The market is driven by substantial government policy support through various schemes to incentivize initial offshore wind projects, combined with strengthening international collaborations focused on supply chain and financing model development. Besides this, continuous technological advancements and rising electricity demand is fueling the India offshore wind turbine market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

| Market Size in 2025 | USD 720.32 Million |

| Market Forecast in 2034 | USD 1,845.72 Million |

| Market Growth Rate (2026-2034) | 11.02% |

| Key Segments | Location of Deployment (Shallow Water, Deepwater), Foundation Type (Fixed Foundation, Floating Foundation), Capacity (Up to 5 MW, 5 to 8 MW, Above 8 MW), Component (Rotor Blades, Nacelle and Drivetrain, Generator, Tower, Power-electronics and Control), Application (Utility-scale, Commercial and Industrial, Residential and Micro-grid) |

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

India Offshore Wind Turbine Market Outlook (2026-2034):

The market expansion appears promising over the next decade, supported by the government’s focus on renewable energy diversification and reducing dependence on fossil fuels. Early-stage policy frameworks, planned projects off the coasts of Gujarat and Tamil Nadu, and the growing interest from global turbine manufacturers indicate strong long-term potential. Advancements in technology, declining turbine costs, and expected policy incentives are likely to accelerate development. Collaborations with international players will help build expertise, infrastructure, and supply chains.

To get more information on this market Request Sample

Impact of AI:

AI is revolutionizing the offshore wind turbine sector by enabling sophisticated digital twin implementations that create virtual replicas of physical turbine assets for real-time performance monitoring and predictive maintenance scheduling. Machine learning (ML) algorithms integrated with finite element analysis facilitate early fault detection across critical components, including foundations, nacelles, and mooring systems, significantly reducing operational downtime and inspection costs. As offshore installations are scaling, AI-driven analytics will become increasingly crucial for managing complex wind farm operations, enhancing safety protocols.

Market Dynamics:

Key Market Trends & Growth Drivers:

Government-Led Viability Gap Funding and Policy Framework Establishment

The Indian government has demonstrated strong commitment towards offshore wind development through comprehensive policy measures designed to de-risk initial investments and provide financial viability for pioneering projects. Recognizing that offshore wind installations require capital expenditures much higher than onshore equivalents due to specialized marine-grade equipment, underwater transmission networks, and extensive port infrastructure requirements, policymakers have instituted targeted financial support mechanisms. In September 2024, the Union Cabinet approved the Viability Gap Funding (VGP) scheme for offshore wind energy projects with a total budget of Rs 7,453 Crores. This included Rs 6,853 Crore earmarked specifically for the installation and commissioning of 1,000 MW of offshore wind projects off the coasts of Gujarat and Tamil Nadu, along with Rs 600 Crore allocated for port infrastructure upgrades to support offshore wind logistics requirements. These policy interventions are creating an enabling regulatory environment in the country.

Strategic International Partnerships and Supply Chain Ecosystem Development

India's offshore wind sector is witnessing accelerated momentum through strategic bilateral collaborations aimed at knowledge transfer, technology access, and manufacturing ecosystem establishment. Recognizing the absence of domestic offshore wind supply chains and specialized installation capabilities, Indian authorities are prioritizing international partnerships to bridge capability gaps and accelerate market maturation. In February 2025, India and the UK declared the formation of the UK-India Offshore Wind Taskforce to promote the broadening of the offshore wind ecosystem, strengthening supply chain capabilities and developing innovative financing models to accelerate offshore wind deployment in both nations. International equipment manufacturers and installation contractors are increasingly exploring joint venture arrangements with Indian enterprises to establish localized manufacturing facilities for critical components, including nacelles, towers, foundations, and offshore substations.

Technological Advancement in Turbine Capacity and Foundation Systems

Technological advancements in turbine capacity and foundation systems are fueling the India offshore wind turbine market growth. Modern turbines feature enhanced rotor diameters, improved aerodynamic efficiency, and sophisticated control systems enabling operation in variable offshore wind regimes. Floating foundation technologies are gaining prominence in deepwater applications, enabling access to superior wind resources farther offshore while avoiding seabed constraints associated with fixed-bottom monopile and jacket structures. In February 2025, Scientists from CSIR-Structural Engineering Research Centre (CSIR-SERC) created a hybrid floating platform capable of generating both wind and solar energy from a single structure. The platform could be utilized in both offshore and inland water bodies, allowing the harnessing of ocean and lake surfaces for renewable energy production. Semi-submersible and tension-leg platform designs compatible with next-generation turbines are advancing towards commercial readiness, with several international technology providers offering proven floating concepts. The identified zones encompass both shallow-water sites suitable for fixed foundations and deepwater locations conducive to floating installations, providing developers flexibility in technology selection based on site-specific bathymetric conditions.

Key Market Challenges:

High Capital Investments and Complex Project Financing

The India offshore wind turbine market is facing a major growth barrier due to the extremely high capital investments required for project development, which are substantially greater than onshore wind or solar projects. Offshore wind farms demand costly components, such as seabed foundations, undersea cabling, specialized installation vessels, and advanced turbines, designed for marine environments. Financing becomes challenging because investors perceive offshore wind as a high-risk sector in India due to its nascent stage, lack of operational benchmarks, and long project gestation periods. Uncertainty over power purchase tariffs, viability gap funding, and government incentives further complicates bankability. Additionally, fluctuating foreign exchange rates impact project costs, as key equipment and expertise are sourced internationally. These financial hurdles limit private sector participation and delay large-scale commissioning, making it difficult for India to attract consistent investments needed to achieve offshore wind capacity targets.

Underdeveloped Marine Infrastructure and Supply Chain Gaps

Another critical challenge to the growth of the market in India is the lack of robust marine infrastructure and a mature domestic supply chain to support large-scale offshore installation and maintenance. Dependence on foreign technology and imported components leads to higher project timelines and costs. Additionally, local manufacturing clusters, workforce expertise, underwater grid connectivity, and maintenance services for offshore environments are still underdeveloped. Without purpose-built coastal infrastructure and streamlined supply chain networks, scaling offshore wind projects beyond pilot phases becomes difficult. Upgrading port infrastructure, establishing fabrication yards, and developing marine engineering capabilities require long-term planning and coordination among multiple government bodies. These gaps slow industry growth and hinder India’s ability to compete with mature offshore markets, such as Europe and China.

Regulatory Uncertainty and Environmental and Permitting Challenges

Regulatory complexity and lengthy approval processes are creating another major barrier for offshore wind turbine development in India. Offshore projects require multiple clearances covering environmental impact, marine ecology, coastal zone regulations, seabed leasing rights, fishing community concerns, defense and maritime security permissions, and grid connectivity approvals. The absence of a streamlined single-window clearance system results in delays and increases project risk. Additionally, uncertainty around long-term policy direction, revenue-sharing frameworks, transmission pricing, and offshore bidding mechanisms makes it harder for developers to plan large investments. Environmental impact assessments are more complex for offshore than onshore projects, as marine biodiversity, fishing routes, and coastal livelihoods must be protected. Balancing ecological safeguards with project execution remains challenging.

India Offshore Wind Turbine Market Report Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the India offshore wind turbine market, along with forecasts at the country and regional levels for 2026-2034. The market has been categorized based on location of deployment, foundation type, capacity, component, and application.

Analysis by Location of Deployment:

- Shallow Water

- Deepwater

The report has provided a detailed breakup and analysis of the market based on the location of deployment. This includes shallow water and deepwater.

Analysis by Foundation Type:

- Fixed Foundation

- Floating Foundation

A detailed breakup and analysis of the market based on the foundation type have also been provided in the report. This includes fixed foundation and floating foundation.

Analysis by Capacity:

- Up to 5 MW

- 5 to 8 MW

- Above 8 MW

The report has provided a detailed breakup and analysis of the market based on the capacity. This includes up to 5 MW, 5 to 8 MW, and above 8 MW.

Analysis by Component:

- Rotor Blades

- Nacelle and Drivetrain

- Generator

- Tower

- Power-electronics and Control

A detailed breakup and analysis of the market based on the component have also been provided in the report. This includes rotor blades, nacelle and drivetrain, generator, tower, and power-electronics and control.

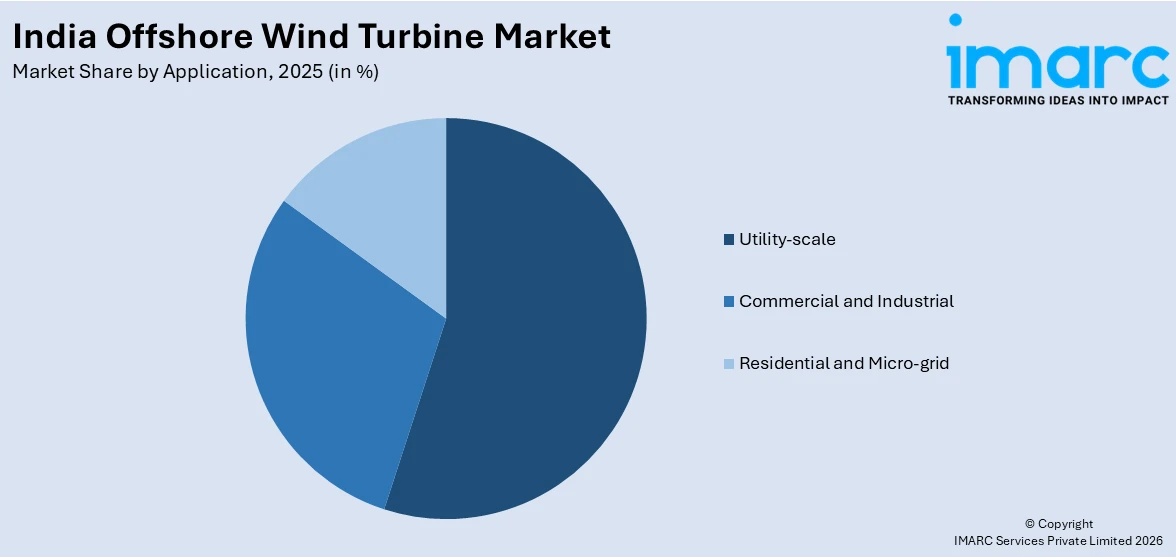

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Utility-scale

- Commercial and Industrial

- Residential and Micro-grid

The report has provided a detailed breakup and analysis of the market based on the application. This includes utility-scale, commercial and industrial, and residential and micro-grid.

Analysis by Region:

- North India

- South India

- East India

- West India

The report has also provided a comprehensive analysis of all the major regional markets, which include North India, South India, East India, and West India.

Competitive Landscape:

The India offshore wind turbine market is characterized by an emerging competitive landscape dominated by potential entry from established international original equipment manufacturers (OEMs) alongside domestic public sector undertakings aimed at exploring joint venture partnerships. Competition at this nascent stage centers primarily around securing early-mover advantage through strategic alliances, technology transfer agreements, and manufacturing ecosystem establishment. International turbine suppliers, including established European and Asian manufacturers possessing proven offshore track records, are actively evaluating Indian market entry strategies, seeking local partnerships to navigate regulatory frameworks and establish component supply networks. Domestic energy majors, particularly public sector enterprises with renewable energy subsidiaries, are positioning themselves as anchor developers capable of aggregating initial project pipelines.

India Offshore Wind Turbine Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Locations of Deployment Covered | Shallow Water, Deepwater |

| Foundation Types Covered | Fixed Foundation, Floating Foundation |

| Capacities Covered | Up to 5 MW, 5 to 8 MW, Above 8 MW |

| Components Covered | Rotor Blades, Nacelle and Drivetrain, Generator, Tower, Power-electronics and Control |

| Applications Covered | Utility-scale, Commercial and Industrial, Residential and Micro-grid |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India offshore wind turbine market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India offshore wind turbine market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India offshore wind turbine industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Offshore Wind Turbine Market Report

The India offshore wind turbine market reached a value of USD 720.32 Million in 2025.

The market is projected to grow at a CAGR of 11.02% during 2026-2034, reaching USD 1,845.72 Million by 2034.

Key growth drivers include substantial government policy support through Viability Gap Funding incentivizing initial offshore wind projects, strengthening international collaborations focused on supply chain and financing development, continuous technological advancements in turbine capacity, floating foundation systems, and rising electricity demand.

The report covers segmentation by location of deployment, foundation type, capacity, component, application, and region. Each segment includes detailed market size and forecast analysis.

Key trends include growing deployment of AI-powered digital twin technology for predictive maintenance, rising adoption of floating foundation systems accessing deepwater resources, accelerating hybrid wind-solar platform development, and increasing joint venture arrangements establishing localized manufacturing capabilities for critical offshore components.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)