India Oil and Gas Market Size, Share, Trends and Forecast by Type, Application, and Region 2026-2034

India Oil and Gas Market Size, Share, Trends & Forecast (2026-2034)

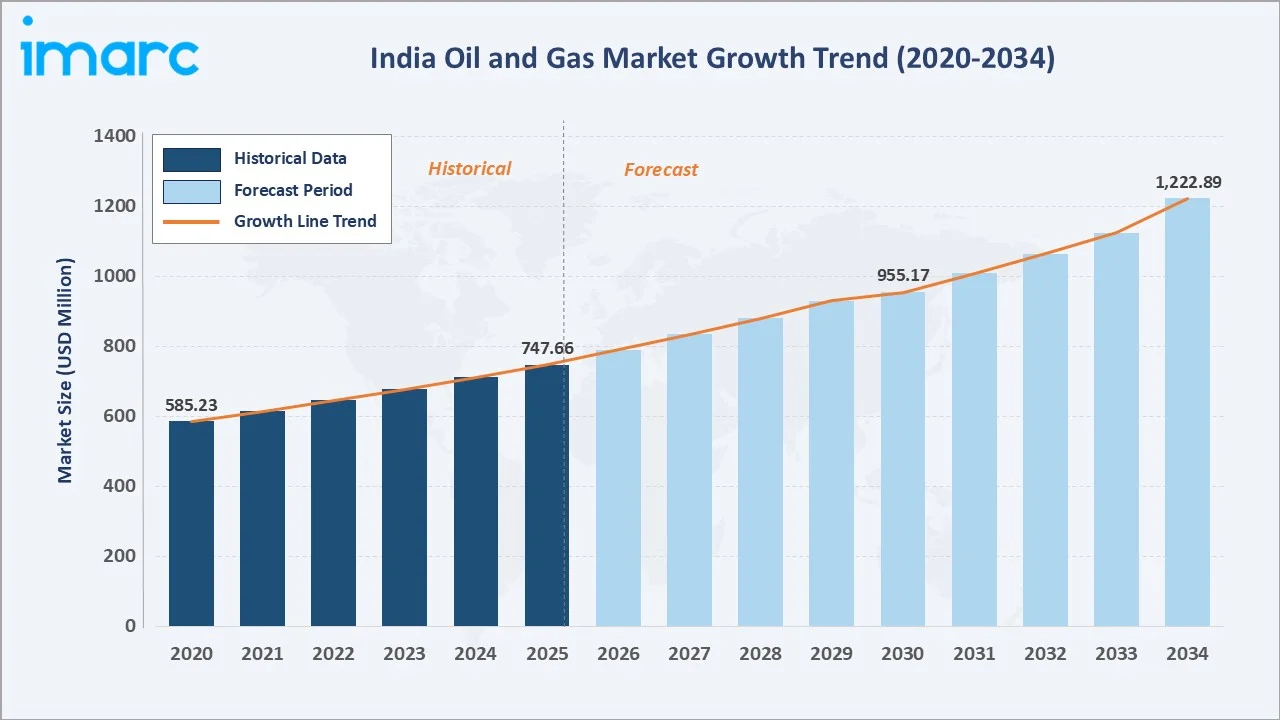

The India oil and gas market reached USD 747.66 Million in 2025 and is projected to reach USD 1,222.89 Million by 2034, growing at a CAGR of 5.02% during 2026-2034. Increasing innovations in exploration, extraction, and production technologies that open up new reserves, reduce costs, and improve operational efficiency are primary growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 747.66 Million |

|

Forecast Market Size (2034) |

USD 1,222.89 Million |

|

CAGR (2026-2034) |

5.02% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

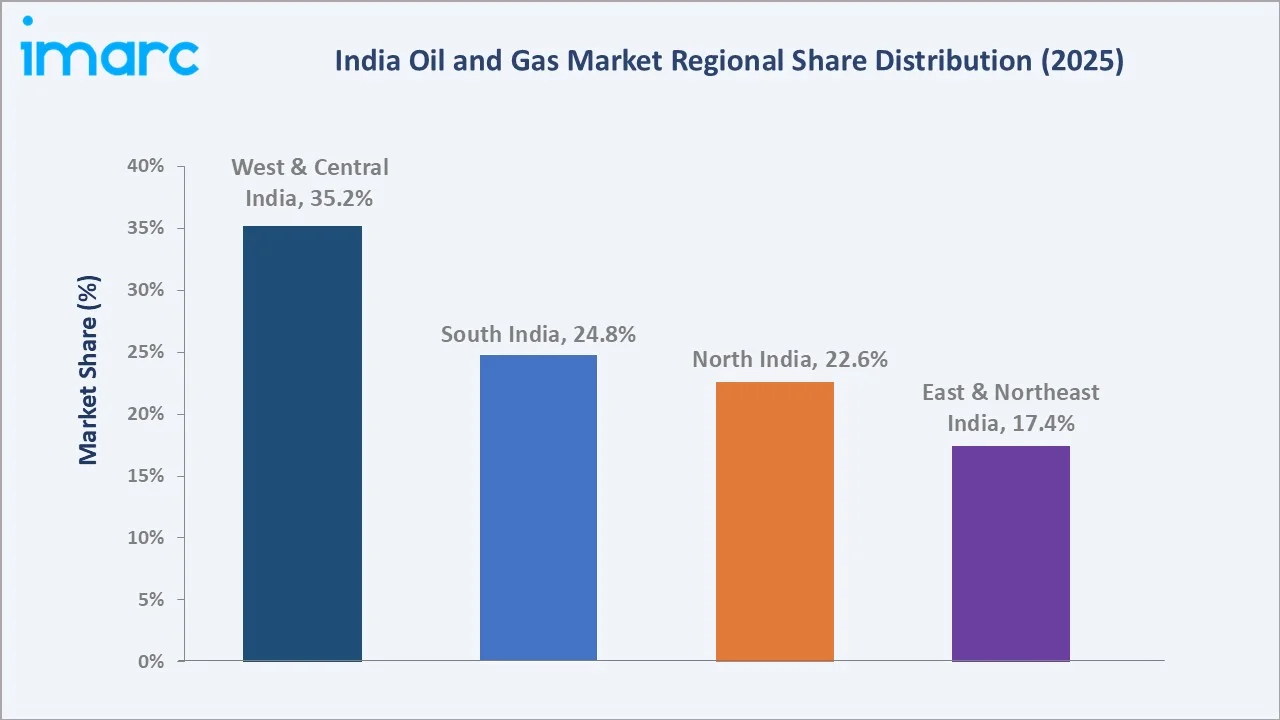

Largest Region |

West and Central India (35.2% share, 2025) |

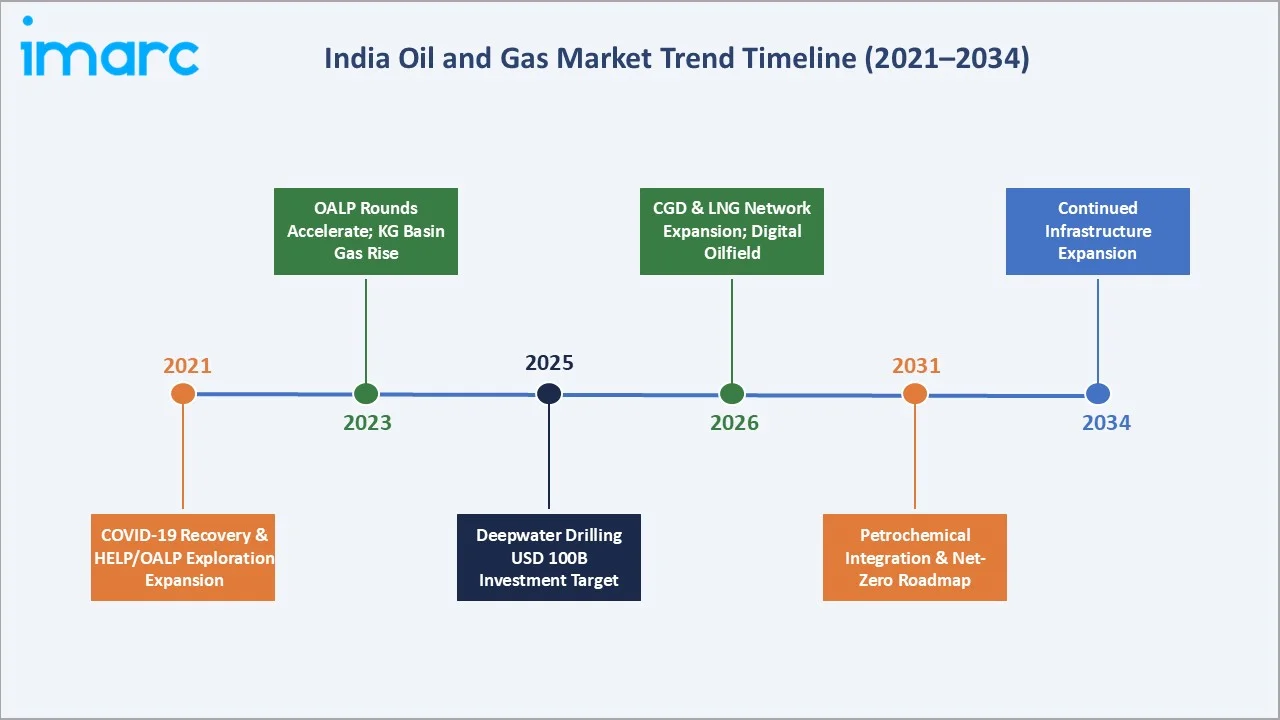

Rising domestic energy demand, government policy reforms under the Hydrocarbon Exploration Licensing Policy (HELP) and Open Acreage Licensing Programme (OALP), and accelerating deepwater developments in the Krishna-Godavari Basin are collectively reinforcing the market's growth trajectory.

To get more information on this market, Request Sample

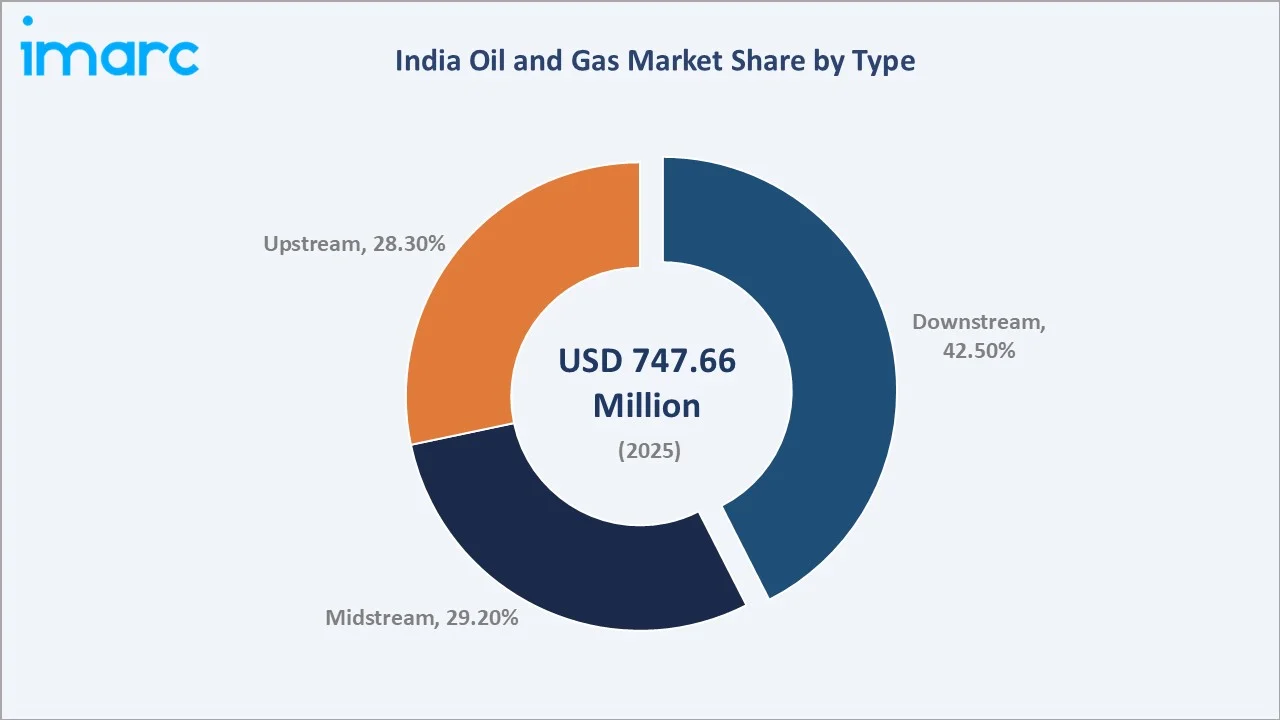

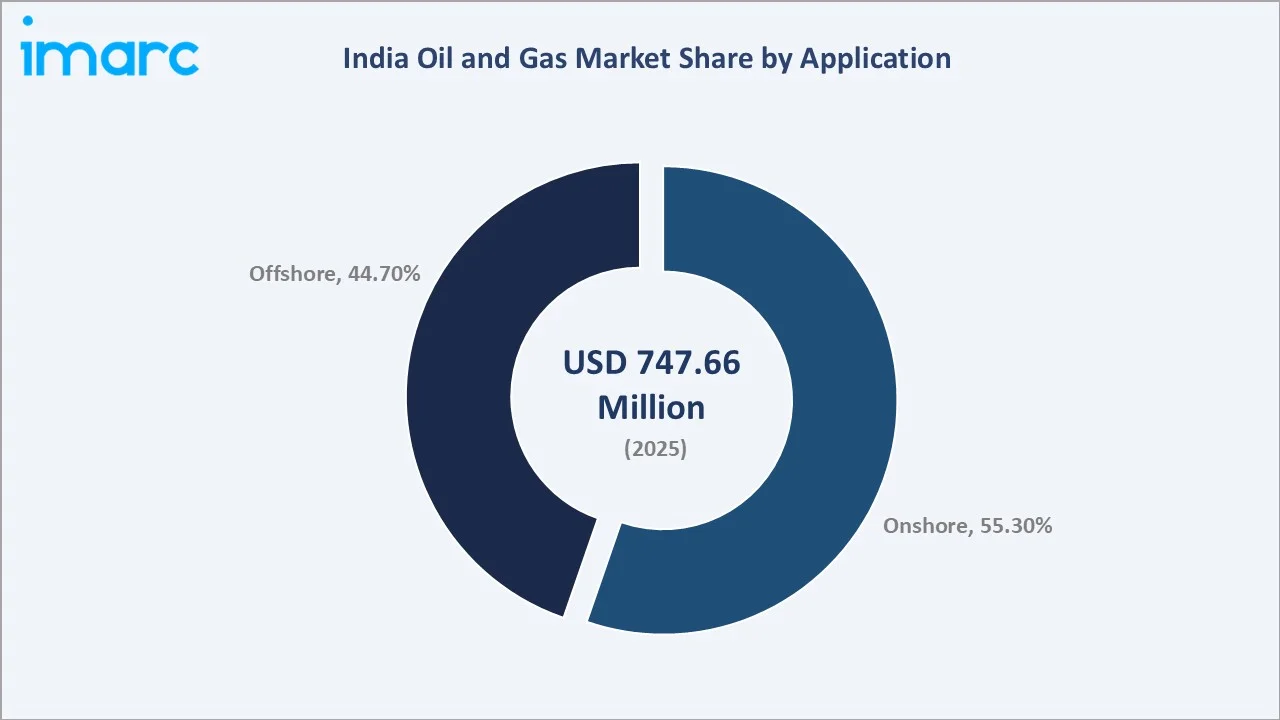

The downstream segment leads the type segmentation with 42.5% share in 2025, while onshore applications dominate at 55.3%. West and Central India commands the largest regional share at 35.2%, anchored by Gujarat's refining infrastructure and the prolific Rajasthan Basin. Key players include Oil and Natural Gas Corporation Limited, Indian Oil Corporation Ltd, Reliance Industries Limited, Bharat Petroleum Corporation Limited, Hindustan Petroleum Corporation Limited, GAIL (India) Limited, and Oil India Limited.

Executive Summary

India oil and gas market is on a sustained growth trajectory underpinned by robust domestic energy demand, policy-driven exploration expansion, and accelerating deepwater development. The market reached USD 747.66 Million in 2025 and is forecast to cross USD 1,222.89 Million by 2034, reflecting a steady CAGR of 5.02%. This growth reflects India's strategic imperative to reduce crude import dependency, which currently exceeds 85-88% of domestic consumption, through enhanced exploration, production capacity expansion, and refinery-petrochemical integration.

West and Central India dominate with a 35.2% regional share (2025), anchored by Gujarat's world-class refining complex at Jamnagar, operated by Reliance Industries, and prolific onshore basins in Rajasthan. The downstream segment leads type segmentation at 42.5%, driven by India's expanding refining capacity, projected to reach 450 MMTPA by 2030, while the midstream (29.2%) and upstream (28.3%) segments are both growing as OALP rounds open new exploration blocks.

India's government has set an ambitious target of attracting USD 100 billion in oil and gas sector investments by 2030, supported by HELP/OALP policy reforms, CGD network expansion, and LNG import terminal buildout. Key players, Oil and Natural Gas Corporation Limited, Indian Oil Corporation Ltd, Reliance Industries Limited, Bharat Petroleum Corporation Limited, Hindustan Petroleum Corporation Limited, are investing aggressively across all value-chain segments to capture this growth.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Downstream – 42.5% share (2025) |

|

Leading Application |

Onshore – 55.3% share (2025) |

|

Leading Region |

West and Central India – 35.2% revenue share (2025) |

|

Fastest Growing Segment |

Offshore (KG Basin deepwater; CAGR ~5.3%) |

|

Top Companies |

Oil and Natural Gas Corporation Limited, Indian Oil Corporation Ltd, Reliance Industries Limited, Bharat Petroleum Corporation Limited, Hindustan Petroleum Corporation Limited |

|

Key Market Opportunity |

USD 100 billion investment target by 2030; CGD network expansion |

Key Analytical Observations Supporting the Above Data:

- Downstream accounts for 42.5% of the Indian oil and gas market in 2025, reflecting India's position as the world's third-largest crude refiner, with total installed refinery capacity reaching 258.1 MMTPA as of April 2025 and a strategic goal to nearly double this to 309.5 MMTPA by 2030.

- Onshore applications lead at 55.3% of the market (2025), driven by producing basins in Rajasthan (Barmer), Assam, Gujarat, and the Krishna-Godavari onshore zone, supported by OALP bidding rounds that have awarded over 105 exploration blocks covering 156,580 sq km.

- West and Central India generates 35.2% of national oil and gas revenues (2025), anchored by Jamnagar, home to the world's largest refinery complex operated by Reliance Industries, and Gujarat's dense midstream pipeline and CGD infrastructure.

- In May 2025, Oil and Natural Gas Corporation (ONGC) announced two major offshore oil and gas discoveries, Suryamani in OALP‑6 block MB‑OSHP‑2020/2 and Vajramani in OALP‑3 block MB‑OSHP‑2018/1 in the Mumbai Offshore hydrocarbon basin, reinforcing India's offshore growth potential.

- According to OPEC estimates, India’s oil demand growth is expected to reach 5.99 million bpd in 2026, driven by transportation, industrial, and petrochemical sector expansion, sustaining strong downstream refining and midstream distribution demand.

- Government HELP and OALP policies have liberalized exploration licensing, with new blocks awarded in under-explored basins including Andaman & Nicobar, Mahanadi, and Kutch deepwater areas, creating a pipeline of future production growth.

India Oil and Gas Market Overview

India's oil and gas market encompasses the full value chain of exploration, extraction, transportation, refining, and distribution of crude oil, natural gas, LPG, and petroleum products serving the country's 1.4 billion population. As the world's third-largest consumer of crude oil and third-largest LPG consumer, India's energy requirements are structurally growing, driven by rapid urbanization, industrialization, and an expanding vehicle fleet projected to double by 2040.

The market ecosystem spans state-owned enterprises that dominate core value-chain positions, private sector leaders, and international participants providing technology, capital, and expertise for deepwater and unconventional projects. The Hydrocarbon Exploration Licensing Policy (HELP), introduced in 2016, and its Open Acreage Licensing Programme (OALP) have progressively liberalized exploration, attracting new entrants and accelerating block awards.

India's strategic ambition to increase the share of natural gas in the energy mix from 6.7% currently to 15% by 2030 is reshaping the midstream segment, driving CGD network expansion to 300+ districts, LNG import terminal capacity buildout, and GAIL's national gas grid expansion. Simultaneously, the downstream segment is undergoing a refinery-petrochemical integration wave, as IOCL, BPCL, and HPCL race to bolt high-margin polymer, aromatics, and specialty chemical units onto existing crude processing trains to capture value-added margins.

Market Dynamics

To evaluate market opportunities, Request Sample

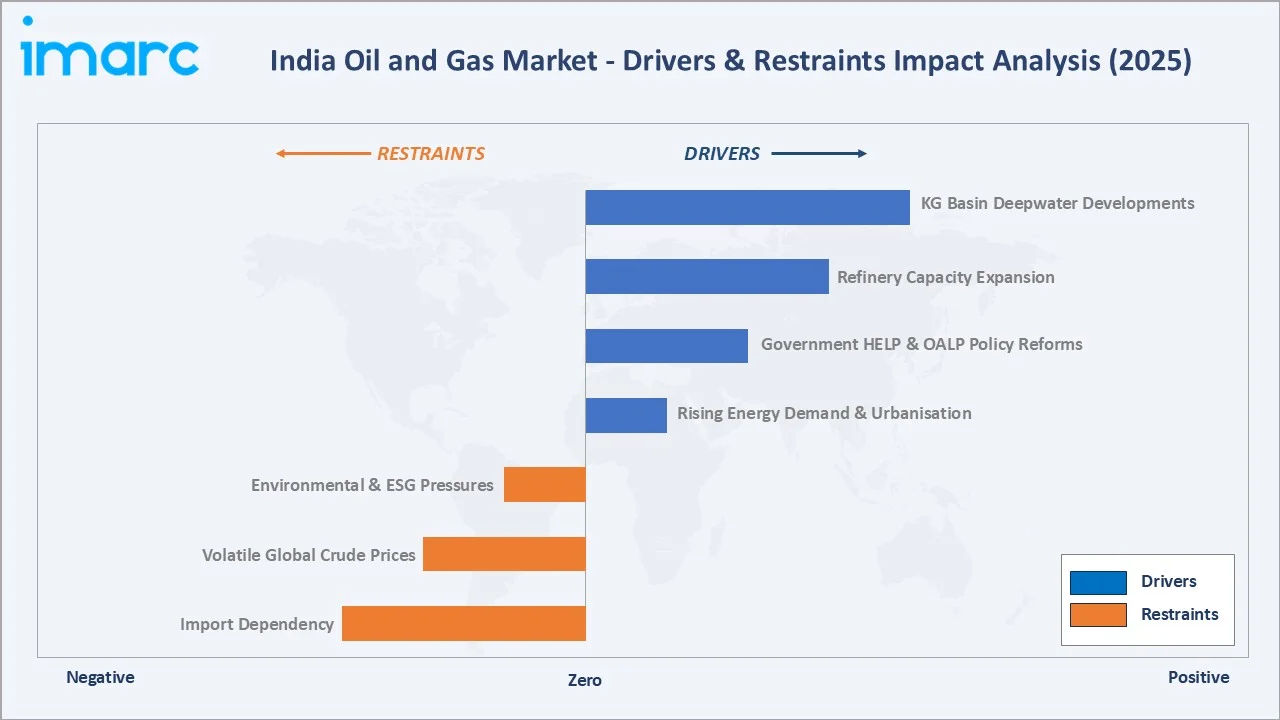

Market Drivers

- Rising Energy Demand Driven by Economic Growth and Urbanization: India's GDP growing at 6–7% annually is sustaining robust energy demand. Oil demand reached 5.57 million barrels per day in 2024, up 4.19% year-over-year, with transportation sector consumption (gasoline, diesel) expanding as India's vehicle fleet continues its rapid growth trajectory.

- Government HELP/OALP Policy Reforms and Exploration Expansion: The Indian government's commitment to doubling exploration area from 0.5 million sq km (2025) to 1 million sq km by 2030, combined with fiscal incentives under the OALP framework, is driving sustained upstream investment.

- Refinery Capacity Expansion and Petrochemical Integration: India's refining capacity of 258.1 MMT (April 2025) is projected to reach 450–500 MMT by 2030, representing one of the world's largest refinery buildout programs. IOCL's five refinery-cum-cracker complexes, BPCL's Project Aspire (INR 1.5 lakh crore investment strategy), and HPCL's Barmer refinery commissioning are driving downstream investment at an unprecedented pace.

- KG Basin Deepwater Developments and Offshore Output Growth: Reliance Industries and ONGC's deepwater gas fields in the Krishna-Godavari Basin, including R Cluster, Satellite Cluster, and MJ fields, are driving offshore output growth.

These drivers create policy reforms that attract exploration investment, increasing domestic production reduces import dependency, refinery capacity expansion multiplies downstream value, and gas infrastructure growth broadens end-user market penetration.

Market Restraints

- High Crude Import Dependency and Price Volatility Exposure: India imports over 85% of its crude oil requirements, creating significant exposure to global price volatility and geopolitical supply disruptions. While strategic crude reserves (Vishakhapatnam, Mangaluru, Padur) provide 9.5 days of buffer, the structural import dependency constrains India's energy security and creates fiscal risk for domestic fuel pricing.

- Volatile Global Crude Prices and Downstream Margin Compression: India's government-administered pricing mechanism for automotive fuels creates a lag between international crude price movements and domestic retail prices, periodically creating under-recovery for public sector oil marketing companies (OMCs), particularly BPCL, HPCL, and IOCL.

- Environmental, ESG, and Energy Transition Pressures: India's international climate commitments (45% reduction in emissions intensity by 2030 vs. 2005) and domestic renewable energy targets (500 GW of non-fossil capacity by 2030) are progressively diverting capital toward clean energy, creating a structural shift in institutional investment priorities away from long-term upstream oil & gas commitments.

Market Opportunities

- City Gas Distribution (CGD) Network Expansion: Sixth and seventh CGD bidding rounds covering 300+ districts represent a massive market expansion opportunity for natural gas distribution. With only approximately 6% gas share in India's energy mix versus a 15% target by 2030, the CGD opportunity for compressed natural gas (CNG), piped natural gas (PNG) residential, and industrial connections represents a multi-billion-dollar infrastructure investment.

- LNG Import Terminal Buildout and Gas Infrastructure: India's LNG import capacity is being substantially expanded across new terminals (Dhamra, Ennore, Jaigarh, Chhara). GAIL held 59.25% of India's 33,203 km natural gas pipeline network as of March 2025, with the national gas grid expansion program creating new demand corridors in Eastern and Northeastern India.

- Petrochemical Downstream Integration: India's per capita polymer consumption at approximately 14 kg versus the global average of 35 kg represents a substantial structural demand growth opportunity.

Market Challenges

- Land Acquisition and Infrastructure Right-of-Way Delays: Pipeline corridor land acquisition and right-of-way challenges continue to delay midstream infrastructure projects, particularly in densely populated states. The Urja Ganga and Northeast Gas Grid projects have faced implementation delays due to multi-stakeholder land clearance requirements.

- Mature Field Decline Rates and Reservoir Management: India's legacy producing fields, Mumbai High (ONGC), Assam fields (Oil India), and Ankleshwar (ONGC), are experiencing natural decline rates of 5–8% annually, requiring sustained enhanced oil recovery (EOR) investments and international technical partnerships to sustain output levels.

Emerging Market Trends

1. Digital Oilfield Technologies and AI-Driven Reservoir Management

Oil India's eleven-module Project DRIVE targets a 15% reduction in non-productive time by 2026, while Cairn Oil & Gas employs predictive analytics to maintain unplanned downtime below 3%. ONGC's technical services agreement with BP for advanced reservoir management at Mumbai High targets a 60% production increase using AI-driven subsurface analysis and 3D seismic reprocessing.

2. Refinery-Petrochemical Integration Accelerating Downstream Value

Indian Oil Corporation (IOC), Bharat Petroleum Corporation Ltd (BPCL), and Hindustan Petroleum Corporation Ltd (HPCL) have agreed to jointly develop the country’s largest oil refinery and petrochemical complex in Maharashtra, with a planned capacity of 60 million tons per year and an estimated investment of around ₹2 lakh crore.

3. KG Basin Deepwater Development Driving Offshore Production Growth

ONGC's USD 5 billion KG-DWN-98/2 cluster development, Reliance-BP's R Cluster, Satellite Cluster, and MJ fields, and ONGC's new Suryamani and Vajramani discoveries are collectively expected to add 15–20 million metric standard cubic meters per day (MMSCMD) of incremental gas production by 2030. Pre-FEED and FEED awards for subsea infrastructure in April 2025 indicate accelerating project timelines.

4. Natural Gas Infrastructure and CGD Network Expansion

In 2023, PNGRB approved a natural gas pipeline network spanning approximately 33,592 km across the country, and the rapid growth of City Gas Distribution (CGD) infrastructure is transforming India's midstream and downstream gas landscape. GAIL's Dabhol LNG terminal, achieving full monsoon-season operations following breakwater completion (May 2025), demonstrates India's resolve to ensure year-round LNG import reliability.

5. Green Hydrogen and Clean Fuels Integration

IndianOil finalized plans for India’s largest green hydrogen project at its Panipat facility, marking a major step in advancing low‑carbon fuel production, while GAIL is piloting hydrogen blending in pipelines up to 5%. ONGC's INR 2,00,000 crore investment plan for new energy and decarbonization projects targeting net-zero Scope 1 and 2 emissions by 2038 signals the sector's long-term energy transition commitment alongside continued hydrocarbon growth.

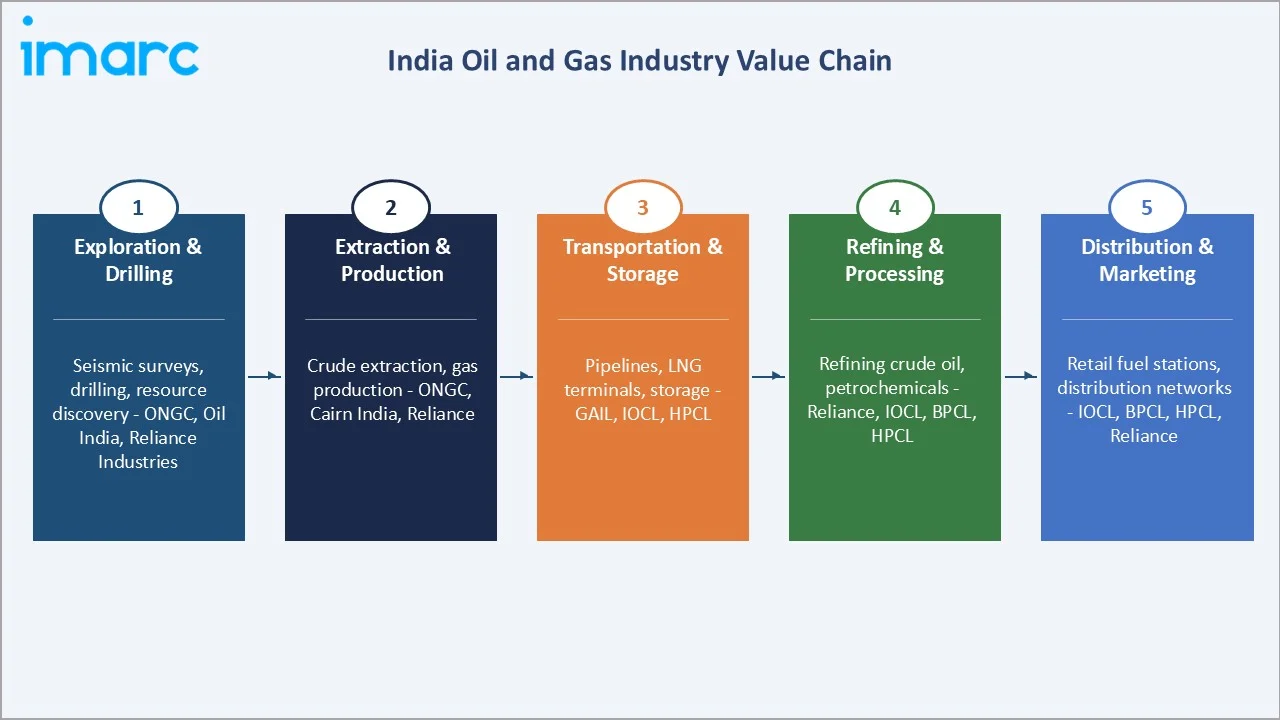

Industry Value Chain Analysis

The India oil and gas value chain spans five interconnected stages from geological exploration through end-consumer product distribution, with each stage populated by specialized operators whose performance directly influences energy security, product cost competitiveness, and market growth.

|

Stage |

Key Players / Examples |

|

Exploration & Drilling |

Oil and Natural Gas Corporation Limited, Oil India Limited, Reliance Industries Limited, Cairn Oil & Gas, Shell India |

|

Extraction & Production |

Oil and Natural Gas Corporation Limited (~70% domestic output), Oil India (Assam), Reliance Industries Limited (KG D6), Cairn Oil & Gas (Rajasthan) |

|

Transportation & Storage |

GAIL (India) Limited (~65–70% market share in gas transmission), Indian Oil Corporation Ltd (crude pipeline), Petronet LNG |

|

Refining & Processing |

Reliance Jamnagar (world's largest), Indian Oil Corporation Ltd (Panipat, Vadodara), Bharat Petroleum Corporation Limited, Hindustan Petroleum Corporation Limited, Nayara Energy |

|

Distribution & Marketing |

Indian Oil Corporation Ltd (40k+ retail outlets), Hindustan Petroleum Corporation Limited (24k+), Bharat Petroleum Corporation Limited (23k+), Adani Total Gas Limited (ATGL), Indraprastha Gas (IGL) |

Technology Landscape in the India Oil and Gas Industry

Advanced Exploration and Deepwater Technologies

Cairn Oil & Gas's partnership with EMGS for 3D Controlled Source Electromagnetic (CSEM) surveys across 3,600 sq km of KG Basin acreage (April 2025) exemplifies the application of advanced geophysical techniques to de-risk deepwater exploration. ONGC's use of high-resolution 3D seismic surveys, high-pressure high-temperature (HPHT) drilling techniques, and subsea multiphase production systems in KG-DWN-98/2 represents the leading edge of Indian offshore technology deployment.

Enhanced Oil Recovery (EOR) and Digital Reservoir Management

Oil India completed 29 cyclic steam cycles in Rajasthan, achieving up to 60% output uplift over cold production (May 2025), demonstrating thermal EOR effectiveness. Digital twin technology, AI-based reservoir modelling, real-time well monitoring, and predictive maintenance analytics are being deployed by ONGC, Cairn, and Oil India to optimize production from legacy assets.

Refinery Technology and Petrochemical Integration

HPCL commissioned a new Residue Upgradation Facility (RUF) at Visakhapatnam in January 2026, significantly boosting distillate yields and refining margins. Multi-phase pumping technology, which eliminates the need to separate gas, oil, and water at the wellhead, is increasingly deployed in both onshore and offshore producing assets.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Type | Downstream | 42.5% |

2025 |

| Application | Onshore | 55.3% |

2025 |

| Region | West and Central India | 35.2% |

2025 |

By Type

The downstream segment dominates India's oil and gas market with a 42.5% share in 2025, reflecting India's status as the world's third-largest crude oil refiner. The downstream boom is driven by refinery-petrochemical integration across IOCL, BPCL, HPCL, and Reliance, as operators seek to shift from commodity fuel production to high-margin petrochemical, polymer, and specialty chemical outputs.

To access detailed market analysis, Request Sample

The upstream segment accounts for 28.3% (approximately USD 211.59 Million), with ONGC maintaining approximately 70% of domestic crude output, Oil India expanding Assam field production, and private explorers (Reliance, Cairn, Vedanta) scaling up under successive OALP rounds.

By Application

Onshore applications lead the segment with a 55.3% share in 2025, anchored by prolific producing basins in Rajasthan (Barmer Basin), Gujarat (Ankleshwar, Cambay), Assam (Oil India operations), and Krishna-Godavari onshore. India's onshore oil and gas production has historically served as the backbone of domestic supply, supported by extensive pipeline and processing infrastructure concentrated in Western India.

Offshore applications hold 44.7% of the market, with growth driven by deepwater Krishna-Godavari Basin developments and Mumbai High redevelopment programs. India's offshore output is forecast to grow at approximately 5.3% CAGR through 2034, led by ONGC's KG-DWN-98/2 subsea development and Reliance-BP's KG D6 gas fields, which averaged 28 million metric standard cubic meters per day in Q4 2024.

Regional Market Insights

West and Central India led the regional market with a 35.2% share (2025, approximately USD 263.17 Million), anchored by Gujarat's world-class refining and processing infrastructure. Jamnagar, home to Reliance's 1.24 million barrels per day refining complex, the world's largest integrated refinery, is the single most important oil and gas hub in India.

|

Region |

Share (2025) |

Key Assets & Drivers |

Key Infrastructure |

|

West and Central India |

35.2% |

Jamnagar refinery complex, Barmer Basin, Gujarat onshore fields |

Hazira LNG, Dahej LNG, IOCL Koyali refinery |

|

South India |

24.8% |

KG Basin deepwater, Cauvery Basin |

Ennore LNG, Chennai refinery, Mangalore refinery |

|

North India |

22.6% |

Panipat refinery complex, Delhi NCR CGD, UP gas markets |

IOCL Panipat, Delhi-Noida CGD (IGL), Mathura refinery |

|

East and Northeast India |

17.4% |

Assam crude fields, CBM production, growing pipeline access |

Jagdishpur-Haldia pipeline, Numaligarh refinery |

South India (24.8%, 2025) is the second-largest regional market, with its significance primarily driven by deepwater Krishna-Godavari Basin gas production and the Cauvery Basin's Chennai Petroleum Corporation Limited (CPCL) refinery expansion (targeting 180 kb/d capacity). North India (22.6%) is anchored by IOCL's Panipat refinery complex and India's densest CGD network in the Delhi-NCR region, operated by Indraprastha Gas Limited (IGL) and GAIL subsidiary companies.

Competitive Landscape

India oil and gas market is dominated by public sector undertakings (PSUs) across all value-chain segments, with the top five PSUs, Oil and Natural Gas Corporation Limited, Indian Oil Corporation Ltd, Bharat Petroleum Corporation Limited, Hindustan Petroleum Corporation Limited, and GAIL (India) Limited, collectively accounting for over 65–70% of market revenues in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Oil and Natural Gas Corporation Limited |

ONGC; OVL (ONGC Videsh) |

Market Leader |

~70% of domestic crude output; deepwater KG Basin; Mumbai High operations |

|

Indian Oil Corporation Ltd |

IndianOil; Indane (LPG); SERVO (lubricants) |

Market Leader |

Dominant share in crude pipeline network; 40,000+ retail outlets; around 10 refinery-petrochemical complexes |

|

Reliance Industries Limited |

Jio-bp (retail fuel network) |

Private Sector Leader |

Jamnagar — world's largest refinery; KG D6 deepwater gas; Jio-bp retail network |

|

Bharat Petroleum Corporation Limited |

Bharat Petroleum; MAK Lubricants; Speed (premium fuel) |

Strong Challenger |

Significant investments in Project Aspire; Bina petrochemicals; 23,642 retail outlets |

|

Hindustan Petroleum Corporation Limited |

HP; Laal Ghoda (lubricants) |

Strong Challenger |

Barmer refinery (9 MMTPA); Vizag expansion; 20,000+ outlets; INR 90,000 cr investment |

|

GAIL (India) Limited |

GAIL Gas (CGD arm) |

Midstream Leader |

~70% of India's gas pipeline network; PDH plant at Usar; CGD expansion |

|

Oil India Limited |

OIL |

Upstream Specialist |

Assam upstream operations; EOR thermal recovery; NE pipeline investment |

Private sector challengers, led by Reliance Industries Limited. and Cairn Oil & Gas, compete vigorously in the upstream and downstream segments.

Key Company Profiles

Oil and Natural Gas Corporation Limited

ONGC is India's largest oil and gas exploration and production company, producing about two-thirds (~70%) of India's crude oil and ~80% of natural gas, commanding a dominant upstream position through operations across Mumbai Offshore, KG Basin, Assam, Gujarat, and Rajasthan.

- Product Portfolio: Crude oil, natural gas, LPG, naphtha; offshore and onshore production operations; oilfield services through ONGC Videsh Limited (OVL).

- Recent Developments: Discovered Suryamani and Vajramani fields (Mumbai Offshore, May 2025); awarded pre-FEED and FEED contracts for KG-DWN-98/2 subsea infrastructure (April 2025).

- Strategic Focus: Deepwater production ramp-up; EOR in mature fields; INR 2,00,000 crore new energy investment for net-zero Scope 1 & 2 by 2038; overseas E&P expansion via ONGC Videsh Limited (OVL).

Indian Oil Corporation Ltd

IOCL is India's largest commercial enterprise and the dominant downstream operator, owning the country's largest share of crude oil pipelines (50.88%, 14,000+ km) and the most extensive retail fuel network (40,221 outlets as of FY2025).

- Product Portfolio: Petrol, diesel, LPG, aviation fuel, petrochemicals, lubricants; INDANE LPG; Servo lubricants; XtraPremium (regular premium), XP95 (95-octane), and XP100 (100-octane).

- Recent Developments: L&T contracted for India's first green hydrogen plant at Panipat (10,000 TPY, May 2025); targeting 31 GW renewables and 80 ktpa green hydrogen by 2030; INR 2.4 lakh crore net-zero investment roadmap to 2046.

- Strategic Focus: Petrochemical integration at Panipat and Gujarat refineries; CGD network expansion; green hydrogen and biofuel blending mandates; LPG distribution to rural markets.

Reliance Industries Limited

Reliance Industries' Jamnagar refinery complex in Gujarat has a 1.4 million barrels per day capacity, making Reliance the most formidable private sector oil and gas player in India. The company's KG D6 deepwater gas fields, jointly developed with BP, are central to India's gas supply security.

- Product Portfolio: Petrol, diesel, jet fuel, LPG, petrochemicals (polymers, polyester, aromatics); KG D6 natural gas; Jio-bp retail fuel network.

- Recent Developments: KG D6 averaged 28 MMSCMD gas production in Q4 2024; 10-year Rosneft crude supply deal for Jamnagar boosting margins; entered resource-sharing pact with ONGC for KG Basin and Andaman offshore infrastructure.

- Strategic Focus: Jamnagar refinery-petrochemical integration; KG D6 gas production maximization; Jio-bp retail fuel network expansion; INR 75,000 crore renewable energy and green hydrogen investment.

GAIL (India) Limited

GAIL is India's dominant natural gas infrastructure company, holding the largest share (~65–70% market share in gas transmission) of India's 20,000+ km national gas pipeline network as of March 2025. GAIL is central to India's gas growth strategy, driving CGD expansion, LNG terminal connectivity, and pioneering green hydrogen blending in gas pipelines.

- Product Portfolio: Natural gas transmission and distribution; LPG; petrochemicals (polymers, polyester); LNG regasification.

- Recent Developments: Dabhol LNG terminal full monsoon operations (June 2025); 500 kt/yr PDH facility at Usar expected to start 2025; hydrogen blending pipeline pilot (up to 5% H2 blend).

- Strategic Focus: National gas grid expansion to 35,000 km by 2030; CGD network coverage in 300+ districts; LNG import capacity augmentation; green hydrogen infrastructure development.

Market Concentration Analysis

India's oil and gas market exhibits high concentration in the PSU segment, with ONGC, IOCL, BPCL, HPCL, and GAIL collectively dominating core value-chain positions through government-backed capital, integrated infrastructure networks, and retail distribution scale.

However, the competitive landscape is increasingly bifurcated, and private sector companies, including Reliance Industries Limited. (refining), Cairn Oil & Gas (upstream), Adani Total Gas Limited (ATGL), and Petronet LNG (regasification) are carving out dominant positions in their respective market niches. The government's strategic divestment process for Bharat Petroleum Corporation Limited, while periodically delayed, signals a long-term intent to introduce greater private sector competition in downstream retail.

Investment & Growth Opportunities

Fastest Growing Segments

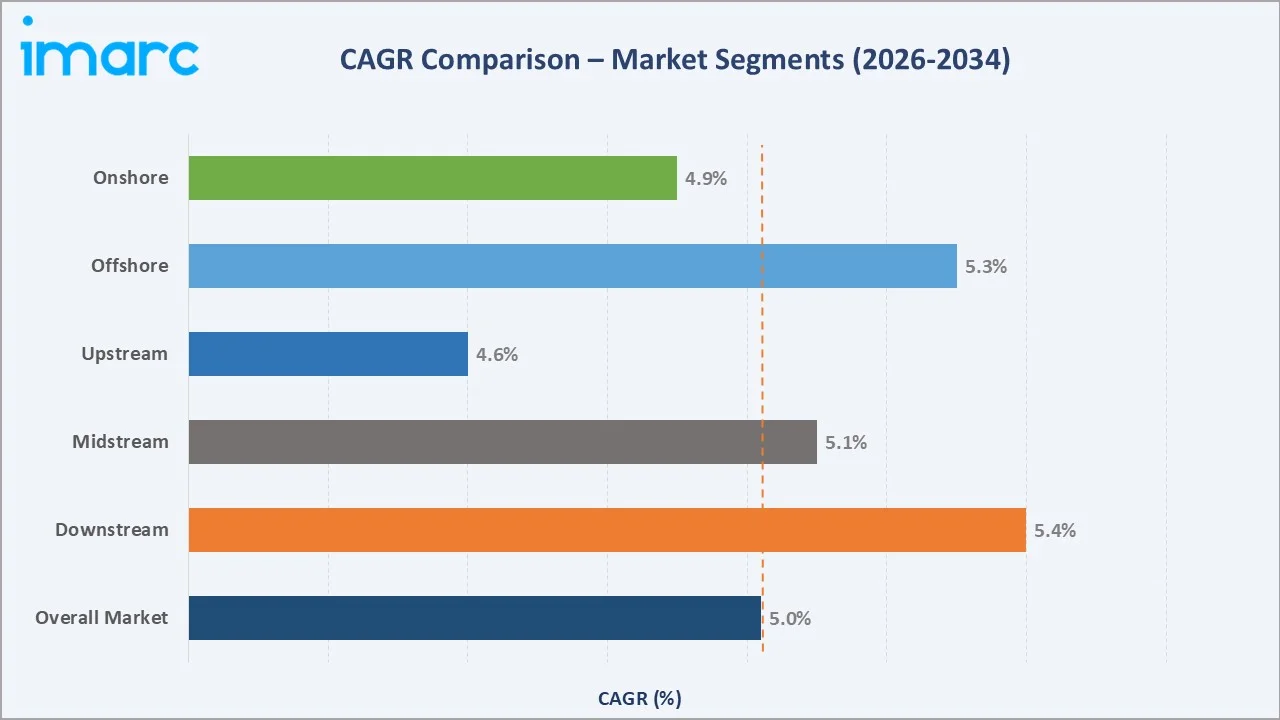

Offshore deepwater development (CAGR ~5.3%), petrochemical-integrated downstream refining (CAGR ~5.4%), and City Gas Distribution/LNG midstream infrastructure (CAGR ~5.1%) represent the three highest-growth investment vectors in the India oil and gas market through 2034. Together, these segments address a total addressable capital investment requirement of USD 60–70 billion over the forecast period, driven by India's ambition to attract USD 100 billion in sector investments by 2030.

Emerging Market Expansion

East and Northeast India (17.4% share, 2025) represents the most strategically significant geographic expansion opportunity through 2034. The Jagdishpur-Haldia-Bokaro-Dhamra natural gas pipeline corridor, ONGC and Oil India's upstream expansion in Assam and Tripura, and the Numaligarh Refinery capacity expansion collectively represent an incremental USD 8–10 billion investment opportunity in India's least-developed oil and gas geography.

Venture and Institutional Investment Trends

India's oil and gas sector attracted record PSU capex of INR 1.28 trillion in FY2023-24, with ONGC, IOCL, BPCL, HPCL, and GAIL all recording multi-year investment highs. International investors, including Saudi Aramco (in discussions for two 9 MTPA refineries with BPCL and ONGC), Petrobras (crude supply agreements and E&P cooperation MoUs), and BP (ONGC MoU, Reliance KG D6 JV) signal sustained FDI interest.

- Key investment themes: KG Basin deepwater infrastructure, refinery-petrochemical cracker complexes, CGD network expansion, LNG terminal capacity, EOR technology deployment in mature fields, and green hydrogen integration.

- Government-directed investment through the India National Investment and Infrastructure Fund (NIIF) and sovereign wealth fund co-investment structures are being pursued for large capital-intensive midstream and downstream projects.

- Private equity and infrastructure funds are increasingly targeting midstream CGD assets, particularly city gas distribution companies, as regulated, long-duration infrastructure investments with stable contracted revenue profiles.

Future Market Outlook (2026-2034)

India oil and gas market is positioned for sustained, broad-based growth through 2034. From USD 747.66 Million in 2025, the market is projected to reach USD 1,222.89 Million by 2034, representing total incremental value creation of USD 475.23 Million over the forecast decade, underpinned by India's position as the world's fastest-growing major oil and gas demand market.

Regulatory evolution, particularly PNGRB's new LNG Terminal Regulations (May 2025), successive OALP bidding rounds, the Gas Grid expansion mandate, and the government's 20% ethanol blending target, will define the competitive operating environment through 2034. Operators that successfully execute deepwater development programs, refinery-petrochemical integration, and CGD network expansion will capture disproportionate market share growth.

Long-term, India's oil and gas market trajectory is tied to three structural macro-themes: energy security imperative, petrochemical transformation (shifting downstream value from commodity fuels to high-margin polymer and specialty chemical products), and the energy transition (integrating green hydrogen, biofuels, and renewable energy into the hydrocarbon value chain).

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 90 industry participants in 2024–2025, including oil and gas exploration executives, refinery operations managers, midstream infrastructure developers, PNGRB and MoPNG officials, downstream marketing specialists, and energy analysts across New Delhi, Mumbai, Ahmedabad, Chennai, and Kolkata.

Secondary Research

Secondary research encompassed a systematic review of company annual reports (ONGC, IOCL, BPCL, HPCL, GAIL, Reliance Industries, Oil India), Petroleum Planning & Analysis Cell (PPAC) statistical data, Directorate General of Hydrocarbons (DGH) block award databases, PNGRB pipeline and CGD reports, Ministry of Petroleum and Natural Gas (MoPNG) policy documents, industry publications (Indian Oil & Gas, Petrowatch), and IBEF sector data.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating India's GDP growth projections, energy demand elasticity coefficients, domestic crude production trajectories, refinery capacity expansion schedules, and historical CAGR benchmarks. A base-case CAGR of 5.02% reflects consensus estimates validated against PPAC demand data and company-reported capital expenditure growth trajectories.

India Oil and Gas Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Upstream, Midstream, Downstream |

| Applications Covered | Offshore, Onshore |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Oil and Natural Gas Corporation Limited, Indian Oil Corporation Ltd, Reliance Industries Limited, Bharat Petroleum Corporation Limited, Hindustan Petroleum Corporation Limited, GAIL (India) Limited, Oil India Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India oil and gas market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India oil and gas market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India oil and gas industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Oil and Gas Market Report

The India oil and gas market reached USD 747.66 Million in 2025. It is projected to reach USD 1,222.89 Million by 2034.

The India oil and gas market is expected to grow at a CAGR of 5.02% during the forecast period from 2026 to 2034, driven by rising domestic energy demand, government exploration policy reforms, refinery capacity expansion, and deepwater offshore development.

West and Central India leads with a 35.2% revenue share in 2025, anchored by Reliance's world's largest Jamnagar refinery complex, Cairn's prolific Barmer Basin upstream operations, and Gujarat's dense midstream pipeline and LNG import infrastructure.

The downstream segment dominates with a 42.5% share in 2025 (approximately USD 317.75 Million), driven by India's expanding refinery capacity target of 450–500 MMT by 2030 and accelerating refinery-petrochemical integration investment across IOCL, BPCL, HPCL, and Reliance.

Onshore applications lead with a 55.3% share in 2025 (approximately USD 413.45 Million), driven by producing basins in Rajasthan, Gujarat, and Assam, supported by OALP exploration block awards covering 156,580 sq km of onshore acreage.

Key players include Oil and Natural Gas Corporation Limited, Indian Oil Corporation Ltd, Reliance Industries Limited, Bharat Petroleum Corporation Limited, Hindustan Petroleum Corporation Limited, GAIL (India) Limited, and Oil India Limited.

Key drivers include India's rising oil demand (5.57 million barrels per day in 2024), government HELP/OALP exploration reforms, refinery capacity expansion (target: 450–500 MMT by 2030), KG Basin deepwater development, and the national gas grid expansion targeting 15% gas share in India's energy mix by 2030.

Key challenges include India's 85%+ crude import dependency, exposing the economy to global price volatility, mature field natural decline rates of 5–8% annually in legacy fields, administered pricing constraints on fuel marketing margins, land acquisition delays for pipeline infrastructure, and the long-term capital reallocation pressure from India's ambitious renewable energy transition targets.

Significant investment opportunities exist in KG Basin deepwater subsea infrastructure, refinery-petrochemical integration, City Gas Distribution network expansion, LNG import terminal capacity, EOR in mature fields, and green hydrogen integration into existing gas pipelines.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)