India Oncology Market Size, Share, Trends and Forecast by Cancer Diagnostics and Treatment, Cancer Type, End Use, and Region, 2026-2034

India Oncology Market Size, Share, Trends & Forecast (2026-2034)

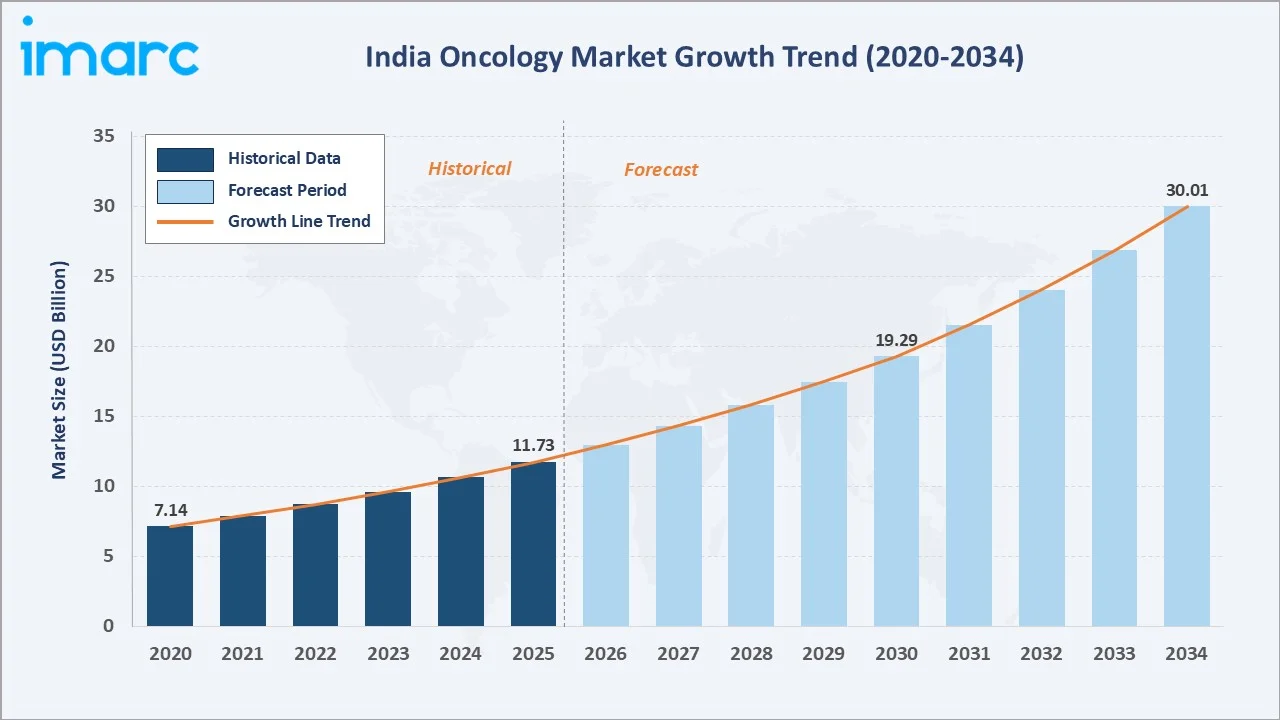

The India oncology market was valued at USD 11.73 Billion in 2025 and is projected to reach USD 30.01 Billion by 2034, exhibiting a CAGR of 10.45% during 2026-2034. Rising cancer incidence, expanding early detection initiatives, increasing adoption of targeted therapies, and supportive government programs are the primary drivers shaping market growth.

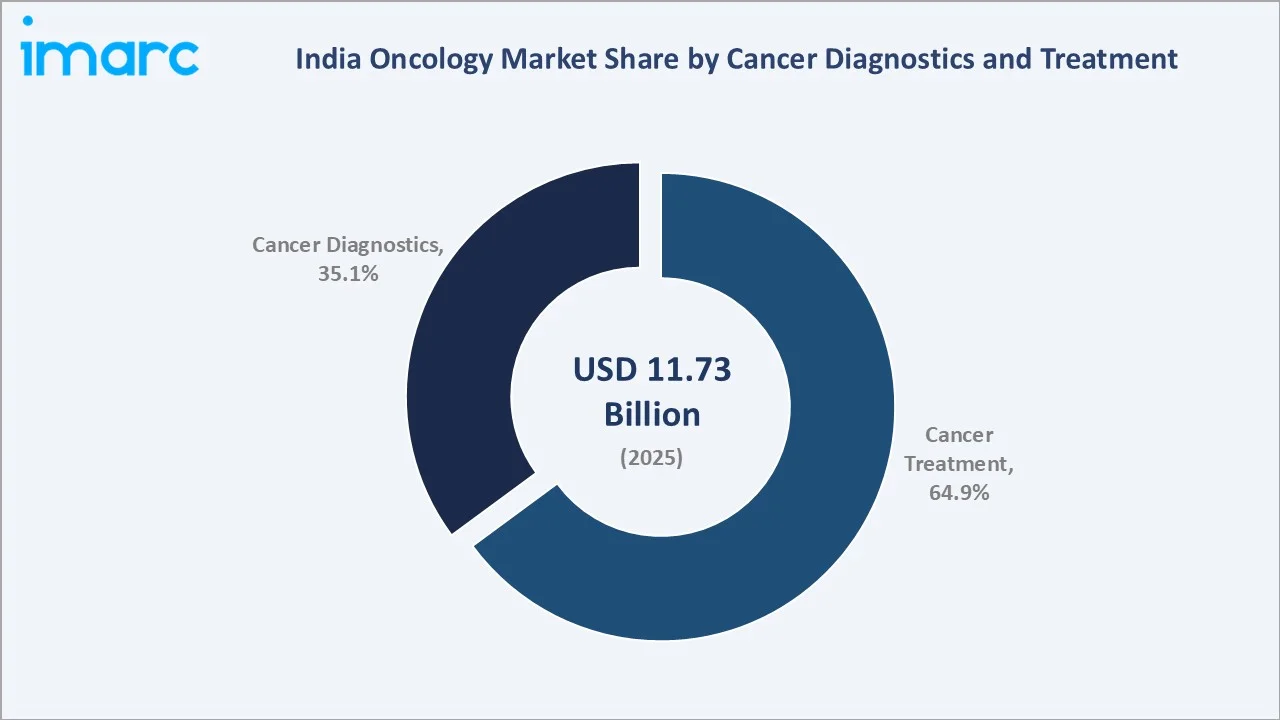

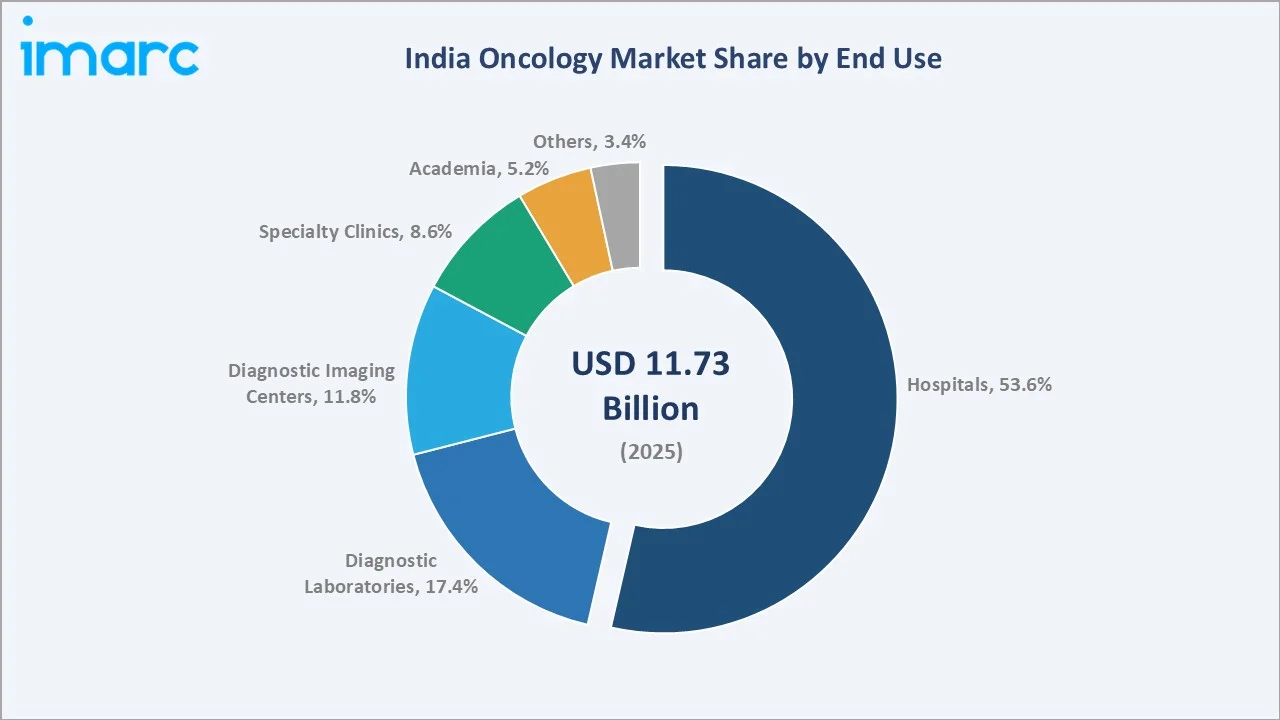

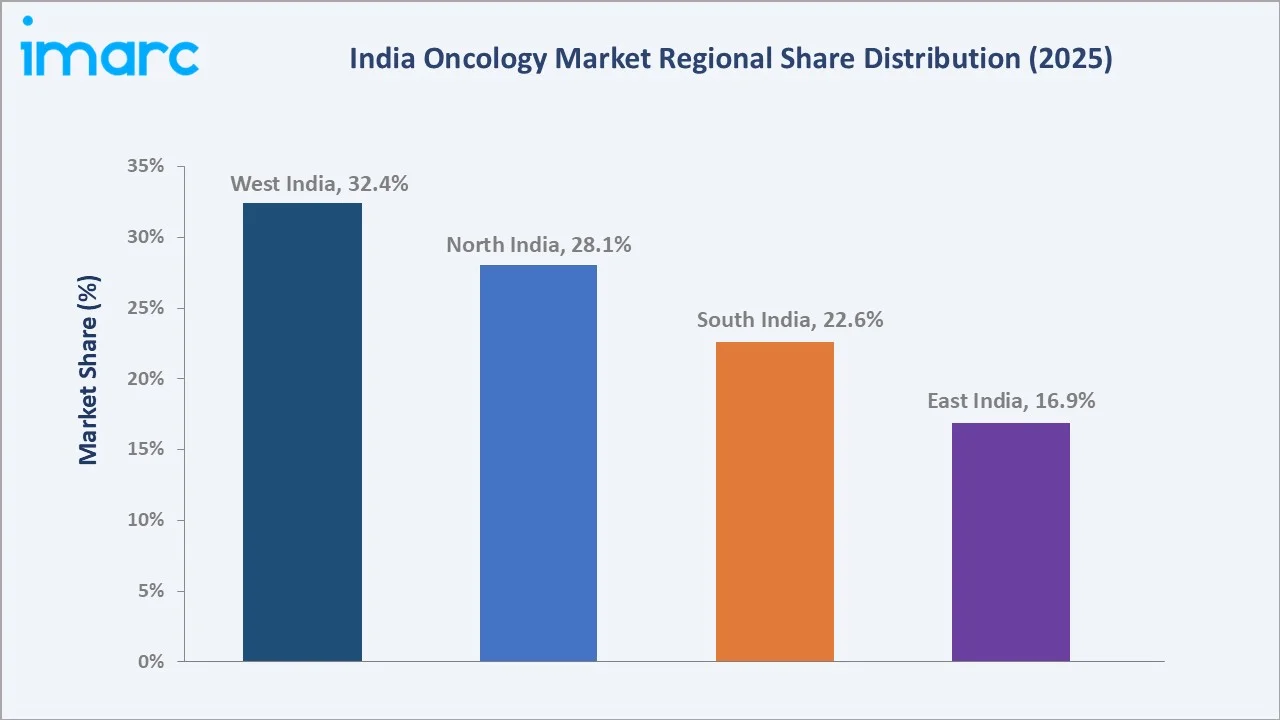

Cancer treatment leads the cancer diagnostics and treatment segment at 64.9% in 2025, while hospitals account for 53.6% of end use demand. West India commands the leading regional share at 32.4%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 11.73 Billion |

|

Forecast Market Size (2034) |

USD 30.01 Billion |

|

CAGR (2026-2034) |

10.45% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West India (32.4%, 2025) |

|

Fastest Growing Region |

East India (16.9%, 2025) |

|

Leading Cancer Diagnostics and Treatment Segment |

Cancer Treatment (64.9%, 2025) |

|

Leading End Use |

Hospitals (53.6%, 2025) |

The India oncology market expanded from USD 7.14 Billion in 2020 to USD 11.73 Billion in 2025, reflecting consistent growth driven by widening access to cancer care, rising awareness, and increasing healthcare expenditure. Anchored at USD 19.29 Billion in 2030, the forecast to USD 30.01 Billion by 2034 is supported by accelerating adoption of precision oncology, expansion of dedicated cancer centers in tier-2 cities, growing availability of biosimilar oncology drugs, and enhanced government-led cancer screening programs.

To get more information on this market, Request Sample

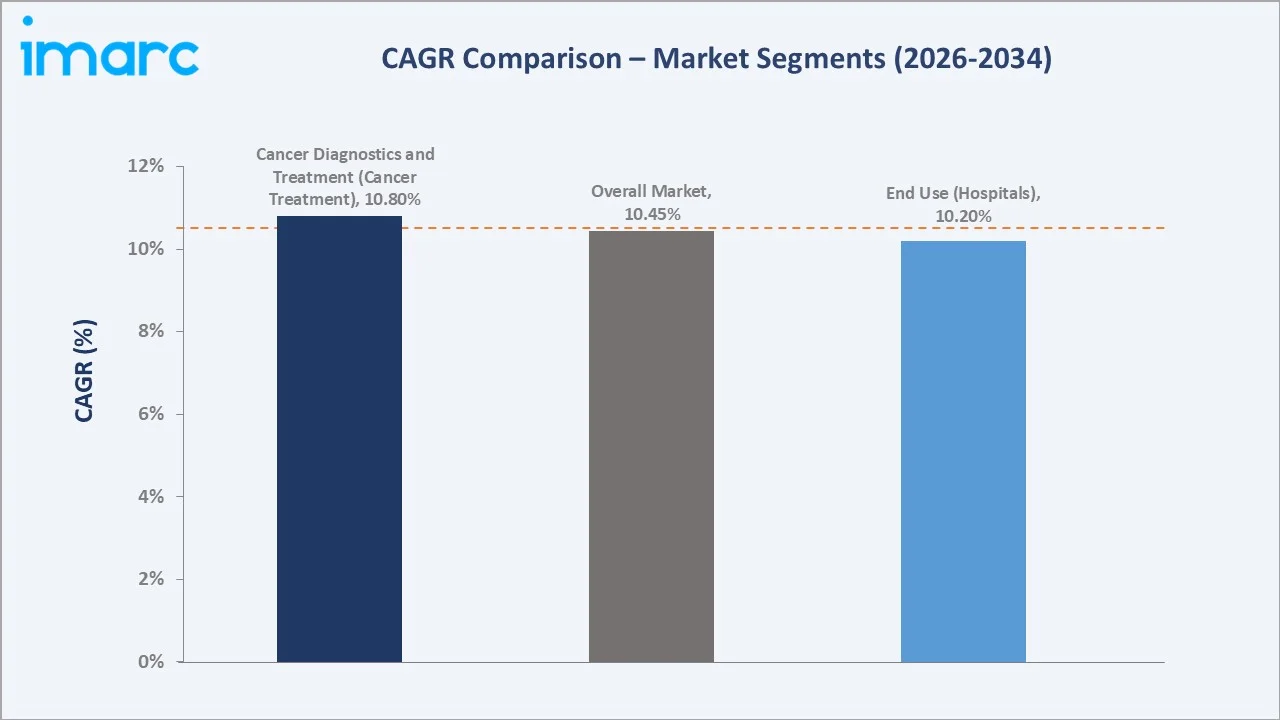

CAGR trajectories across the cancer diagnostics and treatment sub-segments indicate that cancer treatment is expanding faster than the overall market. Diagnostic laboratories are growing faster than the overall 10.45% market CAGR, driven by expanding early detection programs, AI-assisted screening tools, and rising insurance-led diagnostics demand across urban and semi-urban populations.

Executive Summary

The India oncology market is on a robust growth trajectory, expanding from USD 7.14 Billion in 2020 to a projected USD 30.01 Billion by 2034 at a CAGR of 10.45%. The market has evolved from a largely tertiary-care-driven, late-stage treatment model toward a more integrated ecosystem encompassing early detection, precision diagnostics, targeted drug therapy, immunotherapy, and survivorship care. Improved awareness, expanded health insurance coverage under PM-JAY, and growing private sector investment in dedicated cancer centers are reshaping the continuum of oncology care across India.

Cancer treatment dominates at 64.9% in 2025, supported by rising demand for chemotherapy, radiation therapy, immunotherapy, and surgical oncology services. India's cancer incidence rate increased from 84.8 (1990) to 107.2 (2023) per 100,000, requiring immediate intervention. Hospitals command 53.6% of end use demand, anchored by the concentration of multidisciplinary cancer care teams within large tertiary facilities. West India leads regional share at 32.4%, supported by Mumbai’s dense tertiary care network and Pune’s expanding life sciences ecosystem.

Key Market Insights

|

Insight |

Data |

|

Leading Cancer Diagnostics and Treatment Segment |

Cancer Treatment – 64.9% share (2025) |

|

Second Largest Cancer Diagnostics and Treatment Segment |

Cancer Diagnostics – 35.1% share (2025) |

|

Leading End Use |

Hospitals – 53.6% share (2025) |

|

Second Largest End Use |

Diagnostic Laboratories – 17.4% share (2025) |

|

Leading Region |

West India – 32.4% share (2025) |

|

Fastest Growing Region |

East India – 16.9% share (2025) |

|

Top Companies |

Apollo Hospitals, HealthCare Global Enterprises Limited, Max Healthcare, Cipla |

Key Analytical Observations Expanding On The Data Above:

- Cancer treatment dominance at 64.9% reflects strong demand across chemotherapy, radiation oncology, surgical oncology, and rapidly expanding immunotherapy and targeted therapy services. As per IMARC Group, the India cancer immunotherapy market size reached USD 4.4 Billion in 2025.

- Cancer diagnostics at 35.1% is supported by increasing uptake of PET-CT scans, next-generation sequencing, liquid biopsies, and AI-augmented radiology tools that are improving detection accuracy and enabling earlier clinical intervention.

- Hospitals leadership at 53.6% is anchored by the concentration of multidisciplinary oncology teams, advanced radiation equipment, and inpatient chemotherapy administration infrastructure within large tertiary care facilities.

- Diagnostic laboratories at 17.4% are growing steadily, driven by expansion of molecular diagnostics, genetic testing, and insurance-mandated pre-treatment workups that increasingly require specialized oncology lab capabilities.

- West India at 32.4% leads the regional landscape, anchored by Mumbai’s concentration of leading cancer hospitals and research institutions, Pune’s expanding oncology ecosystem, and the region’s high density of diagnostic imaging infrastructure.

India Oncology Market Overview

Oncology encompasses the prevention, diagnosis, and treatment of cancer through a broad range of modalities including medical oncology, radiation oncology, surgical oncology, and supportive care. The India oncology market spans cancer screening, molecular diagnostics, imaging, chemotherapy, targeted drug therapy, immunotherapy, bone marrow transplantation, and palliative care across public, private, and charitable healthcare institutions.

The Indian ecosystem integrates pharmaceutical manufacturers and biotech firms, medical device and equipment suppliers, hospital networks and specialty cancer centers, diagnostic laboratory chains, health insurance providers, government regulatory bodies, and national programs. Together, these actors define the delivery of oncology services within an evolving policy and technology landscape.

Market Dynamics

To evaluate market opportunities, Request Sample

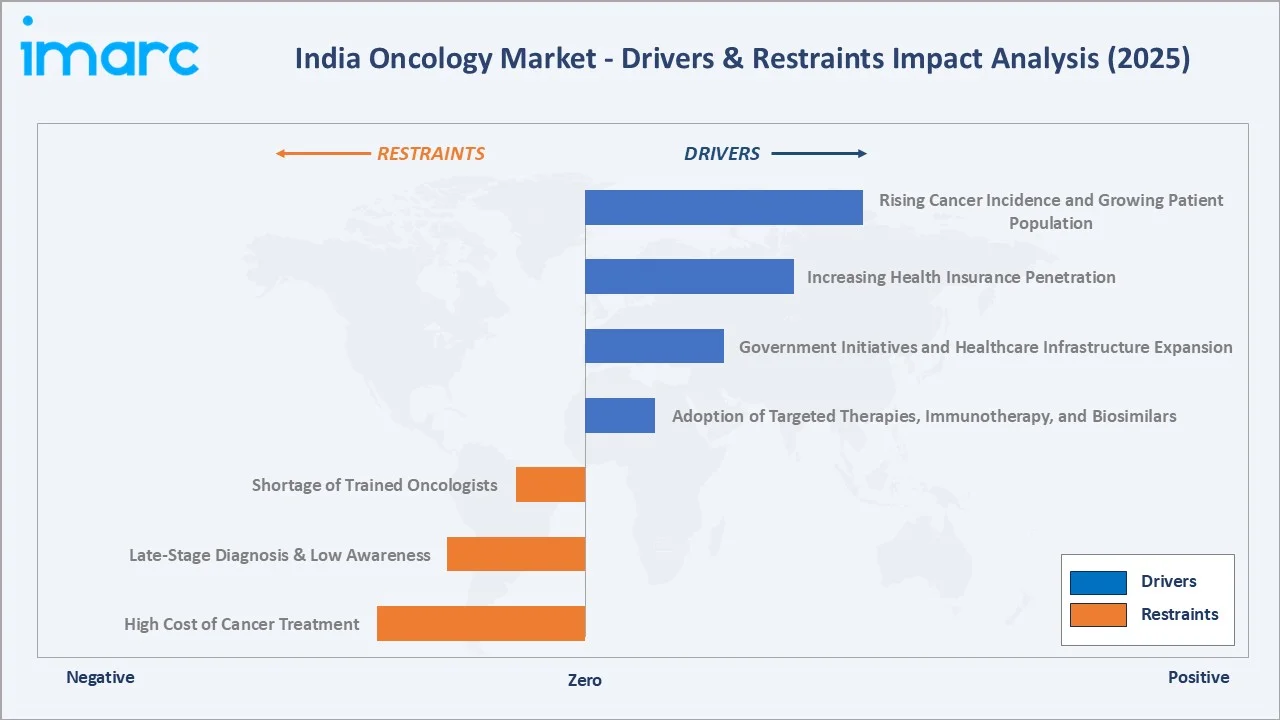

Market Drivers

- Rising Cancer Incidence and Growing Patient Population: India’s rapidly expanding and aging population, combined with changing lifestyle patterns, tobacco use, and environmental factors, is driving a structural increase in cancer incidence across multiple cancer types, sustaining consistent demand growth for both diagnostics and treatment services. As per PIB, the elderly population in India is expected to rise to approximately 230 Million by 2036, accounting for around 15% of the overall population.

- Government Initiatives and Healthcare Infrastructure Expansion: The National Cancer Grid and PM-JAY coverage for cancer treatment are expanding access to oncology care. Increasing investment in regional cancer centers, public hospital modernization, and diagnostic infrastructure is further improving treatment accessibility across tier-2 and tier-3 cities.

- Increasing Health Insurance Penetration: Expanding health insurance coverage through PM-JAY and private insurers is reducing the out-of-pocket burden for cancer treatment, enabling patients to seek timely care at private and semi-private healthcare institutions and driving increased utilization of diagnostics and treatment services.

- Adoption of Targeted Therapies, Immunotherapy, and Biosimilars: Growing clinical adoption of targeted cancer therapies, checkpoint inhibitors, and cost-effective biosimilar oncology drugs is expanding the addressable treatment market. Biosimilar versions of key oncology biologics are making advanced treatments accessible to a broader patient population, supporting both volume and value growth.

Market Restraints

- High Cost of Advanced Cancer Treatment: Advanced oncology modalities remain financially inaccessible for a large proportion of India’s population. High out-of-pocket healthcare expenditure and limited insurance penetration for specialized cancer therapies continue to restrict treatment adoption, particularly in lower-income and rural patient groups.

- Shortage of Trained Oncologists and Specialized Healthcare Professionals: India has a critically low density of trained medical oncologists, radiation oncologists, and oncology nurses relative to its cancer burden, limiting the capacity to diagnose and treat the growing patient population. This shortage is particularly acute in non-metropolitan areas and constrains the expansion of services beyond large tertiary hospitals.

- Late-Stage Diagnosis and Low Awareness in Rural Populations: A significant proportion of cancer cases in India are diagnosed at advanced stages due to limited awareness, insufficient screening infrastructure in rural areas, and poor access to diagnostic imaging and biopsy services. Late-stage diagnoses reduce treatment success rates and increase the economic burden of care.

Market Opportunities

- Expansion of Dedicated Cancer Centers and Diagnostic Networks in Tier-2 and Tier-3 Cities: Significant unmet demand exists in non-metropolitan areas where access to quality oncology diagnostics and treatment is limited. Operators who can establish scalable, asset-right models for cancer screening and treatment in these geographies stand to capture large, underserved patient populations.

- Digital Health, Telemedicine, and AI-Assisted Oncology Diagnostics: Adoption of AI for radiology image interpretation, pathology slide analysis, and treatment response prediction is creating significant opportunities for technology-led diagnostics firms and digital health platforms to improve diagnostic accuracy, speed, and accessibility across India’s tiered healthcare system.

- Biosimilar and Generic Oncology Drug Market: India’s strong pharmaceutical manufacturing base, combined with growing domestic demand for affordable cancer treatments, positions domestic pharmaceutical companies to expand their biosimilar and generic oncology portfolios and serve both domestic and export markets.

Market Challenges

- Regulatory Complexity and Drug Approval Timelines: Navigating CDSCO approval processes for new oncology drugs, biosimilars, and medical devices adds time and cost for market participants, delaying patient access to innovative therapies and complicating commercial planning for both domestic manufacturers and global multinationals.

- Infrastructure Gaps in Radiation Therapy and Advanced Diagnostics: The shortage of linear accelerators, PET-CT scanners, and molecular diagnostic labs outside metropolitan centers limits the ability to scale evidence-based cancer care, creating both a patient access challenge and a structural barrier to market growth in underserved regions.

Emerging Market Trends

1. Expansion of Government-Led Cancer Screening Programs

India’s national health programs are systematically extending cancer screening to primary and community health care levels, with oral, breast, and cervical cancer screening integrated into the NP-NCD framework. This is shifting clinical presentation toward earlier disease stages, improving treatment outcomes, and sustaining the long-term demand pipeline for both diagnostics and treatment services.

2. Adoption of Precision Oncology and Targeted Therapies

The growing availability of molecular diagnostics, next-generation sequencing, and companion diagnostics is enabling oncologists to deploy precision therapy protocols tailored to individual tumor biology. Targeted therapies and immunotherapy agents are becoming a larger component of treatment regimens, increasing the average revenue per patient episode and driving growth in both the treatment and diagnostics segments.

3. AI-Assisted Diagnostics and Digital Oncology Platforms

AI applications in radiology, digital pathology, and clinical decision support are being deployed across leading oncology centers and increasingly adopted by diagnostic laboratory chains. Under the Ayushman Bharat Digital Mission, the National Health Authority issued 500 Million Ayushman Bharat Health Account (ABHA) IDs as of January 2024, establishing the longitudinal digital health data infrastructure that is enabling AI-based cancer screening tools to reach tier-2 and tier-3 healthcare facilities with greater effectiveness.

4. Growth of Biosimilar and Affordable Oncology Drug Market

India’s pharmaceutical industry is rapidly expanding its biosimilar oncology portfolio, including biosimilar versions of trastuzumab, rituximab, and bevacizumab, significantly reducing the cost of biologic cancer treatment. This is broadening patient access to evidence-based therapy and expanding the oncology drug market beyond the branded segment, supporting volume-driven growth across the treatment segment.

5. Rising Private Investment in Dedicated Cancer Care Infrastructure

Private healthcare groups are increasingly investing in dedicated cancer hospitals, day-care chemotherapy centers, and linear accelerator facilities in tier-1 and tier-2 cities. The shift from general hospital oncology wards to specialized cancer care infrastructure is improving clinical outcomes, increasing throughput capacity, and supporting quality-driven market premiumization within the treatment segment.

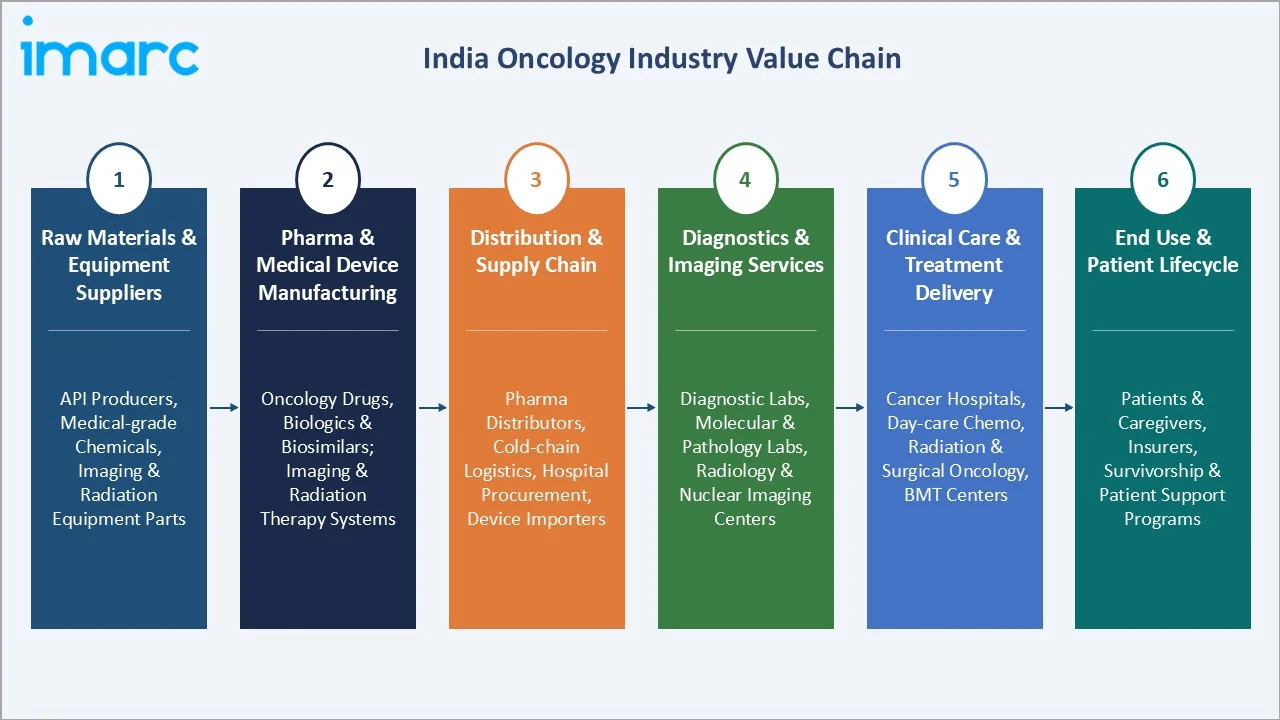

Industry Value Chain Analysis

The India oncology value chain spans six stages from raw material and equipment supply through end user patient care and lifecycle management. Pharmaceutical manufacturing, clinical care delivery, and diagnostics infrastructure capture the highest value-add, while digital health platforms, AI diagnostics, and patient support services are rapidly growing in strategic importance.

|

Stage |

Key Players / Examples |

|

Raw Materials & Equipment Suppliers |

Active pharmaceutical ingredient (API) producers, medical grade chemical suppliers, linear accelerator component manufacturers, imaging equipment parts suppliers, and radiation source providers supporting oncology infrastructure |

|

Pharmaceutical & Medical Device Manufacturing |

Domestic and multinational pharmaceutical companies producing oncology drugs, biologics, and biosimilars; medical device firms manufacturing imaging equipment, radiation therapy systems, biopsy tools, and laboratory diagnostics instruments |

|

Distribution & Supply Chain |

Pharmaceutical wholesale distributors, cold-chain logistics providers for biologics, hospital procurement services, and medical device importers and distributors managing delivery to healthcare facilities across India |

|

Diagnostics & Imaging Services |

Standalone diagnostic laboratory chains, hospital-integrated diagnostic departments, molecular diagnostics labs, radiology and nuclear medicine imaging centers, and pathology service providers |

|

Clinical Care & Treatment Delivery |

Oncology hospitals, dedicated cancer centers, day-care chemotherapy facilities, radiation therapy centers, surgical oncology units, bone marrow transplant centers, and palliative care providers |

|

End Use & Patient Lifecycle |

Cancer patients and caregivers, health insurance providers, patient support organizations, survivorship and rehabilitation programs, and grievance and outcomes monitoring mechanisms |

Vertically integrated players owning proprietary diagnostic infrastructure, treatment delivery capacity, and pharmaceutical distribution relationships are positioned to capture greater value across the oncology care continuum.

Technology Landscape in the India Oncology Industry

Molecular Diagnostics and Next-Generation Sequencing

Advanced molecular diagnostic platforms, including polymerase chain reaction (PCR), fluorescence in situ hybridization (FISH), and next-generation sequencing (NGS), are being increasingly deployed by leading diagnostic laboratories and cancer centers. These technologies enable precise tumor profiling, companion diagnostic matching for targeted therapies, and identification of hereditary cancer risk, supporting more personalized and effective treatment planning.

Radiation Therapy Technology

Modern radiotherapy modalities including intensity-modulated radiation therapy (IMRT), volumetric arc therapy (VMAT), stereotactic radiosurgery (SRS), and image-guided radiation therapy (IGRT) are improving treatment precision and reducing collateral tissue damage. Investment in linear accelerator fleets is expanding among leading hospital networks, with AI-driven treatment planning systems further enhancing clinical workflow efficiency.

AI and Digital Pathology

AI and machine learning (ML) models are being deployed for radiology image interpretation, digital pathology slide analysis, clinical decision support, and patient risk stratification. These tools are reducing diagnostic variability, shortening time-to-diagnosis, and enabling pathologists and radiologists in smaller facilities to access specialist-level analytical support through cloud-based platforms.

Immunotherapy and Targeted Drug Delivery

Checkpoint inhibitor therapies, CAR-T cell therapy, and antibody-drug conjugates represent the frontier of oncology treatment technology. While global innovation is led by multinational pharmaceutical companies, Indian manufacturers are advancing in the development and production of biosimilar versions of key oncology biologics, making advanced drug delivery accessible to a broader segment of the Indian patient population.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Cancer Diagnostics and Treatment |

Cancer Treatment |

64.9% |

2025 |

|

Cancer Type |

Lung Cancer |

18.7% |

2025 |

|

End Use |

Hospitals |

53.6% |

2025 |

|

Region |

West India |

32.4% |

2025 |

By Cancer Diagnostics and Treatment

Cancer treatment commands a 64.9% majority share in 2025, driven by rising demand for chemotherapy, radiation therapy, surgical oncology, targeted drug therapy, and rapidly expanding immunotherapy services. The treatment segment benefits from increasing insurance coverage, growing adoption of high-value targeted and biologic therapies, and ongoing investment in dedicated cancer care infrastructure by both public and private healthcare providers.

To access detailed market analysis, Request Sample

Cancer diagnostics at 35.1% in 2025 encompasses imaging, pathology, molecular diagnostics, and genetic testing services. The diagnostics segment is growing steadily, supported by expanding early detection mandates, increasing adoption of AI-assisted radiology and digital pathology, rising insurance-led pre-treatment diagnostic workups, and growing availability of molecular diagnostic panels in standalone laboratory settings.

By End Use

Hospitals dominate with a 53.6% share in 2025, anchored by the concentration of multidisciplinary oncology teams, advanced radiation equipment, inpatient chemotherapy administration capacity, and surgical oncology infrastructure within large tertiary and quaternary care facilities. Hospitals serve as the primary point of care for the majority of cancer diagnoses and treatment episodes in India.

Diagnostic laboratories hold a 17.4% share, supported by rapid expansion of molecular and genetic testing demand. Growing adoption of AI-assisted diagnostics, liquid biopsy technologies, and preventive cancer screening programs is further strengthening demand for advanced laboratory services across urban healthcare networks.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

West India |

32.4% |

High concentration of tertiary oncology hospitals, strong pharmaceutical and biotech manufacturing base, dense diagnostic infrastructure, and large insured urban population driving demand for quality cancer care |

|

North India |

28.1% |

Large urban population base, strong government hospital network, growing private oncology investment in Delhi-NCR, expanding health insurance penetration, and rising cancer awareness and screening participation |

|

South India |

22.6% |

Well-developed healthcare infrastructure, expanding IT-sector-driven insured workforce, strong medical tourism oncology segment, growing adoption of precision diagnostics, and established teaching hospital oncology programs |

|

East India |

16.9% |

Emerging digital health adoption, growing government investment in healthcare infrastructure, expanding access to diagnostics and cancer screening, rising middle-class health expenditure, and increasing awareness campaigns |

West India at 32.4% in 2025 leads the regional landscape, anchored by Mumbai’s dense concentration of leading oncology hospitals and multiple private cancer centers, along with Pune’s expanding pharmaceutical and biotechnology ecosystem. The region’s high proportion of insured urban consumers, strong diagnostic network, and proximity to pharma manufacturing hubs create a self-reinforcing growth environment.

North India at 28.1% represents the second-largest region, driven by Delhi-NCR’s concentration of private and government tertiary cancer care institutions, Uttar Pradesh’s large catchment population, and the expanding oncology services in Chandigarh’s Post Graduate Institute and other regional centers.

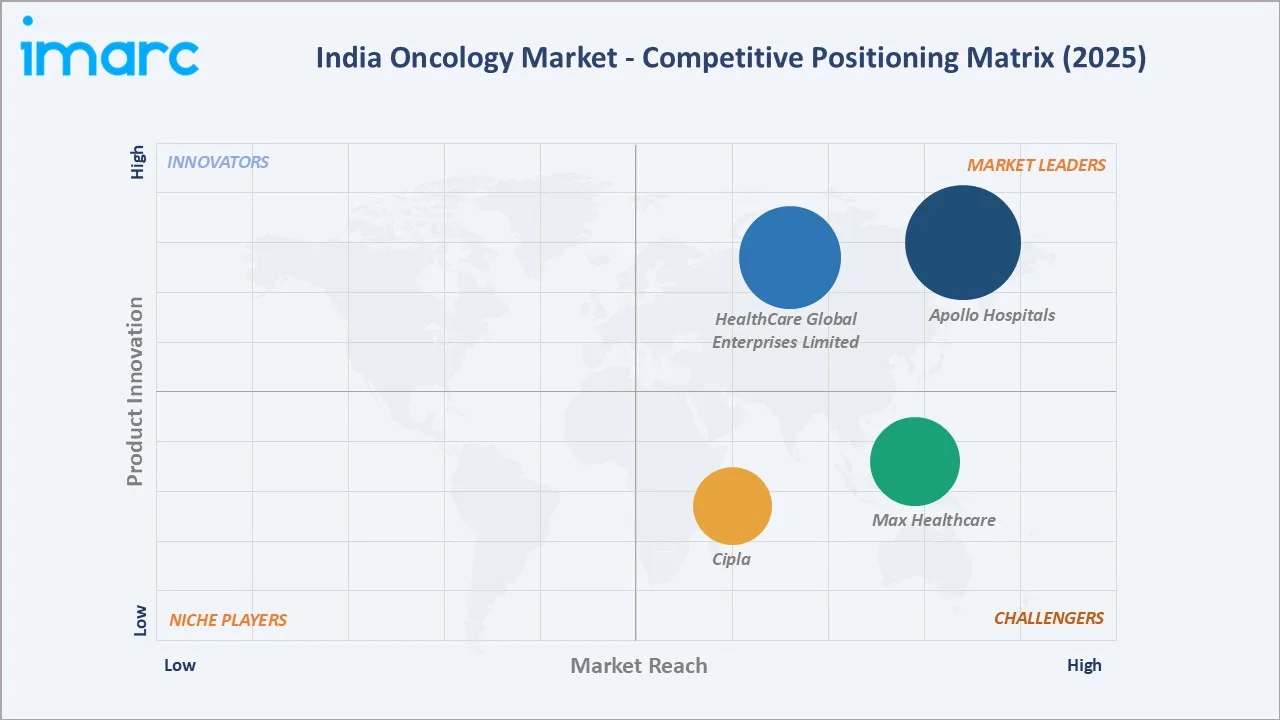

Competitive Landscape

The India oncology market is moderately fragmented, with large hospital-based cancer care networks, specialty oncology chains, and pharmaceutical companies competing across diagnostics, treatment, and drug supply dimensions. Clinical excellence, technology investment, geographic network depth, pharmaceutical portfolio breadth, and regulatory compliance capability form the key competitive differentiators across the market.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

| Apollo Hospitals | Apollo Cancer Centres |

Leader |

Expanding multi-city cancer care network with integrated diagnostics, surgery, radiation, and medical oncology services |

| HealthCare Global Enterprises Limited | HCG Cancer Centres |

Leader |

Growing dedicated oncology network across tier-1 and tier-2 cities with specialized technology and molecular diagnostics |

| Max Healthcare | Max Institute of Cancer Care | Challenger | Building comprehensive cancer care capability in North India through integrated clinical and diagnostic oncology services |

| Cipla | Cipla Oncology Portfolio (including more than 32 drugs) | Challenger | Expanding oncology generics and specialty drug portfolio with focus on accessible and affordable cancer therapeutics |

Key players include Apollo Hospitals, HealthCare Global Enterprises Limited, Max Healthcare, and Cipla, among others.

Key Company Profiles

Apollo Hospitals

Apollo Hospitals is one of India’s largest integrated private healthcare organizations, operating a wide network of hospitals, clinics, diagnostic centers, and pharmacies across major cities in India. The group is widely recognized as a pioneer in organized private healthcare delivery and provides a broad range of clinical specialties, with oncology forming a strategically significant and growing component of its clinical services portfolio.

- Product Portfolio: Apollo Cancer Centres provides comprehensive cancer care services across medical oncology, surgical oncology, and radiation oncology, supported by advanced imaging, PET-CT diagnostics, tumor board-based treatment planning, targeted therapy, immunotherapy, and palliative care. The network integrates advanced radiation therapy equipment and precision oncology tools across its multi-city footprint.

- Recent Developments: Apollo Hospitals launched Apollo Athenaa in Delhi in 2025, Asia’s first dedicated cancer center exclusively for women, integrating gender-specific oncology care across diagnostics, surgery, and treatment.

- Strategic Focus: Expanding the Apollo Cancer Centres network to new geographies, advancing precision and proton oncology capabilities, and integrating digital health and AI-assisted tools into the oncology care pathway to improve clinical outcomes and patient access across tier-1 and tier-2 cities.

HealthCare Global Enterprises Limited

HealthCare Global Enterprises Limited is a dedicated cancer care hospital network headquartered in Bengaluru, operating as India’s largest specialized oncology hospital chain. The company focuses exclusively on cancer care and operates a network of comprehensive cancer centers across multiple cities in India, delivering a full spectrum of oncology services from diagnostics through treatment and supportive care.

- Product Portfolio: HCG Cancer Centres offer end-to-end oncology services encompassing radiation therapy, medical oncology, surgical oncology, hematology, bone marrow transplantation, nuclear medicine, PET-CT diagnostics, and molecular diagnostics. The network deploys advanced radiation therapy equipment including linear accelerators and provides specialized cancer care services across a broad range of cancer types.

- Recent Developments: The company has continued to expand its dedicated cancer care network across India, adding centers in emerging geographies and investing in advanced oncology technology and specialized clinical programs to strengthen its position as the country’s leading dedicated oncology provider.

- Strategic Focus: Expanding its dedicated oncology network to tier-1 and tier-2 cities, advancing clinical capabilities in precision oncology and molecular diagnostics, and improving access to specialized cancer care across a broader geographic footprint within India.

Max Healthcare

Max Healthcare is one of India’s leading private hospital networks, operating a chain of hospitals primarily across North India. The company delivers oncology services through the Max Institute of Cancer Care, which serves a large and growing patient population across multiple hospital locations in the Delhi-NCR region and select markets beyond.

- Product Portfolio: Max Institute of Cancer Care provides comprehensive oncology services including medical oncology, radiation oncology, surgical oncology, hematology, and bone marrow transplantation, supported by in-house molecular diagnostics and organ-specific disease management groups with multidisciplinary tumor board-based treatment planning.

- Recent Developments: The company has continued to strengthen its oncology program by expanding the Max Institute of Cancer Care across additional hospital locations, investing in advanced radiation oncology infrastructure, and enhancing specialized cancer care capabilities across its growing hospital network.

- Strategic Focus: Building comprehensive cancer care capability across its North India hospital network through multidisciplinary service delivery, advanced oncology infrastructure investment, and expansion of the Max Institute of Cancer Care to serve a wider geographic patient base.

Market Concentration Analysis

The India oncology market is moderately concentrated, with the top players, including Apollo Hospitals, HealthCare Global Enterprises Limited, Max Healthcare, and Cipla, accounting for a significant share of specialty oncology treatment capacity.

Barriers to entry at the hospital level are high, requiring significant capital investment in radiation oncology equipment, multidisciplinary clinical teams, diagnostic infrastructure, and regulatory approvals. In the pharmaceutical segment, barriers are moderate for generics but high for biosimilars, given the regulatory, manufacturing, and clinical validation requirements. These structural dynamics favor well-capitalized incumbents with established clinical reputations, hospital network scale, and proven drug manufacturing capabilities.

Consolidation is gradually accelerating in the hospital segment as private equity-backed oncology networks acquire smaller specialty centers and as multi-specialty hospital groups invest in upgrading and expanding their oncology divisions. In the pharma segment, in-licensing, strategic alliances, and targeted acquisitions of oncology drug assets are reshaping competitive positioning among the top domestic manufacturers.

Investment & Growth Opportunities

Fastest-Growing Segments

Cancer diagnostics at 35.1% is growing faster than the overall market, supported by precision medicine adoption, insurance-mandated pre-treatment workups, and the expansion of genetic testing. Within end use, diagnostic laboratories at 17.4% in 2025 are on an above-average growth trajectory, driven by outsourcing of specialized cancer diagnostic workups from hospitals to accredited standalone labs.

Emerging Markets

East India at 16.9% regional share in 2025 represents the highest incremental growth opportunity, anchored by rising government infrastructure investment, increasing cancer awareness, and a large, underserved urban and semi-urban population in states, including West Bengal, Odisha, and the Northeast. Tier-2 and tier-3 cities across all regions represent significant untapped demand for investors and operators willing to build right-sized oncology delivery models.

Investment & Venture Trends

Investment is concentrated in digital health platforms for oncology patient management, AI-based diagnostics start-ups, biosimilar pharmaceutical manufacturing, and expansion of day-care chemotherapy and radiation therapy infrastructure in underserved geographies. Private equity and strategic investors are increasingly targeting oncology-specific platforms, diagnostic chains, and pharmaceutical assets with differentiated cancer therapy portfolios.

Future Market Outlook (2026-2034)

The India oncology market is forecast to expand from USD 11.73 Billion in 2025 to USD 30.01 Billion by 2034 at a CAGR of 10.45%, adding approximately USD 18.28 Billion in incremental annual market value over the forecast period. The market is expected to pass USD 19.29 Billion by 2030, reflecting sustained above-average healthcare expenditure growth driven by rising cancer incidence and expanding access to care.

Four forces will shape the market through 2034: a strengthening national oncology policy framework anchored by PM-JAY, the National Cancer Grid, and enhanced NP-NCD screening programs; the rise of precision oncology, immunotherapy, and biosimilar drug therapy; deeper integration of AI-assisted diagnostics, digital pathology, and telemedicine in the oncology care pathway; and accelerating investment in dedicated cancer care infrastructure beyond the major metropolitan centers.

By 2034, India’s oncology market is expected to be defined by earlier-stage diagnosis, personalized treatment protocols, and a more equitable geographic distribution of quality cancer care. Pharmaceutical innovation in biosimilars and targeted therapies will continue to expand accessible treatment options, while technology-driven efficiency gains in diagnostics will reduce the cost of early detection, collectively supporting a structurally favorable long-term growth outlook.

Research Methodology

Primary Research

Primary research included structured interviews with hospital-based oncologists, radiation oncology specialists, pharmaceutical company executives, diagnostic laboratory chain leaders, health insurance executives, and government health program officials. These conversations validated market sizing, segment mix, regional demand patterns, technology adoption trends, and competitive positioning assessments.

Secondary Research

Secondary sources included Indian Council of Medical Research (ICMR) and National Cancer Registry Programme (NCRP) cancer incidence data, Ministry of Health and Family Welfare program documents, National Health Authority publications, Central Drugs Standard Control Organization (CDSCO) drug approval data, annual reports and investor presentations from key listed healthcare and pharmaceutical companies, and publicly available clinical guidelines and health policy documents.

Forecasting Models

Market forecasts used a combination of top-down and bottom-up models integrating cancer incidence projections, healthcare expenditure per cancer patient, segment mix evolution, government program funding trends, technology adoption curves, and macroeconomic variables including GDP growth and health expenditure ratios. Scenario analysis addressed regulatory changes, biosimilar penetration rates, and infrastructure investment pacing.

India Oncology Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Cancer Diagnostics and Treatments Covered |

|

|

Cancer Types Covered |

Lung Cancer, Prostate Cancer, Colon and Rectal Cancer, Gastric Cancer, Esophageal Cancer, Liver Cancer, Breast Cancer, Others |

|

End Uses Covered |

Hospitals, Diagnostic Laboratories, Diagnostic Imaging Centers, Academia, Specialty Clinics, Others |

|

Regions Covered |

North India, South India, East India, West India |

|

Companies Covered |

Apollo Hospitals, HealthCare Global Enterprises Limited, Max Healthcare, Cipla, etc. |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Oncology Market Report

The India oncology market was valued at USD 11.73 Billion in 2025, driven by rising cancer incidence, expanding cancer care infrastructure, growing health insurance penetration, and increasing adoption of targeted therapies and diagnostic innovations.

The market is projected to grow at a CAGR of 10.45% from 2026 to 2034, reaching USD 30.01 Billion, supported by precision medicine adoption, biosimilar expansion, and strengthening government-led cancer screening and treatment programs.

Cancer treatment leads at 64.9% in 2025, fueled by strong demand for chemotherapy, radiation therapy, surgical oncology, targeted drug therapy, and immunotherapy services across hospital-based cancer care networks.

Hospitals command 53.6% of the market in 2025, anchored by their concentration of multidisciplinary oncology teams, advanced radiation equipment, and comprehensive inpatient cancer treatment delivery capability.

West India commands 32.4% regional share in 2025, led by Mumbai's dense tertiary oncology hospital network, Pune's pharmaceutical ecosystem, and the region's high concentration of insured, urban healthcare consumers.

Leading players include Apollo Hospitals, HealthCare Global Enterprises Limited, Max Healthcare, and Cipla, among others.

Cancer diagnostics growth is driven by early detection mandates, expanding molecular and genetic testing, AI-augmented radiology adoption, rising insurance-led pre-treatment workups, and increasing deployment of PET-CT and digital pathology platforms.

Biosimilar oncology drugs are expanding treatment access by reducing per-patient drug costs for key biologic therapies, enabling broader patient populations to receive evidence-based cancer treatment beyond premium branded biologics.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)