India Online Education Market Size, Share, Trends and Forecast by Type, Provider, Technology, End-User, and Region, 2026-2034

India Online Education Market Size, Share, Trends & Forecast (2026-2034)

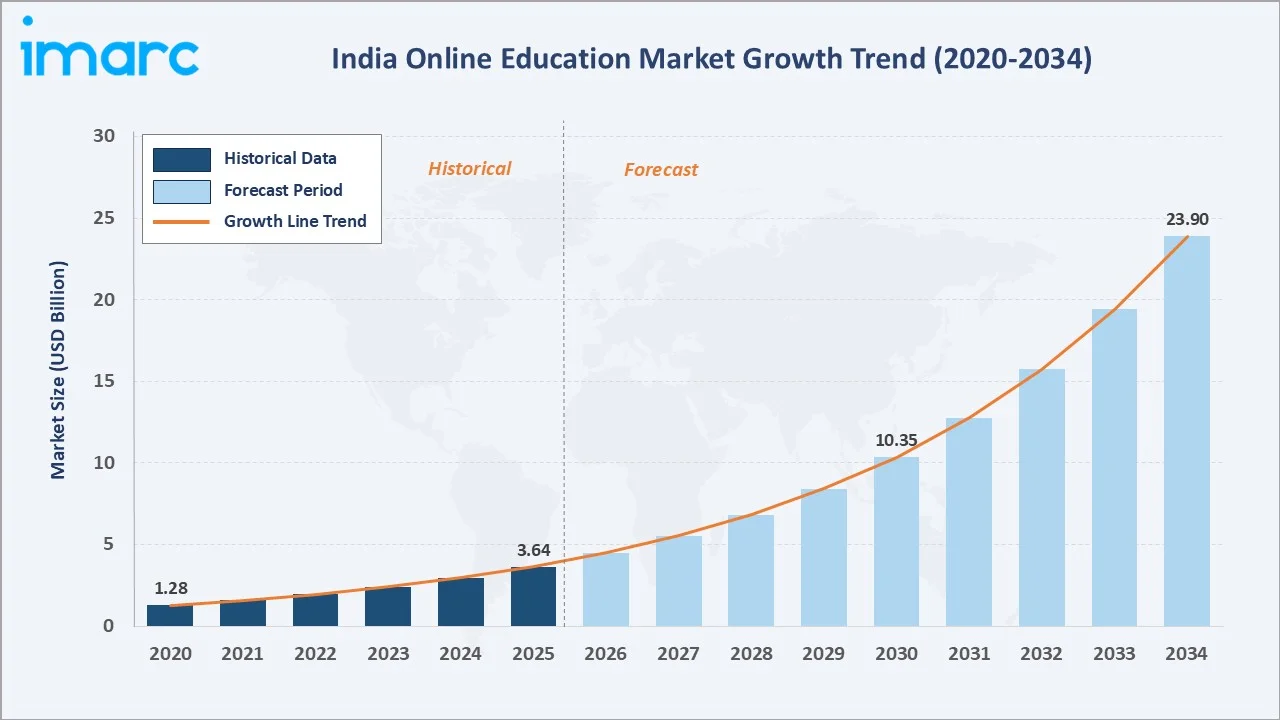

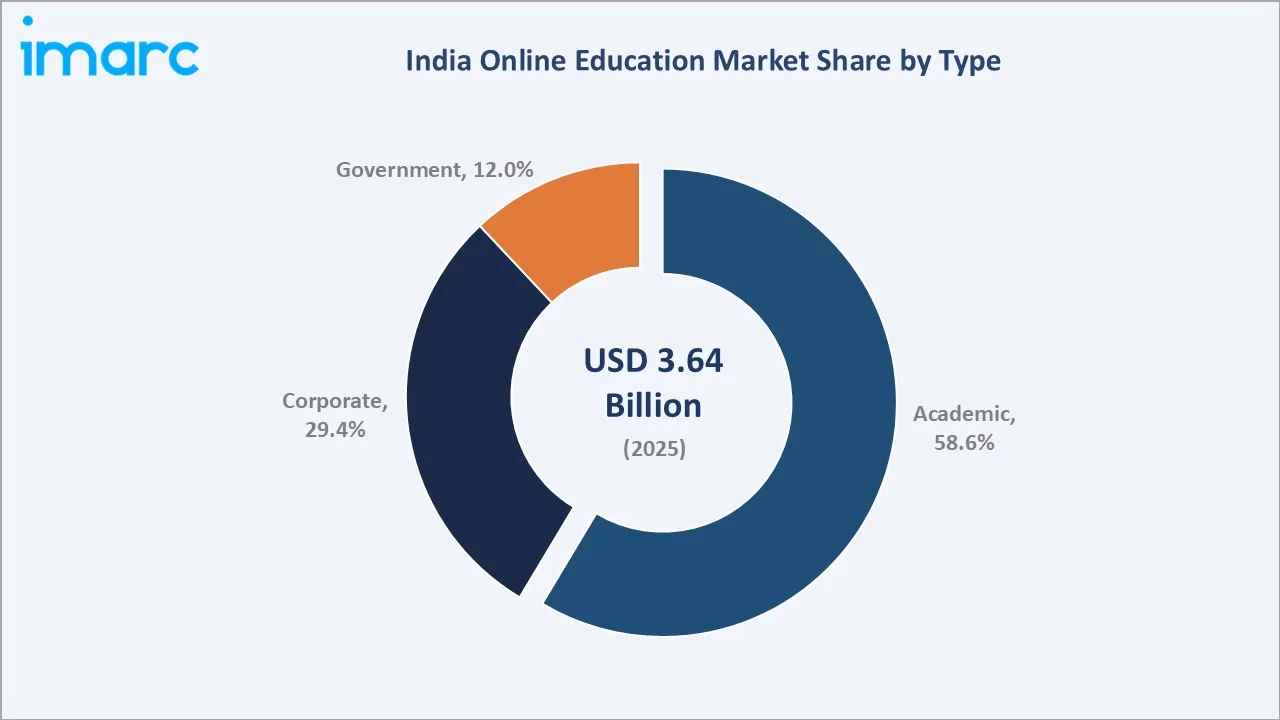

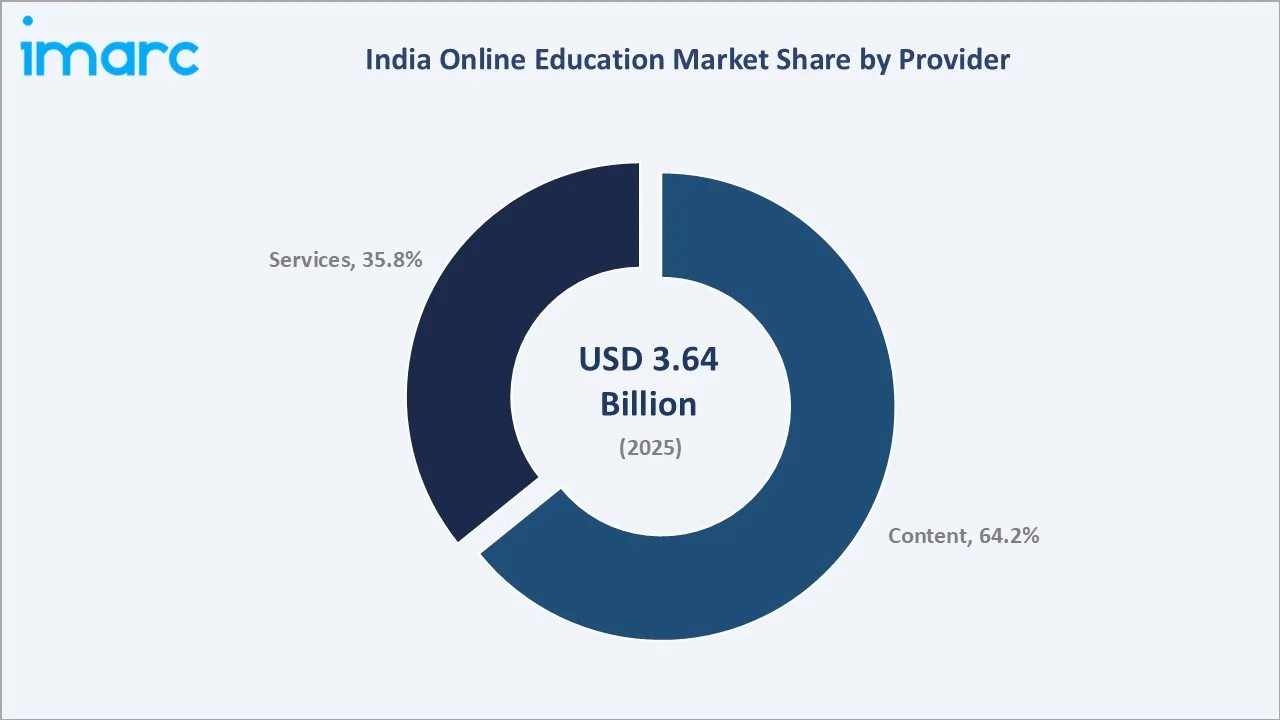

The India online education market size was valued at USD 3.64 Billion in 2025 and is projected to reach USD 23.90 Billion by 2034, exhibiting a CAGR of 23.28% during the forecast period 2026-2034. Surging smartphone penetration, affordable internet access, government-backed digital learning programs, and rapidly evolving EdTech platforms are driving online education market growth in India.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.64 Billion |

|

Forecast Market Size (2034) |

USD 23.90 Billion |

|

CAGR (2026-2034) |

23.28% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

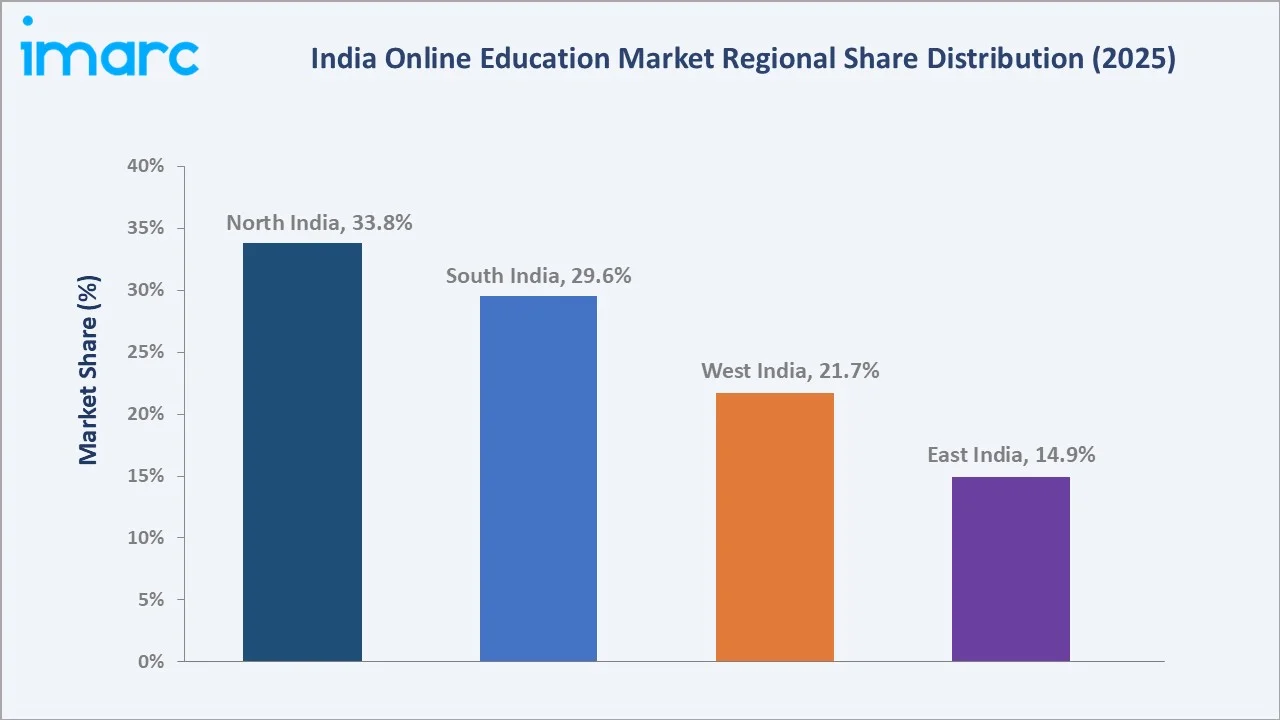

North India (33.8% share, 2025) |

|

Fastest Growing Region |

North India (CAGR ~25.1%) |

|

Leading Type |

Academic (58.6%, 2025) |

|

Leading Provider |

Content (64.2%, 2025) |

The India online education market growth trajectory from 2020 through 2034 reflects historical acceleration post-COVID-19 against a sustained forecast curve powered by EdTech expansion, NEP 2020 digital mandates, rising corporate upskilling demand, and mobile-first learning adoption across Tier-2 and Tier-3 cities.

To get more information on this market, Request Sample

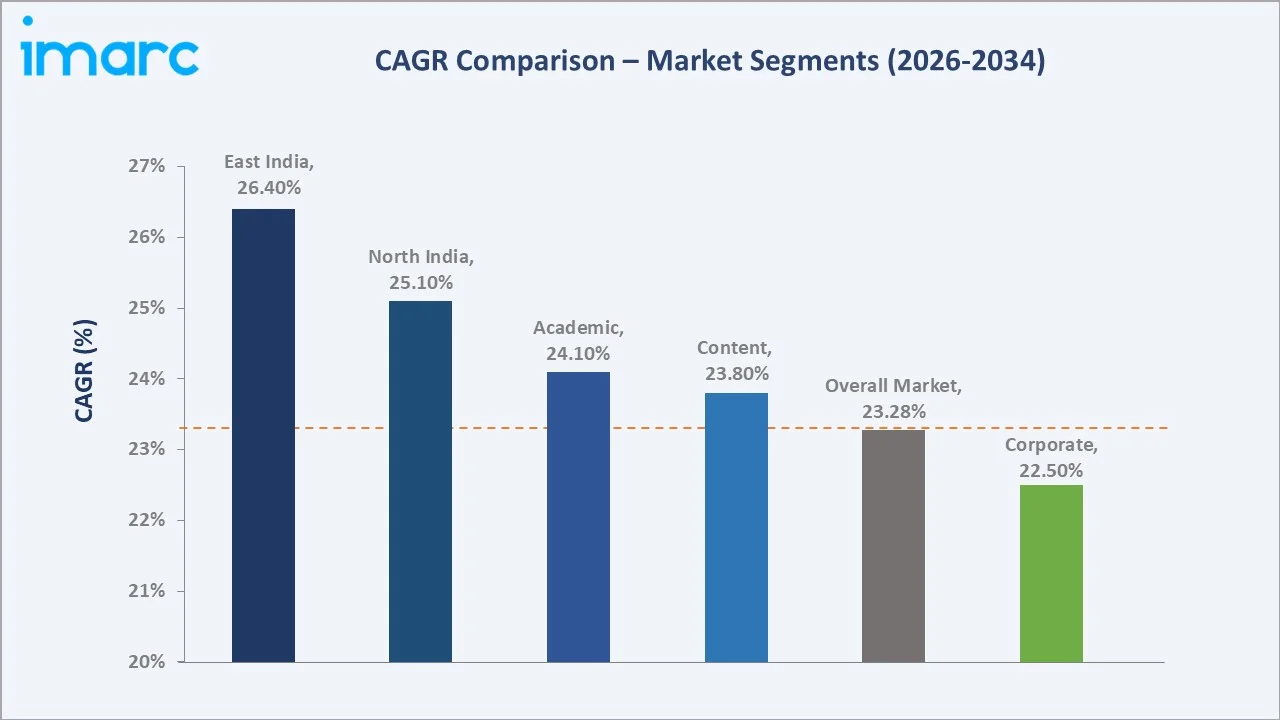

Segment-level CAGR comparisons highlight the academic provider segment and North India region as the fastest-growing sub-categories within the India online education market forecast through 2034, driven by test-preparation culture, NEP 2020 reforms, and digital infrastructure investments.

Executive Summary

The India online education sector is undergoing structural transformation. It is driven by mobile connectivity expansion, regulatory support, and shifting learner expectations. Valued at USD 3.64 Billion in 2025, the market is projected to reach USD 23.90 Billion by 2034 at a CAGR of 23.28%, positioning India as one of the fastest-growing EdTech destinations globally.

Academic applications command 58.6% share in 2025, underpinned by K-12 supplementary learning, higher education online programs, and exam preparation for JEE, NEET, and UPSC. The corporate segment holds 29.4%, expanding rapidly as enterprises invest in upskilling programs for digital transformation readiness. Content providers represent 64.2% of provider revenue, reflecting high learner preference for structured, curated digital content versus standalone services.

North India leads all regions with 33.8% market share in 2025, driven by Delhi NCR's high student density and strong test-prep culture. The online education market outlook remains highly positive as government programs such as PM eVidya, SWAYAM, and DIKSHA, combined with private EdTech innovation, converge to expand addressable learner populations beyond metropolitan centers into Tier-2 and Tier-3 cities across all regions of India.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Academic – 58.6% share (2025) |

|

Second Type |

Corporate – 29.4% share (2025) |

|

Largest Provider |

Content – 64.2% share (2025) |

|

Leading Region |

North India – 33.8% revenue share (2025) |

|

Top Companies |

Sorting Hat Technologies Pvt Ltd, upGrad, Physicswallah Limited, Vedantu.com, Simplilearn Solutions, Great Learning Education Services Private Limited., NIIT, Coursera Inc., Extramarks |

|

Market Opportunity |

Tier-2/3 city learner base; 806 million internet users (2025) |

Key Analytical Observations Supporting the Above Data:

- Academic segment's 58.6% dominance in 2025 reflects the intense competitive exam culture in India, driving sustained demand for online test-prep content.

- Corporate segment's 29.4% share is anchored by enterprise-level reskilling mandates, with numerous large companies integrating digital learning platforms into their employee development frameworks.

- Content providers' 64.2% majority is learner preference for structured, exam-aligned, and skills-focused content libraries, particularly in vernacular languages reaching non-English-speaking learner populations.

- North India's 33.8% regional leadership reflects the Delhi NCR metro cluster, large population base, and high concentration of competitive exam aspirants from coaching hubs transitioning to online formats.

- Mobile e-learning is the dominant delivery mode, supported by widespread internet and smartphone penetration, enabling anytime-anywhere access to learning platforms, especially in rural and semi-urban areas.

India Online Education Market Overview

Online education in India encompasses the delivery of structured learning content, certification programs, and skill development courses through digital platforms, mobile applications, and virtual classrooms. The market spans a comprehensive portfolio including K-12 supplementary learning, higher education degree programs, competitive exam preparation, professional upskilling, corporate training, and government employee development. These solutions are delivered via content-centric platforms, live instructor-led virtual classrooms, mobile e-learning apps, and AI-driven adaptive learning systems.

The industry operates at the intersection of technology innovation, regulatory reform, and demographic opportunity. Macroeconomic drivers include the National Education Policy 2020 mandating digital integration, government initiatives such as DIKSHA and PM eVidya expanding access, rising household internet penetration, and increasing corporate investment in workforce upskilling for digital economy readiness.

Market Dynamics

To evaluate market opportunities, Request Sample

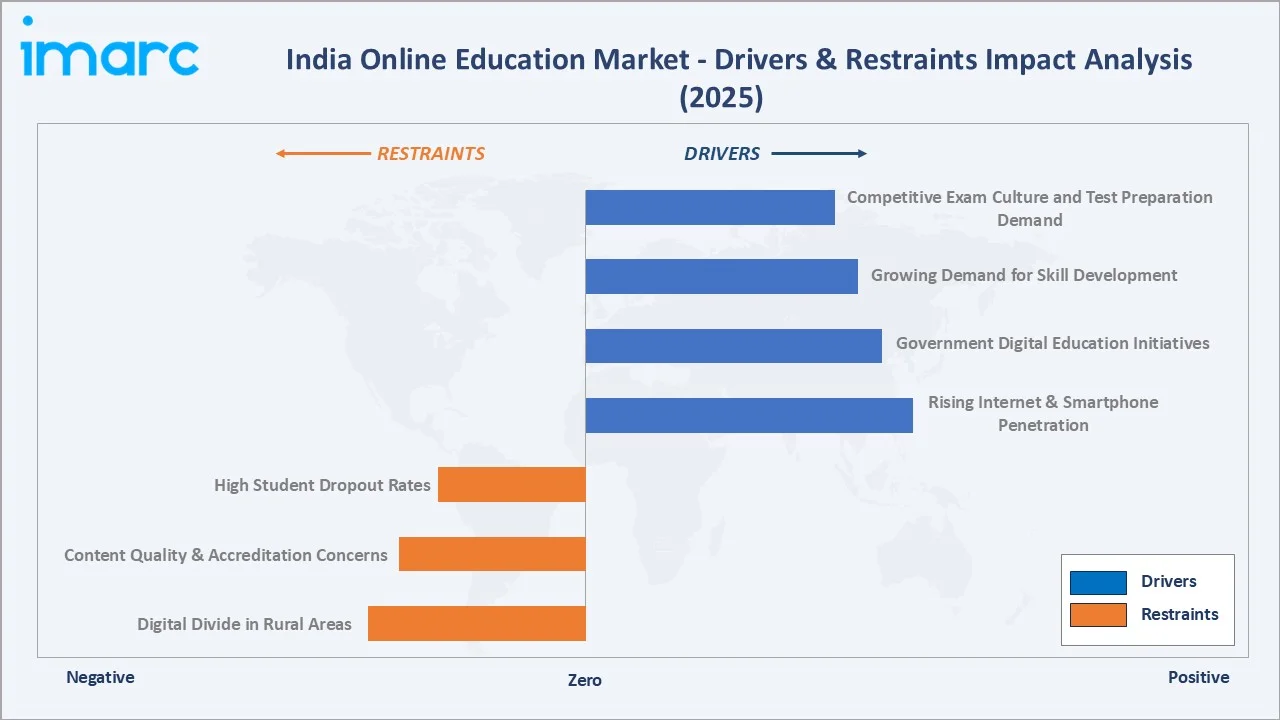

Market Drivers

- Rising Internet and Smartphone Penetration: There were 806 million internet users in India (2025). Affordable smartphones and cheap data plans have made online learning accessible to first-generation learners in semi-urban and rural areas, fundamentally expanding the addressable market beyond metropolitan centers into Tier-2 and Tier-3 cities.

- Government Digital Education Initiatives: The Indian government's PM eVidya, SWAYAM, DIKSHA, and National Digital Education Architecture (NDEAR) programs have created a digitally connected public learning infrastructure. The NEP 2020 mandates technology integration across K-12 and higher education, institutionalizing digital learning as a policy priority with significant public funding supporting platform development and content creation.

- Growing Demand for Skill Enhancement and Vocational Courses: India's rapidly evolving job market, driven by digital transformation across sectors, has generated high demand for upskilling and reskilling among working professionals. The National Skill Development Corporation (NSDC) estimated a large workforce requires reskilling, creating massive structural demand for online certification programs in AI, cloud, data analytics, and digital marketing.

- Competitive Exam Culture and Test Preparation Demand: India's high-stakes competitive examination ecosystem, covering JEE, NEET, UPSC, CAT, and state-level PSC exams, drives sustained, recurring demand for structured online test-prep content. A large number of students annually sit for engineering and medical entrance exams, creating a high-value, retention-sensitive learner segment that is increasingly shifting from offline coaching to online platforms.

Market Restraints

- Digital Divide in Rural and Remote Areas: Despite significant progress, a substantial share of India's rural population lacks reliable internet access. Power outages, limited device availability, and low digital literacy levels constrain online education penetration in Tier-4 and rural geographies, creating structural accessibility barriers for the lowest-income learner segments.

- High Student Dropout and Completion Rates: Online courses in India face low completion rates for self-paced programs, significantly impacting platform retention metrics and learner outcomes. The lack of accountability structures, reduced social learning interactions, and motivational challenges associated with asynchronous formats contribute to high dropout rates, particularly among first-generation online learners.

- Content Quality and Accreditation Concerns: The proliferation of unregulated online learning content and unrecognized certifications creates trust barriers among learners and employers. Standardization of online degree programs under UGC guidelines remains a work in progress, limiting widespread employer recognition of certain online credentials and discouraging learner investment in longer-duration programs.

Market Opportunities

- Vernacular Content Expansion into Tier-2/Tier-3 Markets: India has multiple official languages and hundreds of regional dialects, creating significant opportunity for EdTech platforms offering localized content. Platforms delivering courses in Hindi, Tamil, Telugu, Bengali, and Marathi can access a vast non-English-speaking learner base currently underserved by English-only digital content libraries, representing a high-growth blue-ocean segment.

- AI-Powered Personalized Learning and Adaptive Assessment: The integration of AI and machine learning into learning platforms enables adaptive content delivery, real-time performance analytics, and personalized study paths. EdTech companies deploying AI tutors and intelligent assessment systems can significantly improve completion rates and learning outcomes, creating a value differentiation that justifies premium pricing in both B2C and B2B segments.

- Corporate Training and Enterprise Learning Solutions: Indian enterprises are significantly increasing investments in Learning and Development (L&D) budgets, with the corporate training market growing steadily. EdTech companies offering B2B solutions with measurable ROI, LMS integrations, and industry-specific skill tracks are well-positioned to capture high-value enterprise contracts from both domestic and multinational companies operating in India.

Market Challenges

- Intense Platform Competition and Margin Compression: The India online education market hosts a large number of EdTech platforms, creating fierce competition on pricing, content quality, and marketing spending. This competitive intensity has led to significant customer acquisition cost escalation, straining unit economics and the path to profitability for early-stage platforms.

- Regulatory Uncertainty for Online Degree Programs: The regulatory framework governing fully online degree programs under UGC Open and Distance Learning (ODL) guidelines continues to evolve, creating compliance uncertainty for platforms offering accredited programs. Frequent policy updates require significant compliance investments and can impact platform product roadmaps and marketing claims, particularly for higher education offerings.

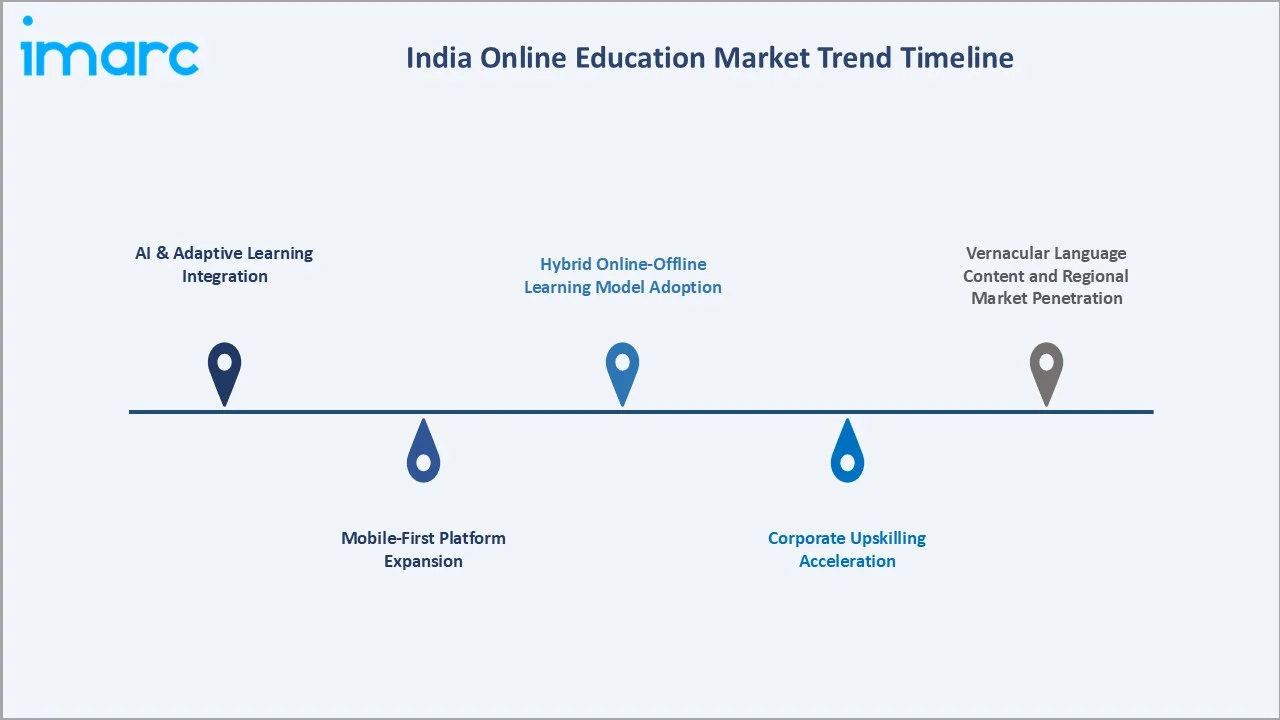

Emerging Market Trends

1. AI-Powered Adaptive Learning and Personalization

Artificial intelligence is fundamentally reshaping the India online education market trends. EdTech platforms are deploying machine learning algorithms to create individualized learning paths that adapt in real-time to learner performance, pace, and knowledge gaps. AI tutors that respond to doubts in natural language, predictive analytics identifying at-risk learners, and automated content recommendations are becoming standard platform features, significantly improving engagement and completion rates across K-12 and professional learning segments.

2. Mobile-First and Offline-Capable Learning

India's mobile-first digital culture is driving EdTech platforms to optimize entirely for smartphone delivery with low-bandwidth adaptability. Platforms offering offline content download, SMS-based micro-quizzes, and data-lite streaming modes are achieving significantly deeper penetration into semi-urban and rural learner cohorts. Mobile e-learning is growing at an estimated CAGR of 26.4% through 2034, outpacing all other delivery modes, as affordable smartphone hardware and Jio's ubiquitous connectivity democratize access to high-quality digital learning resources across geography and income strata.

3. Hybrid Online-Offline Learning Model Adoption

Leading EdTech players, including Unacademy and Physics Wallah, are making substantial investments in physical coaching center networks to complement their digital platforms. This hybrid model combines the scalability and cost-efficiency of online content delivery with the accountability and community benefits of in-person instruction. The hybrid approach is particularly resonating in Tier-2 and Tier-3 cities where learners value structured classroom environments alongside digital content access, creating a differentiated value proposition that pure-online platforms are struggling to replicate.

4. Corporate and Enterprise Upskilling Platform Expansion

India's rapid economic digitalization is generating high-volume enterprise demand for workforce reskilling. Corporate EdTech platforms are launching dedicated B2B products with LMS integration, competency framework alignment, and customizable course libraries targeting sectors including IT, BFSI, manufacturing, and healthcare.

5. Vernacular Language Content and Regional Market Penetration

Content localization into regional Indian languages is emerging as a primary growth driver for platforms targeting non-English-speaking learner populations. Physics Wallah's success with Hindi-medium content for NEET and JEE aspirants has demonstrated that vernacular delivery at scale is commercially viable.

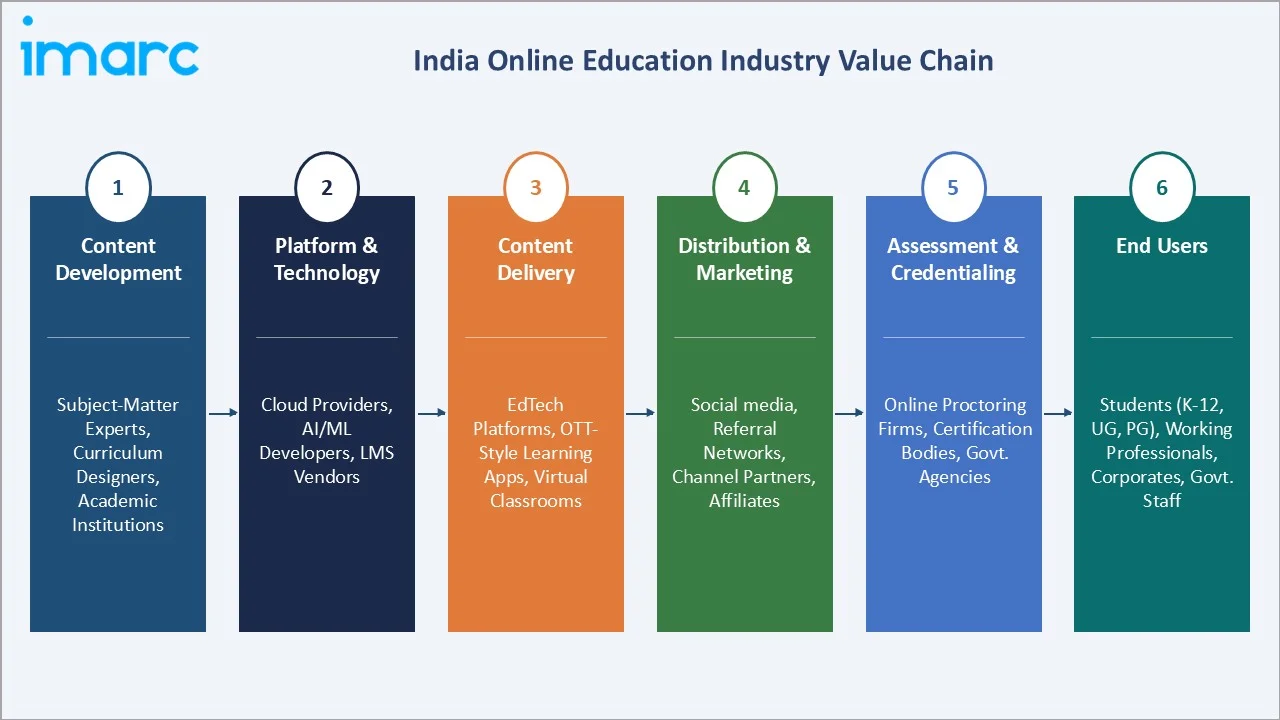

Industry Value Chain Analysis

The India online education industry value chain spans six integrated stages from content development through end-user delivery and credentialing.

|

Value Chain Stage |

Key Participants / Description |

|

Content Development |

Subject-matter experts, Curriculum designers, Academic institutions |

|

Platform & Technology |

Cloud providers, AI/ML developers, LMS vendors |

|

Content Delivery |

EdTech platforms, OTT-style learning apps, Virtual classrooms |

|

Distribution & Marketing |

Social media, Referral networks, Channel partners, Affiliates |

|

Assessment & Credentialing |

Online proctoring firms, Certification bodies, Govt. agencies |

|

End Users |

Students (K-12, UG, PG), Working professionals, Corporates, Govt. staff |

Each stage presents distinct competitive dynamics, investment requirements, and margin profiles relevant to the overall India online education market analysis.

EdTech platforms hold the highest strategic value in the chain by integrating content, technology infrastructure, and distribution into unified learner experiences. Content quality and delivery technology are the primary value-creation levers. Meanwhile, assessment and credentialing partnerships with recognized institutions such as IITs, IIMs, and global universities are becoming critical competitive differentiators as employer recognition of online certifications gains mainstream acceptance.

Technology Landscape in the India Online Education Industry

Mobile E-Learning and Low-Bandwidth Delivery

Mobile applications have emerged as the dominant content delivery vehicle in the India online education market. EdTech platforms are investing in video compression, offline-first app architectures, and progressive web app (PWA) technologies to ensure content accessibility on entry-level Android devices with limited data connectivity. Data-lite streaming modes consuming under 100MB per hour of video content are enabling learning continuity in areas with 2G and limited 4G coverage.

Artificial Intelligence and Adaptive Learning Systems

AI and machine learning are embedded across the full learner journey on leading EdTech platforms. Natural language processing powers real-time doubt resolution chatbots, computer vision monitors engagement and attention during live sessions, and recommendation engines personalize content sequencing based on performance data. Adaptive assessment systems dynamically adjust question difficulty based on learner mastery, providing granular performance insights that static exams cannot deliver.

Virtual Classroom and Live Interactive Technology

Live virtual classroom technology enabling synchronous instruction, interactive whiteboards, real-time polling, and breakout room discussions has become infrastructure-grade for India's leading EdTech platforms. Low-latency video streaming optimized for Indian network conditions, multi-device synchronization, and session recording with AI-generated transcripts are standard feature expectations. Virtual reality (VR) and augmented reality (AR) are in early-stage adoption, primarily for medical education simulation and engineering lab training, with broader rollout anticipated through 2028-2030 as hardware costs decline.

Learning Management Systems and Analytics

Enterprise-grade learning management systems (LMS) integrating course authoring, learner progress tracking, and business intelligence dashboards are driving the corporate EdTech segment. Platforms offering API-based LMS integrations compatible with major HR systems such as SAP SuccessFactors and Workday are commanding premium B2B pricing. Competency mapping frameworks, skills gap analysis, and learning ROI measurement capabilities are becoming mandatory requirements for enterprise contracts, driving significant investment in data analytics and reporting infrastructure across leading platform providers.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Academic | 58.6% | 2025 |

| Provider | Content | 64.2% | 2025 |

| Technology | 🔒 | 🔒 | 2025 |

| End-User | 🔒 | 🔒 | 2025 |

| Region | North India | 33.8% | 2025 |

By Type

To access detailed market analysis, Request Sample

Academic applications lead the India online education market type segment with a 58.6% share in 2025. Demand is driven by the high-stakes competitive examination ecosystem, supplementary K-12 learning adoption, and increasing enrolment in online degree and diploma programs under UGC-approved frameworks. India's annual examination calendar covering JEE Advanced, NEET-UG, UPSC Civil Services, and state-level entrance exams sustains a recurring, high-intent learner base for online test-preparation content.

By Provider

Content providers are the dominant segment at 64.2% of provider revenue in 2025. The primacy of content reflects India's learner preference for structured, outcome-oriented digital resources over platform services. Content providers developing exam-aligned question banks, recorded lecture libraries, and vernacular subject modules command high learner loyalty due to the direct correlation between content quality and examination success.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

33.8% |

Delhi NCR, UP student base; govt. digital initiatives; test prep demand |

|

South India |

29.6% |

High tech literacy; Bengaluru startup hub; strong K-12 & STEM demand |

|

West India |

21.7% |

Corporate upskilling; Mumbai financial sector; fintech-edtech convergence |

|

East India |

14.9% |

Emerging digital infrastructure; rising vernacular content demand; JEE/NEET prep |

North India commands 33.8% national revenue share in 2025. The Delhi NCR metropolitan corridor is the single most important sub-regional market, combining high student density, strong aspirational culture for competitive exams, and well-developed digital infrastructure. Uttar Pradesh, with a population of over 230 million and high concentration of JEE/NEET aspirants, is a structurally significant volume market. The Rajasthan coaching belt transitioning from Kota's offline centers to hybrid online formats represents a major customer acquisition opportunity for EdTech platforms offering structured test-prep programs at affordable price points.

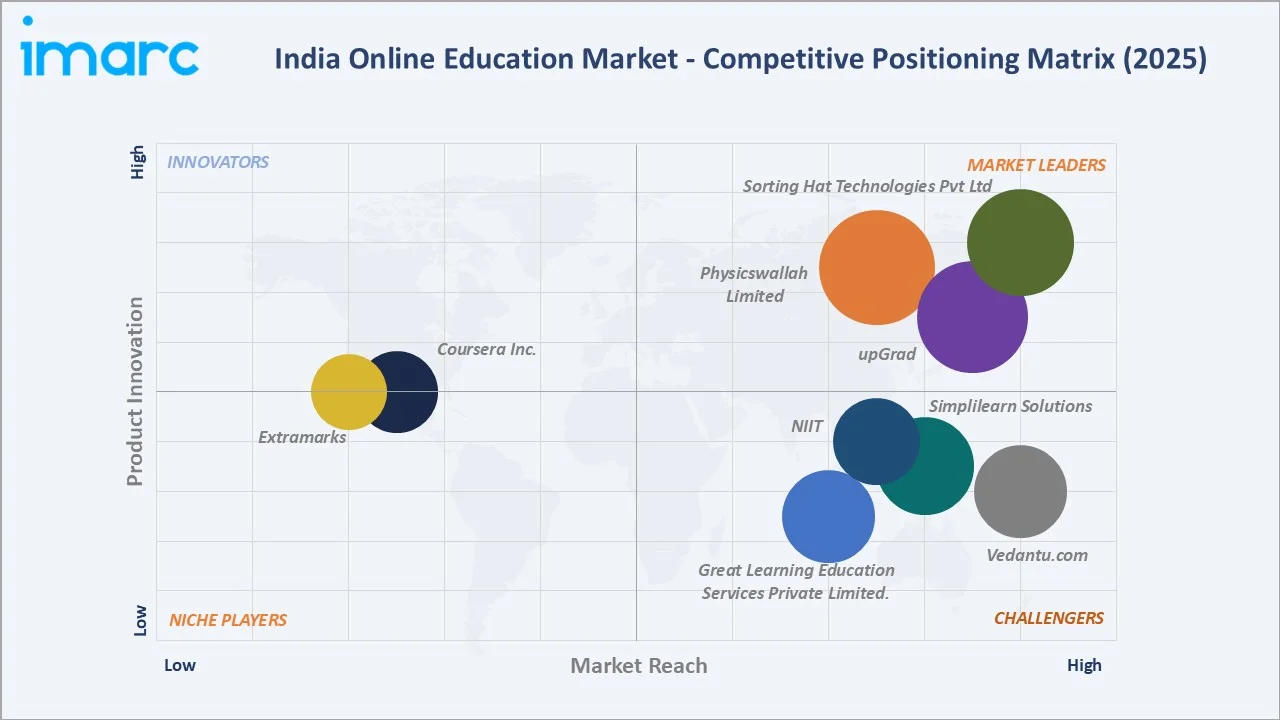

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Sorting Hat Technologies Pvt Ltd |

Unacademy |

Leader |

Test prep, hybrid coaching centers, competitive exam focus |

|

upGrad |

upGrad, KnowledgeHut |

Leader |

Higher ed & professional upskilling, global university tie-ups |

|

Physicswallah Limited |

PW |

Leader |

Affordable pricing, vernacular content, NEET/JEE focus |

|

Vedantu.com |

Vedantu, WAVE |

Challenger |

Live interactive classes, AI tutor, K-12 premium segment |

|

Simplilearn Solutions |

Simplilearn, SkillUp |

Challenger |

Professional certifications, corporate training, global reach |

|

Great Learning Education Services Private Limited. |

Great Learning |

Challenger |

Executive programs, analytics & AI courses, IIT/IIM tie-ups |

|

NIIT |

NIIT, StackRoute |

Challenger |

Legacy IT training, corporate learning, government skilling |

|

Coursera Inc. |

Coursera, Coursera Plus |

Emerging |

Global platform, university credentials, enterprise learning |

|

Extramarks |

Extramarks |

Emerging |

School-tech integration, hybrid learning, B2B school model |

The India online education market's competitive landscape is highly fragmented, with EdTech giants competing alongside specialized exam-prep platforms, enterprise learning providers, and international platforms.

Key Company Profiles

Sorting Hat Technologies Pvt. Ltd.

Sorting Hat Technologies Pvt. Ltd. is an Indian edtech and technology company best known as the parent entity behind Unacademy. Incorporated in 2015 and headquartered in Bengaluru, the company operates in online education, software services, and data-driven learning solutions.

- Product & Platform Portfolio: Unacademy is subsidiary of Sorting Hat Technologies Pvt. Ltd., offer portfolio includes the flagship app, relevel for job-skill assessments, Graphy for creator-led courses, and an expanding network of physical learning centers branded as Unacademy Centres in over 25 cities across India.

- Recent Developments: In 2025, Unacademy is undergoing major strategic reset, shifting its offline coaching business to a franchise-led model to become more asset-light and cost-efficient. The move follows multiple failed acquisition talks, signaling a shift toward self-sustainability rather than external rescue.

- Strategic Focus: Unacademy's pivot centers on scaling its offline coaching center network in Tier-2 and Tier-3 cities, combining physical learning environments with digital content delivery to capture aspirant segments that value structured classroom accountability alongside online flexibility.

upGrad

upGrad is India's leading higher education and professional upskilling platform, headquartered in Mumbai. Founded in 2015, it specializes in online degree programs, executive education, and professional certifications in partnership with top-tier Indian and global universities.

- Product & Platform Portfolio: upGrad's portfolio encompasses postgraduate programs in data science, AI, business management, and software engineering, executive education in partnership with IIT Bombay, IIM Kozhikode, and international universities, and KnowledgeHut for technical skills bootcamps.

- Recent Developments: In 2026, upGrad has acquired internship and training platform Internshala in a 90% stock-swap deal to strengthen its early-career and placement ecosystem. The acquisition integrates upGrad’s higher education and skilling programs with Internshala’s internship marketplace and AI-driven placement courses, creating a full pathway from learning to employment.

- Strategic Focus: upGrad's strategy focuses on dominating the premium professional education segment through outcome-guaranteed programs with placement assistance, income-share agreements, and deep corporate recruitment partnerships that create measurable learner career ROI.

Physicswallah Limited

Physicswallah Limited is India's fastest-growing EdTech unicorn, headquartered in Prayagraj, Uttar Pradesh. Founded by Alakh Pandey, it democratized JEE and NEET preparation through radically affordable pricing, making high-quality online coaching accessible to middle-class and lower-income aspirants across India.

- Product & Platform Portfolio: PW's portfolio includes the flagship PW App for live and recorded JEE/NEET content, PW Skills for professional tech and data science upskilling, Hindi-medium content libraries, and an expanding network of hybrid PW Centers in Tier-2 cities.

- Recent Developments: In 2025, PhysicsWallah reported a sharp surge in paid users to 4.46 million in FY25, marking a 153% increase from FY23, as it strengthens its position ahead of a planned IPO. The platform also recorded 4.13 million transacting users online and expanded into 13 education categories, reflecting rapid scale-up across its offerings.

- Strategic Focus: PW's strategy centers on maintaining its affordable pricing leadership while scaling through hybrid online-offline centers, vernacular content expansion, and diversification into professional skill development through PW Skills to reduce dependency on JEE/NEET exam-prep revenues.

Market Concentration Analysis

The India online education market exhibits high fragmentation at the overall level, with over 4,500 registered EdTech platforms competing for learner attention and market share. However, concentration is significantly higher within individual sub-segments. In the K-12 and competitive exam preparation segment, the top five players, including Sorting Hat Technologies Pvt Ltd, upGrad, Physicswallah Limited, Vedantu.com, Simplilearn Solutions, collectively account for approximately 55-62% of segment revenue in 2025.

The market is experiencing a bifurcated dynamic. At the consumer EdTech tier, intense platform competition and funding contraction post-2022 have triggered significant consolidation through acquisitions, strategic pivots, and market exits by underfunded platforms. Simultaneously, the corporate EdTech segment is seeing rapid consolidation around established B2B players with proven enterprise delivery capabilities. This dual dynamic is reducing fragmentation in high-value segments while the long-tail of niche and regional platforms continues to proliferate in underserved geographies and subject categories.

Investment & Growth Opportunities

Fastest-Growing Segments

Mobile e-learning is the highest-growth delivery channel at approximately 26.4% CAGR through 2034, driven by India's mobile-first connectivity patterns. The corporate upskilling segment is expanding at an estimated 22.5% CAGR, creating significant B2B revenue opportunities. AI-powered personalized learning represents the premium technology growth opportunity.

Emerging Market Expansion

Tier-2 and Tier-3 city learner populations represent the highest-potential emerging sub-markets, driven by rising aspirations, improving internet connectivity, and underserved access to quality offline coaching. East India, representing only 14.9% of the market today, offers the highest untapped growth potential as digital infrastructure investment accelerates in Bihar, West Bengal, and Odisha. Vernacular content platforms serving Hindi-belt, Bengali, and South Indian language learners can access hundreds of millions of previously excluded learners at structurally lower customer acquisition costs.

Venture and Strategic Investment Trends

India's EdTech sector has attracted substantial venture and growth capital in recent years, with the investment thesis shifting from growth-at-all-costs to unit-economics-focused business models post-2022. In October 2024, Eruditus secured fresh funding at a strong valuation, demonstrating continued investor confidence in premium professional education. Strategic acquisitions are expected to intensify as larger platforms seek to acquire content libraries, technology capabilities, and learner bases from financially stressed smaller EdTech operators through the coming years.

Future Market Outlook (2026-2034)

The India online education market forecast projects sustained high-growth value expansion from USD 3.64 Billion in 2025 to USD 23.90 Billion by 2034 at a CAGR of 23.28%. North India will retain regional leadership through 2034. South India, driven by Bengaluru's tech ecosystem and strong engineering culture, will sustain the highest quality-of-revenue growth through premium professional education.

Four key shifts will reshape the India online education market through 2034. First, AI convergence will embed intelligent tutoring and adaptive assessment as standard platform infrastructure, making AI-personalized learning the expected baseline rather than a premium feature. Second, hybrid online-offline models will become the dominant delivery paradigm for exam preparation and higher education as platforms balance digital scalability with physical accountability structures.

Third, vernacular content at scale will unlock the next large learner cohort from Tier-3 cities and rural India, fundamentally shifting the market’s geographic center of gravity. Fourth, outcome-based monetization models—including income-share agreements, pay-after-placement structures, and subscription-based career learning ecosystems will replace one-time course purchases as the primary commercial framework for professional upskilling platforms.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with India online education industry stakeholders, including platform product directors, content development heads, corporate L&D managers, regulatory officials at UGC and NSDC, and institutional investors in the EdTech sector. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines across learner cohorts.

Secondary Research

Secondary sources include Ministry of Education annual reports, UGC Open and Distance Learning framework documents, NSDC skilling target publications, NASSCOM EdTech landscape reports, company annual filings and investor presentations, trade publications including EdTech Review and Educational Technology & Society, and regional digital infrastructure data from TRAI and the Ministry of Electronics and Information Technology.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, internet and smartphone penetration trajectories, enrollment data from UGC and NSDC, and historical EdTech platform revenue evolution. Scenario analysis (base, optimistic, and conservative cases) was performed to account for regulatory uncertainty, funding environment changes, and macroeconomic sensitivity.

India Online Education Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

|

| Providers Covered | Content, Services |

| Technologies Covered | Mobile E-Learning, Rapid E-Learning, Virtual Classroom, Others |

| End-Users Covered | Higher Education Institutions, K-12 Schools |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Sorting Hat Technologies Pvt Ltd, upGrad, Physicswallah Limited, Vedantu.com, Simplilearn Solutions, Great Learning Education Services Private Limited., NIIT, Coursera Inc., Extramarks, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India online education market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India online education market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India online education industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Online Education Market Report

The India online education market was valued at USD 3.64 Billion in 2025, propelled by smartphone penetration, government digital initiatives, and growing demand for online exam preparation and professional upskilling courses.

The market is projected to reach USD 23.90 Billion by 2034, growing at a CAGR of 23.28% during 2026-2034, supported by AI-personalized learning, vernacular content expansion, and rising corporate upskilling demand.

Academic applications lead with a 58.6% share in 2025, driven by K-12 supplementary learning, competitive exam preparation for JEE, NEET, and UPSC, and increasing enrollment in UGC-approved online degree programs.

Content providers dominate with a 64.2% share in 2025, reflecting high learner preference for structured, exam-aligned digital content libraries over standalone platform services.

North India dominates with a 33.8% share in 2025. Delhi NCR's high student density, UP's vast aspirant base, and Rajasthan's coaching culture transitioning online underpin its regional leadership.

Key drivers include rising internet and smartphone penetration, government programs such as PM eVidya and SWAYAM, intense competitive exam culture, growing demand for workforce upskilling, and AI-powered personalization improving learning outcomes.

Mobile e-learning is the fastest-growing delivery mode at approximately 26.4% CAGR through 2034, driven by affordable smartphones, low-cost data plans, and offline-capable app architectures reaching Tier-3 learners.

Major players include Sorting Hat Technologies Pvt Ltd, upGrad, Physicswallah Limited, Vedantu.com, Simplilearn Solutions, Great Learning Education Services Private Limited., NIIT, Coursera Inc., and Extramarks

Key opportunities include vernacular content platforms for Tier-2/3 markets, AI-powered adaptive learning systems, corporate enterprise upskilling solutions, hybrid online-offline models, and outcome-based professional education programs with placement guarantees.

PM eVidya, SWAYAM MOOC platform, DIKSHA for school education, NDEAR, NEP 2020 digital mandates, and Mission Karmayogi for civil servant capacity building are the primary government initiatives driving market growth.

Key challenges include the digital divide in rural areas, low online course completion rates for self-paced programs, content quality standardization issues, intense competition among numerous EdTech platforms, and regulatory uncertainty for online degree accreditation.

AI is enabling adaptive learning paths, real-time doubt resolution through chatbots, personalized content recommendations, predictive learner analytics, and automated assessments, with platforms reporting improved learner retention through AI-driven personalization.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)