India Orange Market Size, Share, Trends and Forecast by Product, Application, and Region, 2026-2034

India Orange Market Summary:

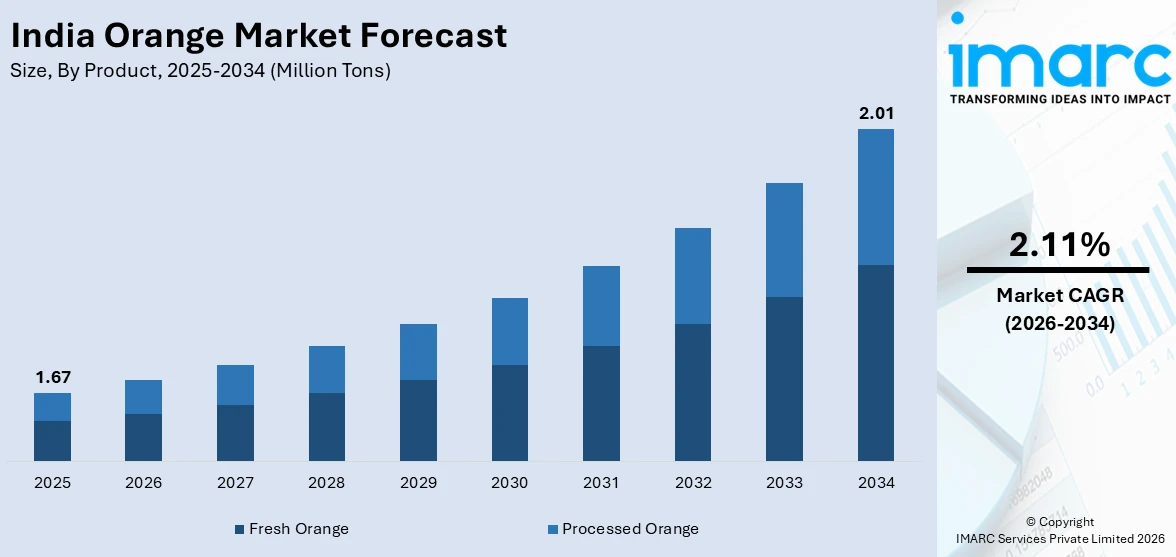

The India orange market size reached 1.67 Million Tons in 2025. The market is projected to reach 2.01 Million Tons by 2034, growing at a CAGR of 2.11% during 2026-2034. The market is driven by rising health consciousness among consumers, significant government investments in orange processing infrastructure, and expanding export opportunities for Indian citrus fruits. Additionally, the growing demand for natural and nutrient-rich fruit juices, particularly those high in vitamin C, is supporting India orange market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

| Market Size in 2025 | 1.67 Million Tons |

| Market Forecast in 2034 | 2.01 Million Tons |

| Market Growth Rate 2026-2034 | 2.11% |

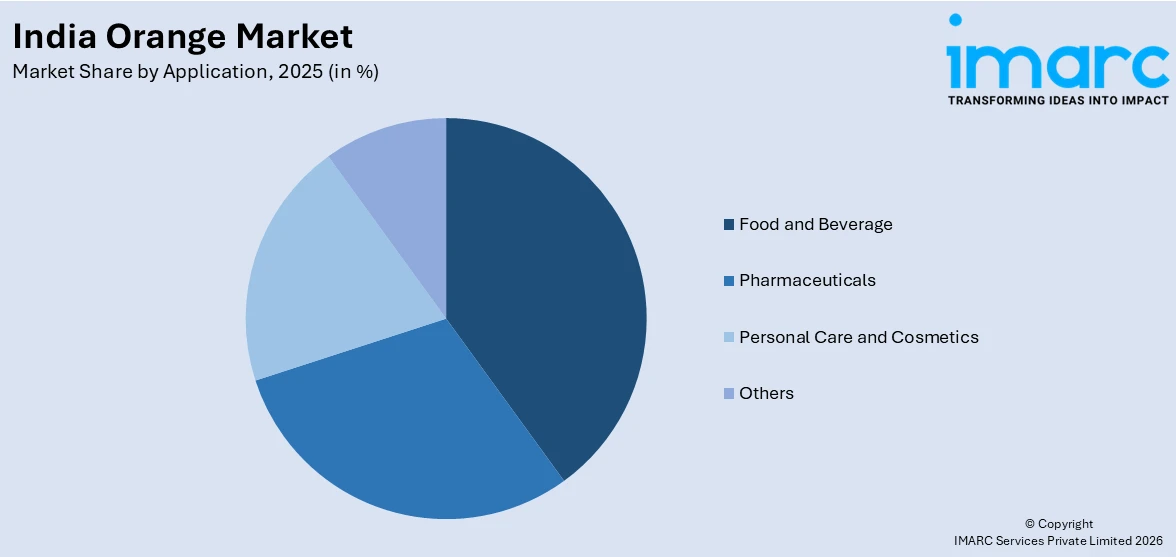

| Key Segments | Product (Fresh Orange, Processed Orange), Application (Food and Beverage, Pharmaceuticals, Personal Care and Cosmetics, Others) |

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

India Orange Market Outlook (2026-2034):

The orange market in India is expected to expand steadily amid rising consumer demand for healthy and natural fruits containing vitamin C and antioxidants. Anticipated government support for agricultural infrastructure development, including large-scale processing plants in important citrus-growing areas such as Nagpur and Vidarbha, should help to enhance the value of the product and farmer incomes. Expanding export market opportunities to the Middle East and other regions will also support the positive trajectory of the market, combined with improved post-harvest management and cold chain infrastructure development.

To get more information on this market Request Sample

Impact of AI:

The Indian orange market is undergoing an initial transformation through the use of agricultural technologies that use advances in artificial intelligence. AI-assisted drones carrying multispectral and thermal sensors can identify and locate early signs of pest infestation, especially the Asian citrus psyllid that carries Huanglongbing (HLB) or citrus greening disease, and nutritional deficiencies in orange orchard, while providing real-time recommendations for precision application of fertilizers and pesticides. On the one hand, these technology-assisted approaches are creating recommended real-time use data and applications that can reduce costs, environmental footprints, while maximizing pest defenses, fertilizer programs, and fruit yield - from farm-field to the consumer.

Market Dynamics:

Key Market Trends & Growth Drivers

Rising Health Consciousness Driving Demand for Nutritious Fruit Beverages

Growing consumer awareness about health and wellness has significantly increased demand for natural and nutrient-rich beverages, with orange juice emerging as a preferred choice due to its high vitamin C content, immune-boosting properties, and antioxidant benefits. The shift towards healthier lifestyles, particularly among urban populations and working professionals, has positioned fruit juices as convenient alternatives to carbonated soft drinks and artificial beverages. India's fruit juice market, which reached USD 5,216.7 million in 2024, and is expected to exhibit robust growth at a CAGR of 11.90% during 2025-2033, reflecting the strong consumer appetite for health-oriented products. Orange juice specifically has gained traction for its refreshing taste combined with nutritional advantages, making it popular for breakfast consumption, post-workout hydration, and as a daily vitamin supplement. The market is witnessing innovation with the introduction of 100% fruit juice variants without added sugars, cold-pressed options that preserve natural enzymes and vitamins, and fortified products targeting specific health benefits. Consumers are increasingly willing to pay premium prices for authentic, fresh-tasting orange juice with transparent sourcing and minimal processing. This health-conscious trend is supported by rising disposable incomes, greater nutrition awareness through digital media and health campaigns, and the growing prevalence of lifestyle diseases that necessitate dietary improvements. The expanding middle class and youth demographic particularly favor convenient, ready-to-drink orange juice products that align with their busy schedules while supporting their wellness goals, thereby driving sustained growth in the India orange market.

Significant Government Investment in Orange Processing Infrastructure Development

Government support through substantial infrastructure investments has emerged as a crucial growth driver for India's orange market, particularly in major producing regions like Nagpur and Vidarbha in Maharashtra. These investments aim to reduce post-harvest losses, enhance value addition capabilities, and improve farmer incomes through better price realization. Additionally, the Maharashtra Government approved five orange processing centers in Vidarbha with a total investment of INR 40 crore, strategically located in Nagpur (three centers) and Amravati districts (two centers). These centers feature advanced packaging facilities, chilling units, and vaccine units designed to maintain fruit quality and extend shelf life for both domestic and export markets. Such infrastructure developments address critical supply chain bottlenecks that have historically plagued citrus farmers, including seasonal gluts, price volatility, and limited market access. Processing facilities enable farmers to sell their produce throughout the year rather than only during harvest season, stabilizing incomes and reducing dependency on intermediaries. The government's Agriculture Export Policy has designated Nagpur District as a cluster for Nagpur Orange development, with APEDA (Agricultural and Processed Food Products Export Development Authority) coordinating capacity building programs, quality enhancement initiatives, and international market linkages. These coordinated efforts between central and state governments, private sector investments, and institutional support are creating an enabling ecosystem that positions India's orange industry for long-term sustainable growth while enhancing competitiveness in global markets.

Export Market Expansion and Quality Enhancement Initiatives for Indian Oranges

Export market development has gained significant momentum as India seeks to capitalize on the global demand for high-quality citrus fruits, particularly targeting Middle Eastern countries where Nagpur mandarin commands premium prices. APEDA's strategic cluster development approach has transformed Nagpur District into a dedicated export hub through comprehensive stakeholder engagement involving farmers, exporters, research institutions, and government agencies. Export initiatives emphasize rigorous quality control through certification of pest-free production zones, implementation of Good Agricultural Practices, adoption of modern post-harvest handling techniques including grading, washing, waxing, and proper packaging, and establishment of cold chain infrastructure to maintain freshness during transportation. The Agricultural Market Intelligence Centre established in 2024 at the College of Agriculture assists farmers in achieving better net prices through market information dissemination and direct buyer connections. Training programs conducted by research institutions educate farmers on export specifications, pre-harvest fruit care, selective harvesting techniques, and maintaining the delicate flavor profile that distinguishes Nagpur oranges. These coordinated efforts are gradually building India's reputation in international citrus markets, creating sustainable revenue streams for farmers, and establishing export as a key pillar of the country's orange industry development strategy.

Key Market Challenges:

Citrus Greening Disease (Huanglongbing) and Asian Citrus Psyllid Infestation

Citrus greening disease, scientifically known as Huanglongbing (HLB), poses one of the most serious threats to India's orange industry, with no known cure currently available. The disease is caused by the bacterium Candidatus Liberibacter asiaticus and is transmitted by the Asian citrus psyllid (Diaphorina citri), a tiny sap-sucking insect that has become widespread in major orange-growing regions including Maharashtra, Madhya Pradesh, and parts of north-eastern India. Once infected, orange trees display characteristic symptoms including asymmetrical yellowing of leaves (blotchy mottle), misshapen and bitter fruits with irregular coloring, premature fruit drop, stunted growth, and eventual tree death within five to eight years. The disease is particularly devastating because symptoms may not appear until months or years after initial infection, during which time the bacteria spread throughout the tree's vascular system and psyllids can transmit it to neighboring healthy trees. Management of citrus greening is extremely challenging and requires integrated approaches including regular monitoring and early detection through visual inspection and laboratory testing, immediate removal of infected trees to prevent disease spread, intensive psyllid population control through coordinated insecticide applications, use of certified disease-free nursery stock for new plantings, and implementation of area-wide management programs involving all growers in a region. However, continuous insecticide use is expensive, raises environmental concerns, and can lead to pest resistance, while tree removal reduces productive capacity and farmer incomes significantly. The unavailability of resistant citrus varieties means all commercial orange cultivars remain vulnerable. Research institutions like the ICAR-Central Citrus Research Institute in Nagpur are investigating potential solutions including development of tolerant varieties through conventional breeding and biotechnology, biological control agents targeting the psyllid vector, and therapeutic treatments to suppress bacterial multiplication in infected trees. Until effective solutions are commercially available, citrus greening continues to threaten the sustainability and profitability of orange cultivation in India, requiring constant vigilance and substantial investments in disease management by farmers.

Climate Change Impacts Including Water Scarcity and Extreme Weather Events

Climate change has emerged as a significant challenge affecting India's orange production through multiple interconnected factors that threaten both yield and fruit quality. Rising temperatures in key growing regions like Vidarbha have begun to alter the delicate climatic balance required for optimal orange cultivation, with extended periods of high temperatures causing heat stress in trees, reduced flowering, poor fruit set, and premature fruit drop. Extreme weather events including unseasonal rainfall, hailstorms, prolonged dry spells, and sudden temperature fluctuations have become more frequent and unpredictable, disrupting the natural phenological cycles of orange trees and creating conditions conducive to disease and pest outbreaks. Water scarcity represents perhaps the most critical climate-related challenge, as orange trees require consistent moisture availability especially during fruit development and maturation stages. Many traditional orange-growing areas in Maharashtra and Madhya Pradesh have experienced recurring droughts over the past decade, severely impacting groundwater levels and the reliability of irrigation sources. The Vidarbha region, historically known for its agrarian economy, has seen repeated water crises that force farmers to make difficult choices between maintaining orange orchards and meeting other water needs. Inadequate irrigation infrastructure, over-extraction of groundwater, and erratic monsoon patterns have compounded water availability issues. Farmers lacking access to drip irrigation systems, which can deliver water efficiently directly to root zones, often struggle to maintain tree health during critical growth periods. Climate-induced stress also makes orange trees more vulnerable to secondary problems including increased susceptibility to fungal infections like anthracnose and citrus canker that thrive in humid conditions, greater pest pressure as warming temperatures allow insect populations to expand their range and increase reproductive cycles, and soil degradation through erosion and nutrient leaching caused by intense rainfall events. The financial burden on farmers intensifies as they must invest in climate adaptation measures such as protective structures, supplementary irrigation systems, and increased pest management inputs without corresponding increases in output or prices. Long-term viability of Vidarbha as a premier citrus-growing region is increasingly questioned as climate projections suggest continued warming and greater rainfall variability, potentially necessitating shifts in cultivation practices, introduction of more climate-resilient varieties, or even geographic relocation of production to more suitable areas.

Post-Harvest Losses and Supply Chain Infrastructure Gaps

Significant post-harvest losses plague India's orange supply chain, with estimates suggesting that 20-30% of harvested oranges fail to reach consumers in marketable condition due to inadequate infrastructure and handling practices. Orange fruits are highly perishable with delicate skin that bruises easily, making them particularly vulnerable to damage during harvesting, transportation, and storage. Many smallholder farmers lack access to proper harvesting tools and training, resulting in mechanical injuries during picking that create entry points for pathogens and accelerate deterioration. The absence of adequate cold storage facilities near production areas means oranges are often stored at ambient temperatures that promote rapid quality degradation, moisture loss, and decay. Transportation infrastructure poses another major bottleneck, with oranges frequently transported in non-refrigerated trucks over long distances on poor-quality roads, subjecting fruits to vibrations, temperature fluctuations, and rough handling that cause bruising and internal damage. The traditional multi-layered marketing system involving multiple intermediaries—farmers, local traders, commission agents, wholesalers, and retailers—creates inefficiencies through repeated handling, extended transit times, and lack of accountability for quality maintenance. Each intermediary stage adds costs while providing opportunities for damage and quality loss. Packaging practices often involve crude methods using wooden crates or plastic crates without proper cushioning, leading to compression damage and fruit-to-fruit contact injuries. Limited availability of grading and sorting facilities means mixed quality lots reach markets, affecting price realization and consumer satisfaction. Seasonal gluts during peak harvest periods (January-March) cause temporary oversupply that depresses prices and overwhelms available marketing channels, forcing farmers to sell at distress prices or allow fruits to rot in orchards. The lack of processing capacity until recently meant excess production couldn't be diverted to value-added products like juice, concentrate, or essential oils, though new facilities like the Patanjali plant are beginning to address this gap. Small landholdings and fragmented production make it difficult to achieve economies of scale in post-harvest operations, with individual farmers unable to invest in proper storage or transportation equipment. Marketing credit constraints limit farmers' ability to hold produce for better prices, forcing immediate sales regardless of market conditions. Weak farmer organization and limited collective bargaining power prevent coordinated marketing efforts that could improve negotiating positions with buyers. Addressing these supply chain challenges requires coordinated investments in cold chain infrastructure, farmer training on proper harvesting and handling techniques, development of farmer producer organizations for collective marketing, expansion of processing capacity to absorb seasonal surpluses, and improvement of rural road connectivity to reduce transit times and damage. Until these systemic issues are adequately addressed, post-harvest losses will continue to erode farmer profitability and constrain market growth potential.

India Orange Market Report Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the India orange market, along with forecasts at the country and regional levels for 2026-2034. The market has been categorized based on product and application.

Analysis by Product:

- Fresh Orange

- Processed Orange

The report has provided a detailed breakup and analysis of the market based on the product. This includes fresh orange and processed orange.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Food and Beverage

- Pharmaceuticals

- Personal Care and Cosmetics

- Others

A detailed breakup and analysis of the market based on the application have also been provided in the report. This includes food and beverage, pharmaceuticals, personal care and cosmetics, and others.

Analysis by Region:

- North India

- South India

- East India

- West India

The report has also provided a comprehensive analysis of all the major regional markets, which include North India, South India, East India, and West India.

Competitive Landscape:

The India orange market exhibits a fragmented competitive landscape characterized by a large number of smallholder farmers who collectively account for the majority of production, alongside emerging processing and juice manufacturing companies seeking to capture value-added opportunities. The market lacks significant organized corporate presence at the cultivation level, with production concentrated in states like Maharashtra, Madhya Pradesh, Andhra Pradesh, and parts of the north-eastern region. Competition primarily occurs at the processing and distribution stages where established FMCG companies like Dabur (Real brand), PepsiCo (Tropicana), Coca-Cola (Minute Maid), and ITC (B Natural) compete for market share in the packaged orange juice segment. Recent infrastructure investments, particularly Patanjali's major processing facility in Nagpur, indicate intensifying competition for raw material sourcing and processed product markets. The competitive dynamics are evolving as traditional agriculture-focused approaches give way to integrated value chains, with companies increasingly establishing direct farmer linkages to ensure consistent supply quality and quantity while processors compete on product innovation, brand positioning, and distribution reach.

India Orange Industry Latest Developments:

- March 2025: Patanjali Ayurved Ltd. inaugurated Asia's largest orange processing plant at MIHAN, Nagpur, with an investment of INR1,500 crore (approximately USD 180 million). The state-of-the-art facility, inaugurated by Union Minister Nitin Gadkari, Maharashtra Chief Minister Devendra Fadnavis, and Swami Ramdev, has a daily processing capacity of 800 tonnes and operates on a zero-waste model. The plant produces 100% pure, pesticide-free orange juice while extracting valuable oils from orange peels to enhance economic viability and benefit farmers in the Vidarbha region.

India Orange Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Fresh Orange, Processed Orange |

| Applications Covered | Food and Beverage, Pharmaceuticals, Personal Care and Cosmetics, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India orange market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India orange market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India orange industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Orange Market Report

The India orange market reached a volume of 1.67 Million Tons in 2025.

The market is projected to grow at a CAGR of 2.11% during 2026-2034, reaching 2.01 Million Tons by 2034.

Key growth drivers include rising health consciousness, government investment in processing infrastructure, export market expansion, and increasing demand for vitamin-C-rich citrus fruit products.

The report covers segmentation by product, application, and region. Each segment includes detailed market size and forecast analysis.

Key trends include cold chain infrastructure development, AI-driven orchard surveillance, government processing center investments, export market expansion, and fresh citrus juice demand.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)