India Organic Pasta Market Size, Share, Trends and Forecast by Product Type, Application, Distribution Channel, and Region, 2026-2034

India Organic Pasta Market Summary:

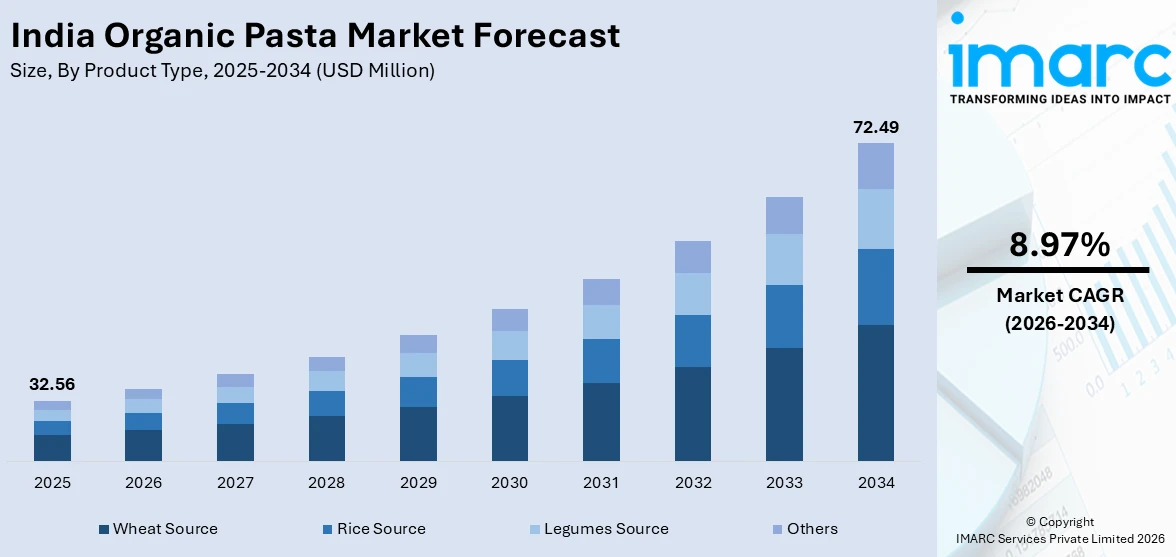

The India organic pasta market size was valued at USD 32.56 Million in 2025 and is projected to reach USD 72.49 Million by 2034, growing at a compound annual growth rate of 8.97% from 2026-2034.

India's organic pasta market is gaining momentum as health-conscious consumers increasingly prioritize clean-label, pesticide-free food options. The rising urban middle class, growing acceptance of international cuisine, and increased availability of certified organic products across modern retail and e-commerce channels are collectively strengthening the market. Supportive government schemes promoting organic agriculture, expanding cold-chain logistics, and the emergence of health-focused D2C food brands are further reinforcing India organic pasta market share.

Key Takeaways and Insights:

- By Product Type: Wheat source dominates the market with a share of 35.0% in 2025, driven by widespread consumer familiarity with wheat-based pasta, its superior texture and cooking properties, and the deep-rooted preference for durum wheat flour across Indian households preparing pasta dishes.

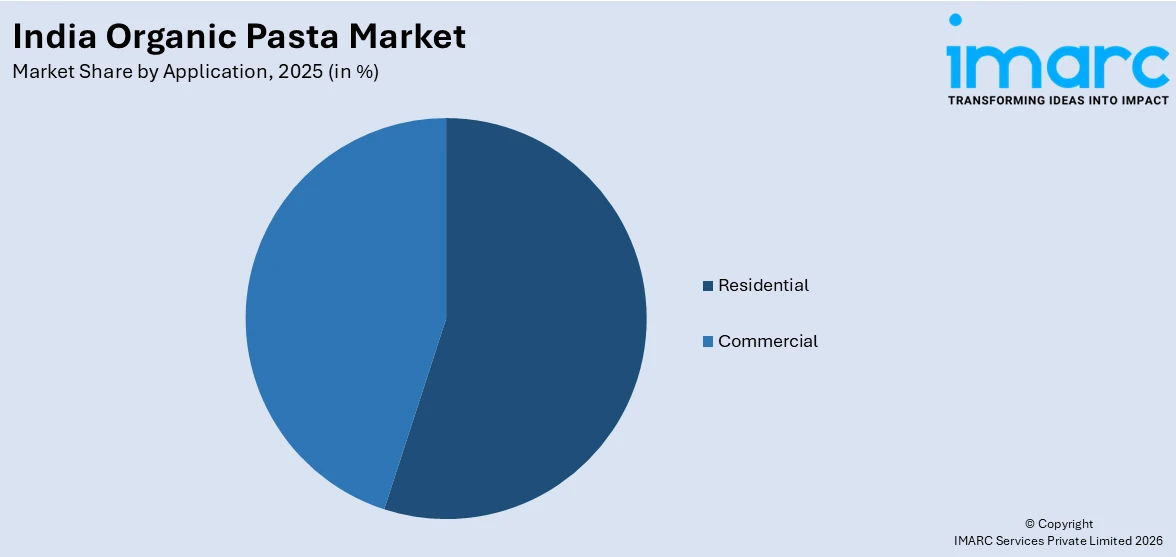

- By Application: Residential leads the market with a share of 55.0% in 2025, underpinned by the growing trend of home cooking among health-aware families, increasing availability of organic pasta through retail and online channels, and rising disposable incomes enabling premium food purchases.

- By Distribution Channel: Offline stores represent the largest revenue share of 52.0% in 2025, owing to consumer preference for in-store product verification, the established presence of organic food sections in supermarkets and hypermarkets, and trust built through physical retail interactions in tier-I and tier-II cities.

- By Region: West India represents the largest segment with a market share of 32.0% in 2025, attributed to the high concentration of health-conscious urban consumers in cities like Mumbai, Pune, and Ahmedabad, strong modern retail infrastructure, and the dominant presence of organic food brands and specialty stores in the region.

- Key Players: The India organic pasta market features a blend of established FMCG companies, specialty organic food brands, and emerging health-focused D2C players competing on product quality, organic certification, pricing, and distribution reach across urban and semi-urban markets.

To get more information on this market Request Sample

India’s organic pasta market is experiencing significant transformation as consumer preferences increasingly shift toward healthier and more natural food options. Rising awareness of the impact of diet on lifestyle-related health conditions is driving demand for products free from synthetic pesticides, artificial additives, and chemical fertilizers. This trend is particularly evident among health-conscious urban consumers, including millennials and dual-income households, who are actively seeking nutritious and clean-label alternatives. Government initiatives promoting organic farming and certification have strengthened the supply chain, ensuring consistent availability of high-quality raw materials for processed organic foods. Corporate investment is also accelerating market growth, exemplified by Tata Consumer Products’ strategic acquisition of Organic India, which underscores growing institutional interest in the sector. Leveraging expansive distribution networks, such investments are enhancing product accessibility across retail and online channels, supporting the adoption of organic pasta, and contributing to the broader development of India’s organized organic food ecosystem.

India Organic Pasta Market Trends:

Surge in Clean-Label and Certified Organic Food Demand

Indian consumers are increasingly scrutinizing ingredient labels, propelling demand for clean-label organic pasta products free from artificial preservatives and chemical inputs. This shift is most visible in metro cities, where health-aware shoppers prioritize transparency. FSSAI's 2025 focus on stricter organic labeling standards and consumer awareness campaigns has formalized the clean-label movement. Health-focused brands are responding by launching fortified and multigrain organic pasta variants, catering to fitness-conscious consumers seeking both nutrition and convenience.

Rapid Expansion of E-Commerce and Quick Commerce Channels

The expansion of digital retail platforms is significantly enhancing the accessibility of organic pasta and other organic food products across urban and semi-urban India. E-commerce and quick-commerce players are increasingly catering to health-conscious consumers, offering convenient delivery of certified organic staples, including grains, specialty foods, and pasta. Partnerships between online platforms and organic brands are enabling faster, more efficient distribution, while also broadening the customer base. This digital push is helping consumers easily adopt organic diets, supporting market growth, and strengthening the presence of organic products in both traditional and modern retail channels.

Government-Led Organic Agriculture Expansion Strengthening Supply Chains

Policy support is playing a catalytic role in scaling India's organic food ecosystem. Through PKVY and MOVCDNER schemes, approximately 59.74 lakh hectares had been brought under organic farming practices by March 2025, with associated financial aid, certification support, and marketing linkages for farmers. In Gujarat, a significant number of farmers achieved organic certification, expanding the supply of certified organic produce. Complementing this, the government launched a digital traceability platform, TraceNet 2.0, enhancing transparency, credibility, and consumer confidence in certified organic products across the market.

Market Outlook 2026-2034:

The India organic pasta market is set for steady growth, driven by increasing health awareness among consumers, expanding urban populations, and broader availability of certified organic products in retail channels. Rising interest in nutritious and clean-label foods, combined with greater adoption of online grocery platforms, is fueling demand. Additionally, the entry of major FMCG companies into the organic food segment is enhancing product variety and accessibility, further strengthening consumer adoption. These factors collectively support the sustained expansion of the organic pasta market across diverse urban and semi-urban regions. The market generated a revenue of USD 32.56 Million in 2025 and is projected to reach a revenue of USD 72.49 Million by 2034, growing at a compound annual growth rate of 8.97% from 2026-2034.

India Organic Pasta Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product Type |

Wheat Source |

35.0% |

|

Application |

Residential |

55.0% |

|

Distribution Channel |

Offline Stores |

52.0% |

|

Region |

West India |

32.0% |

Product Type Insights:

- Wheat Source

- Rice Source

- Legumes Source

- Others

Wheat source dominates the market share of 35.0% of the total India organic pasta market in 2025.

Wheat-based organic pasta holds the dominant share in the Indian market owing to its deeply ingrained consumer familiarity and superior culinary adaptability. Organic durum wheat and whole wheat varieties are well-suited to a wide range of Indian cooking styles, from traditional sauces to fusion preparations incorporating native spices. The category benefits from the highest production volumes among certified organic grain types, supported by government schemes promoting organic wheat cultivation across states like Madhya Pradesh, Punjab, and Uttarakhand. Consumers associate wheat-based pasta with familiar texture, reliable cooking outcomes, and perceived nutritional superiority over refined alternatives.

The organic pasta segment is gaining momentum as health-focused brands introduce whole wheat and multigrain variants that blend wheat with millets or legumes, appealing to nutrition-conscious consumers. These products cater to growing demand for fiber-rich, low-glycemic, and wholesome alternatives to refined grains. Dietary guidelines promoting healthier eating habits are further encouraging consumers to opt for organic whole wheat pasta as a nutritious and better-for-you carbohydrate option. Such innovations and awareness initiatives are reinforcing the segment’s popularity and sustaining its growth trajectory across urban and semi-urban markets.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Residential

- Commercial

Residential leads the market share of 55.0% of the total India organic pasta market in 2025.

The residential segment's dominance reflects the broad-based shift toward home cooking among health-conscious families, particularly in post-pandemic India, where greater awareness of food quality and ingredient sourcing has taken hold. Urban households with children are increasingly opting for organic pasta as a nutritious weekday meal option, driven by parental concerns about pesticide residues in conventional food products. Rising internet and social media penetration have amplified this trend, with cooking influencers and wellness platforms extensively promoting organic pasta recipes, making the product more visible and desirable among homemakers and working professionals alike.

Health-focused direct-to-consumer brands are driving strong demand for cleaner pasta alternatives, offering products made from whole-grain, maida-free ingredients that appeal to nutrition-conscious households. Wider distribution through supermarkets and e-commerce platforms is further supporting the segment by improving accessibility and reducing the price gap with conventional pasta. These developments are making organic pasta an increasingly attractive and affordable choice for a broader range of consumers, reinforcing its adoption in residential kitchens and sustaining growth across urban and semi-urban markets.

Distribution Channel Insights:

- Offline Stores

- Online Stores

Offline stores represent the highest revenue share of 52.0% of the total India organic pasta market in 2025.

Offline retail channels continue to dominate organic pasta distribution in India due to the consumer preference for physically inspecting product packaging, certification labels, and ingredient lists before purchase. Supermarkets and hypermarkets in metro cities have dedicated organic food sections that provide curated product assortments, building consumer trust through physical presence. Specialty organic retailers and natural food stores in cities such as Mumbai, Bengaluru, Delhi NCR, and Pune have further entrenched the offline channel as the primary touchpoint for premium organic food products. Modern trade retailers actively offer promotional discounts and bundled deals on organic food ranges, adding to the channel's attractiveness.

The offline channel is not weak, as the large networks of distribution of the large FMCG players that enter the organic segment support it. With the inclusion of organic brands in strategic acquisitions, retail touchpoints nationwide have been available in the form of grocery stores, modern trade stores, and pharmacy chains, which has greatly increased product availability. It is projected that this increased offline presence will retain its presence, despite the increased pace of online channels, which will ensure that certified organic products such as pasta will be available in the hands of the largest possible number of consumers in the urban and semi-urban markets.

Regional Insights:

- North India

- South India

- East India

- West India

West India exhibits a clear dominance with a 32.0% share of the total India organic pasta market in 2025.

West India, encompassing Maharashtra, Gujarat, and Goa, is the largest regional market for organic pasta in India, driven by the high concentration of health-conscious, high-income urban consumers in cities such as Mumbai, Pune, and Ahmedabad. The region benefits from a robust modern retail infrastructure including premium supermarkets, organic specialty stores, and an active D2C e-commerce ecosystem. Organic café culture, driven by wellness-oriented food chains in Mumbai and Pune, has normalized premium organic food consumption among millennials and working professionals.

North India, particularly Delhi NCR and Uttar Pradesh, represents the second-largest regional market, supported by rising disposable incomes, a large urban middle class, and the rapid expansion of modern trade retail. South India, led by Karnataka and Tamil Nadu, is witnessing an accelerating demand driven by IT-sector employment clusters and a tech-savvy consumer base open to international food formats. East India remains the smallest market due to lower organic awareness and limited retail infrastructure, though government-backed PKVY initiatives in states like West Bengal and Odisha are gradually expanding the organic farming base and consumer accessibility.

Market Dynamics:

Growth Drivers:

Why is the India Organic Pasta Market Growing?

Rising Health Consciousness and Demand for Clean-Label Nutrition

The growing prevalence of lifestyle-related diseases such as obesity, diabetes, and cardiovascular disorders is compelling Indian consumers to reassess their dietary choices, with a distinct preference emerging for foods that are free from synthetic chemicals, pesticide residues, and artificial additives. The shift toward healthier eating is especially evident among urban millennials and Gen Z, who actively look for verified organic certifications on food products. Growing awareness of the benefits of whole, minimally processed foods is encouraging consumers to reduce refined grain intake, directly boosting the adoption and consumption of organic pasta as a nutritious alternative. The India organic food market size was valued at USD 2,303.31 Million in 2025 and is projected to reach USD 11,296.09 Million by 2034, growing at a compound annual growth rate of 19.32% from 2026-2034, reflecting the scale of this behavioral shift. As awareness of long-term health outcomes linked to conventional food inputs grows, organic pasta is increasingly positioned as a premium yet accessible pathway to cleaner eating among nutrition-aware households.

Government Initiatives Expanding the Certified Organic Supply Chain

India’s policy framework has played a key role in developing a strong certified organic supply chain that supports the growth of organic pasta. Government initiatives promoting organic farming provide financial support, certification assistance, and market linkages, encouraging more farmers to adopt chemical-free practices. The National Programme for Organic Production (NPOP) offers a standardized certification system, enhancing consumer confidence in verified organic products. Additionally, digital traceability platforms enable tracking of organic produce from farm to shelf, improving supply chain transparency. These interventions are strengthening the availability of high-quality organic raw materials, ensuring consistent product quality and competitive pricing in the organic pasta market.

Urbanization, Westernization of Diets, and Growth of Digital Food Commerce

India’s rapid urbanization is expanding a consumer base increasingly influenced by global food trends, social media, and exposure to international cuisines. As more people settle in tier-I and tier-II cities, pasta has gained mainstream acceptance, with a growing preference for organic and clean-label options. The rise of e-commerce and quick-commerce platforms has extended the reach of organic pasta beyond metropolitan centers. Additionally, the entry of major FMCG players into the organic food segment has strengthened distribution networks and enhanced consumer awareness, further driving adoption and market growth.

Market Restraints:

What Challenges the India Organic Pasta Market is Facing?

Premium Pricing Restricting Mass-Market Penetration

Organic pasta commands a significant price premium over conventional pasta products, limiting its affordability for a large segment of price-sensitive Indian consumers. The additional costs associated with certified organic raw materials, compliance with NPOP or USDA Organic standards, and smaller production volumes make it difficult for manufacturers to achieve price parity with mainstream options. This premium creates a distinct accessibility gap that constrains adoption beyond affluent urban households and restricts market expansion into tier-III cities and rural areas.

Inconsistent Organic Certification and Supply Chain Fragmentation

Despite established certification frameworks under NPOP and the Participatory Guarantee System (PGS), the quality and consistency of certified organic products remain uneven across India's fragmented agricultural supply chain. Limited access to certification infrastructure in remote farming regions, lack of technical knowledge among smallholder farmers, and insufficient cold-chain logistics create quality variability that erodes consumer confidence. These structural gaps can result in inconsistent product availability and make it challenging for organic pasta brands to guarantee reliable supply at scale throughout the forecast period.

Low Organic Awareness in Tier-III and Rural Markets

Consumer awareness of the health benefits and distinguishing characteristics of certified organic food products remains substantially lower outside India's major metropolitan areas. In tier-III cities and rural regions, limited exposure to organic food marketing, lack of dedicated retail distribution networks, and strong dominance of conventional pasta brands at competitive price points constrain the uptake of organic variants. Overcoming this awareness deficit requires sustained educational campaigns, improved product accessibility, and the development of rural distribution infrastructure, all of which demand significant long-term investment.

Competitive Landscape:

The India organic pasta market is characterized by a moderately fragmented competitive landscape featuring a mix of large domestic FMCG conglomerates, specialized organic food companies, and agile D2C health food startups. Market participants compete on dimensions of organic certification authenticity, product diversity, pricing strategy, and distribution reach. The entry of large corporations into the organic space, such as through strategic acquisitions and portfolio expansions, is intensifying competition and accelerating mainstream adoption. Meanwhile, health-focused D2C brands leverage social media and digital commerce to establish strong brand identities among younger, urban consumers. Regional organic food producers also maintain competitive positions in local markets by offering proximity advantages and direct farm-to-consumer narratives.

Recent Developments:

- May 2025: Organic India, acquired by Tata Consumer Products in 2024, entered a brand ambassador partnership to deepen consumer engagement and strengthen its organic product portfolio positioning across India. With TCPL's distribution network covering over 275 million Indian households, the brand is significantly expanding its retail footprint, enhancing accessibility of certified organic products including processed food categories.

- November 2024: In Gujarat, approximately 1,250 farmers secured organic certification for around 2,250 acres of agricultural land, converting it to chemical-free farming practices. This development strengthens the certified organic raw material supply chain in West India, the largest regional market for organic pasta, supporting greater product availability and competitive pricing.

- January 2024: Tata Consumer Products completed the acquisition of Organic India, a leading organic food and wellness brand, as part of a strategic effort to strengthen its health-focused product portfolio. This deal is expected to leverage TCPL's extensive pan-India and international distribution network to accelerate the growth of organic processed food categories, creating favorable downstream conditions for the organic pasta market.

India Organic Pasta Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Wheat Source, Rice Source, Legumes Source, Others |

| Applications Covered | Residential, Commercial |

| Distribution Channels Covered | Offline Stores, Online Stores |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Organic Pasta Market Report

The India organic pasta market size was valued at USD 32.56 Million in 2025.

The India organic pasta market is expected to grow at a compound annual growth rate of 8.97% from 2026-2034 to reach USD 72.49 Million by 2034.

Wheat source held the largest market share of 35.0% in 2025, driven by its widespread consumer familiarity, superior culinary adaptability, higher organic wheat production volumes, and strong preference among households preparing a diverse range of pasta-based meals.

Key factors driving the India organic pasta market include rising health consciousness and demand for pesticide-free food, government initiatives expanding certified organic farming acreage through PKVY and NPOP, rapid urbanization and westernization of dietary preferences, and the proliferation of e-commerce platforms broadening organic product accessibility.

Major challenges include high price premiums restricting mass-market adoption, inconsistent organic certification and fragmented supply chains across India's diverse agricultural regions, low consumer awareness of organic food benefits in tier-III cities and rural areas and limited cold-chain infrastructure constraining product distribution beyond metropolitan markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)