India Outsourcing Services Market Size, Share, Trends and Forecast by Service Type, Deployment Type, Industry Vertical, and Region, 2026-2034

India Outsourcing Services Market Summary:

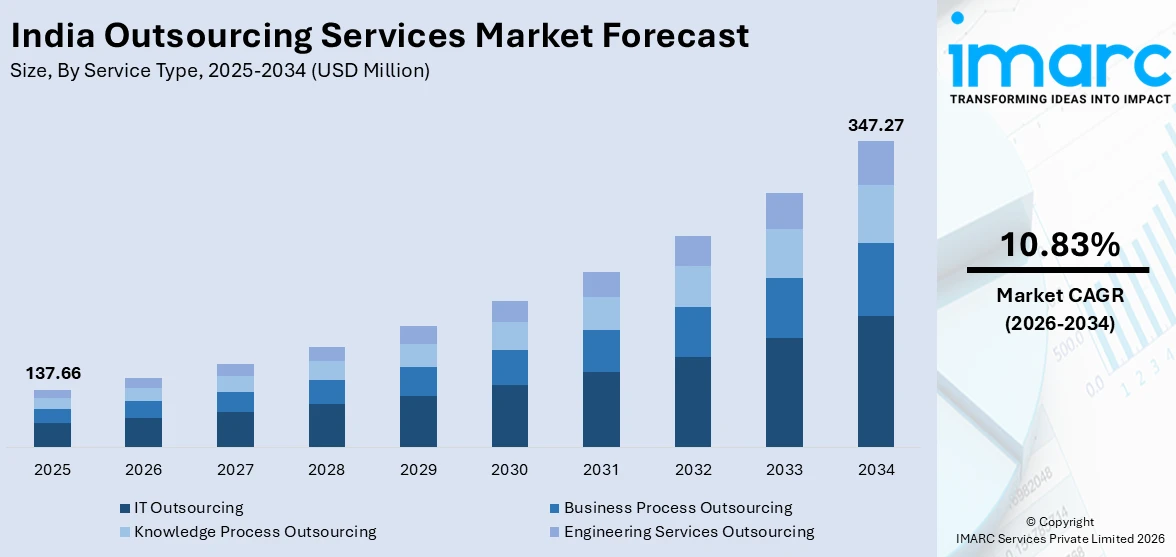

The India outsourcing services market size reached USD 137.66 Million in 2025. The market is projected to reach USD 347.27 Million by 2034, growing at a CAGR of 10.83% during 2026-2034. The market is driven by government-led digital infrastructure development through initiatives like Digital India and BharatNet that have connected over 500,000 villages with high-speed internet, artificial intelligence, and automation integration, transforming traditional service delivery models with major firms training hundreds of thousands of employees in AI capabilities, and a strategic shift towards high-value outcome-based engagements with 36% of companies moving away from traditional FTE-based contracts. Additionally, the expanding presence of Global Capability Centres and continuous talent upskilling initiatives are propelling the India outsourcing services market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

| Market Size in 2025 | USD 137.66 Million |

| Market Forecast in 2034 | USD 347.27 Million |

| Market Growth Rate (2026-2034) | 10.83% |

| Key Segments | Service Type (IT Outsourcing, Business Process Outsourcing, Knowledge Process Outsourcing, Engineering Services Outsourcing), Deployment Type (Onshore Outsourcing, Nearshore Outsourcing, Offshore Outsourcing), Industry Vertical (BFSI, Healthcare and Life Sciences, IT and Telecommunications, Retail and E-commerce, Manufacturing, Transportation and Logistics, Government and Public Sector, Others) |

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

India Outsourcing Services Market Outlook (2026-2034):

The India outsourcing services market is positioned for robust expansion, propelled by accelerating digital transformation initiatives, strategic investments in artificial intelligence infrastructure, and evolving client demand for innovation-led partnerships. Government policies supporting technology adoption, including expanded digital connectivity through BharatNet and skills development programs, will strengthen the talent ecosystem and operational infrastructure. The integration of outcome-based commercial models and hybrid sourcing strategies will drive value creation, while partnerships between Indian firms and global technology leaders will enhance AI and automation capabilities. Additionally, the establishment of specialized Centers of Excellence and increasing adoption of cloud-based delivery models will enable scalable, efficient service delivery across diverse industry verticals throughout the forecast period.

To get more information on this market Request Sample

Impact of AI:

Artificial intelligence is fundamentally transforming India's outsourcing services market by automating routine tasks, enabling intelligent workflows, and shifting the industry toward higher-value service delivery. Major outsourcing firms are investing heavily in AI capabilities, with companies like TCS training over 100,000 employees in AI and machine learning. By 2028, nearly 60% of outsourced services are predicted to incorporate robotic process automation, significantly increasing operational efficiency while creating challenges for traditional labor-intensive roles. While AI adoption threatens displacement of lower-end jobs, it simultaneously expands the total addressable market as enterprises increasingly outsource complex, AI-enabled work including predictive analytics, intelligent document processing, and automated customer service. India's IT sector is projected to reach $400 billion by 2030, driven by firms delivering domain-specific automation that outperforms traditional service models on speed, quality, and cost, positioning the industry for sustained growth through technology-led differentiation.

Market Dynamics:

Key Market Trends & Growth Drivers:

Government-Led Digital Infrastructure Development Accelerating Outsourcing Capabilities

The Indian government's Digital India initiative, launched in 2015 and celebrating its 10th anniversary in 2025, continues to strengthen the country's digital infrastructure through substantial investments in connectivity and technology adoption. The BharatNet project has connected over 500,000 villages with high-speed internet as of 2024, extending reliable connectivity to even remote areas and enabling outsourcing operations beyond traditional urban centers. The initiative has driven India's digital population to 806 million users as of February 2025, up from 688 million in 2020, creating an expansive ecosystem for digital services delivery. The government's strategic investment includes 63 Software Technology Parks of India and 1,500 Global Capability Centres that provide world-class infrastructure supporting the outsourcing ecosystem with modern facilities, high-speed networks, and collaborative environments. Additionally, policies like Skill India ensure a continuous pipeline of skilled talent through upskilling initiatives, with over 70% of outsourcing companies planning to increase employee training spending by 2025 to address evolving technological demands. In February 2025, India's Ministry of Electronics and Information Technology reported significant progress under the Digital India Programme, with DigiLocker expanding to over 53.84 crore registered users and issuing more than 949.24 crore documents digitally as of June 2025. These comprehensive government efforts create an enabling environment that positions India as a technologically advanced and scalable outsourcing destination, reducing operational barriers and facilitating seamless service delivery to global clients across multiple time zones and industry verticals.

Artificial Intelligence and Automation Integration Transforming Service Delivery Models

Indian outsourcing firms are rapidly integrating artificial intelligence and robotic process automation into their service delivery, fundamentally transforming traditional labor-intensive models into technology-enabled intelligent workflows that deliver superior value propositions. Major IT services companies including TCS, Infosys, and Wipro have made substantial investments in AI capabilities, with TCS training over 100,000 employees in AI and machine learning, while Infosys has developed AI awareness programs for 270,000 staff members to ensure organization-wide capability building. By 2028, nearly 60% of all outsourced services in India are predicted to incorporate some form of RPA, significantly increasing from around 25% today, marking a fundamental shift in operational paradigms. The shift towards AI-native operations is enabling firms to deliver faster project turnaround times, enhanced operational efficiency, and superior service quality while simultaneously addressing client demands for cost optimization and measurable business outcomes. Companies are establishing AI Centers of Excellence and AI Foundries to test and deploy solutions across sectors including banking, healthcare, manufacturing, and retail, creating specialized domain expertise. In January 2025, Infosys and Google Cloud launched an AI innovation hub in Bengaluru, significantly enhancing India's IT outsourcing capabilities through accelerated development of AI-driven enterprise solutions. This technological transformation is reshaping India's value proposition from cost arbitrage to innovation-driven partnerships, positioning the India outsourcing services market growth to capture a projected $400 billion market by 2030 as global enterprises increasingly seek intelligent automation and data-driven decision support.

Strategic Shift Towards High-Value, Outcome-Based Engagements

The outsourcing industry is witnessing a paradigm shift from traditional transactional, FTE-based contracts to strategic, outcome-based engagements that deliver measurable business results and align service provider incentives with client success metrics. According to Deloitte's February 2025 report, 81% of organizations plan to increase outsourcing efforts over the next three to five years, with better alignment with business strategy overtaking cost savings as the primary driver for outsourcing decisions. Approximately 36% of companies have shifted to outcome-based contracts, moving away from traditional Full-Time Equivalent pricing models that focused purely on resource deployment rather than value creation. This transformation reflects increasing client demand for value-driven, innovation-led collaborations rather than simple labor arbitrage or transactional service arrangements. Organizations are now outsourcing higher-value strategic services including research and development, financial planning and analysis, AI-enabled workflows, and comprehensive digital transformation initiatives that require deep domain expertise and strategic thinking. About 55% of organizations have adopted hybrid sourcing models combining Global Business Services with third-party providers for improved governance, risk management, and operational efficiency across their outsourcing portfolios. Strategic supplier collaborations enable organizations to achieve average annual cost savings of 10 to 25 percent, with some reaching 15 to 35 percent through balanced vendor portfolios that optimize the mix of large strategic providers and specialized niche players. Nearly 45% of mature outsourcing firms now operate dedicated Vendor Management Offices to enhance governance, supplier risk management, and outsourcing effectiveness through structured oversight mechanisms. This evolution positions Indian firms as strategic partners driving business transformation and innovation rather than mere service providers executing predefined tasks, fundamentally elevating the industry's role in global enterprise value chains.

Key Market Challenges:

Talent Shortage and High Attrition Rates Impacting Service Delivery

Despite India's large talent pool producing over 1.5 million engineering graduates annually, the outsourcing industry faces significant challenges with talent shortages in specialized skills and persistently high attrition rates that disrupt project continuity and client relationships. There exists a critical shortage of professionals with two to five years of experience, representing key personnel essential for effective project execution, client management, and knowledge transfer between junior and senior team members. Average attrition rates across the sector stand at 15.4 percent, with some IT suppliers reporting rates as high as 35 percent, driven by aggressive competition for skilled talent and the lure of higher compensation packages in a tight labor market. WTW's 2024 Salary Budget Planning Report projects India's BPO industry will continue increasing salaries annually by 9.5 percent in 2025 to combat high turnover, significantly eroding the traditional cost arbitrage advantage that historically made India an attractive outsourcing destination. The rapid adoption of AI and emerging technologies has created intense demand for specialized skills in areas like data science, cybersecurity, AI and ML development, and cloud architecture, where supply significantly lags demand and compensation expectations exceed industry norms. Entry-level hiring has dropped to 50 percent below pre-pandemic levels, with Q1 2025 seeing leading IT services firms add just 4,787 net employees compared to tens of thousands in previous years, reflecting cautious workforce expansion amid automation-driven productivity gains. This talent crunch forces vendors to subcontract projects to third parties, operate with less experienced teams, or invest heavily in accelerated training programs, all of which can potentially compromise service quality, increase project risks, and impact client satisfaction in an increasingly competitive global marketplace.

Intensifying Global Competition and Margin Pressure from Automation

Indian outsourcing firms face mounting competitive pressure from multiple fronts including rival service providers, disruptive automation technologies, and rapidly evolving client expectations, creating significant margin compression challenges that threaten traditional business models. The emergence of AI-native challengers offering faster, leaner, and more cost-efficient business models built specifically for intelligence-led outsourcing is intensifying competition in an environment of subdued industry growth and cautious client spending. Cognizant's turnaround under CEO Ravi Kumar, featuring organic growth rates exceeding major Indian IT peers through renewed focus on large deals and AI-led productivity commitments, demonstrates how revitalized competitors can erode market share previously enjoyed by established Indian players. Traditional billable-hour models face fundamental disruption as AI enables faster project delivery with significantly fewer people, forcing companies to transition to outcome-based pricing where clients pay for business results and value creation rather than time spent or resources deployed. This pricing transformation puts pressure on revenue growth and profit margins even as companies invest heavily in AI capabilities, cloud infrastructure, talent upskilling programs, and innovation initiatives that require substantial capital allocation. The industry must navigate these competitive headwinds, technology disruptions, and policy uncertainties while maintaining profitability, justifying premium positioning through innovation and strategic value delivery, and demonstrating clear return on investment to increasingly demanding global clients.

Data Security Concerns and Regulatory Compliance Complexity

Managing data security, privacy protection, and evolving regulatory compliance requirements across multiple jurisdictions presents ongoing operational challenges for Indian outsourcing providers handling sensitive client information across financial services, healthcare, government, and other regulated sectors. The implementation of India's Digital Personal Data Protection Act 2023, with its phased enforcement approach and detailed requirements for data protection, cyber incident reporting, and cross-border data transfers, creates compliance uncertainty for both outsourcing companies and their global clients navigating new regulatory frameworks. While many major corporations implemented GDPR compliance measures years ago, adapting to DPDPA's specific requirements including restrictions on data transfers to certain countries, mandatory parental consent for children's data regardless of business focus, and strict incident reporting timelines requires significant operational adjustments and process reengineering. Cybersecurity threats continue escalating globally with sophisticated ransomware attacks, data breaches, and advanced persistent threats, raising client concerns about outsourcing sensitive operations, intellectual property, and confidential business information to third parties in offshore locations. Despite India's IT Act incorporating electronic contract and cybercrime provisions, and companies achieving international certifications like ISO 27001, SOC 2, and industry-specific accreditations, some clients remain hesitant about offshore data processing due to perceived risks around data sovereignty, compliance gaps, and potential security vulnerabilities in complex multi-party arrangements. Outsourcing agreements increasingly require stringent data security provisions, end-to-end encryption protocols, regular third-party security audits, penetration testing, and robust compliance monitoring frameworks, adding significant complexity and cost to service delivery operations. The challenge is compounded by sector-specific regulations such as those from India's central bank for financial services and HIPAA requirements for healthcare, creating data localization requirements that complicate global delivery models, restrict operational flexibility, and necessitate investment in distributed infrastructure across multiple geographies.

India Outsourcing Services Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the India outsourcing services market, along with forecasts at the country and regional levels for 2026-2034. The market has been categorized based on service type, deployment type, and industry vertical.

Analysis by Service Type:

- IT Outsourcing

- Business Process Outsourcing

- Knowledge Process Outsourcing

- Engineering Services Outsourcing

The report has provided a detailed breakup and analysis of the market based on the service type. This includes IT outsourcing, business process outsourcing, knowledge process outsourcing, and engineering services outsourcing.

Analysis by Deployment Type:

- Onshore Outsourcing

- Nearshore Outsourcing

- Offshore Outsourcing

A detailed breakup and analysis of the market based on the deployment type have also been provided in the report. This includes onshore outsourcing, nearshore outsourcing, and offshore outsourcing.

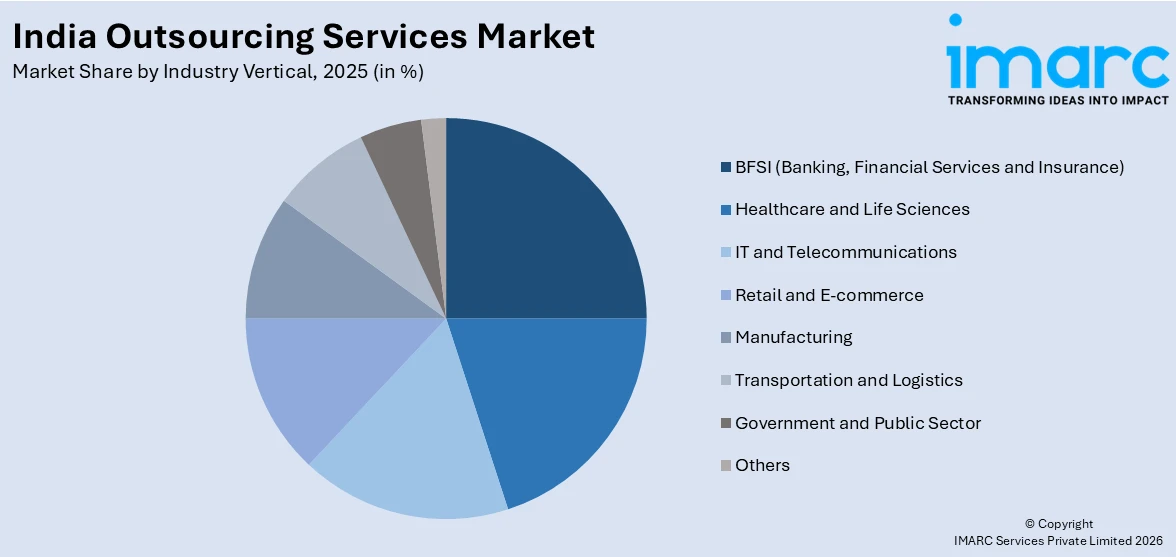

Analysis by Industry Vertical:

Access the comprehensive market breakdown Request Sample

- BFSI (Banking, Financial Services and Insurance)

- Healthcare and Life Sciences

- IT and Telecommunications

- Retail and E-commerce

- Manufacturing

- Transportation and Logistics

- Government and Public Sector

- Others

The report has provided a detailed breakup and analysis of the market based on the industry vertical. This includes BFSI, healthcare and life sciences, IT and telecommunications, retail and e-commerce, manufacturing, transportation and logistics, government and public sector, and others.

Analysis by Region:

- North India

- South India

- East India

- West India

The report has also provided a comprehensive analysis of all the major regional markets, which include North India, South India, East India, and West India.

Competitive Landscape:

The India outsourcing services market features a dynamic competitive environment characterized by the presence of global multinational corporations, established Indian IT giants, and emerging specialized service providers competing across diverse service segments and industry verticals. Competition primarily revolves around technological capabilities, domain expertise, pricing competitiveness, service quality, and the ability to deliver measurable business outcomes rather than traditional cost arbitrage alone. Leading players are increasingly differentiating through strategic investments in artificial intelligence, automation platforms, industry-specific solutions, and outcome-based commercial models that align provider incentives with client success. The market exhibits significant consolidation in traditional IT services while experiencing fragmentation in specialized areas like AI-enabled services, knowledge process outsourcing, and engineering research and development. Major firms leverage their scale, global delivery networks, established client relationships, and brand reputation to secure large multi-year contracts, while niche players compete through deep domain expertise, agility, and innovative service models. Strategic partnerships with technology leaders including Microsoft, Google Cloud, Amazon Web Services, Salesforce, and NVIDIA enable Indian firms to rapidly integrate cutting-edge platforms and tools into client solutions. The competitive landscape is further shaped by the rise of Global Capability Centres established by Fortune 500 companies in India, which represent both captive alternatives and potential collaboration opportunities for third-party service providers seeking to complement in-house capabilities with specialized external expertise.

India Outsourcing Services Industry Latest Developments:

- December 2024: Wipro acquired Applied Value Technologies, a Massachusetts-based IT consulting firm, for $40 million in an all-cash transaction. The acquisition strengthens Wipro's application services capabilities and creates new growth opportunities as part of the company's ongoing business turnaround strategy. AVT helps enterprises transform IT operations through highly customized and data-driven approaches, complementing Wipro's existing service portfolio.

- April 2024: BDO India launched BDO EDGE, a Center of Excellence designed to enhance global outsourcing in tax, assurance, accounting, and technology services. This strategic initiative strengthens India's IT outsourcing segment by expanding service capabilities, leveraging skilled talent, and enabling cost-effective, 24/7 operations for global enterprises seeking comprehensive business process outsourcing solutions.

India Outsourcing Services Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Service Types Covered | IT Outsourcing, Business Process Outsourcing, Knowledge Process Outsourcing, Engineering Services Outsourcing |

| Deployment Types Covered | Onshore Outsourcing, Nearshore Outsourcing, Offshore Outsourcing |

| Industry Verticals Covered | BFSI (Banking, Financial Services and Insurance), Healthcare and Life Sciences, IT and Telecommunications, Retail and E-commerce, Manufacturing, Transportation and Logistics, Government and Public Sector, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India outsourcing services market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India outsourcing services market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India outsourcing services industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Outsourcing Services Market Report

The India outsourcing services market reached a value of USD 137.66 Million in 2025.

The market is projected to grow at a CAGR of 10.83% during 2026-2034, reaching USD 347.27 Million by 2034.

Key growth drivers include digital India connectivity infrastructure, AI and automation integration, outcome-based commercial models, and expanding Global Capability Centre investments in high-value services.

The report covers segmentation by service type, deployment type, industry vertical, and region. Each segment includes detailed market size and forecast analysis.

Key trends include AI-native service delivery models, cloud-based operations, robotic process automation uptake, and strategic acquisitions bringing domain expertise and international client access.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade