India Packaged Food Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Region, 2026-2034

India Packaged Food Market Size, Share, Trends & Forecast (2026-2034)

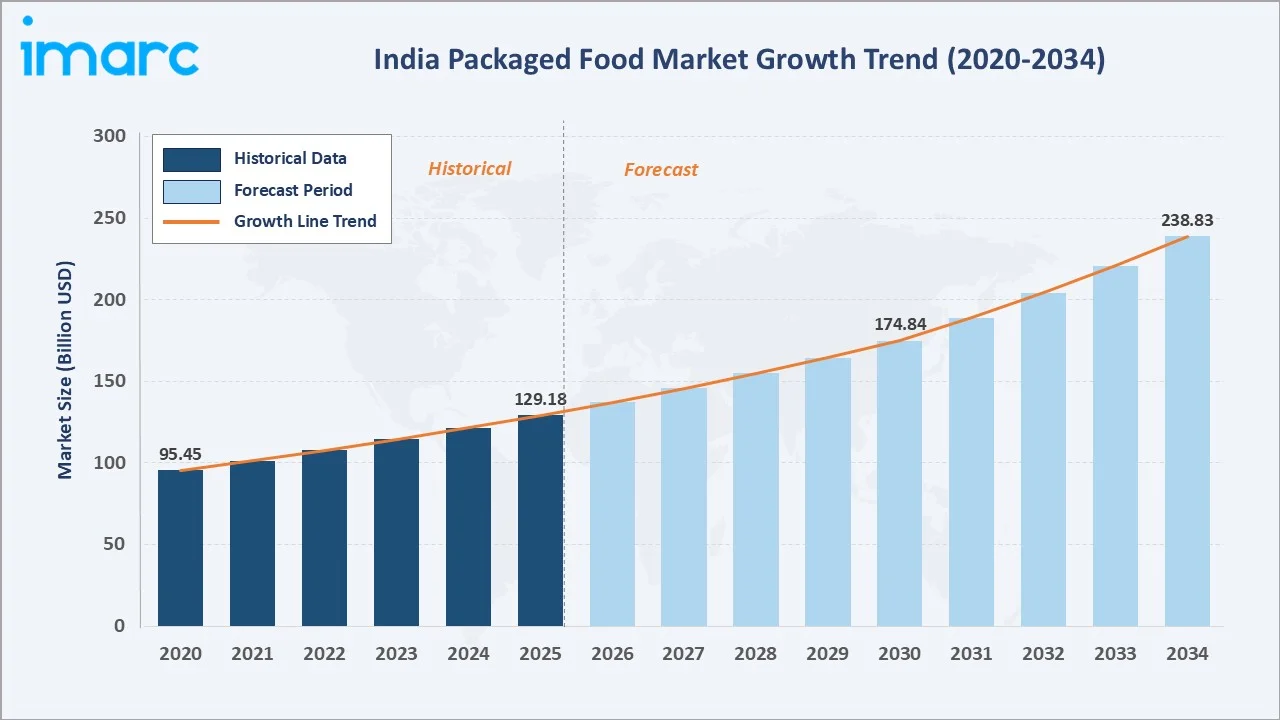

The India packaged food market was valued at USD 129.18 Billion in 2025 and is projected to reach USD 238.83 Billion by 2034, expanding at a CAGR of 6.24% over 2026-2034. Rising disposable incomes, rapid urbanization, expanding modern retail and quick commerce footprint, and growing demand for convenience-led foods are the principal drivers shaping market growth, supported by sustained policy push such as the Production Linked Incentive Scheme for Food Processing Industries (PLISFPI), which attracted cumulative investment of about INR 9,207 Crore by December 2025.

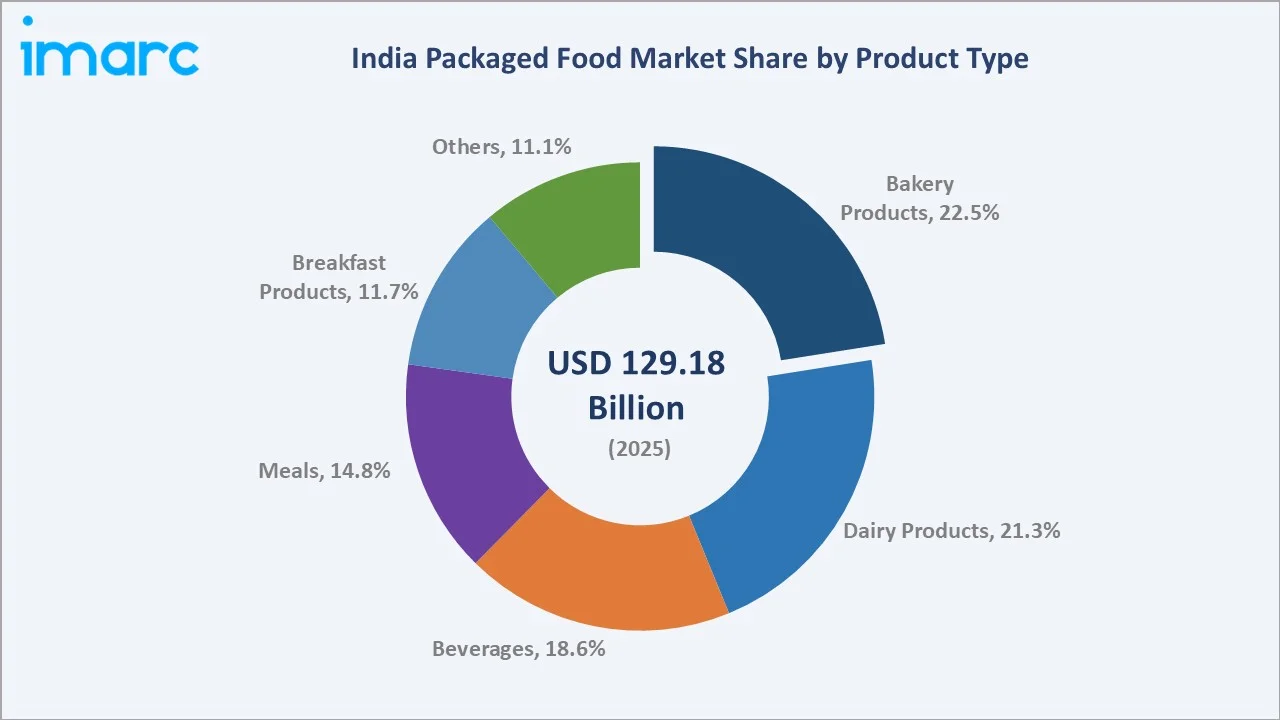

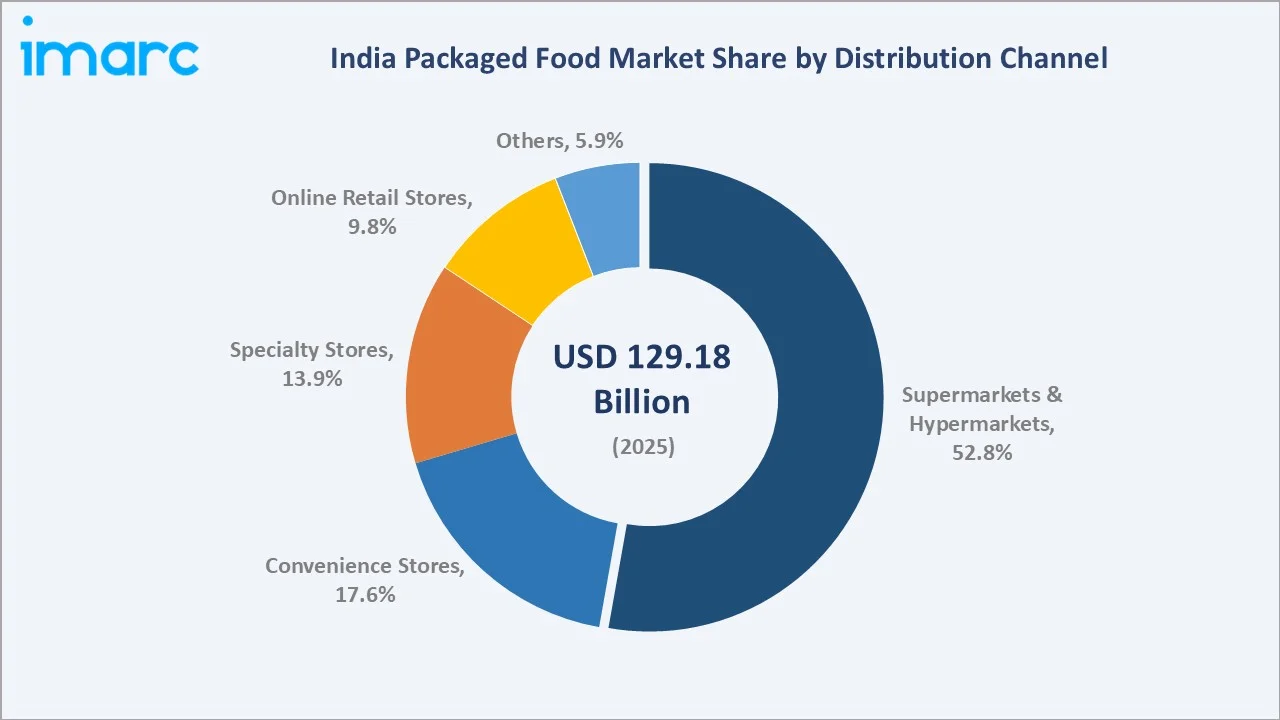

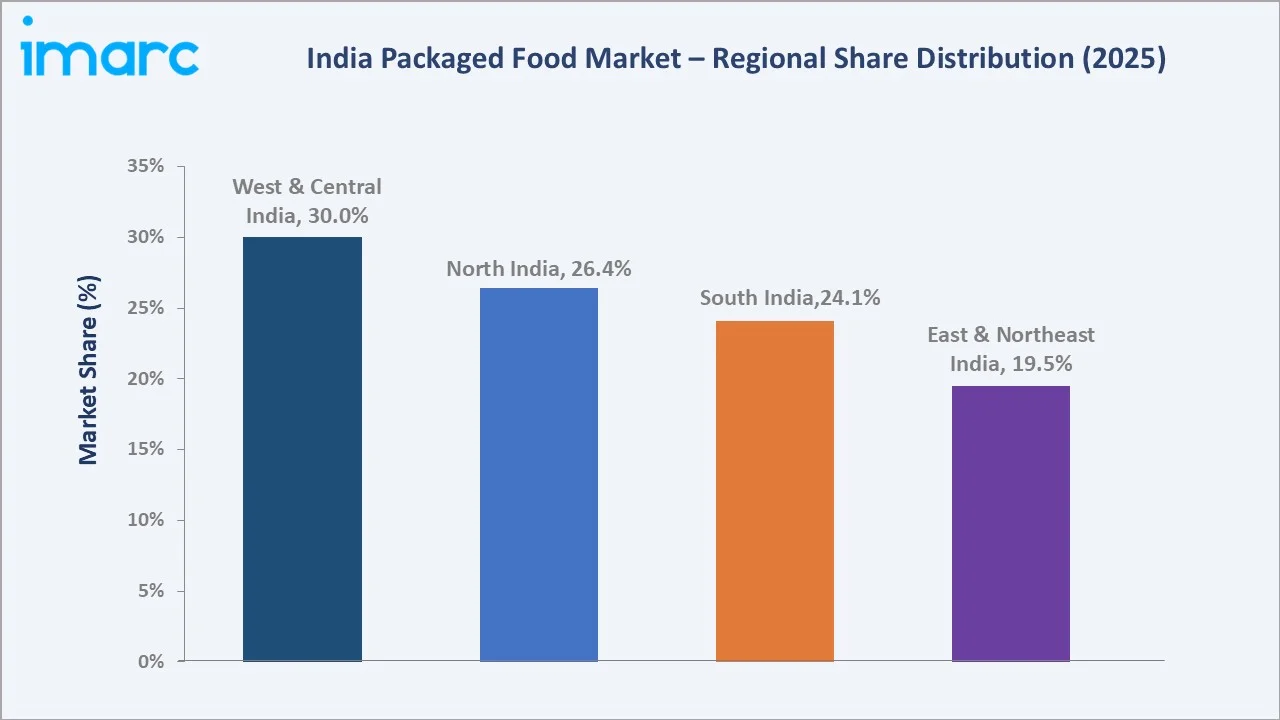

Bakery products lead the product type segment at 22.5%, supermarkets and hypermarkets dominate distribution channel at 52.8%, and West and Central India command 30.0% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 129.18 Billion |

|

Forecast Market Size (2034) |

USD 238.83 Billion |

|

CAGR (2026-2034) |

6.24% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West and Central India (30.0%, 2025) |

|

Fastest-Growing Region |

South India (24.1%, 2025) |

|

Leading Product Type |

Bakery Products (22.5%, 2025) |

|

Leading Distribution Channel |

Supermarkets and Hypermarkets (52.8%, 2025) |

The India packaged food market expanded from USD 95.45 Billion in 2020 to USD 129.18 Billion in 2025, driven by changing consumer lifestyles, deeper retail penetration, and rising demand for ready-to-eat (RTE) and ready-to-cook formats. Anchored at USD 174.84 Billion in 2030, the forecast to USD 238.83 Billion by 2034 reflects sustained middle-class expansion, rising women workforce participation, and continued investment in cold chain and food processing infrastructure.

To get more information on this market, Request Sample

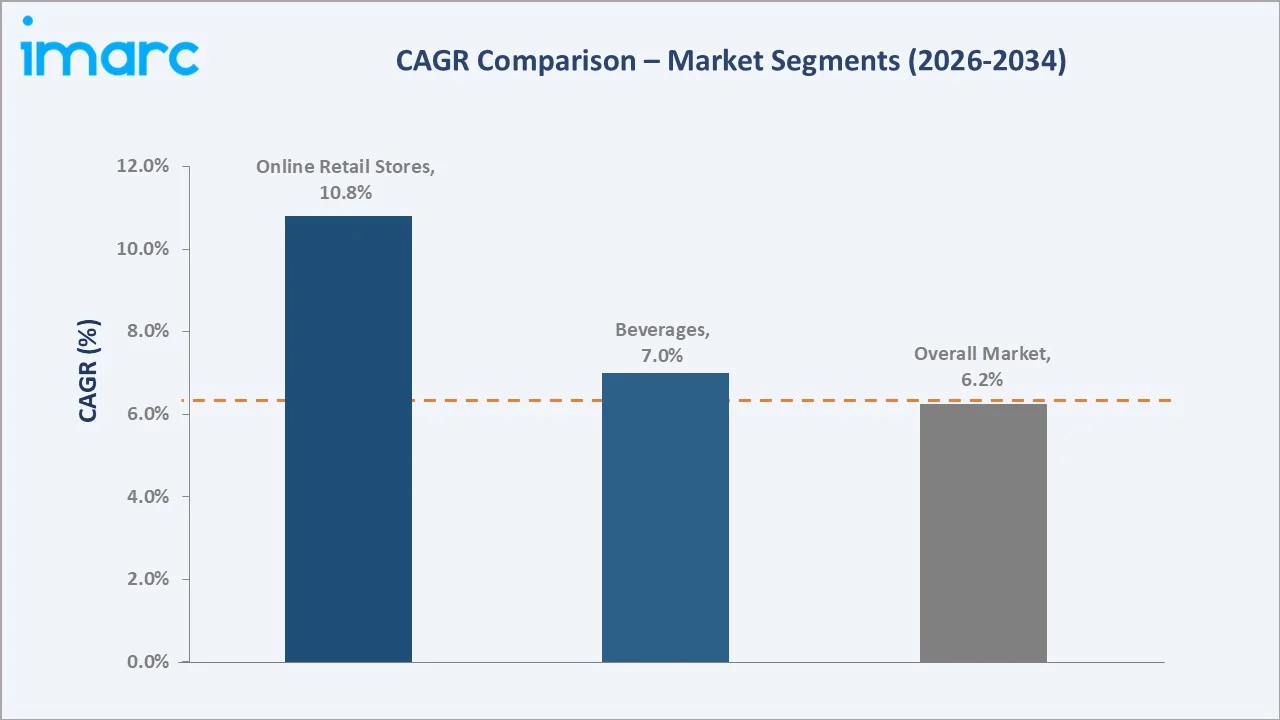

CAGR trajectories across the product type and distribution channel sub-segments show online retail stores and convenience stores expanding faster than the overall 6.24% market CAGR, supported by quick commerce densification, smartphone adoption, and shifting urban shopping habits.

Executive Summary

The India packaged food market is on a strong growth trajectory, expanding from USD 95.45 Billion in 2020 to a projected USD 238.83 Billion by 2034. Packaged formats have shifted from a metro-centric consumption pattern to a mainstream household choice across Tier-2 and Tier-3 markets. Rising disposable incomes, dual-income households, growing time scarcity, and improved cold chain and last-mile logistics are encouraging Indian consumers to switch from unbranded local fare to branded packaged alternatives across urban and semi-urban centres.

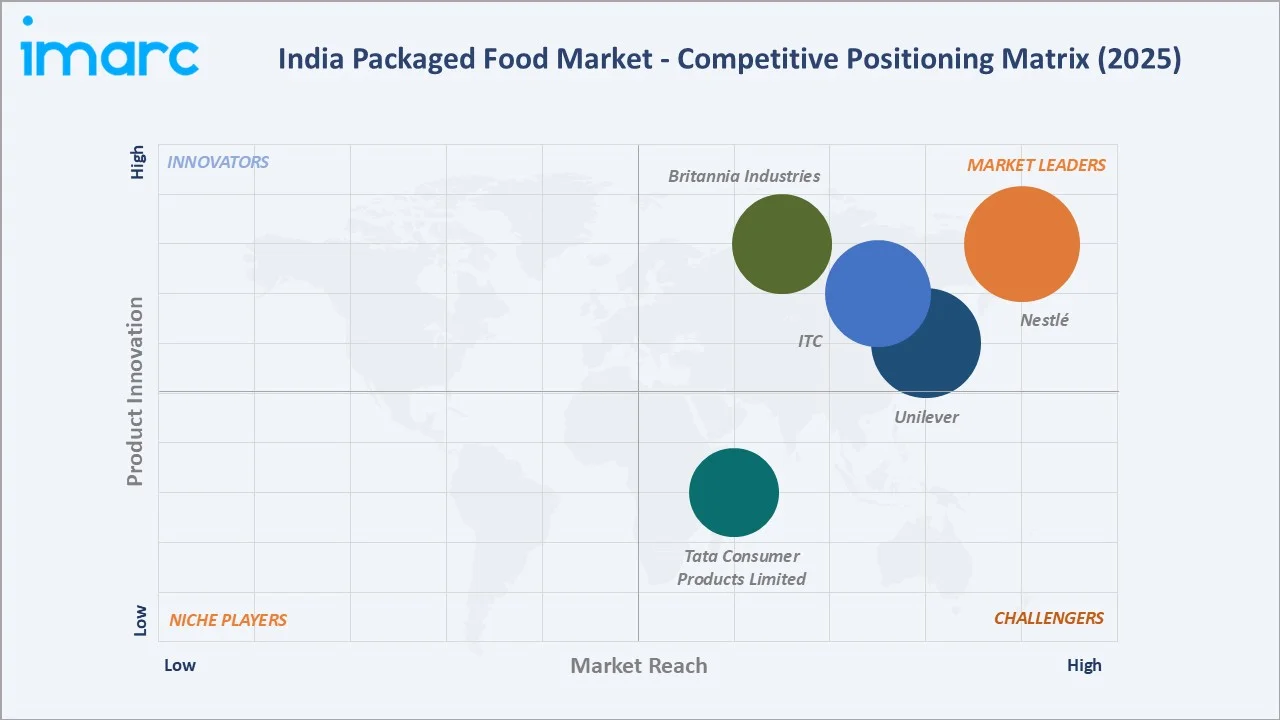

Bakery products dominate by product type at 22.5% in 2025, supported by mass affordability of biscuits, rusks, and packaged breads, while supermarkets and hypermarkets account for 52.8% of distribution channel sales. Competitive intensity is intensifying — in FY24, ITC’s foods business posted consolidated sales of INR 17,194.5 Crore, surpassing Britannia Industries at INR 16,769.2 Crore to become India's second-largest listed packaged foods company, with Nestlé India continuing to lead the field. West and Central India command 30.0% regional share, led by Maharashtra and Gujarat.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Bakery Products – 22.5% share (2025) |

|

Second Product Type |

Dairy Products – 21.3% share (2025) |

|

Largest Distribution Channel |

Supermarkets and Hypermarkets – 52.8% share (2025) |

|

Second Distribution Channel |

Convenience Stores – 17.6% share (2025) |

|

Leading Region |

West and Central India – 30.0% share (2025) |

|

Fastest-Growing Region |

South India – 24.1% share (2025) |

|

Top Companies |

Nestlé, ITC, Unilever, Britannia Industries, Tata Consumer Products Limited |

Key Analytical Observations Expanding on the Data Above:

- Bakery products at 22.5% lead the market, supported by mass affordability of biscuits, rusks, and packaged breads, deep distribution across kirana stores, and continuous product extension into low-sugar and fortified variants.

- Dairy products at 21.3% reflect India's position as the world's largest milk producer as per figures from the Food and Agriculture Organization, with packaged ghee, paneer, butter, and cheese gaining share as consumers move from loose to branded dairy formats.

- Supermarkets and hypermarkets at 52.8% continue to dominate distribution as modern retail expands beyond metros into Tier-2 and Tier-3 markets, with private-label launches and in-store promotions accelerating category creation.

- Convenience stores at 17.6% remain important for impulse and daily household purchases, particularly in urban neighborhoods and transit locations. Their extended operating hours, quick accessibility, and growing stocking of packaged snacks, dairy, and RTE products continue supporting steady category penetration across India.

- West and Central India at 30.0% lead regional consumption, anchored by Maharashtra and Gujarat, driven by a dense modern retail base, a strong food processing manufacturing cluster, and rising urban packaged-dairy uptake.

India Packaged Food Market Overview

Packaged food includes branded, processed food products designed for ready consumption or quick preparation, such as bakery products, dairy products, beverages, breakfast products, meals, and snacks. These products provide convenience, longer shelf life, hygiene assurance, portion consistency, and easier storage, matching the changing dietary and lifestyle preferences of modern consumers.

The Indian ecosystem connects raw material suppliers, food processing manufacturers, packaging companies, cold chain logistics providers, regulatory bodies, modern trade and traditional kirana channels, online retail platforms, and quick commerce networks. Together, these participants enable product flow from farm to consumer across urban metros, Tier-2 and Tier-3 cities, and rural belts.

Market Dynamics

To evaluate market opportunities, Request Sample

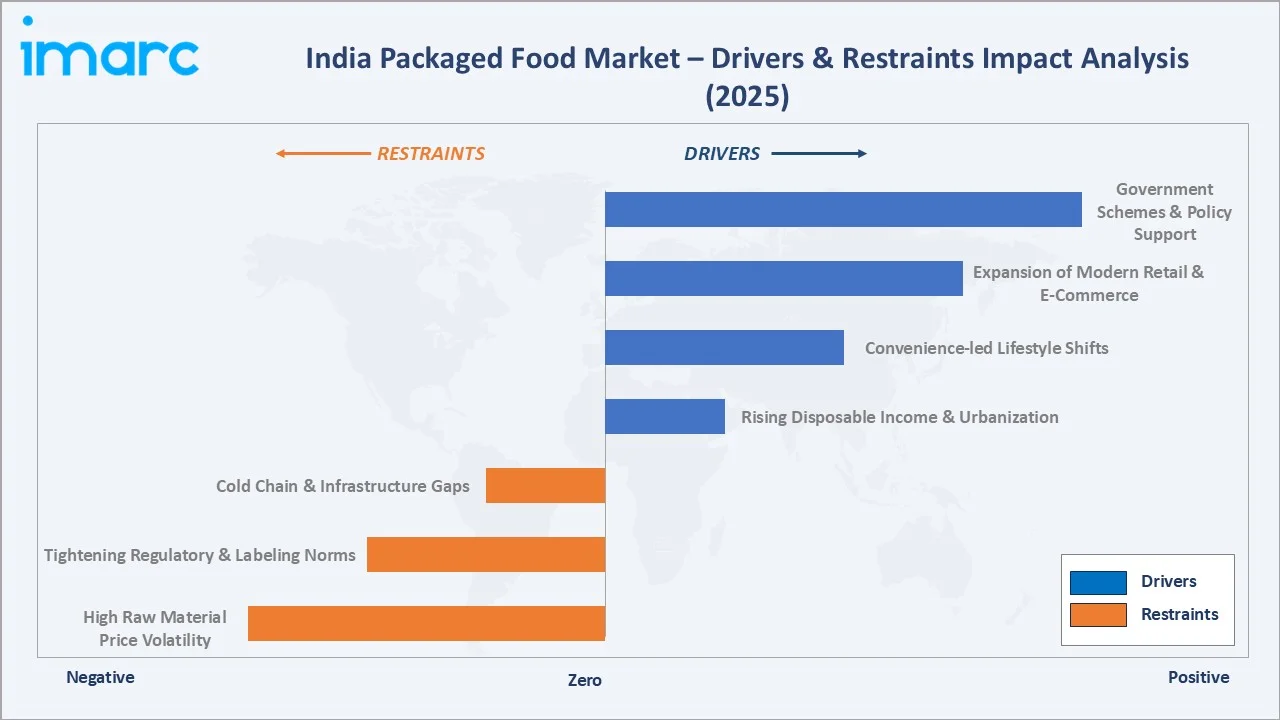

Market Drivers

- Rising Disposable Income and Urbanization: As per the United Nations report, India's urban population is projected to reach 675 Million by 2035, making it the second largest after China's one Billion, fueling sustained demand for branded packaged food across metro and Tier-2 markets. Higher household spending capacity is encouraging consumers to shift from unpackaged staples toward premium and branded food products.

- Convenience-led Lifestyle Shifts: Increasing dual-income households and longer commute times are driving steady migration from home-cooked meals to RTE and ready-to-cook packaged formats, especially among urban professionals and younger consumer cohorts.

- Expansion of Modern Retail and E-Commerce: Supermarkets, hypermarkets, online grocery platforms, and quick commerce dark stores are widening shelf access for branded packaged food, supporting product discovery, premiumization, and impulse purchase behaviour at scale.

- Government Schemes and Policy Support: Initiatives, such as the PLI for Food Processing Industries, are catalyzing investment in cold chain, mega food parks, and processing capacity, strengthening domestic manufacturing competitiveness.

Market Restraints

- High Raw Material Price Volatility: Fluctuations in wheat, edible oils, milk, sugar, and packaging input prices compress manufacturer margins and limit pricing flexibility, particularly for value-segment offerings, restraining short-term category expansion.

- Tightening Regulatory and Labeling Norms: On April 9, 2025, the Supreme Court of India instructed the Central Government to complete regulatory guidelines for Front-of-Pack Nutrition Labels (FOPNL) in three months, requiring clearer disclosure on sugar, salt, and saturated fat content. Compliance with such regulations is expected to demand reformulation, packaging redesign, and added regulatory cost across the industry.

- Cold Chain and Infrastructure Gaps: Inadequate temperature-controlled logistics in Tier-3 and rural markets continue to limit the reach of frozen, dairy, and ready-meal categories, creating product spoilage risk and constraining geographic expansion for several manufacturers.

- Competition From a Strong Unorganized Sector: Local kirana stores, regional brands, and unbranded fresh food retain meaningful share, especially in price-sensitive Tier-3 and rural markets, requiring branded players to invest heavily in distribution, pricing, and consumer trust building.

Market Opportunities

- Health, Wellness, and Clean-Label Expansion: Rising consumer interest in low-sugar, high-protein, fortified, and plant-based offerings is opening space for premium-priced products, dedicated health-food sub-brands, and millet- and ragi-based innovation across bakery, breakfast, and beverage categories.

- Tier-2 and Tier-3 Market Deepening: Improving disposable incomes, broader smartphone adoption, and quick commerce expansion into smaller cities are unlocking sizeable underserved demand pockets for affordable packaged food and small-pack product formats.

- Premiumization and Global Flavors: Growing exposure to international cuisines and rising aspirational consumption are driving demand for imported snacks, gourmet bakery, plant-based dairy alternatives, and specialty beverages, creating new high-margin segments.

Market Challenges

- Health Concerns around Ultra-Processed Foods: Heightened public discourse on lifestyle diseases, such as obesity, diabetes, and hypertension, is pressuring manufacturers to reformulate recipes, reduce salt, sugar, and trans-fat levels, and reposition portfolios toward better-for-you propositions.

- Sustainable Packaging Compliance: Extended Producer Responsibility (EPR) obligations and rules on recycled content and single-use plastics are increasing packaging redesign costs and supply chain complexity, particularly for smaller manufacturers.

- Talent and Supply Chain Bottlenecks: Limited availability of trained food technologists, persistent post-harvest losses, and uneven cold storage capacity continue to limit operational scalability and slow new product rollout in several states.

Emerging Market Trends

1. Rise of Health-Conscious and Clean-Label Packaged Foods

Indian consumers are increasingly choosing low-sugar, low-sodium, high-protein, and high-fibre packaged options, driven by growing awareness of lifestyle diseases. Manufacturers are responding with reformulated recipes, fortified breakfast cereals, millet-based snacks, and protein-enriched dairy variants, supporting sustained India packaged food market growth in premium and wellness sub-categories.

2. Quick Commerce Becoming the Default Urban Grocery Channel

10-30 minute delivery formats have moved from convenience to baseline expectation in metros. Brands are designing pack sizes, exclusive SKUs, and bundled assortments tailored to dark store catalogues, with tamper-evident, moisture-resistant packaging gaining traction. By April 2026, Blinkit operated around 2,100 dark stores while Swiggy Instamart and Zepto had approximately 1,100-1,200 facilities each, underscoring how rapidly instant delivery is reshaping packaged food merchandising and brand-shopper interaction in India.

3. Expansion of Premium and Regional Flavour Portfolios

Brands are localizing portfolios with regional flavors, such as Andhra-style snacks, Bengali sweets in shelf-stable formats, and South-Indian breakfast mixes. Premium and gourmet line extensions in chocolate, cookies, ready-meals, and beverages are also expanding, as urban consumers increasingly trade up to experiential and indulgence-led formats.

4. Plant-Based, Millet-Led Innovation and Sustainable Packaging

India’s millet promotion initiatives are encouraging packaged food companies to expand plant-based and millet-based offerings across breakfast, bakery, and snack categories, highlighting traditional nutrition and health-focused positioning. At the same time, manufacturers are increasingly adopting recyclable and paper-based packaging solutions to reduce plastic usage and support sustainability targets.

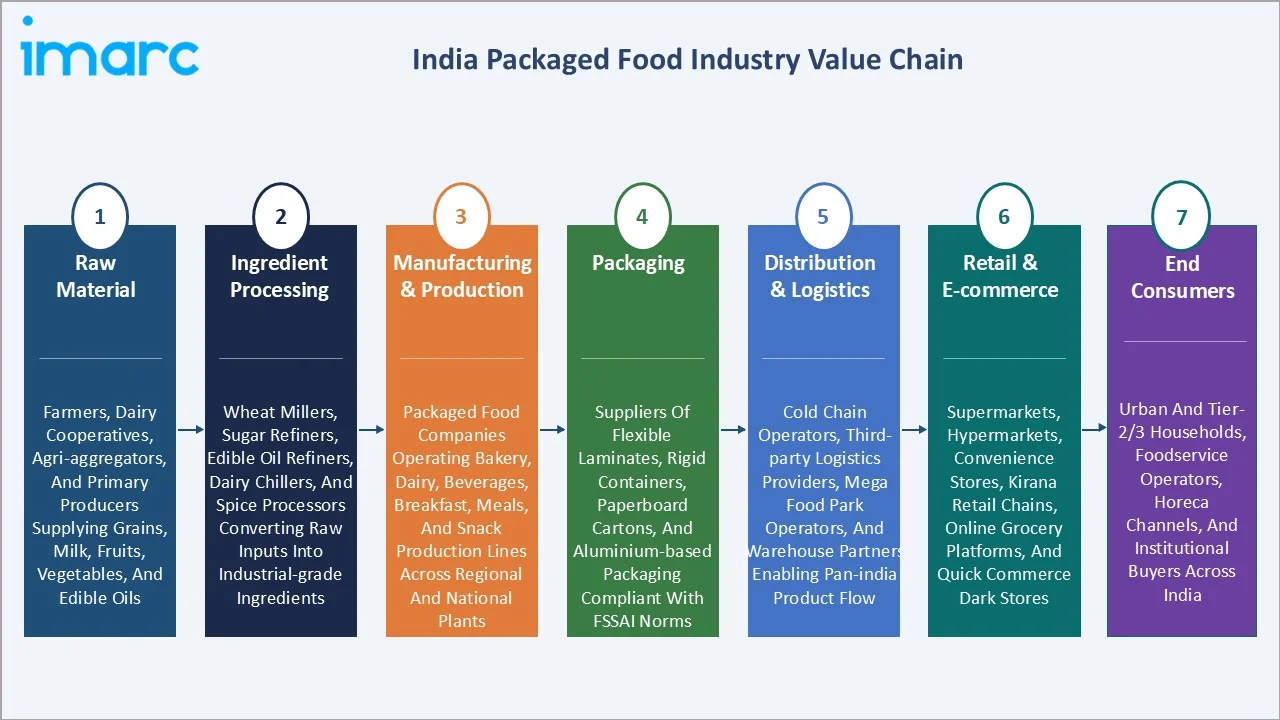

Industry Value Chain Analysis

The India packaged food value chain spans seven stages — from raw material sourcing to end consumer delivery. Manufacturing and brand building capture the highest value-add, while distribution density and modern retail / e-commerce relationships create durable downstream advantage in this fragmented category.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Farmers, dairy cooperatives, agri-aggregators, and primary producers supplying grains, milk, fruits, vegetables, and edible oils |

|

Ingredient Processing |

Wheat millers, sugar refiners, edible oil refiners, dairy chillers, and spice processors converting raw inputs into industrial-grade ingredients |

|

Manufacturing & Production |

Packaged food companies operating bakery, dairy, beverages, breakfast, meals, and snack production lines across regional and national plants |

|

Packaging |

Suppliers of flexible laminates, rigid containers, paperboard cartons, and aluminium-based packaging compliant with FSSAI norms |

|

Distribution & Logistics |

Cold chain operators, third-party logistics providers, mega food park operators, and warehouse partners enabling pan-India product flow |

|

Retail & E-commerce |

Supermarkets, hypermarkets, convenience stores, kirana retail chains, online grocery platforms, and quick commerce dark stores |

|

End Consumers |

Urban and Tier-2/3 households, foodservice operators, HoReCa channels, and institutional buyers across India |

Vertically integrated players capturing more value-chain stages, from agri-sourcing to brand-led retail execution, typically achieve superior cost control, supply security, and traceability compared with manufacturers reliant on third-party ingredient sourcing.

Technology Landscape in the India Packaged Food Industry

Food Processing & Preservation Innovation

Technologies such as high-pressure processing (HPP), aseptic packaging, ultra-high temperature (UHT) treatment, and freeze-drying are extending shelf life and preserving nutrient profiles without heavy preservatives, supporting clean-label positioning across dairy, beverages, and ready-meal categories.

Smart and Sustainable Packaging

Manufacturers are deploying recyclable mono-material laminates, paper-based formats, biodegradable films, and tamper-evident seals to align with regulatory and consumer expectations. QR-code-enabled labels are also being used for traceability, recipe storytelling, and authenticity verification at the SKU level.

Digital Supply Chain and AI-Driven Demand Forecasting

AI-driven demand sensing, real-time cold-chain monitoring, and ERP-integrated dark-store inventory planning are reducing wastage, optimizing stock-outs, and improving service levels for both modern trade and quick commerce channels in India's packaged food network.

Personalized Nutrition and Functional Foods

Functional ingredients, probiotics, and fortification with vitamins, minerals, and protein are entering mainstream packaged food formats. D2C brands are leveraging consumer data and online platforms to launch personalized health-oriented products, including high-protein bars, plant-based dairy, and specialized gut-health beverages.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Bakery Products |

22.5% |

2025 |

|

Distribution Channel |

Supermarkets and Hypermarkets |

52.8% |

2025 |

|

Region |

West and Central India |

30.0% |

2025 |

By Product Type

Bakery products command a 22.5% leading share in 2025, supported by deep penetration of biscuits, rusks, packaged breads, and cookies across both modern trade and traditional kirana outlets. Affordable unit pack sizes, long shelf life, and continuous innovation in low-sugar and fortified variants keep this segment central to Indian household consumption baskets.

To access detailed market analysis, Request Sample

Dairy products follow at 21.3% in 2025, anchored by India's position as the world's leading milk producer and steady consumer migration from loose to branded packaged dairy. Rising demand for value-added products such as cheese, flavored milk, yogurt, and packaged paneer is further strengthening category expansion across urban and semi-urban markets.

By Distribution Channel

Supermarkets and hypermarkets dominate with 52.8% share in 2025, reflecting the rapid expansion of organized retail chains across metros and Tier-2 cities. Wide assortments, in-store promotions, and private-label growth make this channel central to category creation for branded packaged food in India.

Convenience stores at 17.6% serve impulse and on-the-go consumption, particularly in metros and along highways. Their extended operating hours and easy neighborhood access continue supporting frequent purchases of snacks, beverages, dairy items, and RTE packaged foods.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

West and Central India |

30.0% |

Strong urbanization, high disposable income, dense modern retail networks, and well-established food processing manufacturing clusters |

|

North India |

26.4% |

Rapid Tier-2 city expansion, rising organized retail penetration, growing demand for convenience foods, and large youth consumer base |

|

South India |

24.1% |

High brand consciousness, rising health and wellness orientation, robust e-commerce adoption, and well-developed cold chain infrastructure |

|

East and Northeast India |

19.5% |

Improving infrastructure, expanding modern retail reach, growing aspirational consumption, and rising packaged food affordability across emerging urban markets |

West and Central India at 30.0% lead the market in 2025, anchored by Maharashtra and Gujarat. Strong urban consumption, dense modern retail networks, well-developed food processing manufacturing clusters, and established distribution backbones support sustained packaged food adoption across product categories.

North India at 26.4% follows closely, supported by Delhi NCR, Punjab, Haryana, and Uttar Pradesh — large markets with rising organized retail and a youthful consumer base. Strong demand for packaged dairy, bakery products, snacks, and ready-to-cook meals continues to support category expansion across urban and semi-urban households in the region.

Competitive Landscape

The India packaged food market is moderately fragmented, with a few large parent companies leading on brand equity, distribution depth, and innovation pipelines, while regional and unorganized players address local taste preferences and price-sensitive segments. Channel relationships, manufacturing scale, and continuous new product introduction form the principal competitive moats.

|

Company Name |

Brand / Key Products |

Position |

Strategic Focus |

|

Nestlé |

Maggi, Nescafé, KitKat |

Leader |

Premium positioning, deep R&D, and broad nutrition portfolio across categories |

|

ITC |

Aashirvaad, Sunfeast, Bingo!, Yippee! |

Leader |

Integrated agri-sourcing, rapid SKU innovation, and scale-led national distribution |

|

Unilever |

Kissan, Knorr, Brooke Bond |

Leader |

Wide portfolio depth, strong rural reach, and consistent brand investment |

|

Britannia Industries |

Good Day, Tiger, Marie Gold, NutriChoice |

Leader |

Bakery-led leadership, value-segment dominance, and continuous product premiumization |

|

Tata Consumer Products Limited |

Tata Salt, Tata Sampann, Tetley, Tata Tea |

Challenger |

Ingredients-led foods strategy, premiumization, and rapid scaling of millet-based and health-led products |

Key players include Nestlé, ITC, Unilever, Britannia Industries, and Tata Consumer Products Limited, among others.

Key Company Profiles

Nestlé

Nestlé is the leading food and beverage (F&B) company and the global parent of Nestlé India Limited, a major packaged foods company in the country. The group operates across milk products and nutrition, prepared dishes and cooking aids, beverages, and confectionery in India, with a strong urban and semi-urban distribution network supported by multiple manufacturing plants.

- Product Portfolio: Maggi instant noodles, sauces, and seasonings; Nescafé instant coffee; KitKat; Maggi Masala-ae-Magic and Maggi Hot & Sweet ranges.

- Recent Developments: In FY24, Nestlé India Limited, the subsidiary of Nestlé, shifted its financial year to April-March and reported total sales of INR 24,275.5 crore over a 15-month transition period, reflecting consistent volume growth and continued investment in capacity expansion across its India plants.

- Strategic Focus: Premium and nutrition-led positioning, sustained R&D investment, expansion of out-of-home and foodservice business, and ongoing reformulation aligned with health and wellness trends.

ITC

ITC, headquartered in Kolkata, is one of India's largest diversified conglomerates with a fast-growing branded foods business. The company combines deep agri-sourcing capabilities, in-house manufacturing, and an extensive national distribution network to compete across staples, bakery, snacks, dairy, beverages, and ready-meal categories.

- Product Portfolio: Aashirvaad atta, salt, and ghee; Sunfeast biscuits and beverages; Bingo! salty snacks; Yippee! noodles; Sunbean instant coffee jar.

- Recent Developments: In January 2026, ITC expanded the line of high-end, freshness-oriented packaged foods, including cookies, cakes, chutneys, and namkeens, to connect the divide between mainstream snacks and freshly baked excellence.

- Strategic Focus: Agri-integration, rapid new product introduction, premium brand-building, and deep distribution to strengthen leadership across staples, snacks, and beverages.

Unilever

Unilever, headquartered in London, is a leading global FMCG company and the parent of Hindustan Unilever Limited, one of India's largest fast-moving consumer goods players. Through Hindustan Unilever Limited, Unilever operates an extensive packaged food and refreshment portfolio in India spanning tea, coffee, ice cream, ketchup, dressings, and meal solutions, supported by some of the country's most recognized brands and a deep multi-channel distribution system.

- Product Portfolio: Kissan ketchup, jams, and squashes; Knorr soups, noodles, and meal makers

- Recent Developments: Through Hindustan Unilever Limited, Unilever has continued to expand its food and refreshment portfolio in India through premium tea launches, fortified product innovations, and deeper rural penetration, while reformulating across categories to align with health-led consumer trends.

- Strategic Focus: Brand-led growth, deep rural distribution, premium portfolio expansion, and sustained investment in health and wellness-focused product innovation.

Market Concentration Analysis

The India packaged food market is moderately fragmented. The top five organized parent companies (Nestlé, ITC, Unilever, Britannia Industries, and Tata Consumer Products Limited) collectively account for an estimated 35-45% of the organized branded share, with the balance distributed across regional brands, private labels, and unorganized players.

Barriers to entry include scale-led manufacturing, FSSAI compliance, multi-tier distribution depth, and brand-building investment, all of which favour well-capitalized incumbents with integrated supply chains and strong agri-sourcing relationships.

Consolidation is accelerating through portfolio acquisitions, capacity additions, and category extensions into premium and health-oriented sub-segments. Scale advantages in procurement, manufacturing, and route-to-market continue to reinforce the competitive position of established national players.

Investment & Growth Opportunities

Fastest-Growing Segments

Online retail stores at 9.8% are expected to expand faster than the overall 6.24% market CAGR through 2034, driven by quick commerce densification and digital-first buyer behaviour. Within product type, beverages and meals are growing faster than the overall market, fuelled by functional drinks, plant-based options, and RTE innovation.

Emerging Markets

South India at 24.1% is the fastest-growing region, supported by strong urban consumption and rising demand for packaged dairy, snacks, and convenience food products. Tier-2 and Tier-3 cities across North India and East and Northeast India represent the largest untapped opportunity, with rising disposable income, expanding modern retail, and improving cold chain infrastructure unlocking mass-market adoption of packaged dairy, bakery, and breakfast categories.

Venture & Investment Trends

Investment is concentrated in D2C health-food brands, plant-based dairy and meat alternatives, millet-based snacks and breakfast products, and quick commerce-native packaged food labels. Capital is also flowing into cold chain infrastructure, food processing capacity expansion through PLI and PMKSY, and AI-enabled supply chain platforms supporting branded food distribution at scale.

Future Market Outlook (2026-2034)

The India packaged food market is forecast to expand from USD 129.18 Billion in 2025 to USD 238.83 Billion by 2034 at a CAGR of 6.24%, adding nearly USD 110 Billion in incremental annual market value over the forecast period.

Four forces will shape the market through 2034: sustained urbanization and disposable income gains; mainstreaming of health-led, clean-label, and millet-based products; quick commerce-driven category expansion; and regulatory tightening on labeling, ingredients, and sustainable packaging.

By 2034, packaged food is expected to be a regular consumption category in most Indian urban and semi-urban households, with online and quick commerce channels collectively driving a meaningful share of new category creation and brand discovery, while traditional kirana stores continue to evolve into omnichannel retail nodes.

Research Methodology

Primary Research

Primary research included structured interviews with senior leaders at Indian packaged food companies, category managers at modern trade and quick commerce platforms, food technologists, regulatory experts, and household consumers across metros and Tier-2 cities, validating market sizing, regional demand, and segment shares.

Secondary Research

Secondary sources included Ministry of Food Processing Industries publications, Press Information Bureau releases on the PLI scheme and PMKSY, FSSAI regulatory advisories, USDA Foreign Agricultural Service GAIN reports, RBI consumer expenditure data, and annual reports, press releases, and investor presentations from major listed manufacturers.

Forecasting Models

Forecasts were built using a combination of top-down and bottom-up models, integrating per capita consumption trends, urbanization projections, modern retail expansion, e-commerce penetration, and segment-level CAGRs. Scenario analysis covered raw material price volatility, regulatory changes, and shifts in consumer preferences.

India Packaged Food Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | USD Billion |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Bakery Products, Dairy Products, Beverages, Breakfast Products, Meals, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Convenience Stores, Online Retail Stores, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Nestlé, ITC, Unilever, Britannia Industries, Tata Consumer Products Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India packaged food market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India packaged food market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India packaged food industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Packaged Food Market Report

The India packaged food market was valued at USD 129.18 Billion in 2025, supported by rising disposable incomes, urbanization, modern retail expansion, and growing demand for convenience foods.

The market is projected to grow at a 6.24% CAGR over 2026-2034, reaching USD 238.83 Billion by 2034, driven by health-led innovation, quick commerce, and Tier-2/3 expansion.

Bakery products lead at 22.5% in 2025, supported by mass affordability, deep distribution, and continuous innovation across biscuits, breads, rusks, and cookies.

Supermarkets and hypermarkets dominate at 52.8% in 2025, fueled by expanding organized retail networks, wider product assortments, attractive promotional pricing, and growing consumer preference for one-stop shopping formats across urban and semi-urban markets.

West and Central India command 30.0% share in 2025, anchored by Maharashtra and Gujarat, where strong urbanization, higher packaged food penetration, and the presence of major food processing hubs support category leadership. South India follows at 24.1% and is the fastest-growing region.

Leading players include Nestlé, ITC, Unilever, Britannia Industries, and Tata Consumer Products Limited, among others.

Quick commerce is reshaping pack design, SKU strategy, and brand-shopper interaction, with platforms like Blinkit, Zepto, and Swiggy Instamart driving rapid online category creation across urban India.

Schemes such as the PLI for food processing, are catalyzing investment in cold chain, mega food parks, and modern manufacturing capacity across India.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)