India Packaged Rice Market Size, Share, Trends and Forecast by Product Type, Packaging, Pack Size, Distribution Channel, and Region, 2026-2034

India Packaged Rice Market Summary:

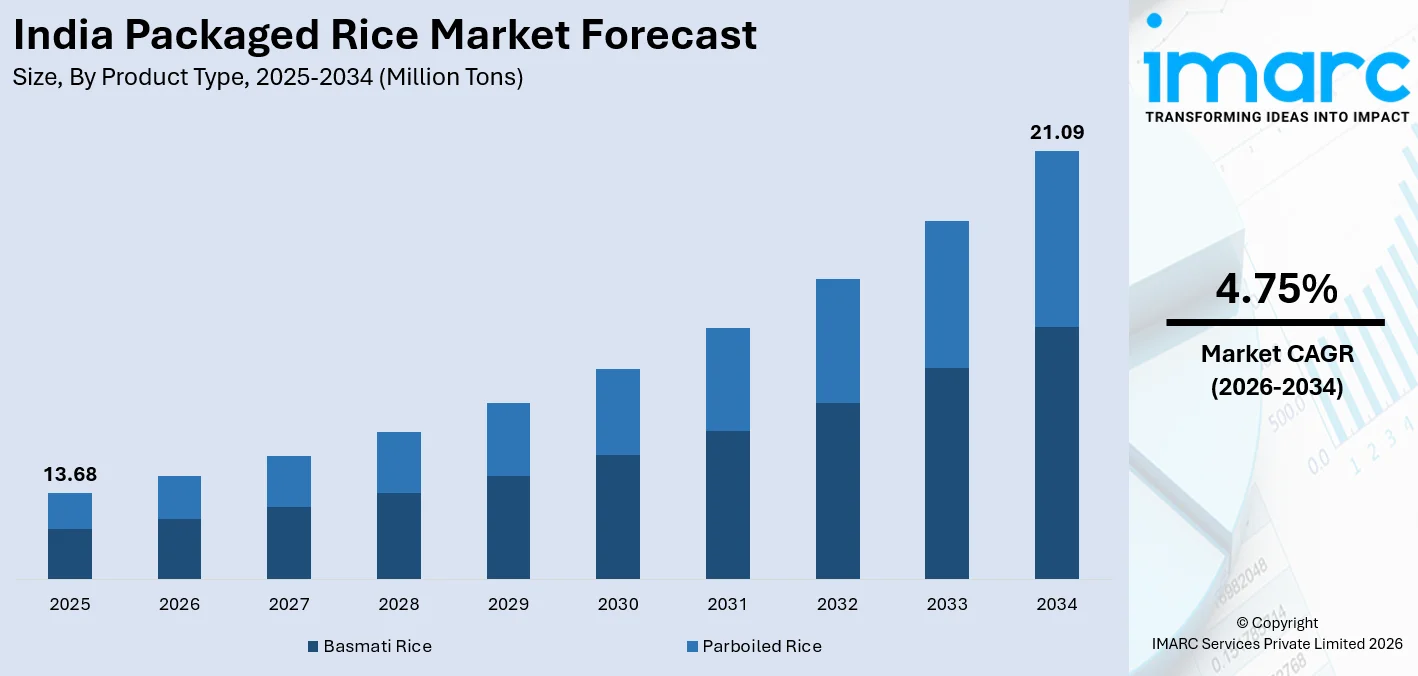

The India packaged rice market size reached 13.68 Million Tons in 2025 and is projected to reach 21.09 Million Tons by 2034, growing at a compound annual growth rate of 4.75% from 2026-2034.

The India packaged rice market is experiencing growth underpinned by rapid urbanization, rising consumer awareness about food safety, and the accelerating shift from loose unbranded rice to hygienically sealed branded products. The growing demand for premium Basmati varieties, expanding modern trade formats, and the proliferation of e-commerce and quick-commerce channels are amplifying product accessibility across urban and semi-urban geographies. Favorable government export policies, technological advancements in rice processing, and increasing premiumization trends are further reinforcing the India packaged rice market share across diverse consumer and retail segments.

Key Takeaways and Insights:

- By Product Type: Basmati rice dominates the market with a share of 51.5% in 2025, driven by its premium positioning, distinctive aroma and elongated grain profile, and sustained domestic and export demand, particularly from households seeking quality-assured branded rice.

- By Packaging: Pouches represent the largest segment with a market share of 55.2% in 2025, owing to their consumer-preferred combination of tamper-evident sealing, superior moisture barrier properties, and lightweight convenience that aligns with the preferences of urban nuclear households.

- By Pack Size: 5 Kilograms lead the market with a share of 42.5% in 2025, reflecting its suitability for average-sized Indian families seeking cost-effective, hygienic, and conveniently portioned packaged rice for regular household consumption.

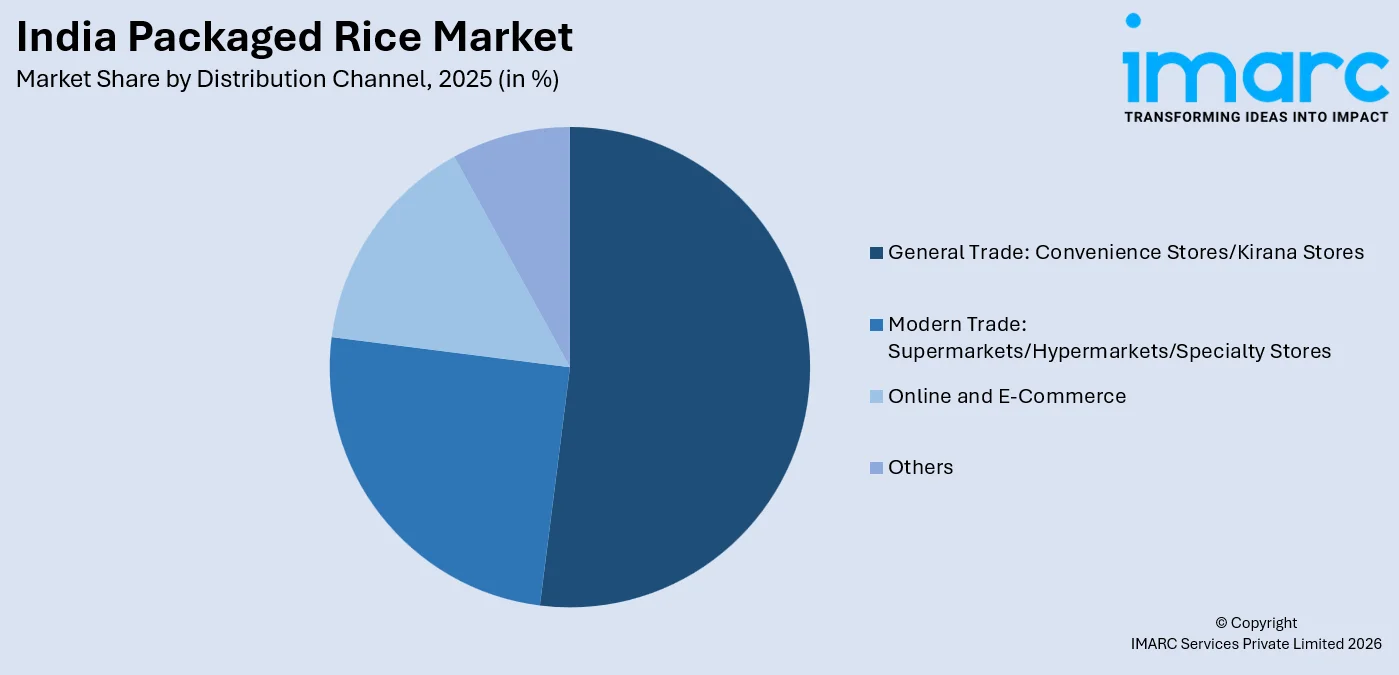

- By Distribution Channel: General Trade: Convenience stores/kirana stores dominate the market with a share of 52.8% in 2025, underpinned by deep rural and semi-urban retail penetration, consumer trust, and proximity-driven purchasing habits across India’s vast, fragmented retail landscape.

- By Region: East India represents the largest segment with a market share of 31.2% in 2025, supported by rice’s deep-rooted cultural and dietary significance across West Bengal, Odisha, and Bihar, along with rising packaged rice adoption driven by increasing retail modernization and health-conscious purchasing behavior.

- Key Players: The India packaged rice market is moderately competitive, with established branded players and integrated rice exporters competing on product premiumization, packaging innovation, distribution expansion, and consumer engagement strategies to consolidate brand loyalty and drive volume growth. Some of the key players in the market include Adani Wilmar Ltd., Aeroplane Rice Ltd., Amira Nature Foods Ltd., Baba Naga Agro Pvt. Ltd., Balashree Foods Pvt. Ltd., Chaman Lal Setia Exports Ltd., Future Consumer Limited, KRBL Limited, Lal Qilla (Amar Singh Chawal Wala), LT Foods, Patanjali Ayurved Limited, Shri Lal Mahal Group, Sriveda Sattva Pvt. Ltd. and VSR Foods.

To get more information on this market Request Sample

The India packaged rice market is advancing steadily, shaped by rising consumer demand for traceable, quality-assured, and hygienically packaged food staples. Changing consumption patterns, the growing urbanization, and rising disposable incomes are encouraging households to shift from loose grains to branded packaged rice that offers standardized quality, consistent grain characteristics, and improved storage. Expanding organized retail networks and digital grocery platforms are also improving the accessibility of branded rice across urban and semi-urban markets. Furthermore, consumers are increasingly exploring premium and specialty rice varieties aligned with evolving food preferences and exposure to international cuisines. Reflecting this shift toward diversified offerings, LT Foods launched Daawat Jasmine Thai Rice in India in 2024, introducing a Non-GMO certified Thai Hom Mali variety aimed at consumers experimenting with Thai and oriental dishes. The product was distributed through major e-commerce platforms and gourmet retail outlets, highlighting how rising interest in global cuisine and premium packaged staples is supporting the growth of the packaged rice market in India.

India Packaged Rice Market Trends:

Growing Middle-Class Population and Rising Disposable Income

The expanding middle-class population in India is strengthening the demand for branded and packaged staple foods, including packaged rice, as households increasingly prioritize quality, convenience, and product reliability. Rising disposable incomes are enabling consumers to move beyond basic purchasing decisions and choose packaged products that offer consistent grain quality, better storage life, and assured processing standards. This transition is particularly visible in urban and semi-urban markets where lifestyle changes and higher spending capacity influence food choices. Supporting this trend, the Ministry of Statistics reported that per capita Net National Income increased to INR 2,05,324 in FY2024–25 from INR 1,88,892 in FY2023–24, reflecting stronger consumer purchasing power. With greater financial capacity, households are more willing to purchase branded packaged rice, reinforcing the steady shift from loose grains toward organized and packaged food products across India.

Packaging Innovation Enhancing Consumer Trust and Product Transparency

Advancements in packaging design and product information are becoming a key trend driving the packaged rice market. Modern packaging not only protects the product but also communicates important details about grain quality, cooking instructions, and brand authenticity. Informative packaging strengthens consumer confidence and helps differentiate branded rice from loose alternatives. Companies are increasingly using packaging as a communication platform to highlight product quality and encourage brand loyalty. Reflecting this trend, KRBL Ltd introduced redesigned packaging for its flagship India Gate basmati rice brand in 2025. The updated packaging included a refreshed logo, detailed grain information, cooking guidance, and QR codes intended to enhance transparency and encourage consumers to transition from loose rice purchases to packaged products.

Intensifying Marketing Campaigns Promoting Branded Packaged Rice

Increasing marketing and consumer awareness campaigns by organized rice brands are propelling the growth of the India packaged rice market by encouraging individuals to transition from loose grains to branded packaged products. Companies are investing in large-scale promotional initiatives to highlight the benefits of packaged rice, including quality assurance, standardized grading, hygiene, and reliable cooking performance. Such campaigns also help build brand recognition and strengthen consumer trust in packaged staples. As part of this trend, KRBL launched the “Only Top Class, No Khulla Class” campaign in 2025, for its India Gate Basmati Rice brand featuring Amitabh Bachchan. The campaign promoted the purity and consistency advantages of packaged rice in a market where nearly 70% of basmati is still purchased loose in Hindi-speaking regions, supported by a 360-degree media strategy, including television, digital platforms, radio, outdoor advertising, and retail activations.

Market Outlook 2026-2034:

The India packaged rice market demonstrates growth potential throughout the forecast period, supported by rising demand for hygienically processed and branded food staples. Increasing urbanization, growth of organized retail, and higher consumer awareness regarding food safety are encouraging the shift from loose rice to packaged variants. The market size was estimated at 13.68 Million Tons in 2025 and is expected to reach 21.09 Million Tons by 2034, reflecting a compound annual growth rate of 4.75% over the forecast period 2026-2034. Manufacturers are also expanding product offerings with premium varieties, fortified rice, and convenient packaging formats.

India Packaged Rice Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product Type |

Basmati Rice |

51.5% |

|

Packaging |

Pouches |

55.2% |

|

Pack Size |

5 Kilograms |

42.5% |

|

Distribution Channel |

General Trade: Convenience Stores/Kirana Stores |

52.8% |

|

Region |

East India |

31.2% |

Product Type Insights:

- Parboiled Rice

- Basmati Rice

Basmati rice leads with a share of 51.5% of the total India packaged rice market in 2025.

Basmati rice represents the largest market share due to its strong consumer preference, premium positioning, and widespread use in traditional and modern cuisines. Known for its long grains, distinctive aroma, and soft texture after cooking, basmati rice is widely used in dishes, such as biryani, pulao, and other rice-based meals across households and food service establishments. Consumers increasingly choose packaged basmati rice as it ensures consistent quality, proper grading, and hygienic processing compared to loose rice sold in local markets. Leading food brands offer multiple basmati variants, including classic, premium, and aged basmati, allowing consumers to select products based on taste preferences and price points.

Rising disposable income and stronger demand for premium food staples are reinforcing the prominence of basmati rice within India’s packaged rice market. Urban households and foodservice establishments increasingly prefer branded basmati rice due to its consistent grain quality, reliable packaging, and extended shelf life. This demand is also being supported by wider availability through organized retail and digital grocery platforms. Reflecting this shift toward premium packaged staples, FarMart launched its consumer brand FarMart Pantry in 2025, introducing 27 products, including basmati rice and distributing them through quick commerce platforms, such as Blinkit and Zepto. Such retail expansion is strengthening the reach of branded packaged rice among urban consumers.

Packaging Insights:

- Pouches

- Woven Bags

- Others

Pouches exhibit a clear dominance with a 55.2% share of the total India packaged rice market in 2025.

Pouches lead the market in terms owing to their convenience, cost efficiency, and strong suitability for large-scale distribution. Flexible pouch packaging allows rice manufacturers to pack products in different sizes ranging from small household packs to large family packs while maintaining product freshness. These pouches are lightweight, easy to store, and simpler to transport compared to rigid packaging formats, which helps reduce logistics costs for both manufacturers and retailers. Many brands also use multilayer laminated pouches that protect rice from moisture, dust, and contamination. The ability to print clear branding and product information on pouch surfaces further strengthens their appeal in retail environments.

The growing demand for packaged food products and expansion of organized retail channels are further supporting the popularity of pouch packaging in the rice market. Supermarkets, grocery stores, and online retail platforms prefer pouch-packed rice because it is easy to stack, display, and ship in bulk. Consumers also favor pouches due to their easy handling and resealable features that help maintain product quality after opening. Manufacturers increasingly adopt advanced packaging technologies to improve durability and shelf life while maintaining attractive visual presentation. As packaged rice brands compete for visibility and convenience in modern retail settings, pouch packaging continues to remain the most widely adopted format.

Pack Size Insights:

- 5 Kilograms

- 1 Kilogram

- Others

The 5 kilograms dominate with a share of 42.5% of the total India packaged rice market in 2025.

5 kilograms hold the biggest market shares driven by their balanced suitability for regular household consumptions and convenient storages. Many urban and semi-urban households prefer these pack sizes as they provide enough quantities for weekly or biweekly uses without requiring frequent purchases. Compared with smaller packs, the 5 kilograms formats offer better values per kilogram, making them attractive for families seeking affordability along with branded qualities. Retailers also favor these pack sizes because they sell consistently across supermarkets, grocery stores, and online platforms. Packaged rice brands widely offer basmati and non-basmati variants in these formats, allowing consumers to choose according to their taste preferences and cooking needs.

Growing urbanization and increasing reliance on packaged staple foods are supporting strong demand for medium-sized rice packs in India, particularly the 5 kilogram format preferred by nuclear families and working households. These pack sizes balance storage convenience with regular consumption needs and align well with weekly grocery purchasing patterns in urban retail environments. Reflecting this demand, Bharat Rice, a fortified rice brand produced by the National Cooperative Consumers’ Federation, was introduced in 2025, and packaged in 5 kg and 10 kg bags to improve household accessibility. Such product formats make packaged rice easier to store and distribute while supporting consistent supply for consumers, reinforcing the sustained demand for practical pack sizes within the packaged rice market.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- General Trade: Convenience Stores/Kirana Stores

- Modern Trade: Supermarkets/Hypermarkets/Specialty Stores

- Online and E-Commerce

- Others

General Trade: Convenience stores/kirana stores stores lead with a share of 52.8% of the total India packaged rice market in 2025.

General trade, including convenience stores and kirana stores, is the leading segment in the market attributed to its deep penetration across urban, semi-urban, and rural areas. Kirana stores remain the primary grocery purchase point for a large share of Indian households, offering easy accessibility and familiarity for daily food purchases. Consumers often prefer buying packaged rice from nearby stores where they can quickly compare brands and pack sizes based on price and household requirements. These stores also maintain strong relationships with local distributors and rice brands, allowing them to stock a wide range of packaged basmati and non-basmati rice products that cater to different consumer preferences and budget segments.

Strong consumer trust and convenient neighborhood access continue to support the dominance of kirana and small retail stores in rice distribution. Many households purchase groceries in smaller or medium quantities during regular visits to nearby shops rather than making large purchases from supermarkets. Retailers also provide flexible purchasing options, product recommendations, and occasional credit facilities that encourage repeat buying. Packaged rice brands actively maintain strong distribution networks with wholesalers and local retailers to ensure consistent product availability across these outlets. Even with the growth of modern retail and online grocery platforms, general trade continues to account for a significant share of packaged rice sales across India.

Regional Insights:

- North India

- West and Central India

- South India

- East India

East India exhibits a clear dominance with a 31.2% share of the total India packaged rice market in 2025.

East India dominates the market because of the region’s strong rice consumption patterns and large population base that relies heavily on rice as a staple food. States, such as West Bengal, Odisha, Bihar, and Assam, have long-standing dietary preferences centered around rice, which drives continuous demand across household and food service sectors. Consumers in these states are gradually shifting from loose rice to branded packaged products as awareness of food safety, quality assurance, and standardized grading increases. Packaged rice brands are expanding their presence in local retail stores and regional distribution networks, allowing consumers easier access to a wide variety of basmati and non-basmati rice products.

The region also benefits from significant rice production, which supports strong supply availability and encourages development of packaging and distribution activities. Many rice mills and processing units operate across eastern states, enabling companies to source raw rice locally and package it for domestic consumption. Expansion of organized retail outlets and growth of online grocery platforms are further increasing the visibility of packaged rice brands in the region. Government initiatives supporting agricultural productivity and rural infrastructure are also improving the rice supply chain. Rising disposable incomes and changing consumer preferences are gradually encouraging households to purchase branded packaged rice products.

Market Dynamics:

Growth Drivers:

Why is the India Packaged Rice Market Growing?

Government-Led Distribution Programs Expanding Packaged Rice Access

Government-supported food distribution initiatives are contributing to the growth of the packaged rice market in India by improving the availability of affordable and quality-assured staple foods across regional markets. Such programs encourage the use of standardized packaging, which helps ensure product hygiene, consistent quality, and efficient distribution to consumers. They also strengthen the reach of packaged rice in areas where loose grain traditionally dominates local supply channels. Reflecting this trend, Sarveshwar Foods Ltd. began distributing subsidized packaged rice under the “Bharat Rice” brand across Jammu & Kashmir and Ladakh in 2024. The company became the first private enterprise from the region to be empaneled by the government to supply subsidized rice in these Union Territories. Initiatives of this nature are expanding access to packaged staples while supporting the broader adoption of organized rice distribution systems.

Rising Urbanization and Changing Lifestyles

Rapid urbanization across India is strengthening the demand for packaged rice as urban households increasingly prefer convenient, hygienic, and easy-to-store staple foods. Migration toward cities is reshaping consumption patterns, with working professionals and dual-income families placing greater emphasis on products that simplify cooking and ensure consistent quality. Packaged rice aligns well with these needs by offering standardized grain quality, cleaner handling, and reliable packaging compared with loose rice traditionally sold in open markets. This shift is supported by demographic trends, as World Bank data shows that about 36.87% of India’s population lived in urban areas in 2024, reflecting the continued expansion of urban consumer bases. As city populations grow and lifestyles become more time-conscious, there is a rise in the demand for branded packaged staples, gradually encouraging consumers to move away from loose grain purchases toward packaged rice products.

Expansion of Organized Retail and E-Commerce Channels

The expanding presence of organized retail stores and digital commerce platforms is significantly supporting the growth of the packaged rice market in India. Supermarkets, hypermarkets, and modern grocery outlets prominently display branded rice with standardized packaging and clear labeling, enabling consumers to easily compare varieties, quality grades, and price ranges. Besides this, online grocery platforms are improving product accessibility through home delivery, subscription services, and wider product selection. This shift toward organized retail channels is supported by the rapid expansion of India’s digital commerce sector. According to IBEF, India’s e-commerce industry was valued at INR 10,82,875 Crore in 2024 and is projected to reach INR 29,88,735 Crore by 2030, reflecting a CAGR of 15%. As digital and organized retail networks expand, packaged rice brands are gaining broader reach across urban and emerging semi-urban consumer markets.

Market Restraints:

What Challenges the India Packaged Rice Market is Facing?

Deep-Rooted Consumer Preference for Loose Bulk Rice in Price-Sensitive Segments

A large share of India’s rural and lower-income consumers continues to purchase rice in loose, unbranded bulk form due to its lower price compared with branded packaged products. Government distribution of subsidized rice through the Public Distribution System also reinforces this behavior. This strong price sensitivity makes it difficult for packaged rice brands to expand in rural and Tier-III markets despite promoting quality, hygiene, and consistency advantages.

Volatile Paddy Procurement Prices and Input Cost Fluctuations Impacting Manufacturer Margins

Packaged rice manufacturers face considerable raw material price volatility due to fluctuations in agricultural output, climate-related disruptions, government minimum support price changes, and shifting export demand. Unstable paddy procurement costs make long-term pricing difficult and can reduce profit margins during high input cost periods. Smaller manufacturers are particularly affected, as they often lack the procurement scale, farming partnerships, and storage capacity needed to manage price fluctuations effectively.

Intense Competition from Unbranded and Local Rice Processors in Fragmented Regional Markets

India’s rice processing and distribution landscape remains highly fragmented, with numerous small and medium local millers and traders operating across regional markets. Many of these players sell unbranded rice at lower prices, making competition difficult for organized packaged rice companies. Their strong retailer networks and familiarity with regional consumer preferences also strengthen their position. This local presence creates barriers for national brands attempting to expand into smaller cities, rural regions, and culturally diverse markets.

Competitive Landscape:

The India packaged rice market features a moderately competitive structure with a combination of large integrated rice exporters, established domestic brand owners, and regional processors competing across product quality, distribution reach, and consumer marketing. Leading market participants are investing significantly in brand-building initiatives, digital marketing campaigns, and modern packaging innovations to differentiate their premium offerings from commoditized alternatives. Companies are also expanding their product portfolios to include organic, fortified, and specialty rice variants that cater to health-conscious and premium consumer segments. Competitive intensity is amplified by the rapid growth of private label offerings, ranging from modern trade chains. Strategic investments in e-commerce distribution partnerships, regional advertising campaigns, and direct-to-consumer digital channels are becoming essential competitive tools as market participants seek to sustain growth.

Some of the key players in the market include:

- Adani Wilmar Ltd.

- Aeroplane Rice Ltd.

- Amira Nature Foods Ltd.

- Baba Naga Agro Pvt. Ltd.

- Balashree Foods Pvt. Ltd.

- Chaman Lal Setia Exports Ltd.

- Future Consumer Limited

- KRBL Limited

- Lal Qilla (Amar Singh Chawal Wala)

- LT Foods

- Patanjali Ayurved Limited

- Shri Lal Mahal Group

- Sriveda Sattva Pvt. Ltd.

- VSR Foods

Recent Developments:

- January 2026: LT Foods launched the ‘DAAWAT I’m Organic’ rice range in India, expanding its portfolio in the premium organic staples segment. The range includes Organic Basmati Rice and Organic Sona Masoori Rice, targeting consumers seeking verified, responsibly sourced food products. Each pack includes QR-based traceability and vacuum packaging to ensure quality, while the products are distributed through major e-commerce and quick commerce platforms.

- April 2025: KRBL launched a nationwide Out-of-Home (OOH) advertising campaign to promote the redesigned packaging of its India Gate Basmati Rice brand. The campaign began on 27 March 2025 and featured large billboards and high-visibility displays across major states, including Maharashtra, Delhi, Punjab, Rajasthan, and Uttar Pradesh. The initiative aimed to strengthen brand recall, highlight premium product quality, and reinforce the shift toward packaged rice consumption among urban consumers.

India Packaged Rice Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Parboiled Rice, Basmati Rice |

| Packagings Covered | Pouches, Woven Bags, Others |

| Pack Sizes Covered | 5 Kilograms, 1 Kilogram, Others |

|

Distribution Channels Covered |

|

| Region Covered | North India, South India, West and Central India, East India |

| Companies Covered | Adani Wilmar Ltd., Aeroplane Rice Ltd., Amira Nature Foods Ltd., Baba Naga Agro Pvt. Ltd., Balashree Foods Pvt. Ltd., Chaman Lal Setia Exports Ltd., Future Consumer Limited, KRBL Limited, Lal Qilla (Amar Singh Chawal Wala), LT Foods, Patanjali Ayurved Limited, Shri Lal Mahal Group, Sriveda Sattva Pvt. Ltd. and VSR Foods |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Packaged Rice Market Report

The India packaged rice market reached a volume of 13.68 Million Tons in 2025.

The India packaged rice market is expected to grow at a compound annual growth rate of 4.75% during 2026-2034 to reach 21.09 Million Tons by 2034.

Basmati rice holds the largest share of 51.5% in 2025, driven by its premium aromatic characteristics, strong domestic consumer preference for quality-assured branded Basmati, and India’s robust Basmati export ecosystem that supports domestic supply quality and brand investments.

Key factors driving the India packaged rice market include improvements in packaging design that enhance product protection, transparency, and consumer trust. Reflecting this trend, KRBL Ltd redesigned packaging for its India Gate basmati rice brand in 2025, adding grain information, cooking guidance, and QR codes to encourage a shift toward packaged rice.

Major challenges include the persistent consumer preference for loose bulk rice in price-sensitive rural and lower-income segments, volatile paddy procurement costs driven by agricultural and policy variability, and intense competition from unbranded local rice millers and processors that limit branded packaged rice penetration in fragmented regional markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade