India Parking Systems Market Size, Share, Trends and Forecast by Component, Type, System, End User, and Region, 2026-2034

India Parking Systems Market Summary:

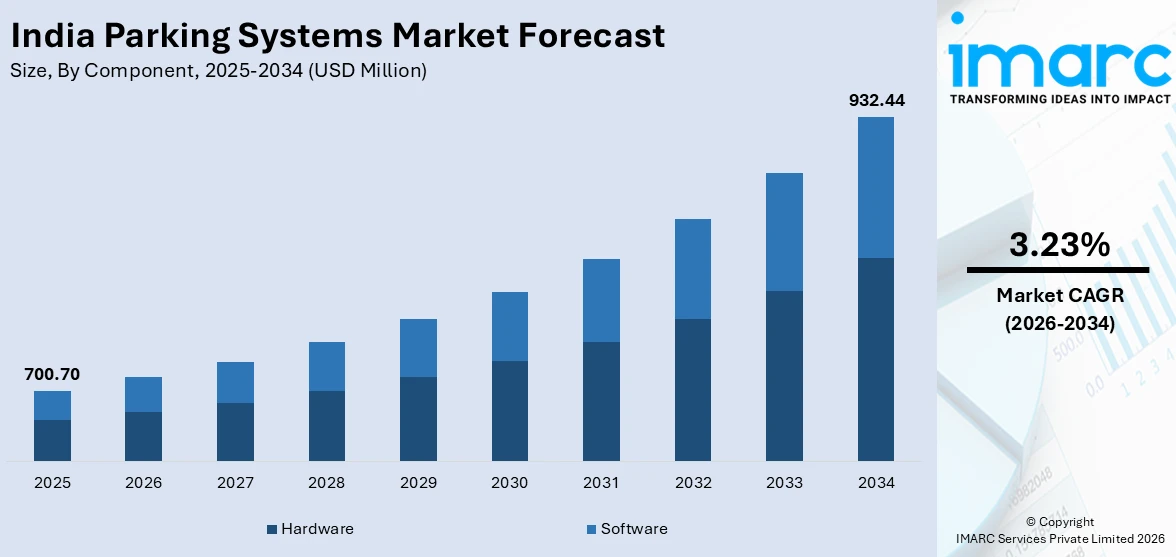

The India parking systems market size was valued at USD 700.70 Million in 2025 and is projected to reach USD 932.44 Million by 2034, growing at a compound annual growth rate of 3.23% from 2026-2034.

The India parking systems market is growing steadily as rapid urbanization, rising vehicle ownership, and increasing demand for organized parking infrastructure converge across the country. Government-led smart city initiatives, technological advancements in automated and sensor-driven parking solutions, and the growing commercial real estate development are collectively reshaping urban mobility. The integration of intelligent parking management platforms, coupled with heightened user expectations for convenience, is driving sustained demand and accelerating the modernization of parking infrastructure across Indian cities.

Key Takeaways and Insights:

- By Component: Hardware dominates the market with a share of 68% in 2025, driven by extensive deployment of sensors, cameras, steel structures, and electrical systems essential for constructing and operating modern parking facilities.

- By Type: Shuttle parking system represents the largest segment with a market share of 15% in 2025, owing to its space-efficient vertical transportation capability and suitability for high-density urban environments requiring compact automated solutions.

- By System: Fully automated system leads the market with a share of 60% in 2025, supported by rising demand for zero-intervention parking technologies that maximize space utilization and improve operational efficiency.

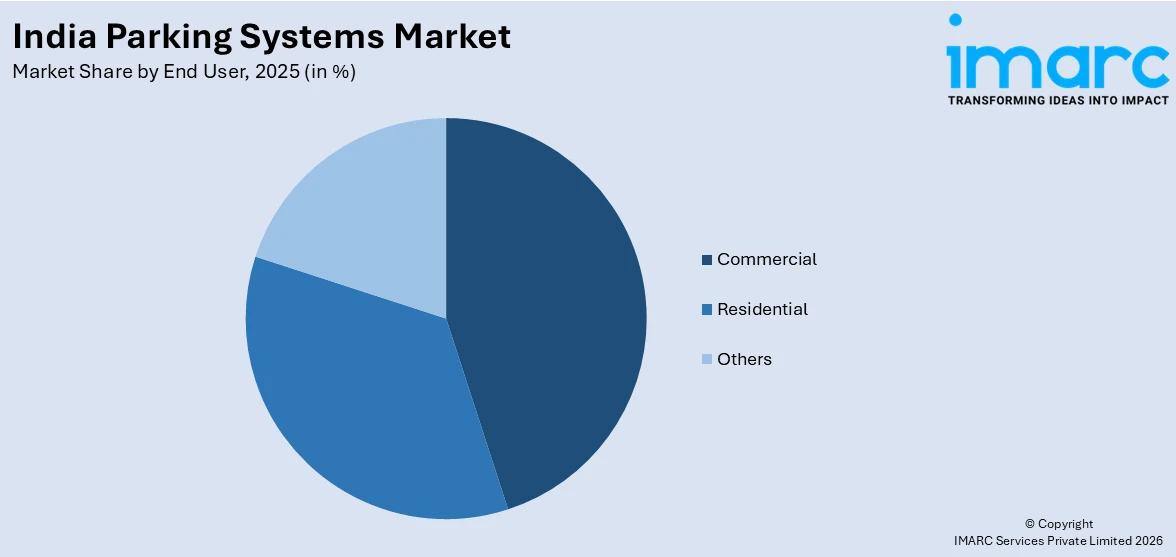

- By End User: Commercial dominates the market with a share of 45% in 2025, due to the increasing development of shopping malls, office complexes, and hospitality venues requiring organized parking infrastructure.

-

Key Players: The India parking systems market exhibits intensifying competition, with established manufacturers and technology providers investing in product innovation, geographic expansion, and strategic partnerships to strengthen their positioning across residential, commercial, and public parking segments.

To get more information on this market Request Sample

The parking systems market in India is gaining momentum amid rapid motorization, constrained urban land availability, and increasing focus on digitized civic infrastructure. Municipal bodies are prioritizing structured parking solutions to reduce roadside congestion, improve compliance, and enhance revenue transparency. The adoption of automated payment systems, integrated monitoring platforms, and data-driven enforcement mechanisms is transforming conventional parking operations into technology-enabled services. Demand is particularly strong in high-footfall commercial districts and transport hubs where efficient vehicle management is critical to traffic flow. Reflecting this shift, in 2025 the Municipal Corporation of Delhi initiated the rollout of a smart, cashless parking system across eight locations, including Karol Bagh, Lajpat Nagar, Nehru Place, Kashmere Gate ISBT, and Okhla Industrial Area, enabling FASTag-based payments for cars and digital options for two-wheelers as part of a broader initiative to digitize civic services and modernize urban parking administration.

India Parking Systems Market Trends:

Deployment of Advanced Access and Payment Technologies

The incorporation of license plate recognition, FASTag integration, and pre-booking capabilities is transforming parking facilities into automated mobility nodes. Advanced access control technologies are reducing manual intervention, improving transaction speeds, and enhancing enforcement accuracy. Integration with digital payment ecosystems supports seamless vehicle throughput and data collection for predictive traffic planning. Such modernization is particularly relevant in high-footfall areas requiring efficient vehicle management. In 2024, DESIGNA India implemented an advanced parking management and guidance system at the JBPC Multi Level Car Parking in Puri, incorporating automated identification and mobile-enabled ticketing solutions. The project, DESIGNA’s first in Odisha and the state’s largest multi-level parking facility, was designed to manage up to 5,600 transactions per day and ease congestion around the temple area.

Growing Use of Real-Time Data Analytics for Urban Traffic Optimization

Data-driven parking systems are emerging as vital tools for congestion mitigation and environmental management. By leveraging real-time sensors and analytics, municipalities can dynamically monitor occupancy levels, reduce unnecessary vehicle circulation, and lower emissions associated with parking searches. These systems contribute to structured curbside management and support sustainable urban mobility planning. The integration of analytics with municipal oversight enhances responsiveness and long-term infrastructure planning. This direction was evident in 2024, when Shimla partnered with Cocoparks to deploy a sensor-based smart parking system aimed at improving traffic flow and reducing congestion. The system used advanced sensors and real time data analytics to detect available parking spots, aiming to reduce congestion, lower emissions, and improve traffic flow in the hill city. Backed by city authorities and sustainability networks, the initiative is positioned as a step toward smarter urban mobility and better curbside management.

Customization of Automated Parking for Real Estate Development

Rising urban density and limited land availability are encouraging real estate developers to adopt customized automated parking solutions. Technology providers are offering modular, semi-automated, and fully automated systems tailored to residential, commercial, and mixed-use infrastructure projects. These solutions enhance project viability by optimizing space utilization and meeting regulatory parking requirements within constrained footprints. Domestic manufacturing capabilities further support cost efficiency and faster deployment cycles. This trend was reinforced in 2025 when Sieger Parking introduced customized automated parking systems targeting Mumbai’s real estate and infrastructure developments. The systems included fully automated, semi-automated, and modular stack parking technologies aimed at maximizing space efficiency in high density urban projects.

Market Outlook 2026-2034:

The India parking systems market is poised for sustained growth throughout the forecast period, underpinned by irreversible urbanization trends, expanding vehicle ownership, and government-driven infrastructure modernization. The market generated a revenue of USD 700.70 Million in 2025 and is projected to reach a revenue of USD 932.44 Million by 2034, growing at a compound annual growth rate of 3.23% from 2026-2034. Increasing investments in smart city infrastructure, proliferation of automated parking technologies, and the integration of digital payment ecosystems are expected to drive higher revenue streams. The convergence of commercial real estate expansion, rising user demand for convenience, and advancements in IoT-enabled parking management will foster a more competitive and technologically mature parking landscape across the country.

India Parking Systems Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Component |

Hardware |

68% |

|

Type |

Shuttle Parking System |

15% |

|

System |

Fully Automated System |

60% |

|

End User |

Commercial |

45% |

Component Insights:

- Hardware

- Camera

- Motors

- Raw Steel

- Sensors

- Electrical Panels

- Electrical Boxes

- Wireless Radios

- Fire Alarms/Audio Alarms

- Sprinklers

- Gears

- PIC Microcontroller

- LCD Display

- Others

- Software

Hardware dominates with a market share of 68% of the total India parking systems market in 2025.

Hardware leads the market due to its foundational role in enabling efficient parking management and access control. Core components, such as sensors, cameras, ticketing machines, automated barriers, and payment kiosks, form the backbone of both on-street and off-street parking infrastructure. The physical system ensures real-time vehicle detection, space monitoring, and secure entry-exit operations across commercial complexes, airports, malls, and residential societies. Compared to software-only solutions, hardware investments are essential for establishing functional parking ecosystems. The demand for reliable, durable, and scalable equipment strengthens hardware adoption, positioning it as the dominant segment in India’s evolving parking systems landscape.

The leadership of hardware is reinforced by rapid urbanization, increasing vehicle ownership, and government initiatives promoting smart city infrastructure across India. According to the Ministry of Housing and Urban Affairs, as of May 2025, 94% of 8,067 Smart Cities Mission projects have been completed, many incorporating hardware-intensive parking infrastructure. Rising demand for multi-level and automated structures further reinforces hardware procurement requirements. Municipal authorities and private developers prioritize installation of automated gates, surveillance cameras, and smart meters to address congestion and optimize space utilization. Additionally, integration of RFID, ANPR cameras, and IoT-enabled sensors enhances operational efficiency and revenue management. As cities modernize parking facilities to improve traffic flow and user convenience, hardware continues to attract significant capital investment, sustaining its dominance in the market.

Type Insights:

- Shuttle Parking System

- Puzzle Parking System

- Rotary Parking System

- Stacker Parking System

- Automated Guided Vehicle Parking Systems

- Rail Guided Parking System

- Crane Parking System

- Silo Parking System

- Tower Parking System

- Others

Shuttle parking system leads with a market share of 15% of the total India parking systems market in 2025.

Shuttle parking system dominates the market owing to its ability to maximize space utilization in dense urban development where land prices are high and plots are constrained. By moving vehicles horizontally on rails and vertically through lifts, it accommodates more cars within the same footprint than conventional ramp-based parking. Real estate developers prefer shuttle systems for residential towers, malls, and mixed-use projects as they reduce excavation depth, cut construction costs, and improve traffic flow within basements. The system also lowers idle time for users, offering faster vehicle retrieval during peak hours in commercial hubs and business districts across major cities.

Shuttle parking system is also gaining traction because it aligns with smart building adoption and automation trends across India. Developers and facility managers value their modular design, which allows phased expansion as vehicle demand grows. Compared with puzzle or tower systems, shuttle configuration offers better load distribution, higher reliability, and easier maintenance access. Indian cities facing rising car ownership and limited public parking supply are encouraging automated solutions through updated building codes and urban redevelopment projects. Shuttle system supports these initiatives by improving safety, reducing human intervention, and optimizing energy use with sensor-based controls. Its adaptability across varied plot sizes further strengthens their market position nationwide today significantly.

System Insights:

- Fully Automated System

- Semi-Automated System

Fully automated system exhibits a clear dominance with a 60% share of the total India parking systems market in 2025.

Fully automated system holds the biggest market share driven by its ability to deliver higher efficiency, safety, and convenience. This system eliminates the need for drivers to enter parking structures, reducing the risk of accidents, theft, and vehicle damage. In high density urban centers where land is limited and traffic congestion is higher, fully automated solution maximizes parking capacity within compact footprints. Developers favor it for premium residential complexes, commercial towers, airports, and hospitals, where seamless user experience is a priority. Faster retrieval times and minimal human intervention make it well suited for large scale projects.

The growing demand for smart infrastructure and contactless services further supports adoption of fully automated parking system across India. Integration with access control, payment gateways, license plate recognition, and building management systems enhances operational transparency and reduces manpower requirements. Property owners benefit from lower long term operating costs, optimized space utilization, and improved asset value. Government initiatives promoting organized urban development and stricter building regulations are also encouraging automated parking solution in metropolitan cities. As car ownership continues to rise and available land becomes scarcer, fully automated system offers a scalable and technologically advanced solution that meets evolving mobility and infrastructure needs nationwide.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Residential

- Commercial

- Shopping Malls

- Office Buildings

- Hospitals

- Public Car Parks

- Others

Commercial dominates with a market share of 45% of the total India parking systems market in 2025.

Commercial establishments, including shopping malls, office buildings, hospitals, and public car parks, represent the primary demand center for parking systems in India. The rapid expansion of organized retail and commercial real estate in tier-one and tier-two cities is driving substantial investment in structured parking solutions. According to SIAM, passenger vehicle sales reached their highest-ever levels in FY 2024-25 with a sale of 4.3 million units intensifying the demand for efficient commercial parking infrastructure capable of managing high vehicle throughput during peak hours.

The commercial segment benefits from the direct correlation between parking convenience and individual footfall, making organized parking a strategic priority for property developers and mall operators. Seamless parking experiences enabled by smart ticketing, FASTag integration, and mobile app-based reservations are becoming standard features across commercial properties. The proliferation of mixed-use developments combining retail, office, and entertainment spaces is further amplifying the need for multi-level and automated parking solutions that can accommodate diverse vehicle types and optimize revenue generation.

Regional Insights:

- North India

- South India

- East India

- West India

North India constitutes a significant demand hub for organized and automated parking systems, supported by dense urban populations across Delhi-NCR, Chandigarh, Lucknow, and surrounding cities. High vehicle ownership levels and persistent congestion in commercial and residential corridors are intensifying the need for structured parking infrastructure. The region also benefits from substantial public expenditure on urban redevelopment, smart city initiatives, and transport modernization projects.

South India is emerging as a vital hub for parking system innovation, supported by robust commercial real estate growth and progressive smart city implementations across Bengaluru, Hyderabad, Chennai, and Coimbatore. The region's technology-driven ecosystem facilitates early adoption of IoT-enabled and AI-powered parking solutions. Indigenous manufacturing capabilities, particularly in Coimbatore and Pune, provide localized supply chain advantages, while public-private partnerships are driving large-scale automated parking deployments across metropolitan and tier-two cities.

East India’s parking systems market is growing as urbanization accelerates across major cities, such as Kolkata, Bhubaneswar, and Patna. Rising vehicle ownership, rising commercial activity, and redevelopment of central business districts are increasing pressure on existing parking infrastructure. Municipal authorities are focusing on structured parking facilities to address roadside congestion and improve traffic circulation in densely populated zones. Smart city initiatives and investments in public transport hubs are further encouraging the integration of automated and digital parking technologies.

West India accounts for significant share of parking systems market, anchored by the high-density urban markets of Mumbai, Pune, and Ahmedabad. Severe land constraints in Mumbai's central business districts have necessitated widespread adoption of automated and vertical parking technologies. The region benefits from established manufacturing ecosystems and a concentration of leading parking system providers. The growing commercial infrastructure development, highway expansion projects, and increasing regulatory mandates for structured parking in new construction projects are sustaining long-term demand.

Market Dynamics:

Growth Drivers:

Why is the India Parking Systems Market Growing?

Adoption of High-Density Automated Parking Infrastructure

Urban land scarcity and persistent congestion in commercial districts are accelerating the deployment of fully automated, high-density parking systems. Municipal authorities are increasingly investing in robotic and shuttle-based solutions to maximize vertical space utilization and reduce on-street parking pressure. These systems minimize human intervention, improve vehicle retrieval efficiency, and optimize land productivity in premium urban locations. The focus on structured, technology-enabled parking is emerging as a foundational element of broader smart mobility strategies. This shift is reflected in 2025, when the Municipal Corporation of Delhi operationalized South Delhi’s first robo parking facility at Greater Kailash I, featuring a nine-level automated system accommodating 399 vehicles.

Integration of App-Based Smart Parking Platforms

The growing preference for digital mobility services is driving the integration of mobile applications into urban parking ecosystems. Cities are adopting app-enabled systems that provide real-time availability data, digital payments, and location-based services to enhance user convenience and traffic discipline. Such platforms improve compliance, reduce search time for parking, and support data-driven urban traffic planning. The digitization of curbside and off-street parking aligns with wider smart city objectives focused on transparency and operational efficiency. This trend was demonstrated in 2025, when Kerala launched the ParKochi Smart Parking Management System. The system was supported by a mobile application that provides real time parking availability, location details of parking lots, and enables digital payments for seamless vehicle parking.

Increasing Popularity of Sensor-Based Integrated Parking Networks

Large-scale deployment of sensor-enabled parking networks is strengthening centralized urban traffic management. Authorities are implementing integrated systems that combine occupancy sensors, automated barriers, digital toll integration, and command-and-control monitoring to streamline citywide parking operations. These solutions enhance revenue tracking, reduce leakages, and support coordinated congestion management across high-traffic zones. Public–private partnership (PPP) models are further enabling scalable rollouts across multiple sites. This approach gained momentum in 2025 when NDMC announced the rollout of an intelligent integrated parking management system covering 1,541 locations in Lutyens’ Delhi. The sensor-based system will cover major hubs such as Connaught Place and Khan Market, enabling real time occupancy tracking, FASTag payments, automated boom barriers, and centralized monitoring via an integrated command and control center.

Market Restraints:

What Challenges the India Parking Systems Market is Facing?

High Capital Investment Requirements Limiting Adoption Among Budget-Constrained Stakeholders

The significant upfront costs associated with installing automated parking systems, smart sensors, and integrated software platforms present a substantial barrier for municipalities, small-scale developers, and independent parking operators with limited financial resources. These capital-intensive requirements restrict broader market penetration, particularly in tier-two and tier-three cities where infrastructure budgets are comparatively constrained. The additional costs of retrofitting existing structures further compound financial challenges for stakeholders seeking to modernize legacy parking facilities.

Fragmented Regulatory Framework Creating Implementation Inconsistencies

The absence of a unified national parking policy and inconsistent regulatory standards across states and municipal bodies create implementation challenges for parking system providers. Varying building code requirements, permit processes, and parking mandates across jurisdictions complicate project planning and execution. This regulatory fragmentation discourages standardized technology deployment and increases compliance costs, slowing the pace of modernization and limiting the scalability of advanced parking solutions across different regions.

Infrastructure Deficiencies in Emerging Urban Areas Constraining Market Expansion

Inadequate supporting infrastructure, including unreliable electricity supply, limited internet connectivity, and poor road access in emerging urban areas, restricts the deployment of technology-driven parking systems. Many developing urban corridors lack the foundational utilities required to operate automated and IoT-enabled parking facilities effectively. These infrastructure gaps create barriers to market expansion beyond established metropolitan centers, leaving significant potential demand in rapidly growing tier-two and tier-three cities underserved.

Competitive Landscape:

The India parking systems market features a dynamic competitive environment characterized by the presence of established international technology providers alongside domestic manufacturers and emerging technology startups. Market participants are differentiating through product innovation, geographic expansion, and integration of advanced digital capabilities, including IoT connectivity, AI-driven analytics, and mobile payment solutions. Competition is increasingly shaped by the ability to deliver end-to-end solutions encompassing hardware manufacturing, software integration, installation, and after-sales maintenance support. Strategic partnerships between technology firms and real estate developers are fostering co-development of customized parking solutions. Public-private partnership (PPP) models are enabling larger infrastructure deployments, while indigenous manufacturing capabilities are strengthening cost competitiveness. The market is further energized by startup activity introducing disruptive approaches to parking management through app-based platforms and shared parking ecosystems.

Recent Developments:

- January 2026: India’s first fully automated multi-level parking complex was inaugurated in Hyderabad’s Nampally area, introducing a sensor based, pallet free parking system using Germany’s Palis technology. The 15-floor facility accommodates 250 cars and up to 200 two wheelers, operates through QR code smart cards, and parks vehicles automatically without human intervention. Developed under a PPP model on HMRL land with over Rs 100 crore investment, the project aims to address urban parking congestion with a high density, tech enabled solution.

- January 2026: Chandigarh Municipal Corporation launched the ‘MC One Pass’ smart parking system, enabling a single monthly digital pass valid across all civic body managed parking sites. The initiative aims to simplify parking access for daily commuters by integrating multiple surface and multi-level parking locations under a unified smart system.

India Parking Systems Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Types Covered | Shuttle Parking System, Puzzle Parking System, Rotary Parking System, Stacker Parking System, Automated, Guided Vehicle Parking Systems, Rail Guided Parking System, Crane Parking System, Silo Parking System, Tower Parking System, Others |

| Systems Covered | Fully Automated System, Semi-Automated System |

| End Users Covered |

|

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The India parking systems market size was valued at USD 700.70 Million in 2025.

The India parking systems market is expected to grow at a compound annual growth rate of 3.23% from 2026-2034 to reach USD 932.44 Million by 2034.

Fully automated system dominates the India parking systems market with a share of 60% in 2025, driven by rising demand for zero-intervention parking technologies that maximize space utilization, reduce labor costs, and improve vehicle security across commercial and residential developments.

Key factors driving the India parking systems market include rising urban density and constrained land availability, prompting developers to adopt customized automated solutions, exemplified in 2025 when Sieger Parking introduced modular and fully automated stack systems for high-density real estate projects in Mumbai.

Major challenges include high capital investment requirements for automated systems, fragmented regulatory frameworks across states and municipalities, infrastructure deficiencies in emerging urban areas, limited awareness of advanced parking technologies, and the complexity of retrofitting existing structures with modern solutions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)