India Passenger Vehicles Market Size, Share, Trends and Forecast by Propulsion, Vehicle Type, Application, Drive Type, and Region, 2026-2034

India Passenger Vehicles Market Size, Share, Trends & Forecast (2026-2034)

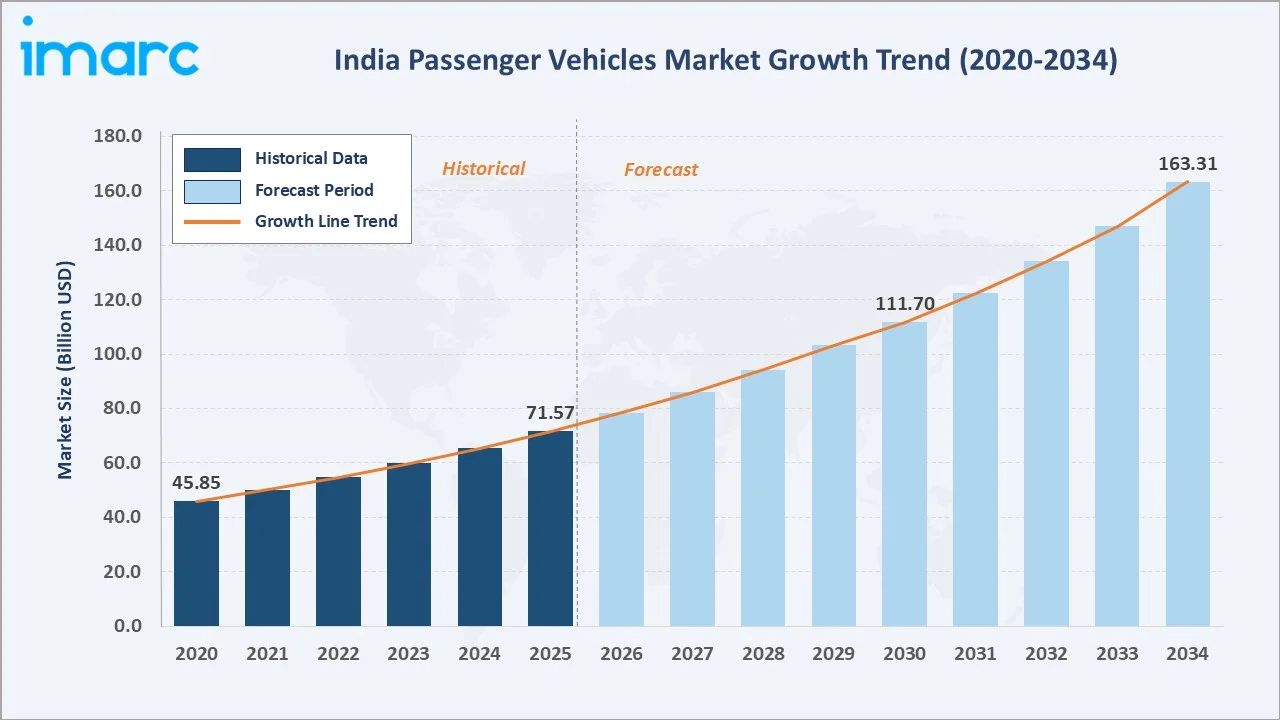

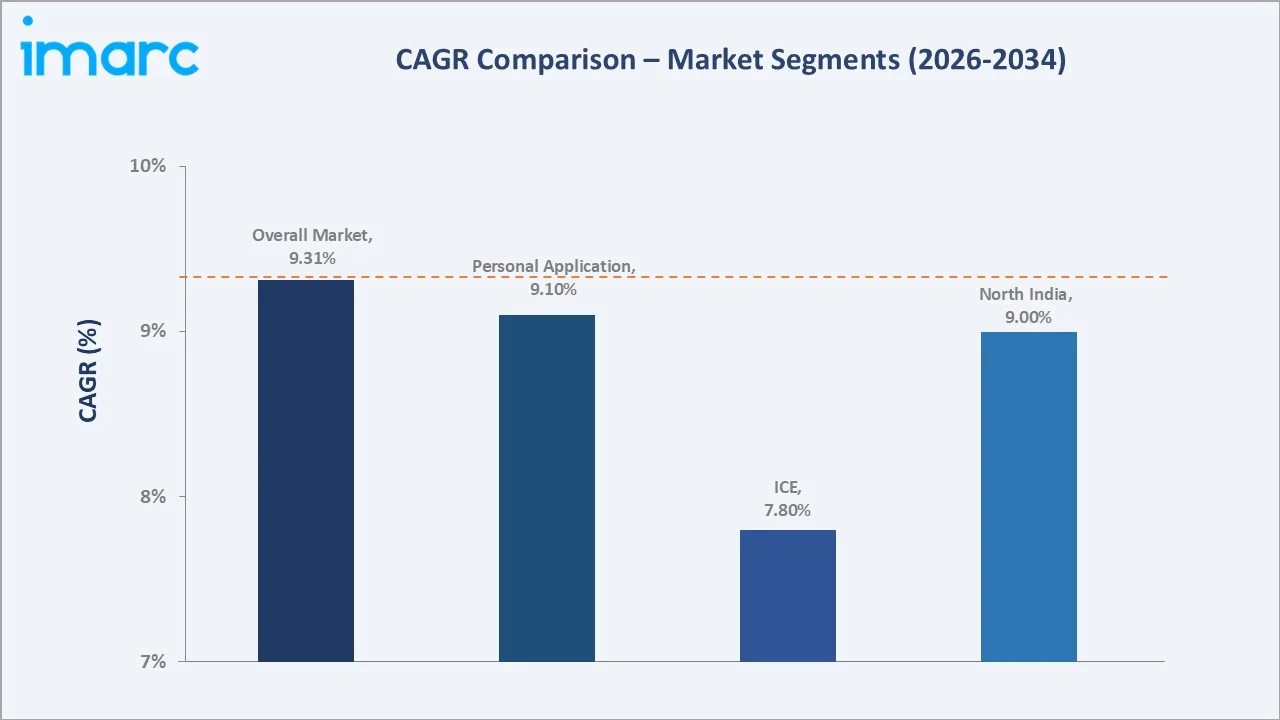

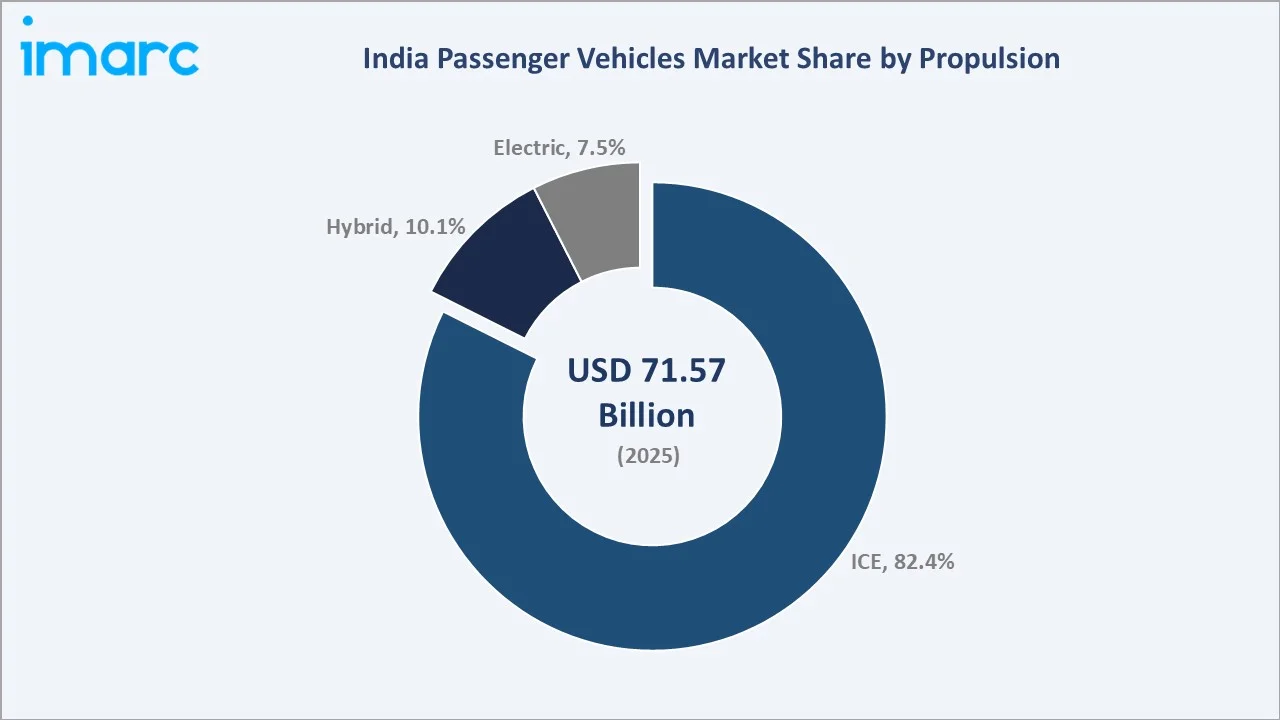

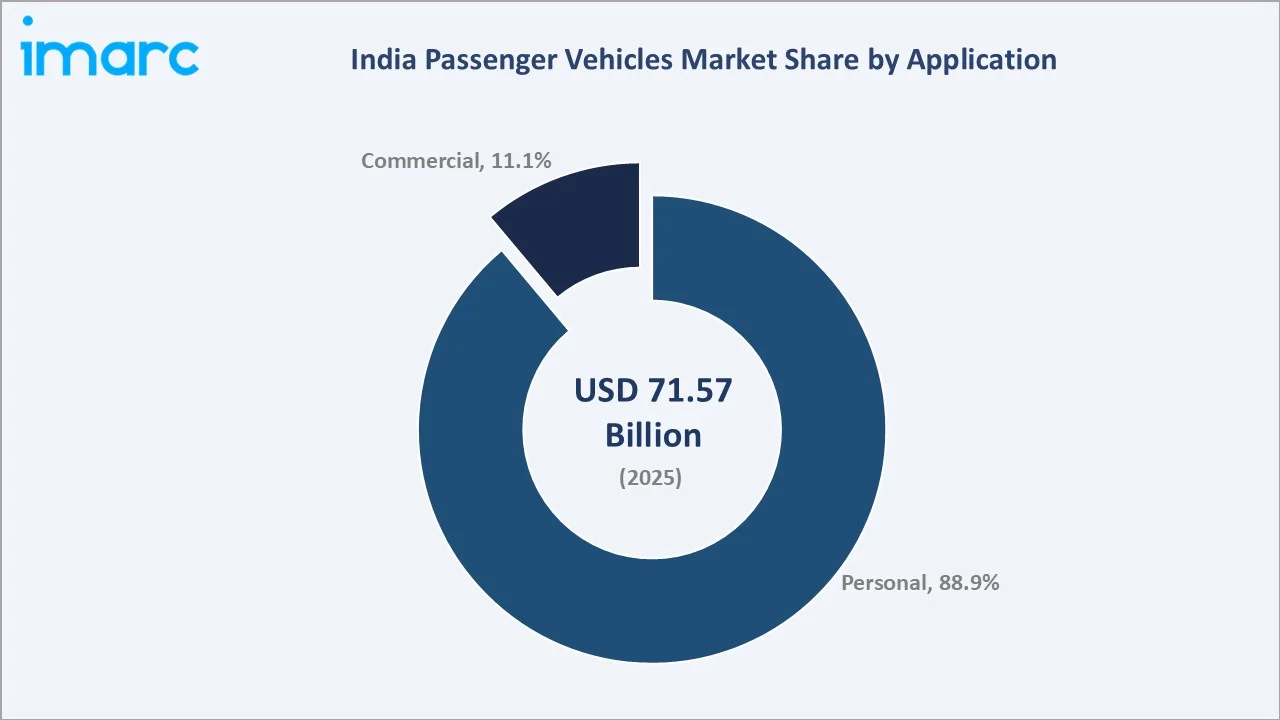

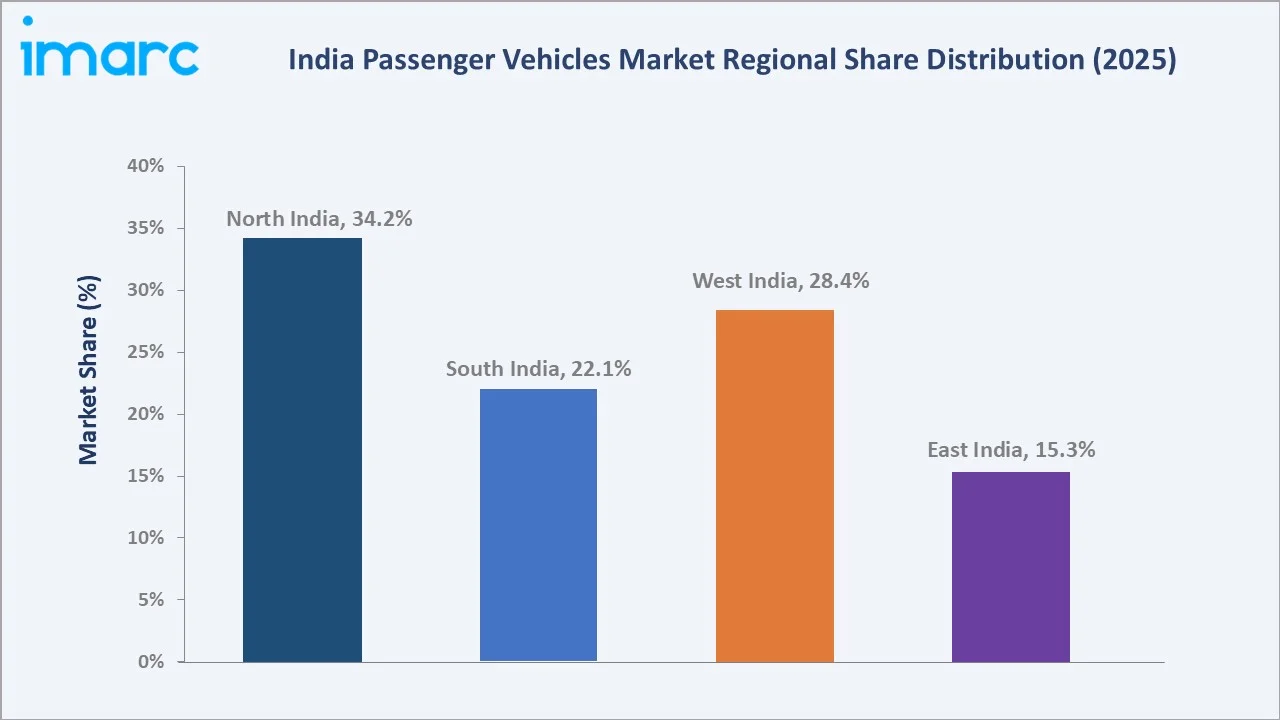

The India passenger vehicles market size reached USD 71.57 Billion in 2025 and is projected to reach USD 163.31 Billion by 2034, growing at a CAGR of 9.31% during 2026-2034. The market is driven by rising disposable incomes, rapid urbanization, and expanding road infrastructure nationwide. Growing consumer aspiration for SUVs, increased adoption of alternative fuel powertrains including CNG and EVs, and favorable government tax reforms are reshaping the competitive landscape. ICE leads propulsion with 82.4% share in 2025. Personal application dominates at 88.9%. North India commands 34.2% of the national market share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 71.57 Billion |

|

Forecast Market Size (2034) |

USD 163.31 Billion |

|

CAGR (2026-2034) |

9.31% |

|

Dominant Propulsion |

ICE (82.4%, 2025) |

|

Dominant Application |

Personal (88.9%, 2025) |

|

Leading Region |

North India (34.2%, 2025) |

The India passenger vehicles market expanded from USD 45.85 Billion in 2020 to USD 71.57 Billion in 2025, anchored at USD 111.70 Billion in 2030, and forecast to reach USD 163.31 Billion by 2034. This trajectory reflects one of Asia's most commercially dynamic personal mobility markets, combining a massive first-time buyer base, rapidly accelerating SUV premiumization, and strong policy-driven EV adoption, making India a high-priority market for global automotive investment.

To get more information on this market, Request Sample

The market is commercially unique in its dual-speed structure: the mass-market ICE and CNG segment sustaining high-volume growth through first-time buyer expansion and rural penetration, while the premium EV and SUV segments generate above-market CAGR through India's rapidly expanding urban professional and high-net-worth consumer base.

Executive Summary

The India passenger vehicles market reached USD 71.57 Billion in 2025, establishing itself as one of Asia's largest and fastest-growing automotive markets by absolute value growth. The market is projected to reach USD 163.31 Billion by 2034, delivering a compound annual growth rate of 9.31% during 2026-2034. This robust expansion reflects the convergence of structural demographic drivers, favorable government policy frameworks, and accelerating consumer premiumization across all vehicle segments.

The market is distinguished by its extraordinary segment stratification. SUVs now command 46.1% of total passenger vehicle dispatches in 2025, reflecting a fundamental shift in consumer preferences toward larger, feature-equipped utility vehicles. The personal application segment dominates with 88.9% share, underpinned by rising household incomes and improving vehicle financing accessibility. Simultaneously, CNG vehicles surpassed diesel in sales share in FY2025, while EV registrations rose 77% in calendar year 2025 to exceed 176,000 units, signaling accelerating powertrain diversification.

North India leads regionally with 34.2% market share in 2025, driven by high population density, strong dealership penetration, and CNG ecosystem maturity across Delhi-NCR, Uttar Pradesh, and Haryana. The competitive landscape is intensifying as domestic manufacturers including Maruti Suzuki, Tata Motors, and Mahindra & Mahindra expand their EV portfolios while defending core ICE positions, and global players like Hyundai and Kia accelerate their India-specific product strategies.

Key Market Insights

|

Insight |

Data |

|

Dominant Propulsion |

ICE - 82.4% share (2025) |

|

Dominant Application |

Personal - 88.9% market share (2025) |

|

Leading Region |

North India - 34.2% share (2025) |

|

Fastest Growing Propulsion |

Electric (EV registrations up 77% in 2025) |

|

Market Opportunity |

EV infrastructure expansion; CNG ecosystem growth; SUV premiumization in Tier-2 cities |

Key Analytical Observations Supporting the Above Data:

- ICE at 82.4% (2025): Internal combustion engines maintain dominance due to well-established refueling infrastructure, competitive pricing across all vehicle segments, and ongoing BS-VI-compliant engine improvements. CNG within the ICE category grew to represent 19.4% of total PV sales in FY2025, outpacing diesel for the first time.

- Personal at 88.9% (2025): The personal segment commands overwhelming share through India's expanding middle class, improved vehicle financing at competitive EMI structures, and the aspiration for private mobility in both urban and rural markets. Rural passenger vehicle retail grew 7.93% in FY2025, outpacing urban growth.

- North India at 34.2% (2025): North India leads through Delhi-NCR's concentration of premium retail, India's highest-density corporate market, and CNG ecosystem maturity across key urban corridors of Uttar Pradesh, Haryana, and Punjab.

- EV Growth: EV registrations grew 77% in calendar year 2025 to exceed 176,000 units, demonstrating accelerating consumer adoption as model ranges expand and acquisition costs decline.

- SUV Dominance: SUVs command 46.1% of total PV dispatches in 2025, with compact and midsize utility vehicles across every price tier reshaping dealer inventory and OEM production planning priorities.

India Passenger Vehicles Market Overview

The India passenger vehicles market encompasses the manufacture, assembly, sale, and service of all four-wheeled, non-commercial personal transportation vehicles registered in India, including hatchbacks, sedans, SUVs, MUVs, and emerging electric and hybrid powertrains. The market ecosystem integrates domestic OEM manufacturing clusters, global technology partnerships, component Tier-1 and Tier-2 supplier networks, franchise dealership distribution, and an expanding digital purchase and subscription commerce layer.

Macroeconomic drivers include India's GDP growth trajectory, urbanization rate exceeding 36% as of 2025, and the Reserve Bank of India's monetary policy environment supporting accessible auto financing. Regulatory frameworks including BS-VI emission standards, EV incentive structures, and state-level road tax rationalization are structuring the competitive landscape. The ecosystem spans raw material procurement through the full after-sales value chain, encompassing over 15,000+ dealerships and 30,000+ outlets nationwide.

Market Dynamics

To evaluate market opportunities, Request Sample

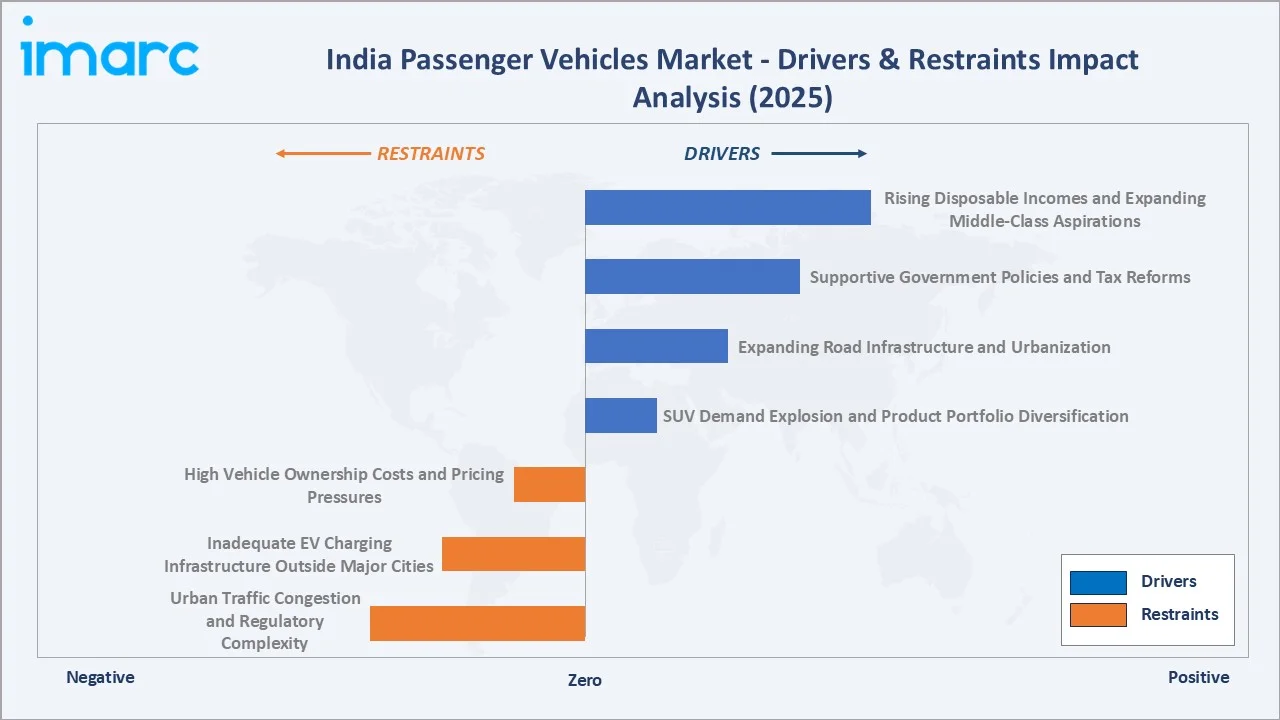

Market Drivers

- Rising Disposable Incomes and Expanding Middle-Class Aspirations: India's sustained GDP growth is driving rapid middle-class expansion, with household disposable incomes rising consistently across urban and semi-urban markets. A larger share of the population is transitioning from two-wheelers to four-wheelers, particularly in semi-urban and rural markets where improved agricultural yields and non-farm income growth are boosting purchasing power. According to the Reserve Bank of India's monetary policy reports, competitive auto loan interest rates and extended tenure options have lowered the effective cost of vehicle ownership, enabling first-time buyers across all income levels to enter the passenger car market.

- Supportive Government Policies and Tax Reforms: The Government of India's progressive regulatory approach has created consistent demand stimulation across both conventional and electric vehicle segments. GST rate rationalization has reduced tax burden on sub-four-meter passenger vehicles, making them more accessible to mass-market consumers. The Ministry of Heavy Industries' national EV incentive framework provides demand-linked subsidies and supports domestic charging infrastructure through public and private investment channeling. State-level incentives including registration fee waivers, road tax exemptions, and preferred parking policies for EVs further reduce total cost of ownership, encouraging manufacturers to expand capacity and introduce segment-specific models.

- Expanding Road Infrastructure and Urbanization: India's National Highways Authority of India (NHAI) has significantly accelerated highway network expansion, with the total national highway length crossing 146,000+ km by 2025. New ring roads, expressways, and access-controlled corridors connecting large cities to Tier-2 and Tier-3 centers are reducing commuting friction and expanding the geographic addressable market for personal vehicles. According to Ministry of Road Transport and Highways annual reports, improved last-mile connectivity in previously underserved regions is catalyzing first-time vehicle purchases beyond conventional metropolitan markets. Fast urbanization is simultaneously increasing demand for personal transportation as public transit capacity in most Indian cities continues to fall short of commuter growth.

- SUV Demand Explosion and Product Portfolio Diversification: Consumer preferences have shifted decisively toward SUVs and utility vehicles, which now account for 46.1% of total passenger vehicle dispatches in 2025 according to Society of Indian Automobile Manufacturers (SIAM) data. Manufacturers are aggressively expanding SUV portfolios across sub-compact, compact, midsize, and full-size categories, covering price points from under INR 8 lakh to above INR 50 lakh. This portfolio diversification is drawing first-time buyers who previously purchased hatchbacks and sedans into the utility vehicle segment, reshaping production strategies and dealership inventory priorities across the entire industry.

Market Restraints

- High Vehicle Ownership Costs and Pricing Pressures: The total cost of vehicle ownership remains a significant barrier for a sizable portion of India's population despite tax reforms. Rising input costs including steel, aluminum, and semiconductor components continue to put upward pressure on ex-showroom prices. Insurance premiums, fuel price volatility, toll costs, and maintenance expenses further increase effective ownership costs. These pressures are most acute in the entry-level hatchback segment, where price sensitivity is highest and marginal cost increases have outsized impact on purchase decisions.

- Inadequate EV Charging Infrastructure Outside Major Cities: Public charging infrastructure remains sparse outside India's top metropolitan centers, with range anxiety continuing to deter potential EV buyers in semi-urban and rural markets. According to the Ministry of Power's data on EV charging stations, the density of fast-charging networks is concentrated along select national highway corridors and urban centers, leaving large geographic gaps that constrain effective intercity EV utility. This infrastructure deficit is slowing the transition away from conventional powertrains in markets that represent the highest growth opportunity for overall passenger vehicle penetration.

- Urban Traffic Congestion and Regulatory Complexity: Severe traffic congestion in India's major cities reduces the functional utility of private vehicle ownership and degrades the overall ownership experience. Fragmented and sometimes conflicting state-level regulations on vehicle registration, road taxes, and end-of-life vehicle scrapping policies add compliance complexity for manufacturers and consumers alike. Sporadic implementation of odd-even traffic schemes and entry restrictions in select cities creates uncertainty in consumer purchase behavior, particularly in the nation's highest-density metropolitan markets.

Market Opportunities

- Electric Vehicle Ecosystem Expansion: India's EV segment represents the most commercially dynamic opportunity in the passenger vehicles market, growing at a substantially higher CAGR than the overall market. Expanding charging infrastructure investment, declining battery costs, and government incentive frameworks are creating conditions for mass-market EV adoption beyond the current early-adopter demographic. Manufacturers with early-mover positions in affordable EV segments - particularly the sub-INR 15 lakh price band - stand to capture significant first-time EV buyer volume as the technology becomes mainstream.

- Tier-2 and Tier-3 City Premium Vehicle Market Penetration: India's smaller cities represent an underserved premium vehicle market, where rising incomes, aspirational consumption patterns, and improving road infrastructure are creating structured demand for mid-range and premium passenger vehicles. Manufacturers with strong dealership expansion strategies targeting Tier-2 and Tier-3 cities are positioned to capture above-average growth as this geographic market segment matures beyond its current relatively low vehicle penetration base.

Market Challenges

- Rapid Technological Obsolescence in Connected and Electric Vehicles: Accelerating software and technology cycles in connected, autonomous, and electric vehicles are compressing product refresh timelines and increasing R&D cost intensity for manufacturers. Consumer expectations for over-the-air update capability, advanced driver assistance systems, and seamless smartphone integration are rising rapidly, requiring continuous technology investment to maintain product relevance. The pace of EV battery technology improvement is shortening effective model lifecycles, putting pressure on inventory management and residual value maintenance.

- Supply Chain Vulnerability for Semiconductor and Battery Components: India's passenger vehicle manufacturers remain dependent on global supply chains for critical semiconductor components and lithium-ion battery cells, creating vulnerability to supply disruptions. The global semiconductor shortage demonstrated the market's exposure to component supply constraints, with production volumes impacted across multiple manufacturers. Building domestic semiconductor fabrication capacity and securing long-term battery supply agreements are strategic imperatives, but require significant capital investment and long development timelines to achieve meaningful localization.

Emerging Market Trends

1. SUV Democratization Across Price Segments Reshaping Market Composition

The consistent expansion of the SUV segment into lower price tiers is structurally reshaping India's passenger vehicle market composition. Sub-compact SUVs priced between INR 7-12 lakh are drawing first-time vehicle buyers who previously would have purchased entry-level hatchbacks, with manufacturers like Maruti Suzuki, Tata Motors, and Kia introducing multiple competing models within this price band. This democratization of utility vehicle access is a defining trend accelerating overall market premiumization and changing the production economics of the entire industry.

2. CNG-Powered Vehicles Outpacing Diesel in Passenger Vehicle Segment

The rapid expansion of city gas distribution (CGD) networks across India is driving a fundamental shift in fuel preference within the ICE segment. According to the Petroleum and Natural Gas Regulatory Board (PNGRB) network expansion data, CGD network coverage extended to over 700 districts by 2025, creating the critical mass of refueling infrastructure needed for mass CNG adoption. In FY2025, CNG passenger vehicles surpassed diesel's share for the first time, with Maruti Suzuki alone selling approximately 620,000 CNG vehicles, representing a 28% year-on-year increase. This trend is being reinforced by factory-fitted CNG dual-fuel systems that eliminate the performance compromises of aftermarket conversions.

3. Premiumization Through Technology and Safety Feature Integration

India's passenger vehicle buyers are increasingly prioritizing advanced technology, safety, and connected features in their purchase decisions, reflecting a broader consumer lifestyle premiumization. Vehicles equipped with Level 2 advanced driver assistance systems, six airbags, electronic stability control, panoramic sunroofs, and multi-screen infotainment setups are becoming mainstream across mid-range segments priced between INR 12-20 lakh. This technology-led premiumization is enabling manufacturers to achieve better revenue per unit and is compressing the previous feature differentiation between mass-market and premium segments.

4. EV Ecosystem Acceleration and Range Expansion

India's electric passenger vehicle segment is transitioning from early-adopter niche to early mainstream adoption, driven by expanding model availability, improving battery range, and declining acquisition costs. EV registrations grew 77% in calendar year 2025 to exceed 176,000 units, reflecting the combination of new model launches, charging infrastructure expansion, and government incentive effectiveness. Manufacturers are investing in purpose-built EV platforms with longer range capabilities and faster charging specifications to address range anxiety and compete on total cost of ownership over five-year ownership horizons.

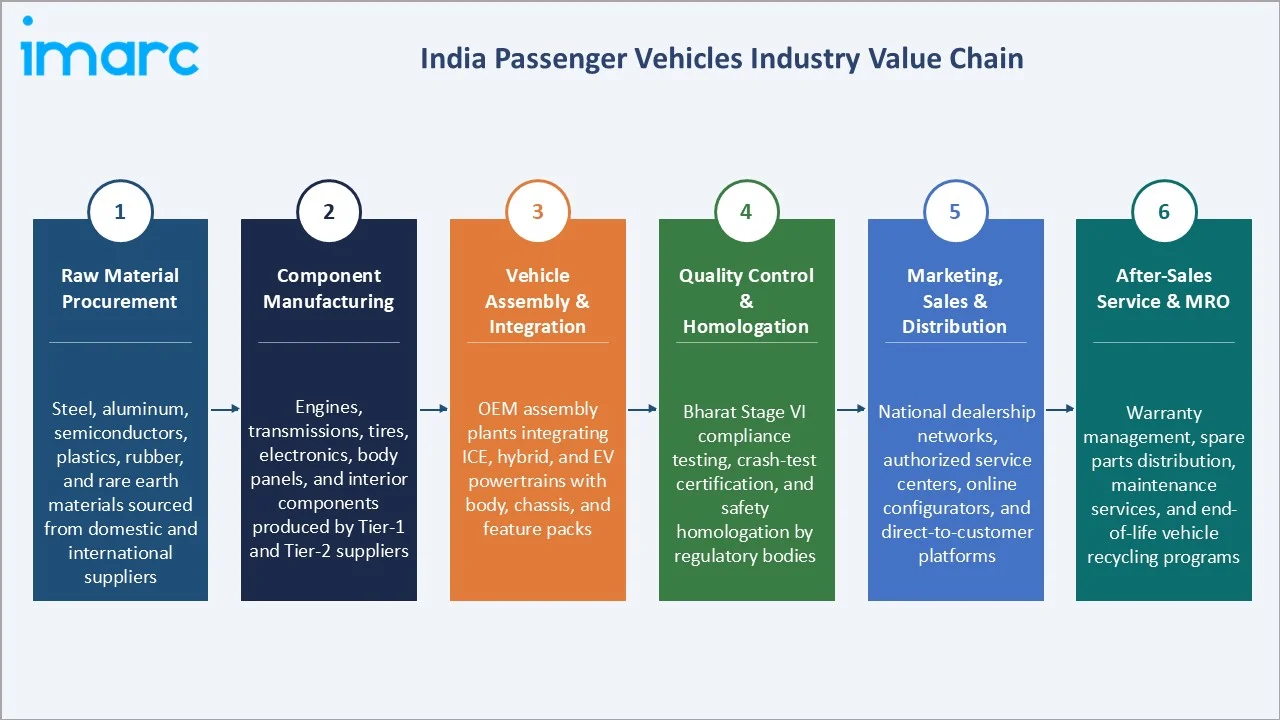

Industry Value Chain Analysis

India passenger vehicles value chain is one of the most vertically complex of any consumer product category, integrating globally sourced raw materials, domestically manufactured components, sophisticated assembly operations, and extensive nationwide distribution and after-sales infrastructure. The value chain's commercial structure determines cost competitiveness, product feature capability, and strategic flexibility for manufacturers operating in India's highly price-sensitive yet aspiration-driven market.

|

Stage |

Description |

|

Raw Material Procurement |

Steel, aluminum, semiconductors, plastics, rubber, and rare earth materials sourced from domestic and international suppliers |

|

Component Manufacturing |

Engines, transmissions, tires, electronics, body panels, and interior components produced by Tier-1 and Tier-2 suppliers |

|

Vehicle Assembly & Integration |

OEM assembly plants integrating ICE, hybrid, and EV powertrains with body, chassis, and feature packs |

|

Quality Control & Homologation |

Bharat Stage VI compliance testing, crash-test certification, and safety homologation by regulatory bodies |

|

Marketing, Sales & Distribution |

National dealership networks, authorized service centers, online configurators, and direct-to-customer platforms |

|

After-Sales Service & MRO |

Warranty management, spare parts distribution, maintenance services, and end-of-life vehicle recycling programs |

The regulatory compliance and quality control stage is commercially critical, with BS-VI emission norm adherence, crash-test certification under Bharat NCAP, and GST compliance creating structured cost and timeline requirements for all market participants. Marketing and distribution investment represents 8-15% of revenue for most manufacturers, with digital configurators, virtual showrooms, and subscription finance platforms increasingly supplementing traditional dealership models.

Technology Landscape in the India Passenger Vehicles Industry

Internal Combustion Engine and CNG Technologies

Internal combustion engine technology remains the backbone of India's passenger vehicle market, accounting for 82.4% of the propulsion mix in 2025. Manufacturers are investing in next-generation direct-injection gasoline engines, turbocharging, and mild-hybrid integration to meet BS-VI Phase 2 emission standards while improving fuel efficiency. CNG dual-fuel systems have achieved commercial maturity with factory-fitted configurations from major OEMs offering performance approaching pure petrol equivalents, eliminating the range and refueling time constraints of early CNG adaptations.

Electric and Hybrid Powertrain Technologies

Electric vehicle technology is advancing rapidly within India's passenger vehicle segment, with battery pack energy density improvements reducing costs toward competitive parity with ICE vehicles. Tata Motors' Acti.ev platform and Mahindra's Born Electric platform represent Indian OEMs' investment in purpose-built EV architectures that optimize battery integration, weight distribution, and feature packaging. Strong and mild hybrid technologies are simultaneously gaining traction among manufacturers seeking to improve fuel efficiency and meet CAFE norms without the full EV infrastructure dependency, with Toyota's strong hybrid models demonstrating commercial viability in the mid-premium segment.

Connected and Advanced Driver Assistance Technologies

Connected vehicle platforms with over-the-air update capability, Level 2 ADAS including automatic emergency braking, adaptive cruise control, and lane keep assist, and advanced infotainment with seamless smartphone integration are becoming commercially standard across the INR 12-25 lakh segment. India's vehicle safety rating system Bharat NCAP, launched in 2023, is accelerating OEM investment in structural safety and active safety technologies. According to SIAM data, the penetration of six-airbag equipped vehicles grew substantially in 2025 as manufacturers standardized passive safety equipment across model ranges ahead of proposed regulatory mandates.

Market Segmentation Analysis

The segments involved in the report include:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Propulsion |

ICE |

82.4% |

2025 |

|

Application |

Personal |

88.9% |

2025 |

|

Vehicle Type |

SUV |

46.1% |

2025 |

|

Drive Type |

Front-wheel Drive |

72.5% |

2025 |

|

Region |

North India |

34.2% |

2025 |

By Propulsion

ICE leads the propulsion segment at 82.4% in 2025. The internal combustion engine segment encompasses India's most commercially mature and geographically extensive vehicle infrastructure, covering petrol, CNG, and diesel powertrain variants across every vehicle type and price segment. ICE's commercial resilience reflects the combination of established refueling infrastructure, consumer familiarity, competitive pricing advantage over EV alternatives, and ongoing technological improvements that sustain the segment's performance and efficiency credentials.

To access detailed market analysis, Request Sample

Hybrid at 10.1% is growing through India's premium consumer base seeking the fuel efficiency benefits of electrification without the range and charging infrastructure dependency of pure EVs. Electric at 7.5% represents the fastest-growing propulsion category, with EV registrations growing 77% in 2025. Government incentive frameworks, expanding charging networks, and new model launches below INR 15 lakh are supporting accelerating EV adoption.

By Application

Personal application dominates at 88.9% in 2025. This segment commands an overwhelming share of India's passenger vehicle market, reflecting the deep aspiration for personal mobility among India's expanding middle-class population. Rising household incomes, improved availability of competitive vehicle financing, and growing preference for private transportation over public transit - particularly in cities with inadequate public transit quality - are sustaining robust personal segment demand. Rural market penetration is expanding rapidly, with rural passenger vehicle retail growing 7.93% in FY2025 according to industry data.

Commercial application at 11.1% serves fleet operators, cab aggregators, and corporate mobility requirements. This segment benefits from India's growing gig economy and ride-hailing market, with Ola, Uber, and other aggregators maintaining large fleets of passenger vehicles for commercial passenger transport services.

Regional Market Insights

|

Region |

Share (2025) |

Key Market Drivers & Characteristics |

|

North India |

34.2% |

High population density in Uttar Pradesh, Delhi-NCR, Haryana, and Punjab. Strong dealership networks and robust consumer purchasing power. CNG adoption driven by city gas distribution along major corridors. |

|

West India |

28.4% |

Maharashtra and Gujarat anchoring demand through Mumbai's HNI consumer base, Pune's growing IT and manufacturing workforce, and strong SUV aspirations among urban professionals. |

|

South India |

22.1% |

Bengaluru, Hyderabad, and Chennai driving premium and EV adoption among tech-sector professionals. Strong demand for connected and feature-rich vehicles across urban centers. |

|

East India |

15.3% |

Rising agricultural incomes and increasing urban aspirations in Kolkata, Bhubaneswar, and Guwahati gradually expanding first-time buyer penetration in four-wheeler categories. |

North India's 34.2% market leadership reflects Delhi-NCR's premium retail concentration, India's highest-density corporate vehicle procurement market, and the CNG ecosystem's maturity along major urban corridors of Uttar Pradesh and Haryana. West India's 28.4% reflects Maharashtra's HNI wealth concentration and Gujarat's industrial prosperity driving above-national average vehicle demand intensity.

South India's 22.1% reflects the IT-sector wealth concentration in Bengaluru and Hyderabad creating premium and EV aspiration, while Chennai's manufacturing ecosystem supports brand loyalty for locally assembled models. East India's 15.3% is the most commercially underdeveloped region but is growing above the overall market CAGR as Kolkata's premium retail development and northeast India's rising urban professional income create first-generation premium vehicle demand from a lower penetration base.

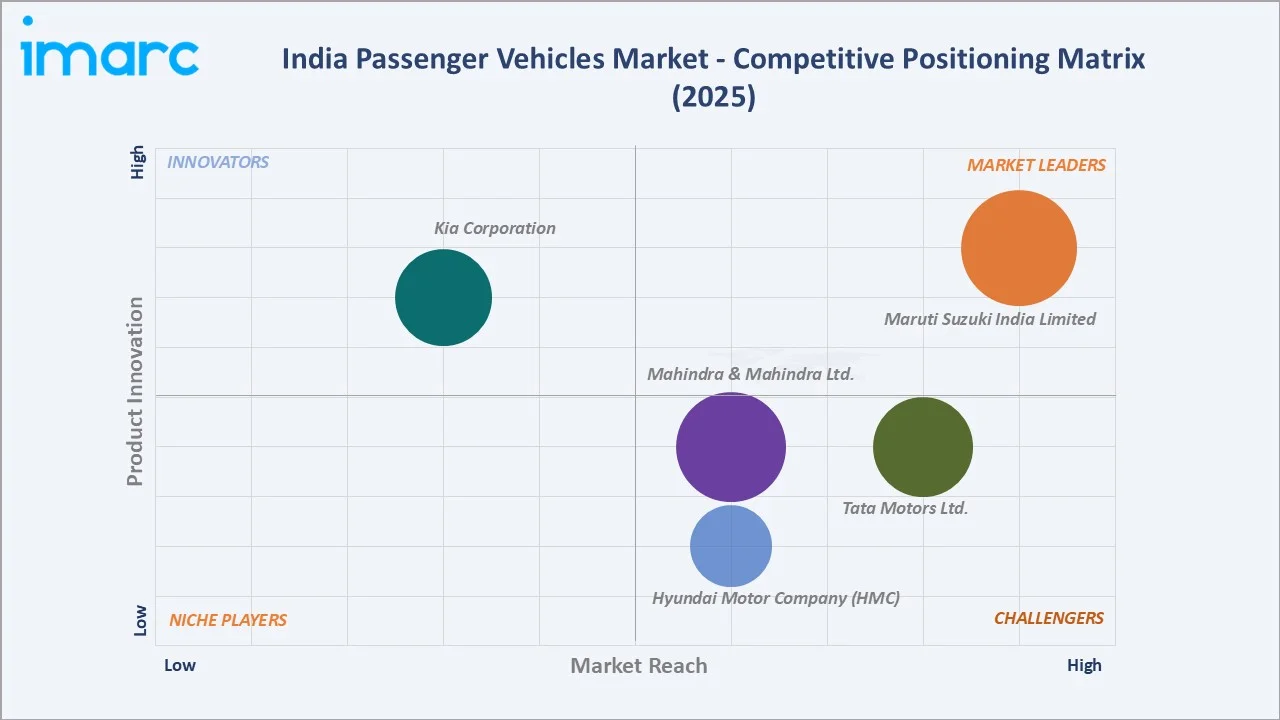

Competitive Landscape

India's passenger vehicle competitive landscape is defined by the dominance of Maruti Suzuki at the mass-market end, with an estimated 40% share of total organized passenger vehicle retail, alongside intensifying competition from Hyundai, Tata Motors, and Mahindra & Mahindra across mid-range and premium segments. The market's commercial structure is characterized by aggressive product proliferation, with manufacturers introducing multiple new models and variants annually to capture evolving consumer preferences. Competition is intensifying through electrification investment, CNG model expansion, digital customer engagement platforms, and strategic tie-ups between domestic and international manufacturers for platform and technology sharing.

|

Company |

Key Brands/Models |

Market Position |

Core Strength |

|

Maruti Suzuki India Limited |

Baleno, Swift, Brezza, Ertiga, Grand Vitara |

Market Leader |

Largest market share through extensive dealership reach, CNG vehicle leadership, and mass-market pricing competitiveness |

|

Hyundai Motor Company (HMC) |

Creta, Venue, Verna, Alcazar, Tucson |

Strong Challenger |

Feature-rich product range with strong appeal across mid-size and premium SUV segments; aggressive EV portfolio expansion |

|

Tata Motors Ltd. |

Nexon, Punch, Harrier, Safari, Tiago, Altroz, Curvv |

Strong Challenger |

EV segment leadership through Nexon EV and Punch EV; five-star safety ratings building brand trust and premium positioning |

|

Mahindra & Mahindra Ltd. |

Scorpio-N, XUV700, XUV 3XO, Thar, BE 6, XEV.9e |

Strong Challenger |

Dominant in premium SUV and off-road segments; Born Electric platform positioning for next-generation EV premium market |

|

Kia Corporation |

Sonet, Seltos, Carens |

Emerging Player |

Rapid market penetration through design-forward SUVs and premium feature integration at competitive price points |

Key Company Profiles

Maruti Suzuki India Limited

Maruti Suzuki India Limited, an Indian subsidiary of Suzuki Motor Corporation, is India's largest passenger vehicle manufacturer by sales volume, maintaining a commanding position across hatchback, sedan, SUV, and CNG vehicle segments.

- Key Models: Baleno, Swift, Brezza, Ertiga, Grand Vitara, Jimny, WagonR, Dzire, Alto, Celerio, S-Presso, Invicto, and others.

- Recent Developments: In June 2026, Maruti Suzuki unveiled India’s first flex-fuel passenger car promoting the vision of Atmanirbhar Bharat. The technology is integrated in Wagon R which provides flexibility to customers to run on any blend of ethanol and petrol from E20 to E100.

- Strategic Focus: Maintaining mass-market leadership while expanding CNG and EV portfolio; investing in new manufacturing facility in Kharkhoda, Haryana with planned capacity of over 2 million units per year to meet growing demand.

Hyundai Motor Company (HMC)

Hyundai Motor Company (HMC), the parent company of Hyundai Motor India Limited, is a prominent passenger vehicle manufacturer in India, known for feature-rich models across the compact, mid-size, and premium SUV segments.

- Key Models: Creta, Venue, Verna, Alcazar, Tucson, Grand i10 NIOS, i20, Aura, Exter, Ioniq, and others.

- Recent Developments: In October 2024, Hyundai Motor India Ltd. announced India’s Largest IPO and plans to expand investment and localize EV supply network.

- Strategic Focus: Reinforcing leadership in feature-rich compact and mid-size SUV segments; accelerating EV localization; expanding after-sales network in Tier-2 and Tier-3 cities.

Tata Motors Ltd.

Tata Motors Limited, operates via Tata Motors Passenger Vehicles (TMPV), is India's leading electric passenger vehicle manufacturer and a strong challenger in the overall passenger vehicle segment, with a portfolio spanning entry-level hatchbacks to premium SUVs and India's most comprehensive EV lineup.

- Key Models: Nexon, Punch, Harrier, Safari, Tiago, Altroz, Curvv, Nexon EV, Punch EV, Curvv EV, and others.

- Recent Developments: In May 2026, Tata Motors Passenger Vehicles (TMPV) announced the launch of the Nexon Pure+ PS, the first car in India, under ₹10 lakh, to have a voice-assisted panoramic sunroof.

- Strategic Focus: Defending EV market leadership through portfolio expansion and cost reduction; building mass-market EV models below INR 12 lakh; leveraging Bharat NCAP safety ratings for premium positioning.

Market Concentration Analysis

India's passenger vehicle market is highly concentrated at the mass-market end, with Maruti Suzuki commanding an estimated 40% of total organized passenger vehicle retail by volume, creating one of the most commercially dominant single-company positions in any major national automotive market. The top five manufacturers - Maruti Suzuki India Limited, Hyundai Motor Company (HMC), Tata Motors Ltd., Mahindra & Mahindra Ltd., and Kia Corporation - collectively account for approximately 85-87% of total passenger vehicle dispatches, reflecting the market's high concentration in established players.

Market concentration is evolving through two opposing dynamics: Maruti Suzuki's continued model expansion and CNG leadership maintaining or incrementally growing its dominant share in the high-volume mass-market segment, while the premium SUV, EV, and connected vehicle segments are experiencing fragmentation as global and domestic manufacturers introduce competing platforms. The EV segment in particular is exhibiting lower concentration than the overall market, with Tata Motors, Mahindra, Hyundai, Kia, BYD, and MG Motor all competing for share in a rapidly growing but still relatively small volume base.

Consolidation trends include technology partnerships between domestic OEMs and global platform suppliers - such as Toyota-Maruti Suzuki's strong hybrid cooperation and Volkswagen Group's Skoda India platform sharing - creating manufacturing economies of scale without formal corporate consolidation. New market entrants including Chinese brands BYD, MG Motor (under SAIC), and emerging Indian EV startups are incrementally adding competitive fragmentation to previously stable market structures.

Investment & Growth Opportunities

Highest Growth Segments

The electric vehicle segment represents India's highest near-term growth investment opportunity, growing at a substantially higher CAGR than the overall 9.31% market rate. EV penetration of 7.5% in 2025 is expected to accelerate significantly through the forecast period as battery costs decline, model availability expands, and charging infrastructure matures. The compact and sub-compact SUV segments present the highest absolute volume growth opportunity, with first-time buyers transitioning from two-wheelers and hatchbacks into the utility vehicle category at scale.

Emerging Investment Opportunities

- EV Charging Infrastructure: Investment in fast-charging networks along national highway corridors and in Tier-2 cities represents a critical enabling infrastructure play, with returns driven by charging revenue and grid services as EV fleet penetration increases.

- Domestic Battery Cell Manufacturing: India's Production Linked Incentive (PLI) scheme for Advanced Chemistry Cell battery manufacturing is creating investment opportunities for battery cell production facilities, reducing India's dependency on imported cells and improving EV cost competitiveness.

- Connected Vehicle Software and Services: OTA update platforms, connected services subscriptions, fleet management software, and in-vehicle commerce represent an emerging revenue stream for OEMs and technology partners as India's connected vehicle base expands.

- Tier-2 and Tier-3 City Dealership Networks: Underserved markets with rising incomes and aspiration present structured opportunity for dealership network expansion, particularly in the premium and mid-premium SUV segment where physical retail experience drives purchase decisions.

Investment Themes

Three priority investment themes define India's passenger vehicle market through 2034: domestic EV value chain development reducing import dependency and enabling competitive pricing; premium SUV segment expansion driven by India's rapidly growing HNI and upper-middle-class consumer base; and digital commerce and ownership model innovation through subscription, guaranteed buyback, and flexible ownership programs that reduce acquisition barriers and broaden the effective market.

Future Market Outlook (2026-2034)

India's passenger vehicles market is projected to grow from USD 71.57 Billion in 2025 to USD 163.31 Billion by 2034, delivering a compound annual growth rate of 9.31% over the forecast period. The market's anchor value of USD 111.70 Billion in 2030 represents India passenger vehicle industry at a structural inflection, where EV penetration will be approaching 15-20%, CNG will be consolidating a dominant position within the ICE segment, and SUVs will command above 50% of total dispatches.

Three structural forces define India's passenger vehicle market growth through 2034: first, India's income expansion creating the world's largest new middle-class consumer cohort entering the four-wheeler purchase market for the first time; second, technology-driven premiumization creating above-inflation average selling price growth across all vehicle segments; and third, India's digital commerce maturation enabling geographic market democratization that extends premium product access to previously underserved Tier-2 and Tier-3 city consumers.

The EV segment is expected to become the fastest-growing segment by volume through the forecast period, supported by declining battery costs, expanding charging infrastructure, and government policy continuity. The ICE segment, while declining as a percentage share, will maintain high absolute volumes driven by CNG adoption and continuous engine efficiency improvements. The SUV segment's share of total dispatches is forecast to reach 55-60% by 2034, reflecting the structural nature of India's utility vehicle preference transition rather than a cyclical trend.

Research Methodology

Primary Research

Primary research comprised structured interviews with India passenger vehicle industry stakeholders, including OEM sales directors, dealer principals, fleet procurement managers, EV infrastructure operators, auto finance executives at leading banks and NBFCs, and consumer survey data from passenger vehicle buyers across North, West, South, and East India. Interviews covered both conventional and electric vehicle purchase behavior, financing preferences, and feature prioritization.

Secondary Research

Secondary research encompassed India passenger vehicle production and wholesale dispatch data from the Society of Indian Automobile Manufacturers (SIAM), retail sales data from the Federation of Automobile Dealers Associations (FADA), EV registration data from the Ministry of Road Transport and Highways VAHAN database, CNG vehicle sales data from city gas distribution company reports, and company annual reports from listed OEMs. Over 60 secondary sources were reviewed, including NHAI highway expansion data, RBI monetary policy reports, and Ministry of Heavy Industries EV policy documents.

Forecasting Models

Market revenue forecasts were developed using a bottom-up segmentation model: vehicle dispatch volumes by propulsion type, vehicle type, and application multiplied by average selling prices per segment, incorporating input from OEM order book data and dealer inventory analysis. Forecast period assumptions incorporate GDP growth projections from the International Monetary Fund's India outlook, EV incentive policy continuation scenarios, and CAFE (Corporate Average Fuel Economy) norm compliance trajectories shared by SIAM industry working groups.

India Passenger Vehicles Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Propulsions Covered |

|

|

Vehicle Types Covered |

Hatchback, Sedan, SUV, MUV, Others |

|

Applications Covered |

Personal, Commercial |

|

Drive Types Covered |

Front-wheel Drive, Rear-wheel Drive, All-wheel Drive |

|

Regions Covered |

North India, South India, East India, West India |

|

Companies Covered |

Maruti Suzuki India Limited, Hyundai Motor Company (HMC), Tata Motors Ltd., Mahindra & Mahindra Ltd., Kia Corporation, etc. |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Passenger Vehicles Market Report

The India passenger vehicles market reached USD 71.57 Billion in 2025, driven by rising disposable incomes, CNG adoption, and growing SUV demand across urban and semi-urban markets nationwide.

The India passenger vehicles market grows at a CAGR of 9.31% during 2026-2034, reaching USD 163.31 Billion by 2034, supported by income growth, infrastructure expansion, and EV adoption.

ICE leads with 82.4% share in 2025, driven by extensive petrol and CNG refueling infrastructure, established consumer trust, and competitive pricing across all vehicle segments.

The India passenger vehicles market is projected to reach USD 111.70 Billion in 2030, as EV adoption accelerates, CNG consolidates its position, and SUV segment continues outpacing overall market growth.

Personal application dominates with 88.9% market share in 2025, driven by rising household incomes, aspiration for private mobility, and improving vehicle financing accessibility across urban and rural markets.

North India leads with 34.2% share in 2025, driven by Delhi-NCR's premium retail concentration, high-density corporate procurement market, and mature CNG ecosystem across Uttar Pradesh and Haryana corridors.

Key players include Maruti Suzuki India Limited, Hyundai Motor Company (HMC), Tata Motors Ltd., Mahindra & Mahindra Ltd., and Kia Corporation, collectively commanding over 85% of organized retail.

Key drivers include rising middle-class incomes, government tax reforms, national highway infrastructure expansion, SUV portfolio proliferation, CNG ecosystem growth, and accelerating EV adoption across urban centers.

Major challenges include high total ownership costs, limited EV charging infrastructure outside metros, urban traffic congestion, state-level regulatory complexity, and global semiconductor and battery supply chain vulnerabilities.

Priority investment opportunities include EV charging infrastructure along highway corridors, domestic battery cell manufacturing under PLI schemes, connected vehicle software platforms, and premium dealership network expansion in Tier-2 cities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)